Transthyretin Amyloidosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

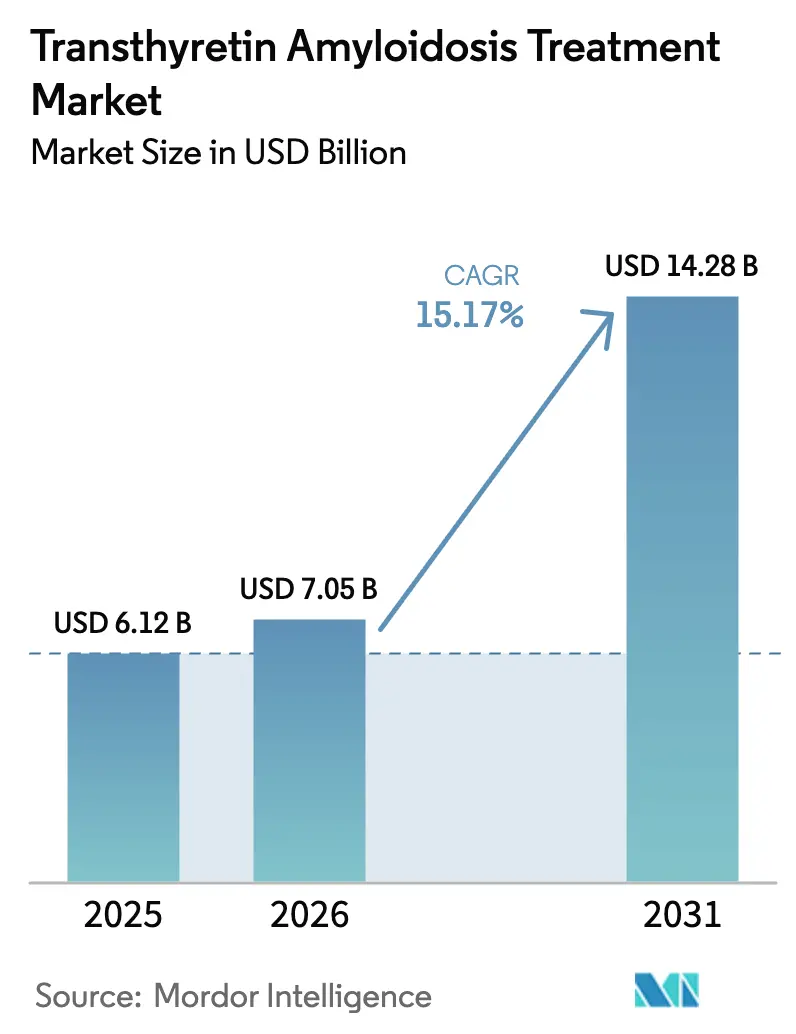

| Market Size (2026) | USD 7.05 Billion |

| Market Size (2031) | USD 14.28 Billion |

| Growth Rate (2026 - 2031) | 15.17% CAGR |

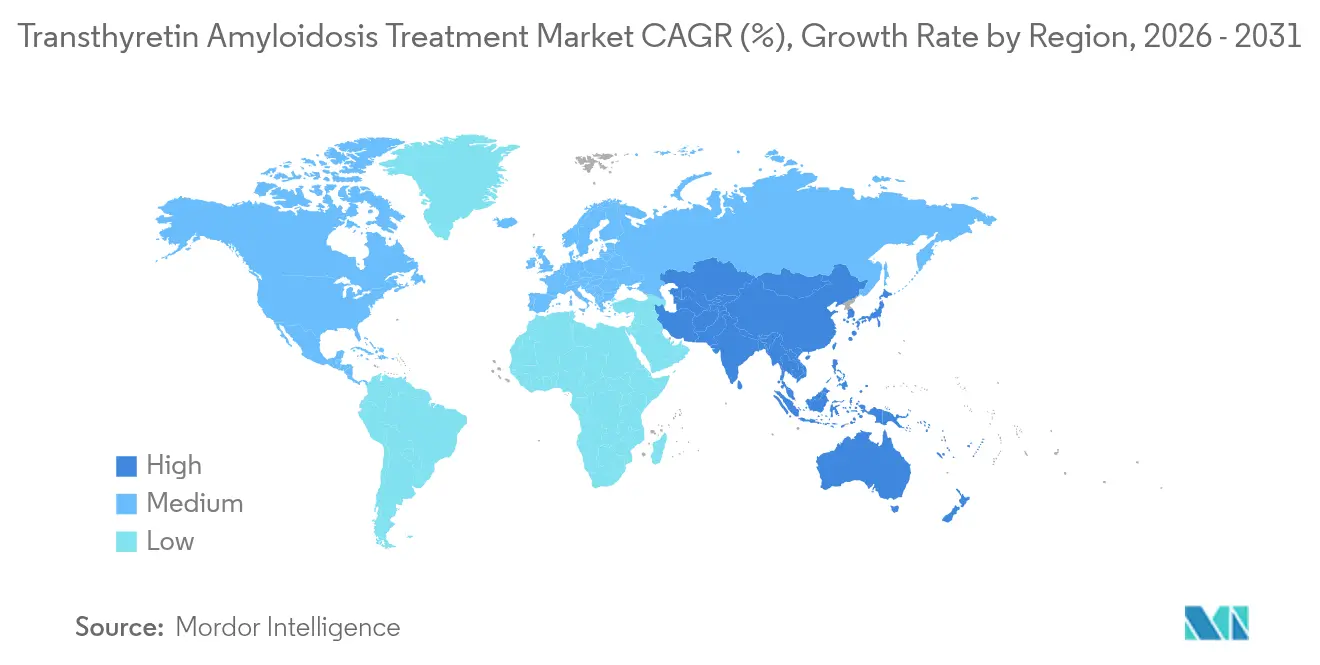

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transthyretin Amyloidosis Treatment Market Analysis by Mordor Intelligence

The Transthyretin Amyloidosis Treatment market size is expected to grow from USD 6.12 billion in 2025 to USD 7.05 billion in 2026 and is forecast to reach USD 14.28 billion by 2031 at 15.17% CAGR over 2026-2031.

This growth reflects rapid regulatory approvals for disease-modifying agents, broadening payer coverage, and earlier detection by AI-enabled screening platforms. Novel stabilizers such as acoramidis and next-generation silencers like vutrisiran reduce cardiovascular death and hospitalization, while single-dose CRISPR interventions promise curative potential. An aging population with preserved-ejection-fraction heart failure, combined with the addition of amyloidosis markers to cardiology guidelines, further widens the diagnosed patient pool. North America leads adoption, but Asia-Pacific shows the fastest expansion as Japan, China, and Australia accelerate approvals and domestic manufacturing capacity.

Key Report Takeaways

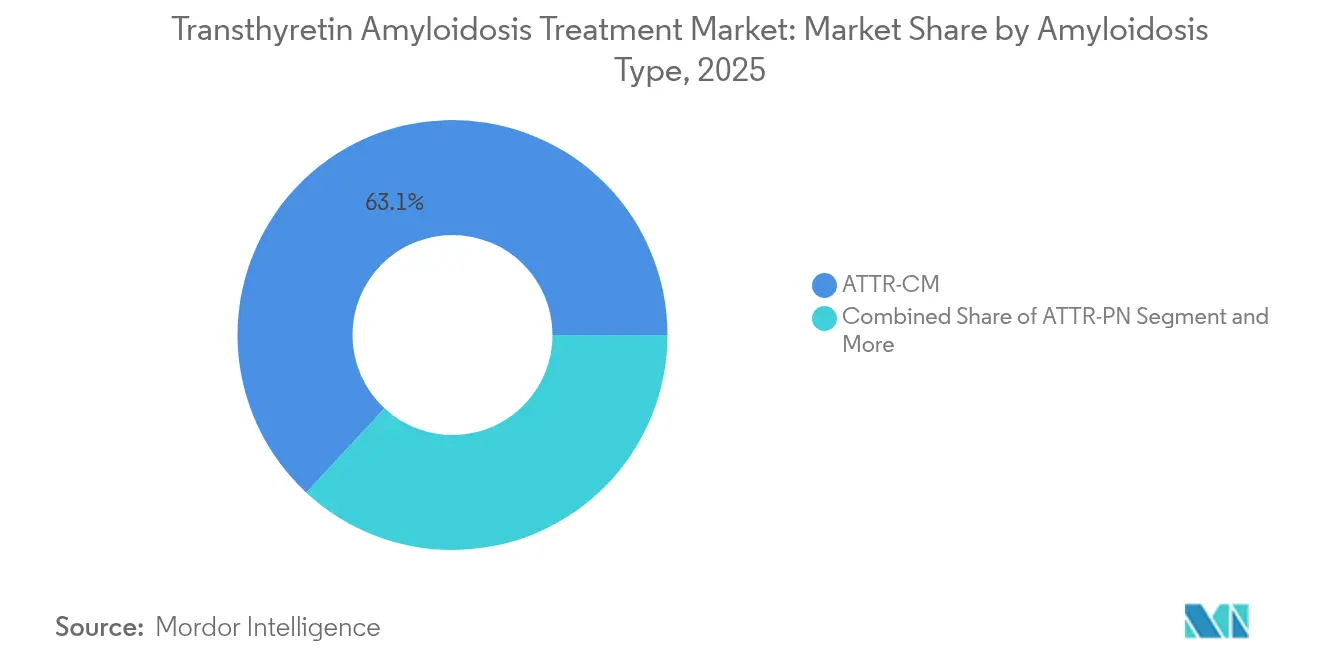

- By amyloidosis type, cardiac manifestations (ATTR-CM) held 63.10% of transthyretin amyloidosis treatment market share in 2025, whereas polyneuropathy variants are projected to expand at 28.12% CAGR to 2031.

- By therapy class, stabilizers accounted for 52.95% of the transthyretin amyloidosis treatment market size in 2025, while silencers are poised to grow at 29.60% CAGR through 2031.

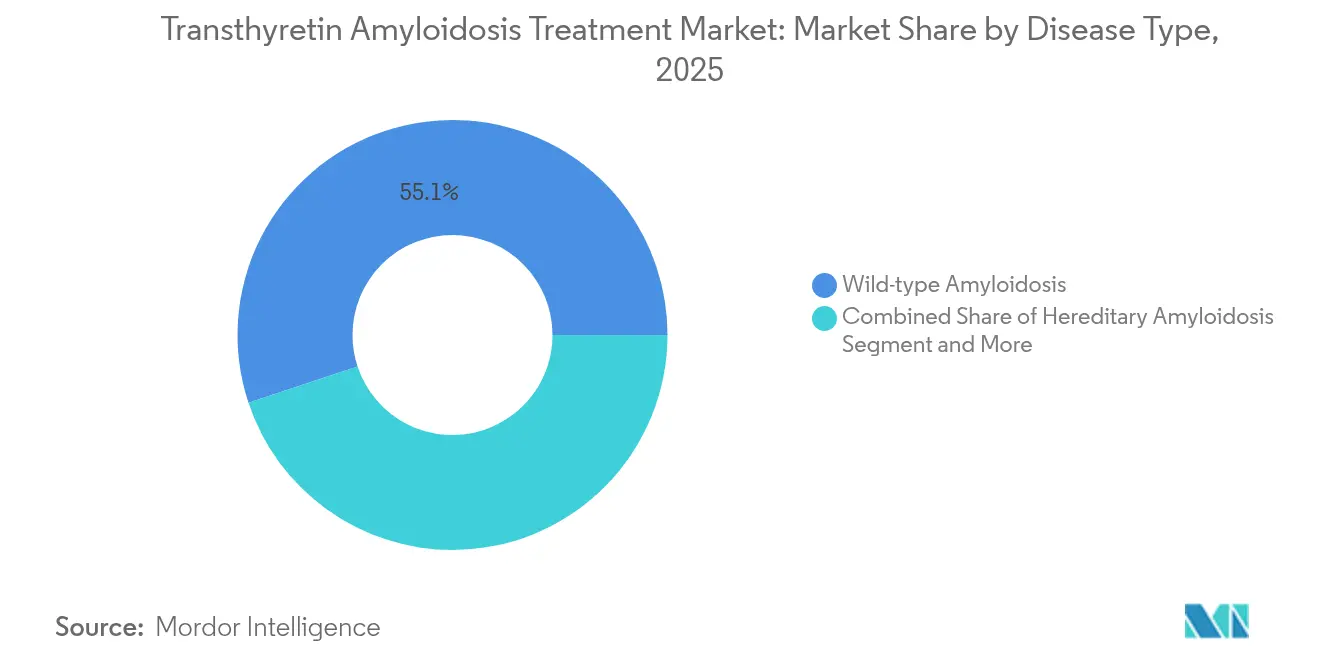

- By disease type, wild-type presentations contributed 55.10% revenue in 2025; hereditary forms are accelerating at 31.40% CAGR on rising genetic-testing uptake.

- By distribution channel, hospital pharmacies controlled 67.45% sales in 2025; specialty channels are advancing at 28.55% CAGR to 2031.

- By geography, North America captured 47.20% revenue in 2025, whereas Asia-Pacific is forecast to climb at 18.20% CAGR, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transthyretin Amyloidosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & HFpEF Prevalence Surge | +3.2% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Regulatory Approvals Of Disease-Modifying Drugs | +4.1% | North America, Europe, Japan | Medium term (2-4 years) |

| Intensifying Clinical-Trial Pipeline (RNA-Silencers, Gene Editing) | +2.8% | Global, led by US & EU regulatory pathways | Long term (≥ 4 years) |

| Rising Disease Awareness Via Centres & Advocacy Groups | +1.9% | Global, with early gains in developed markets | Medium term (2-4 years) |

| AI-Enabled Echocardiography Screening Tools | +1.5% | North America, Europe, select APAC markets | Short term (≤ 2 years) |

| ATTR Markers Added To HF Guidelines/Reimbursement | +2.3% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory approvals of disease-modifying drugs

Three pivotal approvals in 2024-2025 redefined the transthyretin amyloidosis treatment market. The FDA cleared acoramidis in November 2024 after a Phase 3 trial showed 42% fewer deaths and hospitalizations than placebo[1]U.S. Food and Drug Administration, “FDA approves drug for heart disorder caused by transthyretin-mediated amyloidosis,” fda.gov. Vutrisiran followed in March 2025, reducing all-cause mortality by 36% in 655 patients. Europe approved acoramidis in November 2025, and Japan did so in March 2025, creating near-simultaneous global access. These decisions end the tafamidis monopoly, introduce price competition, and broaden mechanistic diversity for different disease stages.

Intensifying clinical-trial pipeline (RNA silencers, gene editing)

CRISPR innovation accelerated as Intellia’s single-dose NTLA-2001 cut mean serum TTR 91% at day 28 in 72 participants. Alnylam’s nucresiran achieved 96% peak reduction with biannual dosing, ushering in longer-acting regimens. Intellia’s 765-patient MAGNITUDE Phase 3 study marks the first pivotal in-vivo gene-editing trial, while Neurimmune’s ALXN2220 Phase 3 effort introduces amyloid depletion. Pipeline breadth supports precision treatment algorithms matched to disease phenotype, mutation, and stage.

Rising disease awareness via centres & advocacy groups

International registries revealed 18% ATTR-CM prevalence among high-risk heart-failure cohorts, up from earlier estimates. The Mayo Clinic detected cardiac amyloidosis in 1.25% of > 31,000 echocardiograms[2]American College of Cardiology, “Efficacy and Safety of Acoramidis,” acc.org. Consensus guidelines published in 2024 recommend routine screening in bilateral carpal-tunnel patients, where 13.4% had ATTR-CM. BridgeBio’s TRACE-AI network deploys machine-learning tools across health systems, multiplying case-finding beyond specialist referrals. Earlier identification enlarges the treatable population and sustains market growth.

AI-enabled echocardiography screening tools

AI models now detect cardiac amyloidosis with 91.1% AUC on routine ECGs. Pfizer’s hospital-based deployments facilitate large-scale automated image analysis, flagging candidates for confirmatory scans. The PANES-HF study documented novice echocardiography paired with AI yielding 84.6% sensitivity and 91.4% specificity. Multicentre algorithms standardize cardiac scintigraphy interpretation, minimizing inter-reader variability. These advances shorten diagnostic latency from 8.6 years to months, expanding the transthyretin amyloidosis treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-High Therapy Costs | -2.8% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Under-Diagnosis Due To Non-Specific Symptoms | -3.1% | Global, pronounced in APAC & Latin America | Medium term (2-4 years) |

| Limited RNA-Therapy Manufacturing Capacity | -1.9% | Global, supply chain concentrated in US & EU | Short term (≤ 2 years) |

| Payer Prior-Authorisation & Cost-Containment Pressure | -2.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ultra-high therapy costs

Annual list prices surpass USD 225,000 for tafamidis and USD 244,000 for acoramidis, placing them among the costliest cardiovascular drugs. Health systems adopting value-based frameworks demand real-world outcome data to justify budgets, and insurers impose step-therapy rules before covering premium agents. These economics restrict uptake in lower-income regions and could temper overall market velocity unless negotiated discounts widen access.

Under-diagnosis due to non-specific symptoms

Up to 80% of patients remain unidentified worldwide. Wild-type disease often presents with musculoskeletal or autonomic symptoms that delay suspicion. European centers detect 24% prevalence in high-risk heart-failure clinics compared with 5% in North America, underscoring variable awareness. In 5% of biopsy-confirmed cases, bone-scintigraphy is negative, necessitating invasive biopsy[3]Orphanet Journal of Rare Diseases, “Bone scintigraphy limitations in cardiac uptake,” ojrd.com. Education and AI-driven diagnostics are expected to narrow this gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Amyloidosis Type: Cardiac Manifestations Drive Market Leadership

ATTR-CM generated 63.10% of 2025 revenue, underpinned by validated scintigraphy and echocardiography pathways and robust cardiology networks. The transthyretin amyloidosis treatment market size for cardiac phenotypes is projected to progress at double-digit CAGR, reinforced by mortality-lowering data from both stabilizers and silencers. ATTR-PN, although smaller, is on a 28.12% trajectory as vutrisiran and eplontersen win broader neurology indications.

Mixed-phenotype cases form a rising clinical subset, prompting combined organ-targeted strategies. THAOS registry evidence shows high-dose tafamidis delivering neurological stability in cardiac-dominant patients, illustrating tailored dosing. Early carpal-tunnel signs, detected in 22% of cardiac patients during routine orthopedic surgery, serve as a cross-phenotype screening trigger. Continuous phenotype refinement sustains stratified demand in the transthyretin amyloidosis treatment market.

By Therapy: Stabilizers Maintain Dominance Amid Silencer Innovation

Stabilizers retained 52.95% revenue share in 2025, paced by once-daily oral tafamidis and acoramidis, the latter achieving ≥ 90% stabilization. The transthyretin amyloidosis treatment market size attributed to stabilizers is forecast to rise steadily yet cede proportion to silencers as mortality curves favor RNA interference.

Silencers are advancing 29.60% annually, aided by quarterly subcutaneous dosing and dual cardiac-neurologic labeling. Gene editing threatens to redraw boundaries; NTLA-2001’s 91% knockdown after a single infusion positions it as a future one-time cure. Depleter antibodies such as ALXN2220 add further mechanistic variety, ensuring multi-modal regimens will characterize the transthyretin amyloidosis treatment market.

By Disease Type: Wild-Type Prevalence Drives Hereditary Innovation

Wild-type disease, representing 55.10% of 2025 sales, dominates aging Western populations. Prevalence reaches 16.8% among preserved-ejection-fraction heart-failure patients, reinforcing volume growth. Hereditary variants grow 31.40% per year as sequencing panels become routine and ethnic-specific mutations receive targeted outreach. The transthyretin amyloidosis treatment market share for hereditary forms is set to widen with mutation-directed registries and newborn-screening pilots.

Ethnic clustering shapes regional strategies: Val122Ile affects 3.4% of African Americans, Ala97Ser is prevalent in East Asia, and Val50Met remains endemic in Portugal and Sweden. Precision screening plus pipeline mutation-specific agents position hereditary segments for outsized contribution to overall transthyretin amyloidosis treatment industry expansion.

By Distribution Channel: Hospital Networks Dominate Specialty Growth

Hospital pharmacies controlled 67.45% spending in 2025 owing to infusion infrastructure and cardiology-neurology co-management. Specialty pharmacies, however, are scaling at 28.55% as home-based RNA administration and manufacturer patient-service hubs proliferate. The transthyretin amyloidosis treatment market size captured by specialty channels is set to rise further after the 2025 Medicare Part D redesign limits out-of-pocket liability to USD 2,000, a policy likely to migrate to other advanced economies.

Retail pharmacies stay marginal because prior-authorisation steps and cold-chain complexities deter stocking. As gene-editing therapies reach commercialization, single-dose hospital infusion combined with lifelong hematology oversight will reinforce hospital dominance while enlarging specialty follow-up services.

Geography Analysis

North America retained 47.20% revenue in 2025, sustained by early FDA approvals, Medicare coverage, and > 1,300 dedicated amyloid clinics. Mayo Clinic data show 1.25% amyloidosis prevalence in echocardiography cohorts, underscoring strong screening penetration. The region’s Part D cost cap entering 2025 improves affordability, likely raising prescription volume for premium agents.

Europe benefits from unified regulatory decisions; the November 2025 acoramidis approval synchronized launches across 27 EU states. Diagnostic prevalence is 24% in high-risk heart-failure clinics, higher than other regions. Germany and Italy host robust amyloidosis centers, while the Bayer-BridgeBio alliance ensures commercial reach. Emerging EU markets leverage cross-border treatment programs, widening access without duplicative regulatory delays.

Asia-Pacific posts the fastest CAGR at 18.20% through 2031. Japan approved acoramidis in March 2025, establishing first-in-class access and reimbursement inside a mature cardiovascular market. China’s EPIC-ATTR study evaluates eplontersen among domestic patients, supporting eventual National Reimbursement Drug List inclusion. Australia’s RNA Blueprint underpins regional production, while Korea’s 13.4% prevalence in preserved-ejection-fraction cohorts points to latent demand. These dynamics collectively bolster the transthyretin amyloidosis treatment market across APAC.

Competitive Landscape

The market shows moderate concentration yet intensifying rivalry. Pfizer’s tafamidis franchise delivered USD 1.5 billion in 2024, exploiting first-mover status and a global footprint. BridgeBio’s acoramidis posted USD 36.7 million in its first quarter, far surpassing projections and signaling swift physician uptake. Alnylam’s TTR portfolio generated USD 1.223 billion, validating silencers as mainstream alternatives.

Gene-editing disruptors loom; Intellia’s Phase 3 MAGNITUDE trial with 765 participants may usher in single-dose cures, potentially compressing chronic-therapy revenue models. Neurimmune’s ALXN2220 antibody tackles amyloid plaque removal, complementing stabilizers and silencers. Diagnostics firms like Attralus, armed with FDA Breakthrough status for 124I-evuzamitide PET imaging, aim to close detection gaps that currently stifle eligible-patient capture. Competitive differentiation now hinges on access programs, AI-screening alliances, and real-world evidence demonstrating survival gains in diverse populations.

Transthyretin Amyloidosis Treatment Industry Leaders

Pfizer Inc.

Alnylam Pharmaceuticals, Inc.

Intellia Therapeutics, Inc.

AstraZeneca PLC

BridgeBio Pharma Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alnylam received FDA approval for AMVUTTRA (vutrisiran), the first RNAi agent to cut cardiovascular death, hospitalizations, and urgent heart-failure visits in adults with ATTR-CM.

- March 2025: BridgeBio won Japanese approval for BEYONTTRA (acoramidis), extending near-complete TTR stabilization to Asia’s largest drug market

Global Transthyretin Amyloidosis Treatment Market Report Scope

As per the scope of the report, transthyretin amyloidosis is a rare disease characterized by the abnormal accumulation of misfolded transthyretin protein, forming amyloid deposits in tissues and organs. Treatment can help manage symptoms, slow disease progression, and improve quality of life.

The transthyretin amyloidosis treatment market is segmented into type, therapy, disease type, distribution channel, and geography. By type, the market is segmented into ATTR-CM (transthyretin amyloid cardiomyopathy) and ATTR-PN (transthyretin amyloid polyneuropathy). By therapy, the market is segmented into targeted therapy and supportive therapy. By disease type, the market is segmented into hereditary amyloidosis, wild-type amyloidosis, and other disease types. Other disease types include AL amyloidosis, AA amyloidosis, and localized amyloidosis. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and other distribution channels. Other distribution channels include specialty pharmacies and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The report offers market size and forecast in terms of the value (USD) for the above segments.

| ATTR-CM |

| ATTR-PN |

| Others |

| Stabilizers |

| Silencers |

| Depleters / Transplant |

| Wild-type Amyloidosis |

| Hereditary Amyloidosis |

| Mixed-phenotype |

| Hospital Pharmacies |

| Retail Pharmacies |

| Specialty Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Amyloidosis Type | ATTR-CM | |

| ATTR-PN | ||

| Others | ||

| By Therapy | Stabilizers | |

| Silencers | ||

| Depleters / Transplant | ||

| By Disease Type | Wild-type Amyloidosis | |

| Hereditary Amyloidosis | ||

| Mixed-phenotype | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Specialty Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the transthyretin amyloidosis treatment market?

The market generated USD 7.05 billion in 2026 and is projected to reach USD 14.28 billion by 2031.

Which therapy class is growing the fastest?

RNA silencers are advancing at 29.60% CAGR through 2031 due to strong survival benefits and quarterly subcutaneous dosing.

Why is Asia-Pacific the fastest-growing region?

Rapid regulatory approvals in Japan and expanding clinical infrastructure in China and Australia are driving an 18.20% CAGR for the region.

How do CRISPR gene-editing programs impact future treatment?

Single-dose approaches like NTLA-2001 reduce serum TTR by 91% and could shift the market from chronic therapy to curative intervention.

What limits broader patient access to new drugs?

Ultra-high annual list prices above USD 225,000, prior-authorisation rules, and under-diagnosis in primary care settings remain key barriers.

Page last updated on: