Brain PET-MRI Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

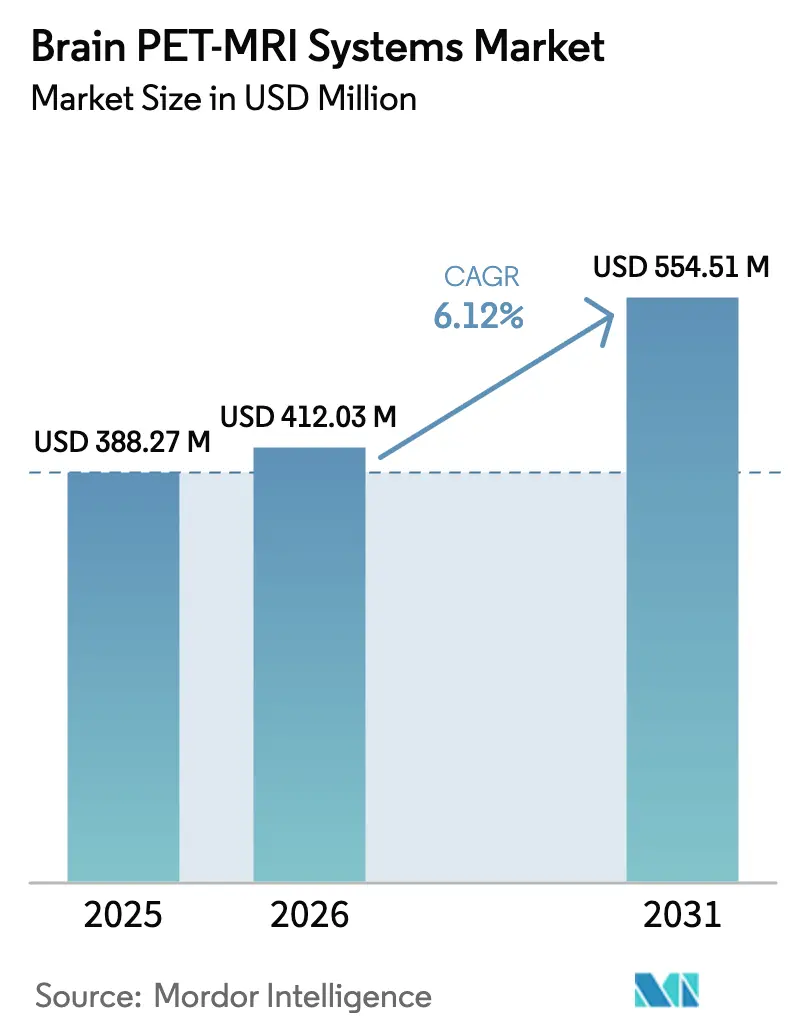

| Market Size (2026) | USD 412.03 Million |

| Market Size (2031) | USD 554.51 Million |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brain PET-MRI Systems Market Analysis by Mordor Intelligence

Brain PET-MRI systems market size in 2026 is estimated at USD 412.03 million, growing from 2025 value of USD 388.27 million with 2031 projections showing USD 554.51 million, growing at 6.12% CAGR over 2026-2031. Growth stems from the convergence of rising neurological disorder prevalence, breakthroughs in hybrid-imaging technology and expanding reimbursement frameworks that lower financial hurdles for advanced neuroimaging. North America remains the revenue anchor, yet Asia-Pacific is advancing fastest as healthcare systems upgrade diagnostic infrastructure and local manufacturers scale production. Traditional PET-MRI platforms continue to dominate installed bases, but helium-free designs are accelerating as providers seek insulation from supply-chain shocks and long-term operating costs. Clinical oncology presently drives scanner utilization, while neurology procedures surge on the back of amyloid-targeted Alzheimer’s therapies. Across regions, hospitals still initiate most purchases, yet outpatient imaging centers are gaining momentum as scan times fall and compact systems arrive.

Key Report Takeaways

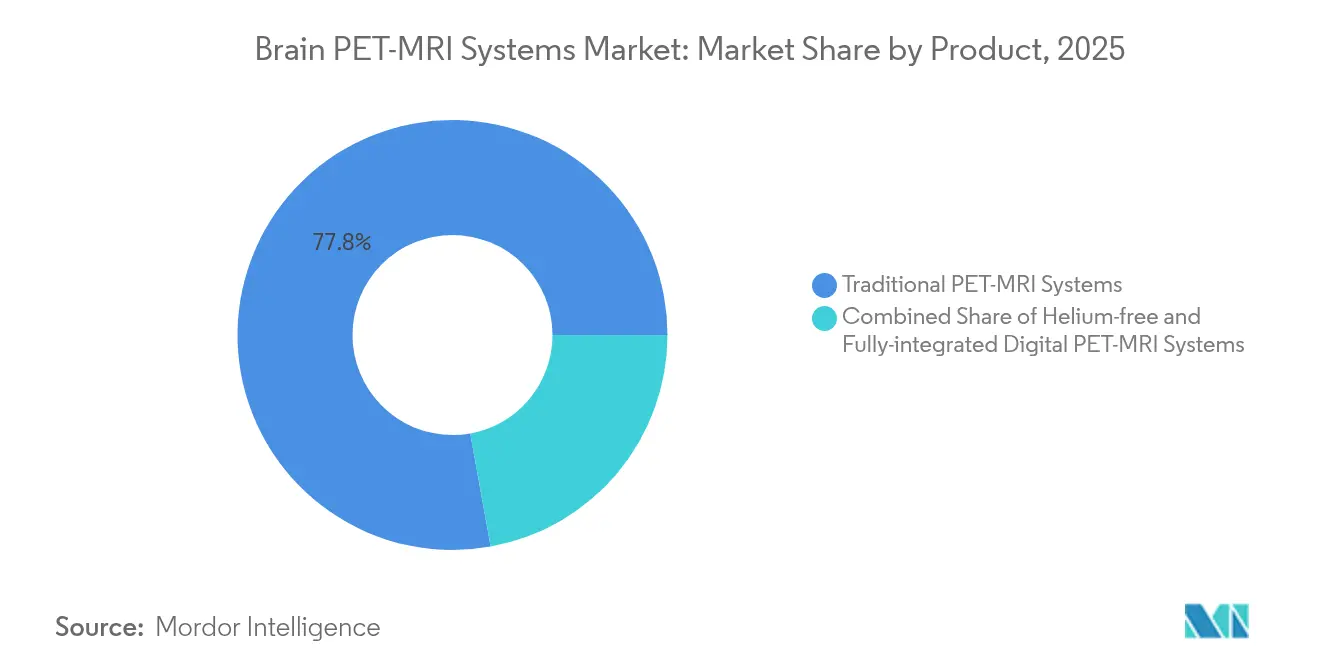

- By product category, traditional PET-MRI systems held 77.84% of the Brain PET-MRI systems market share in 2025; helium-free solutions are projected to expand at a 6.64% CAGR to 2031.

- By phase, clinical applications accounted for 60.74% revenue in 2025, whereas preclinical usage is forecast to climb at a 9.72% CAGR through 2031.

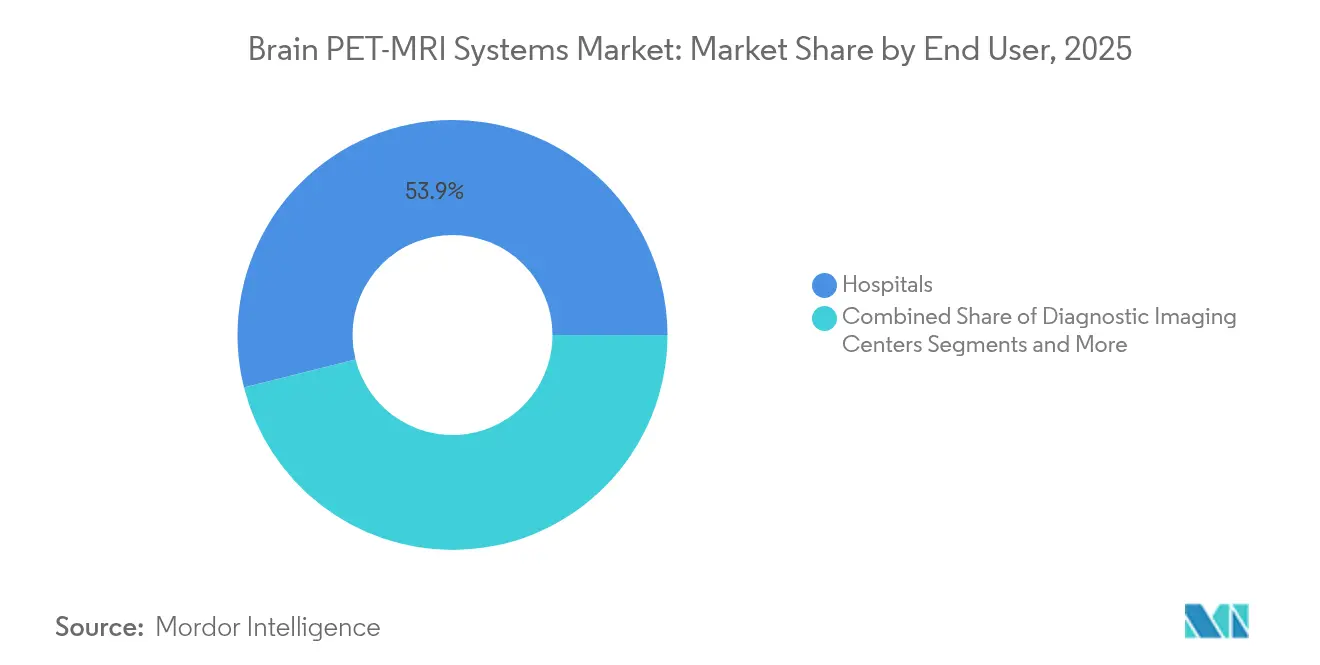

- By end user, hospitals led with 53.92% share of the Brain PET-MRI systems market size in 2025; diagnostic imaging centers are expected to register a 10.08% CAGR to 2031.

- By application, oncology contributed 45.12% revenue in 2025, while neurology procedures are advancing at a 10.02% CAGR through 2031.

- By geography, North America contributed 41.98% revenue in 2025; Asia-Pacific is poised for a 10.31% CAGR, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Brain PET-MRI Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of neurological disorders | +1.8% | Global (high in North America & Europe) | Long term (≥ 4 years) |

| Rapid advancements in hybrid-imaging technology | +1.5% | North America & EU with spill-over to APAC | Medium term (2-4 years) |

| Supportive government funding programs | +1.2% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Growing demand for PET-MRI in neuro-oncology | +1.0% | Global, led by North America | Short term (≤ 2 years) |

| AI-Enabled Quantitative Neuro-Biomarker Integration | +0.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Use In Neuro-Psychiatric Drug-Trial Stratification | +0.6% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Neurological Disorders

Alzheimer’s disease affects 6 million Americans and is projected to reach 13.8 million by 2060, prompting payers and providers to embrace imaging methods that detect amyloid plaques and tau proteins early in the disease course. The European Medicines Agency’s 2024 approval of Lecanemab mandates amyloid confirmation, potentially adding 270,000 amyloid PET exams annually across the EU. Similar momentum is evident in Parkinson’s disease, where specialized PET tracers improve differential diagnosis [1]David Herrero, “Imaging Dopaminergic Pathways in Parkinson’s Disease,” Journal of Nuclear Medicine, snmjournals.org. Combined with longer life expectancy in Asia, these trends expand the Brain PET-MRI systems market by widening the clinical funnel for early-stage detection. Academic medical centers capitalize on this demand by integrating hybrid scanners into dementia clinics and movement-disorder centers.

Rapid Advancements in Hybrid-Imaging Technology

Siemens Healthineers’ Magnetom Flow cuts helium usage from 1,500 L to 0.7 L and halves scan times through AI-assisted reconstruction, reducing ownership costs and throughput constraints. Philips and NVIDIA are co-developing foundation models that automate protocol selection and lesion detection, allowing radiology teams to standardize quality regardless of staffing levels [2]“Philips-NVIDIA AI Collaboration for MRI,” Philips Healthcare Newsroom, philips.com. Research prototypes now attain sub-2 mm PET resolution, opening investigational pathways in micro-metastatic disease and neuro-receptor mapping. Collectively, these innovations differentiate vendors not on magnet strength alone but on workflow intelligence, further fueling Brain PET-MRI systems market adoption among cost-sensitive providers.

Supportive Government Funding Programs

Australia’s Medical Research Future Fund finances FET-PET trials in high-grade glioma, validating hybrid imaging’s impact on surgical planning. Medicare revised national coverage in 2024 to include PET scans for seizure localization and brain-tumor evaluation, lifting utilization caps for U.S. hospitals. Japan’s nationwide medical-image database of 500 million studies underpins AI algorithm training, accelerating regulatory clearance of decision-support tools. Such multilevel incentives lower capital-investment hurdles, expand reimbursement and seed translational research projects, reinforcing long-run Brain PET-MRI systems market expansion.

Growing Demand for PET-MRI in Neuro-Oncology

PET-MRI enables superior lesion-to-brain contrast and functional-metabolic co-registration compared with PET-CT, guiding surgeons when tumors abut eloquent cortex. The [18F]FET tracer allows clinicians to distinguish tumor recurrence from radiation necrosis, a key decision point for high-grade glioma management. AI-driven reconstruction reduces brain-tumor scan time by up to 40%, making outpatient protocols feasible and expanding procedure volume in community cancer centers. As theranostic paradigms merge diagnostic imaging with targeted radiopharmaceuticals, PET-MRI becomes indispensable for both eligibility screening and post-therapy monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Costs | -1.4% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Limited Accessibility In Low-Income Regions | -1.1% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Workflow-Integration & Training Complexity | -0.9% | Global, particularly smaller healthcare facilities | Medium term (2-4 years) |

| Helium Supply-Chain Vulnerability | -0.7% | Global, most severe in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs

Turn-key Brain PET MRI suites can exceed USD 10 million once shielding, cryogenic infrastructure and cyclotron access are included, a hurdle for mid-tier hospitals that compete for limited capital budgets. Helium refill prices have climbed 250% in 10 years, pushing operators toward annual service contracts that exceed those of standalone MRI by 30%. Economic evaluations therefore emphasize throughput; providers must schedule ≥10 patients per day to break even under typical reimbursement schedules. Helium-free magnets and dry-cooling systems promise relief, yet they require peer-reviewed evidence to convince hospital boards accustomed to proven, field-tested technologies.

Workflow-Integration & Training Complexity

Hybrid imaging forces nuclear medicine and radiology departments to synchronize workflow, radiopharmaceutical delivery and scanner availability—a cultural and logistical shift for many institutions. Staff must master dual safety protocols, radio-tracer handling and advanced image fusion interpretation, extending the learning curve. A shortage of hybrid-qualified technologists inflates labor costs and limits after-hours operations. Small hospitals turn to teleradiology for PET-MRI reads, but latency and bandwidth constraints can erode efficiency. Vendors now bundle project-management and education services, yet competency maintenance remains an ongoing expense that stalls Brain PET-MRI systems market penetration in resource-restricted settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Traditional Systems Drive Revenue Despite Helium-Free Innovation

Traditional scanners held 77.84% of the Brain PET-MRI systems market in 2025, underscoring buyer preference for clinically validated platforms with extensive regulatory clearance. The Brain PET-MRI systems market size tied to traditional systems is projected to expand from USD 321.17 million in 2026 to USD 422.28 million in 2031 at a 5.62% CAGR. Hospitals cite multipurpose flexibility and seamless protocol libraries as chief benefits, reinforcing the installed-base lock-in effect.

Helium-free and cryogen-free systems, while accounting for a modest share today, are the fastest-growing category at 6.64% CAGR. Providers value their 97% reduction in helium consumption and 40 MWh annual energy savings, benefits that align with decarbonization mandates. As global helium reserves tighten, the Brain PET-MRI systems market share of helium-free designs is forecast to pass 25% by 2031. Digital detector integration and on-board AI analytics are converging across all form factors, suggesting future competition will pivot on smart-workflow ecosystems rather than pure magnet architecture.

By Phase: Clinical Applications Dominate While Preclinical Research Accelerates

Clinical use generated 60.74% revenue in 2025, propelled by expanded reimbursement, neurologist demand for amyloid confirmation and oncologist reliance on metabolic-anatomical fusion. The Brain PET-MRI systems market size for clinical procedures is expected to rise at a 5.71% CAGR, reflecting rising scan volumes per installed system. Hospitals leverage hybrid imaging to shorten diagnostic odysseys, thereby boosting bed-turnover metrics and attracting tertiary referrals.

Preclinical adoption, though smaller in absolute dollars, is scaling at a 9.72% CAGR as pharmaceutical companies incorporate PET-MRI biomarkers into go-no-go decisions. Bruker’s dDNP signal-amplification platform delivers 10,000-fold metabolic sensitivity, enabling mouse-to-human translation of drug-response signatures. Research institutes deploy compact animal scanners, which cost a third of clinical units and circumvent radiopharmacy complexities, thereby accelerating discovery while nurturing future clinical protocols.

By End User: Hospital Dominance Faces Imaging-Center Challenge

Hospitals commanded 53.92% revenue in 2025 thanks to integrated nuclear medicine departments, on-site radiotracer production and broad payer contracts. The Brain PET-MRI systems market size attributable to hospital sites is projected to reach USD 309.65 million by 2031. Multi-disciplinary teams favor hybrid imaging for surgical planning conferences and tumor boards, embedding PET-MRI into decision pathways.

Diagnostic imaging centers, bolstered by 10.08% CAGR, are reshaping competitive dynamics. Lower construction costs for helium-free consoles enable suburban installations where patient access and scheduling flexibility drive referral capture. Teleradiology networks broaden subspecialty coverage, and mobile radiopharmacy partnerships offset tracer-delivery gaps. Academic institutions, meanwhile, cement their niche via grant-funded translational trials that pioneer protocol optimization.

By Application: Oncology Leadership Yields to Neurology Growth

Oncology remained top with 45.12% revenue in 2025, yet its CAGR of 5.41% trails that of neurology. Surgical teams rely on PET-MRI to delineate glioma margins and differentiate pseudoprogression, supporting precision resections and stereotactic-radiation planning. The Brain PET-MRI systems market share anchored in oncology is forecast to decline marginally as other indications catch up.

Neurology studies, expanding at 10.02% CAGR, will close the gap by 2031. New disease-modifying Alzheimer’s therapies require amyloid verification, while Parkinson’s trials need dopaminergic-receptor imaging for cohort stratification. Emerging protocols in major depressive disorder and epilepsy further enlarge the neurologic canvas. Cardiology and psychiatric imaging remain exploratory but could accelerate once reimbursement pathways crystallize.

Geography Analysis

North America retained 41.98% share in 2025, fueled by Medicare policy expansion, NIH grant pipelines and vendor–academic collaborations such as GE HealthCare’s joint AI projects with UCSF and Stanford Medicine . The Brain PET-MRI systems market size in the region is forecast to surpass USD 233.12 million by 2031. Yet helium-reserve privatization ignites cost-volatility concerns, prompting providers to fast-track helium-free upgrades.

Asia-Pacific is the fastest-growing territory with a 10.31% CAGR. Japan’s national image repository underpins algorithm development, while China’s multi-decade healthcare reform funnels capital toward tertiary neuro centers, albeit with lingering rural-urban gaps. Domestic OEMs now supply gradient coils and RF amplifiers, shortening lead times and lowering price points, further propelling Brain PET-MRI systems market adoption.

Europe exhibits mature uptake; however, the 2024 EU approval of Lecanemab triggers a surge in amyloid scans, enhancing utilization rates. Sustainability policies accelerate adoption of helium-light systems, and cross-border data-sharing aligns protocol standards. South America and the Middle East & Africa are nascent but benefit from public-private diagnostic-center joint ventures that import refurbished scanners and leverage international teleradiology expertise.

Competitive Landscape

The Brain PET-MRI systems market is moderately consolidated, led by Siemens Healthineers, GE HealthCare and Philips, each differentiating via technology roadmaps rather than price. Siemens markets virtually helium-free magnets and eco-designs that slash energy draw by 30%. GE focuses on AIR coil arrays and AI-powered workflow orchestration, underscored by its acquisition of MIM Software to deepen quantitative-image analytics. Philips partners with NVIDIA to embed transformer-based models that automate scan planning and reduce operator variance.

Second-tier players such as Bruker and MR Solutions target research and preclinical niches with ultra-high-resolution detectors. Cubresa’s removable BrainPET insert exemplifies modular add-ons that retrofit into existing MRI suites, a strategy appealing to budget-constrained centers. Vendors increasingly bundle lifetime-software licenses and remote-service diagnostics, creating recurring-revenue streams and deepening customer lock-in.

Strategic alliances characterize recent moves: Siemens collaborates with biotech firms to co-develop tau-imaging tracers, while Philips engages hospital networks in outcome-based contracting where payment aligns to throughput and uptime metrics. The race to on-device AI fosters ecosystem thinking; vendors open software-development kits to third-party algorithm creators, ensuring platform stickiness and data-network effects that reinforce competitive moats.

Brain PET-MRI Systems Industry Leaders

Siemens Healthineers AG

Koninklijke Philips N.V.

GE HealthCare

Bruker

Cubresa Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Philips introduced Smart Quant Neuro 3D, an AI-based quantitative brain-MRI package that streamlines workflow and enhances diagnostic confidence.

- June 2023: GE HealthCare unveiled SIGNA PET/MRI AIR technologies at the Society of Nuclear Medicine and Molecular Imaging annual meeting in Canada.

- May 2023: Cubresa installed its first BrainPET insert system at St. Joseph’s Health Care London in partnership with Lawson Health Research Institute.

Global Brain PET-MRI Systems Market Report Scope

The PET/MRI scan combines positron emission tomography (PET) and magnetic resonance imaging (MRI) into one test. This hybrid technology produces highly detailed images of the body. Doctors use these images to diagnose conditions and plan treatments. These scans help in the diagnosis of Alzheimer's disease, epilepsy, and brain tumors.

The brain PET-MRI systems market is segmented into product, phase, end-user, and geography. By product, the market is segmented into traditional brain PET-MRI systems and Helium-free PET-MRI systems. By phase, the market is segmented into pre-clinical and clinical. By end-user, the market is segmented into hospitals, diagnostic imaging centers and other end users. By geography the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The report also offers the market size and forecasts for 13 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Traditional PET-MRI Systems |

| Helium-free / Cryogen-free Systems |

| Fully-integrated Digital PET-MRI Systems |

| Pre-clinical |

| Clinical |

| Hospitals |

| Diagnostic Imaging Centers |

| Academic & Research Institutes |

| Neurology |

| Oncology |

| Cardiology |

| Psychiatry |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Traditional PET-MRI Systems | |

| Helium-free / Cryogen-free Systems | ||

| Fully-integrated Digital PET-MRI Systems | ||

| By Phase | Pre-clinical | |

| Clinical | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Academic & Research Institutes | ||

| By Application | Neurology | |

| Oncology | ||

| Cardiology | ||

| Psychiatry | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Brain PET-MRI Systems Market?

The Brain PET-MRI Systems Market size is expected to reach USD 412.03 million in 2026 and grow at a CAGR of 6.12% to reach USD 554.51 million by 2031.

Which application segment is growing fastest?

Neurology procedures are expanding at a 10.02% CAGR, propelled by Alzheimer’s and Parkinson’s imaging needs

Who are the key players in Brain PET-MRI Systems Market?

Siemens Healthineers AG, Koninklijke Philips N.V., GE HealthCare, Bruker, Mediso Ltd., MR Solutions, Cubresa Inc. and Aspect Imaging Ltd. are the major companies operating in the Brain PET-MRI Systems Market.

Which is the fastest growing region in Brain PET-MRI Systems Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Brain PET-MRI Systems Market?

North America leads with 41.98% revenue in 2025, thanks to robust reimbursement and research funding.

Page last updated on: