Nicotine Gum Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.6 Billion |

| Market Size (2031) | USD 2.58 Billion |

| Growth Rate (2026 - 2031) | 9.93% CAGR |

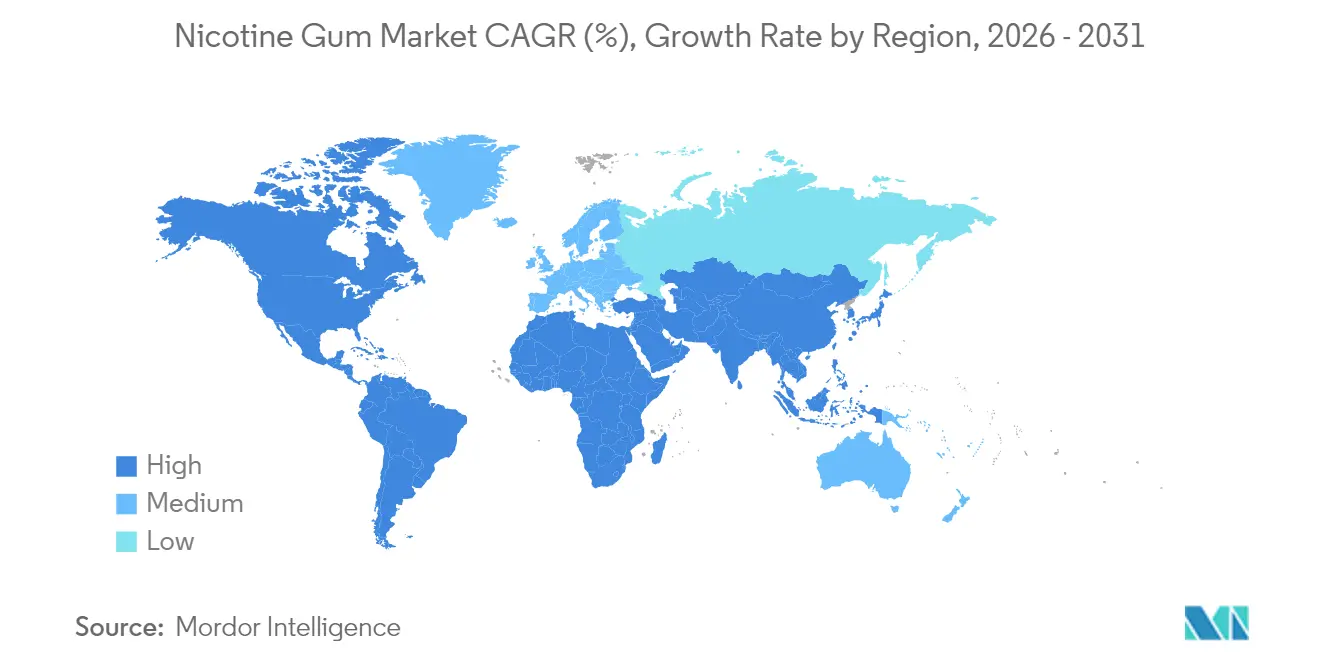

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nicotine Gum Market Analysis by Mordor Intelligence

Nicotine gum market size in 2026 is estimated at USD 1.6 billion, growing from 2025 value of USD 1.46 billion with 2031 projections showing USD 2.58 billion, growing at 9.93% CAGR over 2026-2031. Healthcare payers' focus on reducing tobacco-related diseases, regulatory requirements for cessation methods, and pharmacotherapy integration drive market growth. Global demand for nicotine replacement therapy (NRT) products has risen as more individuals attempt to quit smoking. This growth is significant in regions with robust healthcare systems and tobacco control policies. Government initiatives, including cigarette taxes, cessation programs, and anti-smoking campaigns, expand the NRT market. Manufacturers are improving product palatability through new flavors and coating technologies. Digital pharmacies enhance product accessibility while maintaining regulatory compliance. The FDA continues to approve new oral products, increasing market competition. This regulatory support has prompted pharmaceutical companies to invest in research and development. The market expansion is further supported by increased insurance coverage for cessation products and heightened awareness of tobacco-related health risks.

Key Report Takeaways

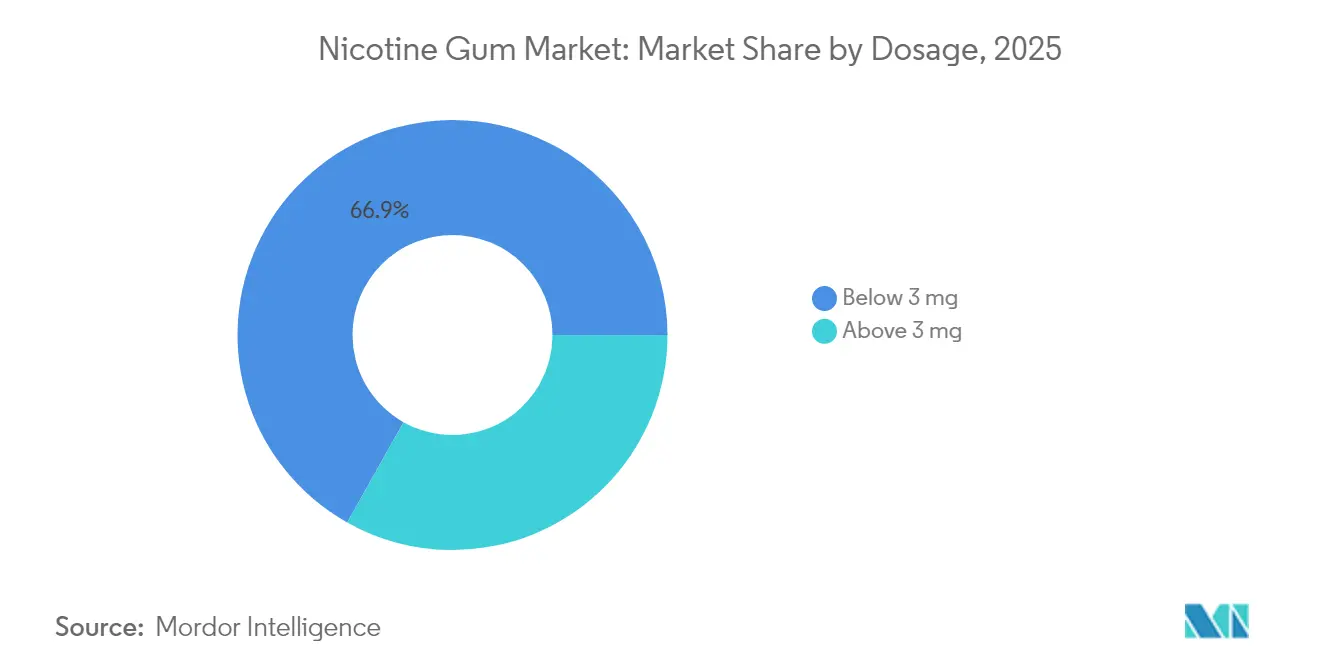

- By dosage strength, below 3 mg led with 66.85% revenue share in 2025; the above 3 mg segment is projected to expand at 9.98% CAGR through 2031.

- By flavor, mint accounted for 44.97% revenue share in 2025, whereas the fruit category is progressing at 9.99% CAGR to 2031.

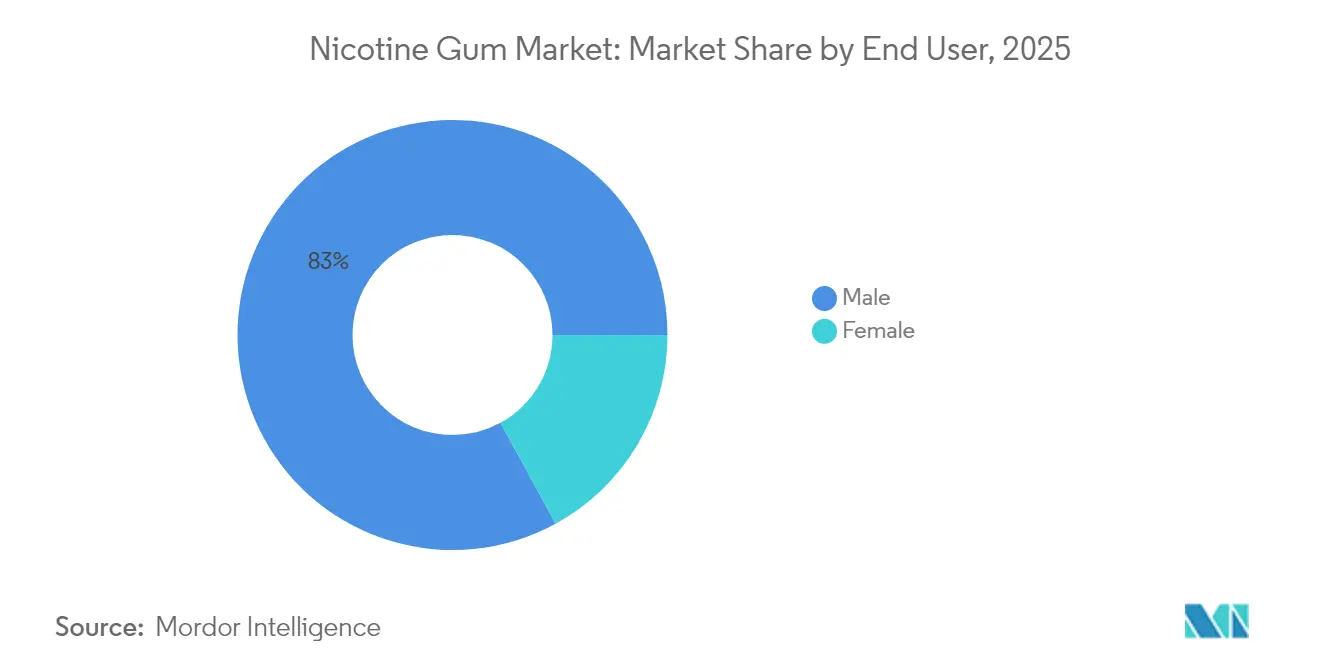

- By end-user gender, male consumers dominated with an 82.96% share in 2025, yet the female segment is climbing at a 9.95% CAGR through 2031.

- By distribution channel, drug stores/pharmacies held 61.02% of the nicotine gum market share in 2025, while online retail stores are forecast to grow at 10.18% CAGR through 2031.

- By geography, North America captured 84.12% share of the nicotine gum market in 2025, and Asia-Pacific is advancing at 10.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nicotine Gum Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Awareness about the Harmful Effects of Smoking | +1.8% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Global Anti-Smoking Initiatives and Public Health Campaigns | +1.5% | Global, particularly effective in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Rising Demand for Convenient and Discreet Smoking Cessation Products | +1.2% | North America and Europe core, expanding to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Innovations in Product Formulations and Flavored Gums | +0.9% | Global, with premium segments in developed markets | Medium term (2-4 years) |

| Physician Recommendations and Medical Support | +1.1% | North America and Europe, growing in Asia-Pacific healthcare systems | Medium term (2-4 years) |

| Collaborations with Healthcare Providers and Strategic Partnerships | +0.7% | Primarily North America and Europe, and select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Awareness about the Harmful Effects of Smoking

The increasing awareness of smoking-related health risks drives the growth of the smoking cessation products and services market. Consumers' understanding of these risks, including lung cancer, heart disease, respiratory problems, and secondhand smoke effects, has increased the demand for evidence-based solutions over reliance on willpower alone. While smoking prevalence has decreased in many regions, population growth has led to a higher total number of smokers, maintaining the demand for cessation aids such as nicotine patches, gums, lozenges, and prescription medications. The medical community's recognition of nicotine dependence as a chronic condition, rather than a lifestyle choice, has validated the use of long-term nicotine replacement therapies (NRTs). This medical perspective has expanded the market beyond short-term solutions to include comprehensive, long-term addiction management approaches, incorporating behavioral support, counseling services, and digital health applications.

Global Anti-Smoking Initiatives and Public Health Campaigns

Government tobacco control initiatives drive nicotine gum demand through frameworks that combine taxation, regulation, and cessation support. The Australian government implemented new tobacco control regulations in April 2024 [1]Source: Australian Government Department of Health and Aged Care, “Smoking and Tobacco Laws in Australia,” health.gov.au.. These regulations aim to reduce the appeal and attractiveness of tobacco products by eliminating flavor additives and standardizing product packaging. The measures restrict tobacco companies' ability to target vulnerable populations through advertising. The regulations mandate standardized dimensions for tobacco packs, pouches, and cigarette sticks. The UK government allocated GBP 70 million annually to stop smoking services in 2024, aiming to help 360,000 people quit each year, expanding the nicotine replacement therapy market [2]Source: UK Department of Health and Social Care, “Local Stop Smoking Services and Support Funding Allocations and Methodology,” gov.uk. The funding provides free nicotine replacement products, counseling services, digital support tools, and specialized programs for high-risk populations. The WHO Framework Convention on Tobacco Control supports market development through standardized approaches across jurisdictions, establishing guidelines for pricing, packaging, and cessation support programs [3]Source: World Health Organization, “Areas of Work,” WHO Framework Convention on Tobacco Control (FCTC) 2030 Project,"who.int. The framework promotes international cooperation, research sharing, and harmonized regulatory standards for tobacco control measures.

Rising Demand for Convenient and Discreet Smoking-Cessation Products

Workplace smoking restrictions and flexible work arrangements have increased demand for discreet nicotine delivery formats. Nicotine gum provides controlled dosage and oral satisfaction without the visibility of patches or inhalers. Office workers can use gum during meetings, while remote employees benefit from its on-demand stress relief compared to continuous-release alternatives. The gum format allows users to manage their nicotine intake based on individual needs and workplace schedules. Manufacturers have improved gum texture to resemble confectionery products, reducing jaw strain and eliminating the strong peppery taste characteristic of earlier formulations. The enhanced texture also promotes longer-lasting flavor and consistent nicotine release. Moreover, compact blister packaging enables convenient portability, meeting contemporary lifestyle needs. This packaging innovation has made nicotine gum more accessible and socially acceptable in various professional settings, contributing to its growing adoption among urban workers.

Innovations in Product Formulations and Flavored Gums

Companies are enhancing nicotine gum through formulation technologies that improve bioavailability, minimize side effects, and expand flavor options beyond traditional mint varieties. Research indicates that fruit and non-mint flavors improve smoking cessation success rates. The FDA's 2023 guidance for nicotine replacement therapy (NRT) products provides comprehensive frameworks for clinical development, including detailed treatment protocols and specific efficacy measurements, establishing clear regulatory pathways for innovative formulations [4]Source: Theresa Michele, M.D., “FDA Issues Final Nicotine Replacement Therapy Drug Products Guidance,” U.S. Food and Drug Administration, fda.gov. Manufacturers are creating advanced coated gum variants that effectively reduce nicotine's initial bitter taste while maintaining optimal therapeutic effectiveness, addressing a significant compliance challenge consistently identified in clinical studies. Advanced polymer technologies enable precise controlled release of nicotine throughout the extended chewing duration, substantially reducing dosing frequency and improving overall user convenience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Competition from Alternative Nicotine Replacement Therapies (NRTs) | -1.4% | Global, particularly intense in North America and Europe | Short term (≤ 2 years) |

| Limited Consumer Awareness | -0.8% | Primarily emerging markets in Asia-Pacific, the Middle East and Africa, and South America | Medium term (2-4 years) |

| Side Effects and User Discomfort | -0.6% | Global, with higher impact in markets with limited healthcare support | Short term (≤ 2 years) |

| Public Perception Challenges | -0.5% | Primarily in traditional markets with established smoking cultures | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense Competition from Alternative Nicotine Replacement Therapies (NRTs)

The FDA's marketing authorization for twenty ZYN nicotine pouch products in January 2025 marks a significant shift in oral nicotine delivery options [5]Source: U.S. Food and Drug Administration, "FDA Authorizes Marketing of 20 ZYN Nicotine Pouch Products after Extensive Scientific Review," fda.gov. Nicotine pouches eliminate the need for chewing, prevent jaw fatigue, and remain discreet under the lip, appealing to professionals who require subtlety in their workplace environments. Therapeutic vaping devices that replicate smoking behaviors receive increasing support from cessation clinics due to their effectiveness in mimicking traditional smoking habits. These new product categories divide consumer attention across multiple nicotine delivery formats, compelling nicotine gum manufacturers to highlight their established clinical background, proven safety record, and controlled dosage mechanisms to maintain their market position. The emergence of these alternative nicotine delivery systems creates additional competitive pressure in the traditional nicotine replacement therapy market.

Limited Consumer Awareness

Knowledge gaps about nicotine replacement therapy (NRT) remain prevalent outside high-income regions. Research conducted among Chinese- and Vietnamese-American smokers shows limited NRT use due to deeply rooted cultural beliefs that associate smoking cessation with personal willpower rather than medical intervention. Common misconceptions, particularly the belief of "substituting one addiction for another," significantly reduce NRT adoption rates among these communities. Users frequently encounter substantial challenges in understanding proper usage patterns, optimal timing between doses, recommended chew-rest cycles, and comprehensive treatment duration protocols. The limited availability of professional counseling services in low- and middle-income countries results in insufficient clinical guidance on dose management, including initial dosing strategies, dose escalation procedures, and tapering protocols. To address these persistent barriers effectively, manufacturers need to develop comprehensive multilingual instructions, detailed pictorial guides, and interactive digital support tools that accommodate varying literacy levels, cultural sensitivities, and provide clear, step-by-step explanations of the medical approach to smoking cessation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage: Higher Strength Gains Momentum

The below 3 mg tier dominated in 2025, capturing 66.85% of the nicotine gum market share as light and moderate smokers selected gradual tapering programs. This dominance stems from user preference for lower systemic exposure and established pharmacy inventory patterns favoring 2 mg products. The segment provides stable revenue for existing manufacturers and serves as an initial option for new users attempting to quit. However, clinical prescribing patterns are evolving. Healthcare facilities now implement the Fagerström Test for Nicotine Dependence to personalize treatment and prevent under-dosing, which studies have identified as a common relapse factor.

The above 3 mg segment demonstrates the highest growth rate, with a projected 9.98% CAGR through 2031. Heavy smokers require the elevated initial plasma concentration to manage withdrawal symptoms during the crucial first 72 hours after quitting. Improved patient retention occuers in cessation programs when 4 mg gum is included in discharge packages, resulting in continued prescription refills after patients return home. Manufacturers have developed bi-layer high-dose formulations with enhanced texture to address previous user concerns about taste and throat discomfort. This shift toward higher doses increases the average selling price and enhances gross margins in the nicotine gum market.

By Flavor: Innovation Beyond Traditional Mint

Mint maintains market leadership with 44.97% of 2025 sales value, supported by its clean aftertaste and established presence in pharmacy channels. Mint-flavored nicotine gums dominate the market, driven by several factors that enhance their appeal and effectiveness. The refreshing and cooling sensation of mint not only masks the bitter taste of nicotine but also makes the gum more enjoyable for users. Leading manufacturers, responding to strong consumer demand, prioritize mint variants in their portfolios, ensuring robust brand recognition and widespread availability. With nicotine strengths of 2 mg, 4 mg, and 6 mg, mint-flavored gums cater to varying levels of nicotine dependence, offering tailored support for those looking to quit. Additionally, market trends highlight a surge in innovations, such as sugar-free and low-calorie mint options, amplifying their allure, particularly among health-conscious consumers.

The fruit category exhibits 9.99% CAGR through flavor diversification. Premium fruit-flavored variants demonstrate higher repurchase frequency and improved cessation success rates. Manufacturers respond by developing subtle warming profiles that target adult consumers within regulatory parameters. Advanced coated-core technology enables sustained flavor release, promoting complete consumption time and enhanced nicotine absorption, contributing to increased consumer retention in the nicotine gum market.

By End User: Female Segment Emerges as Growth Driver

Male consumers account for 82.96% of total nicotine replacement therapy (NRT) purchases in 2025, reflecting traditional smoking patterns. While historical marketing emphasized masculine themes, emerging trends show increasing female smoking rates in developing economies, coupled with heightened quit attempts due to reproductive health concerns. The female segment is projected to grow at a 9.95% CAGR through 2031, influencing product development strategies. Healthcare providers are expanding NRT distribution channels, with obstetric clinics incorporating nicotine gum into prenatal care protocols and gynecologists including it in postpartum support services.

Gender-based biological differences affect treatment recommendations. Women metabolize nicotine more rapidly during specific hormonal phases, requiring more frequent gum usage to manage cravings effectively. Products featuring sugar-free formulations and mild flavors are gaining popularity among female consumers who prioritize oral health and taste preferences. Social media outreach featuring user experiences and support resources has increased NRT acceptance in female communities, contributing to market expansion.

By Distribution Channel: Digital Transformation Accelerates

Pharmacies hold a dominant 61.02% revenue share in 2025, driven by the effectiveness of in-person counseling for smoking cessation and widespread reimbursement policies for pharmacy-dispensed NRT. Health Canada implemented pharmacist-only sales regulations in Canada from August 2024, strengthening this position by directing eligible products through regulated pharmacy channels. In the United Kingdom, community pharmacists work with NHS hospital discharge teams to provide patients with nicotine gum starter packs, ensuring continuity of care from hospital to community settings.

Online stores are projected to grow at a 10.18% CAGR through 2031, driven by telepharmacy platforms that combine digital ordering with video consultations. This model meets regulatory requirements while offering convenience to consumers. Urban consumers benefit from home delivery services, while rural patients reduce travel time to physical stores. The market has developed hybrid models where pharmacists verify orders before dispatch, maintaining professional standards within the e-commerce framework. Supermarkets and hypermarkets continue to serve price-conscious consumers, though their market share decreases as healthcare integration increases. The diversification of distribution channels supports the ongoing expansion of the nicotine gum market.

Geography Analysis

North America accounted for 84.12% of revenue in 2025, driven by comprehensive insurance coverage, hospital-based opt-out protocols, and established retail networks. Indiana's "Quit Now" program reported 40% quit rates when combining nicotine replacement therapy with counseling, compared to 4-7% for unaided attempts in 2023. Canadian regulations require pharmacist involvement for specific products, providing professional oversight while maintaining accessibility. While FDA-cleared pouches and therapeutic vapes increase competition, nicotine gum maintains a strong user base who prefer its self-dosing capability and oral satisfaction.

The Asia-Pacific region demonstrates the highest growth rate at 10.44% CAGR through 2031. This growth stems from high smoking rates, particularly in lower-middle-income countries. South Asian markets offer significant potential, as research indicates major gaps in smoking cessation programs. These markets require improved coordination between anti-smoking organizations, policymakers, and healthcare professionals to develop more effective cessation strategies.

Europe maintains consistent demand through established healthcare systems. The United Kingdom provides annual funding for local smoking cessation services and the "Swap to Stop" program, which offers alternatives like nicotine gum to smokers. In Eastern Europe, lower purchasing power creates opportunities for smaller, more affordable packaging formats. South America, Africa, and the Middle East present growth potential as governments implement World Health Organization recommendations, though healthcare system development remains crucial. International companies partner with regional non-governmental organizations on smoking cessation initiatives to expand nicotine gum market presence.

Competitive Landscape

The nicotine gum industry remains moderately fragmented. Key players in the market include Kenvue Inc., Perrigo Company plc, Cipla Limited, Rusan Pharma Ltd, and ITC Limited. Companies focus on expanding their product portfolios and offering unique products, such as sugar-free gums, to differentiate themselves and meet market demand.

In June 2024, Kenvue's Nicorette gum and patch became the first nicotine replacement therapies (NRTs) to receive World Health Organization (WHO) pre-qualification status. The WHO pre-qualification list evaluates medicinal products' quality, safety, and efficacy, guiding UN agencies and international organizations regarding medicine quality in high-priority therapeutic areas, particularly for low-income countries.

Product development continues to evolve in the market. New bi-layer gum formulations provide immediate and sustained nicotine release to address both acute and ongoing cravings. Manufacturers collaborate with confectionery specialists to develop stable fruit flavors resistant to humidity changes. Companies with manufacturing facilities across multiple continents demonstrate supply chain advantages by reducing geographic and currency risks. As health authorities increasingly approve oral nicotine alternatives, gum manufacturers must demonstrate their products' specific benefits, including precise dosing capabilities and proven effectiveness, while maintaining brand strength in an expanding market.

Nicotine Gum Industry Leaders

-

Kenvue Inc.

-

Perrigo Company plc

-

Cipla Limited

-

Rusan Pharma Ltd

-

ITC Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: ALIBARBAR introduced nicotine gum in a traditional gum canister design with clear nicotine content labeling. Each gum piece contains 3 mg of nicotine, providing consumers with a familiar smoke-free nicotine delivery format.

- June 2024: Dr. Reddy's Laboratories signed an agreement to acquire the nicotine replacement therapy (NRT) business of British consumer healthcare firm Haleon outside the United States market for INR 5,276 crore. The acquisition includes the global NRT brand Nicotinell and its local market-leading brands Nicabate, Habitrol, and Thrive in markets outside the United States.

- May 2024: Ryze, a nicotine gum brand owned by Fertin Pharma, has partnered with digital commerce firm 100days to expand its presence in the Indian market. The company has conducted market research to develop nicotine gums in flavors suited to Indian preferences, including mint, fruit, saunf, pudina, and paan.

- May 2023: Perrigo Company PLC, a leading provider of Consumer Self-Care Products, announced that it had received final approval from the US Food and Drug Administration for Nicotine Coated Mint Lozenges to be sold as 2 mg and 4 mg over-the-counter (OTC).

Global Nicotine Gum Market Report Scope

Nicotine gum is a chewing gum that contains nicotine and is used to help people stop smoking. The Nicotine gum market is segmented by type, distribution channel, and geography. By type, the market is segmented into 2 mg nicotine gum and 4 mg nicotine gum. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores/tobacco stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Below 3 mg |

| Above 3 mg |

| Mint |

| Fruit |

| Others |

| Male |

| Female |

| Supermarkets/Hypermarkets |

| Drug Stores/Pharmacies |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | United Kingdom |

| France | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Dosage | Below 3 mg | |

| Above 3 mg | ||

| By Flavor | Mint | |

| Fruit | ||

| Others | ||

| By End User | Male | |

| Female | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Drug Stores/Pharmacies | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| France | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the nicotine gum market?

The nicotine gum market size is USD 1.6 billion in 2026 and is projected to reach USD 2.58 billion by 2031

Which region leads global sales

North America leads with 84.12% of revenue in 2025 due to mature healthcare integration and insurance coverage.

Which region will grow fastest through 2031?

Asia-Pacific is forecast to expand at a 10.44% CAGR, supported by rising smoking prevalence and broader access to pharmaceutical cessation aids.

What dosage strength is gaining most momentum?

Above 3 mg gum is the fastest growing segment, expected to rise at 9.98% CAGR as clinicians prescribe higher doses for heavy smokers.

Page last updated on: