GDPR Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

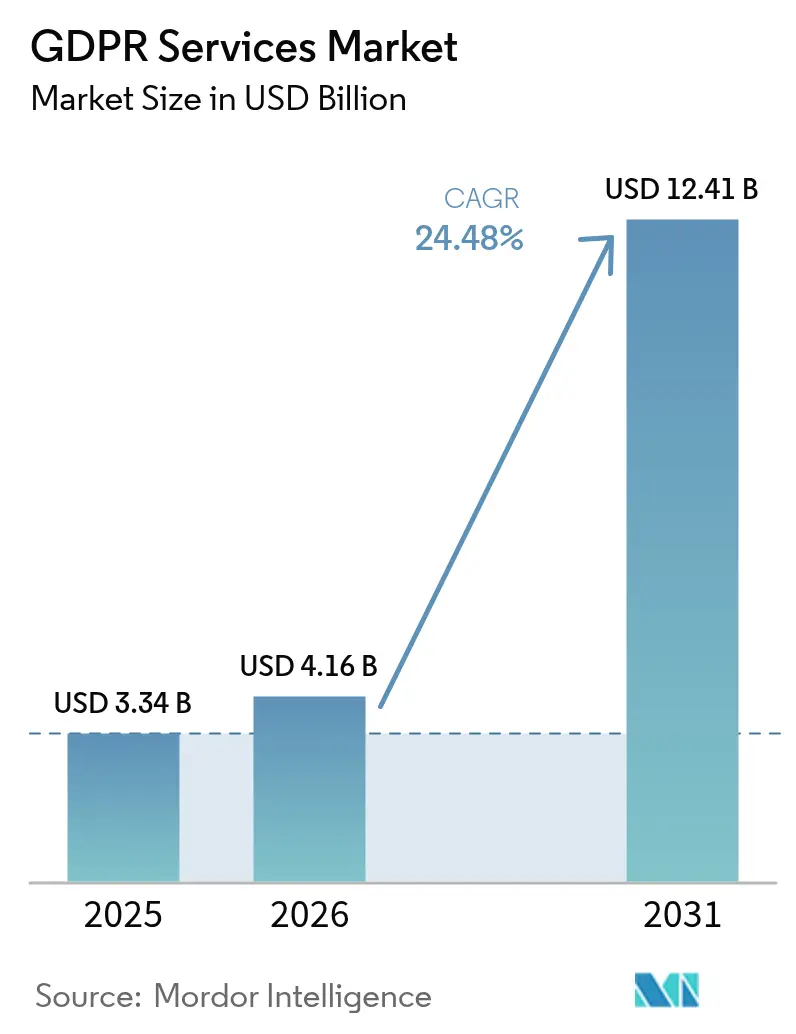

| Market Size (2026) | USD 4.16 Billion |

| Market Size (2031) | USD 12.41 Billion |

| Growth Rate (2026 - 2031) | 24.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GDPR Services Market Analysis by Mordor Intelligence

The GDPR services market size was valued at USD 3.34 billion in 2025 and estimated to grow from USD 4.16 billion in 2026 to reach USD 12.41 billion by 2031, at a CAGR of 24.48% during the forecast period (2026-2031). The growth trajectory reflects enterprises shifting from penalty-avoidance to proactive privacy programs as European data-protection authorities levied EUR 1.2 billion in fines during 2024. Heightened cross-border data transfers following Brexit, along with the EU-U.S. Data Privacy Framework, opened compliance gaps that vendors address with automated discovery engines and privacy-by-design blueprints. Rising cloud adoption, the surge of AI-powered data-mapping tools, and expanding sectoral oversight in finance and energy further accelerate demand for end-to-end governance platforms. Competitive intensity remains moderate; leading software providers integrate consent management, data classification, and continuous monitoring, while global consultancies expand managed-service portfolios to meet the persistent shortage of certified privacy officers.

Key Report Takeaways

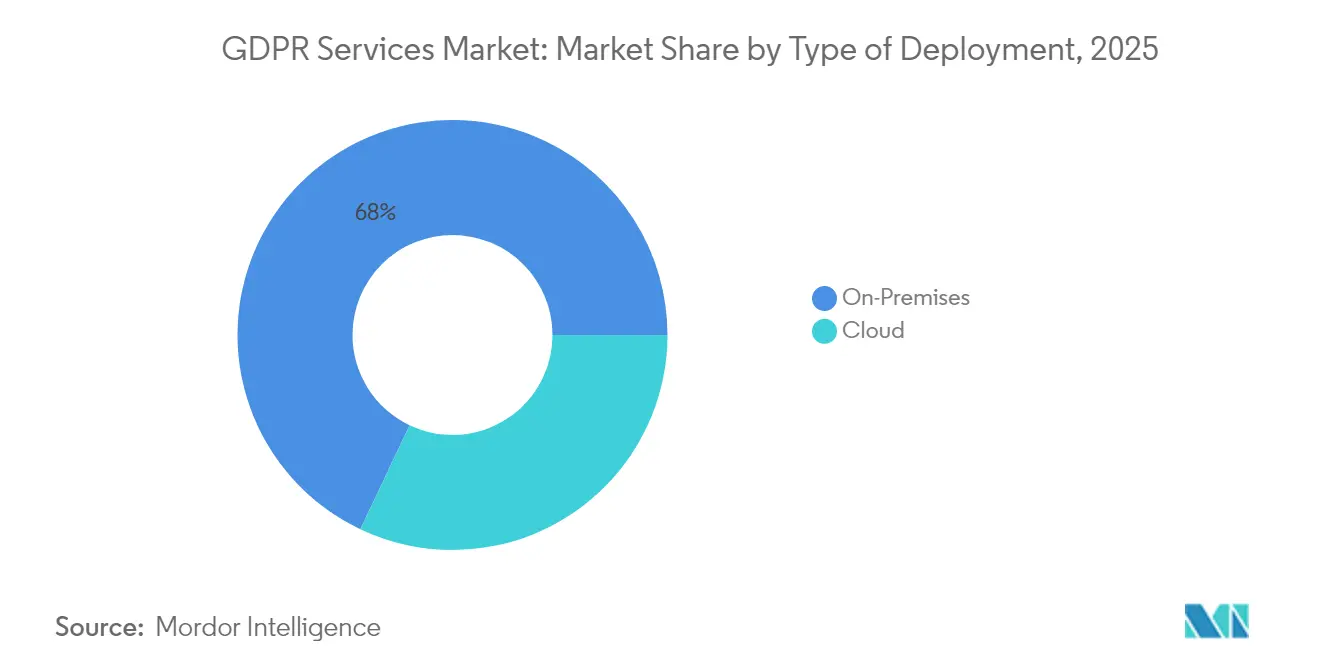

- By type of deployment, on-premises solutions held 67.95% revenue share of the GDPR services market size in 2025, while cloud-based offerings are forecast to expand at 26.2% CAGR.

- By offering, solutions captured 58.05% share of the GDPR services market size in 2025; services are expected to grow at 25.7% CAGR through 2031.

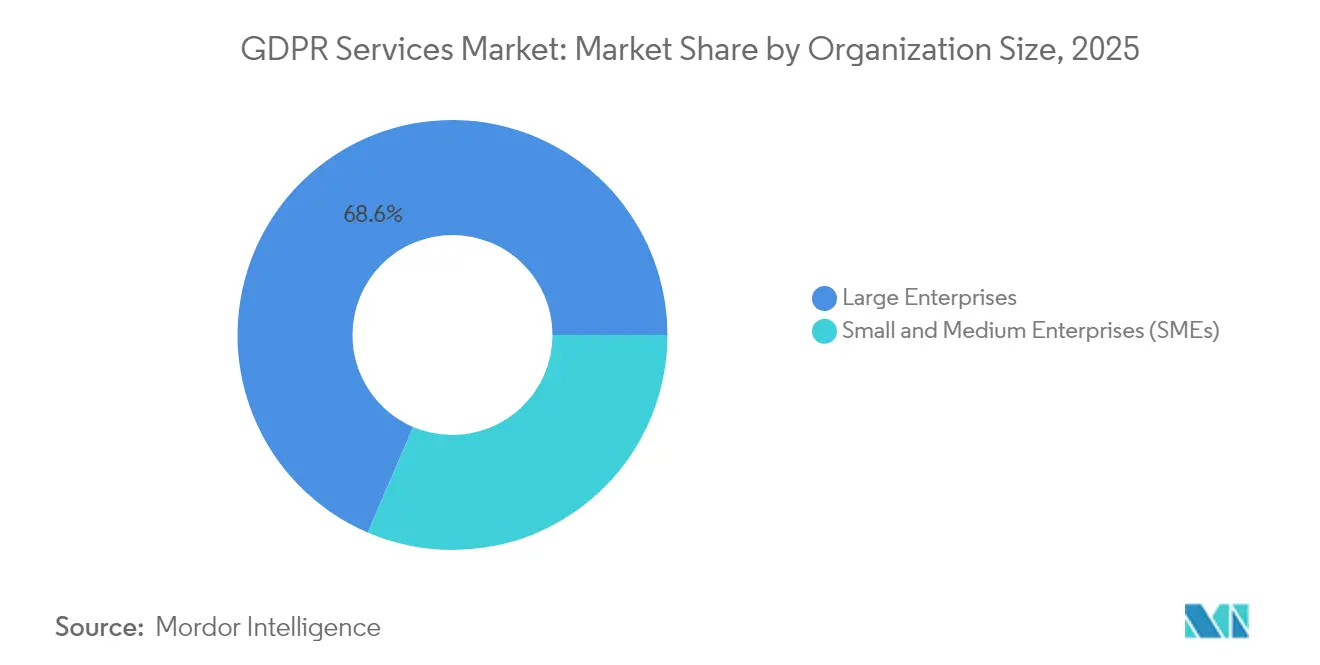

- By organization size, large enterprises controlled 68.55% spending in 2025, but SMEs are advancing at a 26.0% CAGR to 2031.

- By end user, banking, financial services and insurance commanded 34.85% of GDPR services market share in 2025, while retail and consumer goods should accelerate at 24.9% CAGR.

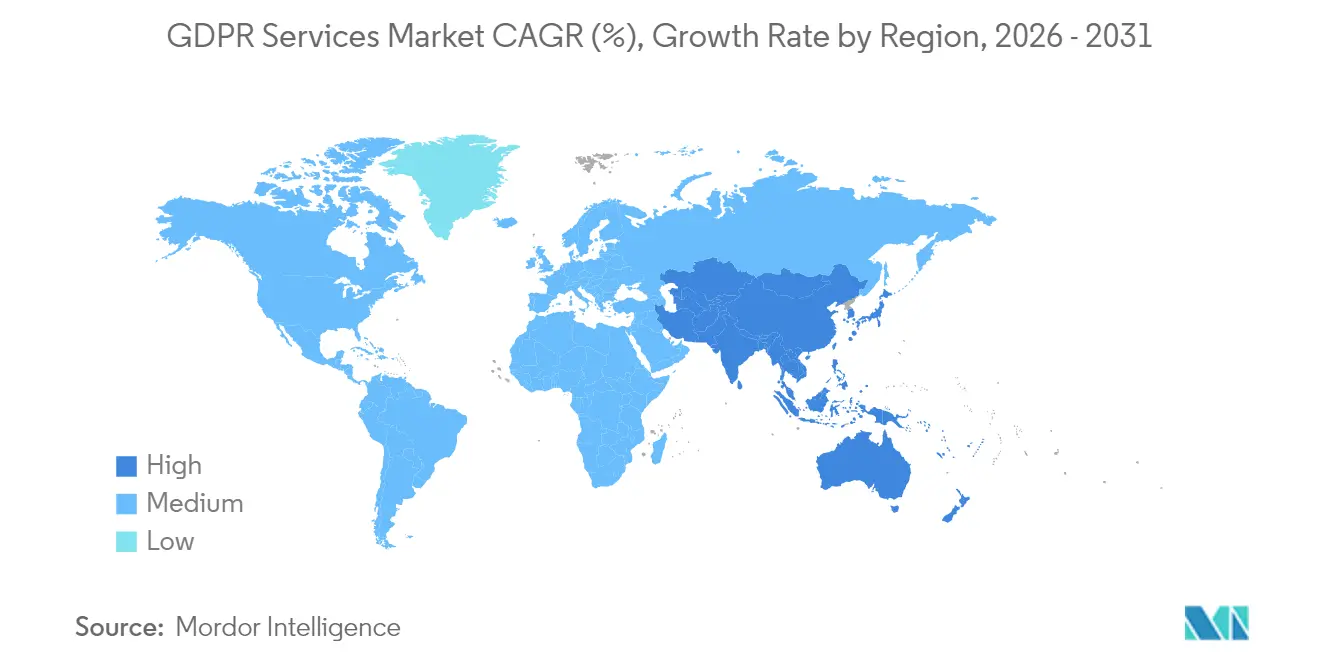

- By geography, Europe led with 38.12% of GDPR services market share in 2025, whereas Asia-Pacific is projected to record a 25.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global GDPR Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating GDPR fine values spur proactive compliance spending | +6.2% | Global; EU core | Medium term (2-4 years) |

| Surge in cross-border data flows post-Brexit and EU-U.S. Data Privacy Framework | +4.8% | North America and EU; spillover to Asia-Pacific | Short term (≤2 years) |

| Rapid cloud-first migrations requiring privacy-by-design architectures | +5.1% | Global; led by North America | Medium term (2-4 years) |

| Heightened frequency of data breaches drives demand for specialized compliance services | +3.7% | Global | Short term (≤2 years) |

| Embedding privacy engineering inside DevSecOps pipelines | +2.9% | North America and EU | Long term (≥4 years) |

| Adoption of AI-powered discovery tools that auto-map personal data | +4.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating GDPR Fine Values Spur Proactive Compliance Spending

European regulators moved from broad awareness campaigns to strategic high-value penalties in 2024, imposing EUR 1.2 billion (USD 1.39 billion) in total fines despite a lower case count. High-profile actions such as LinkedIn’s EUR 310 million (USD 358.31 million) penalty demonstrated a willingness to apply the full 4% revenue ceiling, motivating enterprises to build holistic compliance architectures rather than rely on minimal controls. Financial services, energy, and telecom operators now face the same scrutiny long applied to social-media providers, expanding the addressable market for specialist vendors. Boards increasingly tie executive compensation to privacy metrics, driving larger budgets for data-protection tooling and advisory support. Vendors that can quantify risk reduction and integrate continuous monitoring win favor as organizations abandon checkbox audits for living compliance programs.

Surge in Cross-Border Data Flows Post-Brexit and EU-U.S. Data Privacy Framework

Operationalization of the adequacy decision in 2024 increased data-transfer volumes and complexity; UK firms now juggle UK-GDPR and EU rules concurrently.[1]European Data Protection Board, “Annual Action Plan 2025,” edpb.europa.eu Standard Contractual Clauses remain inconsistently applied, compelling businesses to seek platforms that automate transfer-impact assessments and produce real-time documentation. Service providers that blend legal expertise with technical integration capabilities gain traction as multinationals require unified dashboards for Binding Corporate Rules, certification mechanisms, and continuously updated risk registers.

Rapid Cloud-First Migrations Requiring Privacy-by-Design Architectures

Private-cloud preference rose sharply, with 92% of IT leaders reporting confidence in meeting regulatory obligations on cloud infrastructure. Privacy-by-design now influences architecture from network segmentation to key-management workflows. Hybrid designs dominate because sensitive workloads remain on-premises while analytics functions shift to SaaS, broadening the mix of deployment models within the GDPR services market. Service partners that can orchestrate encryption, access governance, and audit-trail automation across multi-cloud estates are in high demand.

Heightened Frequency of Data Breaches Drives Demand for Specialized Compliance Services

Daily breach notifications averaged 363 across EU member states in 2024, spotlighting operational gaps in 72-hour reporting mandates. Enterprises increasingly purchase incident-response retainers that combine legal counsel with forensic tooling. Vendors embed deletion-at-source and data-subject-rights fulfillment workflows to address the European Data Protection Board’s 2025 focus on the right to erasure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent skills gap in certified Data Protection Officers | -3.4% | Global; acute in Asia-Pacific | Long term (≥4 years) |

| High compliance cost burden on SMEs and micro-firms | -2.8% | Global; emerging markets | Medium term (2-4 years) |

| Fragmented, non-interoperable vendor solutions inflate integration complexity | -2.1% | Global; North America and EU | Medium term (2-4 years) |

| Divergent national enforcement practices causing regulatory uncertainty | -1.9% | Global; cross-border actors | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Persistent Skills Gap in Certified Data Protection Officers

Article 37’s DPO mandate outstrips available talent, prompting regulators to fine even public bodies for non-designation.[2]European Commission, “EU-U.S. Data Privacy Framework Adequacy Decision,” ec.europa.eu Managed DPO-as-a-Service offerings fill the void, blending legal interpretation with technical oversight. Providers holding multi-jurisdictional credentials command premium fees as firms seek turnkey expertise that scales across subsidiaries.

High Compliance Cost Burden on SMEs and Micro-Firms

Typical SME GDPR budgets remain capped near EUR 5,000, far below the investment needed for enterprise-grade governance. Despite exemptions for sub-250-employee entities, obligations around consent, breach notification, and data-subject rights still apply. Cloud-based templated solutions grow popular, yet price sensitivity continues to delay full adoption outside highly regulated verticals. Standardized packages that bundle discovery, assessment, and reporting at predictable monthly rates help vendors penetrate this segment of the GDPR services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Deployment: Private Cloud Gains Compliance Trust

On-premises implementations retained 67.95% revenue in 2025, illustrating continuing appetite for direct data control within the GDPR services market size. Adoption patterns, however, reveal a structural migration path: organizations prioritize private-cloud nodes for regulated workloads while outsourcing less-sensitive analytics to SaaS. The shift is powered by encryption-in-use breakthroughs such as confidential computing, which keep data protected during processing. Data residency rules guide architecture choices; pan-European firms localize storage clusters, then federate queries through secure API gateways. Vendor roadmaps now bundle attested hardware enclaves with policy-driven key escrow, enabling compliance teams to validate technical safeguards without bespoke code reviews.

Cloud-centric offerings record a 26.2% CAGR as boards equate elasticity with resilience. Integration with infrastructure-as-code pipelines means privacy controls are codified alongside network and application states, reducing audit cycles from weeks to hours. Hybrid models allow runtime policy decisions: personal data may execute in a national zone, while aggregated telemetry feeds global dashboards. As customers demand assurances, providers publish cryptographic attestation reports and undergo independent GDPR readiness audits performed by accredited bodies. This transparency is reshaping procurement checklists and reinforcing cloud adoption momentum within the broader GDPR services market.

By Offering: Services Accelerate Through Managed Complexity

Solutions platforms spanning discovery, governance, and consent modules accounted for 58.05% of spending in 2025, yet services revenue is growing faster at 25.7% CAGR as enterprises confront implementation intricacies. Automated data-mapping engines crawl petabyte-scale hybrid estates, normalize metadata, and feed centralized inventories that underpin risk scoring. Consent orchestration nodes propagate granular preferences across websites, mobile apps, and connected devices, replacing legacy banner-only mechanics. Multi-tenant APIs facilitate integration with ticketing, SIEM, and data warehouse tools, making privacy metrics visible in enterprise command centers.

Consulting, managed compliance, and DPO-as-a-Service engagements increasingly generate sticky annuities. Demand for continuous controls testing and regulator-ready dashboards turns point-in-time audits into rolling programs. Providers cultivate sector templates finance, healthcare, retail to expedite onboarding while embedding regulatory nuance. AI-driven playbooks propose remediation tasks, auto-generate DPIAs, and monitor for transfer-impact deviations. These capabilities ensure the GDPR services market stays aligned with regulators’ shift from episodic enforcement to ongoing oversight.

By Organization Size: SMEs Embrace Standardized Solutions

Large enterprises controlled 68.55% of 2025 expenditures, leveraging cross-functional privacy offices, while SMEs logged the fastest uptake at 26.0% CAGR. Early enterprise adopters tailor platforms to complex legal-entity structures, integrating privacy dashboards with GRC suites and enterprise resource-planning engines. They often deploy federated access models that grant regional teams autonomy within corporate guardrails. Vendor professional-services arms embed data-quality checks and classification taxonomies directly into data lakes, ensuring lineage remains intact under AI/ML workloads.

SMEs choose turnkey SaaS packages that activate within hours and price per employee or record count. Pre-configured controls for consent banners, record-of-processing activities, and breach notification templates reduce legal consultation needs. Micro-firms outsource DPO obligations via subscription, gaining instant access to certified professionals versed in EU and local statutes. Automated wizards surface context-aware guidance, allowing non-expert staff to satisfy controller duties without deep legal literacy. These standardized pathways lower adoption barriers, enlarging the customer base and cementing recurring revenue for the GDPR services market. The GDPR services market size for SMEs is projected to expand at the stated CAGR, signaling a durable growth engine for providers.

By End User: Retail Accelerates Digital Commerce Protection

Banking, financial services and insurance retained 34.85% of 2025 revenues, reflecting mission-critical data flows encompassing onboarding, sanctions screening, and fraud analytics. Institutions overlay privacy engines on top of legacy core-banking stacks, automating data-subject rights fulfillment across dozens of downstream processors while maintaining audit trails acceptable to prudential regulators. Inline tokenization and differential-privacy-based analytics allow product teams to mine transactional data while minimizing re-identification risk.

Retail and consumer-goods operators are forecast to grow at 24.9% CAGR as omni-channel commerce ballooned in the wake of pandemic-era digital shift. Customer-journey mapping, loyalty programs, and personalized recommendations necessitate fine-grained consent orchestration. Vendors provide SDKs for mobile apps and point-of-sale systems, synchronizing preferences in real time to avoid undesirable data leakage. Healthcare, telecom, and manufacturing follow closely, each applying industry-specific controls such as pseudonymized research pipelines or employee-monitoring safeguards. This heterogeneity creates niche opportunities for specialists with domain knowledge, broadening the competitive field of the GDPR services market.

Geography Analysis

Europe anchors demand, holding 38.12% revenue in 2025 as regulators pursue coordinated investigations and publish granular guidance that elevates compliance expectations. National authorities increasingly impose structural remedies, compelling controllers to re-engineer processing flows, a factor that sustains platform investments across the GDPR services market. Multinationals with EU headquarters adopt pan-regional privacy operating models, leveraging centralized DPO hubs and harmonized tooling that handles multi-lingual data-subject requests. The European Data Protection Board’s annual action plans set thematic enforcement priorities—AI training data, children’s privacy, and cross-border transfers—ensuring a steady pipeline of remediation projects for service providers.

North America maintains robust growth as state-level regulations such as the California Consumer Privacy Act, Virginia CDPA, and forthcoming federal proposals broaden coverage. U.S. firms operating in both the EU and domestic markets pursue single-framework strategies to reduce duplication, making interoperable platforms critical procurement criteria. Canadian Bill C-27 and updated sectoral codes reinforce the need for unified privacy architecture. Cloud hyperscalers position regional data centers and sovereign cloud variants to satisfy localization demands, while managed-service consultancies bridge statutory interpretation across jurisdictions.

Asia-Pacific records the fastest CAGR at 25.1% as India’s Digital Personal Data Protection Act, China’s Personal Information Protection Law, and amendments in Japan and Singapore mirror EU principles. Local regulators issue sector notices—particularly in fintech, digital health, and smart-city deployments—requiring vendor audits and risk assessments reminiscent of GDPR Article 28. Enterprises deploy region-wide data-mapping programs to cope with divergent breach-notification clocks and consent models. Providers fluent in regional languages and legal cultures grow rapidly, and cross-border data-export assessments become standard service modules. South America and the Middle East follow a similar trajectory, adapting EU elements to domestic contexts, which extends the geographic footprint of the GDPR services market size into new territories.

Regulatory Landscape

The regulatory environment for GDPR services is increasingly shaped by European Data Protection Board (EDPB) coordination and rapidly evolving guidance tied to AI and complex processing practices. In March 2026, the EDPB launched the Coordinated Enforcement Framework (CEF) 2026 on transparency and information duties under GDPR Articles 12 to 14, engaging 25 European data protection authorities, which raises demand for controller-ready privacy notices, layered disclosures, and auditable evidence of how information is delivered across channels.

In 2026, the EDPB also expanded its interpretive framework for emerging use cases, including Guidelines 1/2026 on processing personal data for scientific research (April 2026) and guidelines addressing anonymisation and web scraping in the context of generative AI (July 2026). Alongside these supervisory initiatives, EU-level simplification efforts such as the European Commission Digital Omnibus proposal, discussed in joint institutional settings during 2026, keep attention on how GDPR requirements interact with the broader digital rulebook. That reinforces the use of templates, standardized assessments, and integrated governance tooling in compliance programs.

Value Chain Analysis

The GDPR services value chain begins with governance needs from controllers and joint controllers translating legal duties into operational controls. From there, solution vendors supply discovery and mapping, consent and preference management, DPIA and risk tooling, integration APIs, and monitoring dashboards. Implementation is typically delivered through global consultancies, systems integrators, and specialist privacy firms that configure workflows for data-subject rights, breach notification, records of processing, and transfer-impact assessments, before transitioning clients into managed compliance services and DPO-as-a-Service in response to persistent talent constraints.

Downstream, value is anchored in third-party ecosystems, including cloud providers, SaaS sub-processors, security tooling, and data processors that require continuous governance. EDPB Opinion 22/2024 sharpened expectations that controllers remain fully accountable across processor and sub-processor chains and cannot rely on contractual assurances alone. This elevates due diligence, evidence collection, and continuous verification into core service components, shifting value toward providers that can operationalize vendor risk management, maintain regulator-ready documentation across multi-layer processor networks, and automate transfer and sub-processing controls within hybrid IT environments.

Competitive Landscape

Market concentration is moderate, with platform vendors and global advisors vying for wallet share. OneTrust achieved USD 500 million annual recurring revenue and serves 75% of Fortune 100 enterprises, demonstrating scale advantages in product breadth and global support. Technology-first players emphasize AI-driven discovery, automated DPIA generation, and API-based integrations to embed privacy into agile development practices. Service-heavy incumbents package strategic assessments, remediation roadmaps, and managed operations, leveraging established client relationships to cross-sell privacy offerings.

Osano’s acquisition of WireWheel extended its consent-management and assessment capabilities, while Kyndryl’s partnership with Microsoft folded privacy posture management into traditional infrastructure-outsourcing engagements.[3]Kyndryl, “Data Security Posture Management with Microsoft,” kyndryl.com Sector-specific moves such as Datavant’s purchase of Trace Data target healthcare, marrying de-identification expertise with GDPR compliance requirements. Vendors differentiate through vertical templates, local data-center deployments, and certification coverage across ISO, SOC 2, and CSA STAR.

Barriers to entry remain low at niche scale, enabling regional specialists to flourish; however, enterprise buyers prefer vendors with documented security attestations and proven incident-response capacity. The persistent DPO talent gap favors providers that bundle tools with expert services. Competitive success increasingly depends on the ability to harmonize privacy, security, and data-governance functions under a unified policy engine, a capability only a handful of platforms currently deliver at scale within the GDPR services market.

GDPR Services Industry Leaders

IBM Corporation

Microsoft Corporation

Amazon Web Services Inc.

SAP SE

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace area is productized transparency and information management that scales across web, mobile, and internal systems, supported by the EDPB CEF 2026 enforcement focus on GDPR Articles 12 to 14 across 25 authorities. Vendors and service providers can differentiate by bundling notice generation, consent states, data inventory links, and proof of delivery into auditable workflows that reduce the burden of responding to supervisory requests and coordinated investigations.

Another opportunity is expanding GDPR services into AI and data engineering workflows, where anonymisation and data collection practices face tighter supervisory scrutiny. The EDPB adoption of 2026 guidance on anonymisation and web scraping for generative AI creates demand for updated data discovery, provenance, legal-basis documentation, and re-identification risk testing, particularly for organizations training or procuring AI systems. In parallel, the EDPB 2026-2027 work programme emphasis on ready-to-use templates for legitimate interest assessments, records of processing, and privacy notices supports SaaS-packaged compliance modules for SMEs and distributed enterprises that need standardized, regulator-aligned documentation with less reliance on heavy consulting engagements.

Recent Industry Developments

- July 2026: Kyndryl and Microsoft announced an expansion of sovereignty solutioning that combines Kyndryl advisory services with Microsoft Sovereign Cloud to support architectures aligned with GDPR as well as DORA and NIS2. The move packages compliance design with cloud delivery, helping enterprises operationalize data residency, governance, and control requirements across hybrid estates. It also strengthens Microsoft ecosystem pull-through for privacy, risk, and security programs that were previously handled as separate projects.

- December 2025: IBM was designated by the European Supervisory Authorities as a critical ICT third-party provider under the EU Digital Operational Resilience Act (DORA). Direct EU-level oversight increases scrutiny on operational resilience, governance, and third-party controls for regulated customers, reinforcing demand for integrated privacy, security, and risk management services. The designation also raises the importance of auditable compliance capabilities within large-provider platforms used by financial institutions.

- October 2024: The European Data Protection Board published Opinion 22/2024 clarifying that controllers retain full accountability across processing chains, including sub-processors, and that contractual assurances alone are insufficient. This tightened expectations for documented due diligence, continuous monitoring, and proof of safeguards across vendor ecosystems. Service providers and platforms that automate processor governance, transfer-impact documentation, and sub-processor oversight gain a clearer path to recurring managed compliance engagements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers paid services that help organizations comply with the EU General Data Protection Regulation, including advisory, readiness work, program implementation support, and ongoing managed compliance services tied to GDPR obligations.

Scope exclusions: It excludes cybersecurity hardware, generic backup or disaster recovery contracts, and privacy projects that only address non-EU privacy laws.

Segmentation Overview

- By Type of Deployment

- On-Premises

- Cloud

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Offering

- Solutions

- Data Discovery and Mapping

- Data Governance

- Consent / Preference Management

- API and Integration Management

- Risk-Assessment and DPIA Tools

- Services

- Consulting and Advisory

- Integration and Implementation

- DPO-as-a-Service

- Managed Compliance Services

- Solutions

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End User

- Banking, Financial Services and Insurance (BFSI)

- Telecom and IT

- Retail and Consumer Goods

- Healthcare and Life Sciences

- Manufacturing

- Government and Public Sector

- Other End User

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build a clean starting point on regulatory timelines, enforcement patterns, and enterprise spending signals that relate to privacy compliance. We referred to public sources such as the European Data Protection Board guidance, national data protection authority enforcement statistics, Eurostat digital economy datasets, OECD indicators on the digital economy, and peer reviewed privacy and compliance journals.

Along with these, we reviewed company filings and annual reports, investor presentations, reputable press coverage, and professional association publications that track privacy and risk practices. Where needed, a paid subscription for company financials and intelligence and a patent database were used to sanity-check vendor positioning and feature direction without relying on paywalled narrative reports. The desk sources listed here are illustrative only, and many other public references were used to collect, cross-check, and clarify the data.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with service providers, consulting practices, managed compliance specialists, and buyer-side roles such as privacy, legal, risk, and IT security teams. We used these conversations to confirm what gets bought as a GDPR service, how pricing is typically packaged (project work versus ongoing retainers), and which regions and industries are driving incremental demand.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 22% | APAC: 46% |

| Mid tier: 48% | Functional/Unit leaders: 27% | EMEA: 35% |

| Smaller Players: 22% | Managers: 51% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where compliance services demand is reconstructed from the addressable pool of organizations handling EU personal data, and then filtered through typical service adoption rates by region and industry. The totals are then checked with selective bottom-up approximations, like sampled provider revenue splits, channel conversations, and a simple volume times average price logic for common deliverables (assessments, remediation programs, and managed DPO support), and the model is adjusted when the two views drift too far.

Key inputs that shaped the model included enforcement intensity signals and fine activity, the pace of new GDPR related guidance, enterprise headcount and digitalization indicators, the share of cross-border data processing, and the mix of one-time projects versus recurring managed compliance. Because spend can move quickly after major incidents or regulatory actions, scenario analysis was used for the forecast, and assumptions were aligned to expert consensus on budget cycles, outsourcing trends, and the maturity of privacy programs. When provider-level disclosures were limited, gaps were handled by using peer benchmarks for service mix and typical contract values, followed by re-validation in follow-up calls.

Data Validation & Update Cycle

Validation is done through multiple passes that compare the model output against independent signals, such as enforcement trends, enterprise compliance budget direction, and the observed shift from assessment-only work to ongoing managed services. Outliers are reviewed, and assumptions are revisited when the implied spend per organization or regional split looks inconsistent with what interviewees see in active deals.

Before sign-off, the full workbook is reviewed by another analyst who checks math logic, unit consistency, and year-over-year movements, and then raises questions that must be answered with sources or call notes. The report is refreshed annually, and interim updates are triggered when material events occur, such as major regulatory guidance updates or sharp changes in enforcement activity. Right before delivery, a fresh review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Gdpr Services Market Sizing Compared With Other Published Estimates

Published numbers for GDPR services can look far apart because teams count different line items, use different base years, and apply different assumptions on recurring managed compliance versus short consulting projects. Geography treatment also matters, since some models allocate revenues by where suppliers sit while others allocate by where the regulated data subjects and buyers are.

Generic data-backup contracts sit outside Mordor Intelligence's scope, and that tends to compress the total versus estimates that blend GDPR readiness with broader data protection spend. Differences also show up when a study books GDPR software revenues as services, uses aggressive price escalation for retainers, or does not re-check adoption rates after enforcement and guidance changes, which can move demand faster than a long forecast cadence captures.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.34 B (2025) | |

| Global Consultancy A | USD 4.41 B (2025) | Uses a revenue definition that can include GDPR software and adjacent governance tooling, which can inflate the services-only spend versus a tighter fee-for-service view. |

| Industry Publisher B | USD 3.26 B (2025) | Provides limited clarity on inclusions and exclusions, so overlaps between advisory work, implementation support, and ongoing managed compliance can be treated inconsistently across regions. |

The spread in the table is mostly explained by what gets counted as a GDPR service versus broader privacy and data governance spend, and by how recurring managed work is projected. By tying the model to observable enforcement signals, adoption rates, and service packaging realities, we keep the market total traceable to inputs that can be rechecked each year.

Key Questions Answered in the Report

What is the current size of the GDPR services market?

The market was valued at USD 4.16 billion in 2026 and is projected to grow to USD 12.41 billion by 2031.

Which region leads spending on GDPR compliance services?

Europe held 38.12% of global revenue in 2025 owing to mature enforcement and detailed regulatory guidance.

How fast are cloud-based GDPR solutions growing?

Cloud deployments are expanding at a 26.2% CAGR as organizations adopt privacy-by-design architectures aligned with hybrid-cloud strategies.

Why are SMEs important to future market growth?

SMEs represent the fastest-growing customer cohort with a 26.0% CAGR because standardized SaaS packages now deliver enterprise-grade compliance at affordable price points.

What role do Data Protection Officers play in market dynamics?

A global shortage of certified DPOs drives demand for outsourced DPO-as-a-Service models, boosting recurring revenue for managed-service providers.

Which industry vertical is forecast to grow fastest?

Retail and consumer goods are projected to rise at 24.9% CAGR as digital commerce expands the volume of personal data requiring protection.

Page last updated on: