Trade Surveillance Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

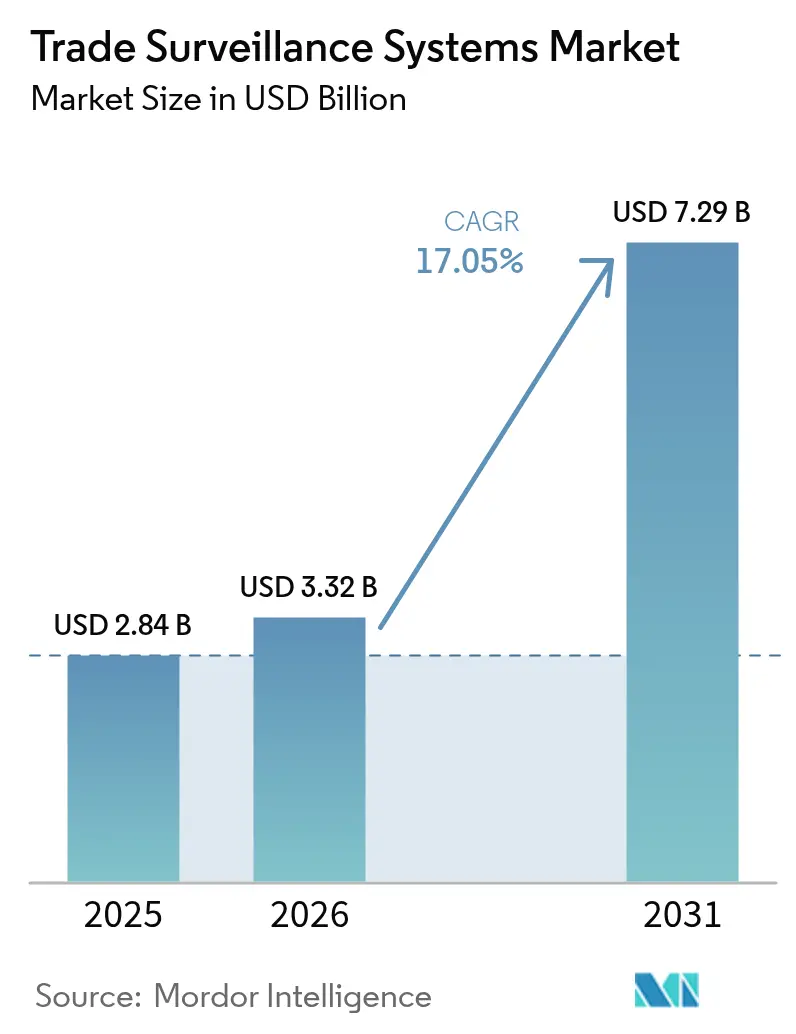

| Market Size (2026) | USD 3.32 Billion |

| Market Size (2031) | USD 7.29 Billion |

| Growth Rate (2026 - 2031) | 17.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trade Surveillance Systems Market Analysis by Mordor Intelligence

Trade Surveillance Systems market size in 2026 is estimated at USD 3.32 billion, growing from 2025 value of USD 2.84 billion with 2031 projections showing USD 7.29 billion, growing at 17.05% CAGR over 2026-2031. Heightened reporting mandates such as the United States’ Consolidated Audit Trail (CAT) and Europe’s evolving MiFID II framework are the core catalysts. Institutions now need near-real-time analytics that screen more than 150,000 transactions per second and spot suspicious patterns with 97.5% accuracy, pushing vendors toward high-performance, AI-driven architectures. Cloud deployment lowers upfront capital requirements, while hybrid models address data-sovereignty concerns. Rapid growth in crypto and tokenized assets adds complexity, forcing surveillance platforms to expand beyond traditional equities and derivatives.

Key Report Takeaways

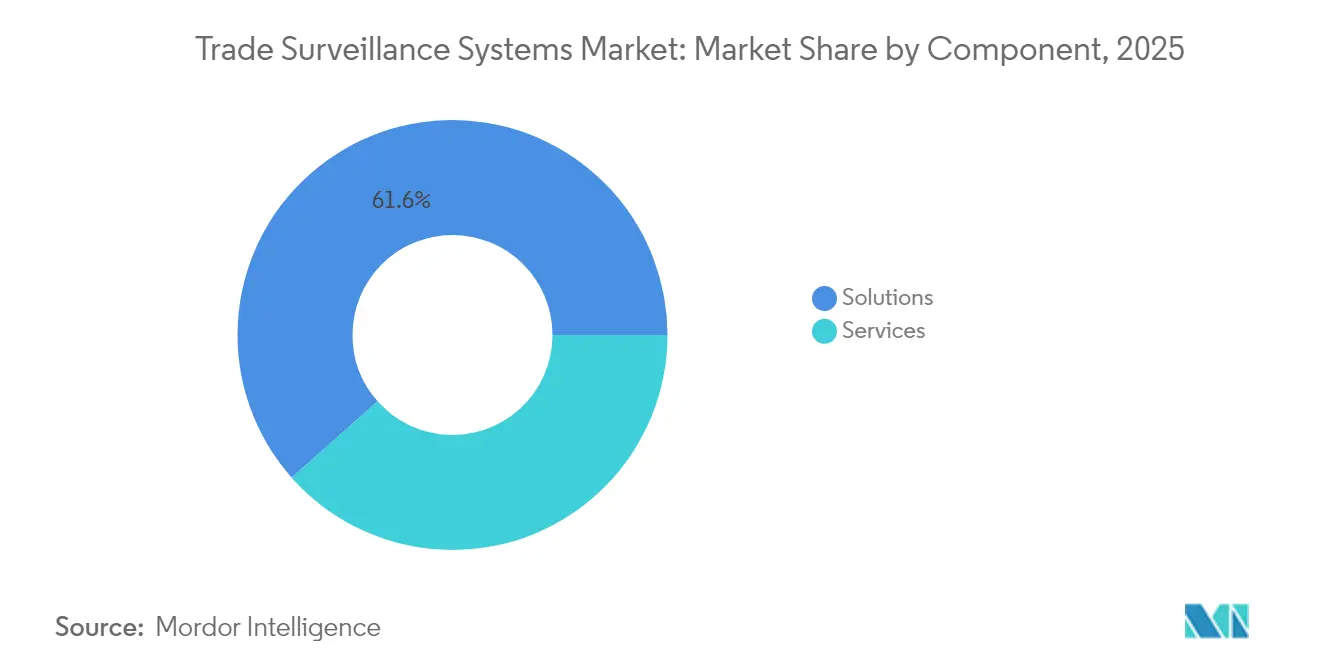

- By component, solutions led with 61.55% of the trade surveillance systems market share in 2025; services are projected to climb at an 18% CAGR through 2031.

- By deployment mode, on-premise held 54.15% share of the trade surveillance systems market size in 2025, while cloud is forecast to expand at 19.05% CAGR between 2026-2031.

- By trading type, equities accounted for a 32.10% share of the trade surveillance systems market size in 2025; digital assets are advancing at a 19.7% CAGR to 2031.

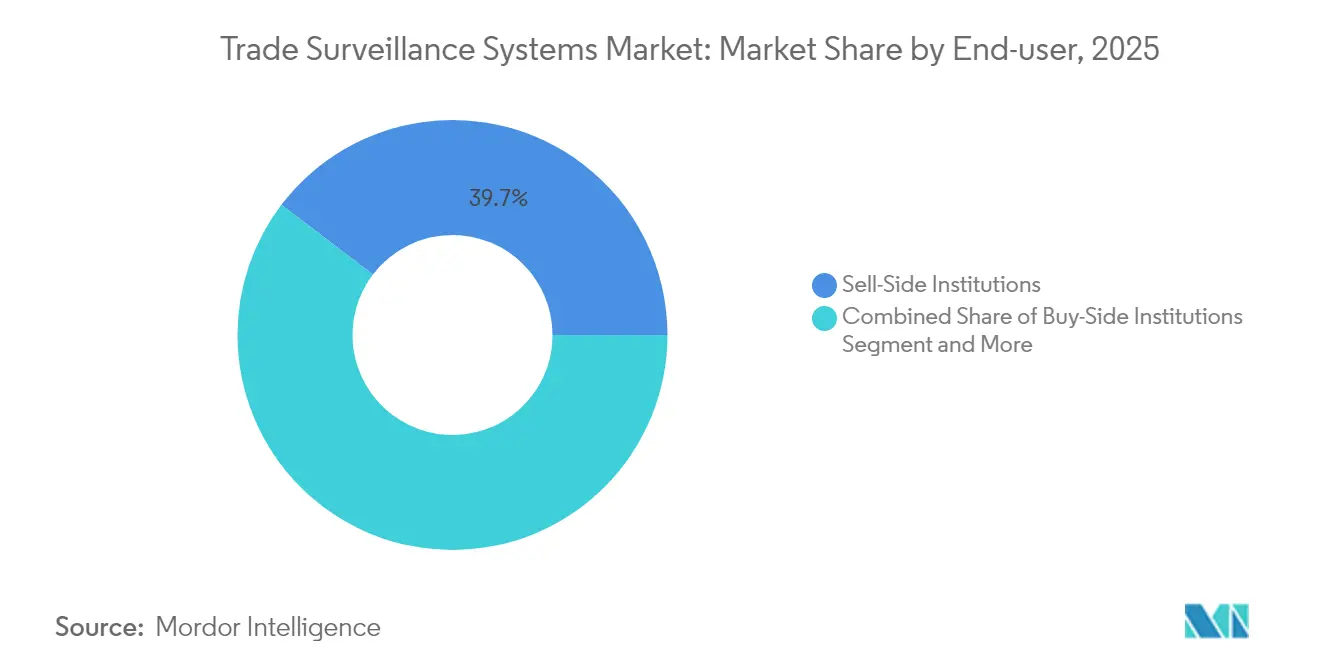

- By end-user, sell-side institutions captured 39.65% of the trade surveillance systems market share in 2025; buy-side firms record the highest projected CAGR at 18.2% through 2031.

- By organisation size, tier-1 global banks commanded 35.65% share of the trade surveillance systems market size in 2025, while FinTech and crypto exchanges are growing at 21.4% CAGR.

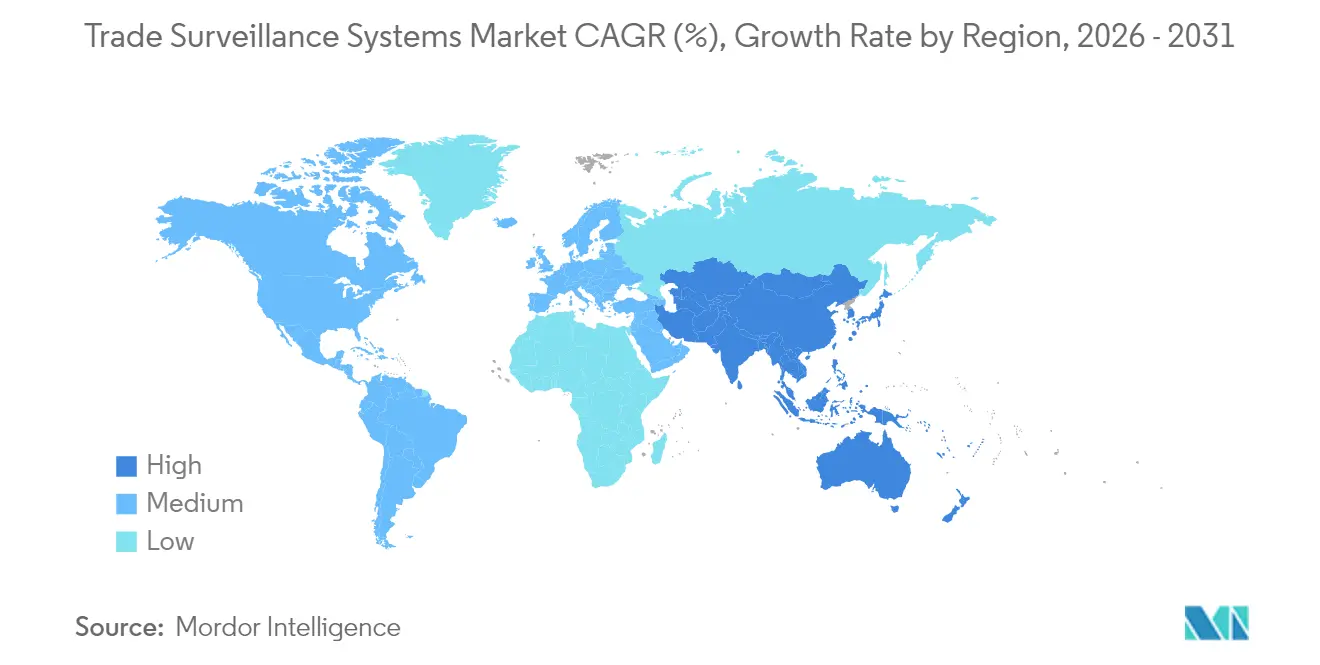

- By geography, North America led with a 33.92% share in 2025; Asia-Pacific exhibits the fastest regional CAGR of 17.6% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Trade Surveillance Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of global multi-asset electronic trading venues | +3.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Mandatory consolidated audit trail (CAT) and other post-trade transparency mandates | +2.8% | North America primary, EU secondary | Short term (≤ 2 years) |

| AI/ML-powered anomaly detection reduces false positives and compliance costs | +4.1% | Global, led by APAC innovation hubs | Long term (≥ 4 years) |

| Cloud-native SaaS delivery lowering total cost of ownership | +3.5% | Global, accelerated in emerging markets | Medium term (2-4 years) |

| Growing adoption of crypto and digital-asset trading by regulated institutions | +2.2% | Global, with regulatory clarity in EU and Singapore | Medium term (2-4 years) |

| Tokenisation of real-world assets creating new surveillance blind spots | +1.9% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Multi-Asset Electronic Trading Venues

High-frequency and algorithmic strategies now drive more than half of US equity volumes, creating surveillance blind spots that legacy rule sets struggle to cover. Firms must correlate order books across equities, fixed income, options, and commodities while accounting for millisecond latency gaps that enable cross-venue arbitrage. The shift from dealer models to fully automated order-driven venues in London illustrates how liquidity gains coexist with higher market-abuse risk. [1]Financial Conduct Authority, “Equity Market Structure Literature Review Part II: High Frequency Trading,” sec.gov Vendors respond by unifying data feeds and embedding venue-specific calibrations that flag spoofing and layering across fragmented markets.

Mandatory CAT and Other Post-Trade Transparency Mandates

The CAT regime obliges US brokers to report every equity and option event under one schema. A March 2025 amendment trimmed personal data fields yet preserved unique identifiers, saving firms USD 12 million yearly while keeping regulators fully informed. Similar pressure builds in Europe, where MiFIR 3 introduces digital-token identifiers and new effective-date tags, compelling upgrades to handle richer payloads. Institutions, therefore, treat surveillance as foundational compliance infrastructure rather than optional risk tooling.

AI/ML-Powered Anomaly Detection Reducing False Positives and Cost

Next-generation platforms move beyond static thresholds toward machine-learning models that learn trader behavior. Detection rates exceed 97% while false positives fall below 1%. Natural-language processing links voice and chat surveillance to trade data so that seemingly benign orders can be tied back to collusive communications. Regulators stress explainability: algorithms must log the features that triggered an alert so supervisors can audit decisions. As a result, vendors now embed transparent model-risk dashboards and human-in-the-loop workflows.

Cloud-Native SaaS Delivery Lowering Total Cost of Ownership

Financial firms increasingly offload compute-heavy analytics to cloud providers, scaling CPU and GPU capacity during volatile sessions without buying hardware. Elastic pricing cuts capital budgets while automatic patching eases cybersecurity burdens. Yet institutions must keep sensitive identifiers within national borders, driving hybrid models that retain raw data on-premise and burst anonymized data to the cloud for model training.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High integration complexity with legacy front-, middle- and back-office systems | -2.1% | Global, acute in established financial centers | Medium term (2-4 years) |

| Shortage of trade-surveillance data-science talent | -1.8% | Global, severe in emerging markets | Long term (≥ 4 years) |

| Fragmented global rule sets leading to costly rule-mapping | -0.8% | EU and North America regulatory markets | Long term (≥ 4 years) |

| Rising privacy regulations limiting holistic surveillance data pooling | -0.6% | Global, with concentration in regulated industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy Front-, Middle- and Back-Office Systems

Nearly 92% of UK institutions still rely on mainframes that batch-process trade files overnight, a cadence incompatible with second-by-second surveillance. Bridging message protocols, field taxonomies, and clock synchronisation requires multi-year roadmaps, often involving 50-plus internal teams. Disconnects cause incomplete data feeds and missed alerts, forcing parallel run periods where old and new platforms coexist until regulators certify data integrity.

Shortage of Trade-Surveillance Data-Science Talent

Demand for professionals who understand both capital-market microstructure and advanced statistics far outstrips supply. Industry studies highlight deficits across blockchain analytics, natural-language processing, and graph-network modelling. Vendors launch training academies to close the gap, but in the short term, banks lean on managed services that bundle model maintenance and regulatory updates, raising vendor-dependency risk for smaller firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Drive Market Foundation

Solutions held 61.55% of the trade surveillance systems market share in 2025, underscoring the primacy of end-to-end platforms that integrate order, execution, and communications data. The segment benefits from high switching costs and continual rule updates, positioning vendors for recurring licensing revenue. The trade surveillance systems market size attached to solutions is projected to lift steadily as banks renew enterprise licences before key regulatory deadlines.

Services, though smaller, grow at 18% CAGR as institutions outsource model tuning and regulatory mapping. Managed-service contracts fill in-house talent gaps and provide 24-hour coverage across regions. Providers bundle implementation, behavioural-model calibration, and post-go-live testing, a package that mid-tier brokers consider more cost-effective than hiring specialised quants.

By Deployment Mode: Cloud Migration Accelerates

On-premise deployments retained a 54.15% share in 2025, reflecting data-sovereignty obligations and auditor preference for systems housed within firewalls. Yet the trade surveillance systems market size attributed to cloud offerings is set to rise fastest, expanding at 19.05% CAGR through 2031 as regulators issue clarifications that encrypted data may reside in approved jurisdictions.

Cloud providers offer elastic compute for back-testing millions of scenarios overnight, an ability that on-premise grids struggle to replicate without oversizing. Hybrid models gain traction because they keep personally identifiable information in local data centres while diverting de-identified trade records to cloud clusters for heavy analytics. Successful pilots in Singapore and Canada demonstrate that such architectures pass regulatory inspection when encryption keys remain client-controlled.

By Trading Type: Digital Assets Transform Surveillance

Equities, with 32.10% of the trade surveillance systems market share in 2025, remain the anchor segment thanks to decades-old reporting rules. Fixed income, derivatives, and FX each add layers of complexity, especially when OTC trades must be matched to exchange prints for full lifecycle visibility.

Digital assets represent the fastest-growing slice at 19.7% CAGR. Platforms must ingest blockchain events, map wallet addresses to legal entities, and detect cross-chain wash trading. Under MiCA, European service providers must show continuous monitoring of decentralised exchanges, driving demand for token-aware analytics that score smart contracts and flag suspicious liquidity pools. The trade surveillance systems market size tied to crypto monitoring could double by the decade’s end as tokenisation of real-world assets broadens the perimeter.

By End-user: Buy-Side Institutions Drive Growth

Sell-side firms controlled 39.65% of the trade surveillance systems market share in 2025, a legacy of long-standing best-execution and market-making obligations. Their complex order flows and proprietary trading desks require multi-layered alert logic and extensive audit trails.

Buy-side entities expand spending at an 18.2% CAGR. Asset managers see surveillance as proof of fiduciary duty and a safeguard against internal misuse of information. Pension funds and insurers integrate alerts into portfolio-management systems to catch crossing violations and unauthorised short selling. These firms previously relied on brokers’ controls, but regulatory guidance now emphasises direct oversight, fuelling vendor pipelines.

By Organisation Size: FinTech Exchanges Lead Innovation

Tier-1 global banks accounted for 35.65% of the trade surveillance systems market size in 2025 and continue to allocate nine-figure budgets to maintain enterprise licences, redundancy zones, and global support desks. Tier-2 and regional brokers typically adopt scaled-down versions, balancing compliance needs with budget limits.

FinTech and crypto exchanges grow revenue at 21.4% CAGR, propelled by venture funding and the race to win institutional crypto order flow. They require cloud-native, API-centric tools that integrate with decentralised protocols and deliver risk scores in seconds, supporting rapid asset listings and high throughput. Vendor blueprints often position these exchanges as launch customers for innovative features later backported to traditional markets.

Geography Analysis

Asia-Pacific records the fastest regional CAGR of 17.6%, moving from follower to front-runner in supervisory technology. Monetary Authority of Singapore pilots AI-based AML-CFT models that feed into trade-surveillance controls, creating reference implementations that other regulators monitor closely. Hong Kong mandates surveillance coverage for licensed virtual-asset operators, lifting spending among exchanges and prime brokers.

North America remains the largest contributor with a 33.92% share, driven by CAT and planned short-sale flags that take effect mid-2025. The United States benefits from vendor proximity to major equity and options venues, while Canada accelerates investment as cross-listing volumes climb.

Europe holds a mature adopter profile where MiFID II and EMIR already embed strict transaction reporting. Upcoming MiFIR 3 changes introduce digital-token identifiers that widen the regulatory perimeter. Continental banks upgrade systems to reconcile trade identifiers across business lines, and UK firms run parallel processes to manage post-Brexit divergence.

Regulatory Landscape

Trade surveillance demand is anchored in expanding audit-trail, market-abuse, and data-quality obligations across major jurisdictions. In the United States, the SEC continued to shape supervisory expectations around surveillance effectiveness and audit data infrastructure through its FY 2026 Examination Priorities, and in April 2026 it issued a concept release reviewing the Consolidated Audit Trail (CAT) and other audit trails with emphasis on cybersecurity, privacy, and cost-efficient technology approaches. This keeps pressure on firms to maintain resilient, scalable data capture and monitoring capabilities.

In Europe, crypto-asset market integrity requirements advanced through Commission Delegated Regulation (EU) 2025/885 under MiCA, which set detailed market-abuse prevention, detection, and reporting expectations, including coverage relevant to DLT-based activity. ESMA work on MiFIR-related technical standards and the March 2026 application of updated MiFIR transparency requirements for non-equity instruments increased the complexity of surveillance for bonds and derivatives. The result is reinforced multi-asset coverage, standardized reporting workflows (including STOR processes), and stronger control evidence for cross-venue investigations.

Value Chain Analysis

The value chain starts with data acquisition and normalization, ingesting exchange and venue market data, order and execution events, reference data, and increasingly communications and digital-asset signals. This stage depends on connectors to OMS/EMS, market-data vendors, and voice/chat capture, and it is often constrained by legacy batch environments and inconsistent taxonomies. Those frictions drive demand for integration services and pre-built adapters.

Analytics and case-management layers translate these inputs into alerts, investigations, and regulatory reporting. Vendors such as NICE Actimize and Nasdaq (SMARTS), as well as FIS and specialists including Eventus Systems, SteelEye, Scila, eFlow Global, and Solidus Labs, compete on detection models (rules plus ML), explainability, and multi-asset scenario coverage. Deployment is split across on-premise, cloud, and hybrid architectures to address data-sovereignty and auditability. Downstream, compliance operations and managed-services providers tune models, maintain regulatory rule content, and support evidencing and testing, which supervisory reviews and standards setters such as IOSCO increasingly emphasize (including in its 2025 thematic review of technological challenges to effective market surveillance).

Competitive Landscape

The market shows moderate consolidation. A small cohort of global vendors supplies multi-asset coverage, AI libraries, and regulatory content updates on a rolling basis. NICE Ltd posted USD 2.7 billion in 2024 revenue, with cloud sales advancing 25% to USD 2 billion, signalling strong uptake of hosted surveillance. [3]NICE Ltd, “Annual Report 2024,” nice.com Nasdaq’s SMARTS platform covers more than 200 markets worldwide and ships pre-configured behaviours for spoofing, cross-product manipulation, and crypto wash trading. [4]Nasdaq, “Trade Surveillance & Market Abuse Software (SMARTS),” nasdaq.com

Strategic alliances between surveillance vendors and hyperscale clouds shorten deployment cycles and bundle encryption, key management, and compliance certifications. Patents rise in graph analytics and blockchain forensics, areas where start-ups such as Solidus Labs specialise in wallet risk scoring and cross-chain heuristics. M&A activity targets communication-surveillance specialists so that trade and voice data converge in one conduct-risk console. Nevertheless, new entrants leverage open-source big-data frameworks to undercut incumbents on price, keeping competitive intensity elevated.

Institutions increasingly demand explainability. Vendors now embed visual model interpretability, scenario replay, and policy-version control to satisfy audit queries. Product roadmaps emphasise SaaS subscription models and marketplace connectors that ingest unstructured data so compliance teams can pivot quickly when new products—such as tokenised bonds—launch.

Trade Surveillance Systems Industry Leaders

NICE Ltd.

Nasdaq Inc.

BAE Systems Digital Intelligence

Fidelity National Information Services Inc. (FIS)

Software AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace sits in unifying surveillance across fragmented data domains: transaction events, e-comms, and digital-asset workflows, with governance that stands up to supervisory scrutiny. Firms are also tightening model lifecycle controls for conduct and market-abuse detection, aligning with 2026 oversight priorities that emphasize data quality and the effectiveness of surveillance testing (for example, FINRA focus areas). That shift raises demand for platforms that operationalize explainability, produce repeatable test evidence, and consolidate control dashboards, beyond alert generation.

Digital-asset and tokenized-market surveillance remains an active build-out area, supported by concrete regulatory and infrastructure moves. The European Commission adopted MiCA-related technical standards for market-abuse controls (Commission Delegated Regulation (EU) 2025/885), expanding requirements for detecting and reporting abusive behavior in crypto-asset markets. On the vendor and market-infrastructure side, Nasdaq partnered with Talos in March 2026 to connect trade surveillance with digital-asset infrastructure for tokenized collateral workflows. This highlights a commercial pathway for surveillance vendors to extend coverage into tokenized instruments without forcing institutions to rebuild their surveillance stack from scratch.

Recent Industry Developments

- March 2026: Nasdaq partnered with Talos to integrate Nasdaq trade surveillance capabilities with Talos digital-asset infrastructure supporting tokenized collateral management workflows. The move connects surveillance to digital-asset market plumbing, expanding monitoring coverage where traditional order and trade data must be correlated with tokenized asset activity.

- February 2026: Japan Exchange Group's Osaka Exchange selected Nasdaq Eqlipse Trading and Market Surveillance technology. The win reinforces exchange-led modernization of trading and monitoring stacks and creates a reference deployment that can accelerate adoption of integrated trading-surveillance platforms in other venues.

- May 2025: NICE Actimize added generative AI capabilities (Actimize Intelligence) into its SURVEIL-X Holistic Conduct Surveillance offering. The update targets investigation efficiency by helping compliance teams triage alerts and navigate multi-source conduct risk data, supporting the market shift toward AI-assisted surveillance operations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The market is defined as software platforms and related services used to monitor, detect, investigate, and document potentially abusive or noncompliant trading activity across financial markets, which supports compliance teams, risk teams, and market oversight functions.

Scope exclusions: We exclude in house internal build costs that are not commercialized, as well as broader AML transaction monitoring and general fraud tools that are not purpose-built for trade surveillance use cases.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- On-Premise

- Cloud

- By Trading Type

- Equities

- Fixed Income

- Derivatives

- Foreign Exchange

- Commodities

- Digital Assets

- By End-user

- Sell-Side Institutions

- Buy-Side Institutions

- Market Venues and Exchanges

- Regulators and SROs

- By Organisation Size

- Tier-1 Global Banks

- Tier-2 and Mid-Sized Firms

- Small FIs and Broker-Dealers

- FinTech and Crypto Exchanges

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Singapore

- Malaysia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public rulemaking and enforcement signals because they shape adoption timing and required coverage. We referenced materials such as SEC and FINRA publications, CFTC updates, ESMA guidance, and IOSCO papers to anchor surveillance obligations, reporting expectations, and market conduct definitions.

To quantify the demand environment, we also reviewed exchange and regulator statistical releases, public annual reports and investor presentations from relevant firms, and reputable press coverage of compliance programs and market integrity actions. Where available, paid subscriptions supporting company financials and news were used to sanity-check revenue ranges and corporate activity, and patent databases helped confirm where analytics and alerting capabilities are evolving. These examples are illustrative only, and many other public sources were reviewed for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on compliance leaders, surveillance managers, operations teams, and technology buyers who run or procure surveillance programs for sell-side and buy-side institutions, venues, and related oversight bodies. We used these conversations to confirm what is counted as trade surveillance spending, how cloud migration and data retention choices affect budgets, and which asset classes (including digital assets where applicable) are being brought into monitoring.

Coverage was balanced across major financial centers so that regional regulation intensity and adoption maturity were not overrepresented, and follow-ups were done when desk signals and interview feedback did not align on pricing or deployment mix.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 17% | APAC: 49% |

| Mid tier: 51% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 22% | Managers: 52% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where regulated trading activity and the supervision footprint were reconstructed by region and institution type, then converted into an addressable surveillance spending pool using adoption and budget-share assumptions. Once that structure was set, selective bottom-up checks were applied using sampled vendor revenues, channel feedback on typical contract values, and seat or account level pricing patterns to keep totals realistic.

Inputs used in the model included the number and type of regulated institutions and venues, surveillance coverage across asset classes (equities, fixed income, derivatives, FX, commodities, and relevant digital assets), the share of cloud deployments versus on-premise, typical alert volumes and case workloads that drive module usage, and compliance program expansion tied to enforcement intensity. Forecasts relied on scenario analysis supported by expert consensus, where adoption speed, pricing progression, and regulatory change timing were varied and then rebalanced to a central case. When gaps appeared in bottom-up checks for smaller regions or niche participants, ranges were carried forward and normalized using institution counts and spending benchmarks shared in interviews.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals such as enforcement activity, compliance hiring trends, and visible platform replacement cycles so that growth did not run ahead of practical buying capacity. Variance checks were run across regions, deployment mix, and end-user groups, and any unusual jumps were reviewed again before numbers were finalized.

The model and assumptions go through multi-step analyst review, and we re-contact sources when key inputs shift, such as major rule changes or unusually large contract announcements. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Trade Surveillance Systems Market Estimate Compared With Other Published Estimates

Published market sizes for trade surveillance systems can look far apart because firms do not always count the same buyer spend, deployment scope, and asset class coverage. Differences also come from how pricing is escalated over time, how much services are bundled with software, and how often assumptions are updated.

The main gap comes from whether the estimate is built around third-party platform spend only or whether it also rolls in adjacent compliance tooling and internal build costs, and then Mordor Intelligence counts revenue only for purpose-built trade surveillance solutions and related services that are sold commercially across covered regions and asset classes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.84 B (2025) | |

| Industry Research Publisher A | USD 2.70 B (2025) | Uses a spend-only lens focused on third-party systems, which can undercount bundled services and wider asset-class coverage when institutions expand surveillance beyond the initial rollout. |

| Industry Research Publisher B | USD 2.10 B (2025) | Applies a tighter product definition and more conservative pricing progression, and it may treat cloud migration and enterprise-wide deployments as slower, which reduces near-term market value. |

The spread in the table is mostly explained by scope choices and how pricing and adoption are pushed forward year to year. By tying the size to identifiable demand drivers like regulated participation, asset-class coverage, and deployment mix, the resulting value stays traceable to clear assumptions that can be rechecked and updated.

Key Questions Answered in the Report

What is the current size of the trade surveillance systems market?

The trade surveillance systems market size stands at USD 3.32 billion in 2026 and is forecast to grow to USD 7.29 billion by 2031.

Which region leads the adoption of trade surveillance solutions?

North America holds the largest regional share at 33.92%, driven by the Consolidated Audit Trail and other transparency mandates.

Why are digital assets a key growth area for surveillance vendors?

Crypto-asset markets expand at 19.7% CAGR, and new regulations such as MiCA require exchanges to detect wash trading and cross-chain abuse.

How does cloud deployment benefit compliance teams?

Cloud-native architectures scale analytics capacity on demand, cut upfront hardware spend, and provide rapid access to AI services while supporting hybrid data-sovereignty models.

What is the main challenge when upgrading legacy surveillance platforms?

Integrating real-time analytics with batch-oriented mainframe systems demands complex data-mapping and clock-synchronisation work across multiple internal teams.

Is there a skills gap in trade surveillance?

Yes, firms struggle to hire specialists who combine market-structure knowledge with data-science expertise, which boosts demand for managed surveillance services.

Page last updated on: