Bronchoscope Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

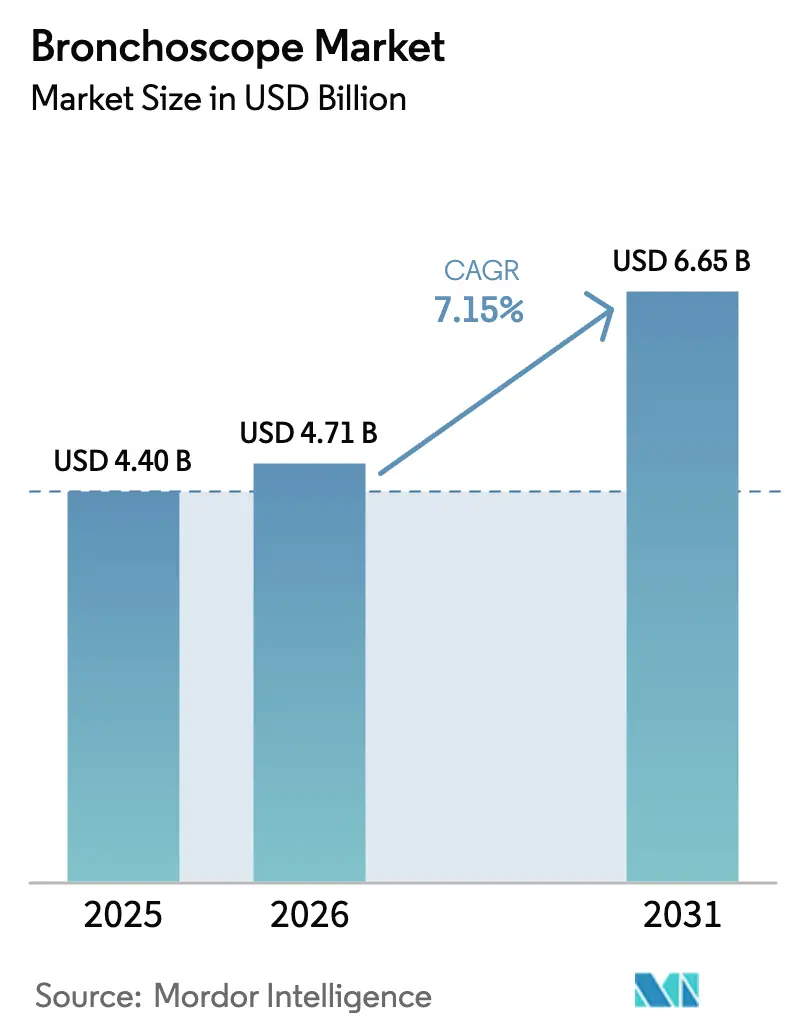

| Market Size (2026) | USD 4.71 Billion |

| Market Size (2031) | USD 6.65 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

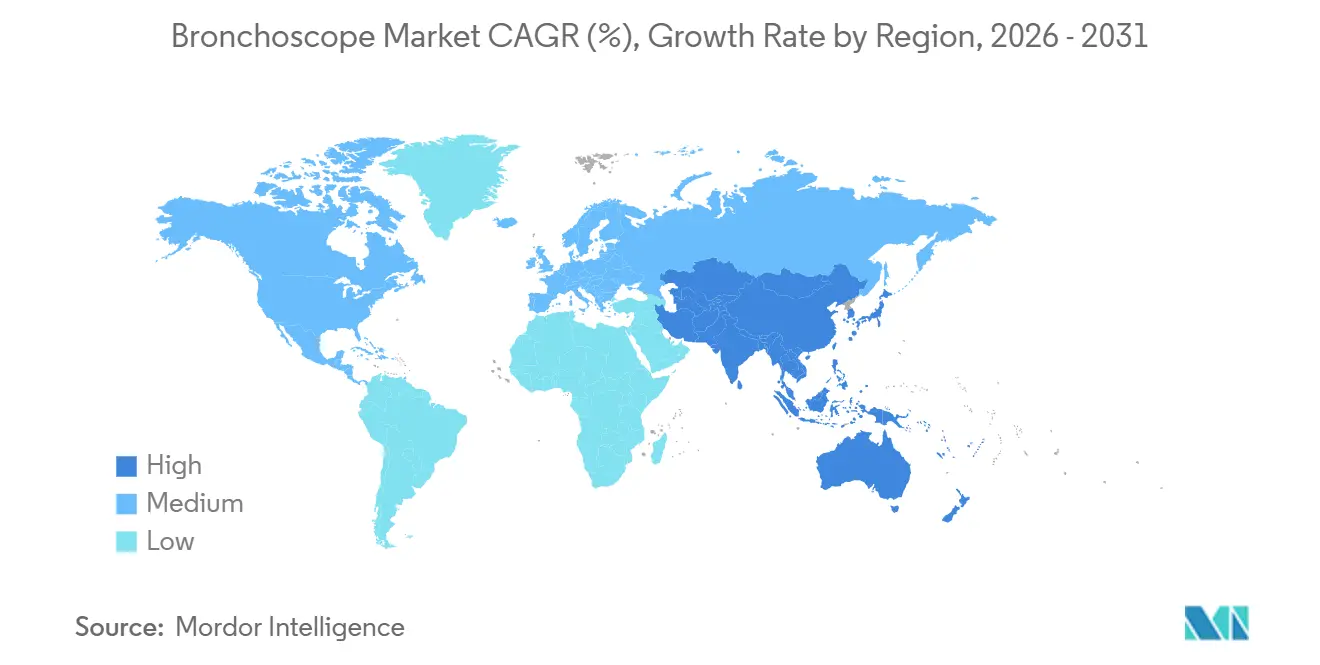

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bronchoscope Market Analysis by Mordor Intelligence

The Bronchoscope Market size is projected to expand from USD 4.40 billion in 2025 and USD 4.71 billion in 2026 to USD 6.65 billion by 2031, registering a CAGR of 7.15% between 2026 to 2031.

Structural tailwinds include the Centers for Medicare & Medicaid Services’ HCPCS C1601 pass-through payment, persistent infection-control pressures, and rising lung-cancer screening volumes that collectively accelerate the swing from reusable to single-use scopes. Hospitals continue to modernize bronchoscopy suites, but ambulatory surgical centers are capturing procedure growth as payers push site-of-care shifts to curb costs. Robotic platforms equipped with AI navigation are improving diagnostic yield, compressing the learning curve, and squeezing legacy flexible-scope differentiation. Asia-Pacific’s screening initiatives anchor long-term demand even as semiconductor and sterile-plastic shortages cloud near-term supply visibility.

Key Report Takeaways

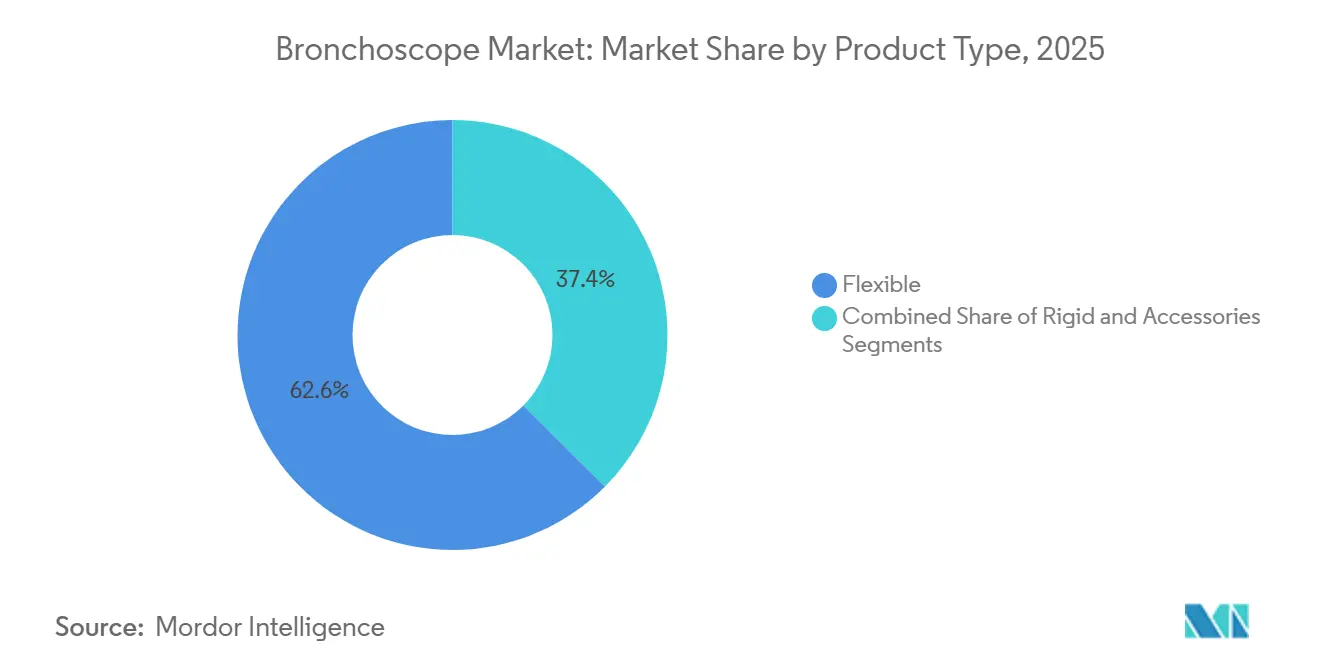

- By product type, flexible bronchoscopes led with 62.56% of bronchoscope market share in 2025, while the same category is advancing at a 10.25% CAGR through 2031.

- By usage, reusable devices accounted for 65.53% share of the bronchoscope market size in 2025; single-use scopes are expanding at a 15.85% CAGR to 2031.

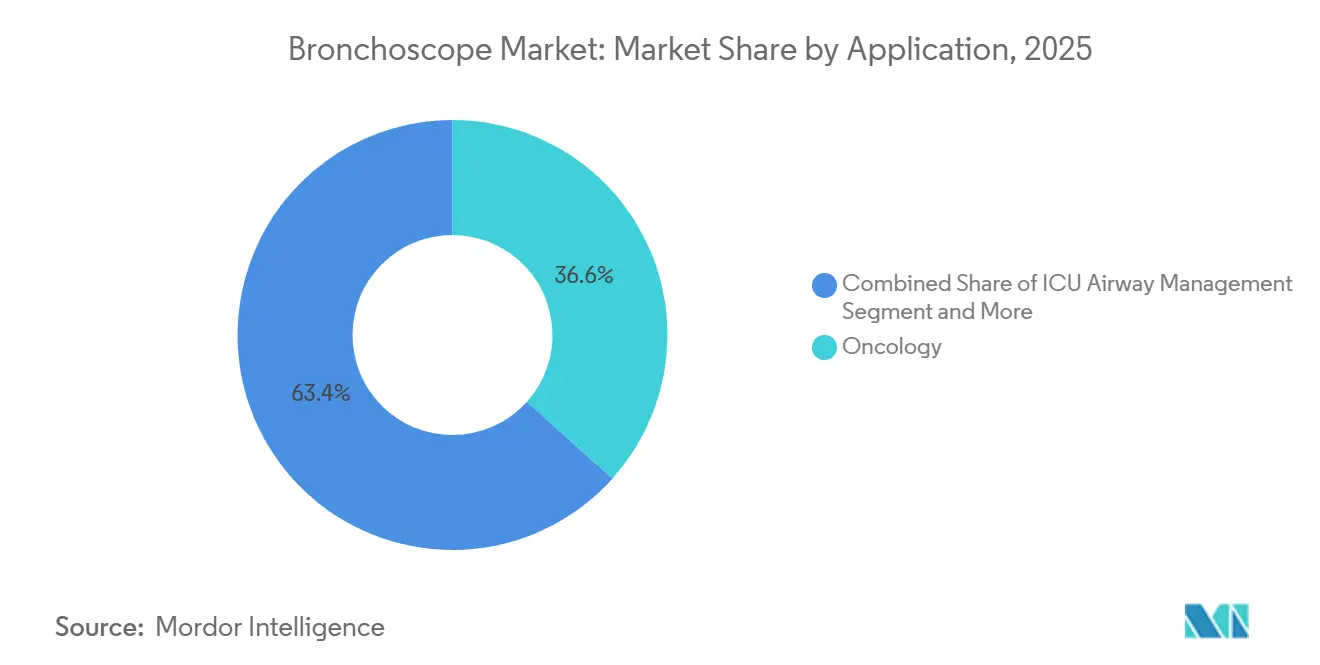

- By application, oncology represented 36.63% of the bronchoscope market size in 2025, whereas ICU airway management is tracking a 12.87% CAGR through 2031.

- By end user, hospitals held 73.33% share of the bronchoscope market size in 2025; ambulatory surgical centers are growing at an 11.7% CAGR to 2031.

- By geography, North America captured 42.13% of bronchoscope market share in 2025, yet Asia-Pacific is forecast to expand at a 9.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bronchoscope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of respiratory diseases & lung cancer | +2.1% | Global, strongest in Asia-Pacific | Long term (≥ 4 years) |

| Growing hospital investment in bronchoscopy suites | +1.3% | North America & Europe, emerging APAC tier-2 cities | Medium term (2-4 years) |

| Technological advances in optics & imaging | +1.5% | Global, led by North America & Europe | Medium term (2-4 years) |

| Rapid adoption of AI-guided navigation bronchoscopy | +1.8% | North America & Europe, early APAC centers | Short term (≤ 2 years) |

| Reimbursement expansion for single-use bronchoscopes | +1.2% | North America, selective Europe | Short term (≤ 2 years) |

| Shift toward office-based/ASC bronchoscopy | +1.0% | North America, Australia, parts of Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Respiratory Diseases & Lung Cancer

GLOBOCAN 2022 logged 2.48 million new lung-cancer cases worldwide and projects 4.62 million by 2050, with Asia responsible for 63% of the load. The 2024 U.S. screening-age reduction to 50 years added 6.4 million eligible adults, stretching interventional capacity and reinforcing robotic bronchoscopy adoption. Chronic obstructive pulmonary disease affects more than 390 million people, underpinning baseline diagnostic demand. Rising case volumes draw bronchoscopy closer to primary care, rewarding portable, single-use devices that avoid capital outlays. China’s 28% jump in lung-cancer diagnoses from 2019-2024 highlights a geographic imbalance that tele-mentored bronchoscopy may help address.

Rapid Adoption of AI-Guided Navigation Bronchoscopy

Johnson & Johnson’s MONARCH QUEST, cleared in March 2025, automates path planning and trims catheter repositioning by 35-40%. Intuitive Surgical’s Ion upgrade gained clearance in October 2025 and now tops 900 global installs, using shape-sensing fiber optics to lift diagnostic yield to roughly 82%. Meta-analysis data place robotic yield 8-11 percentage points above traditional electromagnetic navigation. Noah Medical’s single-use Galaxy system extends these gains to ambulatory settings by embedding real-time tomosynthesis imaging. The shorter 40-60-case proficiency curve alleviates workforce bottlenecks, a critical lever where trained specialists are scarce.

Reimbursement Expansion for Single-Use Bronchoscopes

HCPCS C1601, active January 2024 through December 2026, delivers separate payment for disposable scopes on top of procedure reimbursement, neutralizing their higher per-case price in outpatient sites[1]Centers for Medicare & Medicaid Services, “HCPCS C1601: Single-Use Pulmonary Bronchoscope,” cms.gov . UnitedHealthcare and Anthem adopted parallel coverage in 2024, citing reduced cross-contamination risk. ASCs, numbering 6,308 Medicare-certified centers in 2025, can now offer bronchoscopy without USD 40,000–60,000 capital spend per reusable scope. Manufacturers face a 2026 deadline to cement clinical evidence before pass-through expiration.

Shift Toward Office-Based/ASC Bronchoscopy

Eighty-two percent of U.S. hospitals owned or partnered with an ASC by 2024, anticipating migration of low-acuity procedures. Diagnostic bronchoscopy receives 35-45% lower Medicare payment in ASCs than hospital outpatient departments, creating a payer-driven push. Single-use scopes bypass sterilization, letting freestanding centers schedule same-day cases. Teleflex’s portable platform targets physician-office labs where procedure volumes are modest and capital budgets thin. Hospitals risk losing profitable diagnostics that subsidize complex therapeutics, challenging fellowship economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High overhead cost of bronchoscopy procedure | -1.4% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Infection-control concerns with reusable scopes | -0.9% | North America & Europe | Short term (≤ 2 years) |

| Shortage of trained interventional pulmonologists | -1.1% | Global, severe in tier-2/3 regions | Long term (≥ 4 years) |

| Supply-chain tightness for CMOS sensors & sterile plastics | -0.8% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Overhead Cost of Bronchoscopy Procedure

A 2024 CHEST analysis placed U.S. outpatient bronchoscopy at USD 2,800–3,500 per case, dropping to USD 1,800–2,200 in ASCs yet still beyond reach in markets where annual per-capita health spend is under USD 500. India’s 48% out-of-pocket share limits access to urban insured populations. CMS trimmed payment by 2.8% in the 2025 fee schedule, intensifying throughput pressure. Robotic platforms partly offset cost by elevating first-pass success, but anesthesia and monitoring remain fixed expenses.

Shortage of Trained Interventional Pulmonologists

Fewer than 1,500 board-certified specialists practice in the United States, and fellowship programs add only 80-90 graduates per year. China counts roughly 200-250 trained physicians for 1.4 billion people. Robotic systems cut the learning curve roughly in half, while remote proctoring on the Ion platform allows urban experts to supervise rural cases in real time[3]Intuitive Surgical, “Ion Navigation Software Clearance,” intuitive.com. Single-use scopes with simpler controls enable supervised procedures by nurse practitioners where regulations permit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flexible Scopes Dominate Innovation

Flexible bronchoscopes owned 62.56% of bronchoscope market share in 2025 and are projected to expand at 10.25% CAGR to 2031, buoyed by robotic platforms that reach peripheral nodules previously inaccessible to manual scopes[2]Johnson & Johnson, “MONARCH QUEST FDA Clearance,” jnj.com. Rigid scopes stay confined to central airway work in operating rooms and therefore grow slowly. Accessory disposables, ranging from biopsy forceps to cryoprobes, create a recurring revenue layer that scales with every additional procedure.

Robotic navigation raises diagnostic accuracy from about 70% with standard flexible scopes to 80-84%, pivoting clinical preference toward the new generation of intelligent instruments. Disposable accessories align with infection-control policies and avoid reprocessing downtime. Medtronic’s cryobiopsy probes, introduced in 2024, are expanding tissue-sampling indications, further lifting procedure complexity and volume.

By Usage: Single-Use Gains Despite Reusable Dominance

Reusable devices represented 65.53% of the bronchoscope market size in 2025 because hospitals still rely on installed capital fleets. Yet single-use scopes are accelerating at 15.85% CAGR, thanks to pass-through reimbursement that offsets their higher variable cost. Ambu and Boston Scientific command early traction in ASCs that lack centralized sterilization.

A reusable scope amortized across 400-500 uses averages USD 150-250 per case; contamination incidents and labor costs tilt the equation as FDA alerts increase board scrutiny. Single-use options deliver 1080p imaging in models such as Ambu’s aScope 5, removing historic performance gaps. When pass-through payments sunset in 2026, device makers must prove long-term economic value to sustain adoption.

By Application: ICU Airway Management Surges

Oncology sustained 36.63% of bronchoscope market size in 2025, but ICU airway management is rushing forward at 12.87% CAGR on the back of ventilator-associated pneumonia protocols. Guidelines now endorse bronchoscopy when imaging is inconclusive, making bedside access crucial.

Point-of-care systems such as Ambu’s aView let intensivists avoid moving unstable patients, limiting cross-infection. Diagnostic yield for opportunistic infections in immunocompromised patients surpasses 80% compared with roughly 55% for non-invasive tests. Oncology growth moderates due to rising prior-authorization hurdles, but early-stage detection keeps overall procedure numbers firm.

By End User: ASCs Gain as Hospitals Dominate

Hospitals retained 73.33% of end-user demand in 2025 given their dominance in complex therapeutic work and robotic installations. Ambulatory surgical centers, however, are on an 11.7% CAGR trajectory, fueled by payer directives and single-use economics that bypass sterilization infrastructure.

ASCs focus on diagnostic and simple therapeutic cases with <2% complication rates, while hospitals guard advanced interventions such as airway stenting. Office-based labs remain nascent but are growing where nurse practitioners can conduct supervised procedures. The decentralization trend threatens hospital revenue streams that subsidize fellowship training and capital amortization.

Geography Analysis

North America captured 42.13% of bronchoscope market share in 2025 on the back of 180–220 procedures per 100,000 population and early robotic uptake. The 2024 screening-age drop expanded the eligible pool by 6.4 million, yet trained-specialist shortages lengthened waitlists in many states. HCPCS C1601 accelerates single-use adoption across 6,308 ASCs, while Canada’s capped reimbursement and 4-8-week waits are spawning private clinics. Mexican demand divides between urban private hospitals and under-equipped public centers.

Asia-Pacific outpaces all regions at 9.51% CAGR through 2031. China’s state screening pushes, India’s respiratory-care expansion, and South Korea’s 2024 coverage of robotic bronchoscopy drive volume. Japan’s 28% senior population sustains COPD-related demand; however, 2024 reimbursement cuts encourage disposable-scope adoption to save labor costs. Australia’s 2024 clearance of Ambu’s aScope 5 extends services to remote clinics lacking sterilization.

Europe holds roughly one-quarter of global revenue and sees heterogeneous policy environments. Germany’s DRG incentives promote robotics for efficiency; Charité reported a 22% volume spike after installing Ion in 2024. NHS England pilots single-use scopes in community centers to cut 12-week waits. France added outpatient reimbursement in 2024 after a contamination scare. Fiscal limits in Italy and Spain postpone capital upgrades. Middle East programs in the UAE and Saudi Arabia broaden screening, whereas Latin American growth hinges on Brazilian and Argentine private sectors amid public-sector shortfalls.

Competitive Landscape

The bronchoscope market features a core reusable triad of Olympus, Pentax Medical, and Fujifilm, versus rising single-use leaders Ambu and Boston Scientific. Robotic entrants intensify rivalry. MONARCH QUEST’s 260% computing-power jump and 35-40% repositioning cut shave procedure time, eroding classical flexible-scope loyalty. Intuitive Surgical’s Ion exceeds 900 installs, fighting on diagnostic-yield superiority backed by 18 navigation patents. Noah Medical targets ASCs with a disposable robotic platform that eliminates fluoroscopy and eases capital hurdles.

Two strategic camps emerge. Capital-equipment vendors pursue razor-and-blade revenue via catheter disposables and software subscriptions. Disposable-scope makers battle on infection-control, variable cost, and site-of-care flexibility. Olympus and Pentax defend turf with trade-in deals and extended warranties, but CMS pass-through support for single-use scopes compresses price latitude until 2026.

Tele-mentored bronchoscopy surfaces as whitespace; Ion’s remote proctoring permits urban experts to guide rural operators, partially offsetting workforce gaps. Patent landscapes center on AI path-planning and shape-sensing fiber optics, raising entry barriers for latecomers. Market participants must decide between licensing navigation tech or focusing on cost-efficient, single-use expansion as capital budgets disperse across more sites of care.

Bronchoscope Industry Leaders

Teleflex Inc.

Olympus Corporation

Ambu A/S

Fujifilm Holdings Corporation

Karl Storz GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Olympus launched the BF-UCP190F EBUS bronchoscope across EMEA, enhancing real-time ultrasound visualization.

- March 2025: Johnson & Johnson secured FDA clearance for MONARCH QUEST, bringing AI path planning and 260% higher computational power to peripheral-nodule biopsy.

Global Bronchoscope Market Report Scope

As per the scope, a bronchoscope is used in examining the trachea, windpipe, and lungs, and it mainly consists of a hollow metal tube or a thinner tube with an attached fiberoptic or video camera for transmitting the image.

The bronchoscope market is segmented by product type, usage, application, end user, and geography. By product type, the market is categorized into rigid, flexible, and accessories. By usage, it is divided into single-use bronchoscopes and reusable bronchoscopes. By application, the segmentation includes oncology (biopsy and staging), pneumonia and infection diagnosis, foreign-body removal, and ICU airway management. By end user, the market is segmented into hospitals, ambulatory surgical centers, and specialty clinics and office-based labs. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Rigid |

| Flexible |

| Accessories |

| Single-use Bronchoscope |

| Reusable Bronchoscope |

| Oncology (biopsy & staging) |

| Pneumonia & Infection Diagnosis |

| Foreign-body Removal |

| ICU Airway Management |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics & Office-based Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Rigid | |

| Flexible | ||

| Accessories | ||

| By Usage | Single-use Bronchoscope | |

| Reusable Bronchoscope | ||

| By Application | Oncology (biopsy & staging) | |

| Pneumonia & Infection Diagnosis | ||

| Foreign-body Removal | ||

| ICU Airway Management | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics & Office-based Labs | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the global bronchoscope market size in 2026 and its forecast value for 2031?

Revenue stands at USD 4.71 billion in 2026 and is projected to reach USD 6.65 billion by 2031, supported by a 7.15% CAGR.

How quickly are single-use bronchoscopes expanding compared with reusable units?

Disposable scopes are rising at a 15.85% CAGR through 2031, while reusable devices remain dominant but grow more slowly.

Which geographic region is expected to post the strongest growth through 2031?

Asia-Pacific leads with a 9.51% CAGR, driven by lung-cancer screening programs in China and respiratory-care expansion in India and Southeast Asia.

What CAGR is forecast for flexible bronchoscopes over the next five years?

Flexible platforms, already holding 62.56% share, are forecast to advance at a 10.25% CAGR through 2031 as robotic navigation boosts peripheral-nodule reach.

How does HCPCS C1601 influence device economics in ambulatory surgical centers?

The CMS pass-through payment, active until December 2026, provides separate reimbursement for each single-use bronchoscope, effectively neutralizing higher per-procedure costs for ASCs.

What diagnostic-yield advantage do robotic systems deliver over conventional navigation?

Meta-analyses place robotic-assisted bronchoscopy yields at roughly 80-84%, about 8-11 percentage points higher than traditional electromagnetic navigation.

Page last updated on: