Respiratory And Anesthesia Disposables Market Size and Share

Market Overview

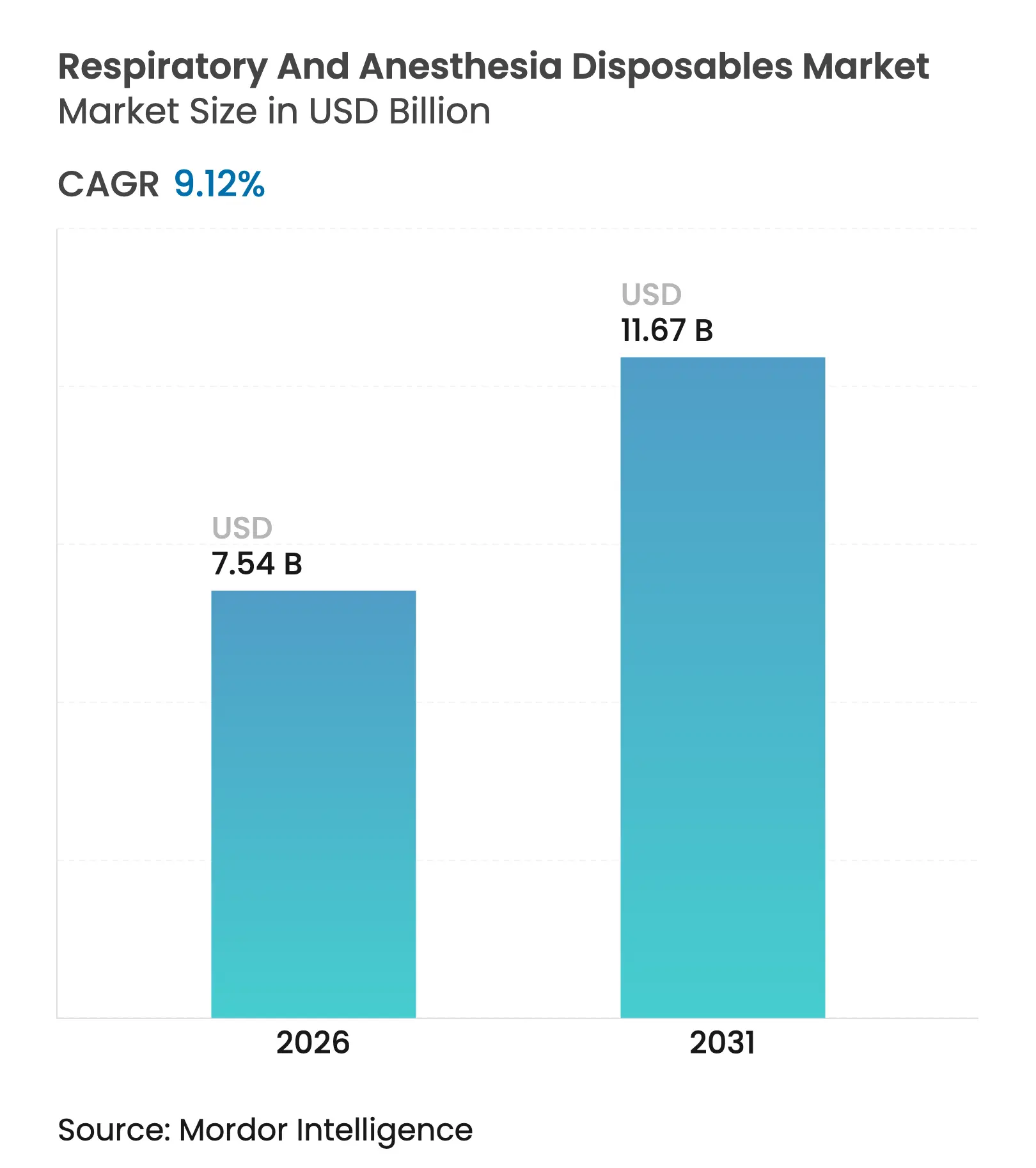

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.54 Billion |

| Market Size (2031) | USD 11.67 Billion |

| Growth Rate (2026 - 2031) | 9.12 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Respiratory And Anesthesia Disposables Market Analysis by Mordor Intelligence

The respiratory and anesthesia disposables market size in 2026 is estimated at USD 7.54 billion, growing from 2025 value of USD 6.91 billion with 2031 projections showing USD 11.67 billion, growing at 9.12% CAGR over 2026-2031. This outlook reflects persistent chronic respiratory disease prevalence, a structural drive toward infection-control protocols, and a fast-rising preference for home-based care. Device innovation is sharpening competitive differentiation, particularly where single-use airway products integrate sensors for real-time monitoring. Hospitals still dominate procurement; however, ambulatory and home-care channels are expanding quickly as payers reward cost-effective care models. Regionally, the respiratory and anesthesia disposables market exhibits a mature but innovation-rich profile in North America, contrasted by high-volume, price-sensitive demand across Asia-Pacific.

Key Report Takeaways

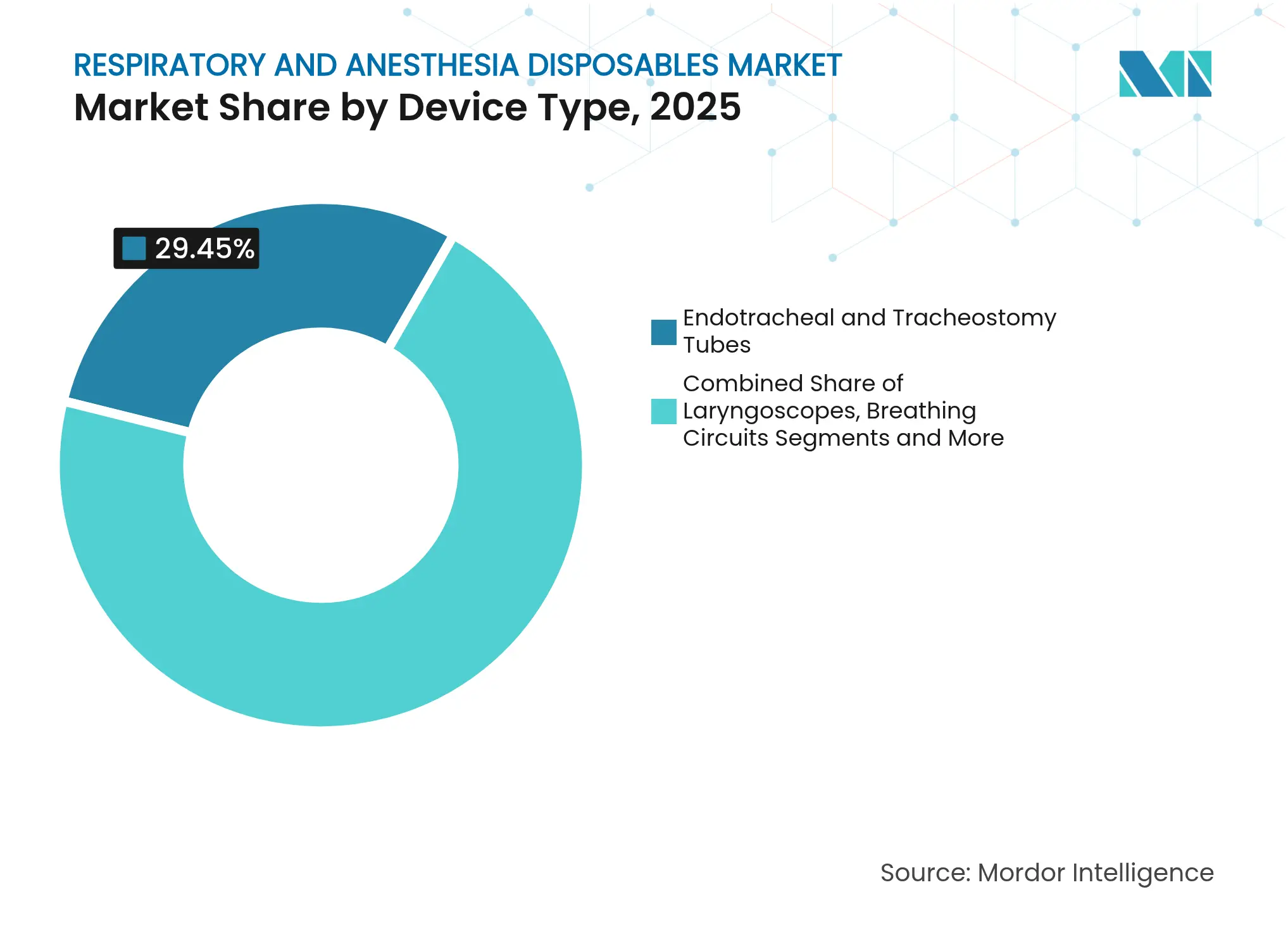

- By device type, endotracheal and tracheostomy tubes led with 29.45% of respiratory and anesthesia disposables market share in 2025. Breathing circuits are projected to grow at an 11.12% CAGR through 2031, the fastest among all product categories.

- By application, COPD accounted for 32.78% of the respiratory and anesthesia disposables market size in 2025. Sleep apnea is set to post the highest 12.05% CAGR between 2026 and 2031.

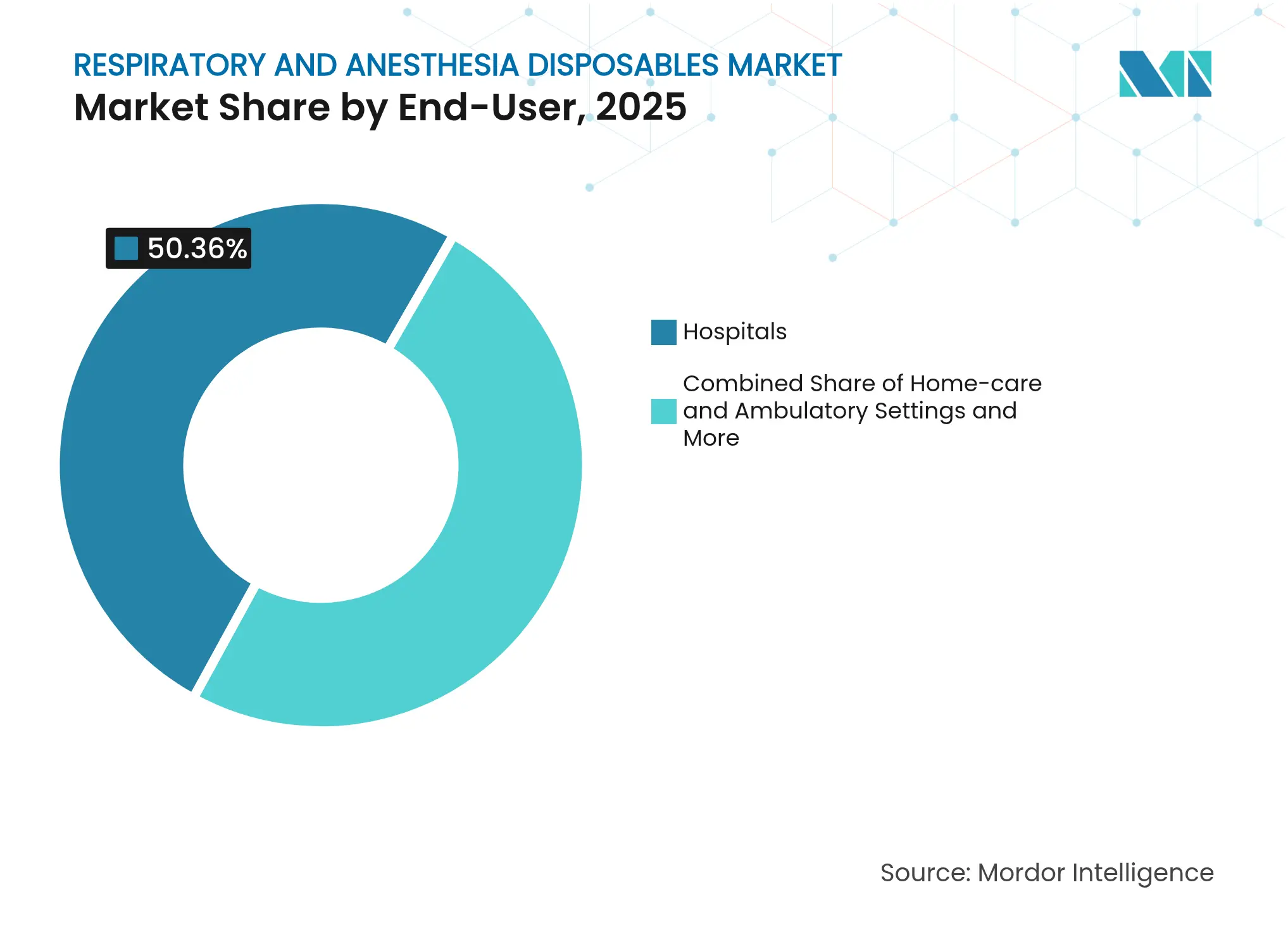

- By end-user, hospitals commanded 50.36% of 2025 revenue, while home-care and ambulatory settings are expanding at a 10.14% CAGR through 2031.

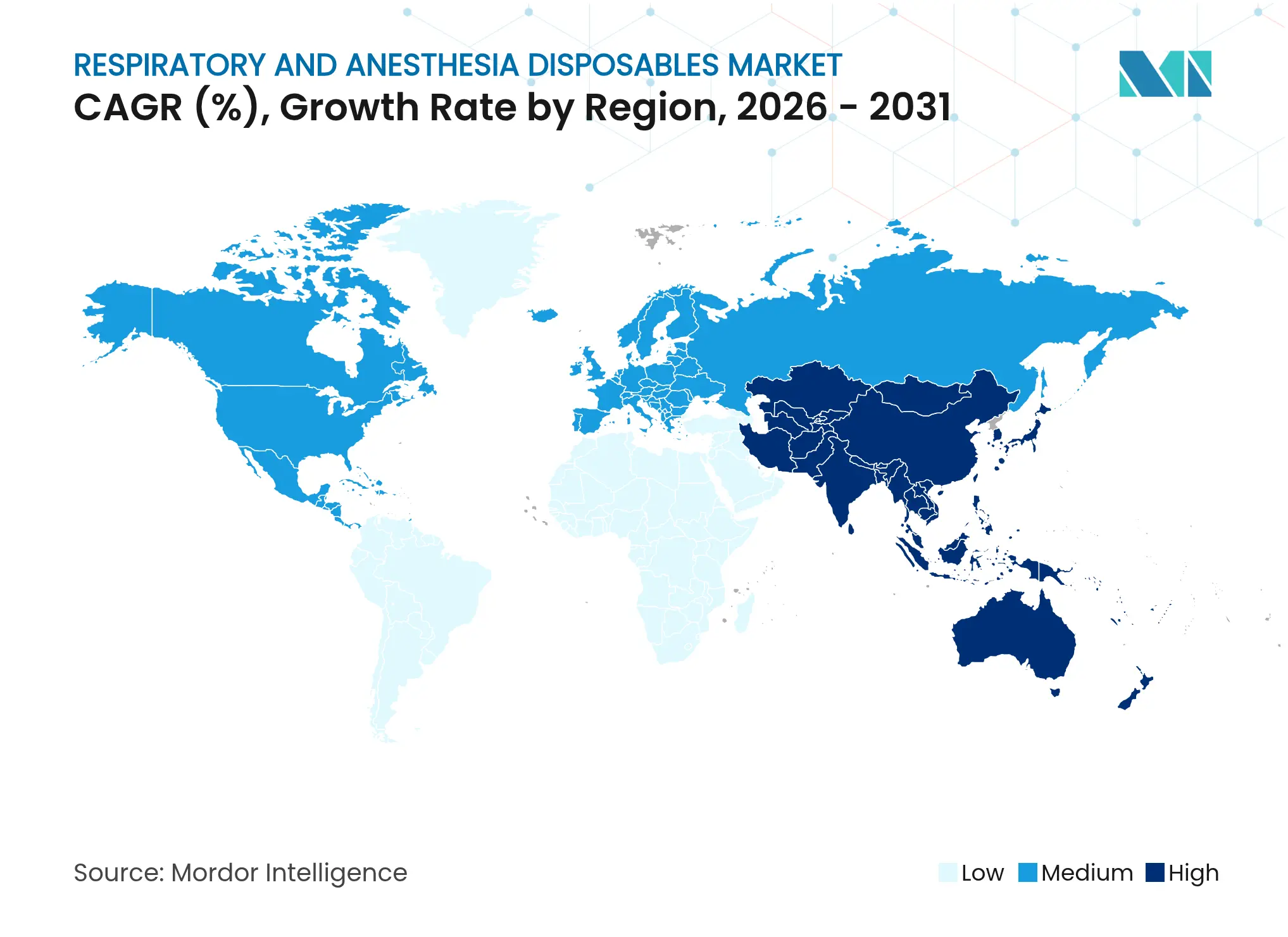

- By geography, North America held 40.15% of global revenue in 2025, whereas Asia-Pacific is forecast to register a 10.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Respiratory And Anesthesia Disposables Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of respiratory disorders

Rising prevalence of respiratory disorders

| +2.1% | Global; concentration in Asia-Pacific and aging Western markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+2.1%

| Geographic Relevance:

Global; concentration in Asia-Pacific and aging Western

markets

| Impact Timeline:

Long term (≥ 4 years)

|

Growing volume of surgical procedures

Growing volume of surgical procedures

| +1.8% | North America and EU core; spillover to Asia-Pacific | Medium term (2-4 years) | |||

High prevalence of tobacco smoking

High prevalence of tobacco smoking

| +1.4% | Asia-Pacific core; secondary impact in Eastern Europe and MEA | Long term (≥ 4 years) | |||

Infection-control push for single-use airway products

Infection-control push for single-use airway products

| +2.3% | Global; accelerated in hospital-dense regions | Short term (≤ 2 years) | |||

AI-enabled disposable sensors for ventilation monitoring

AI-enabled disposable sensors for ventilation monitoring

| +1.2% | North America and EU early adoption; Asia-Pacific following | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence Of Respiratory Disorders

Chronic obstructive pulmonary disease affects 213 million people and causes 3.71 million deaths annually, anchoring long-run demand for consumable airway devices. Urbanization, aging, and industrial pollution in emerging economies add incremental patient pools that need both hospital-grade and home-care consumables. Health systems are shifting resources toward early intervention and continuous monitoring, prompting interest in disposables embedded with diagnostic sensors. Because respiratory compromise remains a leading cause of preventable hospitalizations, payers view investment in advanced single-use devices as a cost-avoidance strategy. The combined demographic and environmental backdrop signals enduring momentum for the respiratory and anesthesia disposables market.

Growing Volume Of Surgical Procedures

Inpatient surgical volumes are expected to climb 3% to 31 million procedures by 2030, while outpatient surgeries rise 17% to 5.82 billion. Each procedure requires a fresh set of airway consumables, binding disposable demand directly to procedural growth. Ambulatory surgery centers, which emphasize rapid turnover and cross-contamination avoidance, rely almost exclusively on single-use airway kits. New minimally invasive and robotic techniques often specify higher-performance breathing circuits and filters, reinforcing premium segment expansion. As elective surgery backlogs clear, distributors prioritizing consistent supply and compliance gain negotiating power with providers.

High Prevalence Of Tobacco Smoking

Asia-Pacific accounts for more than half of global smokers, sustaining elevated incidence of obstructive lung pathologies that demand ongoing respiratory interventions. Eastern Europe and parts of the Middle East also maintain high smoking prevalence, extending geographic breadth for disposable device consumption. Public health campaigns moderate smoking rates in developed markets, yet legacy patient cohorts continue to require chronic respiratory support. Device makers that bundle smoking cessation monitoring or data-capture capabilities into disposables can align with preventive health financing trends.

Infection-Control Push For Single-Use Airway Products

Guidance from the Centers for Disease Control and Prevention underscores that single-use items eliminate cross-infection risk inherent to reprocessed airway equipment. Pandemic-era lessons elevated infection control from a cost discussion to a safety imperative, making disposable adoption a non-negotiable standard in many acute-care settings. The U.S. Food and Drug Administration treats hospitals that reprocess single-use devices as manufacturers, exposing them to full regulatory scrutiny and liability[1]Centers for Disease Control and Prevention, “Best Practices for Single-Use (Disposable) Devices,” cdc.gov. Providers therefore favor suppliers that guarantee sterile, individually packaged products with clear chain-of-custody documentation. These requirements reinforce demand for high-quality disposables and strengthen supplier relationships where reliability is proven.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost of single-use consumables

High cost of single-use consumables

| -1.6% | Global; acute in cost-constrained systems | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-1.6%

| Geographic Relevance:

Global; acute in cost-constrained systems

| Impact Timeline:

Short term (≤ 2 years)

|

Margin pressures from bulk-purchase tenders

Margin pressures from bulk-purchase tenders

| -1.2% | North America and EU; spreading to organized markets worldwide | Medium term (2-4 years) | |||

Lengthy product-registration timelines

Lengthy product-registration timelines

| -0.8% | Global; varied regulatory efficiency | Long term (≥ 4 years) | |||

Sustainability backlash against single-use plastics

Sustainability backlash against single-use plastics

| -1.1% | EU core; expanding to environmentally conscious regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost Of Single-Use Consumables

Medical supply spend reached USD 146.9 billion in 2023, consuming 10.5% of average hospital budgets. With payer reimbursement often lagging inflation, providers scrutinize every purchase order, forcing aggressive negotiations and multi-year framework agreements. Manufacturers must demonstrate lower total cost of ownership through reduced complication rates and faster patient turnover. Value-based pricing and risk-sharing contracts are moving from concept to requirement, pressuring margins for suppliers unable to quantify outcomes.

Margin Pressures From Bulk-Purchase Tenders

Group purchasing organizations and national tenders consolidate buying power, particularly in Europe and North America. Larger suppliers with diversified portfolios can absorb thinner unit margins, while smaller firms may struggle to compete. Strategic differentiation now depends on dependable supply, documented compliance, and adjunct service offerings rather than price alone. Manufacturers therefore invest in digital inventory management tools that improve visibility and cut stock-outs, defending position despite price compression.

Segment Analysis

By Device Type: Endotracheal Leadership With Smart Circuit Momentum

Endotracheal and tracheostomy tubes captured 29.45% of respiratory and anesthesia disposables market share in 2025, underscoring their centrality in airway management for emergency, critical care, and surgical settings. They remain volume anchors because every intubation event mandates a fresh single-use tube to mitigate infection risk. The respiratory and anesthesia disposables market size for breathing circuits is forecast to expand at an 11.12% CAGR, buoyed by adoption of closed-loop ventilation platforms that rely on circuit-embedded sensors for continuous patient monitoring. Laryngoscope demand benefits from the shift toward video-enabled blades that improve first-pass success rates and reduce soft-tissue trauma. Anesthesia and oxygen masks grow in line with procedure counts, while filters and heat moisture exchangers gain traction as infection-control protocols tighten filtration requirements.

Smart breathing circuits exemplify how disposables evolve into value-added components. The Fraunhofer oxygen sensor demonstrates feasibility of integrating fluorescence transducers that report saturation to bedside monitors, enabling clinicians to titrate ventilation parameters precisely. This capability unlocks premium pricing, especially in high-acuity units where ventilator downtime carries heavy cost. As evidence mounts that closed-loop circuits shorten ventilation duration, procurement teams view them as cost-avoidance investments rather than consumables. Suppliers able to protect intellectual property around embedded analytics should maintain pricing power despite tender pressures.

Note: Segment shares of all individual segments available upon report purchase

By Application: COPD Scale Meets Sleep Apnea Upswing

COPD accounted for 32.78% of 2025 demand and continues to anchor volume as large patient cohorts require both in-hospital and domiciliary respiratory support. The respiratory and anesthesia disposables market size linked to sleep apnea is growing at a 12.05% CAGR, reflecting widespread diagnostic expansion and rising public health campaigns that highlight long-term cardiovascular risks. Home sleep testing and auto-titrating CPAP systems rely on disposable interfaces such as nasal pillows, filters, and humidification chambers that need regular replacement, reinforcing recurring revenue streams.

Application diversification safeguards suppliers against procedural cyclicality. Trauma and emergency events continue to demand rapid-deployment airway kits where reliability trumps price. Surgical applications track overall procedure growth, supporting steady consumption of anesthesia breathing circuits and masks. Asthma-related disposables benefit from swelling incidence in urbanizing Asia, although growth remains moderate compared with COPD and sleep apnea. Collectively, these patterns underpin resilience in the respiratory and anesthesia disposables market even when macroeconomic swings temper elective procedures.

By End-User: Hospitals Hold Scale While Home-Care Gains Ground

Hospitals retained 50.36% of revenue in 2025, largely because intensive care units and operating theaters use high-specification disposables that command premium margins. Purchasing departments favor vendors with proven compliance track records and robust delivery logistics, cementing relationships that can last contract cycles of three to five years. Nevertheless, the respiratory and anesthesia disposables market is witnessing a swift 10.14% CAGR in home-care and ambulatory channels as payers shift treatment to less costly settings. Patients appreciate therapy continuity at home, especially for chronic indications such as COPD and sleep apnea. Clinics and physician offices also gain share by performing more outpatient procedures that previously required hospital admission.

Product design is adapting accordingly. User-friendly connectors, color-coded valves, and intuitive packaging now matter as much as clinical performance. Fisher & Paykel Healthcare, for instance, highlights nasal high-flow therapy kits tailored for domiciliary COPD management, underscoring how the respiratory and anesthesia disposables industry pivots toward the home environment. Manufacturers that can build direct-to-patient distribution and remote troubleshooting capabilities will command loyalty beyond the initial sale.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated 40.15% of global revenue in 2025, supported by advanced hospital infrastructure, predictable reimbursement, and early adoption of AI-integrated breathing circuits. The respiratory and anesthesia disposables market size in the United States benefits from elective surgery recovery and an aging population with high comorbidity rates. Canada’s single-payer system presses for evidence-based cost justification, yet still funds premium disposables when clinical value is clear. Mexico broadens regional opportunity through hospital modernization and medical tourism growth that demands internationally accepted infection-control products.

Europe occupies the second-largest revenue position and sets regulatory tone through the Medical Device Regulation 2017/745, which elevates post-market surveillance and traceability standards. The Packaging and Packaging Waste Regulation will soon require recyclability, compelling material innovation across the respiratory and anesthesia disposables market. Germany, France, and the United Kingdom remain early adopters of sensor-enabled airway consumables, whereas Southern Europe prioritizes cost-efficient product lines. Hospitals increasingly factor environmental scorecards into tender awards, giving an edge to manufacturers with demonstrable circular-economy roadmaps.

Asia-Pacific is the fastest-growing region at a 10.37% CAGR through 2031. China leads in volume, driven by air-quality-related respiratory morbidity and extensive ICU capacity expansion. Japan emphasizes premium products that reduce nursing workload amid labor shortages, while South Korea accelerates rollout of smart operating theaters that specify high-performance disposables. India and Southeast Asia lean toward affordable single-use devices that still meet US FDA or EU CE standards, opening the field to multinational and domestic manufacturers capable of localized production. The fragmented payer landscape across Asia-Pacific necessitates flexible pricing and robust distributor partnerships, but growth potential is unmatched.

Competitive Landscape

Market Concentration

The respiratory and anesthesia disposables industry remains moderately fragmented. Teleflex, Medtronic, and Philips keep positions at the high-end of the market by coupling airway consumables with monitoring systems and capital equipment ecosystems. Teleflex reported USD 95.3 million in anesthesia segment revenue in Q4 2024 as the company balanced innovation spending with margin resilience[2]Teleflex Incorporated, “Teleflex Reports Fourth Quarter and Full Year 2024 Financial Results,” investors.teleflex.com. Medtronic leverages integrated supply agreements to protect share in advanced endotracheal tube sub-segments, while Philips positions its consumables alongside Sleep and Respiratory Care platforms to reinforce device attachment rates.

Competitive intensity is rising as digital health entrants collaborate with established disposables vendors. Becton Dickinson agreed to acquire Edwards Lifesciences’ Critical Care product group for USD 4.2 billion to deepen smart connected-care offerings that rely on single-use sensors. Ambu, well-known for single-use endoscopes, continues to scale its anesthesia disposables line, reporting double-digit organic revenue growth in Q1 2025. Meanwhile, private-label suppliers intensify price competition in basic masks and breathing bags, particularly in Asia-Pacific and South America.

Supply-chain resilience emerged as a differentiator after pandemic shortages. A 2024 American Hospital Association survey found 93% of providers still experience intermittent stock-outs, prompting multi-sourcing strategies[3]American Hospital Association, “2023 Costs of Caring,” aha.org. Vendors that maintain dual manufacturing footprints in different regions or nearshore facilities are preferred partners. Sustainability credentials are also entering contract criteria, favoring large firms with bankrolls to retrofit plants for recyclable materials. Overall, the competitive landscape rewards a mix of scale, regulatory expertise, and technology integration rather than price alone.

Respiratory And Anesthesia Disposables Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: North American Partners in Anesthesia and Sentara Health Plans rolled out a quality-based program aimed at improving patient outcomes while reducing costs for anesthesia care.

- January 2025: EmpNia received FDA clearance to market eMotus, a disposable sensor pad that tracks respiratory motion during image-guided radiation therapy.

Table of Contents for Respiratory And Anesthesia Disposables Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Respiratory Disorders

- 4.2.2Growing Volume Of Surgical Procedures

- 4.2.3High Prevalence Of Tobacco Smoking

- 4.2.4Infection-Control Push For Single-Use Airway Products

- 4.2.5AI-Enabled Disposable Sensors For Ventilation Monitoring

- 4.3Market Restraints

- 4.3.1High Cost Of Single-Use Consumables

- 4.3.2Margin Pressures From Bulk?Purchase Tenders

- 4.3.3Lengthy Product-Registration Timelines

- 4.3.4Sustainability Backlash Against Single-Use Plastics

- 4.4Technological Outlook

- 4.5Porter's Five Forces

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Device Type

- 5.1.1Laryngoscopes

- 5.1.2Endotracheal & Tracheostomy Tubes

- 5.1.3Anesthesia & Oxygen Masks

- 5.1.4Breathing Circuits

- 5.1.5Manual & Bag Resuscitators

- 5.1.6Reservoir/Breathing Bags

- 5.1.7Filters & HMEs

- 5.1.8Other Disposables

- 5.2By Application

- 5.2.1Chronic Obstructive Pulmonary Disease (COPD)

- 5.2.2Surgical Procedures

- 5.2.3Asthma

- 5.2.4Sleep Apnea

- 5.2.5Emergency & Trauma Use

- 5.3By End-User

- 5.3.1Hospitals

- 5.3.2Clinics & Physician Offices

- 5.3.3Trauma & Emergency Centers

- 5.3.4Home-care & Ambulatory Settings

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Teleflex Inc.

- 6.3.2Medtronic plc

- 6.3.3Koninklijke Philips N.V.

- 6.3.4Ambu A/S

- 6.3.5Becton, Dickinson and Company

- 6.3.6ResMed Inc.

- 6.3.7Fisher & Paykel Healthcare

- 6.3.8Vyaire Medical Inc.

- 6.3.9Armstrong Medical Industries Inc.

- 6.3.10SunMed

- 6.3.11Intersurgical Ltd.

- 6.3.12Flexicare Medical Ltd.

- 6.3.13Cardinal Health Inc.

- 6.3.14GE Healthcare

- 6.3.15ICU Medical Inc.

- 6.3.16Dragerwerk AG & Co. KGaA

- 6.3.17B. Braun Melsungen AG

- 6.3.18PARI Respiratory Equipment Inc.

- 6.3.19Boston Scientific Corporation

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Respiratory And Anesthesia Disposables Market Report Scope

The respiratory and anesthesia disposables are medical consumables meant for single use in order to prevent cross-contamination among patients. These disposables greatly reduce the economic burden on the healthcare systems by eliminating the risk of re-infection, as they can be cast off after a single-use or material deterioration.

The respiratory and anesthesia disposables market is segmented by type, application, end-user, and geography. By type the market is segmented as laryngoscope, tubes, masks, breathing circuits, resuscitators, breathing bags, filters, and other types. By application the market is segmented as chronic obstructive pulmonary disease, surgical procedures, asthma, sleep apnea, and emergency use. By end-user the market is segmented as hospitals, clinics, and trauma centers. By geography the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD) for the above segments.