Micro Guide Catheter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

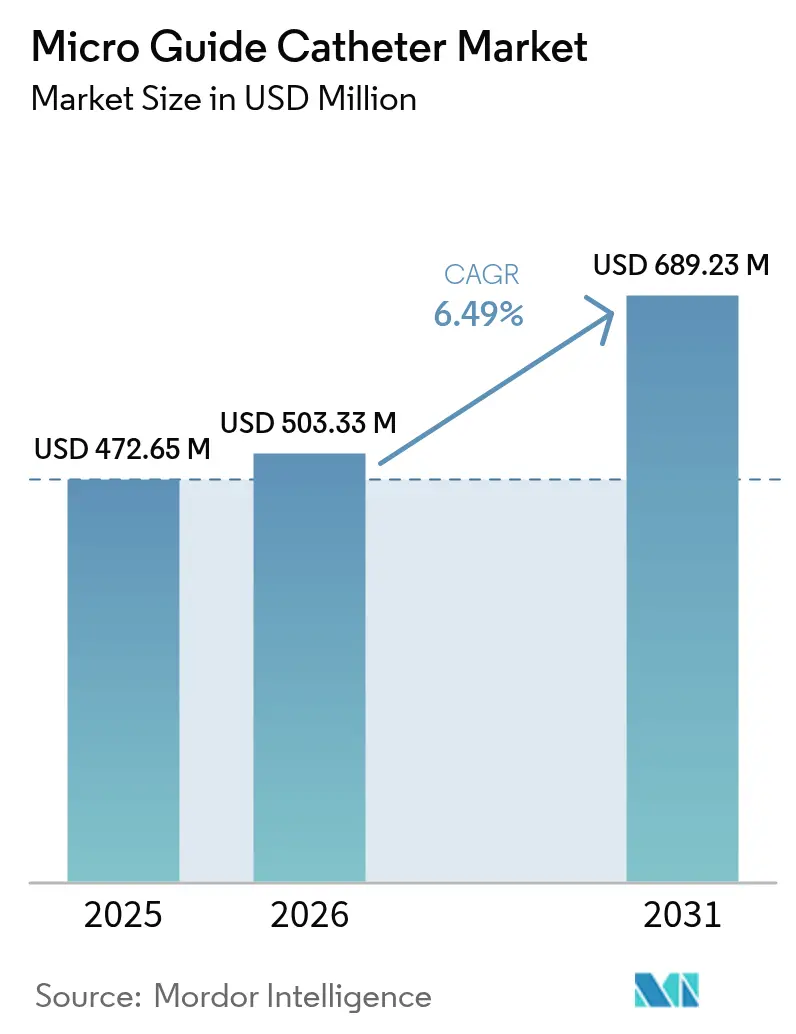

| Market Size (2026) | USD 503.33 Million |

| Market Size (2031) | USD 689.23 Million |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

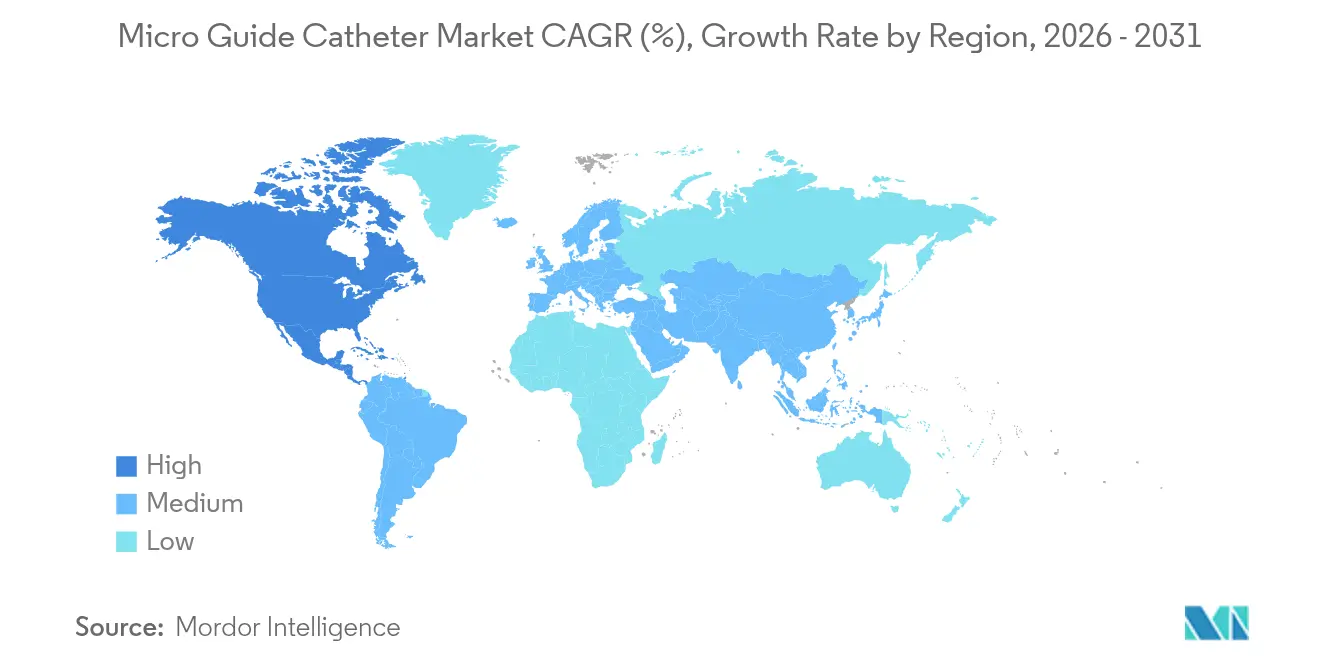

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

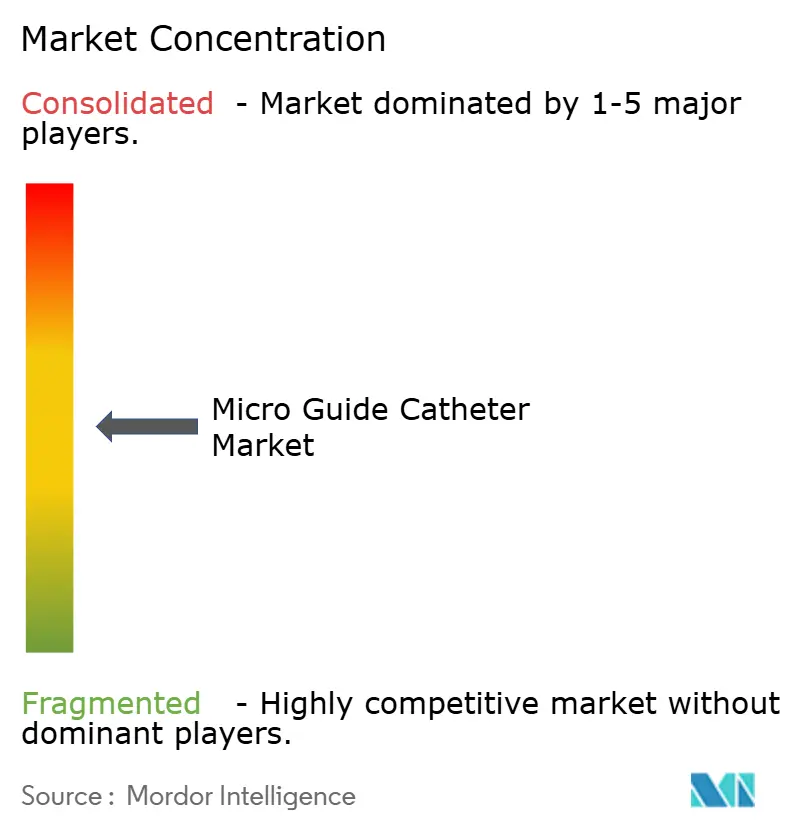

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro Guide Catheter Market Analysis by Mordor Intelligence

The micro guide catheters market size is expected to grow from USD 472.65 million in 2025 to USD 503.33 million in 2026 and is forecast to reach USD 689.23 million by 2031 at 6.49% CAGR over 2026-2031. Demand is rising because aging populations need more interventional procedures, device designs now integrate steerability and pressure-sensing, and policy makers continue to shift routine angioplasty and simple neurovascular work from inpatient suites to cost-saving ambulatory settings. Cardiovascular disease now affects 127.9 million U.S. adults, spurring hospitals to expand chronic total occlusion (CTO) programs that rely on dual-lumen and locking designs able to cross heavily calcified lesions. On the neuro side, mechanical thrombectomy guidelines recommend faster access to distal territories, and computer-assisted shaping algorithms deliver 96% first-trial success, reducing procedure time and fluoroscopy. Consolidation among OEMs, such as Boston Scientific’s USD 1.26 billion purchase of Silk Road Medical, adds scale for R&D and secures polymer supply, yet persistent PTFE shortages and resin plant outages hinder component availability.

Key Report Takeaways

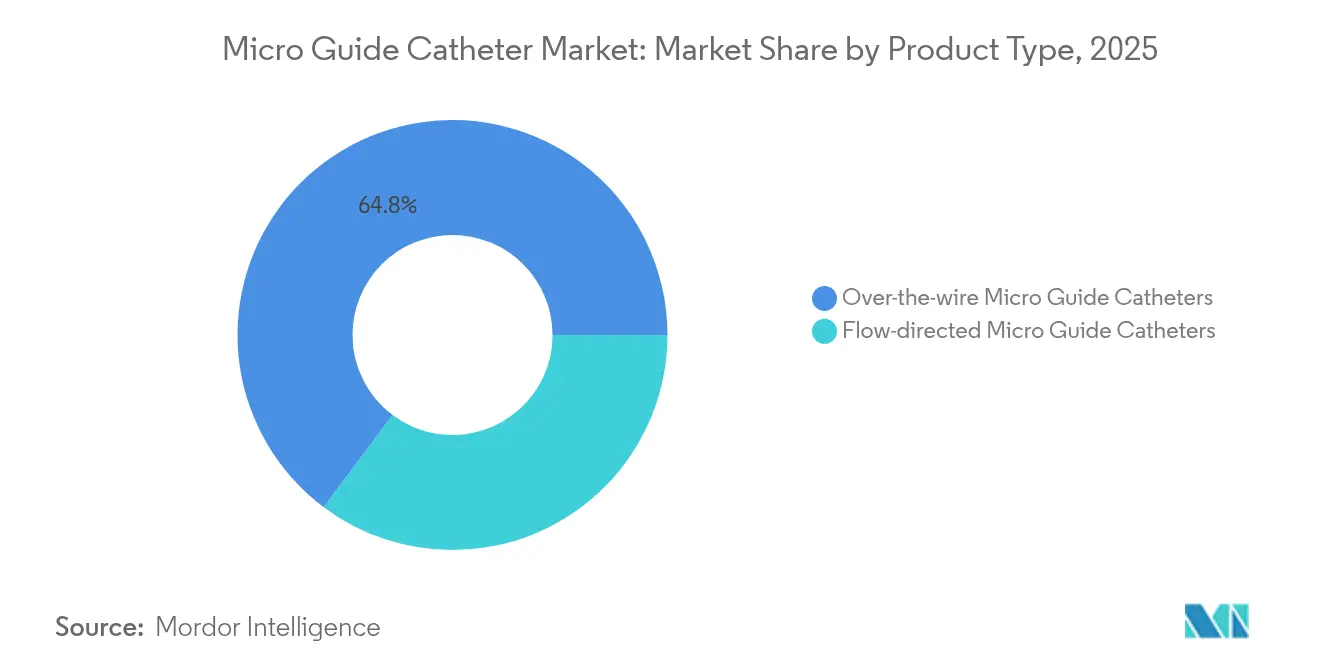

- By product type, over-the-wire devices led with 64.78% revenue share in 2025, while flow-directed units are forecast to expand at a 7.43% CAGR to 2031.

- By application, cardiovascular procedures held 45.10% of the micro guide catheters market share in 2025 and neurovascular is advancing at a 7.79% CAGR through 2031.

- By end user, hospitals and clinics accounted for 63.62% share of the micro guide catheters market size in 2025; ambulatory surgical centers are moving ahead at an 8.11% CAGR to 2031.

- By geography, North America dominated with 42.30% share in 2025, whereas Asia-Pacific is poised for the quickest 8.33% CAGR expansion to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Micro Guide Catheter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Cardiac & Neurovascular Disorders | +1.8% | Global, with highest impact in North America & APAC | Long term (≥ 4 years) |

| Rising Adoption Of Minimally-Invasive Interventions | +1.5% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Expanding Geriatric Patient Pool Worldwide | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Surge In CTO-PCI Driving Demand For Dual-/Locking Microcatheters | +1.0% | North America & EU core markets | Medium term (2-4 years) |

| Rapid Innovation In Steerable & Pressure-Sensing Microcatheters | +0.8% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Expansion Of High-Volume Ambulatory Cath Labs In EMs | +0.6% | APAC & Latin America focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden Of Cardiac & Neurovascular Disorders

Cardiovascular disease imposes USD 422.3 billion in direct costs annually on the United States and continues to rise as lifestyle risk factors intersect with aging demographics. The same pattern is unfolding across Asia-Pacific, where Hong Kong spends USD 4.6 billion and Singapore USD 8.1 billion on treatment, prompting governments to subsidize interventional programs. Increasing stroke incidence means more neurologists are training in catheter skills, and multi-disciplinary stroke teams now perform a record number of thrombectomies that depend on micro guide catheter torque response and tip flexibility. Together, these factors sustain long-run demand in the micro guide catheters market.

Rising Adoption Of Minimally-Invasive Interventions

The clinical community favors less invasive solutions such as TAVR for high-risk elderly patients; self-expanding valves posted a 9.4% combined endpoint versus 10.6% for balloon-expandable platforms in small annuli. Higher volumes of structural heart cases require microcatheters with precise pressure feedback to optimize closure device positioning. Computer-guided shaping software lowers first-pass failure from 34% to 4%, trimming fluoroscopy seconds and operator fatigue. The same digital tools inform stroke systems, where speed of access dictates neurological function, thus creating a meaningful tail-wind for micro guide catheters market growth.

Expanding Geriatric Patient Pool Worldwide

The proportion of adults aged 65+ is climbing; nearly one in six Americans will be in this cohort by 2030, while Japan already exceeds 28% [1]JACC: Advances Editorial, “Geriatric Cardiology: Four Decades of Evolution,” jacc.org. Geriatric vasculature often features tortuosity and calcification, requiring catheters with higher push-ability and kink resistance. Hydraulic steerable shafts deliver precise tip movement, a critical advantage where longer procedural times elevate stroke or bleeding risk. Early-career operators now tackle more high-risk elderly cases than seasoned peers, spotlighting a training gap that specialty microcatheters help to bridge.

Surge In CTO-PCI Driving Demand For Dual-/Locking Microcatheters

Success rates in CTO interventions have climbed to 80-90% on the back of advanced microcatheter engineering and structured proctorship programs. Locking designs such as NHancer deliver 97.5% success in lesions with low J-CTO scores, acting as the sole catheter in nearly 70% of cases. Dual-lumen units preserve side-branch flow and enable controlled re-entry techniques, making them indispensable in bifurcations. Laser-assisted catheters use 0.7 mm tips to ablate inelastic plaque at 80 mJ/mm², expanding options when balloons fail, and reinforcing the role of micro guide catheters market technology in challenging cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of highly-skilled interventional specialists | −1.2% | Global, acute in rural & emerging markets | Long term (≥ 4 years) |

| Product recalls & stringent post-market surveillance | −0.8% | North America & Europe | Short term (≤ 2 years) |

| Accuracy concerns in FFR when using microcatheters | −0.6% | Global clinical practice | Medium term (2-4 years) |

| Supply-chain volatility for high-performance polymers | −0.9% | Global manufacturing footprint | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage Of Highly-Skilled Interventional Specialists

Only one new cardiologist enters the workforce for every two that retire, limiting lab throughput in many hospitals [2]Becker’s Hospital Review Team, “Cardiology Workforce Report 2025,” . Burnout rates have escalated because reimbursement stagnates while case complexity rises. Early-career physicians contend with higher predicted mortality caseloads, reinforcing the need for intuitive catheters that shorten learning curves and improve confidence. Rural regions feel the shortfall most; hospitals ship patients hundreds of miles, delaying treatment and compressing demand for micro guide catheters market devices in underserved areas.

Supply-Chain Volatility For High-Performance Polymers

PTFE and Pebax shortages spike raw material costs by double-digit percentages and trigger allocation protocols at contract manufacturers; Arkema’s cyclododecatriene disruption cut Pebax supply by 75%. Medical device firms now spend up to 20% of revenue on logistics, prompting dual sourcing, resin stockpiles, and accelerated 3D-printing pilots. The U.S. FDA classifies pediatric catheter shortages as a public-health concern and requests proactive shortage notifications under its Resilient Supply Chain program. These constraints restrain growth until alternative chemistries receive regulatory clearance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Over-the-Wire Dominance Faces Flow-Directed Innovation

Over-the-wire configurations held 64.78% of revenue in 2025 as operators continue to favor their incremental support during prolonged balloon inflations and stent delivery. This category’s entrenched clinical familiarity keeps it at the center of CTO protocols, yet flow-directed systems are picking up pace at a 7.43% CAGR, particularly in neurovascular circles that value atraumatic distal access. Boston Scientific’s Renegade HI-FLO exemplifies design gains, posting 36.8% lower force and 7% higher flow than peers . Steerable shafts reduce wire exchanges, helping labs trim fluoroscopy and contrast.

Innovation converges on dual-lumen and tri-lumen form factors that facilitate simultaneous wire or microcoil delivery. Gore’s tri-lumen design handles up to four wires, simplifying fenestrated graft placement. Pressure-sensing lumens promise integrated physiological assessment but remain niche due to calibration limits that trail dedicated wires by 0.03 units in fractional-flow reserve accuracy. As resin suppliers stabilize capacity, manufacturers aim to merge steerability, modularity, and low-profile distal shafts into next-gen lines, ensuring the micro guide catheters market continues its shift toward versatile hybrids.

By Application: Cardiovascular Leadership Meets Neurovascular Innovation

The cardiovascular domain delivered 45.10% of 2025 sales, drawing from high-volume percutaneous coronary and peripheral arterial cases. Operators rely on robust add-on capabilities such as microcatheter-derived fractional flow reserve, which the AQVA-II study shows delivers optimal post-PCI physiology in 77% of patients compared with 54% via angiography guidance. Meanwhile, the neurovascular slice advances at 7.79% CAGR, buoyed by thrombectomy guideline revisions and embolic coil refinements. Liquid embolic agents trialed in the CLARIDAD study achieved 99% occlusion, highlighting the value of platform catheters offering progressive radiopacity fade for multi-stage interventions.

Technology transfer between subspecialties speeds progress. Magnetic microfiber bots less than 300 µm wide visualize submillimeter vessels, while MR-guided fibers forego fluoroscopy entirely, a critical win for pediatrics. Oncology and peripheral vascular indications form a nascent third pillar, and computational fluid dynamics suggests drug-eluting microcatheters could cut chemotherapy infusion times by 28%, broadening the micro guide catheters market coverage across service lines.

By End User: Hospital Dominance Challenged by ASC Expansion

Hospitals and clinics retained 63.62% of sales in 2025 thanks to round-the-clock imaging infrastructure and multidisciplinary staffing. Nevertheless, ambulatory surgical centers (ASCs) posted an 8.11% CAGR, propelled by CMS approval for coronary interventions outside hospital walls and private-equity rollups seeking predictable cash flow. Medicare data show PCI volume at ASCs rose nearly ninety-fold between 2018 and 2022 yet still represents under 1% of all claims, illustrating room for scale.

ASC adoption hinges on stringent patient selection, as operators avoid high-bleeding-risk profiles. To streamline workflow, centers deploy high-speed 256-slice CT angiography as a gatekeeper, cutting same-day cancellation rates by 22%. Catheter vendors develop kits pre-bundled with crossing, support, and exchange tools to fit condensed inventory footprints. Market momentum in this setting incentivizes device makers to craft sterilization and packaging models that align with single-use lean supply.

Geography Analysis

North America anchors 42.30% of 2025 revenue on the strength of comprehensive insurance coverage, high lab density, and rapid adoption of precision navigation features. U.S. operators perform more than 500,000 PCI cases annually, with 29% involving CTO techniques that elevate microcatheter pull-through rates. Canada adopts a hub-and-spoke approach where community hospitals send complex patients to academic centers, increasing national device turnover. Reimbursement for pressure-sensing catheters remains favorable, with CMS paying an extra USD 989 per use when documented in outpatient claims.

Asia-Pacific, projected at an 8.33% CAGR through 2031, will be the swing territory for incremental gains in the micro guide catheters market. China opens more than 250 cath labs each year, and its volume-based-procurement tenders push domestic firms toward differentiated niches like steerable distal tips to escape commodity price ceilings. Japan advances next as an aging society with universal coverage; its neutral reimbursement for novel neuro thrombectomy tools accelerates early adoption. Southeast Asian economies such as Vietnam log double-digit medical device growth rates, though they rely on imports for sophisticated micro guide catheters. Local clinical trial participation increased 65% between 2021 and 2024, enabling faster in-country registrations.

Europe presents stable mid-single-digit expansion fueled by Germany, France, and the UK. The EU Medical Device Regulation (MDR) lengthens approval cycles but raises perceived safety, supporting clinician confidence. Latin America’s fragmented payer mix tempers volume, yet Brazil’s USD 59 million vascular device market sets a foothold for premium catheters targeting private hospitals. Middle East hubs like Saudi Arabia invest in cardiac centers of excellence within Vision 2030, creating procurement contracts that often bundle imaging hardware with disposables.

Competitive Landscape

Industry consolidation has intensified, signaling a tilt toward moderate concentration. Boston Scientific bought Silk Road Medical for USD 1.26 billion, followed by its USD 664 million Bolt Medical deal, aligning a neuro-peripheral pipeline with chronic carotid work. Teleflex acquired Biotronik’s vascular unit for €760 million and now fields drug-coated balloons alongside nested dual-lumen catheters under a single IFU, winning integrated product line contracts. These roll-ups allow combined sourcing of Pebax and stainless braid, buffering raw inflation costs.

Technology is the prime differentiator. Start-ups like Vantis Vascular secured USD 5 million to miniaturize intravascular lithotripsy heads onto microcatheter shafts for calcified CTOs. Patent filings cluster around polymeric fiber optics that integrate pullback FFR measurements without separate wires, though validation remains early. White-space emerges in pediatrics where lumen diameters below 1.2 Fr require unique extrusion tolerances; no incumbent has yet achieved broad commercial scale.

Commercial strategy now revolves around hybrid sales models pairing capital equipment with disposable micro guide catheters. For example, AI software licenses bundle with sensor-enabled catheters, creating recurring revenue and device lock-in. Supplier resilience is rising on the agenda; OEMs dual-source shafts in Southeast Asia and Latin America to mitigate resin shutdown risk. Overall, players must balance R&D burn with MDR and FDA post-market surveillance costs while racing to secure ICU-light ambulatory labs as first-mover territory in the micro guide catheters market.

Micro Guide Catheter Industry Leaders

Boston Scientific Corporation

Medtronic PLC

Merit Medical Systems

Terumo Corporation

Cardinal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: BIOTRONIK and IMDS launch Micro Rx Catheter, the fourth IMDS-manufactured device distributed by BIOTRONIK in the United States.

- November 2023: Terumo Europe establishes a South African subsidiary to strengthen its international footprint.

- July 2023: ASAHI INTECC merges with Toyoflex Corporation, expanding production capacity and global reach.

Global Micro Guide Catheter Market Report Scope

As per the scope of the report, catheters are tubes made of medical-grade materials. They are used for treatment in different types of disease conditions, such as cardiovascular, gastrointestinal, urological, and neurological.

| Over-the-wire Micro Guide Catheters |

| Flow-directed Micro Guide Catheters |

| Cardiovascular |

| Neurovascular |

| Others |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Over-the-wire Micro Guide Catheters | |

| Flow-directed Micro Guide Catheters | ||

| By Application | Cardiovascular | |

| Neurovascular | ||

| Others | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Micro Guide Catheter Market size?

The micro guide catheters market size is USD 503.33 million in 2026 and is forecast to reach USD 689.23 million by 2031.

Who are the key players in Micro Guide Catheter Market?

Boston Scientific Corporation, Medtronic PLC, Merit Medical Systems, Terumo Corporation and Cardinal Health Inc. are the major companies operating in the Micro Guide Catheter Market.

Which product type leads revenue today?

Over-the-wire designs held 64.78% of revenue in 2025, reflecting clinician familiarity and broad clinical indications.

How does Asia-Pacific compare with North America?

North America retains 42.30% of 2025 revenue, but Asia-Pacific will grow faster at 8.33% CAGR through 2031 as hospital capacity and disease incidence climb.

Page last updated on: