Traditional Toys And Games Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 97.73 Billion |

| Market Size (2031) | USD 106.12 Billion |

| Growth Rate (2026 - 2031) | 1.66% CAGR |

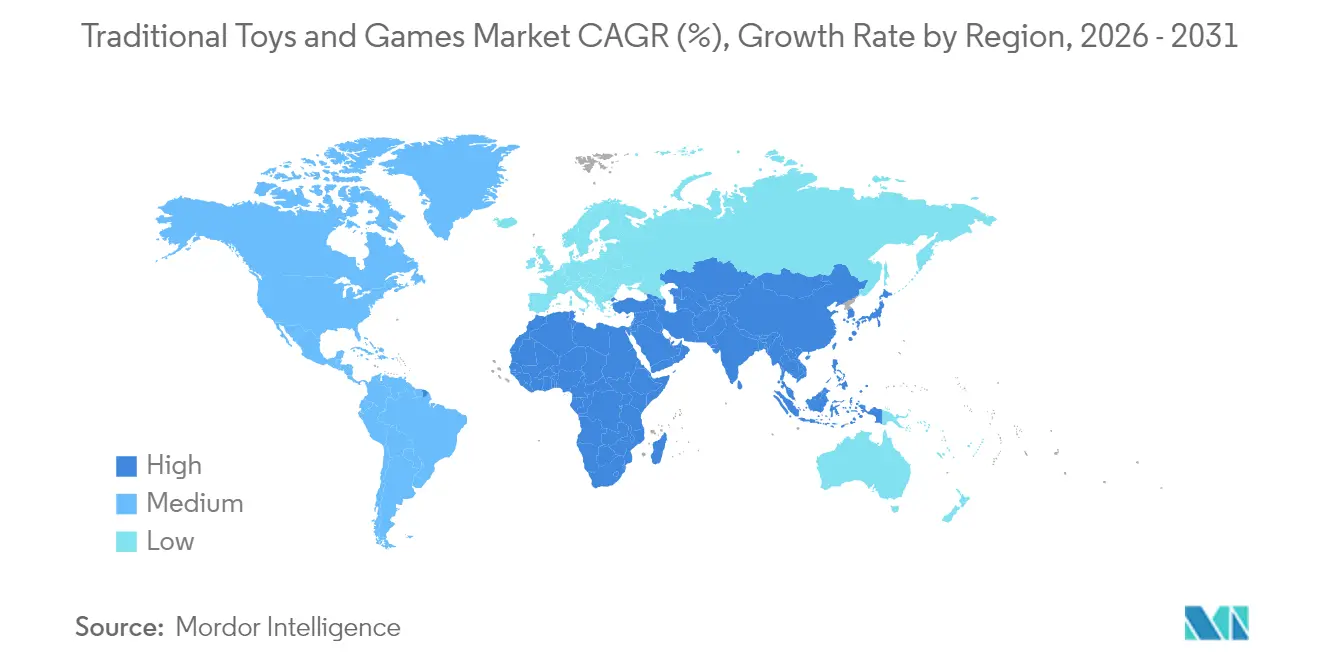

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Traditional Toys And Games Market Analysis by Mordor Intelligence

The global traditional toys and games market size was valued at USD 96.13 billion in 2025 and estimated to grow from USD 97.73 billion in 2026 to reach USD 106.12 billion by 2031, at a CAGR of 1.66% during the forecast period (2026-2031). Parents' preference for toys with educational and developmental benefits, especially STEM-focused products and eco-friendly options, supports market expansion. The enduring appeal of classic toys, strong brand recognition, and hands-on play experiences maintain market stability despite competition from video games, mobile apps, and digital entertainment platforms. Manufacturers continue to address supply chain challenges while adapting to consumer preferences. Additionally, increasing parental concerns about excessive screen time strengthen the market as families incorporate traditional toys to promote balanced childhood development. These market dynamics indicate sustained growth potential for traditional toys, particularly in segments that emphasize learning and development.

Key Report Takeaways

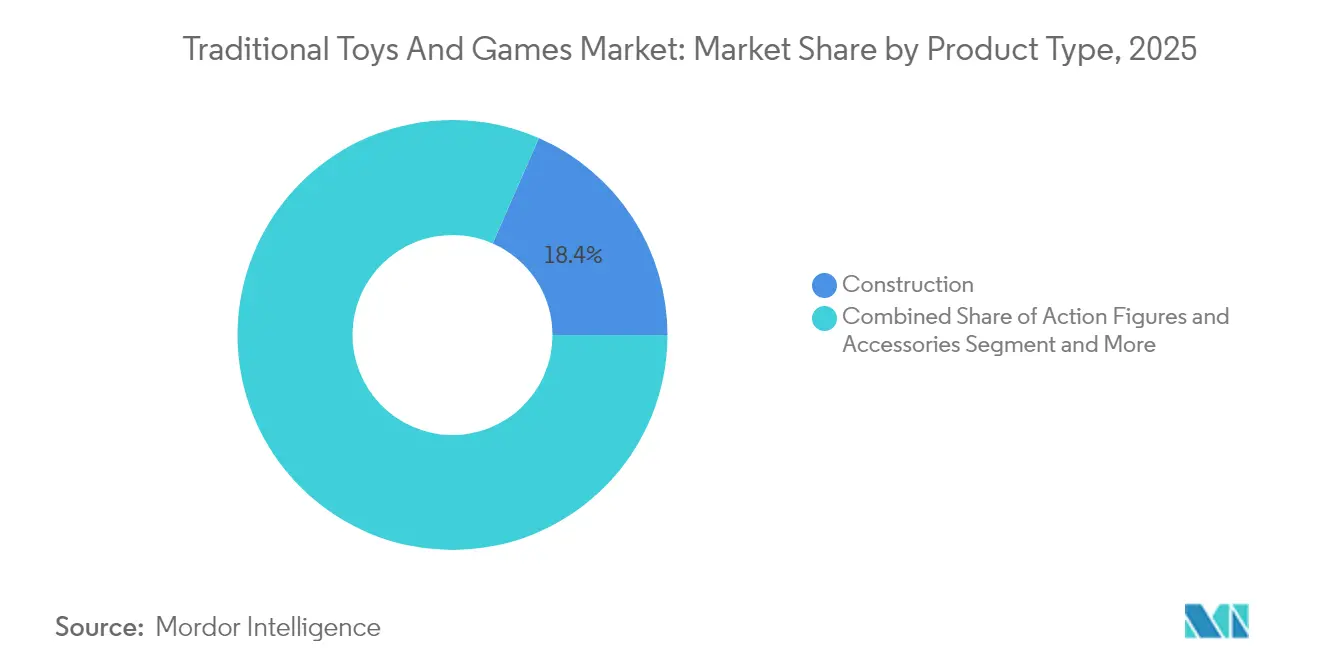

- By product type, construction toys captured 18.42% of the global toy market share in 2025, while games and puzzles are projected to expand at a 1.98% compound annual growth rate (CAGR) through 2031.

- By mode of operation, manual toys accounted for 73.88% of the global toy market size in 2025; electric/battery-operated toys are expected to lead growth with a 2.38% CAGR to 2031.

- By age group, the children/teenager cohort accounted for 63.92% of the global toy market size in 2025, whereas infant and toddler toys are set to grow at a 3.75% CAGR in the forecast period.

- By category, mass-market products held 69.02% revenue share in 2025, but premium toys are advancing at a 3.11% CAGR through 2031.

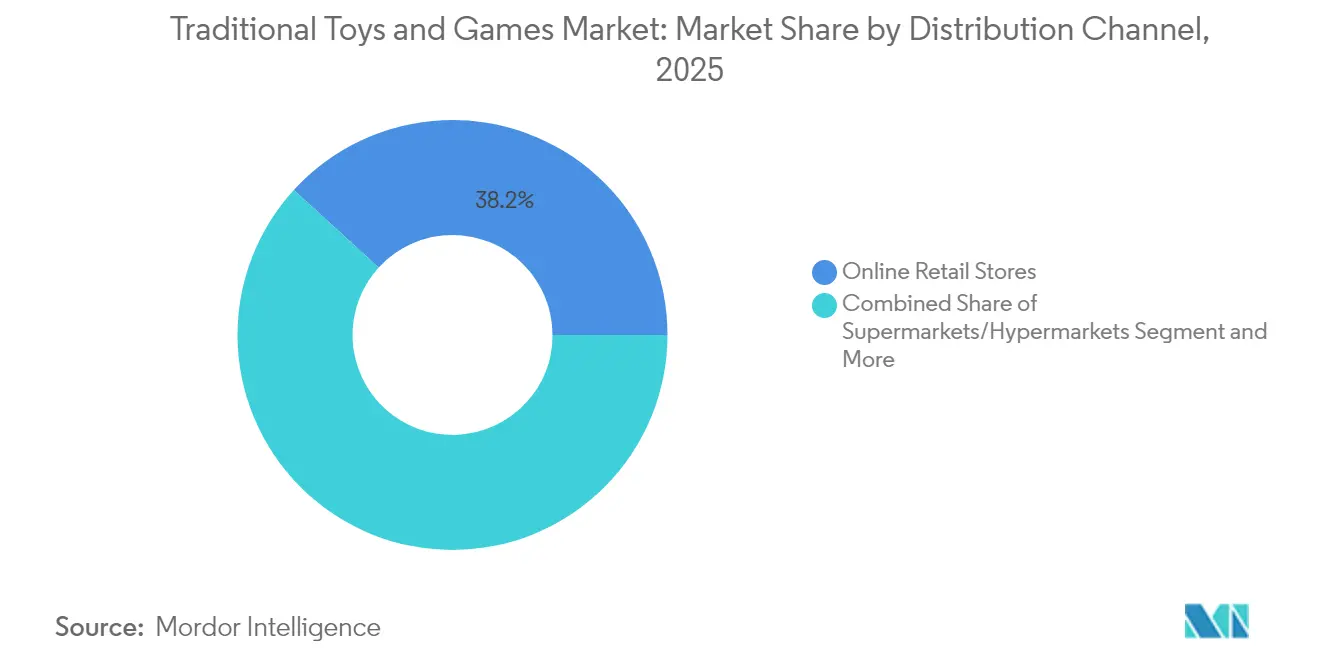

- By distribution channel, online retail stores dominated with a 38.21% share in 2025 and will rise at a 3.62% CAGR to 2031.

- By geography, North America led with 34.21% of the global toy market size in 2025, yet Asia-Pacific is poised for the fastest regional CAGR at 4.15% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Traditional Toys And Games Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Educational toy demand | +0.8% | Global; early gains in North America, Europe, APAC | Medium term (2-4 years) |

| Construction toy popularity | +0.6% | Global | Short term (≤ 2 years) |

| Health and outdoor play awareness | +0.4% | North America & EU; spill-over to APAC | Medium term (2-4 years) |

| Technological integration with traditional toys | +0.5% | APAC core, North America, selective EU markets | Long term (≥ 4 years) |

| Sustainability and eco-friendly materials | +0.3% | EU, North America, global premium segment | Long term (≥ 4 years) |

| Growth of 3D games and graphics | +0.2% | Developed markets worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand of Educational Toys

Educational toy demand is experiencing significant growth, driven by parents' increasing emphasis on STEM learning and cognitive development over passive entertainment. This shift is reflected in rising export figures, with China's toy exports reaching USD 2.94 billion in April 2025, indicating robust market expansion[1]Source: China Customs, “China: monthly toy exports,” english.customs.gov.cn. Parents' growing concerns about excessive screen time have led to a preference for hands-on learning experiences that develop spatial reasoning, problem-solving abilities, and persistence. STEM toys effectively combine learning with play, making complex concepts more accessible and enjoyable for children while enhancing critical thinking skills. This trend is exemplified by recent market developments, such as the October 2024 launch of the Wondery Kids and Wow in the World STEM toy line, which integrates educational elements into traditional toys to foster meaningful engagement between children and caregivers. The integration of technology in educational toys, such as coding robots and augmented reality learning tools, has further enhanced their appeal among tech-savvy parents seeking balanced educational experiences. Additionally, manufacturers are responding to this demand by investing in research and development to create innovative educational toys that align with current educational curricula and developmental milestones.

Rising Popularity of Construction Toys

Construction toys are experiencing a renaissance driven by their cross-generational appeal and technological integration. These toys, including building blocks and Lego sets, stimulate cognitive development, enhance fine motor skills, and foster creativity while encouraging problem-solving, logical thinking, and engineering skills. The category's growth is further amplified by social media platforms showcasing elaborate builds, creating viral marketing effects that traditional advertising cannot replicate. Manufacturing innovations enable increasingly sophisticated designs while maintaining safety standards, with players like Mattel, which launched its Brick Shop brand in May 2025, challenging established players in high-growth building set segments. The integration of augmented reality features and mobile applications has added new dimensions to traditional construction play patterns, allowing children to interact with their physical creations in digital environments. Educational institutions increasingly incorporate construction toys into their STEM curricula, recognizing their value in developing spatial awareness and engineering concepts. Additionally, the rise of adult fans of construction toys has led to the development of more complex sets targeting mature audiences, expanding the market beyond its traditional youth demographic.

Health and Outdoor Play Awareness

The growing recognition among parents of the developmental benefits of tactile, three-dimensional play experiences over screen-based activities is driving the traditional toys and games market. This trend particularly benefits categories like sports equipment, outdoor games, and physical building sets that promote motor skill development and social interaction. The movement is supported by pediatric recommendations limiting screen time for young children and research linking physical play to cognitive development and emotional regulation. According to Toy Association data, retail sales of outdoor and sports toys in the United States reached approximately USD 4.3 billion in 2024[2]Source: Toy Association, "Outdoor and sports toy retail sales in the United States from 2020 to 2024", toyassociation.org. The Children's Hospital of Philadelphia emphasizes that outdoor play helps children socialize, understand their bodies better, engage in imaginative play, and enjoy the outdoors[3]Source: Children’s Hospital of Philadelphia, “Benefits of Outdoor Play,” chop.edu. This growing preference for traditional play experiences is reflected in the market performance. Manufacturers are responding to this trend by developing innovative outdoor play equipment and traditional toys that incorporate educational elements while maintaining their physical nature. Additionally, schools and educational institutions are increasingly incorporating traditional play-based learning methods into their curricula, further strengthening the market demand for conventional toys and games.

Sustainability and Eco-Friendly Materials

Environmental consciousness is transforming material sourcing and production processes across the toy industry, with key players investing heavily in sustainable alternatives. For instance, in March 2024, PLAYMOBIL selected plant-based styrenics material from INEOS Styrolution for new sustainable toys. Consumer willingness to pay premiums for eco-friendly toys is driving innovation in bioplastics, recycled materials, and packaging reduction, addressing mounting criticism of the industry's plastic waste contribution while creating competitive differentiation opportunities for early adopters. This shift toward sustainable practices is expected to significantly influence the traditional toys and games market's growth trajectory in the coming years. Industry participants are increasingly incorporating recycled ocean plastics and biodegradable materials into their production processes, demonstrating their commitment to environmental stewardship. Additionally, market leaders are redesigning packaging to minimize waste and implementing take-back programs to ensure proper recycling of end-of-life products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital and screen-based entertainment | -0.9% | Global | Short term (≤ 2 years) |

| Supply-chain disruptions and raw-material shortages | -0.6% | Global; China-dependent chains | Medium term (2-4 years) |

| Competition from educational apps | -0.4% | North America, Europe, urban APAC | Medium term (2-4 years) |

| Stringent regulatory and safety standards | -0.3% | EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense Competition from Digital and Screen-Based Entertainment

Digital entertainment platforms, including video games, streaming content, and social media, pose a significant threat to traditional toy engagement. According to the Entertainment Software Association's 2024 data, 83% of parents play video games with their children, indicating the growing prevalence of digital entertainment in family activities[4]Source: Entertainment Software Association, “Essential Facts About the U.S. Video Game Industry 2024,” theesa.com . The increasing time spent on these digital platforms, which offer instant gratification and social connectivity, particularly appeals to children and restrains the growth of the traditional toys and games market. This shift in entertainment preferences has prompted traditional toy manufacturers to adapt their strategies, with many incorporating digital elements into their product offerings. The integration of augmented reality features and app-connected toys represents manufacturers' efforts to remain competitive in an increasingly digitalized play environment. Studies show that children aged 5-12 spend an average of 4-6 hours daily on digital devices, further highlighting the challenge faced by traditional toy manufacturers.

Rising Competition from Educational Apps and E-Learning Tools

Educational technology platforms create a significant market restraint for traditional toys and games, as consumers increasingly shift towards digital learning solutions. These platforms deliver interactive learning experiences with personalized paths, immediate feedback, and progress tracking capabilities that conventional toys cannot replicate. The COVID-19 pandemic accelerated the adoption of digital learning solutions, establishing persistent usage patterns that continue to influence consumer behavior. This shift in learning preferences compels traditional toy manufacturers to emphasize their unique advantages in tactile learning, spatial reasoning development, and face-to-face social interaction to maintain market relevance. Many traditional toy manufacturers are responding by incorporating hybrid elements that combine physical play with digital components to stay competitive. Parents increasingly seek toys that offer both educational value and traditional play experiences, creating opportunities for innovative product development. The continuous evolution and accessibility of educational technology platforms present an ongoing challenge for traditional toy manufacturers, potentially limiting their market growth and requiring constant adaptation to maintain competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Construction Leads Innovation-Driven Growth

Construction toys dominate the traditional toys and games market with an 18.42% share in 2025, driven by their perceived educational value and appeal across multiple generations. This segment's success extends beyond children to engage adults, while Games and Puzzles emerge as the fastest-growing category with a projected 1.98% CAGR from 2026-2031, reflecting increased family engagement and focus on cognitive development. Action Figures and Accessories maintain robust performance through licensed properties and collectibles, though Dolls and Accessories face challenges from evolving play patterns and digital entertainment alternatives.

Model Vehicles show sustained growth by targeting adult collectors and incorporating premium detailing, with particular emphasis on electric and autonomous vehicle themes. The market also encompasses various emerging categories, including STEM kits and sensory toys, which address specific developmental requirements and therapeutic applications, demonstrating the industry's adaptation to changing consumer needs and educational priorities. These specialized segments benefit from increasing parental awareness of developmental milestones and educational benchmarks in early childhood. Additionally, manufacturers continue to innovate within these categories by incorporating sustainable materials and eco-friendly packaging to align with growing environmental consciousness among consumers.

By Mode of Operation: Manual Dominance Faces Electric Innovation

Manual toys continue to dominate the market with a 73.88% share in 2025, as consumers consistently prefer tactile, hands-on play experiences that enhance creativity and motor skill development. While electric/battery operated toys represent a smaller segment, they exhibit stronger growth potential with a 2.38% CAGR, driven by increasing emphasis on early learning and parental investment in developmental toys. This preference for manual toys is particularly evident in emerging markets, where traditional play patterns remain deeply ingrained in cultural practices. Additionally, the lower price points and durability of manual toys contribute to their sustained market leadership, especially in price-sensitive regions.

The electric toy segment faces regulatory challenges, particularly from Consumer Product Safety Commission proposals regarding button and coin cell battery safety, which may necessitate design modifications and increase compliance costs. However, advancements in battery life, safety features, and interactive capabilities are enabling manufacturers to expand electric toy applications beyond traditional categories into educational and therapeutic markets, supporting the segment's growth trajectory. The integration of smart features and connectivity options in electric toys is creating new opportunities for manufacturers to differentiate their products. Furthermore, the growing focus on STEM education has led to increased demand for programmable and tech-enabled toys, despite the regulatory hurdles.

By Age Group: Children/Teenager Segment Drives Market Dynamics

The children/teenager segment (2-18 years) dominates the toy market with a 63.92% share in 2025, while the infant and toddler segment (below 2 years) exhibits the highest growth rate at 3.75% CAGR from 2026-2031. The infant and toddler segment maintains consistent demand through developmental toys and safety-certified products, while the children/teenager segment's expansion is driven by the emerging kidult market phenomenon. The parents are increasingly prioritizing educational value in toys for children aged 2-18 years, leading to higher spending in this segment. Additionally, the integration of technology in traditional toys has created new opportunities within the children/teenager segment, particularly in STEM-focused products.

The growing trend of adult consumers purchasing toys for personal enjoyment rather than gifting has transformed traditional age-based consumption patterns. This shift has prompted manufacturers to adapt their product development and marketing strategies, particularly in collectibles, construction sets, and licensed properties that combine nostalgic appeal with display value. Consumer insights show that adults aged 25-40 represent a significant portion of premium toy purchases, especially in categories like action figures and limited-edition collectibles. Furthermore, social media communities centered around toy collecting have strengthened this market segment, encouraging manufacturers to release more sophisticated and detailed products that appeal to adult collectors.

By Distribution Channel: Online Retail Transforms Market Access

Online retail stores dominate the market with a 38.21% share in 2025 and are projected to grow at a CAGR of 3.62% from 2026-2031. This leadership position stems from accelerated digital adoption and consumer preference for convenience, which has continued beyond the pandemic period. While specialty retail stores maintain their relevance through experiential shopping and expert guidance, supermarkets and hypermarkets face increasing pressure from online competition and declining impulse purchases. The integration of mobile shopping applications and seamless payment systems has further strengthened online retail's market position. Additionally, the expansion of same-day delivery services in urban areas has addressed immediate gratification needs, traditionally a strength of physical retail.

The e-commerce channel's growth is supported by enhanced logistics networks, virtual try-before-buy technologies, and effective social media marketing that facilitates product discovery and viral trends. This digital transformation has created opportunities for smaller manufacturers to access global markets without significant retail infrastructure investments, while alternative channels like direct-to-consumer platforms and subscription services offer personalized product curation and exclusive offerings. The implementation of artificial intelligence for personalized recommendations and inventory management has improved the online shopping experience. Furthermore, the integration of augmented reality tools for product visualization has reduced return rates and increased consumer confidence in online purchases.

By Category: Premium Segment Capitalizes on Quality Focus

Mass market toys command a dominant 69.02% market share in 2025, driven by consumer price sensitivity and volume-focused retail strategies. However, the Premium toys segment is experiencing faster growth at a 3.11% CAGR from 2026-2031, as consumers increasingly value superior quality, educational features, and sustainable production methods. This shift reflects a growing willingness to invest in durable toys that offer long-term value, particularly benefiting established brands with strong safety records and innovative features. The mass market segment maintains its position through extensive distribution networks and economies of scale, enabling competitive pricing strategies. Additionally, mass market manufacturers focus on licensed products and popular entertainment franchises to maintain market relevance and consumer appeal.

The premium segment's growth aligns with evolving consumer preferences that emphasize quality over quantity and educational value. Companies like LEGO exemplify successful premium positioning through their commitment to innovation, rigorous safety standards, and brand heritage. This strategic approach enables them to maintain higher price points and margins, which in turn supports continued research and development investments for market expansion. Premium toy manufacturers are increasingly incorporating advanced technologies and sustainable materials in their products to justify premium pricing. The segment also benefits from growing parental awareness about the developmental benefits of high-quality educational toys, leading to increased investment in premium products despite their higher cost.

Geography Analysis

North America holds the dominant market position with a 34.21% share in 2025, supported by high disposable income levels, robust toy safety regulations, and well-developed retail infrastructure. The region's market strength is further reinforced by the presence of major toy company headquarters in Los Angeles. The market benefits from sophisticated e-commerce platforms and omnichannel retail strategies that enhance consumer accessibility to toy products. Additionally, the region's strong intellectual property protection framework encourages innovation and investment in new toy development.

Asia-Pacific is experiencing the most rapid market expansion with a projected CAGR of 4.15% during 2026-2031. While China maintains its position as the primary manufacturing hub for US and European toys, increasing labor costs and trade tensions are prompting companies to diversify their supply chains. India's manufacturing transformation is contributing significantly to the region's growth trajectory. The emergence of local toy brands in countries like Japan and South Korea is reshaping regional market dynamics. The growing middle-class population across Southeast Asian nations is also driving increased toy consumption and market expansion.

Europe exhibits steady market growth, characterized by strict safety standards and sustainability requirements that influence product development. The region's strong focus on environmental responsibility has increased demand for eco-friendly toys and sustainable packaging, creating market opportunities for manufacturers who adopt environmentally conscious production methods. The market is particularly influenced by the European Union's comprehensive toy safety directives, which set global benchmarks for quality and safety standards. The region's emphasis on educational and developmental toys aligns with consumer preferences for products that combine learning with play.

Regulatory Landscape

Traditional toys and games are shaped by safety, testing, and documentation requirements that affect product design and time-to-market, particularly in North America and Europe. In the United States, the Consumer Product Safety Commission (CPSC) framework requires toys intended for children 12 years and under to be supported by third-party testing and a Children's Product Certificate (CPC) that cites applicable sections of the ASTM F963 toy safety standard, which increases compliance intensity for both domestic producers and importers.

In the European Union, Regulation (EU) 2025/2509 was adopted to replace Directive 2009/48/EC, entered into force on January 1, 2026, and includes a transition period ending August 1, 2030. Manufacturers need to update technical documentation and safety assessments to the new baseline. Cross-border trade and customs compliance are also getting more process-driven: beginning July 8, 2026, U.S. importers of regulated consumer products must electronically file certificates of compliance with U.S. Customs and Border Protection via a Partner Government Agency (PGA) Message Set, pushing the industry toward tighter data readiness and traceability alongside evolving U.S.-EU tariff actions during 2025-2026.

Value Chain Analysis

The traditional toys and games value chain starts with upstream materials (plastics, textiles, paper/board, inks, and electronics/batteries for certain electric or hybrid products), then moves through design and tooling, manufacturing and assembly (with a large share of global output concentrated in Asia, particularly mainland China). Testing and certification, packaging, and outbound logistics follow, feeding wholesaling and retail. Brand owners typically manage product development, licensing, and quality systems, while contract manufacturers and component suppliers provide scale production; third-party labs and certification workflows sit between factory release and market entry for regulated products.

Downstream, distribution spans mass retail, specialty retail, and e-commerce, supported by global warehousing and seasonal logistics planning that peaks around major holiday cycles. Supply-chain stress has influenced assortment and bill-of-materials decisions, with cost-control actions such as simplifying packaging, reducing accessories, and removing batteries from some playsets to manage tariff-driven cost pressure and lead-time volatility. Retailers and brands have also adopted more disciplined inventory planning and consolidated supplier networks, while compliance documentation and cross-border customs readiness, including tighter certificate handling, has become a more prominent operational requirement for global shipments.

Competitive Landscape

The global toy market demonstrates moderate concentration with oligopolistic characteristics, as major players like LEGO, Mattel, and Hasbro hold substantial market shares while smaller companies operate in niche segments. Companies focus on brand portfolio diversification, entertainment property licensing, and expansion into emerging markets to maintain competitive positions. Market consolidation continues through strategic acquisitions and partnerships, enabling larger companies to strengthen their market presence. The industry's competitive dynamics are further shaped by regional preferences and distribution networks, with successful companies maintaining strong relationships with retailers and e-commerce platforms.

Technology integration has become essential for market differentiation, with companies incorporating AI-powered personalization, augmented reality experiences, and connected play platforms to enhance user engagement beyond physical products. Additionally, manufacturers are diversifying their supply chains away from China in response to trade tensions and sustainability concerns, creating opportunities for companies with flexible and regional production capabilities. Digital transformation initiatives extend to manufacturing processes, improving efficiency and reducing production costs. The integration of data analytics enables companies to better understand consumer preferences and optimize product development cycles.

The market continues to evolve as manufacturers explore new segments and opportunities. For instance, Jazwares' introduction of BLDR, a construction toy brand in February 2025, demonstrates the industry's expansion into new categories. Companies are also targeting previously underserved segments, including sustainable toy manufacturing, educational technology integration, and adult collector markets. Innovation in materials and manufacturing processes has enabled the development of more environmentally friendly products. The rise of direct-to-consumer sales channels has created new opportunities for market entry and brand development.

Traditional Toys And Games Industry Leaders

-

Mattel

-

Hasbro

-

TOMY Company Ltd

-

Kirkbi A/S

-

Bandai Namco Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is building around segments where hands-on play aligns with measurable learning, family engagement, and premiumization, while still fitting the report scope of non-digital primary play value. Category performance points to this shift: Circana reported that US toy industry dollar sales grew 13% through April 2026 versus the same period in 2025, led by games and puzzles (39%), explorative toys (36%), and building sets (20%), reinforcing upside for construction sets, puzzles, and STEM-oriented traditional play that supports cognitive development and social interaction.

Sustainability and compliance-driven redesign is also creating differentiation lanes across materials, packaging, and end-of-life solutions. In the United Kingdom, Wastebuster launched the Recycle to Read hard plastic toy recycling service with Mattel and Tesco in 167 Tesco stores on 22 April 2026, highlighting retail-based circular collection as a scalable route for brands selling high volumes of plastic toys. Packaging reduction programs from major IP owners and manufacturers, along with industry initiatives focused on improved chemical and labor risk management in Southeast Asian factories (Vietnam and Indonesia), are further pushing suppliers toward documented, auditable production that can support premium positioning and smoother access to tightly regulated markets.

Recent Industry Developments

- March 2026: Mattel unveiled a full Masters of the Universe product line tied to the upcoming live-action film, with retail rollout beginning April 25, 2026. The coordinated entertainment-linked launch expands the company's collectible and action-figure lineup and concentrates demand into a defined global retail window.

- February 2026: Mattel announced an agreement to acquire full ownership of the Mattel163 mobile games studio from partner NetEase for USD 159 million. The acquisition strengthens its digital games capability through owned development resources that can amplify toy IP via game-led engagement and cross-promotion.

- May 2025: LEGO opened Asias largest store in India through a partnership with Ample Group, moving beyond online and multi-brand retail distribution into a flagship branded location. The expansion supports premium assortment visibility and strengthens direct consumer engagement in a fast-developing retail market.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of physical, non-digital toys and games that are bought for play, learning, and gifting, and that are sold through retail and other formal channels. The scope includes board games, puzzles, dolls, construction sets, action figures, plush, and outdoor play items.

Scope exclusions: video games and app-based play, VR or console software, and purely digital game downloads are excluded from this sizing.

Segmentation Overview

-

By Product Type

- Action Figures and Accessories

- Construction

- Dolls and Accessories

- Games and Puzzles

- Model Vehicles

- Other Product Types

-

By Mode of Operation

- Manual

- Electric/Battery Operated

-

By Age Group

- Infant and Toddler (Below 2 Years)

- Children/Teenager (2-18 Years)

-

By Category

- Mass

- Premium

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Retail Stores

- Online Retail Stores

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by building a fact base from child population figures, household spending patterns, and retail trends that affect how many units get sold and at what prices. We relied on public sources such as World Bank demographics, UN population statistics, OECD consumer indicators, and US Census retail trade releases, then cross-checked directionally with national statistics offices in major countries.

To keep the model realistic by channel and seasonality, we also used company annual reports, investor presentations, and import and export statistics where relevant. Where available, we referenced reputable press coverage on peak shopping periods and product recalls. In a few places, paid subscriptions covering company financials and news, plus shipment-level import and export records, were used to validate revenue splits and trading intensity. The desk sources listed here are not exhaustive, and other public documents were checked to fill gaps and confirm assumptions.

Primary Interviews and Surveys

Primary work focused on validating what sells, where it sells, and how pricing changes over time. Promotional intensity and product mix can shift value even when unit demand looks stable, so we used interviews to pressure-test the model assumptions. We spoke with a mix of manufacturers, brand owners, distributors, large retailers, specialty stores, and industry experts across APAC, EMEA, and the Americas, which helped confirm channel shares, typical price ladders, and how safety and sustainability preferences influence purchase decisions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 14% | APAC: 45% |

| Mid tier: 54% | Functional/Unit leaders: 39% | EMEA: 33% |

| Smaller Players: 19% | Managers: 47% | Americas: 22% |

Market-Sizing & Forecasting

The core sizing uses a top-down build where consumer and retail indicators are translated into an addressable demand pool for physical toys and games, then adjusted using category and channel splits gathered through research. To keep totals practical, the outputs are corroborated with selective bottom-up checks such as sampled price times volume checks by major categories, plus distributor and retailer channel checks where coverage is clear.

Key inputs used in the model include child population by age bands, household disposable income trends, retail sales growth by channel (especially specialty and online), and import intensity for major toy-producing and toy-consuming countries, along with price movement patterns around promotions and peak seasons. Since product mix affects the average selling price and basket value, assumptions were also reviewed for shifts toward educational items, construction sets, board games, and outdoor play.

For forecasting, scenario analysis was used around macro demand drivers and channel migration, and then the selected path was aligned to what primary respondents expect for pricing and promotional cadence over the next few years. Where bottom-up references were incomplete for smaller markets, gaps were handled using proxy splits from comparable countries, then rechecked against trade and retail signals before finalizing.

Data Validation & Update Cycle

Validation is done by checking the model against independent signals such as trade flows, retail growth rates, and publicly visible financial performance trends for key parts of the value chain. When a variance shows up, the inputs are reviewed again, and follow-up calls are triggered to confirm whether the change is due to pricing, mix, distribution shifts, or a one-time issue such as supply disruption.

Before sign-off, the work goes through multi-step analyst reviews where assumptions, conversions, and year-on-year movements are checked for consistency across regions and channels. Reports are refreshed annually, and interim updates are added when material events happen, followed by a final pre-delivery review so clients receive the latest updated view.

Mordor Intelligence's Traditional Toys and Games Market Size Measured Against Other Published Estimates

Published market sizes for traditional toys and games can differ even when the topic sounds identical, because the boundaries and measurement choices are not always the same. Differences usually show up around what is treated as traditional versus digital play, how retail channels are counted, and which year is used as the anchor for prices and currency conversion.

By tracking category-level inclusions and exclusions, refreshing currency timing and price normalization, and then cross-checking with primary feedback, Mordor Intelligence keeps the estimate tied to physical toy and game demand rather than blended entertainment spending. Gaps also arise when a study stretches the definition to include adjacent categories, uses a longer forecast window with an aggressive growth case, or does not clearly state how promotions and mix shifts affect average selling prices.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 97.73 B (2026) | |

| Industry Publisher A | USD 96.63 B (2025) | Uses a different base year and a longer horizon, and it may apply broader product groupings and channel assumptions that lift the later-year forecast faster than what near-term retail and pricing signals support. |

| Industry Publisher B | USD 96.31 B (2024) | Anchors the sizing on an earlier year and projects through 2030 with a higher implied growth rate, which can reflect stronger online expansion and price uplift assumptions than those validated through recent channel and trade checks. |

The spread in values becomes easier to explain once base year, scope edges, and the treatment of pricing and channel migration are lined up side by side. Our approach aims to keep each step traceable, so a buyer can see which demand indicators and adjustments are driving the total and why the resulting number sits where it does.

Key Questions Answered in the Report

What is the current size of the global traditional toys and games market?

The global traditional toys and games market reached USD 97.73 billion in 2026.

How fast will the global traditional toys and games market grow through 2031?

The market is projected to advance at a 1.66% CAGR, reaching USD 106.12 billion by 2031.

Which product segment holds the largest share in the global traditional toys and games market?

Construction toys led with an 18.42% share in 2025 due to cross-generational educational appeal.

What distribution channel is expanding fastest?

Online retail stores, which captured 38.21% share in 2025, are set to grow at a 3.62% CAGR through 2031.

Why are premium toys gaining traction?

Consumers value durability, educational features, and sustainable materials, driving premium toys to a 3.11% CAGR outlook.

Which region will offer the highest growth rate?

Asia-Pacific is forecast to post a 4.15% CAGR between 2026-2031 thanks to rising middle-class spending and supply-chain localization.

Page last updated on: