Magneto-resistive RAM (MRAM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.43 Billion |

| Market Size (2031) | USD 18.24 Billion |

| Growth Rate (2026 - 2031) | 32.72% CAGR |

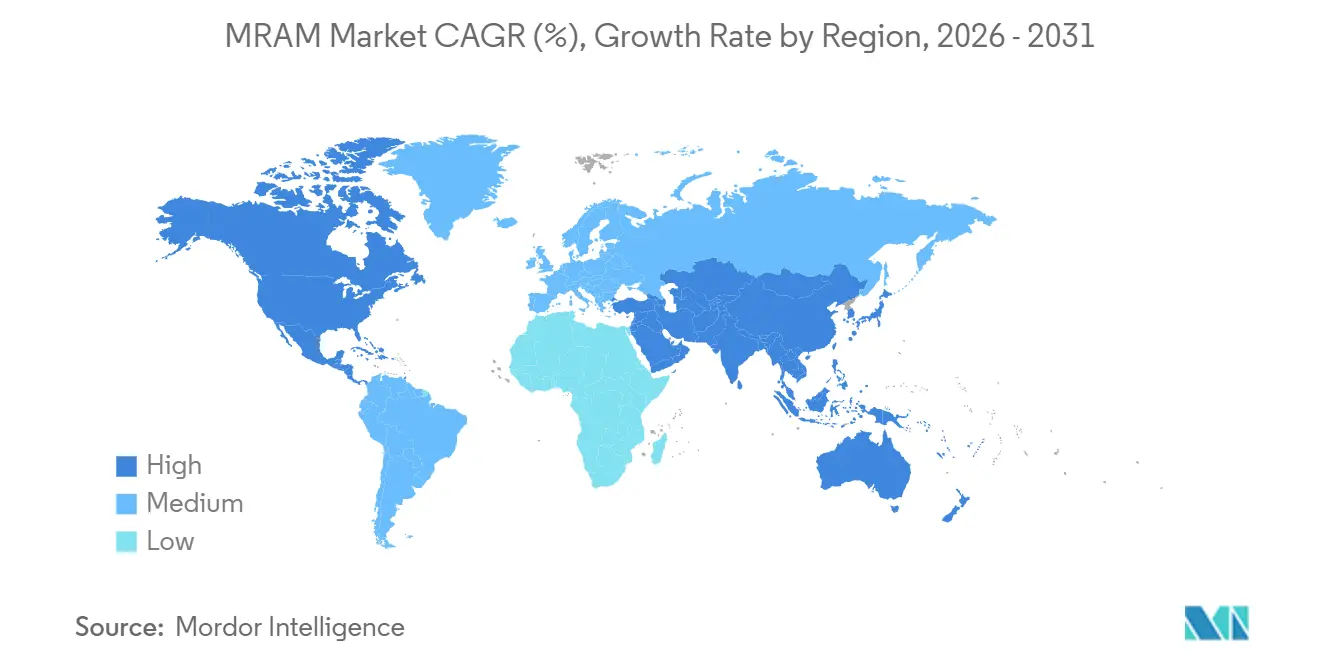

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

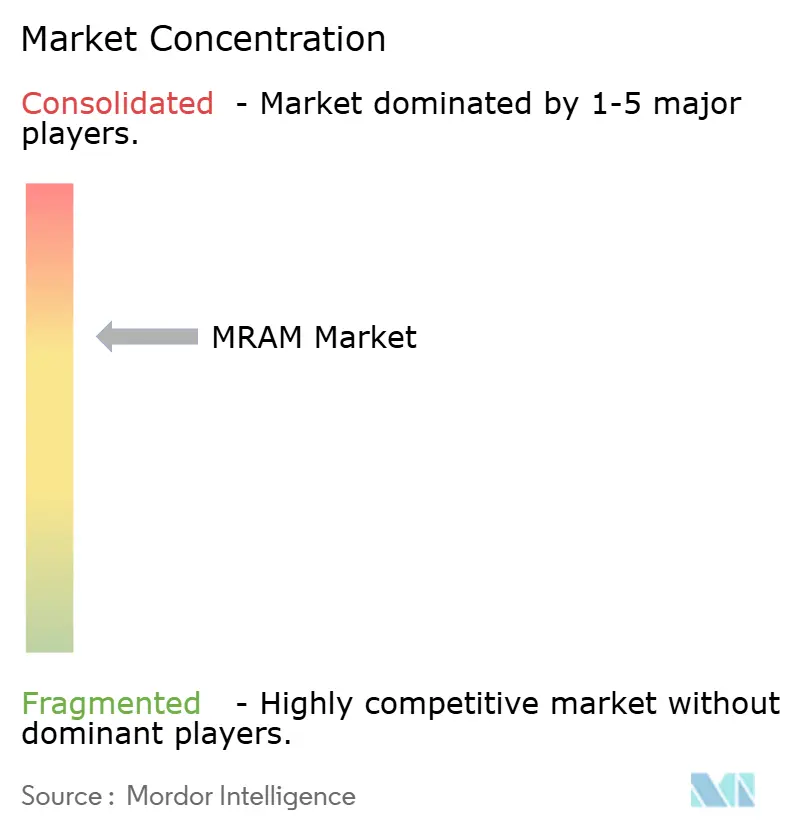

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magneto-resistive RAM (MRAM) Market Analysis by Mordor Intelligence

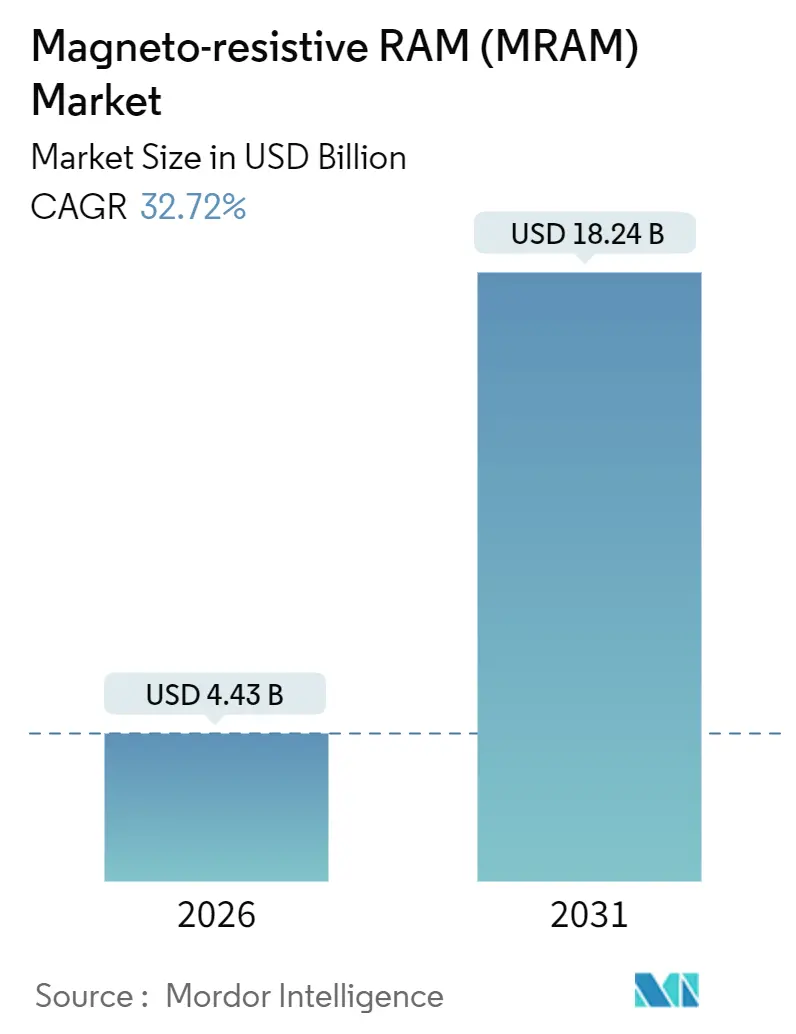

The Magneto-resistive RAM (MRAM) market size stands at USD 4.43 billion in 2026 and is projected to reach USD 18.24 billion by 2031, expanding at a 32.72% CAGR over the forecast period. Robust functional-safety mandates in automotive electronics, rapid deployment of battery-constrained IoT edge nodes, and the rise of on-device AI inference that benefits from compute-in-memory architectures are the primary growth engines. Foundries in Asia-Pacific have qualified 22 nm and 28 nm embedded processes that bundle MRAM cells with logic, cutting component count and enabling instant-on operation in mission-critical controllers. In parallel, research labs across Europe and North America are commercializing voltage-controlled switching mechanisms that halve write energy and push endurance past 10¹⁵ cycles. Competitive intensity is therefore shifting from pure hardware sales toward IP licensing and design services that monetize process know-how, controller firmware, and endurance-focused error-correction schemes.

Key Report Takeaways

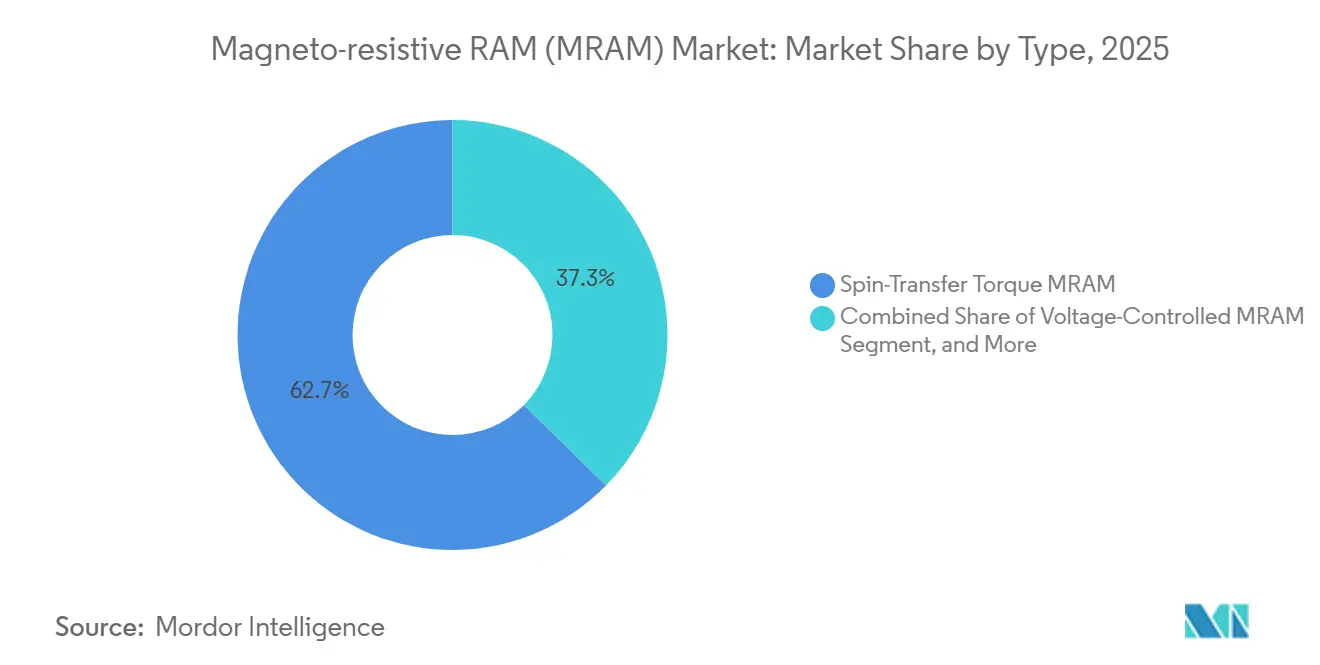

- By type, spin-transfer torque captured 62.66% of Magneto-resistive RAM (MRAM) market share in 2025. Voltage-controlled MRAM is forecast to expand at a 33.21% CAGR through 2031.

- By offering, embedded devices held 62.00% of MRAM market share in 2025. IP cores and design services are projected to grow at a 33.83% CAGR to 2031.

- By technology node, processes at or below 28 nm accounted for 46.00% of the MRAM market size in 2025 and are poised for a 34.02% CAGR through 2031.

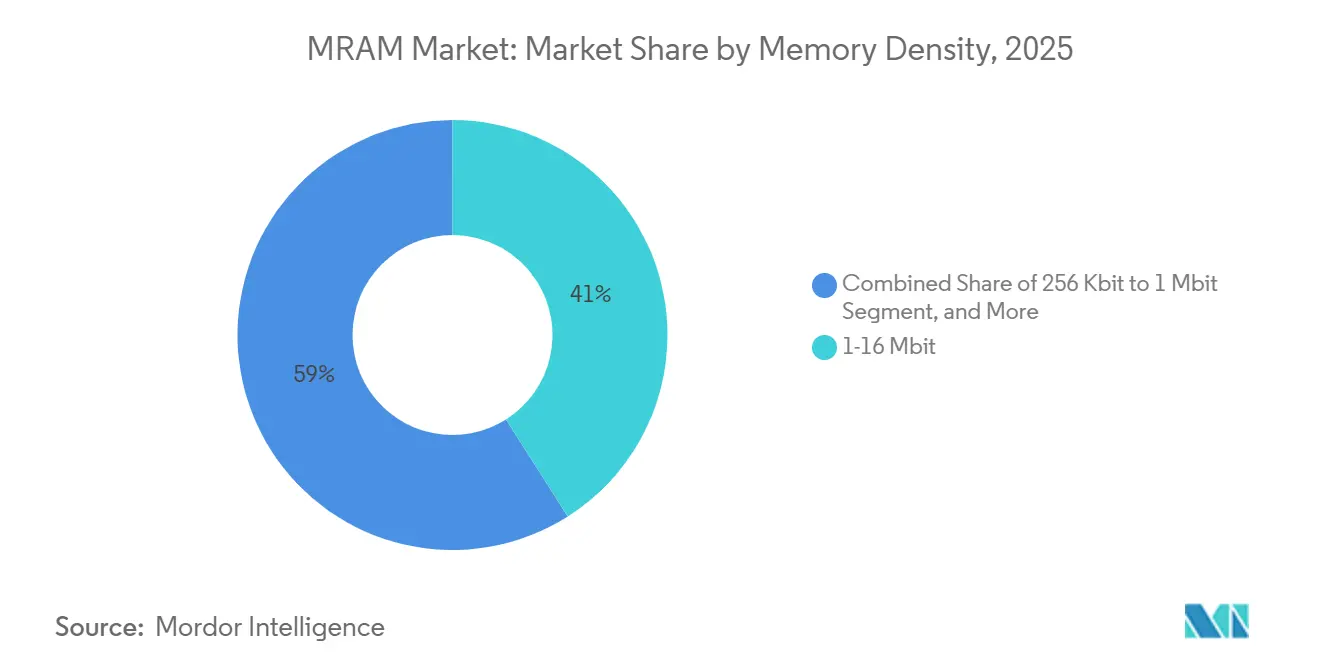

- By memory density, the 1-16 Mbit range accounted for 41% of the MRAM market size in 2025 and sub-256 Kbit devices are expected to advance at a 34.21% CAGR through 2031.

- By geography, Asia-Pacific generated 48.00% of 2025 revenue, while the Middle East is expected to advance at a 34.52% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Magneto-resistive RAM (MRAM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT and Edge Devices | +6.50% | Global, with APAC and North America leading deployments | Medium term (2-4 years) |

| Rising Adoption in Automotive Functional-Safety Systems | +5.80% | APAC (Japan, South Korea, China), Europe (Germany), North America | Long term (≥ 4 years) |

| Increasing Miniaturization in Consumer Electronics | +3.20% | APAC (China, South Korea, Taiwan), North America | Short term (≤ 2 years) |

| Deployment as Storage Class Memory in Data Centers | +4.10% | North America, Europe, APAC (Singapore, Hong Kong) | Medium term (2-4 years) |

| Defense-Grade Radiation Hardness for Satellite Edge Computing | +2.90% | North America, Europe, Middle East (Israel), APAC (Japan) | Long term (≥ 4 years) |

| On-Chip NVM Scratchpads for AI Accelerators | +3.80% | Global, with North America and APAC leading AI chip development | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of IoT and Edge Devices

Industrial automation, smart metering, and wearable health monitors now embed local processing to cut latency and protect data privacy. Octal-interface Magneto-resistive RAM (MRAM) parts deliver 400 MB/s throughput, replacing battery-backed SRAM and eliminating supercapacitors. Microcontroller makers cite 90% lower standby power versus flash, enabling five-year battery life for condition-monitoring sensors. High endurance means designers no longer provision wear-levelling firmware, saving precious ROM space. As component footprints shrink, more edge boards adopt MRAM arrays that share the supply rail with logic blocks, removing board-level voltage translators and trimming bill-of-materials cost.[1]Everspin Technologies, “PERSYST xSPI STT-MRAM,” everspin.com

Rising Adoption in Automotive Functional-Safety Systems

Powertrain and ADAS controllers must retain calibration data across ignition cycles without latency or wear-levelling overhead. Embedded MRAM in 16 nm FinFET microcontrollers supports ISO 26262 ASIL-D safety targets while operating from -40 °C to +125 °C. Unlimited write endurance avoids field failures that could trigger costly recalls. Electric-vehicle battery-management units write state-of-charge logs thousands of times per second, a duty cycle traditional flash cannot sustain. With automotive semiconductors moving to 22 nm and below, MRAM cells scale in lockstep, delivering multi-megabit densities within tightly constrained die areas.[2]NXP Semiconductors, “S32K5 MCU Introduction,” nxp.com

Miniaturization In Consumer Electronics

Smartphones, wearables, and AR headsets demand low-leakage memory to extend battery life while keeping firmware instantly accessible after deep sleep. Embedded Magneto-resistive RAM (MRAM) in 14 nm application processors eliminates the need for separate NOR flash dies, freeing board space for larger batteries or additional sensors. Sub-10 µs wake-to-active times enhance user experience in voice-activated earbuds and health trackers. Component consolidation reduces overall device mass, supporting lighter form factors that appeal to style-conscious consumers.

On-Chip NVM Scratchpads For AI Accelerators

Edge inference engines store model weights in MRAM, allowing compute-in-memory operations that cut data movement energy by an order of magnitude. Prototype analog chips show 10× lower power than SRAM-based designs and sustain inference after power loss, critical for autonomous drones and industrial robots that must restart safely. Engineering services deals indicate commercial traction, with MRAM vendors tailoring controller IP for convolutional neural networks and transformer blocks. As model parameters balloon, embedded MRAM arrays at 16 nm and below deliver hundreds of megabits without incurring standby leakage penalties seen in eDRAM.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Fabrication Cost of Perpendicular MTJ Process | -2.40% | Global, with higher impact in regions lacking advanced foundry infrastructure | Medium term (2-4 years) |

| Competition from Alternative NVM Technologies | -2.10% | Global, with APAC and North America leading ReRAM and PCM development | Short term (≤ 2 years) |

| Yield Variability at Sub-28 nm Nodes | -1.80% | APAC (Taiwan, South Korea), North America | Medium term (2-4 years) |

| Tooling Supply-Chain Bottlenecks | -1.30% | Global, with dependencies on ion-beam etching and deposition equipment vendors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Fabrication Cost Of Perpendicular MTJ Process

Perpendicular magnetic tunnel junction stacks add up to 40 back-end-of-line steps, including ion-beam milling and ultra-high-vacuum MgO deposition. Tool sets cost millions of U.S. dollars and demand sub-angstrom surface control, pushing wafer-level costs to roughly twice that of embedded flash at comparable nodes. Only a handful of foundries have qualified these modules, limiting supply and keeping average selling prices elevated. Until equipment suppliers widen availability and second-source capacity emerges, OEMs remain cautious about single-sourcing critical memory.

Competition From Alternative NVM Technologies

Resistive RAM and phase-change memory promise lower bit cost and similar endurance, especially in microcontrollers that do not require the radiation hardness MRAM offers. A leading foundry plans high-volume ReRAM production on its 22FDX+ line beginning 2026, creating price pressure for embedded non-volatile options. Benchmark papers report sub-10 ns write speeds and 10⁹-cycle durability for phase-change cells, narrowing the performance gap. Should these technologies achieve parity on retention and endurance, Magneto-resistive RAM (MRAM) vendors may need to pivot toward aerospace, defense, and AI compute niches where deterministic latency and radiation immunity remain differentiators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: STT-MRAM Dominates, VC-MRAM Accelerates

Spin-transfer torque devices captured 62.66% Magneto-resistive RAM (MRAM) market share in 2025 on the strength of qualified 22 nm and 28 nm flows that meet automotive and industrial reliability standards. Toggle MRAM persists in extreme-temperature systems, such as oil-field sensors, because its in-plane geometry tolerates 200 °C excursions. Voltage-controlled switching reduces write current by roughly 50%, a critical win for edge AI accelerators, and is forecast to clock a 33.21% CAGR through 2031. Spin-orbit torque remains in the research domain, but its decoupled read-write paths suggest write endurance exceeding 10¹⁵ cycles, positioning it as a long-term successor.

Adoption momentum proves two-tiered. Mainstream controllers favour mature STT-MRAM for near-term programs, whereas AI startups engage with research fabs to prototype voltage-controlled arrays that slash energy per inference. Industry roadmaps show pilot VC-MRAM lines at 14 nm by 2028. If yield ramps on schedule, the MRAM market could migrate to this topology for high-volume consumer processors, reinforcing the technology’s twice-per-decade architecture refresh cadence.

By Offering: Embedded Leads, IP Licensing Surges

Embedded variants accounted for 62.00% share of Magneto-resistive RAM (MRAM) market in 2025 because they integrate directly into logic wafers, eliminating external packages and boosting system reliability. Stand-alone serial parts still serve industrial retrofit boards that need a pin-compatible replacement for parallel SRAM. The MRAM market size for IP cores and design services, however, is projected to expand at a 33.83% CAGR, reflecting fabless demand to license hardened memory macros without owning masks. Controller IP firms bundle error-correction engines that mitigate bit-error-rate drift at sub-28 nm, easing qualification for automotive ASIL-D targets.

As more OEMs embrace chiplets and heterogeneous integration, MRAM macro IP can be dropped into a reticle on advanced interposers, shortening design cycles. Vendors thus pivot from component revenue toward annuity-style royalties, mirroring the shift ARM catalysed in CPU cores. This structural change underpins healthier gross margins despite falling per-bit prices in commodity densities.

By Technology Node: Sub-28 nm Scales, Legacy Nodes Persist

Nodes at or below 28 nm generated 46.00% of the Magneto-resistive RAM (MRAM) market size in 2025 and are trending toward a 34.02% CAGR because leading-edge automotive and AI chips crave higher density. A 16 nm FinFET microcontroller now packs over 8 MB of non-volatile code storage within the same die footprint that held 2 MB on 40 nm, proving the density advantage. Yet legacy 55 nm and 40 nm flows remain indispensable for radiation-hardened satellites and extreme-temperature industrial drives where larger geometries improve robustness.

Foundries monetize both ends of the spectrum. Premium wafers on EUV nodes target consumer flagships, while fully depreciated 65 nm lines capture long-tail industrial programs with 15-year lifecycles. The bifurcation supports stable overall wafer demand, cushioning the MRAM market from cyclic swings in any single end-use sector.

By Memory Density: 1-16 Mbit Anchors, Sub-256 Kbit Accelerates

Densities between 1 Mbit and 16 Mbit held 41.00% share in 2025 of Magneto-resistive RAM (MRAM) market, favoured by automotive control units and programmable logic controllers that log calibration data. Below 256 Kbit, growth is fastest, topping a 34.21% CAGR, because smart tags, tire-pressure sensors, and disposable medical patches need just kilobytes of firmware but must eliminate standby leakage. At the other extreme, 128 Mbit serial devices now buffer enterprise SSD writes, while gigabit-class die target data-center metadata logging and satellite edge compute platforms.

The segmentation confirms a barbell demand profile. Ultralow-density parts proliferate in billions of sensor nodes, while high-density parts capture margin-rich storage and aerospace sockets. Mid-density components remain the workhorse that sustains foundry utilization rates.

By Application: Automotive Leads, IoT Surges

Automotive electronics contributed 29.00% of 2025 revenue, anchored by stability control and battery-management modules. Design wins at multiple tier-one suppliers underpin steady volumes through the decade because platform lifetimes exceed seven years. IoT and edge computing devices, however, should post a 33.57% CAGR, outpacing all other segments. Smart meters now ship with MRAM to preserve cumulative usage registers even if installers cut power abruptly. Wearable ECG patches leverage MRAM’s instant capture of high-frequency data bursts without risking corruption on battery depletion.

Enterprise storage, healthcare instrumentation, industrial robots, and smart-card authentication together form a balanced second tier of demand. Each niche values MRAM’s unique mix of endurance, shock tolerance, and power-fail safety, insulating the Magneto-resistive RAM (MRAM) market from reliance on any single vertical.

Geography Analysis

MRAM Market in North America

Asia-Pacific generated 48.00% of Magneto-resistive RAM (MRAM) market revenue in 2025, reflecting deep foundry capacity in Taiwan and South Korea and surging automotive semiconductor demand in China. Government incentives, such as South Korea’s USD 27 million program that funds 48 memory projects, accelerate process tweaks and mask re-spins. Japan’s collaboration between a leading university and a regional foundry brings pilot production of voltage-controlled MRAM on-shore, reinforcing supply-chain resilience amid geopolitical uncertainty.

The Middle East is projected to post the highest regional CAGR at 34.52% between 2026-2031. Israel’s vibrant fabless cluster anchors design talent, while Gulf nations channel sovereign funds into semiconductor parks that court memory startups. Defense-grade requirements for satellite constellations dovetail with MRAM’s radiation tolerance, creating sticky demand even as cost curves improve.

North America remains pivotal for aerospace and data-center deployments. Arizona-based manufacturers logged double-digit revenue growth in 2025 from space-qualified parts, and the United States federal programs subsidize low-Earth-orbit component testing. Europe leverages its automotive supply chain in Germany and advanced R&D hubs in Belgium to pilot perpendicular MTJ stacks below 20 nm. Both regions jointly ensure that global sourcing of MRAM devices spans at least three continents, mitigating single region supply shocks.[3]South Korea Ministry of Trade, Industry and Energy, “Memory R&D Funding Announcement,” motie.go.kr

Competitive Landscape

The five largest suppliers command roughly 45% of MRAM market share, indicating moderate concentration. Two pure-play vendors focus on discrete and IP business models, while three global foundries embed MRAM in mainstream logic processes. Strategic moves in 2025 included an engineering-services contract worth USD 4.1 million to adapt compute-in-memory architectures and a 22FDX+ ReRAM announcement that intensifies cross-technology competition. Leading OEMs cite endurance and deterministic latency as reasons to dual-source MRAM despite ReRAM’s cost advantage.

Integrated device manufacturers exploit scale to push qualified nodes from 28 nm to 16 nm. Meanwhile, startups secure venture rounds by specializing in voltage-controlled or spin-orbit torque physics that promise radical energy savings. Patent filings on spintronic stack engineering rose sharply in 2025, signalling that differentiation now pivots on process IP rather than basic cell structures.

Future battlegrounds include AI edge accelerators, where unified MRAM scratchpads can collapse SRAM and DRAM hierarchies, and radiation-hardened defense electronics, where incumbent MRAM suppliers already possess heritage qualification data.

Magneto-resistive RAM (MRAM) Industry Leaders

Honeywell International Inc.

Infineon Technologies AG

Intel Corporation

Avalanche Technology Inc.

Samsung Electronics Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: NXP led a USD 17.5 million Series A round in Israel-based RAAAM Memory, targeting spin-orbit torque MRAM.

- October 2025: Everspin partnered with Quintauris to expand European distribution of automotive-grade MRAM devices.

- October 2025: Renesas launched RA8M2 and RA8D2 microcontrollers with embedded MRAM for industrial automation and consumer electronics.

- August 2025: GlobalFoundries introduced 22FDX+ ReRAM for 2026 volume production.

Global Magneto-resistive RAM (MRAM) Market Report Scope

Magneto-resistive RAM (MRAM) is a non-volatile method of storing data bits in random-access memory using magnetic states instead of electrical charges, which is different from dynamic random-access memory (DRAM) and static random-access memory (SRAM), as they maintain data only until the power is applied.

The magneto-resistive RAM (MRAM) market is segmented by type (toggle MRAM and spin-transfer torque MRAM), application (consumer electronics, robotics, automotive, enterprise storage, and aerospace and defense), and geography.

The MRAM Market Report is Segmented by Type (Toggle MRAM, Spin-Transfer Torque MRAM, Voltage-Controlled MRAM, Spin-Orbit Torque MRAM), Offering (Stand-Alone, Embedded, IP Cores and Design Services), Technology Node (≤28 nm, 28-40 nm, 40-65 nm, >65 nm), Memory Density (<256 Kbit, 256 Kbit-1 Mbit, 1-16 Mbit, >16 Mbit), Application (Consumer Electronics, Industrial Automation and Robotics, Enterprise Storage, Automotive Electronics, Aerospace and Defense, Healthcare Devices, IoT and Edge Computing Devices, Smart Card and RFID), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Toggle MRAM |

| Spin-Transfer Torque MRAM |

| Voltage-Controlled MRAM |

| Spin-Orbit Torque MRAM |

| Stand-Alone |

| Embedded |

| IP Cores, Design Services |

| Less than equal to 28 nm |

| 28-40 nm |

| 40-65 nm |

| Greater than 65 nm |

| Less than 256 Kbit |

| 256 Kbit-1 Mbit |

| 1-16 Mbit |

| Greater than 16 Mbit |

| Consumer Electronics |

| Industrial Automation and Robotics |

| Enterprise Storage |

| Automotive Electronics |

| Aerospace and Defense |

| Healthcare Devices |

| IoT and Edge Computing Devices |

| Smart Card and RFID |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Toggle MRAM | |

| Spin-Transfer Torque MRAM | ||

| Voltage-Controlled MRAM | ||

| Spin-Orbit Torque MRAM | ||

| By Offering | Stand-Alone | |

| Embedded | ||

| IP Cores, Design Services | ||

| By Technology Node | Less than equal to 28 nm | |

| 28-40 nm | ||

| 40-65 nm | ||

| Greater than 65 nm | ||

| By Memory Density | Less than 256 Kbit | |

| 256 Kbit-1 Mbit | ||

| 1-16 Mbit | ||

| Greater than 16 Mbit | ||

| By Application | Consumer Electronics | |

| Industrial Automation and Robotics | ||

| Enterprise Storage | ||

| Automotive Electronics | ||

| Aerospace and Defense | ||

| Healthcare Devices | ||

| IoT and Edge Computing Devices | ||

| Smart Card and RFID | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is forecast for the MRAM market between 2026-2031?

The MRAM market is projected to expand at a 32.72% CAGR during the 2026-2031 period.

Which region contributed the highest revenue in 2025?

Asia-Pacific generated 48.00% of global revenue in 2025, driven by strong foundry capacity and automotive demand.

Why is MRAM gaining traction in automotive electronics?

Embedded MRAM satisfies ISO 26262 functional-safety needs, offers instant-on behavior, and delivers unlimited write endurance critical for battery-management and ADAS controllers.

How do voltage-controlled MRAM devices improve energy efficiency?

VC-MRAM switches by electric-field modulation instead of spin-polarized current, cutting write energy by about 50% while maintaining sub-nanosecond speed.

What competitive threat do alternative memories pose?

Resistive RAM and phase-change memory aim to undercut MRAM on cost, but still lag in deterministic latency and radiation tolerance valued in aerospace, automotive, and edge AI applications.

Which density segment is growing fastest?

Sub-256 Kbit devices are forecast to post the highest CAGR, fueled by ultra-low-power IoT sensors and smart tags that need kilobytes of non-volatile code storage without standby leakage.

Page last updated on: