Horse Riding Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

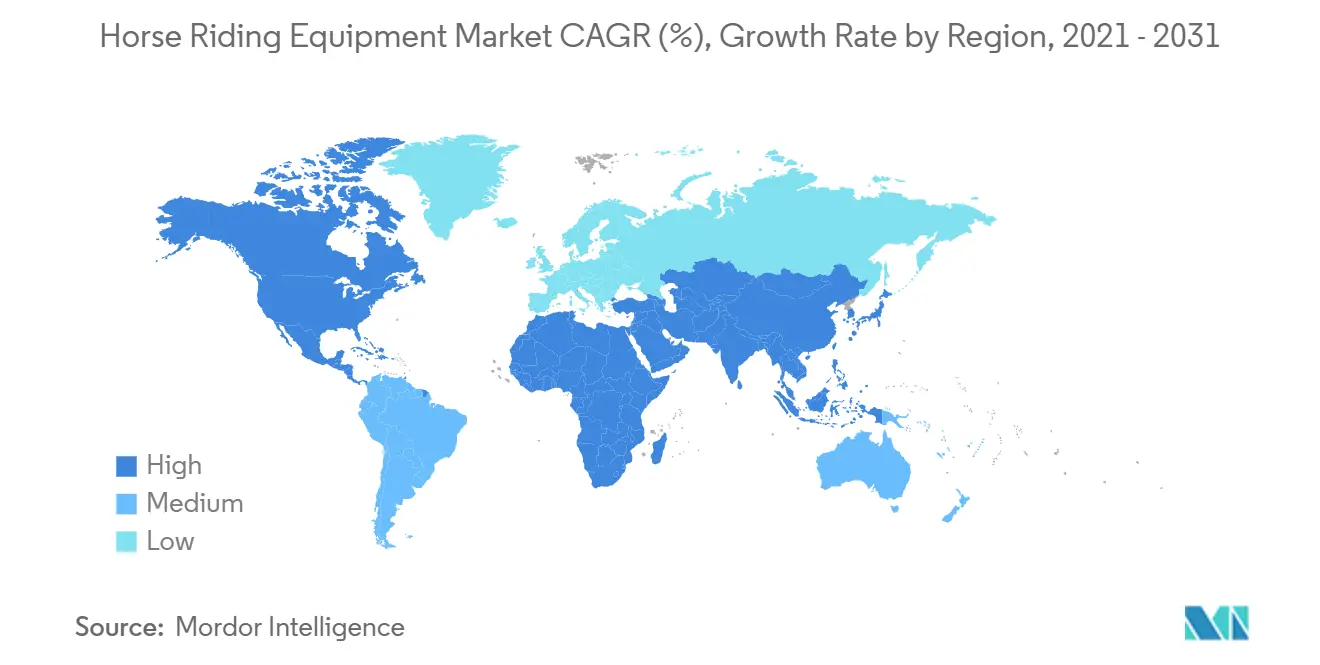

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Horse Riding Equipment Market Analysis by Mordor Intelligence

The horse riding equipment market size was valued at USD 0.93 billion in 2025 and estimated to grow from USD 0.98 billion in 2026 to reach USD 1.31 billion by 2031, at a CAGR of 5.87% during the forecast period (2026-2031). Tighter headgear and body protection standards across North America and Europe are shifting spending from discretionary to compliance-driven, thereby shortening replacement cycles and stabilizing underlying demand for certified products. The 2026 update to FEI-accepted helmet standards, together with the EU’s publication of EN 1384:2023, is pushing manufacturers to dual-certify models and refresh inventories created before recent benchmarks, which is supporting premium pricing for safety-led designs. Brands are responding with new materials and modular features that blend style with performance, while omnichannel operators expand experiential retail to complement digital research and purchasing habits. As safety protocols become institutionalized in riding schools and competition rules, the horse riding equipment market is positioned to grow through consistent safety-upgrade cycles rather than one-time discretionary purchases.

Key Report Takeaways

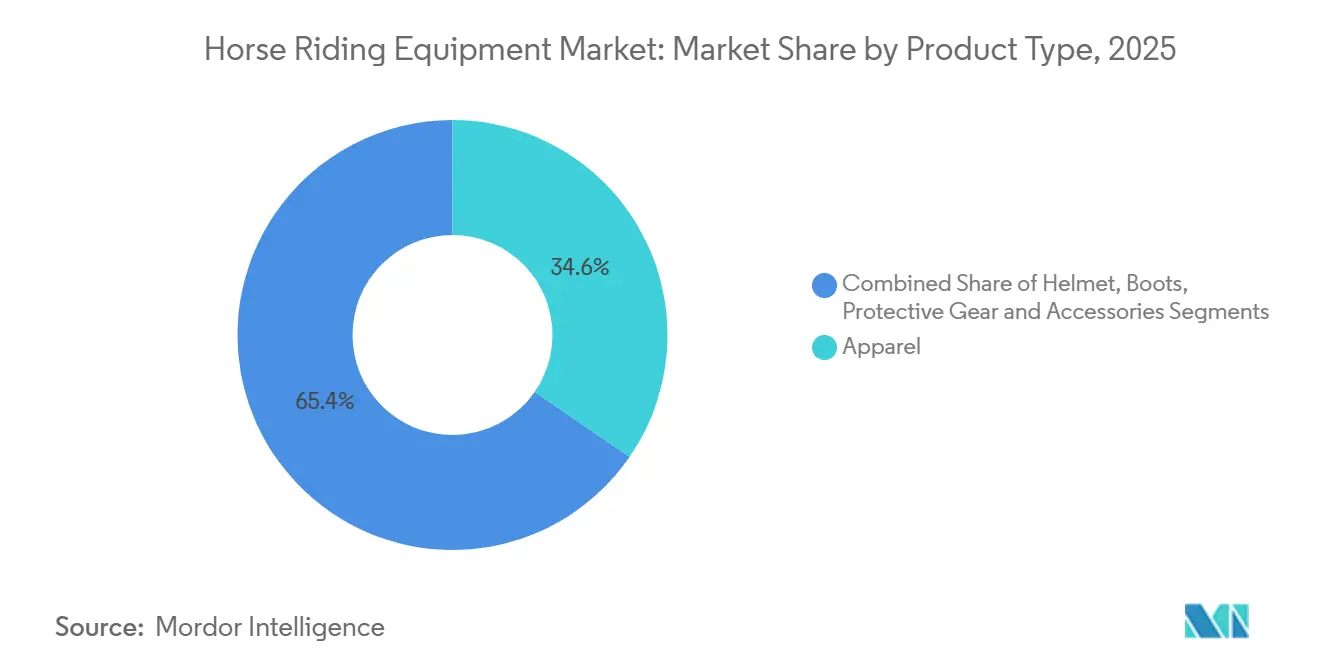

- By product type, apparel led with 34.55% revenue share in 2025, while protective gears and accessories are forecast to expand at a 7.57% CAGR through 2031.

- By end user, adults accounted for 86.28% of 2025 revenue, and the kids segment is projected to grow at a 6.18% CAGR to 2031.

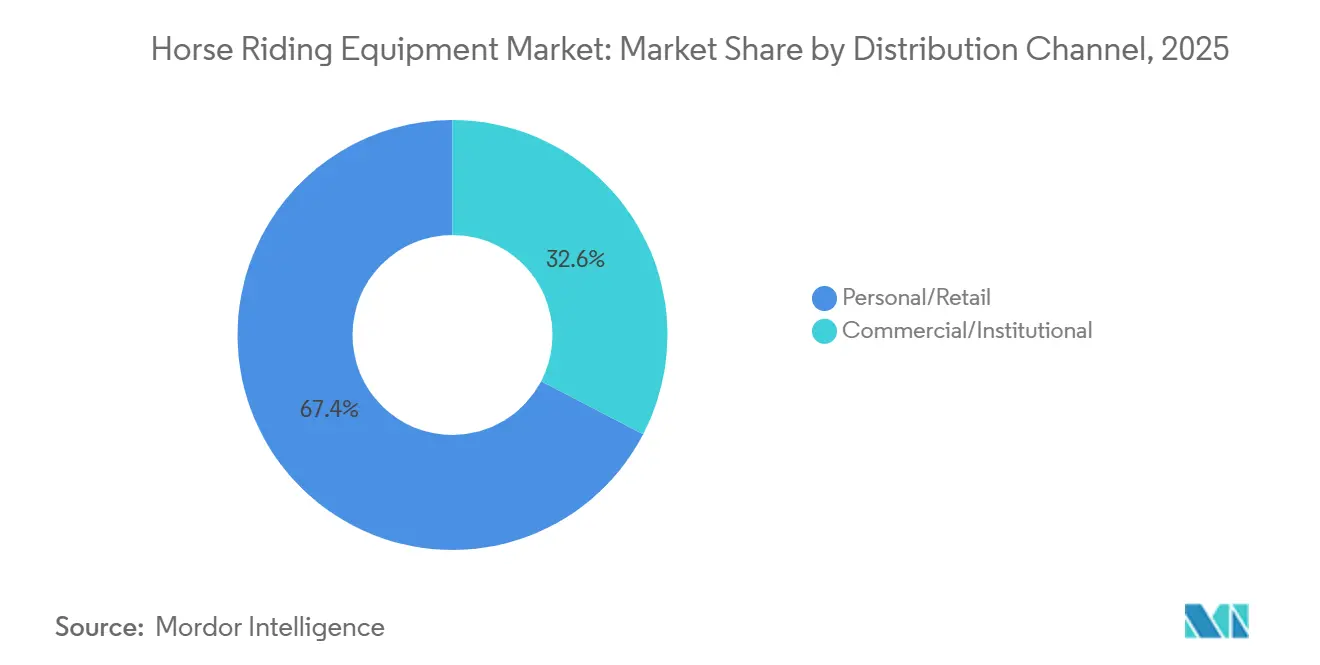

- By distribution channel, personal/retail held 67.36% share in 2025, while commercial/institutional channels are set to grow at a 5.94% CAGR through 2031.

- By geography, North America captured 43.42% share in 2025, and Asia-Pacific is expected to be the fastest-growing region at a 7.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Horse Riding Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Popularity of Recreational Horse Riding and Trail Adventures | +1.3% | Global, North America, Western Europe, and China, Thailand, UAE | Medium term (2-4 years) |

| Increasing Demand for Certified Rider Safety Equipment | +1.8% | North America and Europe, Middle East high-performance centers | Long term (≥ 4 years) |

| Expansion of Equestrian Tourism and Riding Schools Worldwide | +1.1% | China, Saudi Arabia, India | Medium term (2-4 years) |

| Technological Advancements in Smart Riding Helmets and Wearables | +0.9% | North America and Northern Europe, pilot programs in Australia and Japan | Long term (≥ 4 years) |

| Surge in Custom-Fit and Personalized Riding Equipment Preferences | +0.7% | Western Europe and North America, and urban Chinese markets | Short term (≤ 2 years) |

| Growing Influence of Social Media on Equestrian Lifestyle | +0.8% | Global with urban concentration across North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising popularity of recreational horse riding and trail adventures

Equestrian tourism bookings rose by 27% year-on-year in 2025, driven by increasing demand for wellness-oriented outdoor activities and culturally immersive travel experiences, according to Trip.com’s December report. Chinese millennials showed particularly strong interest in destinations such as Inner Mongolia and the Tibetan Plateau, reflecting a broader shift from competition-focused participation toward leisure riding and recreational experiences. European markets also experienced growth, with Icelandic trail-riding operators reporting capacity constraints during summer 2025 as tourists extended average trip durations from 3.2 to 4.7 days, increasing demand for multi-day riding packages that included guided tours and equipment rentals. Trail riding in regions with harsh climates, including Patagonia, the Canadian Rockies, and the Scandinavian highlands, contributed to a 29% increase in weatherproof equestrian equipment sales between 2024 and early 2026, encouraging manufacturers such as Dubarry of Ireland to introduce premium products like the Connemara tall boots with Gore-Tex linings in April 2025. Insurance and liability requirements also supported equipment demand, as riding schools increasingly mandated helmet use for trail excursions, while social media platforms accelerated consumer awareness, with horseback vacation-related hashtags on TikTok and Instagram surpassing 2.1 billion cumulative views by Q1 2026, according to ChinaTravelNews.

Increasing demand for certified rider safety equipment

The British Horse Racing Authority’s January 2025 requirement that all racecourse riders wear body protectors meeting BS EN 13158:2018 Level 2+ standards reflects the broader tightening of safety regulations across both competitive and recreational equestrian activities[1]Source: British Horse Society, “Horse Riding Helmets: Fitting & Safety,” The British Horse Society, bhs.org.uk. Advances in helmet testing are also reshaping product demand, with Virginia Tech Helmet Lab expanding its STAR rating system to include oblique-impact testing that simulates rotational forces associated with 64% of equestrian traumatic brain injuries. Manufacturers have responded through innovations such as Charles Owen’s integration of MIPS technology into its Halo helmet range, with MIPS-equipped models commanding 25–30% price premiums while achieving strong adoption rates globally[2]Source: Charles Owen, “Technology,” Charles Owen, charlesowen.com. Insurance providers and riding institutions are further reinforcing compliance, as international competitions increasingly require certified protective equipment and riding schools across North America mandate helmet use. Regulatory changes at the state level, including helmet laws introduced in New York and Florida in 2024 and 2025 for riders under 14 at public equestrian facilities, are also expanding the addressable market. At the same time, replacement cycles are accelerating due to recommendations from the Fédération Équestre Internationale to replace helmets every three to five years, alongside faster turnover in children’s equipment as riders outgrow products. Manufacturers are responding with accessibility-focused initiatives such as Samshield’s 2025 rental-exchange program covering 3,200 riding schools across eight countries, while organizations such as the British Horse Society continue to formalize certification requirements through updated 2026 guidance standards for assessments and international events.

Expansion of equestrian tourism and riding schools worldwide

China’s expanding equestrian infrastructure under the 14th Five-Year Plan, supported by approximately CNY 180 billion (USD 24.8 billion) in investment for venues and training facilities, is driving rising demand for riding equipment, particularly synthetic saddles that are 30% lighter and easier to maintain than leather alternatives, contributing to a 29% increase in bulk purchases between 2024 and 2025. International developments further reflect growing institutional investment, including the launch of Abu Dhabi Royal Equestrian Arts (ADREA) on Jubail Island in November 2025 as the first classical horsemanship school outside Europe, and the reopening of Hong Kong Jockey Club’s Pokfulam Public Riding School following a HKD 375 million (USD 48.1 million) redevelopment. Riding schools are also accelerating replacement cycles for shared equipment, such as helmets, due to hygiene and heavy-use requirements, while affordable product launches like Decathlon’s Fouganza range in India and Southeast Asia are expanding accessibility by offering EN-certified gear at prices 40–50% below those of specialist brands. Tourism integration is also supporting market growth, with Tuscany agriturismo operators reporting a 14% increase in horseback excursion bookings between 2024 and 2025, according to the World Travel & Tourism Council, while the European Commission’s Implementing Decision (EU) 2024/3260 is reducing cross-border operational barriers through harmonized equine movement regulations.

Technological advancements in smart riding helmets and wearables

Smart equestrian equipment is increasingly integrating wearable technology, data analytics, and connected ecosystems to support both performance monitoring and animal health management. Garmin’s Blaze equine wellness system combines GPS tracking and optical heart-rate monitoring through a tail-mounted sensor connected to smartphone apps and smartwatches, positioning equestrian wearables within the broader quantified-self trend. Similarly, Equestic’s SaddleClip, approved by the FEI and USEF for dressage competitions, applies AI algorithms trained on more than 400,000 rides across 65 countries to analyze gait, balance, impulsion, and symmetry with 99% precision, shifting rider expectations toward actionable performance insights rather than basic ride summaries. Product innovation is also extending into smart materials and preventive health monitoring; for example, Horse Pilot’s Teknit Boot uses adaptive 3D knit technology to improve fit and reduce production waste, while Protequus’ NightWatch Smart Halter monitors heart rate, respiration, activity, and distress indicators to detect conditions such as colic or foaling complications. However, adoption remains constrained by high costs and validation concerns, with premium products such as Equimetrics’ S-PRO saddle pad priced above USD 400 and industry groups such as the American Association of Equine Practitioners funding research to verify sensor accuracy in lameness detection. At the same time, manufacturers are increasingly pursuing app-based ecosystems integrating multiple devices and analytics platforms to create recurring subscription-based revenue models beyond one-time hardware sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Premium Horse Riding Equipment and Accessories | -1.2% | Global, APAC, Latin America, and MEA | Medium term (2-4 years) |

| Injury Risks and Safety Concerns Among Beginner Riders | -0.9% | Global, concentrated where professional instruction and supervision are limited | Long term (≥ 4 years) |

| Limited Accessibility to Professional Riding Facilities in Developing Regions | -0.7% | APAC, Sub-Saharan Africa, rural Latin America, select Middle East markets | Long term (≥ 4 years) |

| Counterfeit and Low-Quality Riding Gear Affecting Brand Trust | -0.6% | Core in APAC with global spillover via online marketplaces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of premium horse riding equipment and accessories

The equestrian equipment market remains highly segmented by price and income levels, with significant cost differences across product categories limiting accessibility for many consumers. Certified ASTM/SEI helmets with MIPS technology typically retail for USD 300-375 compared to USD 120–150 for standard models, while bespoke tall boots from brands such as Parlanti and Deniro can cost USD 1,200-1,800 versus USD 300-500 for mass-market alternatives. Although the American Horse Council estimated in 2024 that the US horse industry contributes USD 122 billion to the economy, median horse-owner income remains around USD 60,000, with 64% earning below USD 75,000, highlighting the sport’s growing middle-class participation despite its premium image. Rising material costs are adding further pressure, with leather prices increasing 22% between Q3 2024 and Q1 2025 due to supply disruptions in Pakistan and India. Affordability challenges are especially pronounced among youth, where parents often replace helmets every 2 years as children outgrow equipment, resulting in recurring costs of USD 200-400. Second-hand platforms such as Equestrian Closet and Ride on Reserve reported 24-28% annual growth between 2024 and 2025, although safety concerns remain, with Iberosattel Portal warning that one in four used saddles may contain hidden structural defects. In emerging markets, where annual per capita income averages USD 5,000-10,000, a full riding kit costing USD 800-1,000 represents a substantial financial barrier, creating opportunities for lower-cost brands such as Decathlon’s Fouganza, which offers EN-certified helmets below USD 100. Subscription and rental initiatives, including Samshield’s 2025 rental-exchange program across 3,200 riding schools, are helping reduce upfront costs, although these models remain most viable in dense European and North American markets with established logistics networks.

Injury risks and safety concerns among beginner riders

Equestrian sports continue to face participation barriers due to elevated injury risks, with concussion rates exceeding those in football or rugby and approximately one in five riders experiencing serious injuries, prompting insurers to tighten underwriting standards for riding schools. In the United States, insurance premiums for riding facilities increased by an average of 22% between 2022 and 2025, leading many operators to raise lesson fees or reduce capacity, thereby limiting access to affordable instruction. Regulatory measures are also expanding, including Maryland’s October 2024 helmet law for minors, which imposes fines of up to USD 250 for non-compliance, although enforcement remains inconsistent in rural regions. According to British Equestrian’s 2024 State of the Nation report, 60% of lapsed riders cited fear of injury as a key barrier to returning to the sport, while high-profile accidents involving minors continue to generate negative publicity and suppress participation. Safety standards are also increasing equipment costs; for example, the United States Pony Clubs’ updated January 2025 policies banning peacock stirrups and mandating body protectors for cross-country riding added an estimated USD 150–300 in additional expenses for participating families, highlighting the growing tension between rider safety and affordability[3]Source: United States Pony Clubs, “2025 USPC Safety Policy Updates,” United States Pony Clubs, ponyclub.org .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protective Gears Lead Innovation Velocity

The product mix continues to shift toward certified protection, with apparel remaining the largest share at 34.55% in 2025, while protective gear and accessories record the fastest trajectory at a 7.57% CAGR through 2031, reflecting regulatory support and advances in materials. The horse riding equipment market share for apparel reflects the broad base of everyday riders, while safety-driven adoption of helmets and body protectors drives upgrades as FEI-accepted standards and EU norms converge. Manufacturers continue to integrate rotational-impact systems and refined fit to sustain price premiums and demonstrate measurable benefits to riders in training and competition. The horse riding equipment market size for protective categories is supported by clearer guidance from associations on helmet fit and retirement timelines, which anchors predictable replacement cycles. As standards harmonize, riders and schools show a stronger willingness to invest in dual-certified models and novel impact-absorbing materials that target both linear and rotational forces.

Apparel innovation has tilted toward breathable knits, UV protection, and durable seat grips that extend use across seasonal changes, while tall boots and paddocks gain comfort and stability upgrades validated through event and lesson-day trials. Airbag vests are adding electronic deployment and multi-standard certification to improve usability and broaden appeal to riders who straddle disciplines or commute by bike or scooter, improving value across use cases. Sustainability features, such as recyclable or biodegradable components within armor layers, resonate with younger riders who want environmental progress alongside credible safety. With event operators and schools aligning rules to accepted standards, incremental gains in comfort and maintenance ease should continue to expand adoption for body protection beyond eventing into jumping and schooling contexts. These patterns keep protective categories central to growth in the horse riding equipments market through 2031.

By End User: Adults Dominate, Kids Segment Accelerates

Adults commanded 86.28% of 2025 spending because they tend to purchase fully built kits and replace apparel and footwear at a steady cadence, while the kids segment is set to expand at a 6.18% CAGR through 2031 as program participation and safety expectations rise. Youth safety policies that clarify minimum protection requirements and ban outdated designs are supporting more frequent helmet refresh cycles for growing riders, which speed up unit turnover in lesson barns and school teams. The horse riding equipment market benefits as parents favor certified headgear and fit-first footwear for confidence and injury mitigation during early training stages. Adult demand remains resilient in replacement cycles driven by comfort, ventilation, and aesthetic updates that keep kits current across seasons and disciplines.

Lifetime value increases when families and adult riders build brand trust at the beginning, which often carries over as riders progress and diversify their gear. Associations and event organizers are supporting this continuity through education and fit programs that help match riders to certified options and correct sizes. The horse riding equipment industry is also diversifying size ranges and offering youth-forward designs that make safety upgrades more attractive for style-conscious teens. By keeping safety front and center while improving comfort and aesthetics, brands can maintain momentum in the youth pipeline and retain engaged adult buyers who cycle through apparel and footwear on a predictable timeline.

By Distribution Channel: E-Commerce Gains Ground, Retail Holds

Personal and retail channels accounted for 67.36% of sales in 2025 as riders rely on in-person fittings for helmets, boots, and select apparel where precision sizing and comfort are critical, while commercial and institutional purchasing is projected to grow at 5.94% as riding schools formalize equipment standards. Experiential retail at major venues pairs event calendars with in-store fitting services to reduce returns and increase satisfaction, with multi-brand destinations building traffic through competition seasons. Retailers also extend reach through curated digital storefronts and flexible returns for footwear categories that otherwise carry high fit risk online. As institutions standardize safety requirements, there is a growing appetite for procurement programs that streamline compliance and maintenance.

Omnichannel operators are integrating content and team partnerships to turn online discovery into store visits and brand loyalty, with federation-branded capsules and seasonal collections anchoring campaigns. The horse riding equipment market continues to adopt digital tools for sizing and selection, while in-person fittings remain essential to address safety and comfort. Over the forecast period, retailers that harmonize inventory, service, and returns across channels should sustain share as institutional demand scales for certified equipment and lesson-ready kits.

Geography Analysis

North America held 43.42% of 2025 revenue, underpinned by mature participation across recreational and competitive formats and supported by clear certification pathways and retail infrastructure that pairs fittings with event calendars. Omnichannel expansion at leading venues continues to strengthen the connection between competition hubs and retail services that emphasize helmet and boot fitting. Partnerships with national bodies are elevating safety communication and awareness, and team-branded collections are helping translate visibility into purchases across footwear and apparel. Behind the scenes, consolidation in farrier distribution and upgraded supply networks are improving availability and service for hard goods categories that support farming and performance stables. These dynamics keep the horse riding equipment market on a firm footing in the region, sustained by predictable replacement cycles and continued retail investment.

Europe remains the second-largest region with strong traditions and institutional structures that support consistent gear refresh cycles as standards evolve. The EU’s harmonized EN 1384:2023 standard, reinforced by national guidance, is producing cross-border alignment on helmet performance and compliance documentation. Membership growth across federations and robust event calendars continue to drive apparel and protection demand even as household budgets adjust to inflation. Strategic investment in European manufacturing and distribution is strengthening premium saddle and apparel capacity, supporting export-led growth. As consumer expectations evolve toward sustainability and personalization, brands are expanding certified portfolios with aesthetic and fit options to protect share in a competitive market shaped by standards and style.

Asia-Pacific is the fastest-growing region with a projected 7.22% CAGR through 2031, supported by infrastructure investment for venues, training centers, and competition facilities under national plans that prioritize equestrian programs. Government allocations under China’s 14th Five-Year Plan exceeded CNY 180 billion (USD 24.8 billion) for equestrian infrastructure, which improves access and increases demand for certified headgear and lesson-ready kits across clubs and schools. Product launches that blend electronic airbag protection with riding and urban mobility use cases indicate how cross-category adoption can scale in regional markets with dense urban riders. Wearables and analytics-enabled tack are also gaining profile as riders adopt mainstream fitness ecosystems that integrate equine metrics. The horse riding equipments market in APAC should continue to benefit from facility growth, safety standard alignment, and localized assortments that balance affordability with certification.

Competitive Landscape

The horse riding equipment market operates with moderate concentration, reflecting competitive dynamics where established brands leverage certification expertise and retail footprints to defend premium segments, yet remain vulnerable to digital-native disruptors and private-equity-backed consolidators reshaping value chains. Product leadership increasingly depends on translating standard updates and test data into clear rider benefits while maintaining comfort and fit across sizes. Headgear stands out for visible innovation as brands integrate rotational-impact technologies, airflow management, and refined retention systems to command premiums. At the same time, tall boots and paddocks advance with durability and stability features tested across schooling and event routines to reduce fatigue and improve control.

Strategic moves across the value chain have expanded capacity, footprint, and category coverage. A leading U.S. equestrian venue added a flagship store for a major retailer, deepening fittings and services tied to competition schedules. Team partnerships with national federations support education and co-branded collections that reinforce certified protection and apparel performance. In the farrier distribution channel, integration with a global horseshoe manufacturer improved product availability and broadened a consolidated brand roster across North America. On the equipment side, a major surfaces and training products company acquired an established jumps and cavaletti brand, preserving supply to show organizers and retailers. These coordinated steps help incumbents protect share while preparing for faster handling of standards-driven replacement cycles.

Sustainability and smart protection are emerging as differentiators. Biodegradable armor components and recyclable materials are moving from concept to limited production, which aligns with the expectations of younger riders without diluting safety claims. Electronic airbags that achieve multi-standard certification and app-connected wearables show how safety and analytics can converge to expand utility across riding and daily mobility, unlocking recurring engagement beyond a single piece of gear. As certification, comfort, and digital analytics become table stakes, winners will integrate standards credibility with omnichannel fitting services and transparent service policies that reduce friction and protect brand trust in the horse riding equipments market.

Horse Riding Equipment Industry Leaders

Ariat International

Dover Saddlery

Decathlon (Fouganza)

Charles Owen

Samshield

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Decathlon (Fouganza) and In&motion launched the Fouganza electronic airbag vest, the first to achieve dual certification for horse riding (NF S72-800) and urban mobility (AMU-001), deploying in 60 milliseconds to protect the back, chest, abdomen, and neck without cables or external sensors.

- February 2026: Ariat introduced the M7 Classic Rise jean with a higher rise for improved saddle coverage, addressing rider feedback on comfort and functionality during extended sessions.

- February 2025: Horseware Ireland and EquiFit announced a strategic merger, forming a partnership to enhance global market presence, with EquiFit maintaining an independent brand identity as a premium offering alongside Micklem and Alessandro Albanese within Horseware's portfolio.

- February 2025: Ariat unveiled the redesigned Heritage Paddock Boot featuring padded collars with mobility curves, elastic twin gores, modernized rubber branding, and Duratread outsoles with rider-tested traction zones including specialized stirrup grip across the forefoot.

Global Horse Riding Equipment Market Report Scope

Horse riding equipment refers to protective gear, apparel, and accessories used by riders to ensure safety, comfort, and performance during equestrian activities. The horse riding equipment market is segmented by product type, end user, distribution channel, and geography. By product type, the market includes helmets, protective gear and accessories, boots, and apparel. Based on end user, the market is categorized into kids and adults. By distribution channel, the market is segmented into commercial/institutional and personal/retail channels. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market size and forecasts provided for each region. Market sizing and forecasts for all segments are calculated based on value (USD).

| Helmet |

| Protective Gears and Accessories |

| Boots |

| Apparel |

| Kids |

| Adults |

| Commercial/Institutional |

| Personal/Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Belgium | |

| Iceland | |

| Portugal | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| Australia | |

| Mongolia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa |

| By Product Type | Helmet | |

| Protective Gears and Accessories | ||

| Boots | ||

| Apparel | ||

| By End User | Kids | |

| Adults | ||

| By Distribution Channel | Commercial/Institutional | |

| Personal/Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Iceland | ||

| Portugal | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| Australia | ||

| Mongolia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the horse riding equipments market?

The horse riding equipments market size is USD 0.98 billion in 2026 and is projected to reach USD 1.31 billion by 2031, reflecting a 5.9% CAGR over 2026-2031.

Which segments are leading and which are growing fastest in this space?

Apparel led with 34.55% revenue share in 2025, while protective gears and accessories are the fastest-growing category at a 7.57% CAGR through 2031.

How are safety standards influencing buying behavior in the horse riding equipments market?

FEI-accepted standards and updates to ASTM and EN 1384:2023 are compressing replacement cycles and making certified protective gear a compliance purchase rather than a discretionary choice.

Which regions are most important for demand and growth?

North America held 43.42% of 2025 revenue due to mature participation and retail infrastructure, while Asia-Pacific is the fastest-growing at 7.22% CAGR through 2031.

Page last updated on: