Graves Disease Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Graves Disease Market Analysis by Mordor Intelligence

The Graves’ disease market size was valued at USD 2.15 billion in 2025 and estimated to grow from USD 2.26 billion in 2026 to reach USD 2.87 billion by 2031, at a CAGR of 4.92% during the forecast period (2026-2031). The pivot away from symptom-focused antithyroid drugs toward precision immunotherapies keeps demand high while attracting fresh capital, clinical talent, and regulatory attention. Women under 40 remain the largest single patient group, yet the rise in pediatric cases since the COVID-19 pandemic broadens the addressable population. FcRn and IGF-1R biologics are setting new efficacy benchmarks, pulling share from radioactive iodine in cardiovascular-risk patients and reshaping hospital formularies. Supply chain fragility for I-131 isotopes, combined with payer willingness to reimburse high-priced disease-modifying biologics, nudges providers toward treatments that hold greater long-term value for patients and health systems. Overall, the Graves’ disease market is progressing toward a precision-medicine standard in which biomarker-guided care, targeted immunomodulation, and remote monitoring converge to improve outcomes and cut lifetime costs.

Key Report Takeaways

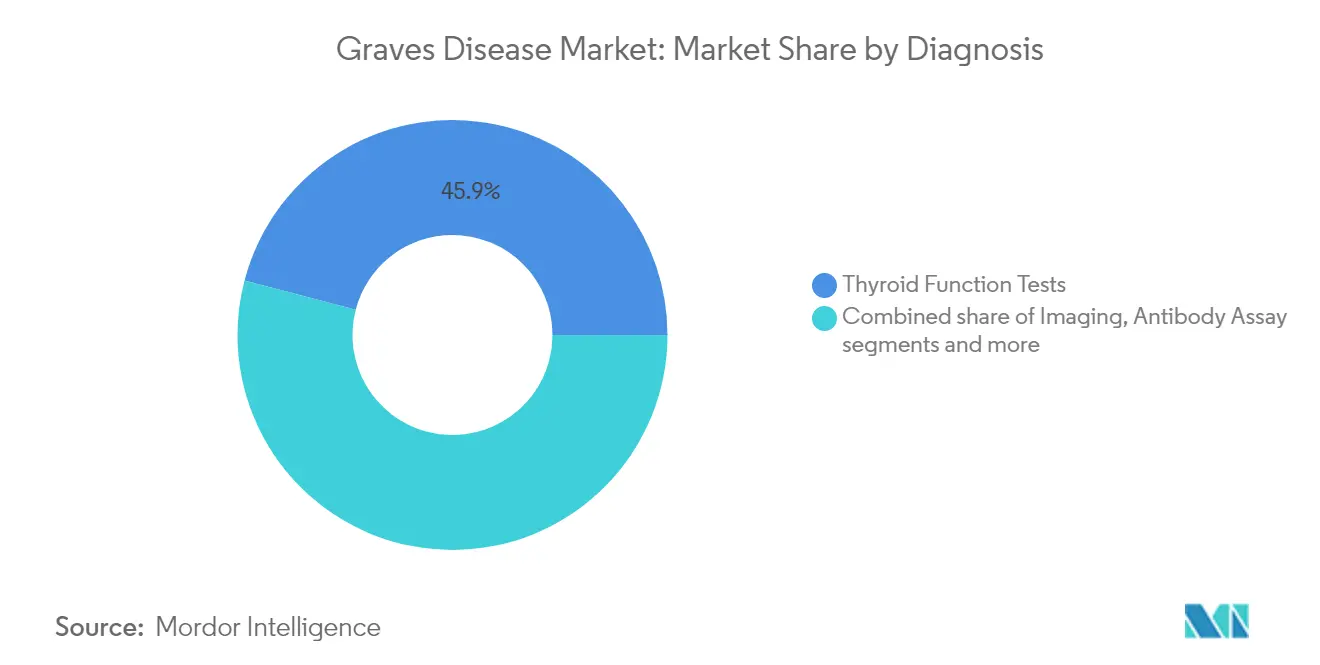

- By diagnosis, TSH testing led with 45.92% revenue share in 2025; antibody assays are projected to expand at a 6.15% CAGR through 2031.

- By treatment, anti-thyroid medications held 40.78% of the Graves’ disease market share in 2025, while targeted immunotherapies and biologics are tracking a 6.02% CAGR to 2031.

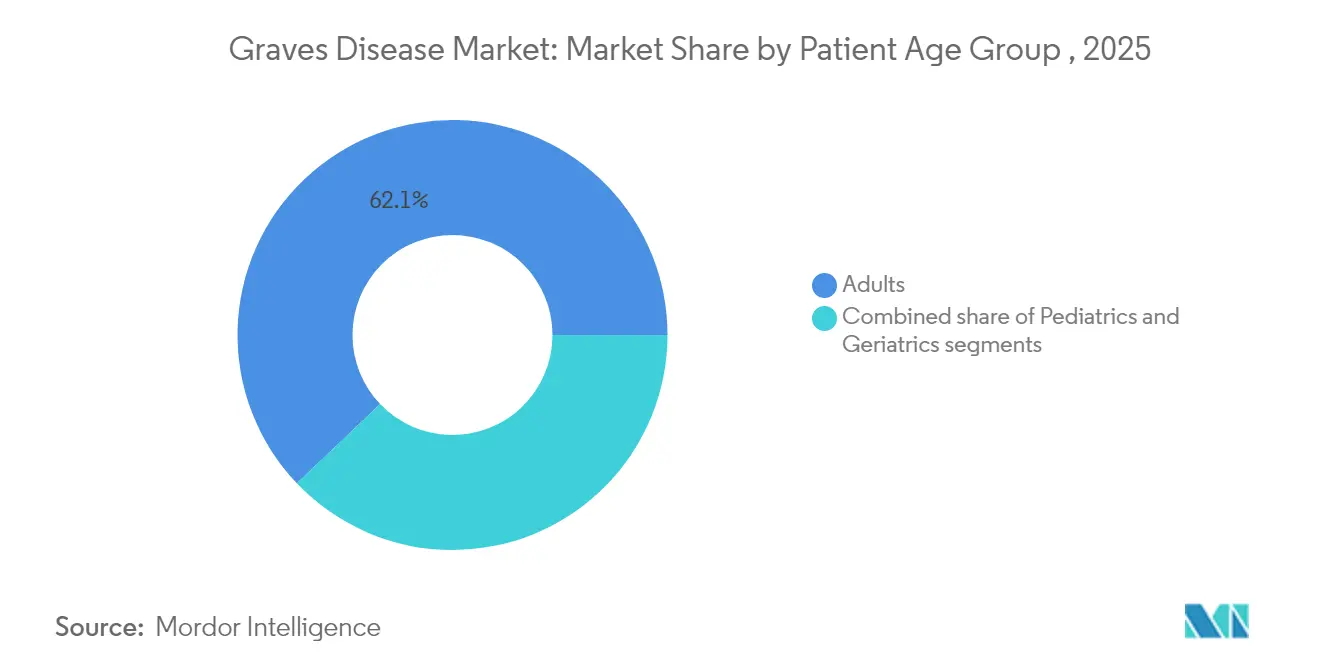

- By patient age group, adults (18-64 years) represented 62.12% share of the Graves’ disease market size in 2025; pediatric cases are poised for a 6.21% CAGR to 2031.

- By end-user, hospitals commanded 51.76% share of the Graves’ disease market size in 2025, while online and retail pharmacies show the fastest growth at 6.44% CAGR.

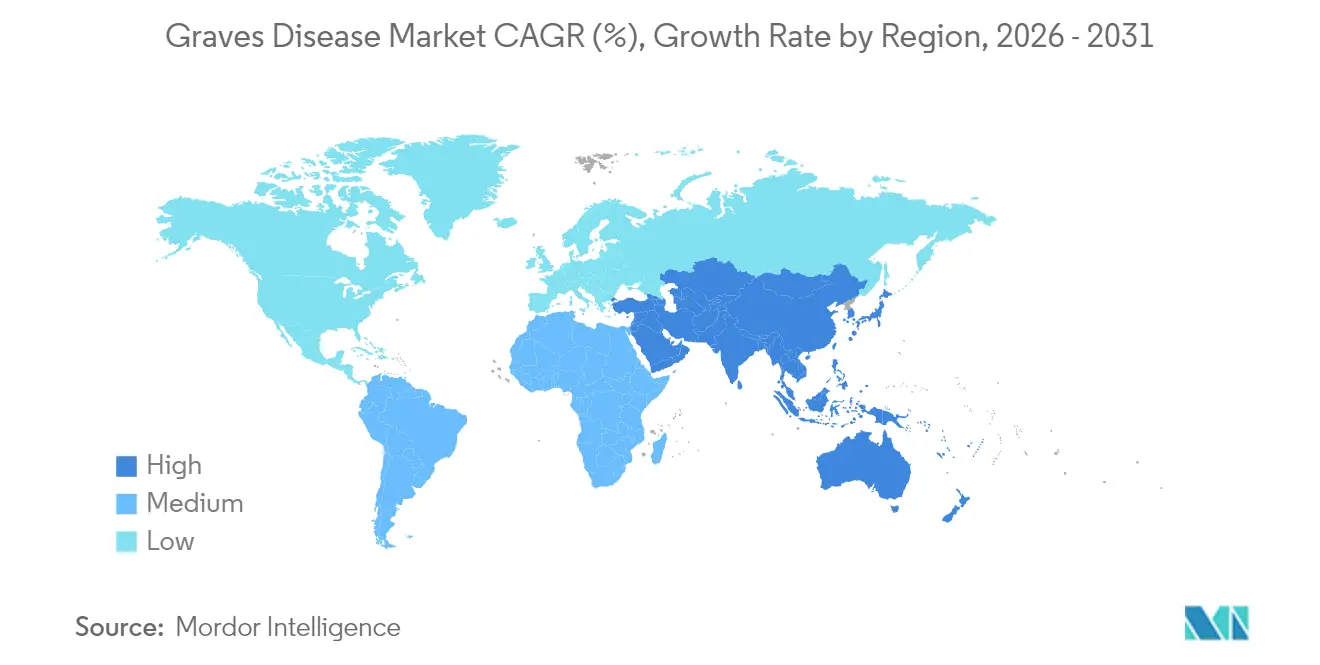

- By geography, North America led with 39.42% share in 2025; Asia Pacific is forecast to be the fastest-growing region at 5.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Graves Disease Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of hyperthyroidism & Graves' disease | +1.2% | Global, with higher impact in Asia Pacific and North America | Medium term (2-4 years) |

| Pipeline of targeted immunotherapies (FcRn & CD40 antagonists) | +1.1% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Growing adoption of radio-iodine therapy in high-CV-risk patients | +0.8% | North America & Europe, expanding to Asia Pacific | Short term (≤ 2 years) |

| Expanding reimbursement & funding for rare autoimmune disorders | +0.9% | North America & EU core, gradual expansion to emerging markets | Long term (≥ 4 years) |

| Rapid uptake of ultrasound-guided thermal ablation techniques | +0.7% | Asia Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Advances in high-resolution, fusion-guided thyroid imaging | +0.6% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hyperthyroidism & Graves’ Disease

The Graves’ disease market continues to expand as incidence climbs in both developed and emerging economies. During the pandemic period, pediatric cases rose 60%[1]N Pollack-Schreiber, “Increased incidence of Graves’ disease during the COVID-19 pandemic in children and adolescents in the United States,” Frontiers in Endocrinology, frontiersin.org, underscoring the role of viral triggers in autoimmune thyroid dysfunction. Higher diagnostic penetration in iodine-replete regions uncovers previously missed subclinical disease, particularly among Asian and White populations with strong genetic predisposition. Pharmaceutical developers leverage these epidemiological insights to refine inclusion criteria, improve trial enrollment, and boost the likelihood of regulatory success. Health systems respond by scaling endocrinology tele-consultation services that lower specialist bottlenecks and enhance early intervention rates. As lifestyle and nutritional transitions continue, incidence growth remains a key demand driver across every tier of care delivery.

Pipeline of Targeted Immunotherapies

Novel FcRn inhibitors and CD40 antagonists reinforce the innovation narrative that positions the Graves’ disease market for sustained premium pricing. Batoclimab posted a 76% response rate in patients uncontrolled on antithyroid drugs, with more than half discontinuing conventional therapy entirely. Clinical differentiation reduces the need for lifelong thyroid replacement and mitigates relapse risk, shifting payer calculus toward disease-modifying solutions. Breakthrough Therapy and orphan drug designations shorten development timelines, encouraging venture investment and licensing deals. As multi-indication platforms emerge, developers exploit scale economies in manufacturing and distribution that further strengthen long-run margins.

Growing Adoption of Radio-Iodine Therapy in High-CV-Risk Patients

Radioactive iodine retains clinical relevance where rapid thyroid ablation lowers atrial fibrillation burden in cardiovascular-risk cohorts. Updated cardiology guidelines support earlier I-131 use, particularly in elderly patients for whom surgery is less feasible. Lithium carbonate co-administration now boosts cure rates by 12%[2]Abd-ElGawad "Determining the best dose of lithium carbonate as adjuvant therapy to radioactive iodine for the treatment of hyperthyroidism: a systematic review and meta-analysis" BMC Endocr Disord, bmcendocrdisord.biomedcentral.com, improving confidence in remission durability. Personalized dosimetry cuts hospital stays, while remote radiation monitors ease outpatient management. These advances preserve a stable revenue base even as biologics gain popularity, reinforcing multimodal treatment diversity within the broader Graves’ Disease market.

Expanding Reimbursement & Funding for Rare Autoimmune Disorders

Payers steadily broaden coverage criteria for high-cost biologics when evidence shows avoidance of surgery and long-term steroid complications. Aetna now pre-authorizes teprotumumab for adults with thyroid eye disease, creating a benchmark for private insurers. Medicare Advantage plans align by standardizing reimbursement for thyroid surgeries that meet defined necessity thresholds. Manufacturers backfill residual gaps through patient-assistance programs that drive early uptake, generate real-world evidence, and strengthen future reimbursement negotiations. Over the forecast horizon, these policies push the Graves’ disease market toward higher biologic penetration and more predictable revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of lifelong disease management | -0.9% | Global, with higher impact in emerging markets | Long term (≥ 4 years) |

| I-131 isotope supply chain and disposal constraints | -0.8% | Global, with acute impact in regions dependent on aging reactors | Short term (≤ 2 years) |

| Relapse & adverse-event profile of anti-thyroid drugs | -0.6% | Global, particularly in pediatric populations | Medium term (2-4 years) |

| Regulatory uncertainty around first-in-class biologics | -0.5% | North America & Europe, affecting global pipeline | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Lifelong Disease Management

The Graves’ disease market absorbs significant cost pressure when biologic courses exceed USD 380,000, and annual levothyroxine prescriptions top 82 million in the United States. Indirect expenses from monitoring, lost productivity, and comorbidity management add to the burden, especially in low-resource settings where insurance penetration is limited. Currency volatility inflates import costs for active pharmaceutical ingredients, threatening generic supply security. These economic frictions drive value-based-care pilots that link payment to long-term outcomes and stimulate demand for solutions that shorten or eliminate chronic medication use.

I-131 Isotope Supply Chain and Disposal Constraints

Fragile isotope supply constrains radioactive iodine therapy expansion. Aging reactors in Europe and previous shutdowns at Canada’s Chalk River facility expose geographic dependency risks. New American projects require years to come online, while stricter waste-disposal rules raise hospital handling costs. Providers hedge by incorporating thermal ablation or biologic alternatives into treatment algorithms, a trend that redirects share toward less supply-sensitive modalities across the Graves’ disease market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diagnosis: Precision Biomarkers Redefine Clinical Decisions

TSH testing retained 45.92% revenue share in 2025, underscoring its status as the primary screening and monitoring tool. Nevertheless, antibody assays are expanding at a 6.15% CAGR as clinicians correlate thyroid-stimulating immunoglobulin (TSI) titers with disease activity and treatment response. The Graves’ disease market accommodates both modalities, yet rapid-turnaround antibody panels increasingly guide personalized treatment strategies. Free T4 and T3 measurements remain indispensable for dose titration, while thyroglobulin tests monitor post-surgical recurrence. Vitamin D status testing is gaining ground after studies linked serum levels of 20-29 ng/mL to better TRAb remission rates.

A growing installed base of point-of-care platforms moves initial diagnostics closer to primary care, accelerating specialist referrals and expanding the overall Graves’ Disease market. High-resolution ultrasound and fusion imaging add structural insights that drive selection between radioiodine, surgery, or emerging ablation techniques. The Graves’ disease industry benefits from bundled diagnostic-and-therapy offerings that streamline patient journeys and raise provider margins. As reimbursement policies catch up with the clinical value of antibody profiling, labs capable of multiplex testing are poised to capture additional share.

By Treatment: Immunotherapies Challenge Traditional Dominance

Anti-thyroid drugs still control 40.78% revenue in 2025, reflecting easy oral dosing and low acquisition cost. Yet FcRn inhibitors and IGF-1R antagonists are set to generate the fastest 6.02% CAGR through 2031, rewriting the value hierarchy of the Graves’ disease market. Batoclimab’s 76% response rate in refractory patients illustrates the step-change in efficacy. Radioactive iodine therapy persists, favored for elderly cardiovascular-risk cohorts, while supply uncertainty limits aggressive expansion plans.

Thermal ablation offers a minimally invasive bridge option, achieving 96% one-year euthyroid status with minimal complications. Surgical thyroidectomy remains the definitive approach for large goiters, malignancy suspicion, or treatment failure, with updated nerve-monitoring protocols reducing complication rates. Overall, diversified modality availability protects patient choice, though the revenue mix skews increasingly toward biologics as payers embrace long-term cost avoidance.

By Patient Age Group: Pediatric Surge Drives Innovation

Adults aged 18-64 accounted for 62.12% of the Graves’ disease market share in 2025, reflecting peak disease onset years. This cohort benefits from the broadest trial access and drives data generation that shapes global guidelines. Pediatric cases, growing at 6.21% CAGR, introduce distinct needs around growth, development, and medication adherence. Lower remission rates and higher symptom severity push clinicians to explore immunotherapies and tailored dosing regimens for children . Neonatal thyrotoxicosis cases underscore the need for maternal antibody screening, influencing obstetric protocols.

Geriatric patients often favor radioiodine due to comorbidity concerns, while novel biologics may reduce polypharmacy and improve quality of life. The Graves’ disease market therefore spans three age-defined sub-segments, each requiring unique safety data, formulation options, and support programs. Such complexity fuels investment in age-stratified research and opens secondary opportunities in caregiver support services.

By End-User: Digital Transformation Reshapes Distribution

Hospitals captured 51.76% of the Graves’ disease market size in 2025 through integrated diagnostic, surgical, and nuclear medicine capabilities. Multidisciplinary endocrinology boards improve complex-case outcomes and facilitate early enrollment in investigational biologic trials. Specialty clinics leverage telemedicine to maintain frequent contact during dose titration, improving adherence and capturing ancillary lab revenues. Online and retail pharmacies, expanding at 6.44% CAGR, benefit from the oral formulation trend and direct-to-consumer prescription fulfillment models.

Ambulatory surgical centers gain traction for outpatient thermal ablation and minimally invasive thyroidectomy, offering lower overhead and faster scheduling. Digital consultation platforms such as Medii link primary-care physicians to specialists, accelerating referral cycles and raising diagnostic throughput. As therapy delivery decentralizes, manufacturers craft omnichannel distribution strategies to safeguard patient experience and ensure temperature-controlled biologic integrity. The Graves’ disease industry thus illustrates how virtual care and retail pharmacy growth can coexist with traditional hospital dominance.

Geography Analysis

North America maintains leadership with 39.42% revenue share in 2025, supported by advanced infrastructure, deep clinical-trial networks, and payer readiness to cover first-in-class biologics. The region’s 4.38% CAGR through 2031 stems from steady transition to value-based care and widening access to precision diagnostics. United States providers increasingly bundle imaging, antibody panels, and endocrine consultations into integrated care pathways, reducing time to treatment initiation. High private-equity investment in specialty clinics further accelerates patient throughput and data generation for real-world evidence studies.

Asia Pacific is the fastest-growing arena for the Graves’ disease market, rising at 5.98% CAGR. Government health-insurance expansions in China and India drive higher diagnostic uptake, while Japan pioneers outpatient ablation protocols that shorten wait times and lower total cost of care. Domestic biotech investment unlocks localized manufacturing for biosimilar antibodies, boosting affordability. Telemedicine adoption soars in rural provinces, enabling specialists to manage complex cases remotely. Overall, demographic scale, economic growth, and policy reform combine to make Asia Pacific the primary engine of incremental revenue. Europe contributes a balanced 4.59% CAGR, anchored by public healthcare systems that emphasize cost-effectiveness and early technology assessment. Harmonized regulatory frameworks streamline biologic approvals, while well-established thyroid research consortia facilitate multicenter trials. Middle East & Africa achieves a 5.61% CAGR as infrastructure upgrades and rising chronic-disease awareness improve specialist access. Regional centers of excellence in the Gulf export know-how across North Africa, while pharmaceutical manufacturers target tender contracts to secure formulary placements. South America advances at 5.05% CAGR, with Brazil’s universal health system adding antibody testing reimbursement and Argentina incentivizing domestic levothyroxine production to cut import dependence. Collectively, these developments widen the global footprint of the Graves’ disease market and encourage multinational players to localize both manufacturing and medical education programs.

Competitive Landscape

The Graves’ disease market exhibits moderate concentration as legacy endocrine franchises face challenger biologics. Amgen’s USD 27.8 billion acquisition of Horizon Therapeutics underscores the strategic value of rare-disease assets, with Tepezza sales reaching USD 488 million per quarter. Immunovant, Viridian Therapeutics, and Argenx deploy platform technologies that aim to treat multiple autoimmune indications, leveraging economies of scale in development and manufacturing. Traditional players such as Abbott and Novartis protect share through broad hormone-replacement portfolios and diagnostic integration but must now adjust commercial models to compete with targeted immunotherapies.

Strategic alliances proliferate as companies spread risk and access complementary capabilities. Bristol Myers Squibb teamed with Repertoire Immune Medicines in a USD 1.8 billion deal to develop tolerizing vaccines. Novartis acquired Calypso Biotech for IL-15 modulators, while Pfizer joined Flagship Pioneering to access next-generation autoimmune discovery engines. Delivery-technology differentiation has become critical: Argenx extended its Halozyme partnership, securing subcutaneous Enhanze technology to improve patient convenience and extend patent life. Competitive intensity spurs investment in patient-support programs and digital adherence tools, raising the service bar for new entrants.

Supply-chain resilience and manufacturing scale play growing roles in competitive positioning. Companies able to guarantee biologic supply during I-131 shortages gain prescribing preference. Meanwhile, real-world outcomes registries enable manufacturers to negotiate outcomes-based contracts that align price with long-term disease-control metrics. Across these dynamics, the Graves’ disease market rewards innovation, platform breadth, and customer-centric delivery models that de-risk the choice for physicians and payers alike.

Graves Disease Industry Leaders

-

Abbott Laboratories

-

F. Hoffmann-La Roche AG

-

Horizon Therapeutics plc

-

Immunovant Inc.

-

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Viridian Therapeutics received FDA Breakthrough Therapy Designation for veligrotug (VRDN-001) for treating thyroid eye disease, accelerating regulatory review timelines and validating the IGF-1R antagonist approach for autoimmune complications of Graves' disease. This designation positions veligrotug for potential commercial launch in 2026 following BLA submission in late 2025.

- April 2025: Merida Biosciences, a biotechnology firm developing precision therapeutics, secured USD 121 million in Series A financing. The company is focusing on programs for Graves’ disease, allergies, and primary membranous nephropathy, a chronic autoimmune kidney disease.

- December 2024: Viridian Therapeutics announced positive topline results from THRIVE-2 Phase 3 trial of veligrotug in chronic thyroid eye disease, achieving 56% proptosis responder rate and 56% diplopia response rate, with 94% patient completion demonstrating strong tolerability profile.

- September 2024: Immunovant provided development updates reporting 60% response rate in Graves' disease patients treated with batoclimab, with plans to initiate potentially registrational trial for IMVT-1402 by end of 2024, addressing unmet needs for patients uncontrolled on antithyroid drugs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the Graves Disease market as the worldwide spend on diagnostic tests (TSH, TRAb, imaging), therapeutic products (antithyroid drugs, radioactive iodine, thyroidectomy kits, emerging biologics such as IGF-1R and FcRn antibodies), and associated hospital services required to manage the autoimmune hyperthyroid condition in all age groups.

Scope exclusion: purely cosmetic ophthalmic procedures for Graves orbitopathy and general thyroid function test panels ordered for unrelated disorders are not counted.

Segmentation Overview

-

By Treatment

- Anti-Thyroid Medication

- Radioactive Iodine Therapy

- Surgery (Thyroidectomy)

- Targeted Immunotherapies & Biologics

- Ultrasound-Guided Thermal Ablation

-

By Patient Age Group

- Pediatrics

- Adults

- Geriatrics

-

By End-User

- Hospitals

- Specialty Clinics & Endocrinology Centers

- Ambulatory Surgical Centers

- Retail & Online Pharmacies

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Endocrinologists, nuclear-medicine pharmacists, payor medical directors, and supply-chain managers across North America, Europe, Asia-Pacific, and key emerging economies were interviewed. Their insights refined prevalence splits, biologic adoption curves, typical course-of-therapy costs, and the practical lag between diagnosis and definitive treatment that pure desk research cannot capture.

Desk Research

We gathered foundational volumes and prices from public datasets issued by bodies such as the World Health Organization, the American Thyroid Association, Eurostat's hospital cost files, and national nuclear-medicine registries that track I-131 shipments. Clinical incidence trends were cross-checked in peer-reviewed journals like The Lancet Diabetes & Endocrinology and the Journal of Clinical Endocrinology & Metabolism. Company revenue splits came from 10-K filings and D&B Hoovers, while Dow Jones Factiva provided real-time pipeline updates that flag market-moving events. These sources illustrate, not exhaust, the wider information pool tapped by our analysts.

Our desk work also consulted trade association briefs (Endocrine Society, Asia Oceania Thyroid Association) and customs flow data that highlight regional isotope availability, helping us judge therapy uptake swings before the new forecast was locked.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid model was applied. Starting with country-level hyperthyroidism prevalence, we derived Graves Disease shares and multiplied them by treated-patient ratios, average annual therapy cost, and follow-up test frequencies. Supplier roll-ups of antithyroid tablets, biologic vials, and radioiodine doses then validated totals. Key variables include pediatric incidence growth, biologic price erosion pace, isotope production outages, insurance coverage expansion, and guideline updates that shorten treatment durations. Multivariate regression, informed by the most sensitive of these drivers, projects values through 2030, while scenario checks bracket uncertainties in biologic penetration.

Data Validation & Update Cycle

Our outputs undergo variance checks against independent usage surveys and hospital billing indices. Senior reviewers challenge anomalies, and material events trigger interim refreshes. Reports are fully revisited every twelve months, and a last-minute sweep is completed before client delivery.

Why Mordor's Graves Disease Baseline Earns Practitioner Trust

Published sizes often differ because analysts select distinct product baskets, geographies, and refresh cadences. We acknowledge those gaps upfront so users see where numbers may drift.

Key gap drivers include narrower therapeutic scope, regional focus, or reliance on historical ASPs without verifying biologic launches that Mordor has already baked in. Currency treatment and inflation deflators also vary.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.15 B (2025) | Mordor Intelligence | - |

| USD 430.6 M (2025) | Regional Consultancy A | Leaves out diagnostics and biologics; covers five regions only |

| USD 403.48 M (2024) | Trade Journal B | Counts medication sales only, omits hospital procedural spend |

| USD 641.22 M (2024) | Industry Association C | 7MM geography, ignores spend on radioactive iodine therapy |

These comparisons show that, by aligning scope with real-world care pathways and refreshing data annually, Mordor delivers a balanced, transparent baseline that decision-makers can confidently apply.

Key Questions Answered in the Report

Why are targeted immunotherapies gaining momentum in Graves’ disease treatment?

Targeted immunotherapies such as FcRn and IGF-1R antagonists directly modulate the autoimmune pathways driving the disorder, leading to higher response rates and the possibility of discontinuing conventional antithyroid drugs for many patients.

How is radioactive iodine therapy adapting to cardiovascular-risk considerations?

Clinicians now prefer I-131 for patients with arrhythmias or other heart conditions because it normalizes thyroid hormone levels more rapidly than prolonged drug therapy, thereby lowering cardiac complications.

Clinicians now prefer I-131 for patients with arrhythmias or other heart conditions because it normalizes thyroid hormone levels more rapidly than prolonged drug therapy, thereby lowering cardiac complications.

Tests for TSI and TRAb are increasingly used to gauge disease activity, forecast treatment response, and help physicians decide whether a patient is a candidate for immunotherapy or more traditional options.

Why is the pediatric segment attracting heightened R&D attention?

Children show rising incidence rates, especially post-COVID-19, and often experience more severe symptoms, prompting the search for therapies that balance efficacy with long-term growth and developmental safety.

How are supply chain issues influencing therapy choices?

Intermittent shortages of I-131 isotopes encourage providers to explore non-radioactive alternatives such as thermal ablation and biologics, reshaping the therapeutic mix offered by hospitals and specialty centers.

What digital trends are reshaping medication access for Graves’ disease patients?

Growth in online and retail pharmacies, alongside telemedicine platforms, improves adherence and enables remote dose adjustments, making long-term management more convenient for both patients and clinicians.

Page last updated on: