Inferior Vena Cava Filter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

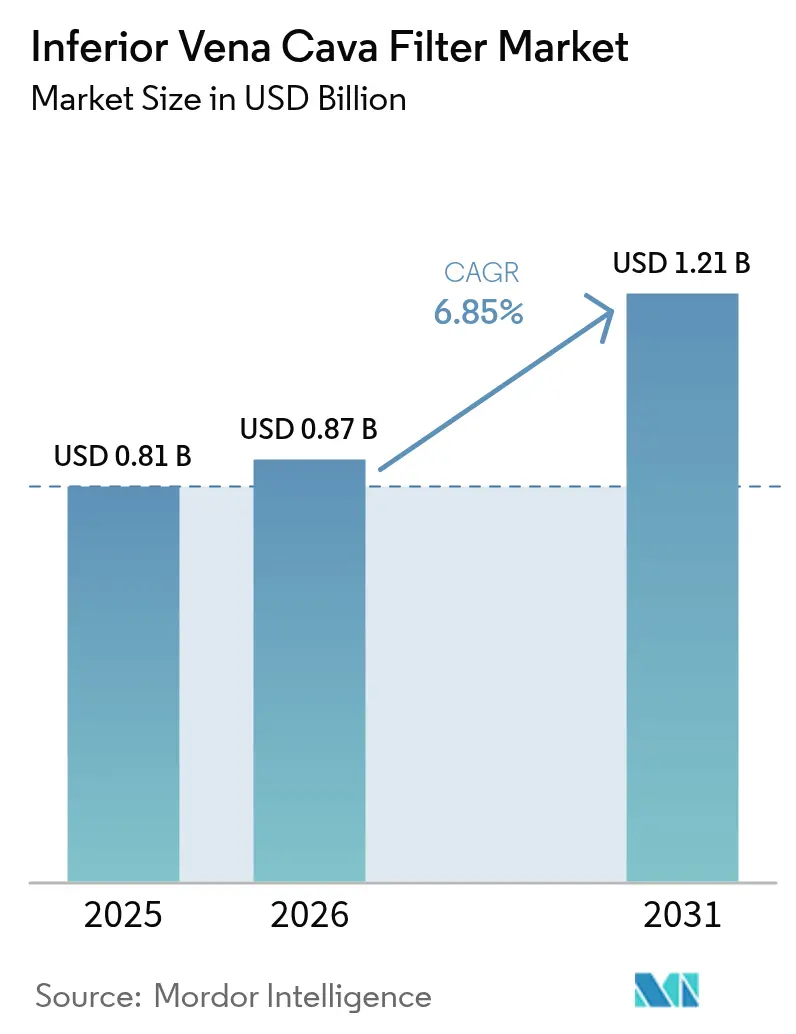

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Inferior Vena Cava Filter Market Analysis by Mordor Intelligence

The Inferior Vena Cava Filter was valued at USD 0.81 billion in 2025 and estimated to grow from USD 0.87 billion in 2026 to reach USD 1.21 billion by 2031, at a CAGR of 6.85% during the forecast period (2026-2031). Growth reflects an intricate balance between rising venous thrombo-embolism prevalence, tightened professional-society guidance that discourages routine prophylaxis, and a litigation climate that raises manufacturer risk profiles. Despite shrinking placement volumes reported in multiple payer datasets, steady demand persists because oncology, trauma, and complex surgical cohorts still require mechanical protection when anticoagulation is contraindicated. Economic analyses now show permanent filters producing higher quality-adjusted life-years at lower lifetime costs, a finding that starts to reshape buying patterns even as physicians continue to value the perceived reversibility of retrievable designs. Meanwhile, artificial-intelligence-guided imaging improves placement precision and retrieval planning, potentially shortening procedure time and mitigating complication risk. Parallel advances in pharmacomechanical thrombectomy introduce a credible substitute, yet high capital outlay and operator learning curves limit full displacement of filters in the short term.

Key Report Takeaways

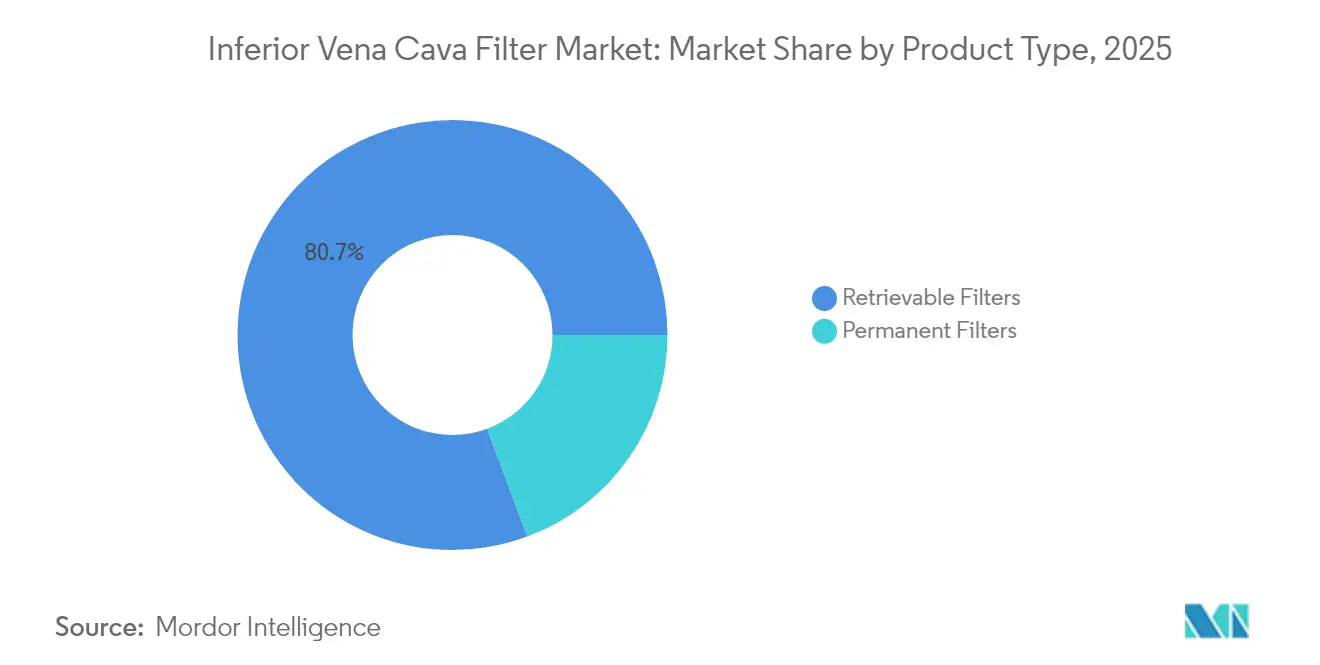

- By product type, the retrievable segment led with 80.65% revenue share in 2025, while permanent filters recorded the fastest 7.55% CAGR through 2031.

- By application, treatment accounted for 61.55% of the Inferior Vena Cava Filter market share in 2025; prevention is advancing at a 7.62% CAGR to 2031.

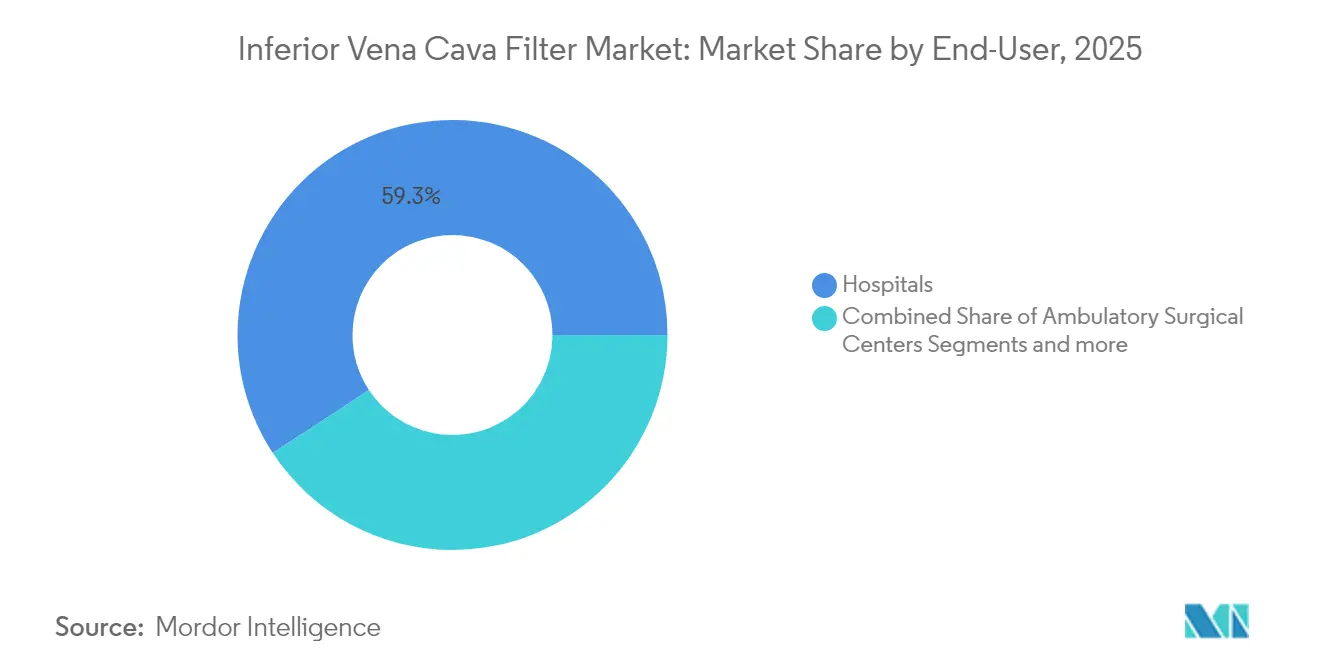

- By end-user, hospitals held 59.25% share of the Inferior Vena Cava Filter market in 2025, whereas specialty clinics are projected to expand at an 7.8% CAGR.

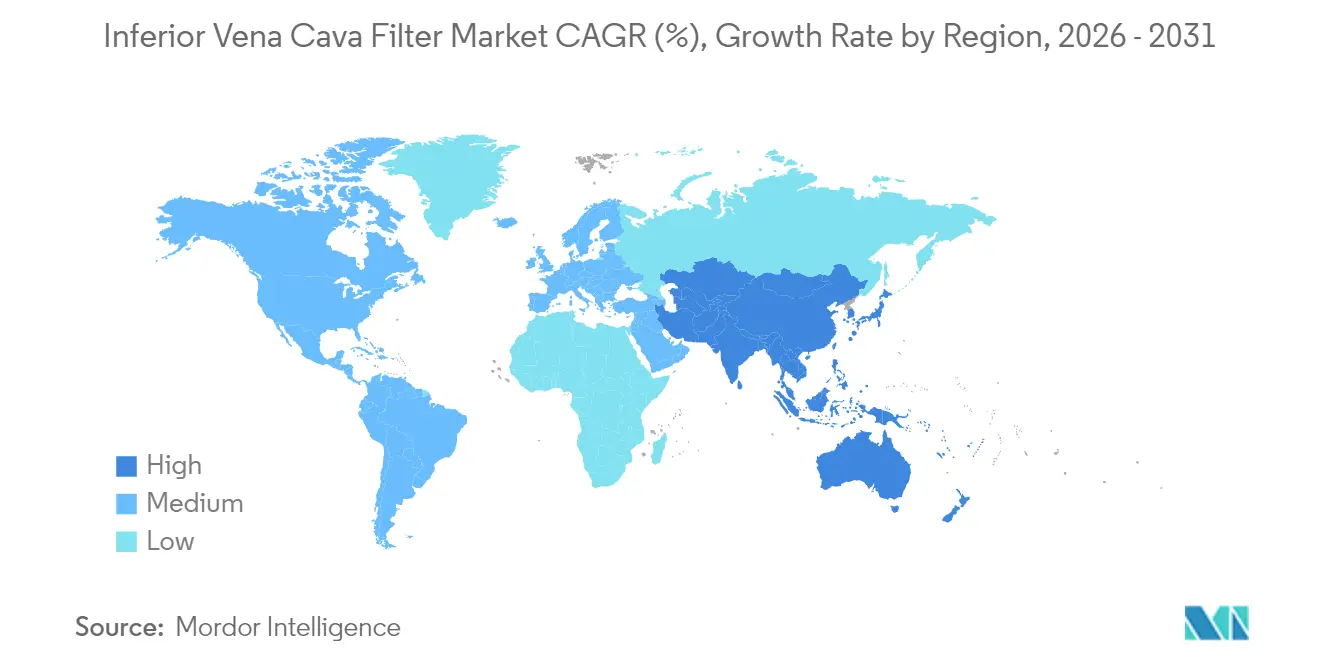

- By geography, North America commanded 41.78% of 2025 revenue, while Asia–Pacific is set to register the fastest 7.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inferior Vena Cava Filter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of VTE & PE | +1.8% | Global with higher impact in North America & Europe | Long term (≥ 4 years) |

| Growing adoption of retrievable filters | +1.2% | North America & Europe, expanding to Asia–Pacific | Medium term (2-4 years) |

| Increasing prophylactic use in surgeries | +0.9% | North America & Europe, selective Asia–Pacific uptake | Medium term (2-4 years) |

| Biodegradable polymer filters in pipeline | +0.8% | North America & Europe | Long term (≥ 4 years) |

| AI-enabled imaging for accuracy | +0.7% | Early global adoption | Long term (≥ 4 years) |

| Higher PE recurrence in oncology patients | +0.6% | Developed healthcare markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Venous Thrombo-embolism & Pulmonary Embolism

Cancer-associated thrombosis drives recurrent PE rates of 22.5% even under optimized anticoagulation, creating a continual need for mechanical protection [1]Gerald A. Soff, "Cancer-Associated Thrombosis: Management of a Patient With an Isolated Calf Deep Vein Thrombosis," Journal of Clinical Oncology, ascopubs.org. Aging populations amplify this demand because frailty and comorbidities limit drug therapy durability. Earlier disease detection through multidetector CT and duplex ultrasound means more clinically silent clots are captured, pushing the Inferior Vena Cava Filter market toward routine rather than exceptional use in high-risk cohorts [2]Seble Birhane, "Outcomes of deep venous thrombosis management and associated factors among patients in tertiary hospitals in Addis Ababa, Ethiopia: a multicenter retrospective cohort study," Thrombosis Journal, thrombosisjournal.biomedcentral.com. Artificial intelligence further elevates diagnostic sensitivity, with deep-learning models identifying small, segmental emboli that were previously overlooked. Combined, these factors sustain double-digit procedural growth in oncology centers despite overall utilization decline in the general population.

Growing Adoption of Retrievable Filters Over Permanent Designs

Physicians frequently select retrievable filters because they can, in theory, be extracted once the clotting window closes. National databases confirm this behavioral bias even though only 15% of implanted devices are eventually retrieved. Complication registries attribute 86.8% of adverse events to retrievable products, yet hospitals prefer them for immediate peri-operative flexibility. Aggressive retrieval techniques now reach 94.7% success, but the higher procedural complexity elevates peri-operative complication risk to 5.3%. Predictive algorithms embedded in electronic records help identify patients unlikely to return for extraction, nudging decision-makers toward permanent or bioconvertible solutions. The net result is a mixed demand curve that keeps both device classes commercially relevant and maintains vibrancy in the Inferior Vena Cava Filter market [3]Lihao Qin, "A nomogram model to predict non-retrieval of short-term retrievable inferior vena cava filters," Frontiers in Cardiovascular Medicine, frontiersin.org.

Increasing Prophylactic Use in Bariatric & Major Orthopedic Surgeries

Bariatric surgery combines morbid obesity with limited mobilization, a pairing that multiplies VTE risk; yet extreme body habitus also complicates fluoroscopic visualization, raising deployment difficulty and malposition hazards. Orthopedic evidence is more encouraging. A prospective spinal series recorded thrombus capture in 17% of devices at retrieval with zero symptomatic PE, validating targeted prophylaxis. AI-driven risk stratification models now discern which elective surgical patients derive net benefit, enabling narrower but more defensible indications. These targeted pathways support steady expansion of the Inferior Vena Cava Filter market in prevention while mitigating medico-legal exposure tied to blanket prophylaxis.

AI-enabled Imaging Improving Placement & Retrieval Accuracy

Machine-learning algorithms achieve 82.3% accuracy in estimating right atrial pressure from handheld ultrasound clips, equaling expert cardiologist performance and enhancing intra-procedural decision-making. Computer-vision platforms integrated into fluoroscopy suites automatically detect caval landmarks, lowering radiation exposure and shortening deployment time. Post-procedure, AI models mine electronic charts to flag eligible retrieval candidates before fibrous ingrowth renders extraction hazardous. FDA-cleared triage tools such as Aidoc sharply improve PE detection specificity, consequently reducing inappropriate filter placement triggered by false-positive scans. These incremental workflow efficiencies are beginning to compress cost per case, bolstering long-term attractiveness of the Inferior Vena Cava Filter market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device-related complications & litigation | -2.1% | Global, highest impact in North America | Short term (≤ 2 years) |

| Restrictive professional guidelines | -1.6% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Uptake of pharmacomechanical thrombectomy | -1.4% | North America & Europe, global spread | Medium term (2-4 years) |

| Limited reimbursement for retrieval | -1.0% | Global, variable by region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Device-related Complications & Product Liability Litigation

Becton Dickinson accrued USD 1.7 billion in reserves for ongoing filter lawsuits, the highest product-specific medical-device liability provision on record. More than 11,000 cases remain active and reference migration, fracture, and organ perforation, all of which scale with indwelling time. FDA-mandated post-market analysis revealed penetrations exceeding 20% when dwell exceeded 90 days, adding urgency to improved retrieval programs. Legal exposure compels manufacturers to redirect capital from R&D to settlement funds, slowing pipeline diversification and tempering growth prospects for the wider Inferior Vena Cava Filter market.

Rapid Uptake of Pharmacomechanical Thrombectomy as an Alternative

Device-assisted thrombectomy immediately clears clot burden and eliminates the need for a mechanical barrier. Real-world series place episode costs at USD 10,682–19,669 depending on disposable mix, which can compare favorably with the cumulative cost of filter placement, retrieval, and anticoagulant therapy. ClotTriever technology posts an in-hospital mortality of 1.0% versus 2.9% for comparator devices. The multicenter DEFIANCE trial, launched in 2024, will benchmark thrombectomy outcomes against anticoagulation alone and could prompt guideline changes that depress Inferior Vena Cava Filter market demand in acute DVT. However, high upfront equipment costs limit adoption outside tertiary centers, providing a temporal buffer for filter suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Permanent Filters Stage a Quiet Comeback

Permanent devices contributed a smaller revenue base but delivered the swiftest 7.55% CAGR to 2031 as economic evidence gains traction. Retreivable filters generated 80.65% market share in 2025. The Inferior Vena Cava Filter market size for permanent designs is projected to widen materially because they generate 5.41 quality-adjusted life-years at an average lifetime expenditure of USD 2,070, compared with 5.33 QALYs and USD 4,650 for retrievable models. Nonetheless, retrievable systems retain dominant 2025 share owing to deeply ingrained clinical preference and favorable reimbursement coding.

Physician education programs now highlight low national extraction rates and heightened adverse-event frequency, encouraging risk committees to reassess device selection protocols. Predictive scoring tools embedded within electronic medical records identify patients who will likely default on follow-up, directing clinicians toward permanent or bioconvertible implants. Early-phase polymer-based filters that dissolve after thrombo-protective windows may merge the advantages of both archetypes and inject fresh momentum into the Inferior Vena Cava Filter market.

By Application: Prevention Segment Gains Momentum

Treatment indications still represented 61.55% of 2025 revenue, anchored by oncology and trauma populations with contraindications to anticoagulation. The Inferior Vena Cava Filter market share tied to prevention is, however, rising faster at a 7.62% CAGR as high-risk bariatric and complex orthopedic procedures look to minimize peri-operative PE.

Clinical spine data showing a 17% thrombus capture rate during elective fusion surgeries help justify selective prophylaxis. Trauma registries also reveal survival benefit when filters are placed within 72 hours of admission. Simultaneously, AI-driven risk tools shrink unnecessary placements by stratifying candidates more accurately, strengthening economic justification and enhancing public perception of the Inferior Vena Cava Filter market.

By End-User: Specialty Clinics Expand Footprint

Hospitals controlled 59.25% of placements in 2025 because they own interventional suites and manage complex comorbidities. Still, specialty vascular centers and ambulatory surgical facilities are growing at an 7.8% CAGR, luring referrals with shorter wait times and higher retrieval success rates. The Inferior Vena Cava Filter market size attributed to ambulatory sites remains modest yet doubles in some metropolitan areas where payer networks reward lower facility fees.

Dedicated retrieval programs at specialty clinics surpass 30% extraction compliance by coupling automated reminders with tele-follow-up, a metric that appeals to malpractice insurers. Capital investment in high-definition fluoroscopy and AI overlay software further differentiates these centers and accelerates their share gain inside the broader Inferior Vena Cava Filter market.

Geography Analysis

North America accounted for 41.78% of 2025 revenue because of comprehensive reimbursement coverage and advanced imaging infrastructure. Medicare claims nevertheless show a steep decline in filter placements from 44,680 in 2013 to 19,501 in 2021, reflecting revised professional guidance and expanding thrombectomy alternatives. Litigation costs stifle innovation budgets, but AI-enabled imaging and registry-linked performance tracking nurture pockets of growth in high-acuity oncology centers.

Asia–Pacific is the fastest-growing territory with an 7.9% CAGR. China drives volume via insurance reform and large-scale physician-training programs in endovascular techniques. Baseline VTE incidence remains lower than Western cohorts; nonetheless, rapid growth in complex surgeries and trauma care sustains healthy demand. Japan and South Korea mature more slowly because national cost-containment policies emphasize pharmacological prophylaxis, yet they still adopt AI-guided retrieval platforms that showcase superior safety.

Europe exhibits balanced dynamics. Germany and the United Kingdom lead utilization through integrated trauma systems, while France prioritizes oncology indications. Middle Eastern Gulf states invest in fully digital cath-lab expansions that favor filter procedures for medical tourists. Africa’s share is embryonic, limited by infrastructure and reimbursement shortfalls, but private-sector projects in South Africa lay groundwork for future participation in the Inferior Vena Cava Filter market.

Regulatory Landscape

In the United States, inferior vena cava (IVC) filters and associated retrieval accessories remain under FDA cardiovascular-device oversight. IVC filters are regulated as Class II devices (for example, under 21 CFR 870.3375), and the FDA provides guidance for cardiovascular intravascular filter 510(k) submissions. A notable 2026 classification action further clarified the pathway for advanced retrieval technology, when, in April 2026, the FDA classified a laser-powered IVC filter retrieval catheter as Class II with special controls (21 CFR 870.5125), emphasizing performance and safety controls around retrieval.

In Europe, IVC filters are regulated under the EU Medical Device Regulation (Regulation (EU) 2017/745), where implantable endovascular devices generally require robust conformity assessment and post-market evidence. In March 2026, Delegated Regulation (EU) 2026/1359 amended aspects of the MDR related to certain class IIb implantable devices and the technical documentation assessment approach, affecting compliance planning and notified-body interactions for manufacturers with standardized product lines. Globally, harmonization and procurement specifications increasingly reference ISO 25539-3:2024 (published October 2024) for vena cava filter systems, tightening expectations for evaluation, nomenclature, design attributes, and manufacturer-provided information across markets.

Value Chain Analysis

The value chain starts with specialty inputs, such as biocompatible metals and alloys and polymer components for introducers and sheaths, and proceeds through precision manufacturing, surface finishing, assembly, sterilization, and packaging. It then moves through regulatory release, distributor logistics, and hospital or outpatient inventory management for interventional radiology, vascular surgery, and cath-lab settings. Demand fulfillment continues to track procedure-site dynamics, with placements still concentrated in hospitals while retrieval programs and follow-up workflows increasingly shift toward specialty clinics and ambulatory settings that can operationalize scheduling, reminders, and higher-touch follow-up.

Quality systems and post-market surveillance are a central constraint and differentiator across the chain, since recalls and safety scrutiny feed back into supplier qualification, in-process controls, and clinician confidence. For example, Argon Medical Devices initiated a voluntary recall in September 2025 for specific lots of the Option ELITE Vena Cava Filter System after reports of increased resistance during dilator advancement, illustrating how lot-level issues can ripple into downstream distributor stock rotation, provider preference, and risk-management reviews. At the same time, procurement teams face higher supply-chain complexity, including trade and tariff-related cost volatility for specialty materials and manufacturing equipment, which pushes manufacturers toward dual-sourcing and more resilient regional supply strategies, even as procedural economics and reimbursement for retrieval remain practical bottlenecks.

Competitive Landscape

The Inferior Vena Cava Filter market features moderate concentration. The 2024 top-five vendors commanded a combined 62% revenue share, with Becton Dickinson, Cook Medical, and Boston Scientific at the forefront. Becton Dickinson absorbed C.R. Bard and now manages the industry’s broadest installation base, though a USD 1.7 billion litigation reserve clouds its near-term earnings outlook. Cook Medical leverages deep surgeon relationships and offers bioconvertible prototypes positioned as next-generation solutions. Boston Scientific reported USD 16.747 billion net sales in 2024, a 17.6% rise that funds continuous clinical-evidence generation.

Strategic priorities pivot toward device safety, integrated retrieval tracking, and AI-assisted deployment. Manufacturers advertise training platforms that couple real-time fluoroscopy with predictive positioning software. Smaller companies pursue regional playbooks, supplying cost-optimized filters to emerging markets and partnering with local distributors.

Mechanical thrombectomy entrants such as Inari Medical influence competitive tactics. Device makers diversify by bundling filters with hemodynamic monitoring or hybrid clot-extraction kits to maintain share against these disruptive modalities. The next critical battleground is Asia–Pacific, where domestic brands court public hospitals with aggressive pricing, forcing multinationals to emphasize clinical differentiation and post-purchase service within the Inferior Vena Cava Filter market.

Inferior Vena Cava Filter Industry Leaders

-

Becton, Dickinson and Company

-

Boston Scientific Corporation

-

Cardinal Health

-

Cook Medical

-

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest whitespace sits in retrieval performance and structured follow-up, where provider incentives and institutional protocols increasingly shape device demand. For 2026, MIPS Quality Measure #421 tracks the appropriateness of assessment for retrievable IVC filter removal within 3 months post-placement, creating a measurable compliance driver for retrieval-tracking services, patient outreach workflows, and device-adjacent software that flags eligible removals. 2026 clinical evidence on closed-loop management protocols reported improvements in retrieval rates at 90 days (from 41.2% to 65.4%) and at 180 days (from 41.8% to 73.1%), reinforcing the commercial value of solutions that link implants with retrieval planning, reminders, and clinic coordination.

A second opportunity centers on safer and more effective retrieval tools and accessories, since long-dwell filters remain clinically challenging and litigation-sensitive. The FDA’s April 2026 Class II (special controls) classification for a laser-powered IVC filter retrieval catheter provides a clearer regulatory route for advanced retrieval technologies, encouraging product development around controlled energy delivery, embolic protection, and complication mitigation. Ongoing post-market surveillance obligations, including long-horizon observational studies for established filter families (with studies running into 2030), also support demand for real-world evidence generation and registry-linked monitoring services that can inform procurement decisions and strengthen appropriate-use positioning amid restrictive guidance discouraging routine prophylactic placement.

Recent Industry Developments

- April 2026: The US FDA classified a laser-powered inferior vena cava (IVC) filter retrieval catheter as a Class II device with special controls (21 CFR 870.5125). This formalizes a clearer regulatory pathway for advanced retrieval technologies, reinforcing product-development focus on safer, more predictable extraction in long-dwell cases where complications and medico-legal exposure are elevated.

- July 2025: Teleflex Incorporated completed the acquisition of BIOTRONIK’s Vascular Intervention unit for EUR 760 million (USD 825 million). The deal broadens Teleflex’s peripheral intervention footprint and can strengthen bundled offerings across access and endovascular procedure workflows that overlap with IVC filter placement and retrieval settings.

- October 2024: Inari Medical, the American Venous Forum, and the National Blood Clot Alliance initiated the DEFIANCE trial to compare mechanical thrombectomy with anticoagulation alone in DVT management. The trial adds higher-quality clinical benchmarking for a substitute therapy, influencing how hospitals and physicians weigh thrombectomy versus mechanical protection strategies in acute VTE pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of inferior vena cava (IVC) filters that are placed in the IVC to help prevent pulmonary embolism, typically for patients with deep vein thrombosis or high thromboembolism risk. Revenue is counted at the device level across major care settings and geographies.

Scope exclusions: Excludes anticoagulant drugs, diagnostic imaging procedures, guidewires and catheters sold as general-purpose accessories, and post-procedure follow-up services unless they are bundled into the filter device price.

Segmentation Overview

-

By Product Type

- Retrievable Filters

- Permanent Filters

-

By Application

- Treatment of Venous Thrombo-embolism

- Prevention of Pulmonary Embolism

-

By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping how IVC filters are used and billed, then aligning that to a consistent definition of device revenue across countries. We relied on public sources such as the US FDA device safety communications and device-related databases, the US Centers for Disease Control and Prevention (CDC) for venous thromboembolism context, and the World Health Organization (WHO) for health system indicators that influence procedure access.

We also reviewed sources such as the US Centers for Medicare and Medicaid Services (CMS) for procedure and payment context, OECD health statistics for utilization signals, and peer reviewed clinical literature on guideline shifts and retrieval behavior. Company annual reports, investor decks, and reputable press releases were used to understand portfolio focus and geographic exposure. A paid subscription for company financials and a patent database helped cross-check product activity and timing. These are illustrative sources, and many other public references were also used for data collection, clarification, and validation.

Primary Interviews and Surveys

Primary inputs were taken from interviews and surveys with interventional specialists, hospital procurement teams, and device distributors who see day to day usage and tender behavior. We also spoke with product and sales leaders to validate price bands, retrieval versus permanent mix, and how clinical guidance is changing demand across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 15% | APAC: 48% |

| Mid tier: 44% | Functional/Unit leaders: 36% | EMEA: 29% |

| Smaller Players: 21% | Managers: 49% | Americas: 23% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where procedure demand and care access are translated into an addressable pool for IVC filter placements, then adjusted by adoption patterns for retrievable versus permanent designs. Before the total is finalized, it is checked with selective bottom-up approximations using sampled average selling prices by care setting and a reasonableness roll-up of supplier presence in major regions.

Key inputs used in the model include the incidence and treatment rate of venous thromboembolism, the share of patients with contraindications to anticoagulation, retrieval attempt and success rates for retrievable filters, and regional procedure capacity in hospitals and ambulatory surgical centers. Pricing assumptions are built as ranges by geography and end user, then stress-tested against procurement feedback and publicly visible reimbursement signals where available. Forecasts are produced using scenario analysis with a base case informed by clinician feedback on guideline adherence, safety concerns, and the pace of minimally invasive clot management substitutes. Where direct volume signals are thin for smaller countries, gaps are handled using proxy indicators such as hospital procedure intensity and regional adoption benchmarks, then rechecked with interview feedback.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including disease burden indicators, procedure access metrics, and the implied device price and volume relationship by region. When a country total looks unusual, assumptions are revisited and, if needed, experts are re-contacted to confirm whether the variance is linked to policy, safety actions, or temporary stocking effects.

A multi-step internal review is completed before sign-off, with checks on year over year movements, mix shifts between retrievable and permanent filters, and currency conversion timing. The dataset is refreshed annually, and interim updates are triggered when material events occur, including major regulatory actions, guideline changes, or sharp pricing resets. Right before delivery, a final analyst pass is done so clients receive the most current view available at the time.

Mordor Intelligence's Inferior Vena Cava Filter Market Size Measured Against Other Published Estimates

Published market sizes for IVC filters can vary more than buyers expect, even when they describe the same device category. The differences usually come from how each study treats device scope, how it converts procedures into units, and how it applies pricing and currency assumptions across regions.

The main gap comes from whether adjacent clot management devices and accessory revenue are counted together with the filter, and how retrievable filter utilization is adjusted for retrieval attempts over time. Different base years also matter, because guideline changes and safety communications can shift usage and ASPs quickly, and not every publisher refreshes assumptions on the same cadence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.81 B (2025) | |

| Global Publisher A | USD 0.82 B (2025) | Uses a broader segmentation lens that can blend filter demand with adjacent accessory revenue and applies a longer forecast window, which may smooth near-term guideline and safety driven utilization changes. |

| Global Publisher B | USD 0.86 B (2025) | Applies a more aggressive growth path tied to higher assumed procedure adoption and less explicit adjustment for retrievable filter retrieval behavior, which can lift implied unit demand and value. |

The spread in the table is largely explained by scope treatment and how procedure-to-unit conversion is adjusted over time, especially for retrievable filters. By separating filter-only revenue and explicitly adjusting the demand pool for retrieval-related utilization, Mordor Intelligence keeps the estimate traceable to procedure indicators and price bands that can be rechecked during updates.

Key Questions Answered in the Report

What is the current size of the Inferior Vena Cava Filter market?

The market is valued at USD 0.87 billion in 2026 and is projected to reach USD 1.21 billion by 2031.

How fast is the Inferior Vena Cava Filter market growing?

Industry revenue is forecast to expand at a 6.85% CAGR through 2031.

Which region offers the highest growth potential?

Asia–Pacific leads with an 7.9% CAGR to 2031, while North America remains the largest regional market at 41.78% of 2025 revenue.

How significant is prophylactic use compared to treatment use?

Treatment applications held 61.55% of 2025 revenue, yet prevention is rising faster at a 7.62% CAGR through 2031.

What legal and competitive pressures influence this market?

Ongoing product-liability litigation, including a USD 1.7 billion reserve by Becton Dickinson, and the accelerating adoption of pharmacomechanical thrombectomy are key factors that temper growth.

Page last updated on: