Global Amyotrophic Lateral Sclerosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 1.27 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Amyotrophic Lateral Sclerosis Treatment Market Analysis by Mordor Intelligence

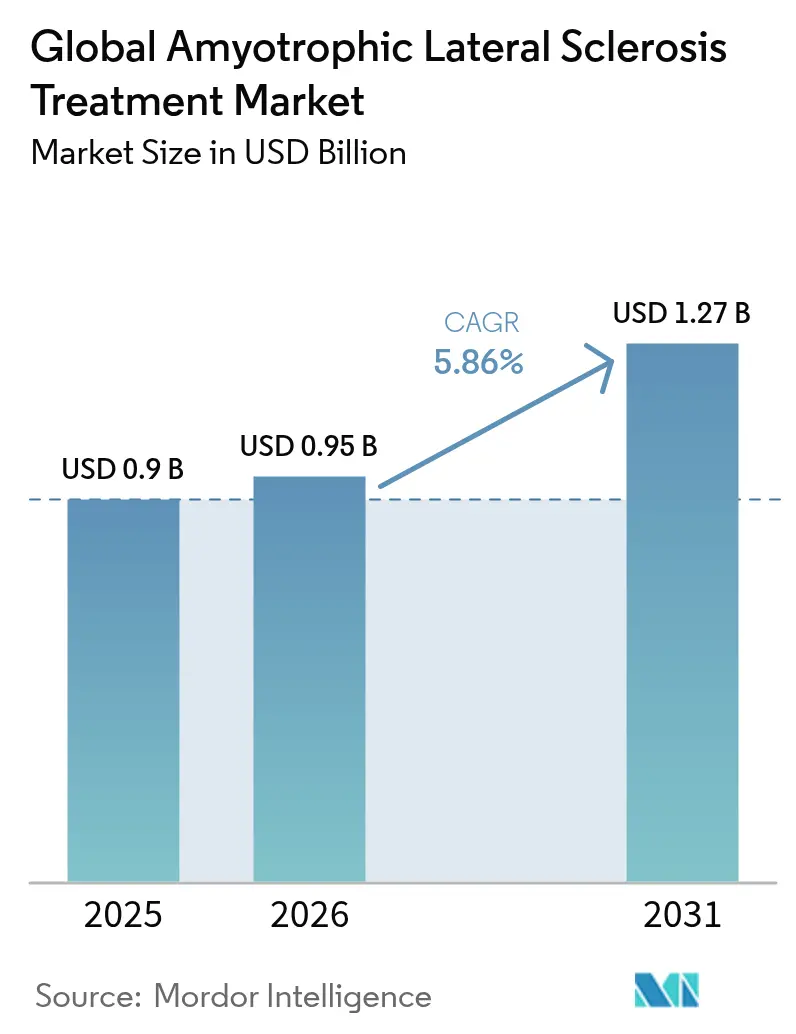

The Amyotrophic lateral sclerosis treatment market size was valued at USD 0.9 billion in 2025 and estimated to grow from USD 952.74 million in 2026 to reach USD 1.27 billion by 2031, at a CAGR of 5.86% during the forecast period (2026-2031). The growth trajectory reflects a decisive shift from symptomatic relief toward disease-modifying options as the first antisense oligonucleotide (ASO) for SOD1-ALS secured United States approval in 2023, followed by European clearance in 2024. Commercial momentum is reinforced by an expanding orphan-drug pipeline, regulatory fee waivers, and right-to-try provisions that collectively shorten time to market and widen patient access. Capacity investments in oligonucleotide manufacturing, together with scalable viral-vector platforms, are lowering per-dose production costs and improving gross margins for gene-based products. Meanwhile, multidisciplinary ALS centers continue to demonstrate survival and quality-of-life benefits that underpin a steady rise in specialty-clinic prescriptions. Market risks include biologics capacity shortfalls, high therapy prices, and emerging safety signals for edaravone, yet patient advocacy and AI-enabled drug-repurposing initiatives sustain capital inflows and diversify the therapeutic portfolio.

Key Report Takeaways

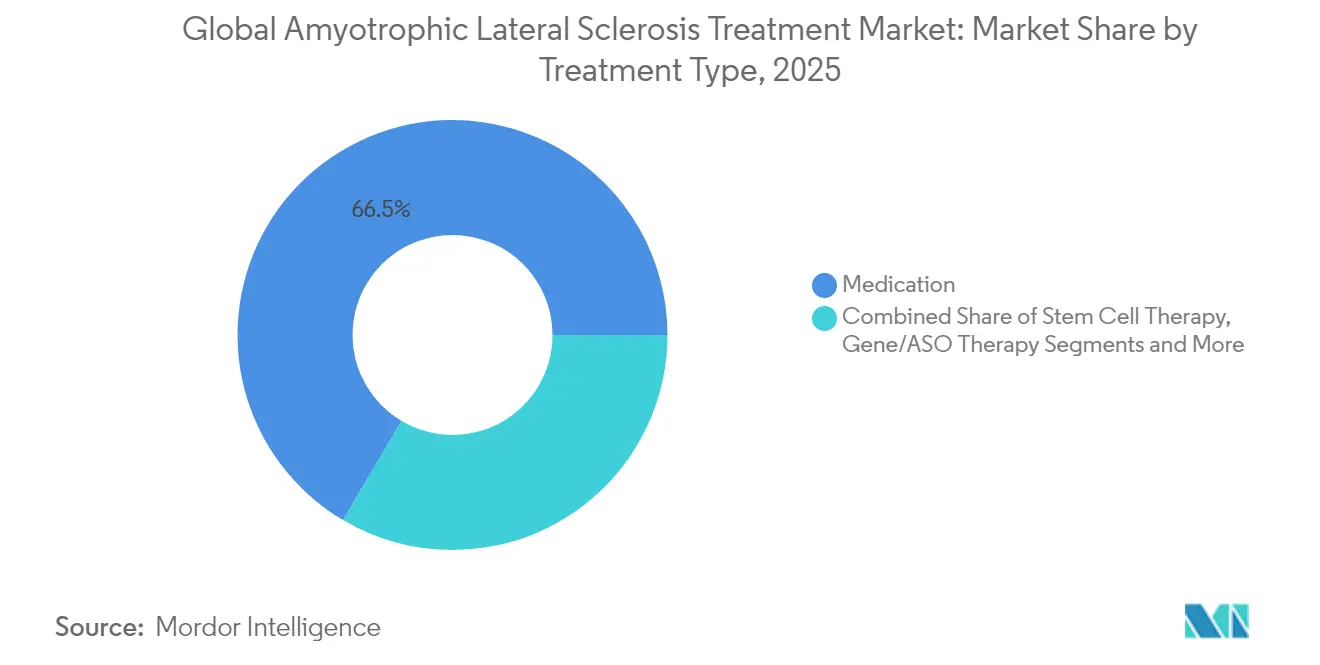

- By treatment type, medication held 66.50% of 2025 revenue, while gene & ASO therapy is forecast to expand at a 6.55% CAGR through 2031.

- By drug class, riluzole led with 37.40% of the Amyotrophic lateral sclerosis treatment market share in 2025; ASOs post the fastest 5.45% CAGR to 2031.

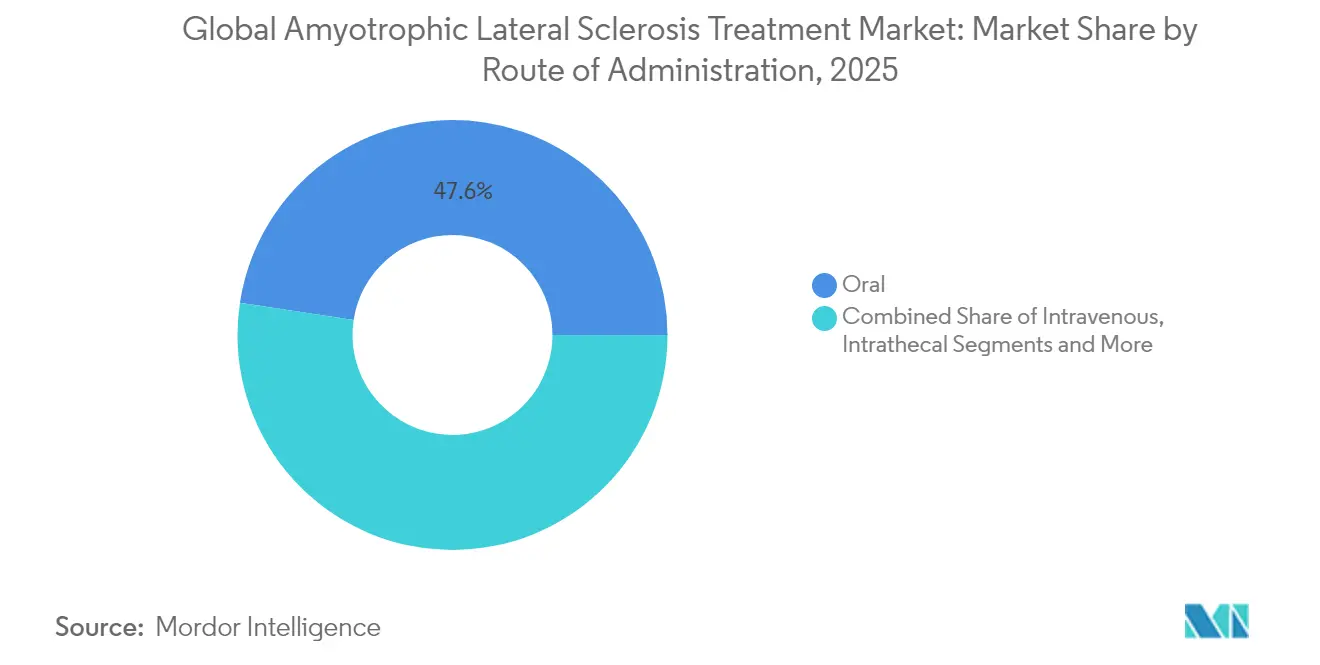

- By route of administration, oral products accounted for 47.60% of the Amyotrophic lateral sclerosis treatment market size in 2025; intrathecal delivery is rising at 5.62% CAGR.

- By end-user, hospitals dominated with 63.60% revenue share in 2025, whereas specialty clinics record the highest 4.28% CAGR to 2031.

- By geography, North America captured 42.05% revenue in 2025; Asia Pacific registers the quickest 6.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Amyotrophic Lateral Sclerosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Incidence And Prevalence Of ALS | +1.20% | Global, with higher impact in aging populations of North America & Europe | Long term (≥ 4 years) |

| Regulatory Tailwinds For Orphan / Rare-Disease Drugs | +0.80% | North America & EU leading, expanding to APAC | Medium term (2-4 years) |

| Breakthroughs In Gene And Antisense-Oligonucleotide Therapies | +0.60% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| AI-Driven Drug-Repurposing Accelerating Pipeline Diversity | +0.50% | North America & EU core, expanding globally | Long term (≥ 4 years) |

| Right-To-Try And Expanded-Access Laws Boosting Early Uptake | +0.40% | North America leading, selective EU adoption | Short term (≤ 2 years) |

| Adoption Of Digital Biomarkers And Remote Patient Monitoring | +0.30% | Global, with faster adoption in digitally mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence and Prevalence of ALS

Epidemiologic studies record rising ALS incidence, especially in aging Western populations, where enhanced neurodiagnostic tools have trimmed diagnostic delay from 16 months to under 12 months.[1]American Journal of Managed Care, “Improved ALS Diagnostic Timelines,” ajmc.comEarlier detection widens the therapeutic window for ASOs that show greatest efficacy in presymptomatic carriers, thereby boosting unit demand and supporting premium pricing. Emerging economies post parallel prevalence gains as specialist neurologists and genetic testing become more available. The demographic surge combines with precision medicine momentum to reinforce sustained volume growth in the Amyotrophic lateral sclerosis treatment market.

Regulatory Tailwinds for Orphan / Rare-Disease Drugs

The FDA’s accelerated approval of tofersen on biomarker endpoints and the EMA’s 2024 endorsement under exceptional-circumstances status underscored a transatlantic realignment toward expedited, evidence-adaptive reviews.[2]Food and Drug Administration, “FDA Grants Accelerated Approval to Tofersen for ALS,” fda.gov Parallel incentives such as fee waivers, priority vouchers, and extended exclusivity, among others, attract venture financing and shorten average development timelines by 3–5 years. Health technology agencies are increasingly receptive to surrogate endpoints, easing reimbursement hurdles for validated biomarker-directed products.

Breakthroughs in Gene and Antisense-Oligonucleotide Therapies

Landmark phase 3 read-outs showed a 55% drop in neurofilament light chain with SOD1-targeted ASO, confirming biomarker-driven disease modification. Platform modularity now speeds mutation-specific candidates for FUS-ALS and C9orf72-ALS, fostering a robust pipeline. Production yields for synthetic oligonucleotides improved 40% since 2023, shrinking cost of goods and enabling broader geographic launches. Intrathecal infrastructure created for early ASOs benefits future gene therapies directed at other neurodegenerative disorders.

AI-Driven Drug-Repurposing Accelerating Pipeline Diversity

Machine-learning engines that interrogate multi-omics and phenotypic datasets have surfaced repurposing leads like FB1006, which advanced from computational hit to first-in-human dosing within 18 months. Computational optimization slashes early-stage R&D spend by up to 70% and diversifies the candidate pool to include combination regimens targeting inflammation, mitochondrial dysfunction, and synaptic failure. The result is a more resilient pipeline that limits single-asset attrition risk and supports long-term CAGR acceleration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs And Limited Reimbursement | -0.90% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Limited Efficacy Of Current Disease-Modifying Drugs | -0.70% | Global, affecting all therapeutic classes | Long term (≥ 4 years) |

| Biologics / Autologous-Cell CMC Capacity Bottlenecks | -0.50% | Global, with severe constraints in specialized manufacturing | Short term (≤ 2 years) |

| Emerging Safety Signals For Long-Term Edaravone Use | -0.40% | Global, with regulatory scrutiny intensifying | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Limited Reimbursement

Annual therapy costs for approved ASOs exceed USD 450,000, and real-world analyses show out-of-pocket spending topping USD 36,000 when supplemental coverage is absent.[3]American Journal of Managed Care, “Improved ALS Diagnostic Timelines,” ajmc.com European payers apply stringent cost-effectiveness thresholds, delaying launches by one to two reimbursement cycles. In middle-income countries, list prices surpass per-capita income, severely curtailing uptake. These affordability gaps temper overall revenue growth despite robust clinical demand.

Limited Efficacy of Current Disease-Modifying Drugs

Legacy standards, riluzole and edaravone, provide only modest survival extensions of 2–3 months and functional benefits that vary widely across genotypes. Recent phase 3 setbacks, including reldesemtiv’s miss on primary endpoints, reinforce clinician caution and can dampen first-line uptake of new entrants absent compelling evidence. Consequently, prescribers prioritize multidisciplinary care and supportive interventions unless apparent patient-level efficacy is demonstrated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Gene Therapy Disruption Gains Pace

Medication retained 66.50% revenue leadership in 2025, reflecting entrenched prescribing patterns and widespread availability. Gene & ASO therapies, however, are advancing at a 6.55% CAGR that will narrow the gap through 2031. The Amyotrophic lateral sclerosis treatment market size for gene-based modalities is forecast to rise as hospital formulary committees increasingly endorse intrathecal ASO protocols following consistent biomarker correlation with slowed clinical decline. Capacity bottlenecks in autologous cell manufacturing persist, yet gene-editing platforms avoid many of these constraints, accelerating commercial scale-up.

Stem cell therapy occupies a high-touch niche anchored by South Korea’s Neuronata-R approval, while BrainStorm’s NurOwn pursues an FDA special protocol. Their progress reinforces sustained investment even as manufacturing scale limitations cap near-term volumes. Oral medications remain the mainstay for symptom control, but payer focus is migrating toward high-value therapies that demonstrably alter disease trajectory, sharpening competitive dynamics across all categories.

By Drug Class: ASOs Challenge Riluzole Dominance

Riluzole’s 37.40% share benefits from generic penetration and favorable neurologist familiarity, yet ASOs are growing 5.45% annually through 2031 as genetic testing becomes routine at diagnosis. The Amyotrophic lateral sclerosis treatment market share for riluzole is projected to erode once additional mutation-specific ASOs transition from the pipeline to the bedside. Edaravone retains intravenous share but faces safety surveillance over long-term hepatic events, prompting some payers to restrict the duration of therapy. Combination products integrating neuroprotection and anti-inflammatory action are progressing in late-phase trials, signaling a future market composed of multimodal regimens rather than single-agent therapies.

By Route of Administration: Intrathecal Uptake Accelerates

Oral therapies represented 47.60% of 2025 revenues, driven by convenience and established reimbursement coding. Intrathecal delivery is the fastest-rising route at 5.62% CAGR, supported by hospital investments in fluoroscopy suites and trained specialist nurses. The Amyotrophic lateral sclerosis treatment market size allocated to intrathecal products will climb notably as next-generation ASOs and gene vectors demand direct cerebrospinal access for optimal bioavailability. Intravenous administration maintains a sizeable share via edaravone infusions, while subcutaneous options are in early development to balance efficacy with outpatient practicality.

By End-user: Specialty Clinics Drive Multidisciplinary Care

Hospitals controlled 63.60% of sales in 2025 because complex dosing and monitoring requirements align with inpatient settings. Nonetheless, specialty ALS clinics are expanding 4.28% annually, owing to evidence that coordinated team care extends survival by nearly 300 days and cuts hospitalizations in half. As payers gravitate toward value-based contracts, multidisciplinary centers gain leverage in negotiating formulary inclusion of high-cost ASOs. Home-based care adoption grows through tele-neurology platforms, yet invasive delivery techniques keep the highest-value prescriptions anchored to specialist sites.

By Distribution Channel: Digital Health Boosts Online Dispensing

Hospital pharmacies oversaw 56.90% market share in 2025, but online channels are expanding at a 6.06% CAGR as chronic patients seek doorstep delivery and synchronized refills. Specialty digital pharmacies integrate teleconsultation, prior-authorization support, and adherence analytics, meeting payer requirements for high-touch oversight of expensive biologics. Retail chains remain relevant for generic riluzole refills but see diminished share as therapy complexity climbs.

Geography Analysis

North America held 42.05% of global revenue in 2025, propelled by immediate Medicare eligibility for ALS patients and early FDA approvals that grant first access to innovative treatments. Legislation such as the ACT for ALS program finances expanded clinical-trial infrastructure, and right-to-try provisions accelerate compassionate-use uptake. Despite comprehensive insurance, coverage caps and variable state supplemental policies expose income-linked disparities in therapy access, especially for ASOs priced beyond USD 400,000.

Europe follows with mature reimbursement networks and the EMA’s coordinated authorization pathway that endorsed the first ASO in 2024. Although pan-EU marketing approval is centralized, country-specific health technology appraisals produce launch stagger delays of 6–12 months. Germany’s AMNOG framework and the United Kingdom’s NICE evaluations often impose early price-volume agreements that shape commercial forecasts. Research consortia anchored in Germany, France, and the United Kingdom underpin a robust clinical-trial ecosystem that draws foreign sponsors.

Asia Pacific posts the highest 6.98% CAGR through 2031 as large unmet need intersects with rapid neurology-center expansion. Japan leads commercial uptake, leveraging prior edaravone familiarity and government funding for neurodegeneration R&D. South Korea’s regulatory head start on stem cell therapy positions the country as a manufacturing exporter for regional demand. China’s volume opportunity is vast, but provincial reimbursement heterogeneity and lengthy drug-price negotiations delay full monetization. Australia, Singapore, and India are emerging nodes in multinational trial networks, offering enrollment scale and cost efficiencies.

Competitive Landscape

Market concentration is moderate, with the top five companies controlling roughly 45% of 2024 sales. Biogen and Ionis Pharmaceuticals co-lead the ASO field by virtue of validated clinical data and proprietary chemistry platforms. Mitsubishi Tanabe secures intravenous share via edaravone, while Eisai maintains a domestic Japanese foothold with oral riluzole and adjunct pipeline assets. Strategic alliances dominate growth strategy: Eli Lilly’s USD 45 million acquisition of QurAlis’s UNC13A program in 2024 exemplifies big-pharma sourcing of de-risked assets.

Technology adoption centers on companion diagnostics and remote monitoring. Device companies supplying intrathecal delivery systems have formed cross-licensing pacts with gene-therapy developers, creating vertically integrated care packages that streamline hospital purchasing decisions. AI-driven startups leverage cloud-based discovery platforms to identify multitarget small molecules, lowering entry barriers and fostering a pipeline of challengers whose cost structures undercut heritage players.

Manufacturing capability remains a competitive divider. Firms with in-house oligonucleotide lines meet scale requirements faster than those reliant on contract partners, safeguarding launch timelines. Conversely, autologous cell-therapy developers must secure additional viral-vector capacity or risk supply disruptions that impede commercial roll-out. In response, several incumbents announced 2025-to-2026 capital plans for cGMP suites that will roughly double global ASO output.

Global Amyotrophic Lateral Sclerosis Treatment Industry Leaders

Mitsubishi Tanabe Pharma Corporation

CORESTEM, Inc

BrainStorm Cell Limited

Amylyx Pharmaceuticals Inc.

Biogen

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: QurAlis advanced the ANQUR study of QRL-201 into dose range-finding, marking steady progress toward a mutation-specific ASO for ALS.

- January 2025: Neuvivo published data indicating NP001 immunotherapy prolonged survival by up to 17 months and preserved lung function, followed by an FDA New Drug Application submission.

- December 2024: MediciNova received positive FDA feedback to begin a Phase III trial of MN-166 (ibudilast) targeting neuroinflammation in ALS.

- October 2024: Neuvivo filed an FDA NDA for NP001 after obtaining Orphan-Drug and Fast-Track status.

Global Amyotrophic Lateral Sclerosis Treatment Market Report Scope

As per the scope of the report, amyotrophic lateral sclerosis (ALS) is a neurological disorder and fatal disease that affects nerve cells in the neuron and spinal control which controls voluntary muscle movement in the human body. This disorder affects neurons which results in the blockage of messages between muscles and the brain. The amyotrophic lateral sclerosis treatment market is segmented by treatment type, end-user, and geography. By treatment type, the market is segmented into medication, stem cell therapy, and other treatment types. The others segment is further bifurcated into respiratory therapy and chemotherapy. By end-user the market is segmented into hospitals, diagnostic centers, and other end-users. The others segment is further bifurcated into research and academic institutes and homecare settings. The report also covers the market size and forecasts for the amyotrophic lateral sclerosis treatment market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Medication |

| Stem Cell Therapy |

| Gene / ASO Therapy |

| Others |

| Riluzole |

| Edaravone |

| Antisense Oligonucleotides |

| Combination / Multi-target |

| Symptomatic Modifiers |

| Oral |

| Intravenous |

| Intrathecal |

| Sub-cutaneous |

| Hospitals |

| Specialty Clinics / ALS Centers |

| Home-care Settings |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Medication | |

| Stem Cell Therapy | ||

| Gene / ASO Therapy | ||

| Others | ||

| By Drug Class | Riluzole | |

| Edaravone | ||

| Antisense Oligonucleotides | ||

| Combination / Multi-target | ||

| Symptomatic Modifiers | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Intrathecal | ||

| Sub-cutaneous | ||

| By End-user | Hospitals | |

| Specialty Clinics / ALS Centers | ||

| Home-care Settings | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Global Amyotrophic Lateral Sclerosis Treatment Market?

The Global Amyotrophic Lateral Sclerosis Treatment Market size is expected to reach USD 952.74 million in 2026 and grow at a CAGR of 5.86% to reach USD 1.27 billion by 2031.

What is the current Global Amyotrophic Lateral Sclerosis Treatment Market size?

In 2026, the Global Amyotrophic Lateral Sclerosis Treatment Market size is expected to reach USD 952.74 million.

Who are the key players in Global Amyotrophic Lateral Sclerosis Treatment Market?

Mitsubishi Tanabe Pharma Corporation, CORESTEM, Inc, BrainStorm Cell Limited, Amylyx Pharmaceuticals Inc. and Biogen are the major companies operating in the Global Amyotrophic Lateral Sclerosis Treatment Market.

Which is the fastest growing region in Global Amyotrophic Lateral Sclerosis Treatment Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Amyotrophic Lateral Sclerosis Treatment Market?

In 2025, the North America accounts for the largest market share in Global Amyotrophic Lateral Sclerosis Treatment Market.

What years does this Global Amyotrophic Lateral Sclerosis Treatment Market cover, and what was the market size in 2025?

In 2025, the Global Amyotrophic Lateral Sclerosis Treatment Market size was estimated at USD 0.95 billion. The report covers the Global Amyotrophic Lateral Sclerosis Treatment Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Amyotrophic Lateral Sclerosis Treatment Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: