Trail Running Shoes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

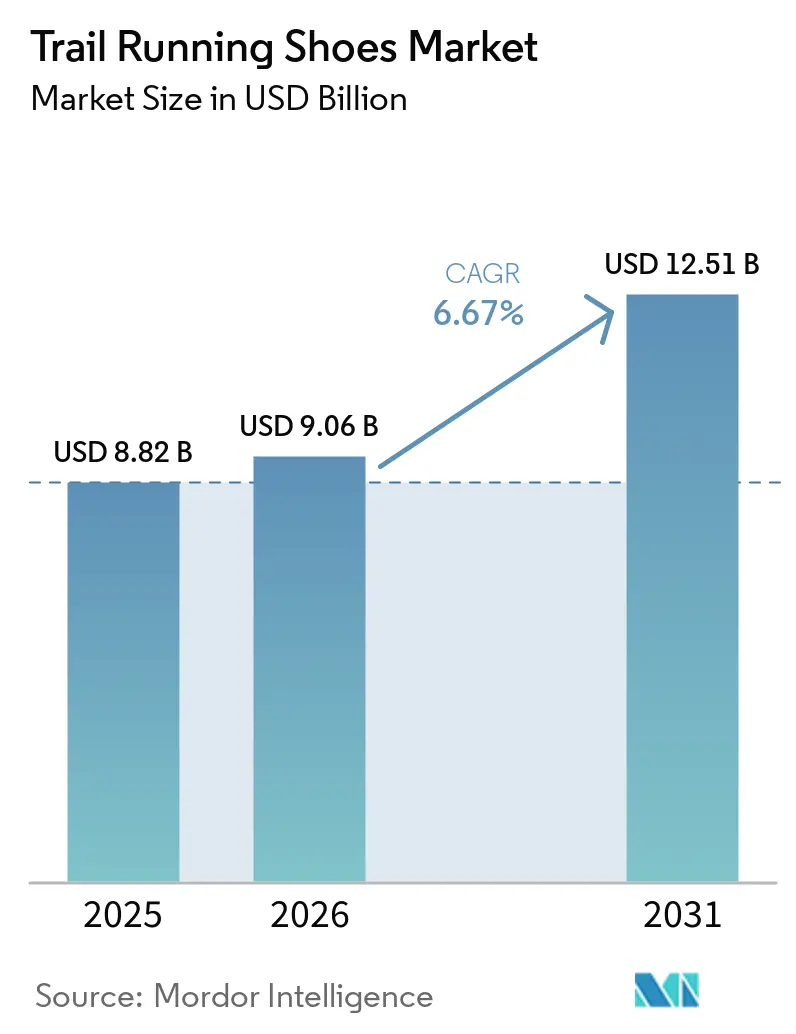

| Market Size (2026) | USD 9.06 Billion |

| Market Size (2031) | USD 12.51 Billion |

| Growth Rate (2026 - 2031) | 6.67% CAGR |

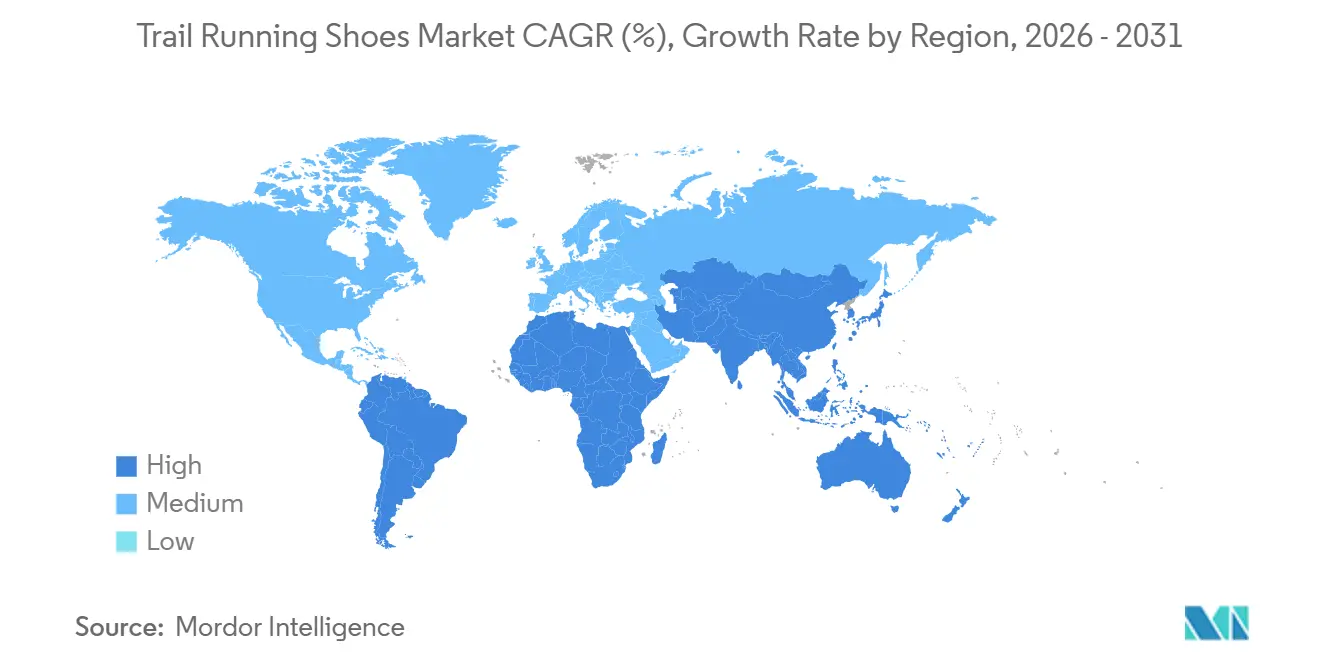

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trail Running Shoes Market Analysis by Mordor Intelligence

The Trail Running Shoes market size is expected to increase from USD 9.06 billion in 2026 to USD 12.51 billion by 2031, growing at a CAGR of 6.67% over 2026-2031. Steady gains reflect a structural migration from road to off-road running as health-minded consumers look for low-impact exercise that blends fitness with nature. Rising female participation, broader Gen Z and Millennial engagement, and a swelling race calendar all reinforce volume growth, while rapid product refreshes allow brands to defend premium price points. Continuous improvement in foam chemistry, plate geometry, and outsole rubber keeps replacement rates high, and the surging popularity of women-centric trail communities is widening the addressable base. Counterfeiting, supply volatility in specialty rubber compounds, and elevated average selling prices remain headwinds, yet brands that marry innovation with tiered price ladders protect both volume and margin.

Key Report Takeaways

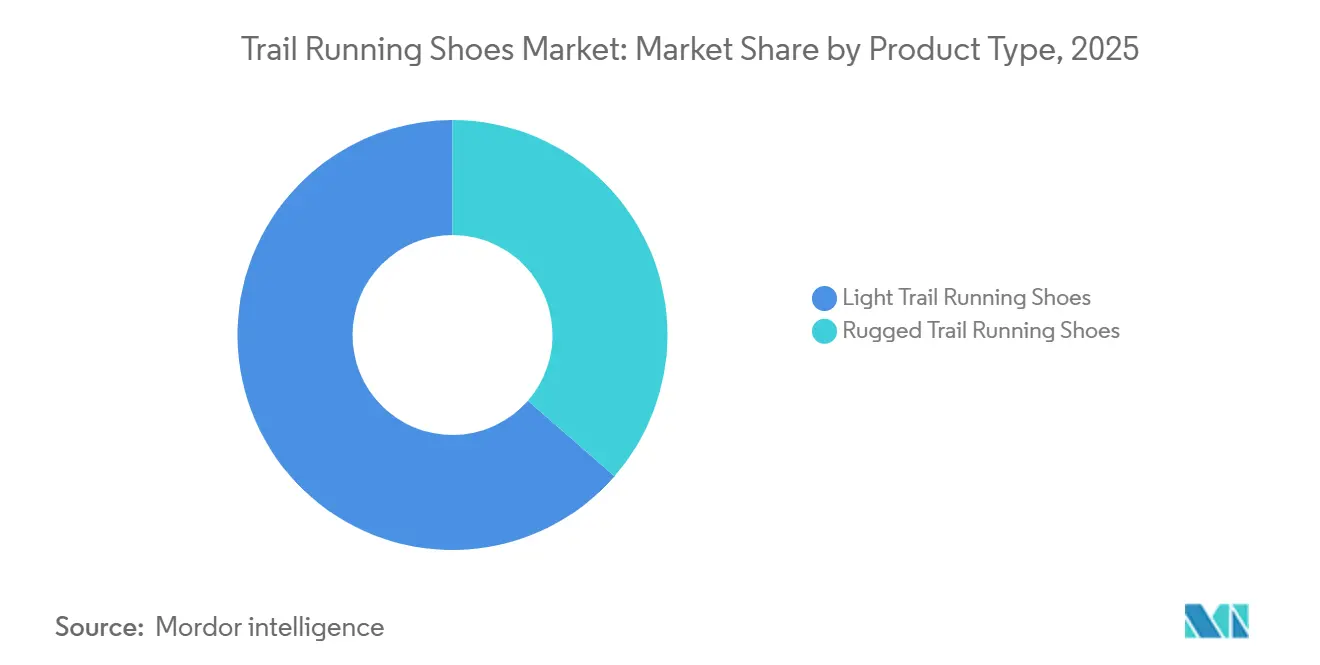

- By product type, Light Trail Running Shoes led with 63.59% of the Trail Running Shoes market share in 2025, while Rugged Trail Running Shoes are projected to expand at a 7.08% CAGR through 2031.

- By End User, Men represented 56.69% of end-user demand in 2025, yet Women are forecast to grow at a 6.97% CAGR.

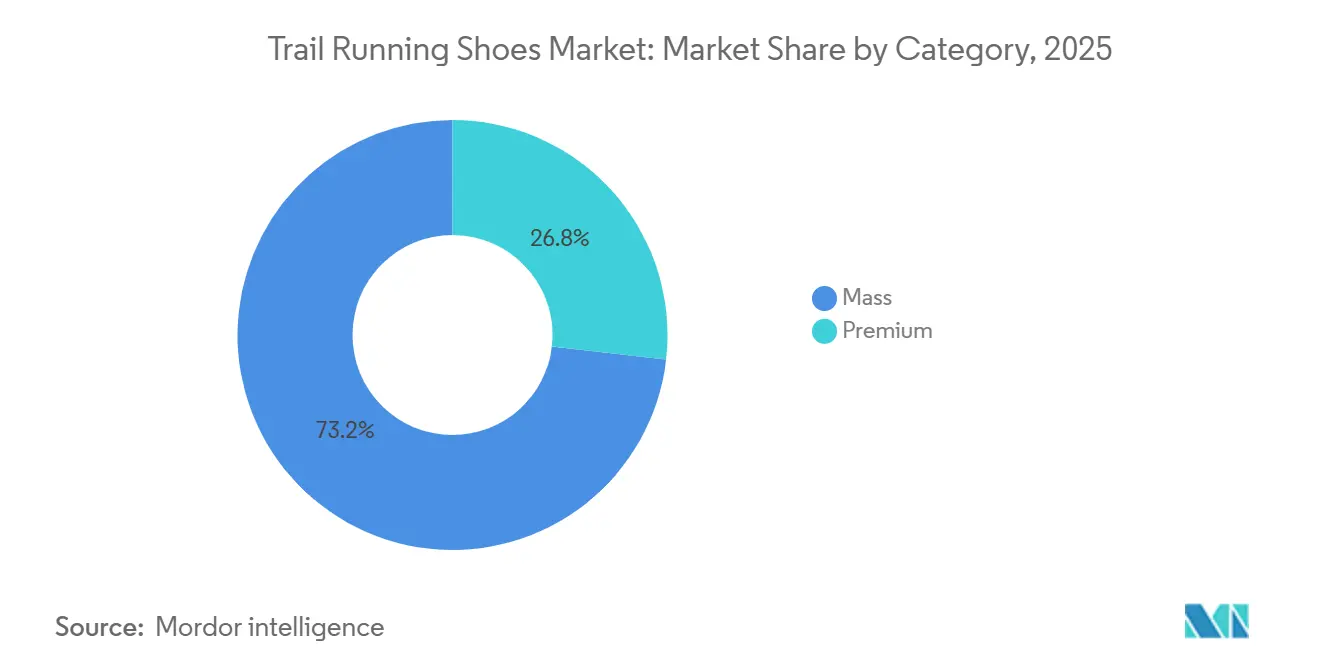

- By Category, Mass-category footwear captured 73.18% of the Trail Running Shoes market size in 2025, while Premium offerings are set to advance at a 7.07% CAGR.

- By Distribution Channel, Specialty Stores held 35.72% share of the Trail Running Shoes market size in 2025; Online Retail Stores will climb at a 7.81% CAGR to 2031.

- By Geography, North America held 35.40% share of the Trail Running Shoes market size in 2025; Asia-Pacific will climb at a 7.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Trail Running Shoes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health-and-wellness focus | +1.2% | Global, with the strongest gains in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Outdoor recreation and trail-race participation on the rise | +1.5% | Global, led by North America, Europe, and China | Short term (≤ 2 years) |

| Continuous innovation in lightweight and traction tech | +1.0% | Global, research and development concentrated in North America and Europe | Long term (≥ 4 years) |

| Expansion of online and specialty retail channels | +0.9% | Global, fastest in Asia-Pacific and North America | Medium term (2-4 years) |

| Shift toward eco-friendly and recycled uppers | +0.7% | Europe, North America, and spillover to Asia-Pacific | Long term (≥ 4 years) |

| New SKUs driven by women-centric trail communities | +0.8% | Global, with early momentum in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health-and-Wellness Focus

Health-driven motivations are reshaping the trail running demographic, drawing participants from sedentary lifestyles and road running into technical outdoor environments. In 2024, the U.S. saw 15.1 million trail running participants, marking an 8.5% year-over-year increase. Female participation rose from 51.9% to 53.2%, with Gen Z and Millennials making up the bulk of newcomers, as reported by the Sports & Fitness Industry Association[1]Source: Sports & Fitness Industry Association, “2024 U.S. Participation Report,” sfia.org. In 2025, Japan's trail running community, as noted by the Japan Trail Running Association, highlighted health improvement as a key motivator. The country is witnessing a "third wave" of growth, characterized by younger generations and an increasing number of women joining the sport. This demographic shift is significant; it alters product demands from elite-performance features to a focus on comfort, injury prevention, and adaptability for both road and trail use. Brands that incorporate cushioning, wider toe boxes, and lower drop profiles at accessible price points stand to gain the most from this wellness-focused group. In contrast, brands that remain solely race-centric may lose ground to competitors who cater to a more lifestyle-oriented audience.

Outdoor Recreation and Trail-Race Participation on the Rise

Trail racing, once a niche ultra-distance event, has evolved into a global phenomenon with multiple entry tiers, driving a consistent demand for specialized footwear. In 2025, the UTMB World Series saw 146,933 runners participate in 55 events across 28 countries, with female runners making up 30% of the total, a rise from 25% in 2022. France, as reported by European Athletics, recorded 1.44 million trail race results in 2025, marking a 150% surge over the last decade, and played host to around 6,000 trail races. China's trail racing scene has seen a meteoric rise, expanding to about 500 events in 2025, up from just 65 in 2014. This sevenfold growth has been bolstered by domestic brands like KAILAS, which boasted a wear rate surpassing 40% at major races. The International Trail Running Association highlighted a significant leap in ITRA-sanctioned events, jumping from roughly 1,300 in 2012 to over 7,000 globally in 2024. This growth underscores trail racing's organizational maturity, paving the way for sustained year-over-year participant increases. Brands that strategically sponsor event series, engage in athlete-testing feedback, and synchronize product launches with race calendars stand to gain heightened visibility and conversion rates.

Continuous Innovation in Lightweight and Traction Tech

Brands are increasingly turning to midsole foam chemistry and outsole-rubber collaborations as key differentiators, often seeking proprietary compounds and exclusive supplier ties to carve out performance advantages. Nike's ZoomX foam boasts an impressive 85% energy return. Meanwhile, Nike's ReactX compound has achieved a notable 43% reduction in carbon footprint compared to its earlier EVA formulations. In 2025, Vibram rolled out Megagrip Elite, an upgraded version of its Megagrip compound. The company also broadened its ECOSTEP range, a lineup of recycled rubber formulations, producing a staggering 42 million pairs and raking in revenues of EUR 279 million (around USD 295 million). Adidas, in 2025, unveiled its Lightstrike Pro Evo midsole foam, touting a 50% weight cut from its predecessor and an 11% boost in forefoot energy return. HOKA's Rocker Integrity Technology integrates a curved TPU plate within dual-density EVA foams. This innovation not only preserves the rocker geometry over time but also diminishes fatigue and injury risks for ultra-runners, all while offering a plush ride akin to the brand's Clifton and Speedgoat lines. Such advancements empower brands to set premium price tags. For context, models featuring carbon plates and these exclusive foams command prices exceeding USD 250. Moreover, these innovations erect formidable barriers for smaller competitors, who often lack the necessary research, development budgets, or supplier alliances.

Expansion of Online and Specialty Retail Channels

Brands are increasingly turning to direct-to-consumer and e-commerce channels to reshape their margin structures and enhance customer acquisition. This shift allows them to sidestep wholesale markdowns and gain valuable first-party data. In 2025, Amer Sports, the parent company of Salomon, revealed that direct-to-consumer sales constituted 41% of its revenue, a notable rise from 33% in 2024. The brand also expanded its footprint by opening over 50 stores in Greater China. Additionally, in a strategic move, Amer Sports partnered with Warner Bros. Discovery to broadcast the Golden Trail Series, reaching an impressive 687 million potential viewers across 90 territories. Brooks, another key player, celebrated a 16% global revenue growth in 2025, attributing much of its success to direct-to-consumer sales and specialty retail partnerships. On Running reported a significant 39% surge in direct-to-consumer sales for the quarter ending March 31, 2026. These sales now make up 37.5% of the brand's total volume, with a gross profit margin nearing 60%. Strava boasts a user base of 125 million, predominantly comprising Gen Z and Millennials. This demographic advantage translates to a 23% increased likelihood of purchasing HOKA products within 30 days of campaign exposure, as highlighted by Deckers Outdoor Corporation[2]Source: Deckers Outdoor Corporation, “2026 Investor Day Presentation,” deckers.com . While specialty stores held onto 35.72% of the distribution share in 2025, thanks to their expertise and immediate product access, online retail is poised for growth. With an anticipated CAGR of 7.81% through 2031, brands are integrating virtual try-on tools, subscription models, and influencer partnerships into their digital storefronts.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit and grey-market products | -0.9% | Global, concentrated in Europe, Asia-Pacific, Middle East | Short term (≤ 2 years) |

| Specialty-rubber supply volatility (e.g., Megagrip) | -0.5% | Global supply is concentrated in Italy and Asia | Medium term (2-4 years) |

| Concerns over injury liability and technical terrain | -0.4% | North America, Europe (litigation-prone markets) | Long term (≥ 4 years) |

| High average selling point compared to road-running footwear | -0.8% | Global, most acute in price-sensitive Asia-Pacific and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit and Grey-Market Products

Counterfeit trail running shoes not only undermine brand equity and erode profit margins but also expose consumers to substandard materials, heightening the risk of injuries. This situation creates both regulatory challenges and reputational damage for legitimate manufacturers. In a significant crackdown, the European Union Intellectual Property Office's Operation Fake Star II led to the seizure of over 8 million counterfeit products, resulting in 264 arrests and involving over 500 brands[3]Source: European Union Intellectual Property Office, “Operation Fake Star II Report,” euipo.europa.eu. Notably, footwear constituted a substantial portion of the confiscated items. In 2025, authorities at Dublin Port intercepted 9,156 counterfeit Nike pairs, with a valuation of EUR 1.6 million (around USD 1.7 million), as reported by the Revenue Commissioners of Ireland. An investigation by Indonesia's Trade Ministry uncovered a monthly import of 5,000 to 8,000 counterfeit footwear pairs and a staggering USD 392 million discrepancy in trade data. This pointed to sophisticated supply chains, tracing back to origins in Putian and Guangzhou. Furthermore, a briefing from the International Trademark Association underscored the evolution of counterfeit networks, which have now embraced advanced manufacturing techniques. This advancement complicates visual detection, prompting brands to pivot towards blockchain-based authentication, RFID tagging, and heightened consumer education initiatives. Meanwhile, the U.S. Shop Safe Act, as proposed by Congress, aims to make e-commerce platforms accountable for counterfeit listings. While this move could curtail grey-market availability, it also threatens to escalate compliance costs for online marketplaces.

High Average Selling Point Compared to Road-Running Footwear

Trail running shoes, equipped with specialized outsole compounds, rock plates, and reinforced uppers, command a premium over their road counterparts. However, this price premium poses challenges for price-sensitive consumers, hindering market expansion in emerging economies. On average, trail shoes retail for USD 150, with high-end carbon-plated variants surpassing USD 250. In contrast, mainstream road running shoes are priced between USD 100 and USD 130. In 2025, NOBULL's trail and outdoor segment generated USD 112 million, marking a 46% year-over-year growth. This surge was bolstered by an average selling price of USD 126, following the brand's introduction of technical upgrades. HOKA's Cielo X1, priced at USD 275, and the Skyward X at USD 225, firmly establish both models at the pinnacle of performance and comfort. This pricing strategy effectively divides the market: premium buyers prioritize performance and sustainability, while mass buyers seek functional footwear at accessible prices. Brands neglecting a tiered product portfolio risk ceding ground to competitors offering entry models under USD 100. This is especially pertinent in regions like Asia-Pacific and South America, where disposable income and trail infrastructure lag behind North America and Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Technical innovation propels rugged segment momentum

In 2025, light trail shoes dominate the trail running footwear market, capturing 63.59% of the segment revenue. These shoes are the go-to choice for newcomers to trail running, especially those transitioning from urban settings to occasional wooded trails. Priced competitively, thanks to efficient production scales, they align closely with everyday trainers, appealing to a mass-market audience. Fashion trends, notably the media-driven "gorpcore," have heightened the demand for these lightweight, urban-centric designs, leading to rapid sales turnover, particularly in cities. Capitalizing on this trend, industry players have broadened their product lines, enabling consumers to transition smoothly from lighter models to more technical ones as their running expertise grows. The light trail category thrives on its widespread appeal, value-centric offerings, and prominent visibility in both fashion and running circles.

The rugged or technical trail shoe segment is on an impressive upswing, with projections indicating a 7.08% compound annual growth rate through 2031. This growth is driven by innovations like Carbitex DFX plates and rock-shield constructions, which enhance stability and protection on rugged terrains, catering to the rising number of ultra-marathoners. High-profile events, such as the UTMB World Series, boost demand for specialized features, including advanced lug patterns and hybrid foams. Premium sub-categories in this segment, with average selling prices exceeding USD 190, boast features like water-resistant knit collars, vibration-damping plates, and 3D-printed midsoles. Investments in abrasion-resistant rubber compounds facilitate the production of exclusive limited editions, generating excitement and fostering brand loyalty among dedicated users. Collaborative designs between brands and top athletes further drive innovation, solidifying the technical segment's prominence and its pivotal role in shaping industry standards and brand value.

By End User: Women accelerate demographic diversification

Trail running shoe sales are led by men, who command a 56.69% share of the market's revenue. While men still dominate sales figures, the women's segment is catching up, showing a faster year-on-year growth. Shoes designed for men often boast a diverse array of performance features and styles, appealing to both seasoned and casual runners. Marketing campaigns frequently spotlight endurance, durability, and cutting-edge technology, resonating with the brand's loyal male audience. Even with this slower growth pace, men's trail running shoes hold a robust position, spanning both entry-level and premium offerings. Given the high participation rates and deep-rooted brand loyalty among men, this segment is poised to continue its revenue dominance for the foreseeable future.

Women are rapidly emerging as a dominant force in the trail running shoes market, with their segment growing at an impressive 6.97% CAGR, outstripping the industry's overall pace. Brands are fine-tuning their products to align with female biomechanics, introducing features like wider forefoot platforms and tailored heel-to-toe drops. Marketing campaigns are increasingly showcasing female athletes conquering ultra and sub-ultra races, effectively breaking down psychological barriers and boosting participation. Retail insights reveal that women tend to replace their shoes 15% sooner than men, a trend linked to their higher mileage on varied terrains, leading to more frequent purchases. Moving away from conventional male-centric designs, brands are now offering inclusive sizing and a broader spectrum of colors. Partnerships with women's trail running groups facilitate swift feedback and innovation, while initiatives targeting younger audiences cultivate early brand loyalty. Consequently, the women's segment is on track to grow, signaling a broader market reach and bolstering the industry's resilience.

By Category: Premium positioning sustains value creation

In 2025, the mass segment dominates the trail running shoes market, generating 73.18% of total revenue. This segment primarily features budget-friendly models priced under USD 140, catering to novice runners and urbanites drawn to trendy designs. Retailers often turn to private-label brands in this segment to drive sales and solidify their market presence. With widespread distribution across diverse retail channels, the mass segment ensures steady demand, bolstering the industry's overall scale. Yet, challenges like currency fluctuations and potential tariff hikes could narrow the price divide between mass and premium tiers, swaying consumer buying habits. In response, companies are crafting mid-tier lines that merge affordability with select premium features, easing the transition for customers eyeing an upgrade in the trail running shoes market.

The premium segment is the fastest-growing category, boasting a notable CAGR of 7.07% projected through 2031. Shoppers in this segment are ready to pay for tangible performance boosts, as seen with On Running’s 170-gram carbon-plate shoe, retailing at USD 275. Sustainability plays a pivotal role in the premium segment's appeal, with eco-friendly innovations like Norda™’s bio-based Dyneema uppers and On’s LightSpray technology resonating with green-minded athletes. To bolster their premium pricing, brands are also offering bundled services, including digital training programs and extended warranties. The segment's high profit margins fuel continuous research and development, leading to advancements like graphene-enhanced outsoles and adaptive cushioning systems. This cycle of innovation not only boosts product performance but also elevates brand prestige, propelling the segment's growth and its prominence in the trail running shoes market.

By Distribution Channel: Digital engagement redefines purchase journeys

Specialty stores dominate the trail running shoes market, capturing 35.72% of total sales. Their success hinges on expert gait analysis and curated inventories, crucial for injury prevention and ensuring a perfect fit. In-store try-ons let runners test grip on simulated rocky surfaces, slashing product return rates. Retail staff, trained by biomechanics specialists, offer tailored recommendations on insoles and advanced lacing techniques, boosting average transaction values. Many specialty chains have set up shop in bustling trail locations, hosting events like demo days and athlete talks, strengthening bonds with local running communities. This blend of expert service and community involvement cements specialty stores as a cornerstone of the trail running shoe market.

Online retail is rapidly emerging as the dominant force in the trail running shoes market, with projections indicating a robust 7.81% CAGR through 2031. E-commerce platforms boast a broader product range and real-time inventory updates, outpacing physical stores. Cutting-edge virtual try-on technologies, leveraging smartphone cameras to analyze foot shape, enhance first-time purchase accuracy, and reduce return rates. Online marketplaces often clinch exclusive colorways, drawing in both collectors and fashion-forward consumers. Targeted ads via retail media networks, embedded in running communities, achieve conversion rates exceeding 4.5%, outstripping the norm for sporting goods. Moreover, services like buy-online-pick-up-in-store and locker pickups are crafting a fluid omnichannel experience, underscoring the digital realm's pivotal role in the trail running shoes market's growth and consumer appeal.

Geography Analysis

In 2025, North America accounted for 35.40% of global revenue, driven by a robust outdoor infrastructure and high discretionary spending. College-level cross-country programs are now integrating trail intervals into their training, introducing athletes to off-road footwear and fostering familiarity with trail-specific gear. According to the American Trail Running Association, nearly 48% of North American consumers run 3 to 5 times a week, highlighting a strong culture of recreational and competitive running. While proposed import tariffs introduce short-term volatility, brands are proactively diversifying their sourcing strategies by reducing reliance on single-country suppliers and expanding assembly operations within North America. These measures aim to cushion potential price shocks and maintain market stability.

Europe is witnessing a pronounced shift towards sustainability, with consumers increasingly opting for premium products that align with environmental norms. In 2024, ASICS launched its circular-design NIMBUS MIRAI shoe and the NEOCURVE sneaker, crafted from reclaimed deadstock, both making their debut in Europe. These innovations reflect the region's growing demand for eco-friendly and high-performance footwear. PUMA, capitalizing on trust built through stringent third-party certifications, has integrated 90% recycled materials into its footwear line, setting a benchmark for sustainable practices in the industry. Additionally, the alpine trail networks in France, Italy, and Switzerland are driving demand for technical footwear, especially those with advanced lug patterns tailored for diverse terrains like scree, snow, and forest paths. These networks not only support recreational activities but also attract professional athletes, further boosting the market.

Asia-Pacific is emerging as the fastest-growing region, boasting a 7.82% CAGR. Japan's Onitsuka Innovative Factory project underscores the region's dedication to high-value production and craftsmanship, facilitating agile manufacturing for limited-series trail shoes. This initiative highlights the region's focus on blending traditional expertise with modern manufacturing techniques. Urbanization, coupled with government-backed fitness initiatives like city-trail campaigns in Beijing and Seoul, is broadening access to nearby trailheads, encouraging more individuals to adopt trail running. Furthermore, cross-border e-commerce platforms are bridging the gap, enabling Asian consumers to snag new models just days after their Western launches. This streamlined access to global product releases is significantly amplifying demand and fostering a more connected consumer base.

Competitive Landscape

Competition in the trail running shoes market is moderately concentrated, suggesting that no single player dominates and that innovation, rather than sheer scale, is the key to leadership. While Nike and Adidas maintain significant market visibility, they're increasingly challenged by specialists like Hoka, On Running, and Brooks. Nike's 2024 launch of the Ultrafly trail shoe, featuring carbon-plate technology, underscores how established players are adapting road-running research and development to niche markets. On Running, on the other hand, is bolstering its premium image by expanding its LightSpray low-carbon manufacturing, showcasing its commitment to process innovation.

Newer brands are carving out niches in sustainability and designs tailored for women. Brands like Norda™, Speedland, and Zen Running Club are pushing the envelope in material science, experimenting with bio-based yarns, modular components, and recyclable midsoles. Their strategy of limited production fosters exclusivity, allowing them to command prices exceeding USD 250. In a different vein, PUMA's direct-to-consumer approach yielded a 17.3% surge in e-commerce sales in Q1 2025. The brand is eyeing an 8.5% EBIT margin by 2027, banking on cost optimizations while still prioritizing innovation. ASICS, meanwhile, is not only championing circular economy principles but is also introducing gender-adaptive fits, aiming to broaden its appeal among casual runners.

Brands are leveraging strategic partnerships with event organizers, tech suppliers, and sustainability certifiers to amplify their reach. For instance, Carbitex teamed up with Speedland to embed DFX carbon plates, tailored for rugged terrains, setting them apart in the market. Sponsoring high-profile events like the Golden Trail World Series allows brands to gain valuable product feedback and media visibility. Collaborations with retailers like Dick’s Sporting Goods and JD Sports enhance physical presence, catering especially to consumers who value the try-before-you-buy experience. In conclusion, success in the trail running shoes market hinges on agility in material innovation, channel optimization, and community engagement, presenting opportunities for disruptors to make their mark.

Trail Running Shoes Industry Leaders

Amer Sports

Deckers Outdoor Corporation

Nike Inc

Adidas AG

ASICS Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nike unveiled the Ultrafly trail racing shoe, marking its inaugural foray into off-road footwear. This model boasts a carbon plate, dubbed the "Flyplate," and a Vibram outsole, both tailored for racing on diverse terrains. Priced at approximately $250, the Ultrafly is aimed squarely at trail athletes.

- January 2025: ASICS revealed plans to rebrand its domestic manufacturing arm as Onitsuka Innovative Factory Corporation. This move pivots the facility into a specialized production center for the premium Onitsuka Tiger brand, adopting a cohesive production model.

- November 2024: INOV8 introduced its latest trail running shoe lineup: TRAILTALON, TRAILTALON GTX, and TRAILTALON SPEED. Each model in the TRAILTALON series showcases INOV8’s innovative anatomical foot-shaped design, ensuring an enhanced locked-in fit. These new offerings hit the shelves across the United Kingdom and other regions where the brand operates.

Global Trail Running Shoes Market Report Scope

A trail running shoe is a specialized athletic shoe designed for off-road environments like dirt paths, rocky terrain, and forest trails. The trail running shoe market is segmented by product type, end user, category, distribution channel, and geography. By product type, the market is segmented into light trail shoes and rugged/technical trail shoes. By end user, the market is segmented into men, women, and kids. By category, the market is segmented into mass and premium. By distribution channel, the market is segmented into online retail stores, specialty stores, supermarkets/hypermarkets, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Light Trail Running Shoes |

| Rugged Trail Running Shoes |

| Men |

| Women |

| Kids |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Light Trail Running Shoes | |

| Rugged Trail Running Shoes | ||

| End User | Men | |

| Women | ||

| Kids | ||

| Category | Mass | |

| Premium | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Trail Running Shoes market be by 2031?

The Trail Running Shoes market size is projected to reach USD 12.51 billion by 2031, expanding at a 6.67% CAGR from 2026 to 2031.

Which product segment grows the fastest to 2031?

Rugged Trail Running Shoes are forecast to expand at a 7.08% CAGR thanks to the rising number of ultra-distance events and technical races.

What region leads growth over the forecast period?

Asia-Pacific posts the strongest regional CAGR at 7.82%, led by China’s expanding event calendar and rising female participation.

Which channels will gain the most share in the coming years?

Online Retail Stores will climb at a 7.81% CAGR to 2031 as direct-to-consumer platforms, virtual try-on tools, and social engagement boost digital conversion.

Page last updated on: