Neurovascular Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

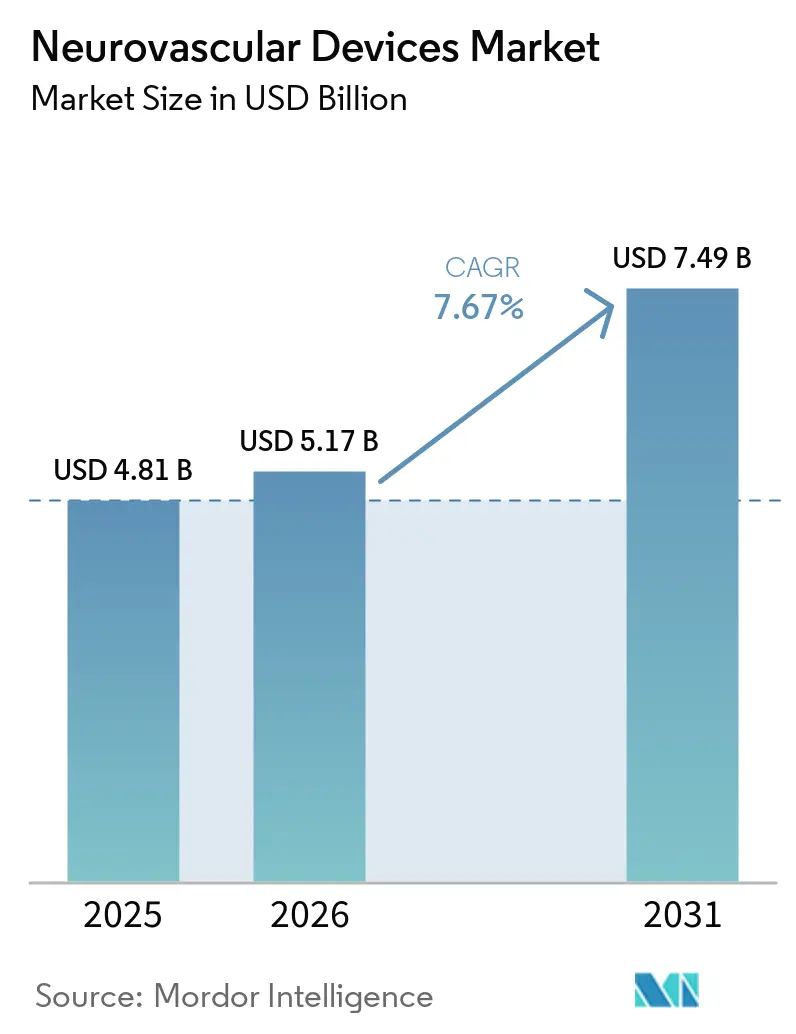

| Market Size (2026) | USD 5.17 Billion |

| Market Size (2031) | USD 7.49 Billion |

| Growth Rate (2026 - 2031) | 7.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurovascular Devices Market Analysis by Mordor Intelligence

The Neurovascular Devices Market size was valued at USD 4.81 billion in 2025 and estimated to grow from USD 5.17 billion in 2026 to reach USD 7.49 billion by 2031, at a CAGR of 7.67% during the forecast period (2026-2031). Sustained demand for minimally-invasive stroke interventions, reimbursement tailwinds in North America, and the diffusion of advanced imaging platforms are reinforcing the growth trajectory of the neurovascular devices market. North America continues to lead procedure volumes as hospitals standardize mechanical thrombectomy for large-vessel occlusions, while Asia-Pacific propels incremental growth through infrastructure build-outs that narrow treatment-access gaps. Device suppliers amplify competitive intensity by launching aspiration catheters with higher recanalization rates, flow diverters with faster occlusion profiles, and robotic navigation systems that lower radiation exposure. At the same time, expanded public and private payer coverage—most recently Medicare’s broader carotid stenting policy—removes cost barriers that previously dampened adoption.

Key Report Takeaways

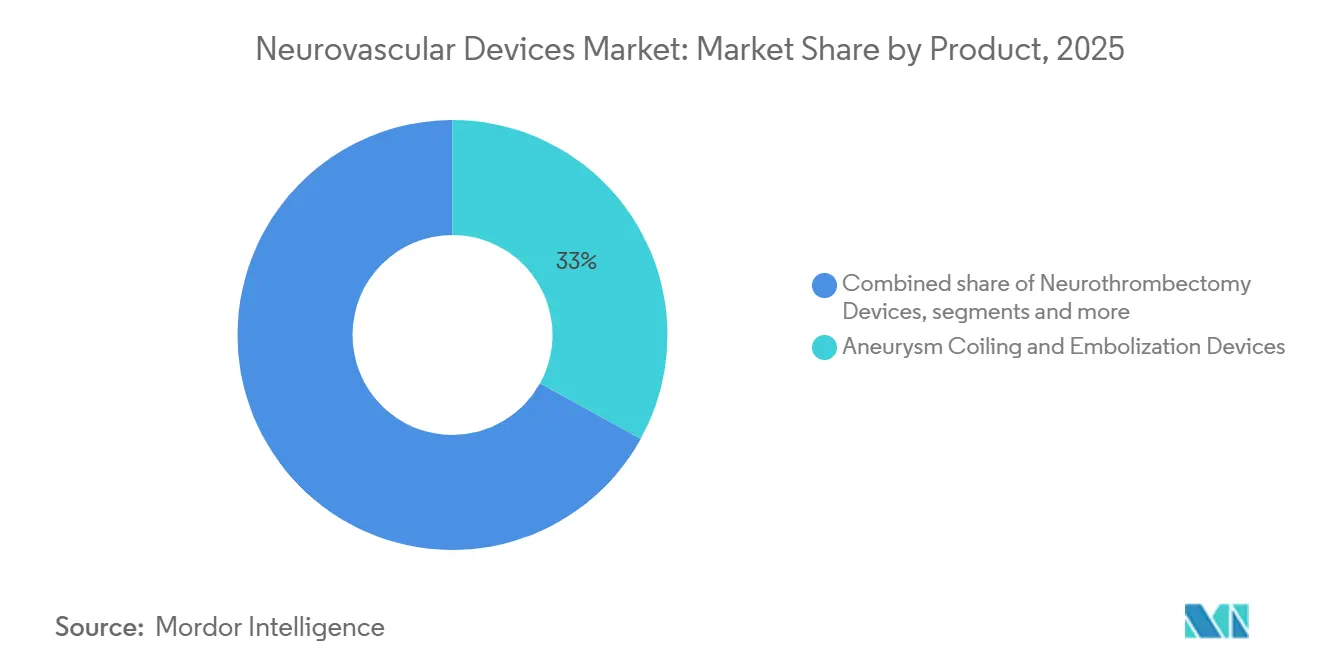

- By product, Aneurysm coiling and embolization devices held the largest 32.35% neurovascular devices market share in 2025, whereas neurothrombectomy devices are advancing at a 8.52% CAGR through 2031.

- By target disease, Ischemic stroke therapies accounted for 49.96% of the neurovascular devices market size in 2025; cerebral aneurysm interventions are forecast to climb at a 8.27% CAGR to 2031.

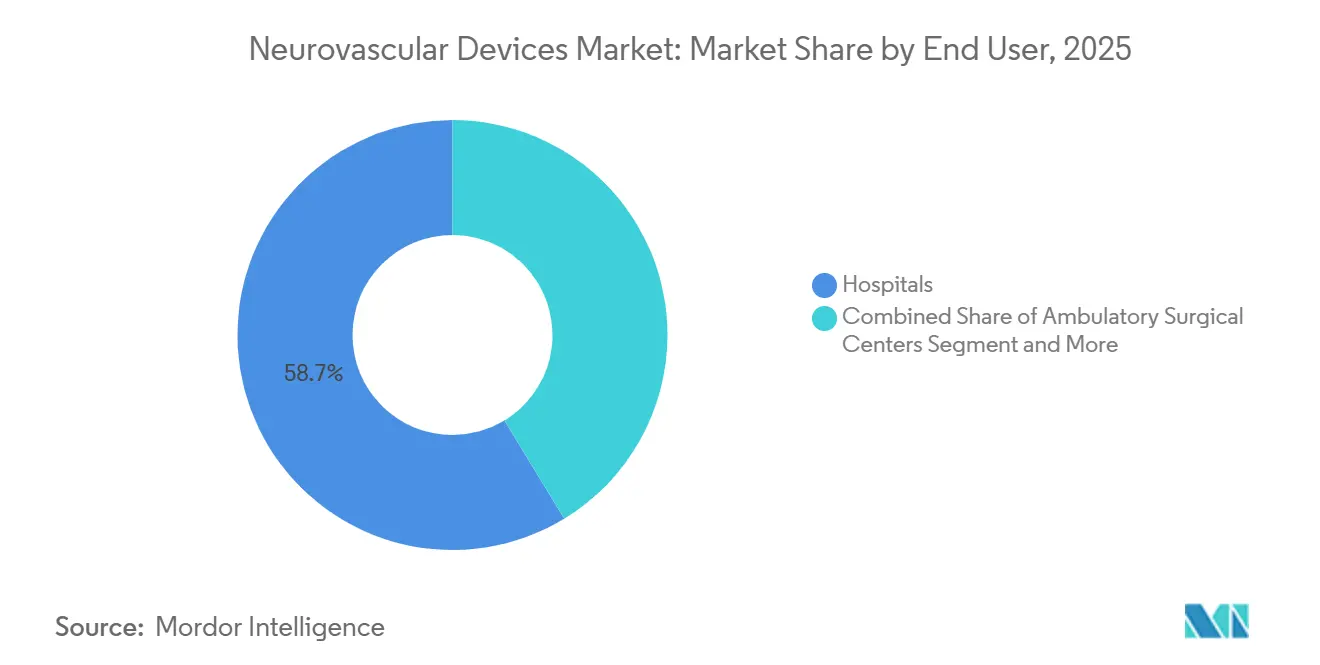

- By end user, Hospitals captured 58.70% of the neurovascular devices market share in 2025, yet ambulatory surgical centers are expanding fastest at a 8.73% CAGR.

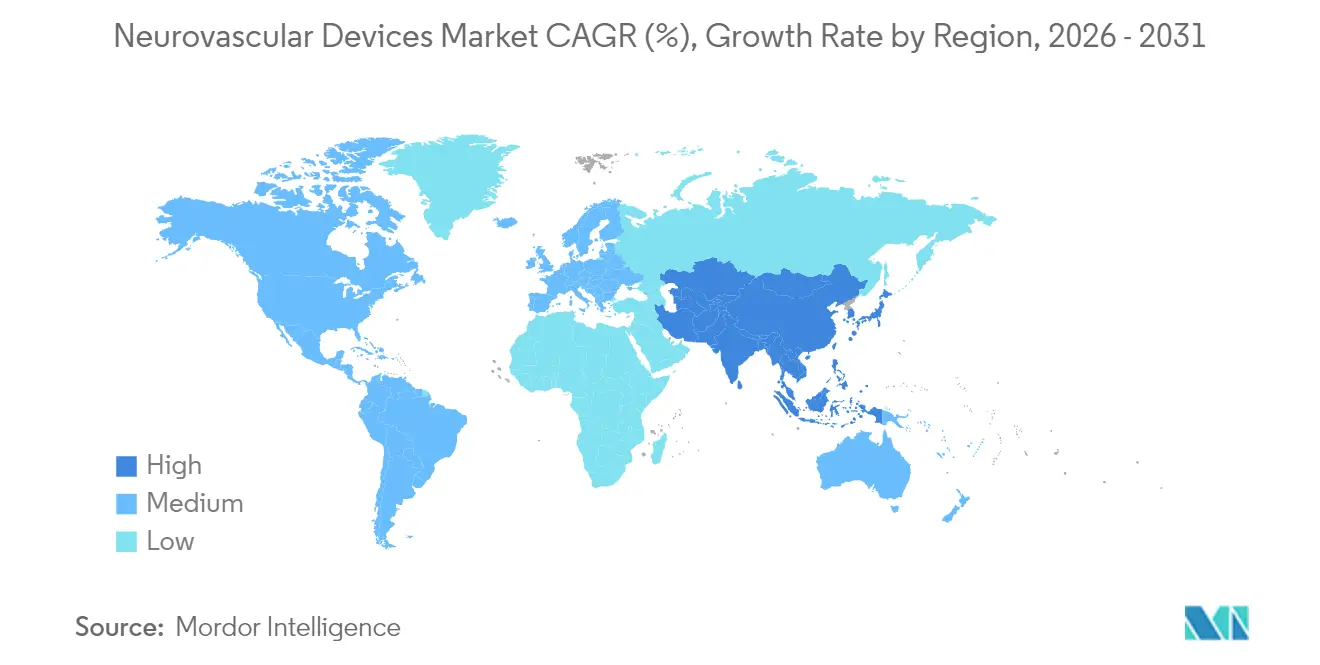

- By region, North America represented 44.24% of 2025 revenues, while Asia-Pacific is set to log the highest 8.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Stroke Incidence and Associated Socio-economic Burden | +2.1% | Global, with highest impact in Asia Pacific and emerging markets | Long term (≥ 4 years) |

| Rapid Innovation in Minimally Invasive Neuro-interventional Technologies | +1.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Hospital Adoption of Biplane Angio Suites Boosting Procedure Volumes | +1.3% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Increasing Research and Development Investments | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Expanding Reimbursement Coverage for Endovascular Stroke Care | +1.1% | North America & EU, selective APAC markets | Short term (≤ 2 years) |

| Expansion of Healthcare Infrastructure in Emerging Markets | +0.8% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Stroke Incidence and Associated Socio-economic Burden

Worldwide, stroke-related productivity losses cost USD 45.5 billion annually, incentivizing payers to reimburse early interventions that trim long-term care spending. Mortality rates in emerging economies remain 40–60% higher than in developed nations, reflecting infrastructure gaps that the neurovascular devices market can address. Asia-Pacific’s demographic shift toward older cohorts is projected to lift regional stroke incidence another 30% by 2030, accelerating device uptake. Health systems now quantify the return on investment of neurovascular programs by weighing shorter rehabilitation timelines against societal productivity gains.

Rapid Innovation in Minimally-Invasive Neuro-interventional Technologies

Next-generation aspiration catheters such as the SOFIA family deliver 85% recanalization versus the 65% benchmarks of earlier designs, providing a clinical edge that speeds adoption.[1]Source: Medical Device Network, “Radical Catheter Technologies Presents Data at SNIS,” medicaldevice-network.com Flow diverters like Pipeline Vantage achieve 95% aneurysm occlusion at 12 months while cutting average procedure times by 25%. Early evidence from robotic-assisted thrombectomy shows a 20% reduction in radiation exposure, supporting hospitals’ safety initiatives. AI-enhanced imaging platforms now deliver real-time vessel analysis that reduces complications by up to 20%. These performance gains lock in premium pricing, reinforcing the revenue potential of the neurovascular devices market.

Hospital Adoption of Biplane Angio Suites Boosting Procedure Volumes

Installations of biplane angiography systems climbed 18% in 2024 as hospitals pursued 30% lower contrast-agent usage and 20% faster case times. Dual-plane imaging reduces catheter repositioning and stroke risk, expanding treatable lesion complexity. Return-on-investment studies show 25–30% volume lifts and payback periods of 3.5 years in high-throughput centers. North American penetration already exceeds 65%, while Asia-Pacific hospitals advanced from 25% to 35% in 2024. The equipment also broadens patient eligibility, enlarging the procedure pool that feeds the neurovascular devices market.

Increasing Research and Development Investments

Medtronic’s Neuroscience unit posted USD 2.451 billion in 2024 revenue while sustaining double-digit R&D ratios that fund thrombectomy and flow-diverter pipelines.[2]Source: Medtronic, “Q2 FY2025 Results,” news.medtronic.com Stryker’s USD 4.9 billion acquisition of Inari Medical fast-tracked peripheral vascular adjacency and cross-portfolio synergies. FDA breakthrough designations now accelerate more than 40 neurovascular devices in review, shortening time to reimbursement. Venture-backed firms such as Contego Medical won FDA approval for combined stent-balloon-filter systems that recorded zero major strokes at 12 months. Constant innovation sustains pricing power and intensifies competition within the neurovascular devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and Lengthy Regulatory Approval Processes | -1.4% | Global, most pronounced in US and EU | Medium term (2-4 years) |

| High Procedure and Capital Equipment Costs | -1.2% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Persistent Shortage of Trained Neuro-interventionalists | -0.9% | Global, severe in low- and middle-income regions | Long term (≥ 4 years) |

| Procedural Complications and Diagnostic Delays | -0.7% | Global, variable by healthcare system maturity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent and Lengthy Regulatory Approval Processes Across Key Markets

Average US 510(k) clearance time stretched to 201 days in 2024, more than doubling the statutory target and delaying commercial launches.[3]Source: FDA, “510(k) and PMA Review Times,” fda.gov PMA approvals now exceed 12 months, and the EU Medical Device Regulation forces manufacturers to prepare separate clinical datasets costing up to USD 5 million per category. Smaller innovators struggle to fund dual-region submissions, damping pipeline diversity. Protracted approval cycles erode first-mover advantage, discouraging investors who weigh time-value of capital. The resulting lag constrains revenue realization within the neurovascular devices market.

High Procedure and Capital Equipment Costs Limiting Adoption in Budget-Constrained Hospitals

Mechanical thrombectomy cases average USD 35,000–50,000, with devices accounting for roughly half of the bill. A biplane suite demands USD 2–3 million upfront and USD 300,000 annual service fees, a heavy load for hospitals facing staffing inflation. Bundled procurement can shave USD 2,900 per intervention but often clashes with physician preference. One-third of rural US hospitals do not reach minimum volumes that justify a neurovascular program, widening geographic inequity. Emerging-market facilities buy 60–70% fewer units than developed peers because capital budgets remain restricted. These cost pressures temper uptake in parts of the neurovascular devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Aneurysm Coiling Anchors Value While Thrombectomy Accelerates Growth

Aneurysm coiling and embolization devices captured 32.35% of the neurovascular devices market share in 2025 thanks to proven efficacy across diverse aneurysm morphologies. Hydrogel and bioactive coils now deliver 92% five-year occlusion versus the 85% benchmark of bare platinum variants, keeping the segment firmly entrenched in hospital protocols. Over the forecast horizon, continuous material and delivery improvements help sustain unit demand.

Neurothrombectomy devices are growing fastest at a 8.52% CAGR, catalyzed by guideline expansions that allow treatment up to 24 hours after onset. Aspiration-first techniques and larger-bore catheters extend eligibility to patients with large core infarcts, broadening the neurovascular devices market. Cerebral balloon angioplasty and stenting systems post steady gains from refinements in balloon compliance and closed-cell stent design. Support devices such as micro-catheters and guidewires maintain consistent pull-through revenues as each thrombectomy consumes multiple disposables. Niche categories—liquid embolics, occlusion balloons, and next-gen flow diverters—offer incremental growth where conventional tools meet anatomical limits.

By Target Disease: Ischemic Stroke Dominates; Aneurysm Therapies Catch Up

Ischemic stroke solutions accounted for 49.96% of the neurovascular devices market size in 2025 because of their alignment with the highest-incidence cerebrovascular condition. Broader adoption of perfusion imaging elevates patient inclusion, while outcome data from DEFUSE 3 and DAWN continue to validate late-window thrombectomy. Hospitals therefore prioritize inventory for aspiration catheters and stent retrievers that shorten door-to-revascularization times.

Cerebral aneurysm interventions are projected to register a 8.27% CAGR through 2031 as screening programs escalate and patient awareness rises. Flow diverters and bioactive coils now address wide-neck and complex geometries, prompting prophylactic treatment of unruptured lesions. Arteriovenous malformations and fistulas remain specialized niches that require dedicated centers with multimodality skill sets, whereas intracerebral hemorrhage treatments trail due to uncertain risk-benefit profiles. The broadening disease palette positions the neurovascular devices market for deeper penetration across the stroke-care continuum.

By End User: Hospitals Retain Scale; ASCs Gain Momentum

Hospitals dominated distribution channels with 58.70% revenue share in 2025 by virtue of comprehensive stroke centers, 24/7 neurology call coverage, and intensive-care infrastructure. Their procedural breadth supports inventory management and multidisciplinary workflows for high-acuity cases.

Ambulatory surgical centers, however, are expanding at a8.73% CAGR as reimbursement changes allow site-neutral payments for select neurovascular services. ASCs deliver 20–30% cost savings and faster discharge, resonating with value-based care incentives. Specialty neurology and stroke centers blend hospital-grade equipment with streamlined care pathways, thriving in metropolitan catchments that sustain high case density. End-user evolution thus reflects both efficiency improvements and care-setting diversification within the neurovascular devices market.

Geography Analysis

North America generated 44.24% of global revenue in 2025, buoyed by Medicare coverage expansion for carotid stenting and 65% penetration of biplane angiography among US hospitals. Canadian provinces allocated new stroke-infrastructure budgets that equipped tertiary centers with thrombectomy suites, while Mexican private hospitals invested in aspiration systems to service medical tourists.

Asia-Pacific is forecast to post the strongest 8.66% CAGR, propelled by China’s 2.77 million ischemic stroke cases, Japan’s rapidly aging population, and India’s growing middle class. Nevertheless, device penetration varies: Japan approaches Western adoption levels, whereas emerging ASEAN markets prioritize foundational capacity such as perfusion CT scanners. Local manufacturing incentives in China encourage partnerships that counterbalance import tariffs and regulatory delays, supporting long-term growth for the neurovascular devices market.

Europe maintains steady demand across Germany, the United Kingdom, and France, where evidence-based purchasing committees favor devices with robust cost-effectiveness dossiers. Middle East & Africa show nascent uptake concentrated in Gulf Cooperation Council states, while South America progresses gradually as Brazil deploys stroke networks and Argentina capitalizes on domestic device production. Regional momentum hinges on infrastructure maturity, payer policy, and economic development, necessitating localized commercial models.

Competitive Landscape

The neurovascular devices market features moderate consolidation as Medtronic, and Stryker leverage broad portfolios, global logistics, and sustained R&D to defend share. Medtronic’s Neuroscience revenue reached USD 2.451 billion in 2024 and continues double-digit expansion via pipeline technologies. Stryker’s USD 4.9 billion Inari Medical acquisition accelerated scale in peripheral vascular therapy and created cross-selling synergies.

Mid-sized innovators such as Contego Medical differentiated by bundling stent, balloon, and embolic filter into a single delivery system that recorded zero major strokes at one-year follow-up. Venture-backed entrants exploit regulatory designations to shorten approval timelines in thrombectomy aspiration, robotic navigation, and AI-guided imaging.

Competitive advantage increasingly rests on demonstrable clinical outcomes and cost-per-disability-adjusted-life-year benchmarks rather than incremental engineering tweaks. Firms investing in multicenter real-world databases gain persuasive evidence for payer negotiations. Consequently, value creation within the neurovascular devices market shifts from hardware differentiation to proof of improved patient survival and reduced total-episode cost.

Neurovascular Devices Industry Leaders

Asahi Intecc Co., Ltd.

CERENOVUS (Johnson & Johnson)

Terumo Corporation (MicroVention)

Medtronic plc

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Medtronic entered an exclusive US distribution accord with Contego Medical covering the Neuroguard IEP combined stent-balloon-filter platform.

- January 2025: Q'Apel Medical secured CE mark for the Armadillo SelectFlex 7F neurovascular access system.

- September 2024: Vesalio launched the pVasc thrombectomy device for peripheral occlusion removal in the United States.

- July 2024: Vesalio introduced the NeVa NET 4 mm clot-capture device for ischemic stroke.

Global Neurovascular Devices Market Report Scope

As per the scope of the report, neurovascular devices are used to treat neurological disorders. These include coils, stents, and clips that are used to treat neurovascular disorders such as brain aneurysms. These devices are widely used in the treatment and diagnosis of various types of peripheral and central nervous system disorders and ailments. The Neurovascular Devices Market is classified as follows: Product (Aneurysm Coiling and Embolization Devices, Cerebral Balloon Angioplasty and Stenting Systems, Support Devices, Neurothrombectomy Devices, and Others), Target Disease (Ischemic Strokes, Cerebral Aneurysms, Arteriovenous Malformations, and Fistalus, and Other target diseases), and Geography (North America, Europe, Asia-Pacific, Middle The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values (in USD million) for the above segments.

| Aneurysm Coiling & Embolization Devices |

| Cerebral Balloon Angioplasty & Stenting Systems |

| Neurothrombectomy Devices |

| Support Devices (Micro-catheters, Guidewires, Sheaths) |

| Other Devices (Liquid Embolics, Occlusion Balloons) |

| Ischemic Stroke |

| Cerebral Aneurysm |

| Arteriovenous Malformations & Fistulas |

| Intracerebral Hemorrhage |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Neurology & Stroke Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Aneurysm Coiling & Embolization Devices | |

| Cerebral Balloon Angioplasty & Stenting Systems | ||

| Neurothrombectomy Devices | ||

| Support Devices (Micro-catheters, Guidewires, Sheaths) | ||

| Other Devices (Liquid Embolics, Occlusion Balloons) | ||

| By Target Disease | Ischemic Stroke | |

| Cerebral Aneurysm | ||

| Arteriovenous Malformations & Fistulas | ||

| Intracerebral Hemorrhage | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Neurology & Stroke Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the neurovascular devices market in 2026?

The neurovascular devices market size reached USD 5.17 billion in 2026 and is projected to hit USD 7.49 billion by 2031.

Which product category leads sales?

Aneurysm coiling and embolization devices held the largest 32.35% share of 2025 revenue.

What is the fastest-growing product segment?

Neurothrombectomy devices are expanding at a 8.52% CAGR through 2031.

Which region is forecast to grow quickest?

Asia-Pacific is set to record a 8.66% CAGR driven by rising stroke incidence and infrastructure investments.

Why are ambulatory surgical centers gaining traction?

Medicare’s site-neutral payments and 20–30% cost savings are shifting select neurovascular procedures to ambulatory surgical centers.

What limits faster adoption in emerging markets?

High device and capital-equipment costs, coupled with limited trained specialists, presently constrain uptake.

Page last updated on: