Southeast Asia Health And Fitness Club Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

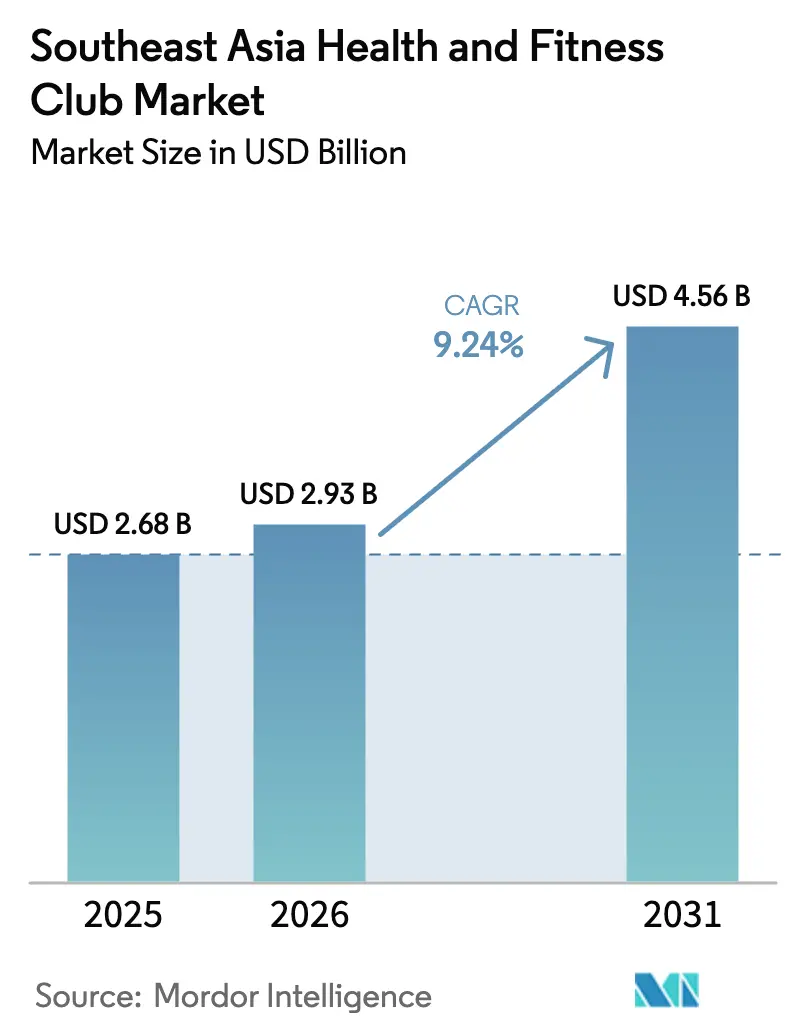

| Base Year Market Size (2025) | USD 2.68 Billion |

| Market Size (2026) | USD 2.93 Billion |

| Market Size (2031) | USD 4.56 Billion |

| Growth Rate (2026 - 2031) | 9.24% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Southeast Asia Health And Fitness Club Market Analysis by Mordor Intelligence

Southeast Asia health and fitness club market size in 2026 is estimated at USD 2.93 billion, growing from 2025 value of USD 2.68 billion with 2031 projections showing USD 4.56 billion, growing at 9.24% CAGR over 2026-2031. Factors such as rapid urbanization, increasing incomes of the middle class, and government-endorsed preventive health initiatives are reshaping consumer perceptions, making fitness memberships seen as vital health investments rather than mere leisure expenditures. For instance, according to the Singapore Department of Statistics, in 2023, the gymnasiums in Singapore recorded approximately 4.02 million attendances, up from 1.97 million in 2021[1]Source: Singapore Department of Statistics, "Usage Of Sports Facilities Managed By Sport Singapore", www.tablebuilder.singstat.gov.sg. Digital innovations, from wearables to AI coaching apps, are now integral to club offerings, enhancing member retention and boosting average revenue per user. Operators who can provide specialized formats are reaping the benefits of premium revenue streams, driven by a rising demand for boutique experiences and increased female participation. Furthermore, as healthcare policies pivot towards chronic disease prevention, fitness clubs are emerging as key players in national wellness strategies, paving the way for collaborations with insurers, corporations, and telehealth entities.

Key Report Takeaways

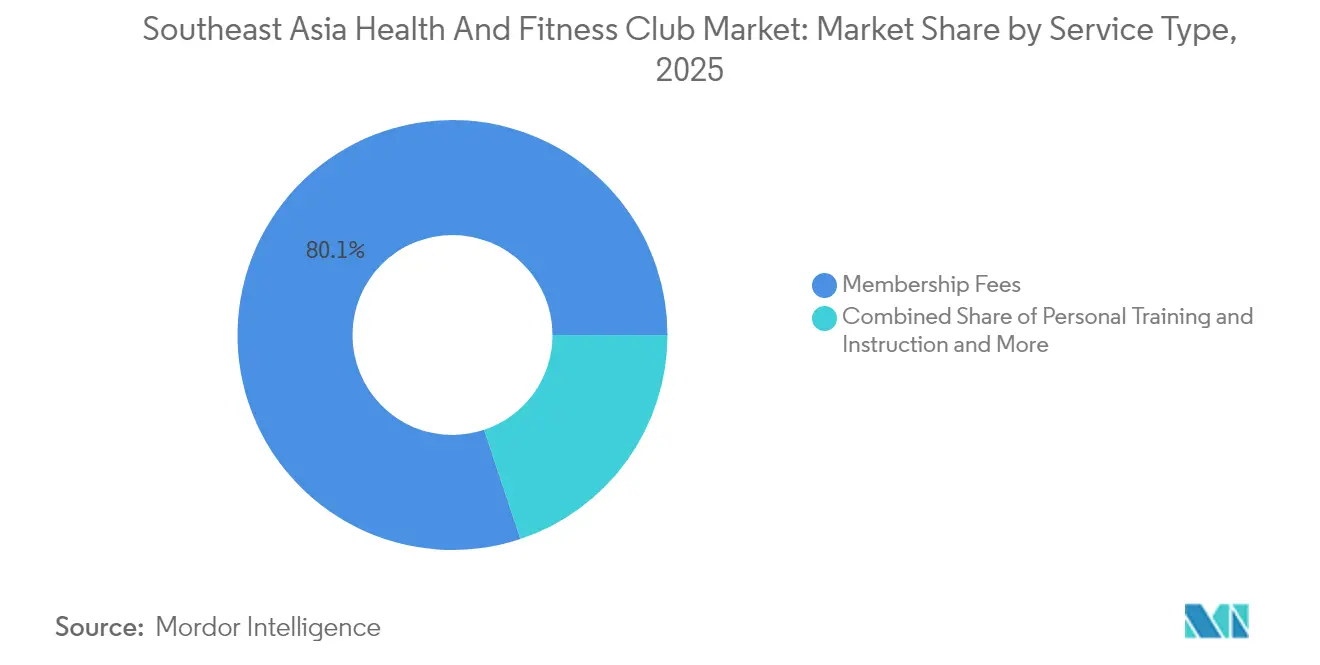

- By service type, membership fees held 80.12% of the Southeast Asia health and fitness club market share in 2025; personal training is advancing at a 11.78% CAGR through 2031.

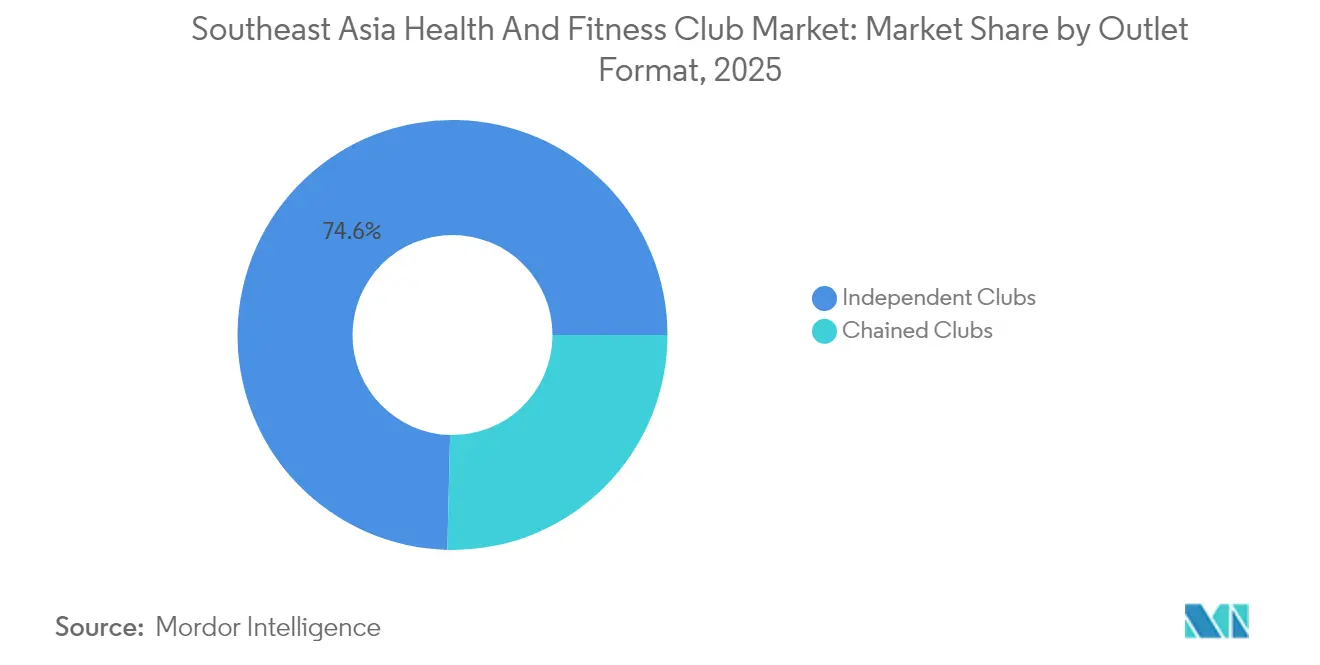

- By outlet format, independent clubs captured 74.62% revenue share in 2025, while chained operators are growing at a 10.05% CAGR to 2031.

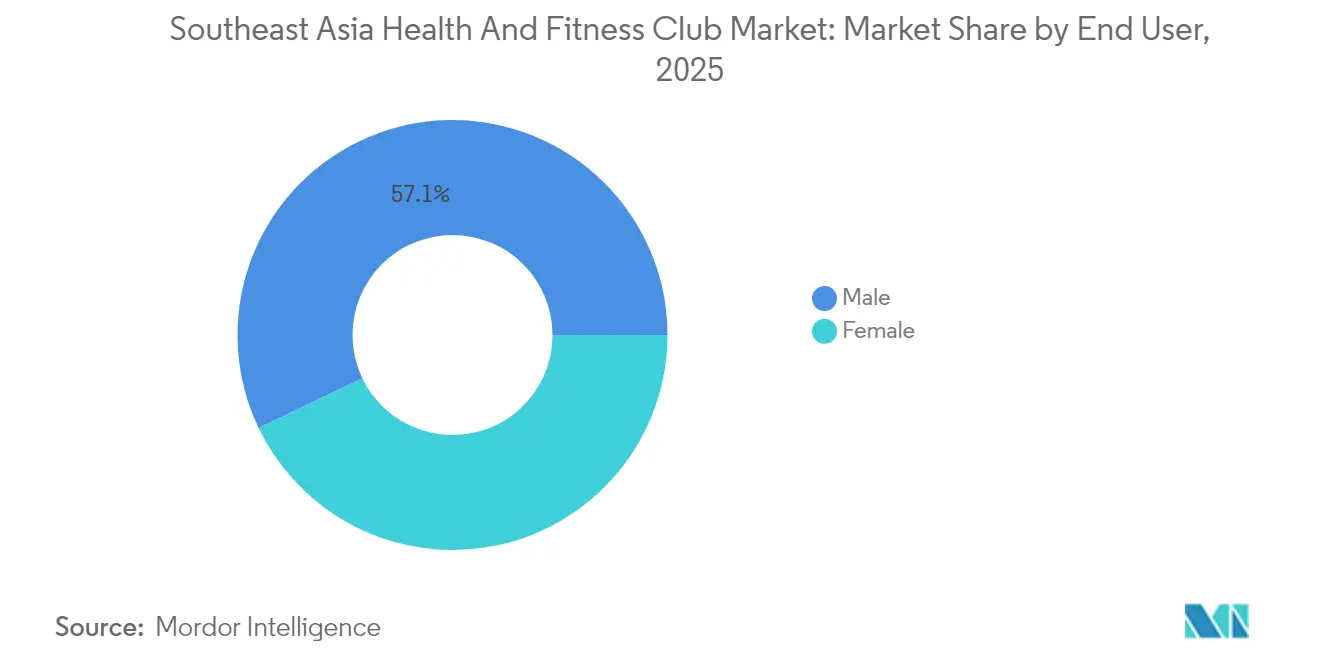

- By end user, male participants accounted for 57.12% of the Southeast Asia health and fitness club market size in 2025; female participation is projected to expand at an 11.08% CAGR between 2026-2031.

- By geography, Singapore led with a 22.05% revenue share in 2025, whereas Indonesia is forecast to post the fastest growth at 11.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Health And Fitness Club Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Health Consciousness and Proactive Wellness Focus | +2.1% | Global, strongest in Singapore and Malaysia | Medium term (2-4 years) |

| Rising Prevalence of Lifestyle Diseases Driving Preventive Healthcare | +1.8% | Indonesia, Thailand, Philippines core markets | Long term (≥ 4 years) |

| Growing Popularity of Specialized Fitness Offerings | +1.5% | Urban centers across all markets | Short term (≤ 2 years) |

| Expansion and Adoption of Fitness Technology | +1.3% | Singapore, Malaysia are leading the adoption | Medium term (2-4 years) |

| Increasing Female Participation in Fitness Activities | +1.2% | Vietnam, Indonesia are showing the highest growth | Medium term (2-4 years) |

| Rising Demand for Personalized Fitness Plans | +0.9% | Premium segments in Singapore, Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Health Consciousness and Proactive Wellness Focus

In Southeast Asia, the wellness economy is evolving, pushing the demand for fitness clubs beyond mere exercise to a holistic approach to lifestyle management. In 2024, Singapore's Health Promotion Board rolled out the 'Healthier SG' initiative, spotlighting preventive care and forging community health partnerships[3]Source: Singapore's Ministry of Health (MOH), "Healthier SG initiative", www.healthiersg.gov.sg. Complementing this, the National Steps Challenge incentivizes citizens, rewarding them for hitting the target of 150 minutes of moderate-to-vigorous physical activity weekly. Such government-endorsed wellness initiatives are not just promoting exercise as a leisure activity but are embedding it into the very fabric of healthcare, ensuring a steady demand for fitness services. As healthcare costs climb and awareness of chronic diseases grows, Southeast Asia's burgeoning middle class is increasingly viewing fitness memberships as vital health investments. This regional health consciousness isn't just about treatment; it's about a proactive approach to fitness, underscored by Thailand's allure, drawing in 2.86 million medical tourists in 2023.

Rising Prevalence of Lifestyle Diseases Driving Preventive Healthcare

As diabetes and obesity rates surge, Southeast Asia's urbanization and sedentary lifestyles underscore the value of fitness clubs. Indonesia's Healthcare Law No. 17 of 2023, prioritizing preventive care and telemedicine, signals a shift. Concurrently, Bio Farma partners with Google Cloud and Fitbit, launching platforms aimed at chronic disease prevention. Such moves elevate fitness clubs from mere service providers to pivotal healthcare allies. With the region's demographic shift leaning towards an aging populace, the demand for preventive healthcare intensifies. Medical professionals increasingly prescribe fitness programs for managing chronic conditions. Highlighting this trend, Thailand's Department of Older Persons reported in June 2024, approximately 7.45 million female and 5.87 million male senior citizens[2]Source: Department of Older Persons, "Number of senior citizens in Thailand", www.stat.bora.dopa.go.th. Recognizing the benefits, corporate wellness programs flourish, as employers see fitness investments curtailing healthcare costs and boosting productivity.

Growing Popularity of Specialized Fitness Offerings

Boutique fitness formats are capitalizing on premium pricing, catering to diverse consumer preferences that traditional gyms often overlook. The American College of Sports Medicine's 2025 trends report highlights specialized programming as a global fitness priority, spotlighting yoga, Pilates, and high-intensity interval training as the fastest-growing segments. Meanwhile, Asian wellness traditions, such as tai chi and other traditional movement practices, are gaining commercial momentum as fitness operators blend these cultural elements with contemporary exercise science. This trend towards specialization not only enables operators to charge higher rates per session but also fosters deeper community ties compared to conventional gyms. FTL Gym's ambitious plan to expand to 30 outlets in Indonesia by 2024, offering specialized services like Pilates Reformer and round-the-clock access, underscores the premium positioning and swift scaling achievable through specialized formats.

Expansion and Adoption of Fitness Technology

Wearable technology and mobile applications are reshaping fitness clubs, shifting them from traditional membership models to data-centric engagement strategies. The 2025 ACSM Worldwide Fitness Trends report highlights wearable tech and mobile exercise apps as leading global fitness trends, underscoring that tech-savvy operators will outpace their traditional counterparts. Singapore's Active Health program exemplifies this shift, merging fitness tracking apps with expert guidance, showcasing a government-endorsed move towards digital fitness. With tech adoption, fitness clubs are evolving: they're not just providing equipment but are becoming holistic wellness platforms. This shift includes personalized workouts, real-time performance tracking, and predictive analytics to boost member retention. Furthermore, the infusion of artificial intelligence and data analytics empowers operators to maximize facility use, foresee equipment maintenance, and tailor experiences to individual member habits. A case in point: the Singapore-based micro-gym chain expanded its offerings in 2024–2025 to include technology-enabled specialized classes, such as Pilates Stretch and Mobility. These micro-gyms, equipped with smart technology, offer a model for efficient facility utilization in space-constrained urban areas.

Restrains Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Competition Among Fitness Providers | -1.4% | All markets, particularly saturated urban areas | Short term (≤ 2 years) |

| High Operating and Maintenance Costs | -1.1% | Singapore, Malaysia are facing the highest cost pressures | Medium term (2-4 years) |

| Competition from Alternative Fitness Formats (Home Workouts, Outdoor Activities) | -1.2% | All markets, particularly saturated urban areas | Long term (3-5 years) |

| Challenges in Retaining Membership and Building Brand Loyalty | -1.6% | Singapore and Indonesia are facing the highest cost pressures | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense Competition Among Fitness Providers

In prime urban locations, market saturation is squeezing operator margins and speeding up consolidation trends. Vietnam's fitness market saw a notable shrinkage, with a drop in gym numbers over the year. Smaller chains faced stiff competition, leading to rising membership fees as operators chased revenue stability. The bankruptcy of WeFit in Vietnam underscores the risks of aggressive pricing. Their unlimited access model, while enticing, set off unsustainable costs, resulting in delayed payments to partners and ultimately, the company's downfall. As international chains ramp up their presence, competition heats up. Notably, Japanese fitness operators are eyeing Southeast Asia, drawn by demographic hurdles back home. This heightened competition pushes operators to stand out, leaning on tech adoption, specialized programs, or elevated service levels, rather than just price wars. In 2024, Thailand boasted 450 Muay Thai gyms, with Bangkok leading the pack at 164.

High Operating and Maintenance Costs

Independent operators face mounting pressures on their margins due to rising rental costs in prime urban areas and escalating equipment maintenance expenses. In Singapore, the strengthening currency and a buoyant real estate market render fitness club operations more capital-intensive. Simultaneously, navigating regulatory compliance across various jurisdictions introduces added operational complexities. Energy expenses, essential for climate control, specialized lighting, and equipment operation, loom large as fixed costs. Notably, these costs scale with the size of the facility, not its membership utilization. As operators vie for top-tier trainers and customer service staff, personnel costs surge. This is especially pronounced in specialized fitness formats, which demand higher-skilled instructors, often leading to premium compensation packages. Such financial pressures tilt the playing field in favor of larger operators, who benefit from economies of scale and have better access to capital markets. This dynamic is driving a swift consolidation in the market, leaning heavily towards chained operators, even as independent clubs continue to hold a majority share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Personal Training Drives Premium Growth

Despite membership fees commanding an 80.12% market share in 2025, personal training services are on track to achieve the fastest growth rate, projected at a 11.78% CAGR through 2031. This trend underscores consumers' readiness to invest in premium, personalized coaching and specialized programming—services that standard gym access fails to offer. Other service categories, such as group fitness classes, nutrition counseling, and wellness services, are emerging as lucrative revenue streams. Operators are increasingly bundling these services with core memberships, aiming to boost both retention rates and average revenue per user.

This pivot towards personalized fitness mirrors a broader healthcare movement that champions individualized treatments and preventive care. Highlighting this trend, Singapore's Active Health program, as noted by Sport Singapore, showcases government endorsement for tailored fitness guidance. By backing qualified experts and bespoke programming, the government lends regulatory credibility to premium service models. Furthermore, operators are harnessing technology to amplify personal training. With tools like virtual coaching, AI-driven workout suggestions, and remote monitoring, trainers can extend their influence beyond traditional one-on-one interactions. This tech infusion not only enables fitness clubs to command higher premiums for personal training but also ensures they operate efficiently while broadening service access to a larger member base.

By Outlet Format: Consolidation Accelerates Despite Independent Dominance

In 2025, independent clubs command a 74.62% market share, but chained operators are outpacing them with a 10.05% CAGR, hinting at looming consolidation pressures in the region. This disparity in growth underscores the advantages chained operators enjoy: better access to capital, advanced technology platforms, and operational know-how, all of which facilitate swift scaling and deeper market penetration. The merger of Celebrity Fitness and Fitness First Asia under Evolution Wellness has birthed one of Asia's fitness giants, boasting 140 clubs and catering to 375,000 members as of August 2025. This underscores how consolidation can yield competitive edges, thanks to economies of scale and broader member access.

Independent operators grapple with mounting pressures: rising operational costs, the need for tech investments, and escalating marketing expenses. These challenges often tilt the scales in favor of larger competitors, who boast diversified revenue streams. Yet, independent clubs hold their ground with advantages like deep local market insights, strong community ties, and the agility to swiftly adapt to evolving consumer tastes. The competitive landscape hints at a dual market trajectory: while some independent operators carve out success in specialized niches or premium offerings, mainstream fitness services gravitate towards consolidation under chained operators, emphasizing standardized services and tech integration.

By End User: Female Participation Accelerates Market Expansion

In 2025, male users hold a 57.12% share of the market, but female participation is on the rise, projected to grow at an 11.08% CAGR through 2031. This surge is fueled by specialized programming and targeted marketing. Research in Singapore highlights that women are primarily motivated to participate in fitness for health benefits, social integration, and guidance from instructors. However, they face barriers such as cost concerns, time constraints, and scheduling conflicts. Meanwhile, studies in Malaysia underscore the importance of social support and tailored programming for women, suggesting that operators can tap into this growth by fostering community initiatives and offering flexible schedules.

The uptick in female participation mirrors broader demographic shifts: more women are joining the workforce, disposable incomes are rising, and cultural attitudes towards women's fitness are evolving. Fitness formats like yoga, Pilates, and dance workouts resonate strongly with women, often commanding premium prices that boost operator profits. Moreover, by integrating wellness services such as nutrition counseling, spa treatments, and childcare, operators are crafting holistic lifestyle platforms. These platforms cater to women's diverse needs, extending beyond mere exercise. Notably, while female participation is on the rise, it still lags behind male levels in many Southeast Asian markets, signaling a significant growth opportunity rather than just a shift in market share.

Geography Analysis

In 2025, Singapore commanded a dominant 22.05% share of the regional revenue, driven by its high per-capita spending and state-led health initiatives that seamlessly integrate gym usage into primary healthcare. Clubs are tapping into the tech-savvy populace, incorporating biometric kiosks that link with national health apps, thereby elevating their service quality. While rental costs are on the rise, clubs counterbalance this with premium pricing and a robust expatriate clientele demanding top-tier facilities. These trends not only position Singapore as a hub for innovation but also set the benchmark for service standards in the broader Southeast Asian health and fitness club arena.

Forecasted to grow at an impressive 11.42% CAGR, Indonesia stands out as the region's fastest-growing market. This surge is fueled by its vast urbanizing populace and a mere 1% gym penetration, significantly trailing its neighbors. The newly introduced Healthcare Law emphasizes preventive programs, aligning seamlessly with offerings from fitness clubs. Noteworthy venture funding, exemplified by FTL Gym’s USD 3-5 million debt raise, highlights the strong investor confidence in Indonesia's growth potential. Chains from both Singapore and Japan are making strategic moves, eyeing Jakarta for multiple site roll-outs, banking on the first-mover advantage as the Southeast Asian health and fitness landscape evolves.

Malaysia, Thailand, the Philippines, and Vietnam present a collective promise of growth. In Thailand, a resurgence in tourism is breathing life into hotel-affiliated fitness centers, which are now extending memberships to local residents, thus widening their reach. In Malaysia, noticeable ethnic and gender participation gaps unveil opportunities for bespoke programming. Meanwhile, Vietnam's recent spate of club closures hints at a market correction, paving the way for more agile players to seize the growing demand as disposable incomes rise. Across these nations, government-backed sports initiatives, coupled with public-private partnerships, are channeling grants and tax incentives into infrastructure enhancements, further propelling the growth of Southeast Asia's health and fitness club market.

Competitive Landscape

Evolution Wellness is spearheading a wave of strategic consolidations across six Southeast Asian nations, even as the market remains fragmented. This scale not only amplifies bargaining power for digital hardware but also trims down per-unit marketing expenses. Leading chains are harnessing technology as a competitive edge, integrating AI-driven form-correction cameras and rolling out exclusive fitness-tracking applications. In response, independent boutiques are fostering community-centric experiences and promoting wellness products, thereby bolstering customer loyalty.

Second-tier cities present untapped potential, boasting rising disposable incomes amidst a sparse supply. Meanwhile, corporate wellness contracts are still finding their footing; multinationals in Kuala Lumpur and Manila are actively pursuing multi-site memberships, aiming to curtail employee healthcare expenses. Entering the fray are tech-centric platforms, devoid of physical locations, yet collaborating with clubs to monetize digital content, thereby redefining boundaries in Southeast Asia's health and fitness club arena.

Strategic maneuvers underscore the intensifying competition. Anytime Fitness has set its sights on a 2024 expansion into Indonesia, opting for a franchise model to mitigate capital expenditure risks in emerging markets. Bio Farma's collaboration with Google Cloud and Fitbit is pioneering preventive-care data platforms, underscoring the potential of partnerships between healthcare and fitness entities. As stakeholders increasingly gravitate towards comprehensive wellness ecosystems over isolated services, such collaborations are poised for a surge.

Southeast Asia Health And Fitness Club Industry Leaders

-

Gold's Gym (RSG Group)

-

Virgin Active (VIRGIN GROUP)

-

Evolution Wellness

-

F45 Training Holdings Inc.

-

Pure International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Anytime Fitness partnered with Apple Fitness+ and offered new members a free 30-day membership with a minimum 13-month Anytime Fitness plan. This partnership aimed to provide members with an unmatched fitness experience by combining Anytime Fitness's in-club access, equipment, and coaching with Apple Fitness+'s extensive library of workouts and meditations.

- January 2024: Anytime Fitness Thailand, operating under Inspire Brands Asia (IBA), announced a significant expansion plan for Thailand, aiming to open 30 new clubs. This move is part of the brand's strategy to strengthen its leadership in the fitness franchise industry across the region. The expansion focused on prime locations in Bangkok and other high growth areas and is aimed at meeting the increasing demand for state-of-the-art facilities, round-the-clock access, personalized coaching, and a strong sense of community.

- January 2024: Anytime Fitness launched Be Fit Fest Season 2 of its annual "Be Fit Fest" campaign, which featured an innovative AI-powered video to engage a wider audience. The campaign aimed to raise awareness about the importance of balancing digital engagement with physical activity, particularly targeting the youth, who are deeply immersed in technology.

- January 2024: Virgin Active invested in Singapore and injected nearly USD 5 million into its Singaporean clubs to upgrade equipment and transform the clubs into more holistic wellness havens. This included the introduction of specialized programs and exclusive Fitness Therapy Zones. This investment highlighted Virgin Active's commitment to enhancing the member experience and adapting to evolving fitness and wellness trends in Singapore.

Southeast Asia Health And Fitness Club Market Report Scope

A health club is a facility center with exercise equipment for physical activities. It may be a for-profit commercial facility or a community- or institutionally-supported center. Such facilities accommodate professional athletes and casual members. The Southeast Asian health and fitness club market is segmented by service type (membership fees, personal training and instruction services, and other service types), outlet (chained and independent), and geography (Singapore, Malaysia, Thailand, Indonesia, Philippines, Vietnam, and Rest of Southeast Asia). The market sizing is in USD for all the abovementioned segments.

| Membership Fees |

| Personal Training and Instruction |

| Other Service Type |

| Chained Clubs |

| Independent Clubs |

| Male |

| Female |

| Singapore |

| Malaysia |

| Thailand |

| Indonesia |

| Philippines |

| Vietnam |

| Rest of Southeast Asia |

| By Service Type | Membership Fees |

| Personal Training and Instruction | |

| Other Service Type | |

| By Outlet Format | Chained Clubs |

| Independent Clubs | |

| By End User | Male |

| Female | |

| By Geography | Singapore |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Philippines | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How large is the Southeast Asia health and fitness club market in 2026?

The market is valued at USD 2.93 billion in 2026 with a 9.24% CAGR outlook to 2031.

Which service type is growing fastest across Southeast Asian clubs?

Personal training is expanding at a 11.78% CAGR, outpacing membership dues and other ancillary services.

Why is Indonesia considered the most attractive growth geography?

Indonesia combines 1% gym penetration with supportive preventive-health legislation and an expanding middle class, driving an 11.42% CAGR forecast.

How are technology trends reshaping club operations in the region?

Wearables, AI-driven coaching, and cloud-based CRMs are boosting retention, optimizing asset use, and differentiating member experiences.

What factors are driving the rise in female participation?

Specialized programming, flexible schedules, and government wellness campaigns are removing barriers and fueling an 11.08% CAGR in female memberships.

Are high operating costs a threat to small fitness businesses?

Yes, escalating rents and equipment outlays favor larger chains, prompting independents to pivot to niche formats or pursue consolidation.

Page last updated on: