Basketball Shoe Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

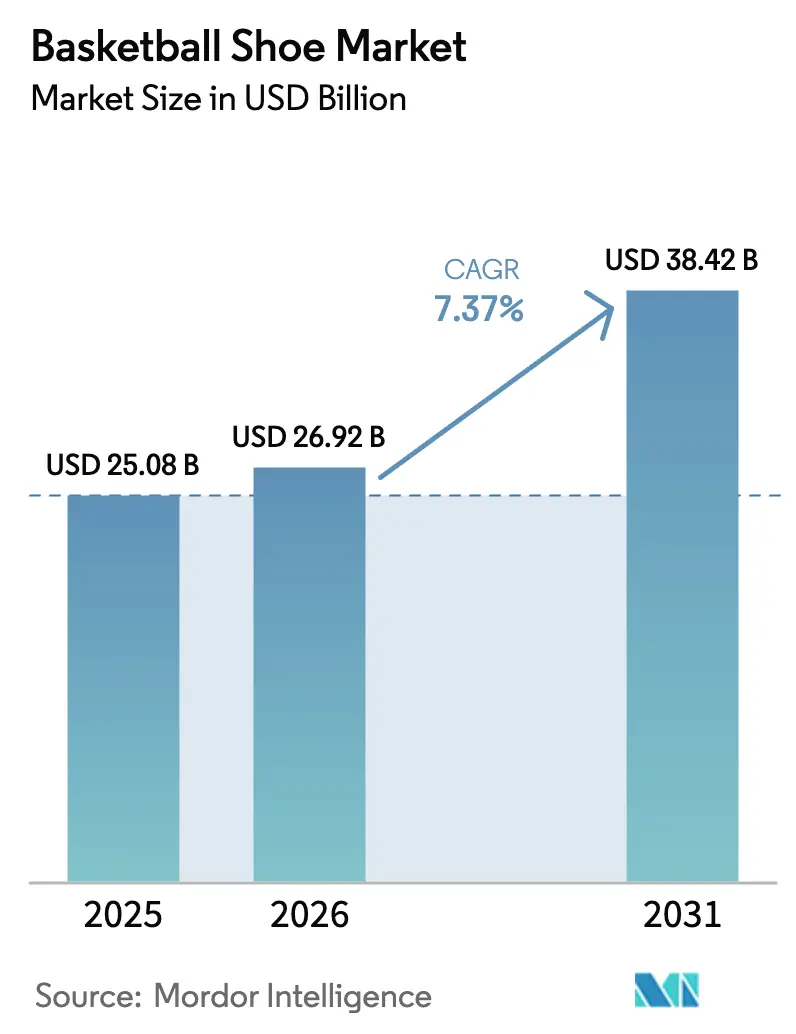

| Market Size (2026) | USD 26.92 Billion |

| Market Size (2031) | USD 38.42 Billion |

| Growth Rate (2026 - 2031) | 7.37% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Basketball Shoe Market Analysis by Mordor Intelligence

The basketball shoe market size is projected to expand from USD 25.08 billion in 2025 and USD 26.92 billion in 2026 to USD 38.42 billion by 2031, registering a CAGR of 7.37% between 2026 to 2031. The market is experiencing significant growth driven by the globalization of professional leagues, the expansion of youth participation infrastructure, and the increasing efficiency of direct-to-consumer channels that enable brands to monetize basketball culture effectively. North America remained the primary revenue contributor in the year 2025; however, the Asia-Pacific region's projected compound annual growth rate highlights a shift in geographic focus. This growth is supported by Chinese brands localizing performance narratives and global players strengthening regional collaborations. Low-top basketball shoes are gaining popularity as younger athletes prioritize mobility and lightweight designs. Additionally, the rising demand for premium products indicates that consumers are willing to spend over one hundred sixty United States dollars when marketing strategies, such as star-athlete storytelling, resonate with them. Online channels, which already dominate repeat purchases, are further benefiting from data-driven product curation, targeted product launches, and rapid restocking of colorways, advantages that traditional brick-and-mortar stores struggle to replicate.

Key Report Takeaways

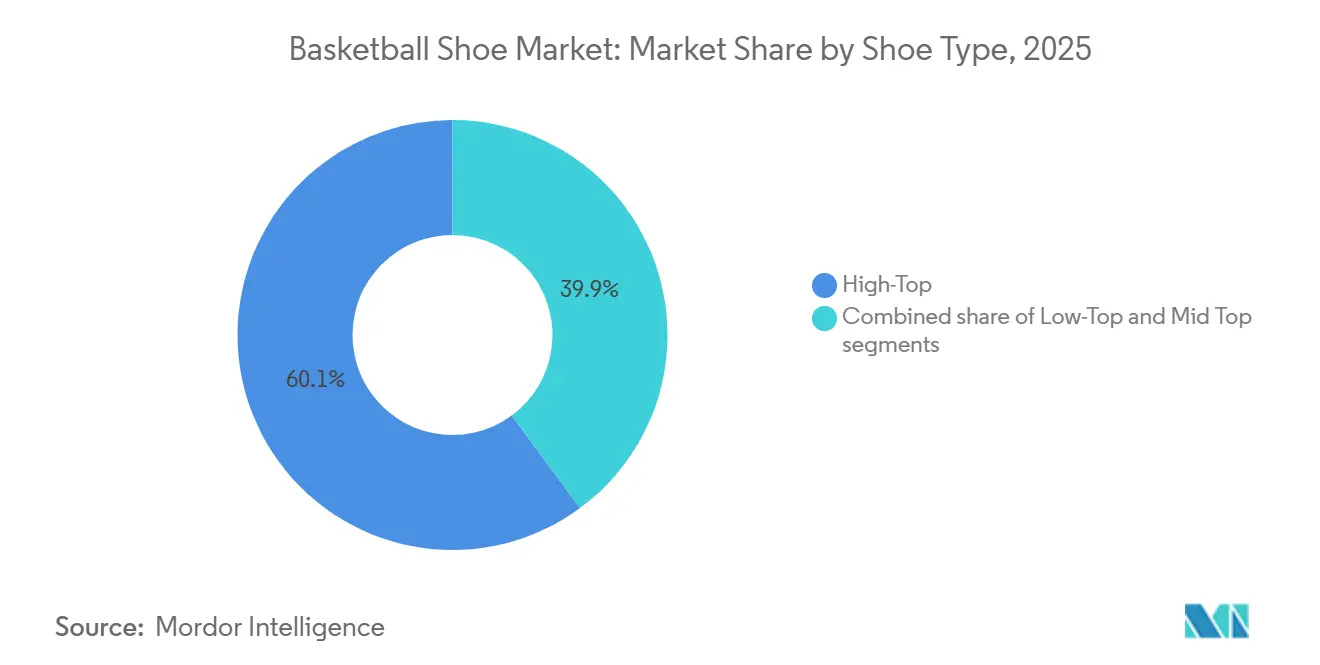

- By shoe type, high-top shoes held 60.11% of 2025 volume, while low-tops are projected to expand at an 8.61% CAGR through 2031.

- By end user, men accounted for 60.63% of 2025 sales, but the kids segment is forecast to grow at 7.91% during 2026-2031.

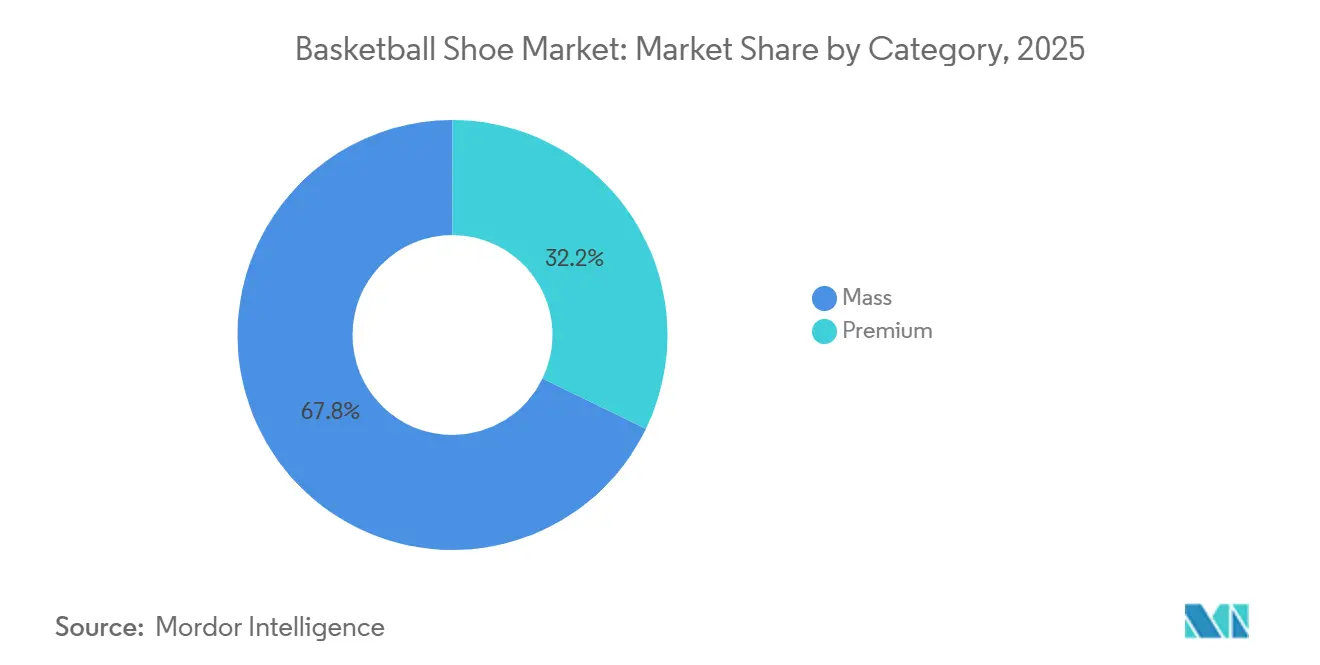

- By category, mass category secured 67.82% of 2025 revenue, yet premium lines are anticipated to advance at an 8.33% CAGR to 2031.

- By distribution channel, sports and specialty stores captured 38.92% of 2025 value, whereas online retail is expected to progress at an 8.98% CAGR over the forecast period.

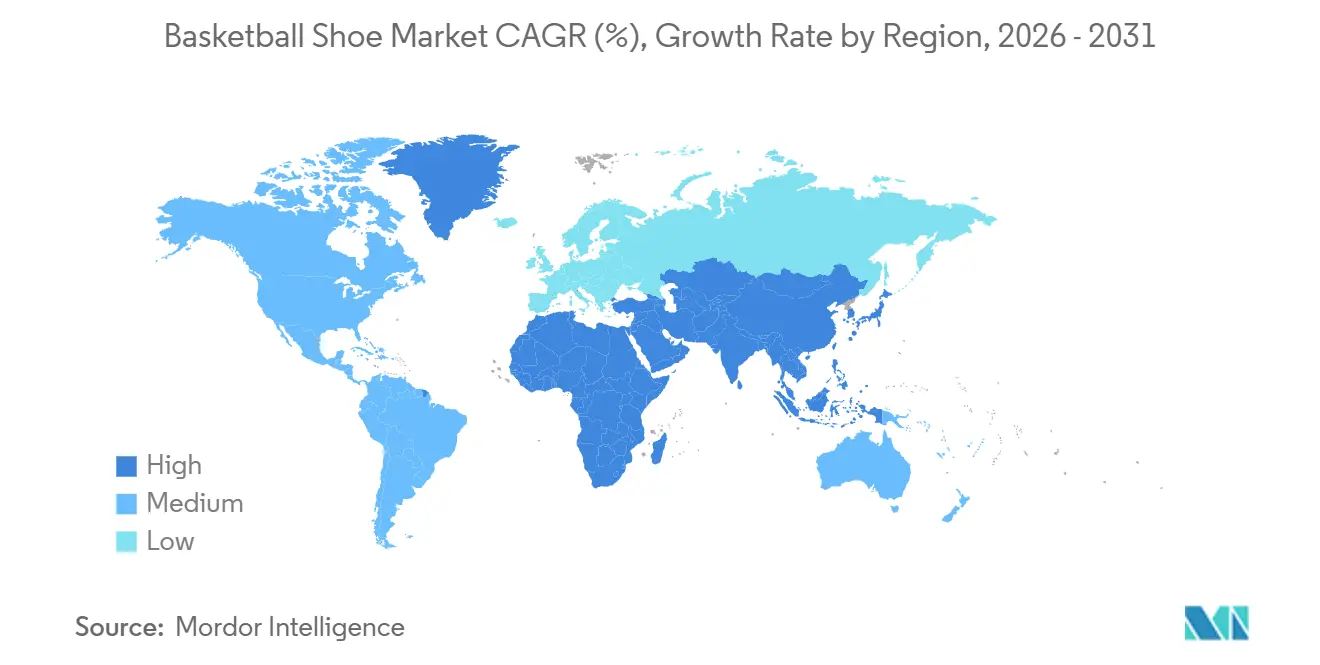

- By geography, North America commanded 40.12% of 2025 revenue, but Asia-Pacific is projected to post the fastest 8.19% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Basketball Shoe Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global participation in basketball at youth, school, college, and amateur levels | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of professional leagues and tournaments raising visibility and aspiration for branded footwear | +1.5% | Global, led by North America and Europe; emerging in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Growth of basketball academies and training programs | +0.8% | North America, Europe, China, India | Medium term (2-4 years) |

| Increasing health and fitness awareness positioning basketball as preferred cardio and team sport | +0.9% | Global, particularly urban centers in developed and emerging markets | Medium term (2-4 years) |

| Athlete endorsement and influencer marketing by star players and social media | +1.3% | Global, with highest impact in North America and Asia-Pacific | Short term (≤ 2 years) |

| Signature shoe lines linked to star players creating emotional attachment and repeat purchases | +1.0% | Global, concentrated in North America, Europe, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising global participation in basketball at youth, school, college, and amateur levels

Youth basketball infrastructure is expanding beyond traditional regions, driven by increasing participation rates and investments from municipal governments and private operators in dedicated facilities. In 2025, the Junior National Basketball Association (Jr. NBA) 3v3 program engaged 174 secondary schools in London, with participants primarily from disadvantaged areas. This highlights the role of grassroots initiatives in improving accessibility and fostering long-term brand loyalty. In the United States, the Sports and Fitness Industry Association (SFIA) reported that 80% of Americans engaged in some form of physical activity in 2024, with basketball participation rising by 7% or more following the 2024 Paris Olympics [1]Source: Sports & Fitness Industry Association (SFIA), “SFIA’s Topline Participation Report,” sfia.org. Hoop Habits, a Minnesota-based training facility, reported an 80% increase in membership and opened a 41,000-square-foot complex in 2025. Similarly, MADE Hoops and HMBL launched a 15,000-square-foot venue in Brooklyn, reflecting significant private-sector interest in youth basketball facilities. This growth in participation has directly influenced footwear demand, as parents increasingly prioritize basketball-specific shoes to reduce injury risks. Research indicates that proper court shoes can lower the incidence of ankle sprains by 40% compared to cross-training or running shoes. Furthermore, the rise of travel teams and Amateur Athletic Union (AAU) circuits has amplified consumption, as competitive players often require multiple pairs of shoes per season to maintain optimal traction and cushioning performance.

Expansion of professional leagues and tournaments raising visibility and aspiration for branded footwear

Professional basketball is expanding its geographic reach, with the National Basketball Association (NBA) announcing plans to establish a European league by 2027. This league will include multiple franchises, with franchise fees set at a substantial amount. The initiative aims to increase basketball's visibility across Europe and create new endorsement opportunities for footwear brands. Similarly, the Women's National Basketball Association (WNBA) introduced significant structural changes through its collective bargaining agreement ratified in 2025. These changes include raising the salary cap, introducing supermax contracts, doubling minimum salaries, and mandating charter travel and housing provisions. These improvements are expected to enhance the league's commercial appeal and provide female athletes with endorsement opportunities comparable to those of male players. For instance, Caitlin Clark earned considerable revenue from endorsements in 2025, surpassing her Women's National Basketball Association salary. Her Nike signature shoe, scheduled for release in spring 2026, is projected to generate substantial first-year revenue. Additionally, the growing number of signature shoe models, which reached a notable count of active lines in 2025, highlights that brands recognize emotional connections with individual athletes are more effective in driving repeat purchases than relying solely on generic performance-focused marketing.

Growth of basketball academies and training programs

Specialized training facilities are expanding as parents and aspiring athletes increasingly seek structured skill development outside traditional school programs. Hoop Habits' 80% membership growth and its 41,000-square-foot expansion in Minnesota highlight the private sector's confidence in basketball training as a viable business model. Similarly, MADE Hoops and HMBL (Hoop Major Basketball League) launched a 15,000-square-foot facility in Brooklyn in 2025, aimed at providing urban youth with year-round access to coaching and competitive play. These academies also serve as brand incubators, as young players often adopt the footwear worn by their coaches and older peers, fostering early brand loyalty that continues through high school and college. The Jr. National Basketball Association (NBA) 3v3 program's expansion into London, involving 174 schools with 31 percent of them from disadvantaged areas, demonstrates how league-sponsored initiatives can increase participation and establish brand preferences before players reach purchasing age. Additionally, the shift toward year-round training, driven by the professionalization of youth sports and the pursuit of college scholarships, has extended the basketball season beyond the traditional winter months. This trend helps smooth demand curves and mitigates the seasonality that has historically impacted footwear sales in regions with temperate climates.

Increasing health and fitness awareness positioning basketball as preferred cardio and team sport

Basketball's appeal as a high-intensity interval workout, combining cardiovascular conditioning with social interaction, is drawing fitness-conscious adults who might otherwise choose activities like running or cycling. According to the Sports and Fitness Industry Association, a large portion of Americans engaged in physical activity, with basketball experiencing notable growth following the Paris Olympics. This trend extends beyond competitive play to include recreational and fitness-focused participation. The sport's accessibility, requiring only a ball and a hoop, reduces entry barriers compared to equipment-intensive activities. Additionally, the team-oriented nature of basketball addresses social isolation, a growing public health concern in post-pandemic societies. Research shows that basketball-specific footwear can significantly lower the risk of ankle sprains compared to cross-training shoes, emphasizing its appeal to health-conscious individuals prioritizing injury prevention. Brands are responding by promoting basketball shoes as lifestyle-fitness hybrids, merging performance with athleisure. For example, Nike's Cosmic Unity, made with a portion of its materials being recycled, targets environmentally conscious consumers seeking to align their fitness choices with sustainability values.

Restrains Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of awareness about benefits of basketball-specific shoes among casual players | -0.5% | Global, particularly in emerging markets and rural areas | Medium term (2-4 years) |

| Proliferation of counterfeit and replica basketball shoes | -0.7% | Global, with highest impact in Asia-Pacific, Middle East, and Africa | Short term (≤ 2 years) |

| Seasonality of basketball in some regions causing uneven demand | -0.4% | Temperate regions in North America, Europe, and parts of Asia | Short term (≤ 2 years) |

| Competition from other athletic footwear categories | -0.6% | Global, particularly in lifestyle and athleisure segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of awareness about benefits of basketball-specific shoes among casual players

Recreational basketball players often choose cross-training or running shoes, unaware that basketball-specific footwear can significantly reduce the risk of ankle sprains due to lateral support structures and traction patterns designed for court surfaces. This lack of awareness is particularly evident in emerging markets and rural areas, where basketball infrastructure is still developing, and retail distribution tends to favor general athletic footwear over category-specific options. Historically, brands have under-invested in educational marketing that highlights the biomechanical benefits of basketball shoes, instead prioritizing endorsement-driven campaigns that focus on style and athlete associations rather than functional advantages. Consequently, a significant market of casual players, who engage in pickup games or recreational leagues, continues to base footwear purchases on price and aesthetics rather than performance features. Addressing this awareness gap requires strategies such as point-of-sale education, digital content showcasing injury-prevention benefits, and collaborations with youth leagues and recreational facilities to influence purchasing decisions at the grassroots level. The growing shift toward direct-to-consumer channels, where brands can control messaging and integrate educational content into the shopping experience, presents an opportunity to mitigate this challenge. However, progress remains inconsistent across different regions and income groups.

Proliferation of counterfeit and replica basketball shoes

The global counterfeit sneaker market is substantial, with Jordan Brand models being the most frequently replicated products. This widespread counterfeiting undermines brand equity and reduces profit margins in secondary markets. Modern counterfeit sneakers, often referred to as "super fakes," are produced in factories using materials and construction techniques similar to those of authentic products, making detection challenging without close examination of stitching, logos, box labels, and serial numbers. Counterfeit activity is most prevalent in the Asia-Pacific, Middle East, and Africa regions, where enforcement mechanisms are less robust, and e-commerce platforms provide anonymity for sellers. The growth of social media marketplaces and peer-to-peer resale platforms has further facilitated counterfeit distribution, allowing sellers to reach global audiences without the need for physical retail infrastructure. To address this issue, brands are adopting authentication technologies such as blockchain-based provenance tracking, Near Field Communication (NFC) chips embedded in shoe tongues, and collaborations with resale platforms like StockX, which verify authenticity before completing transactions. However, these measures increase supply chain costs and complexity, and their success depends on consumers' willingness to pay a premium for verified products. Additionally, the European Union's Ecodesign for Sustainable Products Regulation, which prohibits the destruction of unsold footwear starting in mid-July 2026, may unintentionally worsen counterfeiting [2]Source: European Commission, “New EU rules to stop the destruction of unsold clothes and shoes,” commission.europa.eu. This regulation could compel brands to liquidate excess inventory through discount channels, where counterfeit products are more likely to be mixed with genuine items, creating further challenges for both brands and consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Shoe Type: Low-Top Designs Challenge Ankle-Support Orthodoxy

Low-top basketball shoes are projected to grow at a rate of 8.61% during the period 2026 to 2031, marking the fastest growth among shoe types, even as high-tops maintained a 60.11% market share in 2025. This trend reflects a generational shift in player preferences, with younger athletes prioritizing mobility and reduced weight over the ankle support that has historically influenced design. Mid-top silhouettes serve as a compromise, offering lateral stability without the bulk of high-tops, but their growth remains modest compared to the rapid rise of low-tops. The increasing availability of signature models has further driven this trend, as brands design shoes tailored to individual athletes' playing styles. Guards and perimeter players often prefer low-tops for speed and agility, while forwards and centers tend to choose high-tops for enhanced stability during post play.

Nike's GT Cut 4, a low-top performance model launched in 2025, exemplifies advancements in design that achieve lighter construction while maintaining support. It features Zoom Air cushioning and a carbon-fiber plate to improve energy return. Similarly, Adidas's Harden Vol. 8, which achieved notable sales in the first half of 2026, incorporates a low-top design aligned with James Harden's preference for court feel and lateral quickness. The rising popularity of low-tops also aligns with the lifestyle sneaker trend, as these designs transition seamlessly from court to street, expanding their appeal to fashion-conscious consumers in addition to competitive players.

By End User: Kids Segment Fueled by Youth Academies and Early Brand Loyalty

The kids' segment is expected to grow at a rate of 7.91% during 2026-2031, outpacing the men's segment, which accounted for a 60.63% market share in 2025, as well as the women's segment. This growth is driven by the increasing presence of youth basketball academies, travel teams, and school programs that introduce children to the sport at an early age, helping to establish brand preferences before they gain purchasing independence. The significant membership growth of Hoop Habits and its large-scale expansion in Minnesota highlight the private sector's confidence in youth basketball as a sustainable business model. Additionally, the Junior National Basketball Association (Jr. NBA) 3v3 program's engagement with numerous London schools in 2025 demonstrates the scalability of league-sponsored initiatives in promoting participation. Parents are increasingly prioritizing basketball-specific footwear to reduce injury risks, with research showing that proper court shoes can lower the incidence of ankle sprains by 40% compared to cross-training shoes.

The women's segment, while smaller in absolute terms, is experiencing growth driven by structural changes such as the Women's National Basketball Association's (WNBA) seven-year collective bargaining agreement. This agreement significantly increased the salary cap, enabling female athletes to secure endorsement deals comparable to those of their male counterparts. For instance, Caitlin Clark's signature Nike shoe, set to launch in spring 2026, is projected to generate substantial first-year revenue. This development highlights the growing recognition of female athletes' commercial potential.

By Category: Premium Segment Driven by Signature Models and Emotional Attachment

The premium category is projected to grow at a rate of 8.33% during the period 2026-2031, surpassing the growth of the mass segment, which accounted for a 67.82% market share in 2025. This segmentation highlights the growing income disparity and the willingness of aspirational consumers to spend over USD 160 on signature models endorsed by star athletes. For example, Nike's LeBron 21 achieved notable quarterly sales during the first half of 2026. Similarly, Under Armour's Curry Flow 12 also recorded strong sales, demonstrating that premium pricing does not discourage demand when products are closely associated with well-known athletes.

The mass segment's dominance reflects the fact that most basketball players are recreational participants who prioritize affordability over advanced performance features. Puma's MB.03 and MB.04 captured a significant share of the sub-USD 150 segment by adopting a value-premium positioning that combines performance credibility with accessible pricing. Additionally, the European Union's Ecodesign for Sustainable Products Regulation, which will prohibit the destruction of unsold footwear starting in mid-July 2026, is expected to drive brands to reevaluate production volumes and end-of-season clearance strategies. This regulation could result in higher working-capital requirements and reduced profit margins within the mass segment.

By Distribution Channel: Online Retail Gains as Brands Pursue Direct-to-Consumer Models

Online retail stores are projected to grow at a rate of 8.98% during the period from 2026 to 2031, marking the fastest growth among distribution channels. In contrast, sports and specialty stores accounted for a 38.92% market share in 2025. This trend highlights the strategic focus of brands on direct-to-consumer models, which offer higher profit margins and direct access to customer data through their own channels. By the middle of the decade, Nike achieved notable success in adopting this model, with Adidas also making significant progress. The growth of signature models, supported by online channels, has been driven by the ability to showcase a wide range of color options and storytelling content, free from the shelf-space limitations of physical retail stores. At the same time, supermarkets and hypermarkets continue to serve price-sensitive consumers looking for mass-market products. The "others" category, which includes factory outlets and off-price retailers, focuses on clearing prior-season inventory. According to the International Trade Administration, global business-to-consumer (B2C) e-commerce revenue is expected to grow steadily at a compound annual growth rate [3]Source: International Trade Administration, “2024 eCommerce Size & Sales Forecast,” trade.gov. The leading segments for business-to-consumer e-commerce include consumer electronics, fashion, furniture, toys and hobbies, biohealth pharmaceuticals, media and entertainment, beverages, and food.

Sports and specialty stores maintain strengths such as expertise in product fitting and the opportunity for customers to test products before making a purchase. However, their market share is declining as brands increasingly invest in augmented-reality sizing tools and flexible return policies, which reduce barriers to online shopping. Additionally, the European Union's Ecodesign for Sustainable Products Regulation, which will take effect in the second half of the decade, prohibits the destruction of unsold footwear. This regulation is expected to further drive the shift toward online channels, as brands can more effectively manage inventory and adjust pricing dynamically to clear excess stock without resorting to destruction.

Geography Analysis

North America held a 40.12% share of the Basketball Shoe Market in 2025, driven by the United States' strong basketball culture, extensive youth infrastructure, and the National Basketball Association's (NBA) commercial influence. The region's mature market is defined by high per-capita consumption, with competitive high school and college programs encouraging frequent purchases as players often require multiple pairs per season. While Canada and Mexico contribute to incremental growth, their smaller populations and lower basketball penetration result in a smaller market share compared to the United States. The NBA's announcement of a European league set to launch in 2027, featuring 16 franchises with franchise fees starting at USD 1 billion, highlights the league's ambition to replicate its North American success globally. This development could indirectly benefit North American brands by elevating basketball's global profile and creating new endorsement opportunities.

The Asia-Pacific region is expected to grow at a rate of 8.19% during 2026-2031, making it the fastest-growing geography. Growth in this region is driven by China's domestic brand expansion, India's increasing youth participation in basketball, and rising disposable incomes across the broader region. ANTA Sports reported revenue of RMB 70.83 billion in 2024, reflecting a 13.6% year-over-year increase, and held a 23% share of the Chinese market. However, its basketball category faced challenges in the third quarter of 2025 due to shifting consumer preferences toward lifestyle and running footwear. Similarly, Li Ning reported revenue of RMB 29.6 billion in 2025, a 3.2% increase year-over-year, but its basketball category declined by 19%, accounting for 17% of omni-channel sell-through. This decline highlights intensifying competition and the difficulty of maintaining relevance among younger consumers.

Europe, South America, and the Middle East and Africa represent smaller but strategically important markets. In Europe, basketball culture is concentrated in countries such as Spain, Italy, France, Germany, and the Balkans, where professional leagues and national teams maintain visibility. However, basketball's popularity remains secondary to football. The NBA's planned European league, launching in 2027, aims to address this gap by establishing a year-round professional circuit that could rival domestic football leagues in media attention and commercial appeal. In South America, basketball's presence is primarily limited to Argentina and Brazil, where infrastructure and youth programs are less developed compared to football. Similarly, the Middle East and Africa face challenges such as limited court access and lower disposable incomes, with basketball participation largely concentrated in urban areas. However, the region's young demographics and increasing smartphone penetration present opportunities for digital-first engagement strategies that bypass traditional retail infrastructure.

Competitive Landscape

The Basketball Shoe Market is moderately consolidated, with Nike, Adidas, and Jordan Brand collectively holding a significant share of global revenue. Meanwhile, Chinese brands such as ANTA, Li Ning, and Peak are leveraging their domestic market scale and competitive pricing to challenge established players, particularly in the Asia-Pacific region. ANTA's acquisition of a significant stake in Puma in January highlights its strategic focus on enhancing credibility in the European market and achieving cross-border portfolio synergies. This acquisition allows ANTA to utilize Puma's distribution network while accessing Western design expertise.

Signature shoe lines have reached a record high in active models in recent years, compared to fewer than two decades ago. This growth has fragmented endorsement budgets and encouraged brands to justify premium pricing through storytelling rather than relying solely on performance differentiation. Opportunities are emerging in the value-premium segment, where Puma's MB.03 and MB.04 have captured a notable share of the sub-premium market by offering performance-oriented products at accessible price points. These models directly compete with higher-priced offerings such as Nike's LeBron 21 and Under Armour's Curry Flow 12, which are positioned at premium price levels.

New entrants are disrupting the market, including Skechers, which entered the basketball category in December with the Skechers SKX JE1, Joel Embiid's signature shoe. Skechers has leveraged its global distribution network and strong brand recognition in lifestyle footwear to expand into performance footwear. Additionally, the women's segment presents a growing opportunity, highlighted by Nike's launch of Caitlin Clark's signature shoe in spring. This product is expected to generate significant revenue in its first year, reflecting the increasing commercial potential of female athletes.

Basketball Shoe Industry Leaders

Nike Inc.

Adidas AG

Puma SE

Under Armour, Inc

ANTA Sports Products Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Converse introduced the SHAI 001 during the All-Star Weekend in 2025, marking the brand's first signature basketball shoe designed specifically for SGA's dynamic playing style. The SHAI 001 includes a locking zipper for unique styling, a forefoot Zoom Air unit, and radial traction to support explosive movements on the court.

- February 2025: Nike introduced the A’ja Wilson A’One, the first signature shoe for WNBA player A’ja Wilson. Designed with Wilson's input, this low-cut performance model focuses on lightweight responsiveness and aims to inspire young female athletes.

- January 2025: Reebok introduced its Engine A, signifying the brand's return to performance basketball after more than a decade. The shoe incorporates nitrogen-based cushioning foam, offering enhanced comfort and responsiveness.

Global Basketball Shoe Market Report Scope

The Basketball Shoe Market refers to athletic footwear specifically designed for basketball players. These shoes are equipped with features such as high-traction outsoles to ensure better grip, superior ankle support for stability, advanced cushioning technologies for comfort, and lightweight materials to enhance performance, agility, and minimize the risk of injuries during gameplay. The market is segmented by shoe type, including High-Top, Mid-Top, and Low-Top; by end user, covering Kids, Women, and Men; by category, divided into Mass and Premium; by distribution channel, which includes Supermarkets and Hypermarkets, Sports and Specialty Stores, Online Retail Stores, and Others; and by geography, encompassing North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the above mentioned segments.

| High-Top |

| Mid-Top |

| Low-Top |

| Kids |

| Women |

| Men |

| Mass |

| Premium |

| Supermarkets and Hypermarkets |

| Sports/Specialty Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Shoe Type | High-Top | |

| Mid-Top | ||

| Low-Top | ||

| By End User | Kids | |

| Women | ||

| Men | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Sports/Specialty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast will global demand for basketball shoes rise over the next five years?

Revenue is projected to advance at 7.37% CAGR between 2026 and 2031, led by Asia-Pacific and the accelerating kids segment.

Which silhouette is gaining the most momentum with performance athletes?

Low-top shoes are forecast to expand at 8.61% through 2031 because modern plates and foams now provide stability without added collar height.

Why are kids’ sizes outpacing adult pairs?

Earlier participation through academies and school leagues plus rapid foot growth causes children to replace shoes more frequently than adults.

What channel offers brands the highest margins today?

Direct-to-consumer online stores deliver the best gross margins by removing wholesale mark-ups and capturing shopper data for repeat targeting.

Will sustainability rules affect release strategies?

Yes, the European ban on destroying unsold footwear after mid-2026 is prompting brands to adopt tighter production runs and agile markdown tools online.

Page last updated on: