Laundry Detergents Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 107.52 Million |

| Market Size (2031) | USD 134.42 Million |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

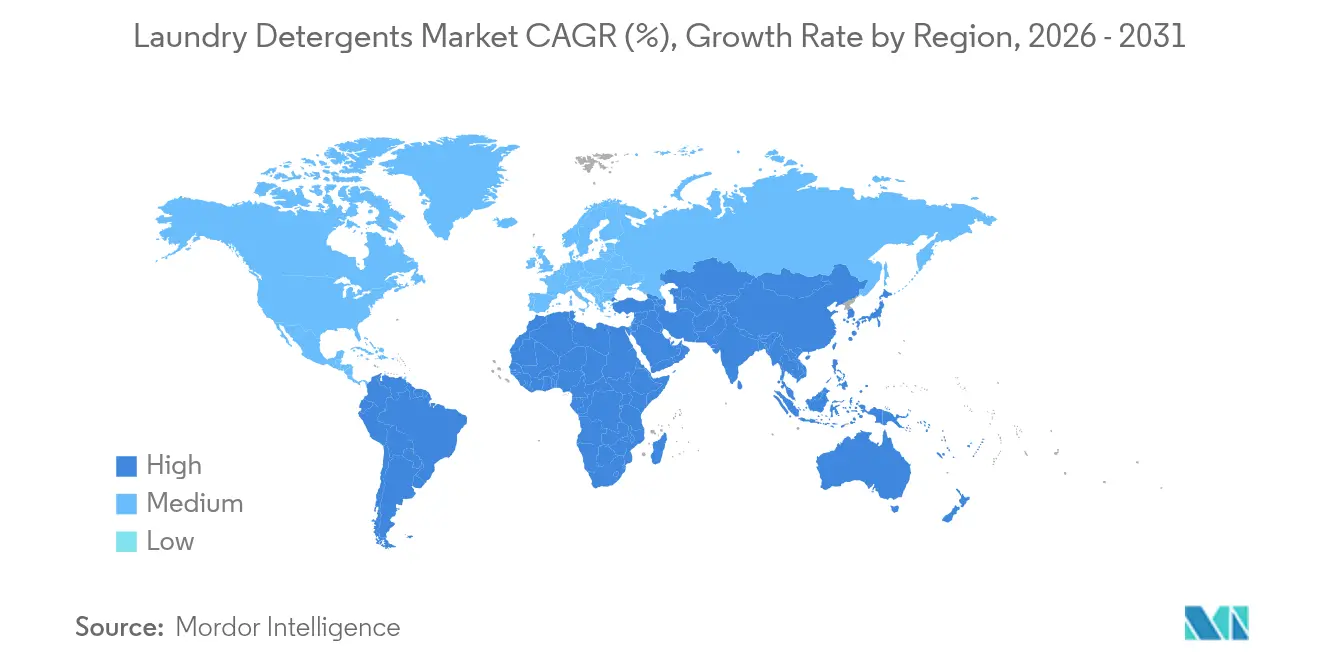

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

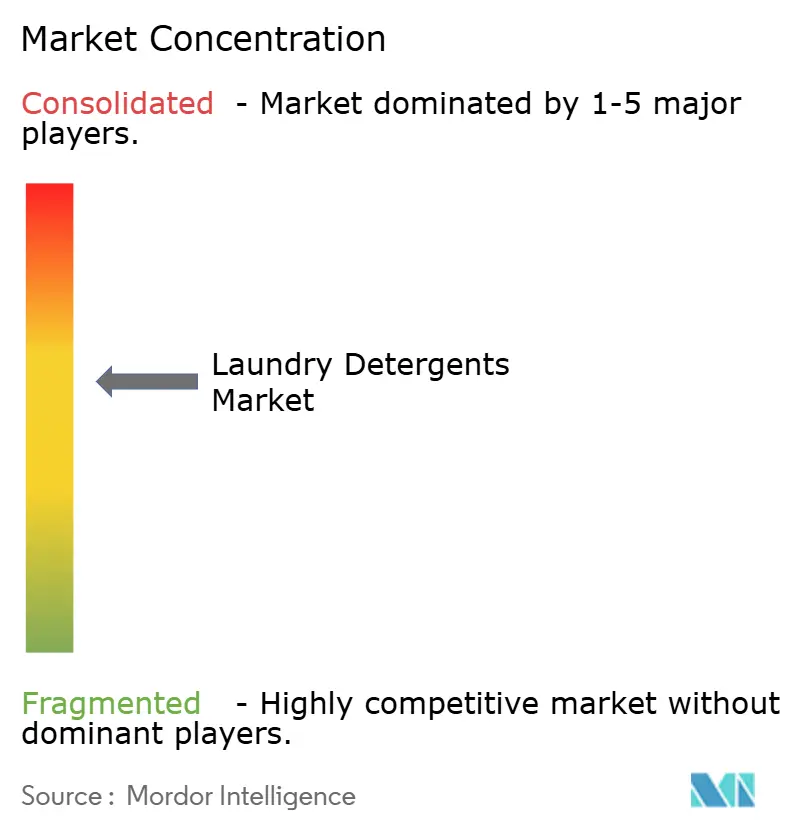

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Laundry Detergents Market Analysis by Mordor Intelligence

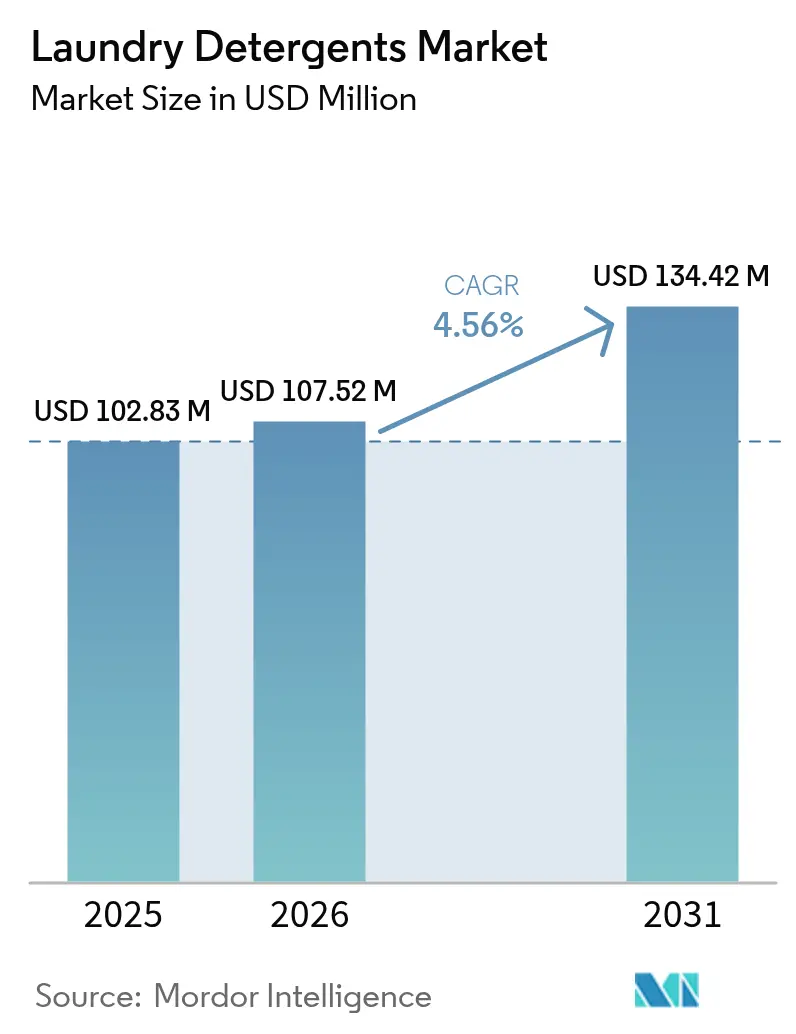

The laundry detergents market size is expected to grow from USD 102.83 million in 2025 to USD 107.52 million in 2026 and is forecast to reach USD 134.42 million by 2031 at 4.56% CAGR over 2026-2031.In a maturing landscape, manufacturers are shifting their focus from sheer volume gains to innovations in energy-efficient cold-water chemistry, bio-based surfactants, and digital distribution. These advancements aim to address evolving consumer preferences and environmental concerns. Regulatory tightening on phosphates and microplastics is prompting manufacturers to renew their portfolios, driving the development of more sustainable and compliant products. In both developed and emerging regions, the demand for premium products like liquids, fabric conditioners, and smart-laundry systems is outpacing that of traditional powders, reflecting a shift toward convenience and enhanced performance. While scale leaders capitalize on their research and development depth and omnichannel reach to maintain a competitive edge, regional specialists are finding success by leveraging sachet economics and localized fragrances, catering to specific market needs. This dynamic has resulted in a moderate competitive intensity across the market.

Key Report Takeaways

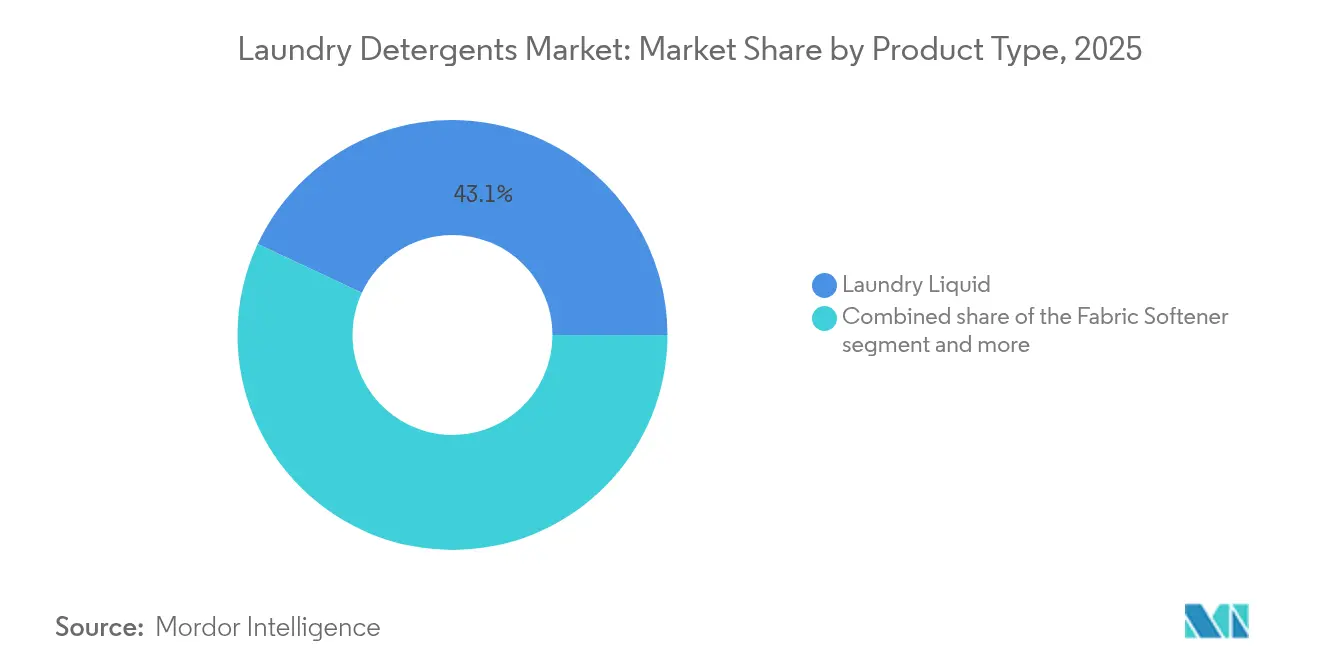

- By product type, laundry liquid led with a 43.05% 2025 share of the laundry detergent market, and fabric softener is projected to post a 6.45% CAGR through 2031.

- By packaging, sachets/pouches held 53.20% of the 2025 laundry detergent market, and PET bottles are expected to advance at a 5.12% CAGR to 2031.

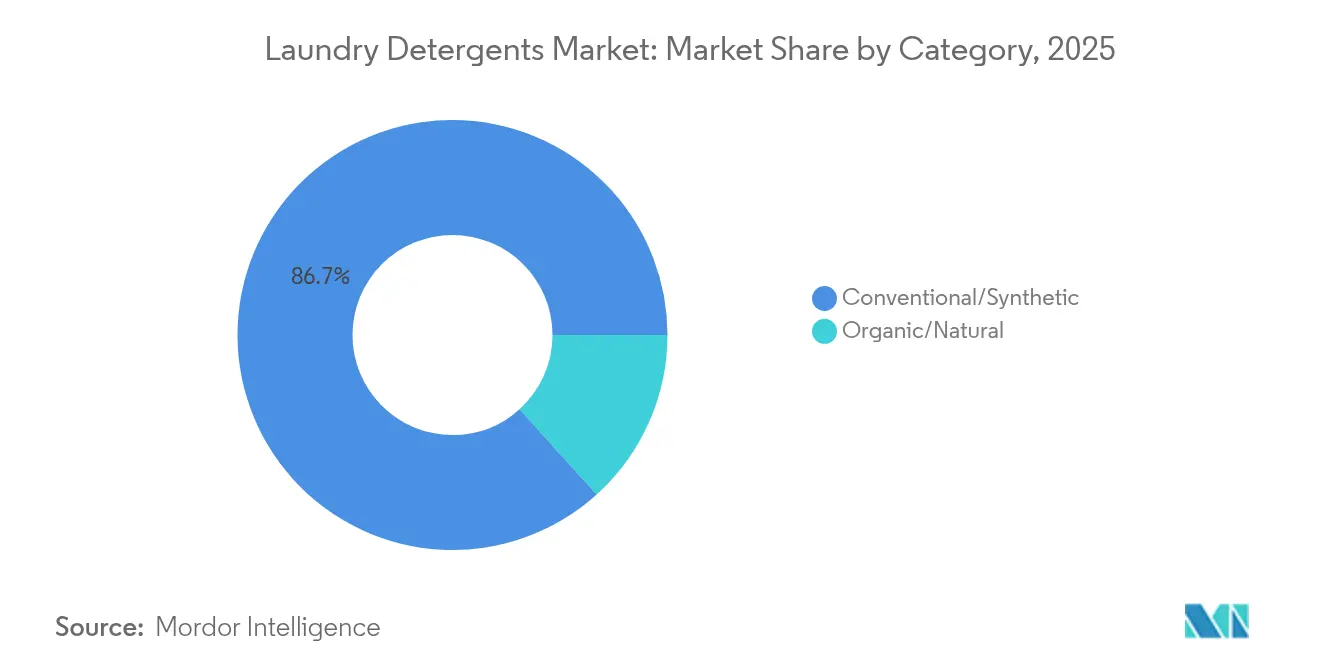

- By category, conventional/synthetic products commanded 86.70% of 2025 revenue, while organic/natural formulations are on track for a 5.95% CAGR over the forecast period.

- By distribution channel, supermarkets/hypermarkets captured 56.90% of the 2025 demand, and online retail stores are forecasted to grow at a 5.55% CAGR through 2031.

- By geography, Asia-Pacific accounted for 36.30% of 2025 revenue, and the Middle East and Africa segment is set for a 5.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laundry Detergents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in cold-water washing formulations | +0.8% | North America and EU early, expanding global | Medium term (2-4 years) |

| Growth of e-commerce refill subscription models | +0.6% | North America and EU core, spreading to Asia-Pacific | Short term (≤ 2 years) |

| Rising washing-machine penetration in emerging Asia | +1.2% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Bio-based surfactant cost parity | +0.9% | EU regulatory push, global scale-up | Medium term (2-4 years) |

| Smart-laundry IoT dispensers in commercial laundromats | +0.3% | North America and EU pilots, Asia-Pacific trials | Long term (≥ 4 years) |

| Ban on phosphate-based detergents in 14 additional nations | +0.7% | Targeted regions worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in cold-water washing formulations

With energy savings ranging from USD 60 to 200 per home and annual CO₂ reductions of 864 lb, cold-water detergents are transitioning from niche products to mainstream essentials. According to the American Cleaning Institute, a significant 90% of a washer's energy consumption is attributed to heating water, underscoring the importance of enzyme-rich blends in reducing energy use and environmental impact[1]Source: American Cleaning Institute, "Cold Water Saves", cleaninginstitute.org. These detergents not only offer cost savings but also align with growing consumer demand for sustainable and eco-friendly products. Procter & Gamble, in collaboration with Walmart, is fast-tracking consumer acceptance by highlighting the premium benefits of cold-wash performance, such as effective cleaning at lower temperatures, reduced energy bills, and a smaller carbon footprint. Utilities are not only setting decarbonization targets but are also facing rising energy tariffs, elevating the efficacy of cold-water detergents from mere marketing claims to essential compliance with sustainability goals. As the industry pivots towards low-temperature proteases and soil-release polymers, suppliers adept in these chemistries are securing lasting advantages on the shelves, positioning themselves as key players in the evolving market landscape. Additionally, the focus on advanced formulations is driving innovation, enabling manufacturers to meet both regulatory requirements and consumer expectations more effectively.

Growth of e-commerce refill subscription models

Unilever's pilot program, "Refill on the Go," in Santiago showcases the power of data-driven subscriptions in minimizing packaging waste and ensuring repeat purchases. By leveraging predictive algorithms, shipments are timed to align with household usage, enhancing customer lifetime value far beyond the benefits of mere shelf placement. These algorithms analyze consumption patterns, enabling precise delivery schedules that reduce the risk of overstocking or running out of products, thereby improving customer satisfaction and loyalty. The logistics of refills favor concentrated liquids and pods, as their lighter weight translates to reduced freight intensity, which not only lowers transportation costs but also contributes to a smaller carbon footprint. In today's marketplace, heightened algorithmic visibility means that strategies for search rankings are becoming as crucial as traditional in-store planogram negotiations. Online platforms now play a pivotal role in influencing consumer purchase decisions, with optimized search rankings directly impacting a brand's visibility and sales performance. With urban millennials placing a premium on doorstep convenience and eco-friendliness, manufacturers that fail to adopt direct-to-consumer fulfillment risk diminishing their brand relevance. This shift underscores the importance of integrating sustainable practices and digital strategies to meet evolving consumer expectations and maintain competitive positioning.

Rising penetration of washing machines in emerging asia

China aims for a 10% reduction in energy and water usage by 2025, pushing detergent manufacturers to collaborate with washer OEMs on high-efficiency liquid detergents[2]Source: China Household Electrical Appliances Association,"Technology Roadmap of China's Household Electric Washing Machine Industry", cheaa.org. This initiative is part of the country's broader sustainability goals, which are driving innovation in detergent formulations to meet stricter environmental standards. In India, a burgeoning middle class is driving sales of automatic washers, leading to increased per-capita detergent consumption and a growing preference for liquids tailored for top-load machines. The shift toward automatic washers is also influenced by urbanization and rising disposable incomes, which are reshaping consumer preferences. Stricter government efficiency labels are elevating minimum performance standards, putting pressure on lower-spec powder detergents to either improve or risk losing market share. These trends solidify the region's 36.68% share of the global laundry detergent market, underscoring its pivotal role as a growth engine for worldwide product pipelines and highlighting the region's influence on shaping global detergent innovation.

Bio-based surfactant cost parity

Global biosurfactant volumes are growing at an annual rate exceeding 20%, narrowing the historical price gap with petroleum derivatives. Advances in fermentation techniques for sophorolipids and rhamnolipids enhance both yield and purity, enabling their integration into mainstream blends without imposing price premiums on consumers. These advancements make biosurfactants more accessible and competitive in the market, driving their adoption across various industries, including personal care, household cleaning, and industrial applications. EU ecolabels provide incentives for this transition by promoting environmentally friendly products, while corporate net-zero commitments ensure a clear demand trajectory, as companies increasingly prioritize sustainability in their operations. With an expanded sourcing of bio-feedstocks, supply security has improved, reducing vulnerability to oleochemical price fluctuations and ensuring consistent availability for manufacturers. Once price parity is firmly established, sustainable surfactants will shift from being a mere line-extension to a central strategy in formulations, enabling companies to align with evolving consumer preferences and regulatory requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile linear alkylbenzene (LAB) feedstock prices | -0.7% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Counterfeits in informal retail networks | -0.4% | Asia-Pacific and MEA | Medium term (2-4 years) |

| Micro-plastic discharge regulations tightening | -0.5% | EU core, expanding global | Medium term (2-4 years) |

| Consumer shift toward detergent-free ultrasonic cleaners | -0.2% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile linear alkylbenzene (LAB) feedstock prices

LAB, accounting for nearly 40% of formulation costs, faces significant pressure from petrochemical price fluctuations. This impact is particularly pronounced for price-sensitive powders manufactured in Asia's key production hubs, where competitive pricing dynamics amplify cost challenges. Furthermore, currency fluctuations and refinery outages exacerbate the timing of cost pass-throughs, compelling manufacturers to adopt risk mitigation strategies such as hedging and ingredient diversification. The heightened volatility in petrochemical markets has also increased the attractiveness of bio-based or synthetic alternatives. These alternatives not only decouple cost structures from crude oil price movements but also provide manufacturers with greater flexibility, improved supply chain resilience, and stability in managing long-term costs. Additionally, the shift toward bio-based or synthetic options aligns with the growing demand for sustainable and environmentally friendly solutions, further driving their adoption in the market.

Counterfeits in informal retail networks

Europol estimates the counterfeit trade, which encompasses items like household cleaners, to be worth a staggering EUR 119 billion[3]Source: European Union Intellectual Property Office, "INTELLECTUAL PROPERTY CRIME THREAT ASSESSMENT 2022", europol.europa.eu. This widespread issue not only undermines brand equity but also erodes consumer trust, posing significant challenges for legitimate businesses. Counterfeit products, such as look-alike sachets, are particularly prevalent in fragmented retail markets, where they divert legitimate market shares and compromise the integrity of category pricing by driving down overall price points. These counterfeit goods often mimic the appearance of genuine products, making it difficult for consumers to distinguish between authentic and fake items. To combat this growing problem, brand owners are increasingly investing in a range of measures. QR-code authentication systems are being implemented to enable consumers and retailers to verify product authenticity quickly. Retailer education programs are being expanded to help store owners and staff identify counterfeit goods and understand the risks they pose to the market. Additionally, brand owners are forming enforcement partnerships with regulatory authorities and law enforcement agencies to crack down on the production and distribution of counterfeit products. While these initiatives are essential to protect brand reputation and consumer trust, they also contribute to rising operational costs for businesses, further straining their resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquids Lead Premium Positioning

In 2025, laundry liquids accounted for 43.05% of the total revenue in the laundry detergent market, cementing their status as the top choice for households using automatic washing machines. Their dominance stems from superior performance in cold washes, excellent solubility, and the ability to support advanced formulations that stabilize enzymes and preserve complex fragrances. Furthermore, liquids facilitate premium product development, allowing for higher suggested retail prices (SRP) while ensuring effective stain removal and fabric care. Continuous packaging innovations, such as monomaterial spouts and refill designs, not only comply with extended producer responsibility (EPR) mandates but also resonate with the growing emphasis on sustainability. Additionally, liquids cater to concentrated formulas and enzyme-boosted gels, offering greater value per wash and appealing to eco-conscious consumers. As market trends lean towards convenience, cleanliness, and sensory appeal, laundry liquids stand firm, enjoying robust loyalty in both developed and emerging markets.

Fabric softeners, though a smaller segment of the laundry care market, are set to grow at a brisk CAGR of 6.45% through 2031, positioning them as the fastest-growing product category. Their allure lies in providing a multisensory laundry experience, boosting fragrance, softness, and freshness, serving as a key differentiator for brands aiming to transcend basic cleaning. This growth is fueled by consumers' increasing willingness to invest in premium garment care, enhancing both the feel and longevity of fabrics. Innovations in scent-release technology and the introduction of allergen-free, plant-based softening agents have expanded their appeal, especially among health- and sustainability-conscious shoppers. Moreover, strategic placement alongside detergents in both brick-and-mortar and online retail channels bolsters cross-selling opportunities, particularly through bundled promotions. As consumers increasingly seek laundry solutions that blend cleaning with fabric conditioning, fabric softeners are set to outpace the growth of other segments in the laundry care market.

By Packaging: Sachets Dominate Emerging Markets

In 2025, single-use sachets and pouches commanded a significant 53.20% share of the laundry detergent packaging market. This dominance is largely attributed to micro-purchase behaviors in rapidly growing markets like India, Indonesia, and Nigeria. While these sachets offer an affordable entry point for consumers, aligning with their cash-flow realities, the cost-per-wash tends to be higher. This packaging format has found a stronghold in rural and low-income demographics, providing immediate access without the need for bulk purchases. In many emerging markets, sachets serve as the initial touchpoint for consumers with branded detergents, fostering brand familiarity and loyalty. Yet, as concerns over plastic waste mount, governments are taking notice, launching pilot initiatives to explore paper-based laminate alternatives. Brands catering to these markets now face the challenge of balancing affordability and convenience with the growing emphasis on sustainability and tightening regulations.

PET bottles are set to emerge as the fastest-growing packaging choice in the laundry detergent sector, boasting an expected CAGR of 5.12% during the forecast period. This surge is largely driven by the rise of refill subscription programs, which champion both convenience and environmental stewardship through container reuse. The rigid structure of PET bottles ensures their inherent durability, making them well-suited for repeated handling and transport. Moreover, their transparent nature allows brands to highlight color-coded liquids, signaling formulation sophistication and a premium image. Urban markets are particularly embracing PET bottles, bolstered by organized retail's bundle promotions and recycling incentives. This trend not only resonates with consumers' evolving sustainability values but also enhances the premium perception of PET bottles, enabling them to capture market share from single-use formats, especially among affluent and environmentally conscious segments. With brands innovating in areas like lightweighting, recycled content, and advanced closure designs, PET bottles are well-positioned for sustained growth in both emerging and established markets.

By Category: Conventional Maintains Scale Advantage

In 2025, conventional laundry detergent formulations captured 86.70% of total revenue, solidifying their dominance in the market. This leadership is rooted in decades of reliable performance, strong consumer trust, and cost structures fine-tuned for mass production and affordability. Most households still favor conventional products, striking a dependable balance between cleaning power and value. Their scale advantages facilitate widespread retail presence in both developed and emerging markets. While some retail channels are shifting shelf space to eco-friendly lines, mainstream synthetic formulations enjoy the benefits of brand loyalty and habitual buying. Despite the rise of innovations in greener segments, conventional formulas bolster their market position by pairing slight efficiency gains with competitive pricing.

Organic and natural laundry detergents are emerging as the market's fastest-growing segment, with projections of a 5.95% CAGR over the forecast period. These eco-friendly products stand out with their use of plant-based surfactants, biodegradable builders, and allergen-free fragrances, catering to health-conscious and environmentally aware consumers. Notably, younger consumers are increasingly willing to pay a premium, provided the cleaning performance rivals that of conventional products. Retailers are boosting the visibility of eco-certified brands, aligning with Scope 3 emissions reduction goals, sometimes sidelining slower-moving legacy powder SKUs. Certification schemes like EU Ecolabel and Safer Choice guide consumers toward products that minimize aquatic toxicity and carbon intensity, bolstering their trustworthiness. While green variants may not surpass mainstream synthetic products soon, their market share is poised for a steady ascent as sustainability becomes a more significant factor in purchasing decisions.

By Distribution Channel: Digital Disruption Accelerates

In 2025, supermarkets and hypermarkets dominated the laundry care market, accounting for 56.90% of total sales. Their dominance is bolstered by strong shopper loyalty, driven by frequent promotions, bulk-buy incentives, and strategic cross-aisle merchandising that pairs detergents with related household items. Shoppers favor these channels for their one-stop shopping experience, where competitive pricing meets convenience and a diverse product range. For instance, placing laundry fragrances near cleaning products boosts impulse buys and encourages trials of complementary items. Established supplier relationships and consistent inventory levels guarantee product availability, reinforcing shopper trust. Despite the rise of digital sales, the tactile shopping experience and instant product possession at supermarkets and hypermarkets solidify their market leadership.

Online retail is emerging as the fastest-growing channel in the laundry care market, with projections indicating a CAGR of 5.55% in the coming years. This surge is largely attributed to subscription services, which ensure households remain stocked with essential detergents. Online marketplaces harness algorithms to spotlight top-rated products, suggest refills based on previous purchases, and guide buyers towards digital replenishment, moving them away from traditional in-store impulse buys. The vast online assortment allows niche offerings, like eco-friendly and fragrance-specific variants, to stand shoulder-to-shoulder with mass-market brands. Moreover, supply-chain analytics facilitate quicker deliveries from strategically located warehouses, often matching or beating the time of a typical store visit. As consumers prioritize time savings, personalized suggestions, and product diversity, online channels are poised to steadily increase their market share at the expense of traditional retail formats.

Geography Analysis

In 2025, Asia-Pacific commanded a dominant 36.30% share of the laundry detergent market, buoyed by a burgeoning middle class, rising appliance ownership, and robust local manufacturing. China's push for energy-efficient washers has catapulted advanced concentrated liquids into the spotlight, as consumers increasingly prioritize performance and sustainability. In India, a penchant for sachets drives impressive unit volumes, even with modest per-capita spending, as these small, affordable packs cater to cost-sensitive consumers in both urban and rural areas. Meanwhile, Japan and South Korea, influenced by their compact urban lifestyles, gravitate towards premium pods and fabric conditioners, which offer convenience and cater to space-saving needs in smaller households.

Though smaller in size, the Middle East and Africa corridor is set to outpace others with a projected growth rate of 5.05% CAGR. Members of the Gulf Cooperation Council are channeling investments into modern retail and water-saving appliances, spurring a heightened demand for HE liquids that align with water conservation efforts. In Sub-Saharan Africa, a youthful demographic surge and infrastructure advancements pave the way for sachet adoption among newly urbanized consumers, as these affordable options meet the needs of first-time buyers. However, navigating diverse regulatory landscapes means ensuring localized label adherence and halal certifications in certain regions, which adds complexity for manufacturers aiming to expand their footprint.

North America and Europe, both mature markets, are witnessing a shift towards premium offerings, driven by sustainability mandates and innovations targeting cold-water use and microplastic elimination. Leadership in regulating PFAS and microbeads has spurred early reformulation efforts, setting a precedent for global markets and encouraging brands to invest in eco-friendly alternatives. South America, while seeing mid-single-digit growth, finds its momentum largely in Brazil's organized retail, which benefits from increasing consumer access to branded products. However, the region faces headwinds from exchange-rate fluctuations and import tariffs that sway pricing strategies, creating challenges for manufacturers in maintaining competitive pricing while ensuring profitability.

Regulatory Landscape

Regulation is tightening around ingredient safety, biodegradability, and transparency, which is pushing laundry detergent portfolios toward reformulation and clearer communication. In the European Union, Regulation (EU) 2026/405 was adopted to update the detergents and surfactants framework, replacing Regulation (EC) No 648/2004 and introducing updated safety criteria (including for detergents containing microorganisms), enhanced ingredient disclosure, and harmonized rules covering refill sales, a key route-to-market for concentrated liquids.

In the United States, compliance pressure is reinforced through standards and sector rules affecting formulation and manufacturing. The US EPA updated its Safer Choice and Design for the Environment (DfE) standard in August 2024, strengthening ingredient transparency expectations and restricting certain hazardous substance classes (including PFAS-related criteria for cleaning products). Separately, soap and detergent manufacturing effluent requirements remain governed by EPA effluent guidelines under 40 CFR Part 417, keeping wastewater and discharge controls an operational factor for producers.

Competitive Landscape

The global laundry detergent market features a moderately concentrated competitive landscape, where major players like Procter & Gamble, Unilever, and Henkel compete for market dominance alongside regional competitors and emerging entrants. These top-tier companies harness global research and development investments and diverse marketing channels to fend off challenges from retailer brands and digital newcomers. Their scale advantages are evident in enzyme patents, access to syndicated data, and cost efficiencies in media purchases. The expansion of private labels, highlighted by First Quality Enterprises’ 2025 takeover of Henkel’s North American brands, broadens the market's value spectrum and intensifies pressure on branded pricing. This shift compels established players to innovate and differentiate their offerings to maintain consumer loyalty and market share.

Major players are pivoting towards sustainability, with commitments to 100% recyclable packaging and carbon-neutral factories. These initiatives align with growing consumer demand for environmentally friendly products and stricter regulatory requirements. The digital realm is another battleground; established firms are snapping up direct-to-consumer startups to bolster their expertise and subscription models, enabling them to build stronger customer relationships and streamline supply chains. Meanwhile, regional players are carving out niches with unique fragrances, halal or vegan certifications, and strategic pricing, catering to localized consumer preferences and underserved segments.

Emerging opportunities lie in enzyme-rich cold-water concentrates, microplastic-free fragrance solutions, and IoT-driven commercial dosing systems. These innovations address evolving consumer needs for convenience, sustainability, and enhanced performance. Collaborations, like that of Unilever and Samsung, merge detergent formulation with appliance technology, ensuring optimized cleaning cycles and fostering brand loyalty. Such partnerships also create integrated ecosystems that lock in consumers to specific brands. Companies that don't prioritize performance, sustainability, and cost-efficiency risk being sidelined to generic shelf spaces, losing relevance in an increasingly competitive market.

Laundry Detergents Industry Leaders

-

The Procter & Gamble Company

-

Reckitt Benckiser Group Plc

-

Unilever PLC

-

Kao Corporation

-

Henkel AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory modernization and packaging waste reduction are widening opportunities for compliant concentrates, refills, and next-generation formats that reduce water and plastic intensity. The EU move to Regulation (EU) 2026/405 (in force from March 2026) raises the bar for ingredient disclosure and aligns refill sales requirements, supporting investment in concentrated liquids, monomaterial packs, and controlled-dose systems where documentation and traceability can be standardized across SKUs.

Supply security and performance differentiation are also creating room in both ingredients and localized manufacturing capacity. Examples from 2026 include Nouryon launching a 100% biobased and biodegradable carboxymethylcellulose (CMC) for laundry detergents, and capacity additions such as Unilever inaugurating an OMO Liquid production line in Jeddah, Hayat Kimya commissioning a new detergent facility in Mersin, and First Quality announcing a USD 300 million renovation to manufacture laundry and dishwashing detergents in Ohio. Upstream integration initiatives like Dangote announcing a 400,000-tonne-per-year LAB feedstock plant in Nigeria also point to efforts to reduce reliance on imported inputs and stabilize the cost base tied to LAB-heavy formulations.

Recent Industry Developments

- July 2026: Henkel relaunched the Purex laundry detergent brand with concentrated liquid formulas, updated scents, and packaging incorporating 50% recycled plastic. The relaunch tracks the market shift toward compact formats and packaging sustainability requirements, while refreshing a mass brand to defend shelf space against private label and premium concentrates.

- May 2026: Reckitt agreed to sell a 70% stake in its Essential Home business, which includes laundry-related brands such as Woolite, to Advent International for up to USD 4.8 billion. The deal reshapes competitive dynamics by transferring brands and capabilities to a new owner with scope to reinvest in renovation, innovation, and route-to-market execution.

- April 2026: Unilever launched Persil Smart Series and Comfort Smart Series products engineered for auto-dose washing machines in partnership with Samsung. The release connects detergent chemistry to appliance hardware settings, supporting premiumization through performance claims that are harder to replicate with standard formulas.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The laundry detergents market is defined as the sales value of products used to wash clothes and remove stains in household and institutional laundry, across major retail and business channels, and counted at the point of sale into the market.

Scope exclusions: This sizing excludes laundry appliances, dry-cleaning services, and home-made cleaning mixes that are not sold as packaged laundry detergent products.

Segmentation Overview

-

By Product Type

- Detergent Powder

- Laundry Liquid

- Fabric Softener

- Other Product Types

-

by Packaging

- PET Bottles

- Sachets/Pouches

- Others

-

By Category

- Conventional/Sythetic

- Organic/Natural

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by framing the demand pool and the supply chain boundaries using public references that can be checked, and then translating them into usable model inputs. We typically lean on sources such as UN Comtrade for trade flows, the World Bank and IMF for macro indicators, the US EPA for ingredient-related rules, and the European Chemicals Agency for chemical and labeling context.

To make assumptions less subjective, we also review company annual reports, investor presentations, and press releases to understand mix shifts like liquid versus powder, compact formulations, and pack size changes. In a few places, paid subscriptions for company financials and intelligence, patent databases, and shipment-level import/export records are used to cross-check exposure by geography and to verify whether a new claim or technology is scaling. The sources mentioned here are illustrative and not exhaustive, since many other public documents and data series are used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the model structure and to fill gaps that desk sources do not answer well, such as realistic price ladders by format, private label behavior, and channel margins in key countries. We speak with detergent manufacturers, raw material and packaging participants, large retailers and distributors, and a few institutional laundry buyers. Coverage is balanced across APAC, EMEA, and the Americas so regional mix does not get over-assumed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 17% | APAC: 48% |

| Mid tier: 55% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 20% | Managers: 50% | Americas: 18% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where household and institutional laundry demand is reconstructed using population and household counts, washing frequency, washing machine penetration, and an average dosage per wash that varies by format. That demand pool is then converted to value using observed price ranges by form and pack size, followed by adjustments for channel mix and the split between conventional and natural offerings.

To keep results realistic, totals are corroborated using selective bottom-up approximations, such as supplier and distributor roll-ups in sampled countries, plus quick checks of volume trends against trade signals for key surfactants and builder chemicals where applicable. When smaller markets have thin public data, gaps are handled through regional analogs with similar income bands and washing habits, then corrected after interviews confirm whether dosage and price assumptions are off.

For forecasting, we use scenario analysis anchored to a simple multivariate regression, where price inflation, per-capita consumption, and urbanization act as the main drivers. We then apply interview-based guardrails for promotions and downtrading patterns. If the model implies an abrupt shift in liquid or pod share, it is reviewed again so mix changes remain gradual and explainable year to year.

Data Validation & Update Cycle

Validation is done in layers so the final number is not decided by a single data series. We compare outputs against independent signals such as category growth reported in filings, macro consumption trends, and whether implied per-wash cost is moving in a believable way across regions.

When a country or region shows an unusual jump, the assumptions behind price, dosage, and channel mix are re-checked, and follow-up calls are triggered if the variance cannot be explained with public facts. Before publication, the model goes through multi-step analyst reviews with documented edits, and the full report is refreshed annually with interim updates when material events occur, such as sharp input cost moves, regulatory shifts on ingredients, or trade disruption.

Mordor Intelligence's Laundry Detergents Market Size Versus Other Published Estimates

It is normal to see different market sizes for laundry detergents, even when everyone is talking about the same end use, because the boundary and the counting logic can shift quietly. The biggest differences usually come from what is treated as laundry detergent versus adjacent laundry care items, how retail and institutional demand is blended, and which year and currency timing is used.

By tracking pack-level format mix and checking scope rules across liquids, powders, and fabric softeners, Mordor Intelligence keeps the total tied to an explicit laundry wash demand pool rather than a broader household care basket. Some estimates also lean on a single base year with an assumed price curve, while others refresh pricing and dosage less often, which can overstate value when promotions and concentration changes are common.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 107.52 M (2026) | |

| Global Consultancy A | USD 90.33 B (2024) | Uses a much broader global revenue pool and a different base year, and the scope appears closer to laundry care reporting where adjacent categories and retail value measurement choices can expand totals. |

| Industry Research Group B | USD 76.71 B (2025) | Anchors sizing on a separate base year and relies more on reported trade and price trend constructs, which can shift results if dosage, concentration, and promotion intensity are not re-validated frequently by region. |

The spread in the table is mainly explained by scope boundaries and base-year alignment, and not only by growth expectations. When definitions stay tight and inputs like dosage, format mix, and pricing are refreshed and rechecked through interviews, the resulting market size is easier to trace back to clear steps and to update without rewriting the whole model.

Key Questions Answered in the Report

How big is the Laundry Detergents Market?

The Laundry Detergents Market size is expected to reach USD 107.52 million in 2026 and grow at a CAGR of 4.56% to reach USD 134.42 million by 2031.

How large will global demand be by 2031?

Global demand is projected to reach USD 134.42 million by 2031, expanding at a 4.56% CAGR.

Which region contributes the highest revenue today?

Asia-Pacific generates the largest share at 36.30% of 2025 sales thanks to rising appliance ownership and population scale.

Which product format is growing fastest?

Middle East and Africa is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Laundry Detergents Market?

Fabric softeners are forecast to advance at a 6.45% CAGR through 2031 as consumers seek premium fabric care benefits.

What packaging innovation shows the strongest growth?

PET bottles are set for a 5.12% CAGR because refill programs and premium positioning resonate with urban shoppers.

Page last updated on: