Transaction Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

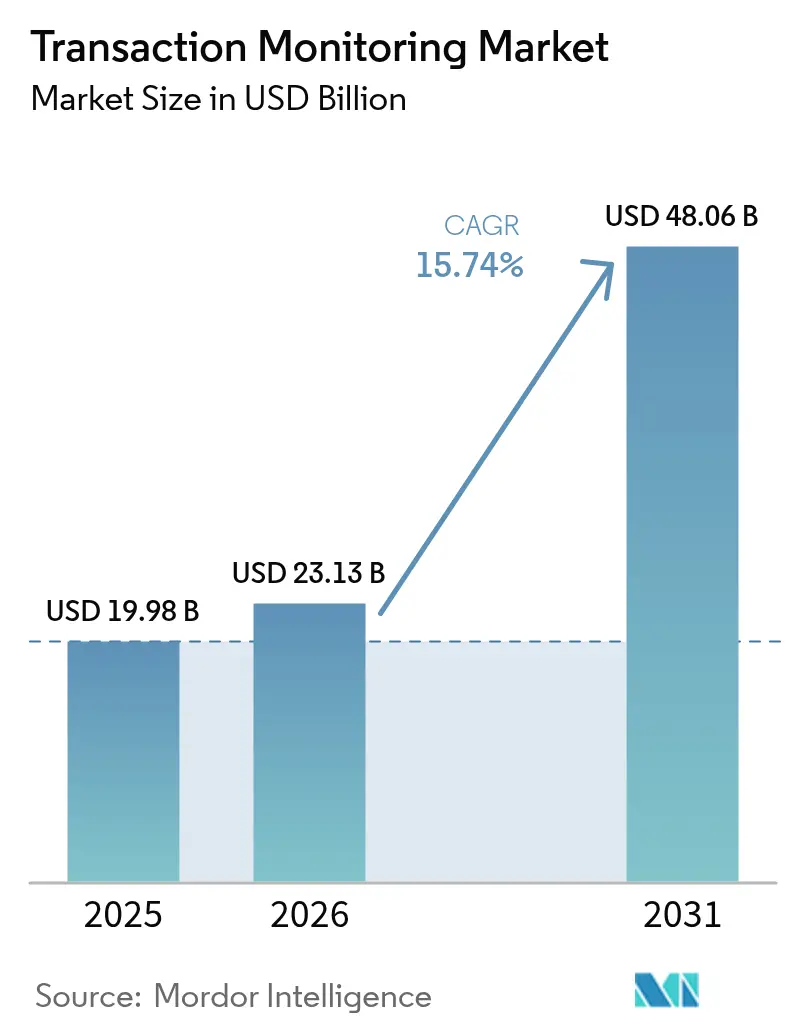

| Market Size (2026) | USD 23.13 Billion |

| Market Size (2031) | USD 48.06 Billion |

| Growth Rate (2026 - 2031) | 15.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Transaction Monitoring Market Analysis by Mordor Intelligence

The transaction monitoring market size was valued at USD 19.98 billion in 2025 and estimated to grow from USD 23.13 billion in 2026 to reach USD 48.06 billion by 2031, at a CAGR of 15.74% during the forecast period (2026-2031). Growth stems from rising regulatory expectations, fast-expanding digital payments, and the rapid infusion of AI into compliance workflows. Vendors are sharpening competitive positioning through entity-centric analytics that shrink false positives, while financial institutions pursue cloud migration to modernize surveillance at scale. The transaction monitoring market is also expanding beyond banking as retail, e-commerce, and fintech platforms embed real-time controls to protect high-velocity payment streams. Heightened focus on integrated “FRAML” solutions is pushing providers to unify AML, fraud, and sanctions monitoring in a single stack, creating richer data contexts for risk scoring. Meanwhile, CBDC pilots and open-banking APIs are opening fresh revenue pools for platforms that can address cross-bank and cross-asset visibility requirements.

Key Report Takeaways

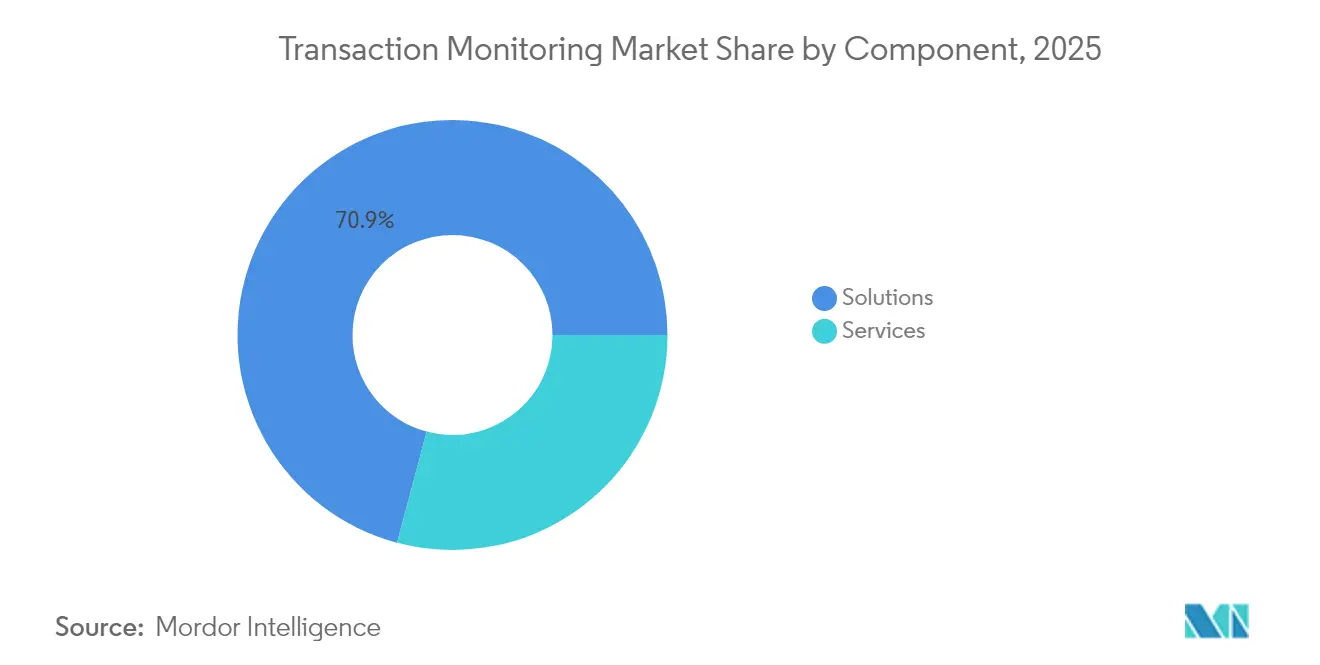

- By component, solutions held 70.85% of the transaction monitoring market share in 2025, while services are projected to grow the fastest at an 18.12% CAGR through 2031.

- By deployment mode, cloud accounted for 63.25% of the transaction monitoring market size in 2025 and is forecast to expand at a 19.28% CAGR between 2026-2031.

- By application, AML captured 41.65% revenue in 2025; fraud detection & prevention is advancing at the highest 20.74% CAGR to 2031.

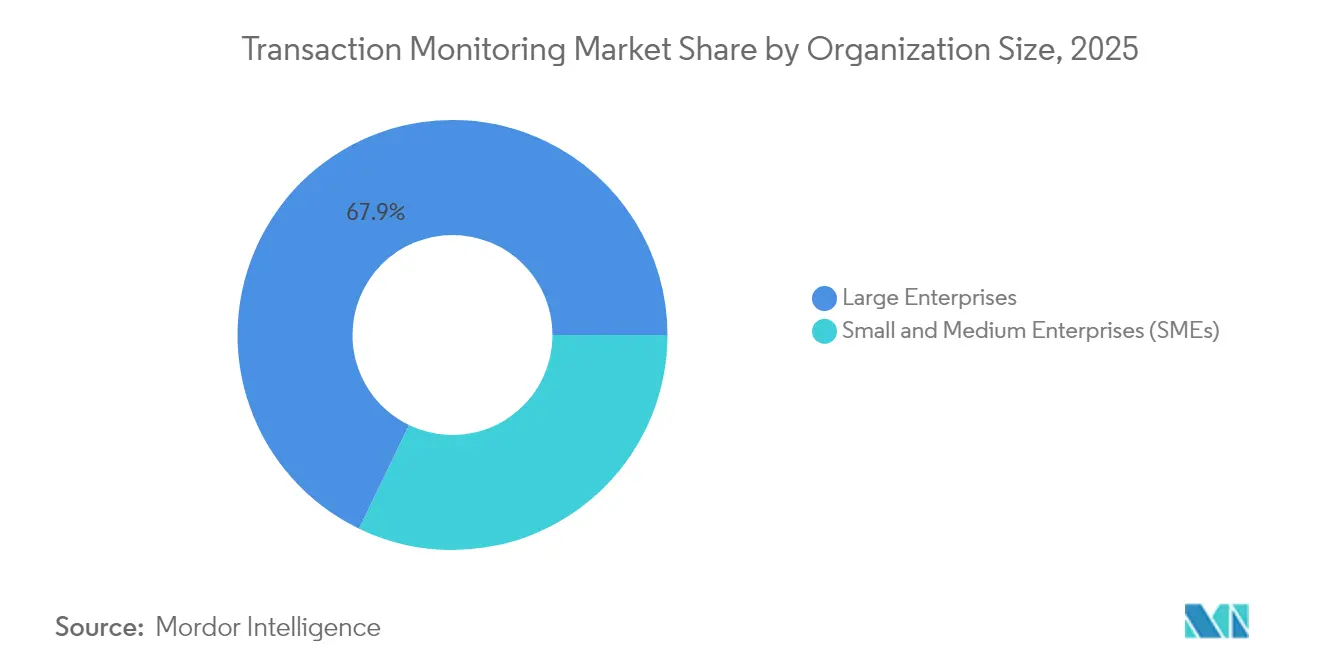

- By organization size, large enterprises held 67.85% share of the transaction monitoring market size in 2025, whereas SMEs post a 20.02% CAGR to 2031.

- By industry vertical, BFSI led with 55.75% share in 2025; retail & e-commerce is projected to post the quickest 21.78% CAGR through 2031.

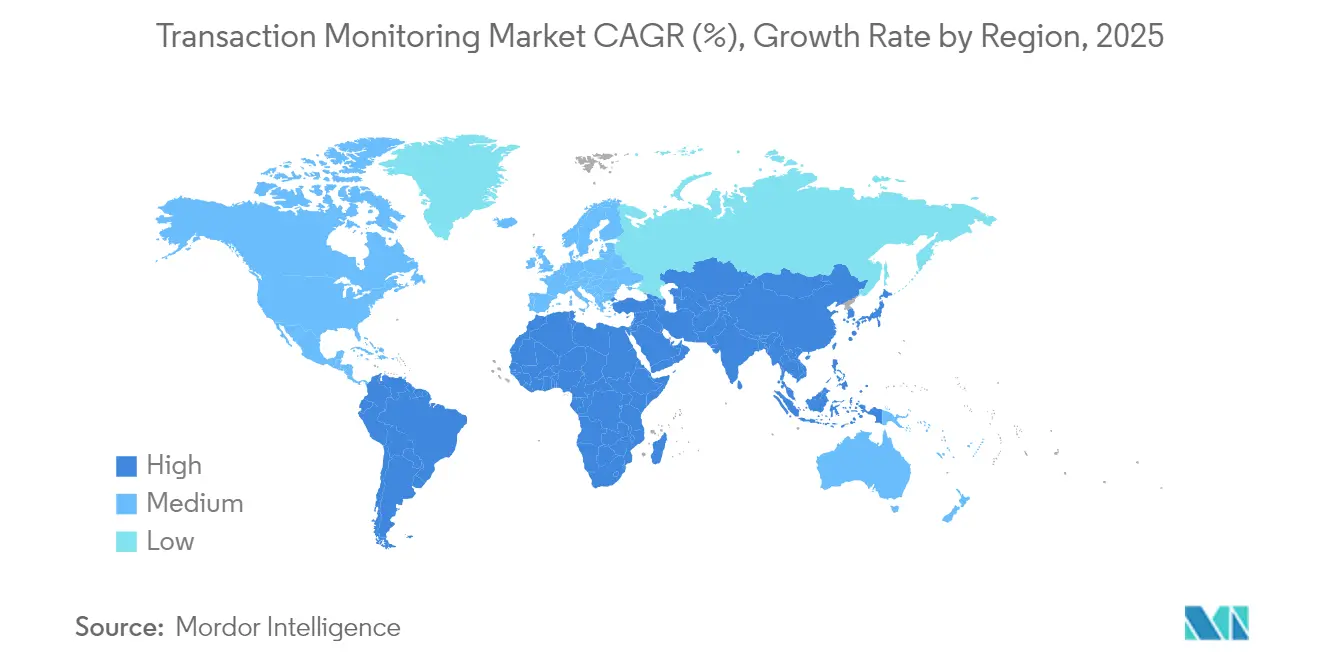

- By geography, North America commanded 32.65% of the transaction monitoring market share in 2025; Asia-Pacific records the strongest 17.14% CAGR to 2031 napier.ai.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transaction Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent AML & KYC regulations | +4.0% | Global – North America, Europe lead | Medium term (2-4 years) |

| Rising volumes of digital & real-time payments | +3.2% | Global – APAC highest | Short term (≤2 years) |

| Integration of AI & ML to cut false positives | +2.4% | Global – early North America uptake | Medium term (2-4 years) |

| Shift toward cloud-based compliance platforms | +1.9% | Advanced economies worldwide | Short term (≤2 years) |

| Open-banking APIs enabling cross-bank monitoring | +1.6% | Europe, North America, APAC | Medium term (2-4 years) |

| CBDC pilots triggering new surveillance mandates | +1.3% | China, EU, then global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent AML & KYC regulations

Global AML penalties climbed 31% year on year to USD 263 million in 2024, prompting banks to retire legacy rule sets in favor of adaptive, AI-enabled engines that address the EU 6AMLD and the US Corporate Transparency Act. Institutions deploying advanced models report 40% fewer false positives and materially stronger examiner confidence, speeding case workflows and reducing compliance backlogs.

Digital payments expansion necessitates real-time monitoring

Real-time payment rails demand sub-second scoring, and firms that upgrade monitoring pipelines see a 49% lift in fraud-prevention effectiveness. Retail and e-commerce adopters leverage the same controls to stem loyalty fraud and card-testing attacks, cutting fraud losses by up to 60% while preserving customer experience.[1]Tookitaki, "Advanced Fraud Protection Solutions: Trends and Innovations", tookitaki.com

AI and machine learning transform detection accuracy

Self-learning models discover complex laundering syndicates by linking transactional, behavioral, and adverse-media data, driving a 2-4× increase in risk detection and slashing false positives by more than 60%.[2]Google Cloud, "Anti Money Laundering AI" , cloud.google.com Natural-language processing now mines unstructured data to flag entities sooner than transaction-only approaches, yielding early-warning benefits.

CBDC pilots trigger new surveillance mandates

More than 130 jurisdictions are testing CBDCs, each adding telemetry that must be folded into AML. [3]Bank for International Settlements, "CBDC Information Security and Operational Risks to Central Banks", bis.orgProviders that master privacy-preserving analytics for sovereign digital currencies unlock a long-run growth vector as pilots mature into production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High false-positive alert fatigue | -2.4% | Global | Short term (≤2 years) |

| Shortage of skilled AML data analysts | -1.9% | Emerging markets most acute | Medium term (2-4 years) |

| Data-sovereignty & privacy-law friction | -1.6% | EU, China, Russia | Medium term (2-4 years) |

| Surge in synthetic-ID fraud bypassing rules | -1.3% | North America first | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High false-positive alert fatigue

Rule-centric systems still generate above-90% noise ratios, forcing banks to hire large analyst teams and risking missed threats amid alert overload. TD Bank’s USD 3 billion penalty underscored the cost of poor triage. AI-powered case managers are cutting false positives by 40%, freeing investigators for high-value reviews.[4]Lucinity, "Combining Scenario-Based and AI-Based Monitoring", lucinity.com

Synthetic identity fraud evades traditional controls

Synthetic-ID schemes produced USD 23 billion in losses during 2024 as criminals blend fabricated and legitimate attributes to mimic normal customers jackhenry.com. Deepfake accelerators widened the threat by 244% year on year. [5]Entrust, "2025 Identity Fraud Report", entrust.com Financial institutions counter with layered biometrics and behavioral analytics to expose anomalous identity footprints, curbing loss velocity and protecting customer onboarding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Strengthen Detection Outcomes

Solutions held 70.85% share in 2025, growing reliance on external expertise signals a shift toward continuous-improvement outsourcing. Specialized providers build recurring revenue around post-implementation optimization, ensuring the transaction monitoring market maintains resilient demand through economic cycles as compliance requirements tighten.

However, Services revenue within the transaction monitoring market is expected to rise at an 18.12% CAGR from 2026-2031 as institutions recognize that technology alone cannot sustain effective compliance. Engagements covering AI-model validation, scenario tuning, and data-quality remediation now accompany most platform deployments, especially for cross-border banks contending with divergent regulator expectations. These advisory and managed-service layers boost precision, delivering up to 30% better threat capture rates.

By Deployment Mode: Cloud Scales Compliance Economically

Cloud platforms accounted for 63.25% of the transaction monitoring market size in 2025 and are projected to grow at 19.28% CAGR through 2031, propelled by elastic throughput and automatic rule updates. Real-time screening across hundreds of millions of transactions has become economically viable for midsize banks and fintechs that previously lacked enterprise-grade infrastructure.

Regulated entities in data-sensitive jurisdictions still blend on-premise cores with cloud analytics, but privacy-enhancing computation is narrowing resistance. As cost-to-serve falls, cloud adoption unlocks adjacent analytics such as customer screening and sanctions testing, reinforcing vendor cross-sell momentum in the transaction monitoring market.

By Application: Fraud Detection Moves Center Stage

AML retained 41.65% share in 2025, yet fraud detection & prevention is forecast to outpace at a 20.74% CAGR as instant payment rails expose banks to speed-of-loss risk. Unified FRAML suites bridge historic silos, letting teams correlate transaction anomalies with identity and behavioral red flags in a single casework interface.

Tighter integration shortens investigation cycles and improves recovery odds, positioning fraud-centric feature roadmaps as a prime differentiator. The transaction monitoring market rewards vendors that deliver explainable AI models capable of both regulatory auditability and real-time interdiction.

By Organization Size: SMEs Join the Compliance Mainstream

Large institutions still contribute 67.85% of 2025 revenue, but SME uptake is accelerating at 20.02% CAGR to 2031 as regulators extend AML obligations to neobanks, PSPs, and credit unions. Cloud-native subscription pricing aligns cost with transaction volumes, allowing smaller firms to adopt enterprise-grade tools without capital outlay.

This democratization expands the overall transaction monitoring market addressable base and fuels a two-tier vendor landscape: incumbents serve complex multinational banks, while challenger platforms tailor simplified rule libraries for SMEs entering regulated payments corridors.

By Industry Vertical: Retail & E-Commerce Outpaces BFSI

BFSI generated 55.75% of transaction monitoring market revenue in 2025; however, the retail & e-commerce segment is projected to advance at 21.78% CAGR as online merchants counter rising card-not-present fraud. High-growth merchant acquirers embed monitoring modules directly within checkout stacks, enabling millisecond-level decisioning that safeguards conversion rates.

Non-financial sectors such as healthcare, telecom, and utilities likewise expand platform usage to guard billing flows and loyalty programs, confirming the broadening relevance of the transaction monitoring market beyond traditional banking confines.

Geography Analysis

North America led the transaction monitoring market with a 32.65% share in 2025, supported by FinCEN enforcement activity and sustained technology spending by tier-1 banks. U.S. institutions racing to lower false positives are piloting explainable AI that meets examiner transparency criteria, while Canada’s FinTRAC pushes mid-tier lenders to adopt real-time analytics.

Asia-Pacific is projected to post the highest 17.14% CAGR through 2031 as China, India, and Indonesia digitize payment ecosystems at scale. China’s central-bank mandates drive domestic vendors to embed continuous monitoring into super-app payment infrastructure, whereas India’s UPI ecosystem requires round-the-clock screening to manage micro-transaction volumes. Developed markets such as Japan, South Korea, and Australia focus on AI-based anomaly detection to offset skilled-analyst shortages.

Europe maintains robust growth as 6AMLD harmonizes AML regimes and MiCA extends surveillance to crypto-asset service providers. Germany and France emphasize privacy-preserving analytics to align with GDPR, while the United Kingdom’s FCA levies stiff penalties for tuning lapses, accelerating modern-platform adoption. Pan-European open-banking initiatives simultaneously widen data inputs and complexity, reinforcing demand for API-centric solutions across the transaction monitoring market.

Competitive Landscape

The transaction monitoring market remains moderately fragmented, featuring legacy enterprise suites from NICE Actimize, Oracle, FICO, SAS, and IBM beside agile RegTech innovators such as Silent Eight, Lucinity, Napier AI, Tookitaki, and Unit21. Competition pivots on model explainability, dynamic scenario updates, and cloud deployment agility.

Strategic M&A is reshaping the field: Fenergo purchased Sentinels to fuse client-lifecycle management with monitoring, while TRM Labs extended coverage to blockchain assets to pre-empt crypto-AML regulation. Large vendors release next-generation engines—NICE Actimize SAM-10 and Google Cloud’s AML AI—showcasing multilayered analytics that map entity networks and automate low-risk case closures.

AI precision is the central battleground. Silent Eight secured regulator sign-off for automated alert closure, highlighting rising trust in black-box models once sufficient validation evidence is provided. Vendors that couple high recall with transparent decision paths are positioned to capture bank budgets as supervisory scrutiny intensifies across the transaction monitoring market.

Transaction Monitoring Industry Leaders

-

Oracle Corporation

-

SAS Institute Inc.

-

Fair Isaac Corporation (FICO)

-

Protiviti Inc.

-

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Fenergo expanded its transaction monitoring capabilities through the launch of a comprehensive SaaS solution designed to detect suspicious transaction activities in real-time while reducing false positives and ensuring compliance with AML regulations.

- March 2025: Silent Eight achieved regulatory approval for auto-closing alerts, demonstrating unprecedented trust in their AI-driven processes for transaction monitoring. Their AI models reached a 98.7% precision rate, crucial for high-risk markets, while delivering a 20-40% reduction in operational costs for clients Silent Eight.

- February 2025: NICE Actimize released SAM-10, an advanced transaction monitoring solution featuring a multilayered approach to address persistent issues like slow tuning cycles and false positives. The system emphasizes an entity-centric strategy to enhance detection of suspicious activities across various business sectors

- January 2025: Google Cloud launched its Anti-Money Laundering AI tool, enhancing transaction monitoring by detecting suspicious activities more accurately and efficiently.

- November 2024: Lucinity introduced a hybrid transaction monitoring approach combining scenario-based and AI-driven monitoring to address the inefficiencies of traditional systems.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the transaction monitoring market as the total annual spending by financial-services providers and other regulated entities on software platforms and related services that screen, score, and analyze payment, deposit, withdrawal, and trade events in real time or near-real time to identify suspicious activity for anti-money-laundering, fraud, and broader compliance purposes.

Scope exclusion: pure-play log-management, standalone KYC utilities, and generic data-visualization tools are excluded from our sizing.

Segmentation Overview

-

By Component

- Solutions

- Services

-

By Deployment Mode

- Cloud

- On-Premises

-

By Application

- Anti-Money Laundering (AML)

- Fraud Detection and Prevention

- Customer Identity Management

- Compliance Management

- Other Niche Use-Cases

-

By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

-

By Industry Vertical

- Banking, Financial Services and Insurance (BFSI)

- Government and Defence

- IT and Telecom

- Retail and E-commerce

- Healthcare

- Energy and Utilities

- Manufacturing

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

APAC

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of APAC

-

Middle East and Africa

-

Middle East

- GCC

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Rest of Africa

-

Middle East

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed compliance officers, reg-tech product managers, and regional AML consultants across North America, Europe, and Asia-Pacific. Conversations tested average alert loads, cloud-migration timelines, and contracted annual recurring revenue, enabling us to refine unit counts and discount rates used in our model.

Desk Research

We reviewed publicly available regulations and guidance from bodies such as the Financial Action Task Force, the European Banking Authority, the U.S. FinCEN, and the Monetary Authority of Singapore, since these documents set the minimum monitoring capabilities institutions must procure. Trade association whitepapers from ACAMS, UK Finance, and the Bankers Association of the Philippines helped quantify adoption benchmarks. Company 10-Ks, investor decks, and selected tender databases (D&B Hoovers, Dow Jones Factiva) supplied price corridors and contract volumes. Academic journals on anomaly-detection models clarified typical false-positive ratios that drive upgrade cycles. The sources cited here are illustrative; many additional references fed into data collection and validation.

Market-Sizing & Forecasting

A top-down framework starts with global banking IT outlays and narrows to the compliance software pool before applying transaction-volume, penalty-incidence, and cloud-migration penetration factors. Supplier roll-ups and sample average selling price times deployment counts act as the bottom-up cross-check, after which totals are adjusted. Key variables include (1) digital-payment transactions per capita, (2) share of instant-payment rails, (3) average regulatory fine per breach, (4) cloud adoption in regulated workloads, and (5) median false-positive ratio. A multivariate regression links these drivers to historical spend, and forecast coefficients are stress-tested with scenario inputs gathered from our expert panel. Data gaps in smaller geographies are bridged by applying regionally proxied spend-per-transaction ratios.

Data Validation & Update Cycle

Outputs pass a three-layer review covering variance against historic spend trends, peer comparisons, and currency normalization. Anomalies trigger re-contact with sources. We refresh each model annually; interim updates occur when regulatory thresholds, major fines, or technology cost inflections materially alter our baseline.

Why Mordor's Transaction Monitoring Baseline Commands Reliability

Published values frequently diverge because firms choose different activity pools, deployment mixes, and refresh timings.

Key gap drivers are scope breadth (some firms fold in log-management suites), treatment of service revenue, and currency conversion at varied exchange dates, while Mordor reports cloud and on-premise spend only, uses constant 2024 USD, and refreshes every twelve months.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.98 B | Mordor Intelligence | - |

| USD 17.14 B (2024) | Global Consultancy A | Includes payment-gateway analytics; uses 2023 FX; model last updated 18 months ago |

| USD 22.76 B (2025) | Industry Association B | Treats AML case-management and trade-finance screening as part of the same pool |

| USD 17.98 B (2024) | Regional Consultancy C | Excludes professional-services revenue and assumes flat cloud-pricing through 2032 |

These comparisons show that by anchoring scope strictly to monitoring platforms and aligning drivers with real-world spend levers, Mordor provides a balanced, transparent baseline decision-makers can track and replicate.

Key Questions Answered in the Report

What is driving double-digit growth in the transaction monitoring market?

Intensifying AML regulation, rapid digital-payment adoption, and AI-driven improvements that lower false positives are the primary growth levers, propelling a 15.74% CAGR through 2031.

How large will the transaction monitoring market be by 2031?

The market is forecast to reach USD 48.06 billion by 2031, up from USD 19.98 billion in 2025.

Which deployment mode is preferred by financial institutions?

Cloud deployment leads with 63.25% 2025 share and is projected to grow at 19.28% CAGR as firms seek scalable, lower-cost compliance.

Why is retail & e-commerce the fastest-growing vertical?

Surging online payments and sophisticated card-not-present fraud push merchants to implement real-time monitoring, supporting a 21.78% CAGR.

How are vendors reducing false-positive alert fatigue?

Vendors integrate machine-learning models and entity-centric analytics that cut false positives by about 40% and automate low-risk alert closure.

What regions are expanding fastest?

Asia-Pacific leads with a 17.14% CAGR thanks to real-time payment expansion, rising regulatory maturity, and large unbanked populations entering digital finance.

Page last updated on: