Abdominal Pads Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.19 Billion |

| Market Size (2030) | USD 1.62 Billion |

| Growth Rate (2025 - 2030) | 6.41% CAGR |

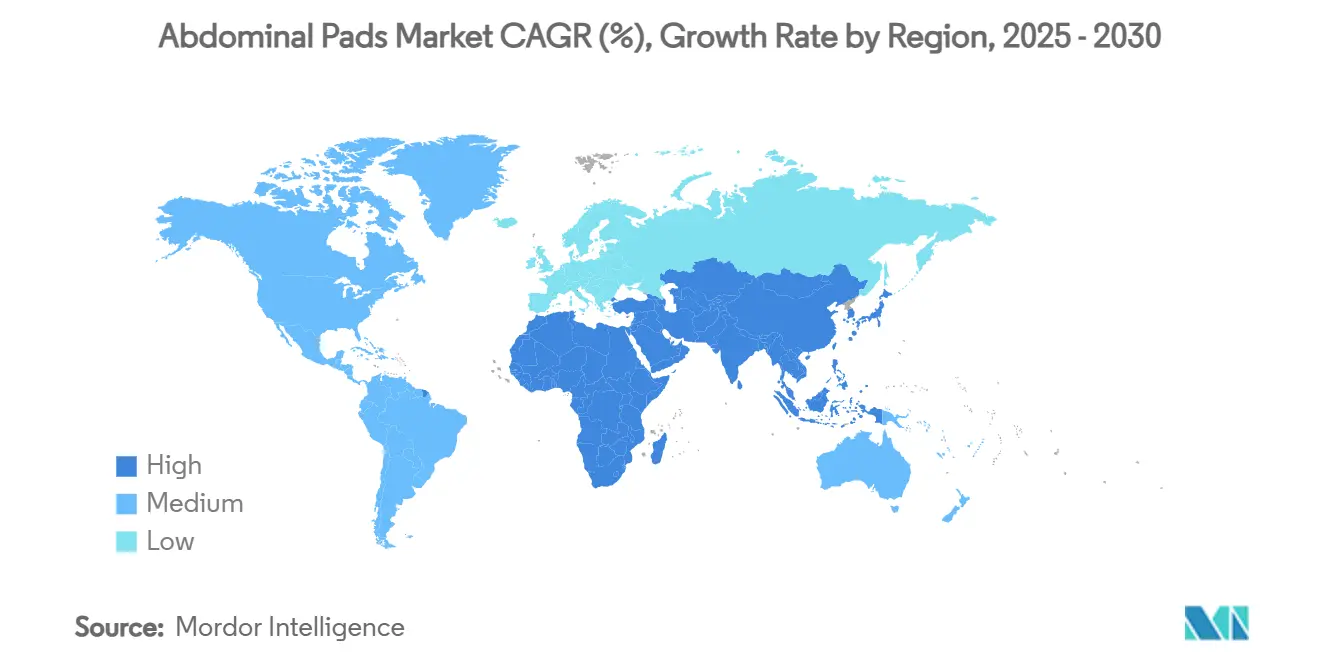

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

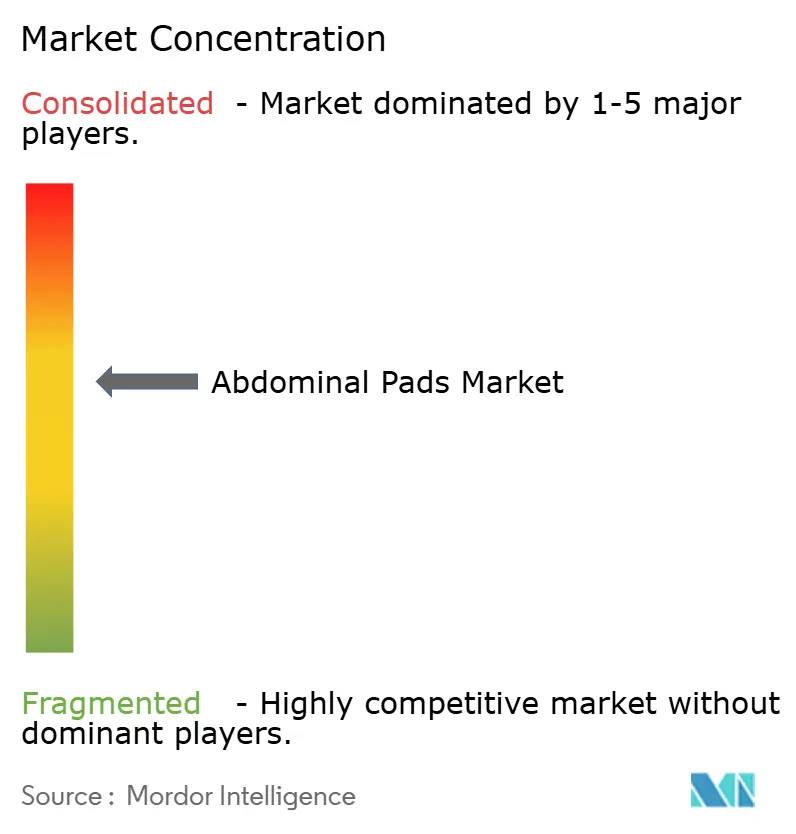

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Abdominal Pads Market Analysis by Mordor Intelligence

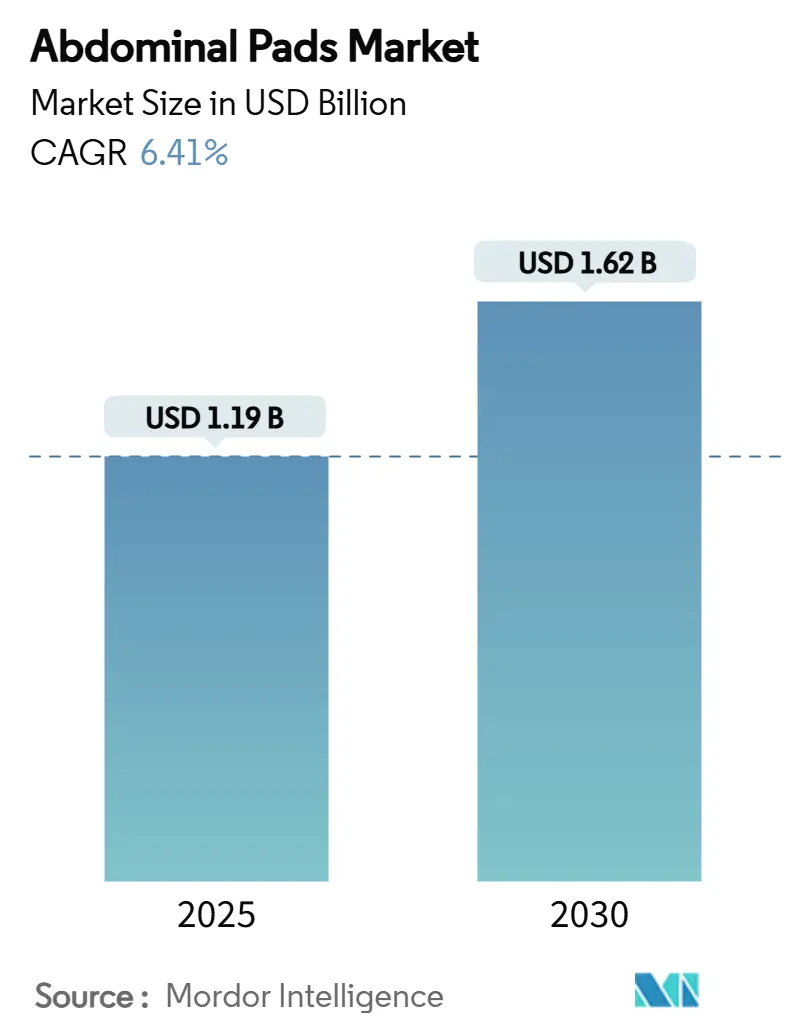

The abdominal pads market size stood at USD 1.19 billion in 2025 and is projected to rise to USD 1.62 billion by 2030, translating to a 6.41% CAGR over the forecast period. Robust demand stems from a confluence of rising surgical procedures, a growing chronic-wound population, and rapid uptake of outpatient care models, all of which heighten consumption of high-absorption dressings. The ambulatory shift now covers 57.8% of hospital-based surgeries, reinforcing requirements for single-use pads able to manage drainage for 24–48 hours. At the same time, stringent FDA Quality Management System Regulation amendments effective February 2026 align domestic manufacturing with ISO 13485, driving both cost and reliability benefits. Material innovation around super-absorbent polymers, coupled with hospital infection-control mandates, is lifting adoption of premium pads, while supply-chain fragility in medical-grade cotton keeps procurement risk on corporate agendas.

Key Report Takeaways

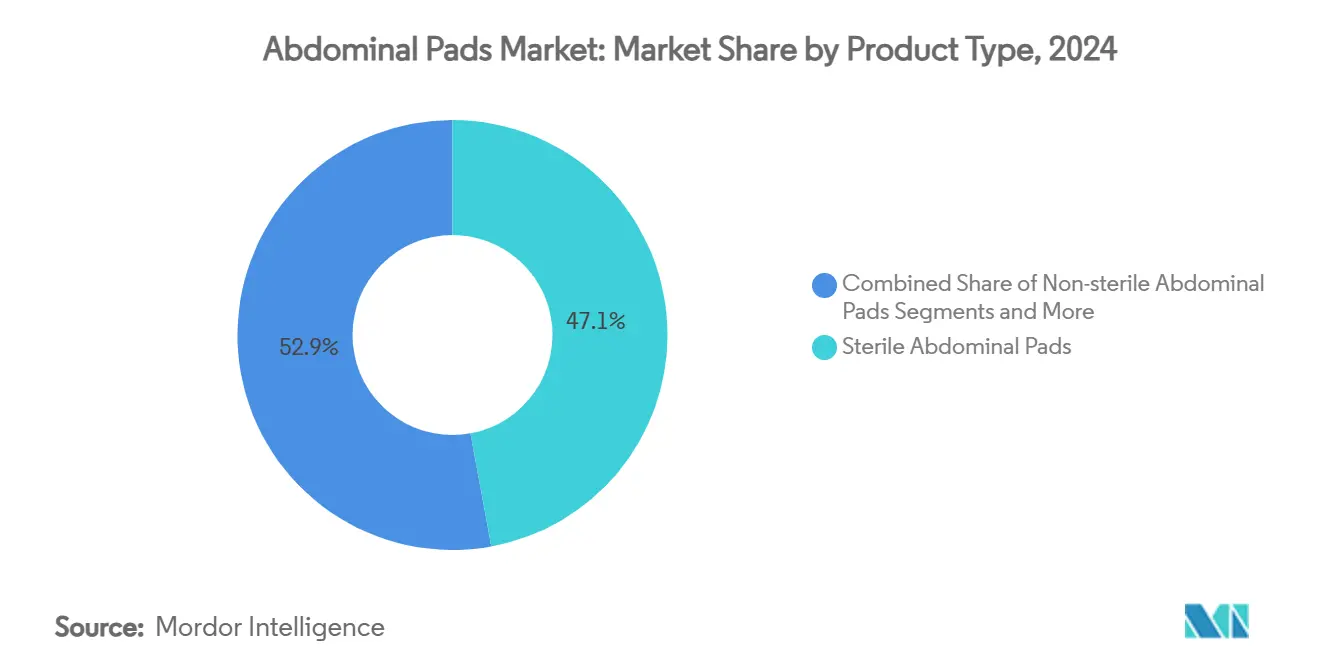

- By product type, sterile variants held 47.12% of abdominal pads market share in 2024, whereas super-absorbent pads are expected to accelerate at a 9.83% CAGR through 2030.

- By material, cotton commanded 52.34% share of the abdominal pads market size in 2024, yet non-woven polypropylene is tracking a 10.37% CAGR to 2030.

- By application, surgical wounds accounted for a 39.68% share of the abdominal pads market size in 2024, while chronic ulcers are forecast to witness a 9.54% CAGR over the same horizon.

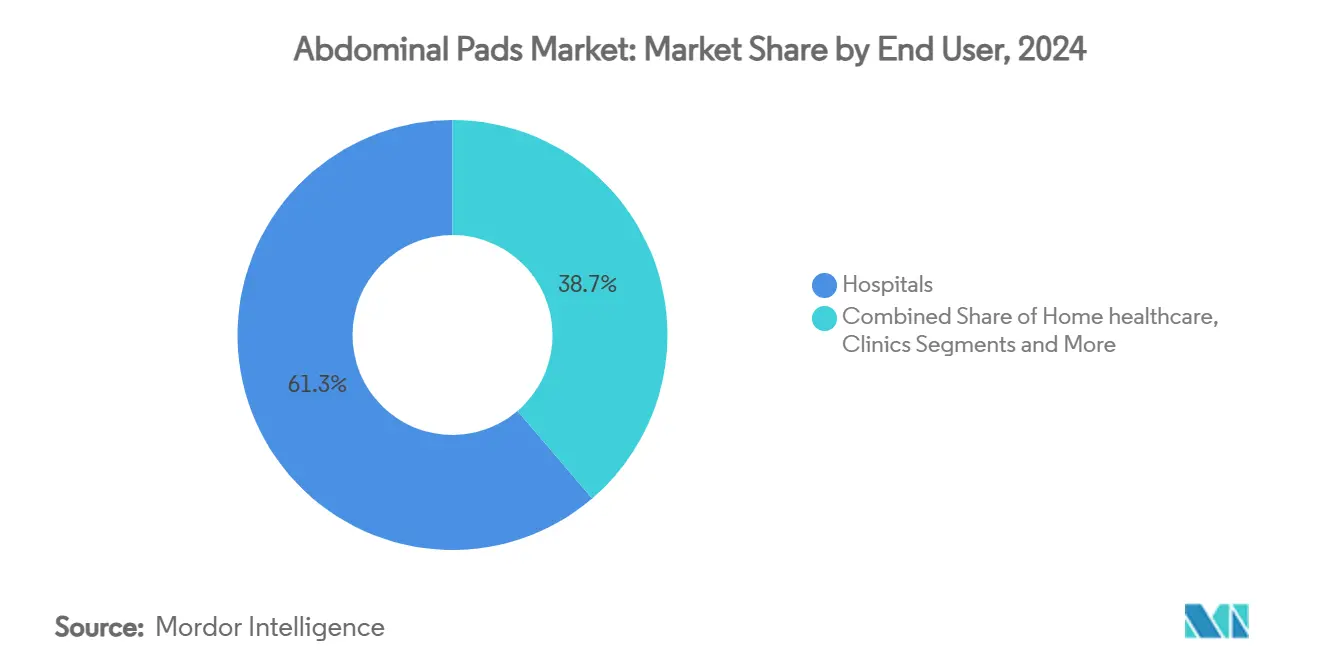

- By end user, hospitals captured 61.26% of the abdominal pads market size in 2024; home healthcare is projected to expand at an 8.33% CAGR to 2030.

- By distribution channel, direct tenders led with 56.77% of the abdominal pads market size in 2024, whereas online pharmacies are advancing at a 10.78% CAGR through 2030.

- By geography, North America secured 36.42% of abdominal pads market share in 2024, and Asia-Pacific is poised for the fastest 8.44% CAGR to 2030.

Global Abdominal Pads Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volume | +1.8% | North America, Europe, global spillover | Medium term (2-4 years) |

| Growing prevalence of chronic wounds | +1.5% | APAC, North America, global | Long term (≥ 4 years) |

| Increasing incidence of trauma & accidents | +0.9% | Primarily APAC, emerging markets | Short term (≤ 2 years) |

| Rapid outpatient shift to single-use XL ABD pads | +1.2% | North America, EU, APAC | Medium term (2-4 years) |

| Adoption of super-absorbent polymer infused pads | +0.7% | Developed markets, global reach | Long term (≥ 4 years) |

| Hospital infection-control mandates in emerging markets | +0.6% | APAC, MEA, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volume

Surgical caseload expansion remains the strongest catalyst for the abdominal pads market. Acute-care surgery patients make up 20% of inpatient admissions yet absorb 25% of total inpatient costs, equating to USD 85.8 billion every year in the United States.[1]Lisa M. Knowlton et al., “The Economic Footprint of Acute Care Surgery in the United States: Implications for Systems Development,” Journal of Trauma and Acute Care Surgery, journals.lww.com Ambulatory centers now complete most hospital-based surgeries, elevating demand for XL single-use dressings that sustain drainage control beyond the procedure window. Same-day discharge pathways require pads that hold fluid for up to two days without assistance, thereby widening the addressable base for advanced absorbent products. Minimally invasive techniques, although reducing incision size, still mandate dependable post-op dressing protocols. Collectively, these factors add 1.8 percentage points to forecast CAGR.

Growing Prevalence of Chronic Wounds

Chronic wounds already burden 10.5 million U.S. Medicare beneficiaries, equal to 2.5% of the population. Care delivery is migrating from outpatient departments to physician offices and home settings, prompting need for pads with prolonged wear, antimicrobial attributes, and caregiver-friendly designs. Chronic ulcers remain the fastest-expanding application at 9.54% CAGR through 2030, riding demographic aging, diabetes, and obesity trends. Economic repercussions include prolonged disability and productivity loss, pushing payers toward preventive wound-care allocations. Home-care models intensify the requirement for intuitive application and easy replacement indicators.[2]Hua Luo et al., “Prospects for the Application of Home Care in Chronic Wound Management,” Journal of Family Medicine and Primary Care, pubmed.ncbi.nlm.nih.gov Ongoing demand keeps upward pressure on unit volumes despite moderating price points.

Increasing Incidence of Trauma & Accidents

Falls contribute 40.51% and road collisions 25.22% of trauma hospitalizations in leading healthcare economies. Emergency departments rely on abdominal pads capable of rapid fluid uptake and hemostasis during critical stabilization windows. The annual economic drag exceeds USD 100 billion, magnifying the need for reliable dressings to support early mobilization and reduce length-of-stay. Composite and gel-forming technologies are gaining favor because they maintain integrity during transport. Incidence concentration in urban hubs enables manufacturers to streamline distribution to trauma centers.

Rapid Outpatient Shift to Single-Use XL ABD Pads

Ambulatory facilities conduct 57.8% of all hospital-based surgeries, reinforcing the move toward high-capacity, extended-wear pads. Outpatient economics prioritize reduced facility overheads and faster bed turnover, rewarding dressings that can stay in place without nursing oversight. Enhanced SAP layers and leak-proof backings are now baseline specifications. The updated FDA quality rule underpins premium pricing by codifying safety and performance benchmarks.[3]Federal Register, “Medical Devices; Quality System Regulation Amendments,” federalregister.gov Outpatient momentum adds a meaningful 1.2 percentage points to expected CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of advanced wound dressings (foams, alginates) | -0.8% | Developed markets, global | Medium term (2-4 years) |

| Pricing pressure from group-purchasing organizations | -0.6% | North America, EU | Short term (≤ 2 years) |

| Supply-chain dependence on medical-grade cotton imports | -0.5% | Emerging markets, global | Short term (≤ 2 years) |

| Environmental scrutiny of single-use cotton disposables | -0.4% | EU, developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Advanced Wound Dressings (Foams, Alginates)

Foam, alginate, and smart hydrogel dressings deliver faster healing for specialty wounds, taking share from traditional pads. Smith+Nephew’s advanced wound division posted 3.8% underlying growth in Q1 2025, buoyed by negative-pressure and novel foam launches. UK health authorities now endorse the PICO single-use negative-pressure system as a superior alternative to standard dressings. Reimbursement frameworks increasingly favor evidence-based dressings, limiting volume upside for commodity pads. Manufacturers respond by adding antimicrobial coatings and moisture-management layers, yet higher costs erode price competitiveness.

Pricing Pressure from Group-Purchasing Organizations

GPO consolidation gives hospitals formidable leverage to demand double-digit unit discounts, compressing margins by up to 25%. Competitive bidding favors the lowest-priced compliant offer, discouraging differentiation. Supply tightness in cotton and synthetic yarns leaves producers absorbing cost inflation rather than passing it through. Smaller firms find it difficult to sustain R&D budgets under continuous price erosion, dampening innovation velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sterile Leadership Drives Innovation

Sterile pads accounted for 47.12% of 2024 revenue, confirming infection-control protocols as the foremost purchasing criterion. Super-absorbent alternatives, however, are lifting the abdominal pads market size through a forecast 9.83% CAGR thanks to longer wear times and lower change frequency. Non-sterile pads remain popular in home-care settings where sterility is less critical, but clinical guidelines increasingly blur this traditional split. Surgical teams prize x-ray-detectable versions as a patient-safety back-stop, even though the added feature raises unit price. Manufacturers are integrating SAP layers that offer 10-fold water uptake, reinforcing value propositions. Successful new products emphasize breathability, low lint, and secure edging that prevents fiber shed. Strong demand across ambulatory centers keeps sterile pad volumes high, yet differentiation is shifting toward super-absorbent composites with visual change indicators.

Continued regulatory alignment under the FDA Quality Management System Regulation should lift baseline performance standards, advantaging firms with advanced sterilization infrastructure. Coupling this compliance with SAP cores allows vendors to command premium hospital formulary placement. The abdominal pads market sees an ongoing migration from commodity sterile gauze to performance-enhanced sterile offerings positioned as cost-effective over an episode of care. Super-absorbent pads also fit outpatient protocols, where a single dressing must manage drainage until the follow-up visit. This dual momentum cements product-type diversification as a major revenue lever through 2030.

By Material: Cotton Dominance Confronts Synthetic Momentum

Cotton retained 52.34% revenue in 2024 on the strength of familiarity and low cost, yet synthetic non-woven polypropylene is staging a 10.37% CAGR challenge. Poly-based layers deliver superior fluid wicking and lower strike-through, extending in-use intervals, which resonates with outpatient discharge protocols. Nonetheless, cotton’s abundant global supply and biodegradability sustain its institutional appeal. Rayon and blended fabrics seek to bridge performance and eco goals, but they incur higher processing expenses and complex quality controls. Hospitals sensitive to supply-chain shocks are adopting dual-sourcing-material strategies to hedge cotton availability risk.

Polypropylene’s hydrophobic surface functions in tandem with SAP granules to trap exudate while keeping the wound bed optimally moist. Yet, single-use polypropylene faces environmental pushback, particularly in the European Union, motivating R&D into bio-based polymers. The abdominal pads market must balance clinical efficacy, sustainability mandates, and cost constraints as it navigates material substitution. Over the forecast horizon, a gradual mix shift is likely with cotton holding plural-majority share but synthetic layers closing the gap as price-performance ratios keep improving.

By Application: Surgical Wounds Lead, Chronic Ulcers Accelerate

Surgical wounds generated 39.68% of 2024 turnover, underscoring their role as the cornerstone for demand forecasting. Post-operative drainage management protocols specify pad changes at set intervals, creating predictable volume pull. Meanwhile, chronic ulcers are set to grow at 9.54% CAGR on the back of a rapidly aging population and the diabetes epidemic. Trauma and accident cases form a smaller yet immediate-need slice, keen on pads that absorb swiftly and resist linting. Post-operative dressing usage overlaps with surgical wounds but extends into longer rehabilitation timelines, widening tonal product requirements.

The abdominal pads market benefits from overlapping use cases, enabling large-scale manufacturing runs that spread fixed costs across multiple indications. Chronic-wound expansion heightens focus on antimicrobial barriers that reduce infection risk during long wear. Surgical volumes, especially within ambulatory facilities, remain the stable bedrock for baseline demand. Overall, multi-application versatility underpins steady order flow for distributors and wholesalers.

By End User: Hospitals Retain Commanding Share, Home Care Gains Pace

Hospitals absorbed 61.26% of global purchases in 2024, helped by bundled procurement contracts and high surgical throughput. Ambulatory surgical centers are a fast-growing sub-segment, reflecting the shift toward same-day discharge. Home-care environments, expanding at 8.33% CAGR, increasingly rely on easy-to-apply dressings with clear change indicators. Clinics round out demand by servicing chronic-wound follow-ups and minor injury treatments.

For suppliers, hospital formularies remain critical gateways, but differentiation is now essential to withstand GPO price pressure. In contrast, home-care channels reward convenience features and patient education. The abdominal pads market continues to recalibrate product portfolios, packaging sizes, and distribution strategies to cater to divergent end-user needs.

By Distribution Channel: Direct Tenders Dominate, E-commerce Emerges

Direct tender contracts represented 56.77% of 2024 revenue, mirroring institutional buyers’ preference for bulk purchasing. Wholesalers and retail pharmacies ensure availability for smaller facilities and individual consumers, though growth is flatter. Online pharmacies stand out with a 10.78% CAGR, buoyed by pandemic-era habits and younger caregiver demographics comfortable with digital ordering.

Tender negotiations stress ISO-certified production and on-time delivery. E-commerce success hinges on intuitive product information, discreet packaging, and reliable last-mile logistics. The abdominal pads market is witnessing increased manufacturer engagement in omni-channel distribution to minimize reliance on any single route while capturing incremental volumes from digitally savvy buyers.

Geography Analysis

North America, responsible for 36.42% of 2024 revenue, combines high procedure volumes, robust insurance coverage, and quick adoption of premium dressings. The United States dominates regional sales, supported by well-established outpatient networks and reimbursement pathways that value advanced wound-care outcomes. Canada and Mexico add incremental growth as healthcare investment rises and elective surgery backlogs clear. Hospitals standardize on SAP-enhanced sterile pads to obey infection-control metrics, feeding sustained order quantities.

Europe displays a mature yet innovation-friendly profile. Strict regulatory oversight favors quality over low price, giving an edge to ISO-compliant vendors. Environmental directives begin to influence material selection, nudging hospitals toward biodegradable options. Growth remains modest but stable, with large public tenders ensuring volume consistency. Nordic countries actively pilot sustainable pad recycling programs, setting precedents likely to be adopted across the continent.

Asia-Pacific is forecast to generate the fastest 8.44% CAGR as demographic aging, urbanization, and universal-health-coverage rollouts improve access to surgical and chronic-wound care. China, India, Japan, South Korea, and Australia serve as core demand engines, each showing distinct reimbursement and procurement pathways. Governments channel funds into infection-control initiatives, benefiting sterile and super-absorbent pads. Rising trauma incidence in densely populated cities further adds to emergency-department consumption. South America and the Middle East & Africa continue to build baseline capacity, yet political and exchange-rate volatility limit near-term acceleration. Across all regions, supply-chain resilience and regulatory compliance shape competitive positioning within the abdominal pads market.

Competitive Landscape

The abdominal pads industry is moderately fragmented, with a blend of multinational conglomerates and agile innovators. Solventum, Cardinal Health, Medline Industries, and Smith+Nephew leverage regulatory expertise and economies of scale to reinforce incumbent advantage. New entrants specialize in eco-friendly materials, smart-sensor integration, and SAP advances, aiming to differentiate beyond price. FDA harmonization with ISO 13485 raises the compliance bar, favoring players that already operate mature quality-management systems.

Strategic activity centers on product upgrades and capacity expansion. Solventum’s V.A.C. Peel and Place Dressing trims application time by 61% and lowers costs by 41%, validating the pivot toward extended-wear solutions. Johnson & Johnson MedTech launched a recycling program for single-use devices, offering hospitals sustainability metrics that aid tender bids. Hollister’s additional EUR 25 million investment in Lithuania underlines the trend toward localized manufacturing to mitigate geopolitical risk.

Partnerships are proliferating between raw-material suppliers and converters to assure cotton and SAP supply security. Digital engagement platforms now provide hospitals with consumption dashboards, enabling vendors to propose outcome-based contracts. Competitive intensity is expected to rise as advanced dressings encroach on traditional pad territory, pressuring manufacturers to innovate while maintaining cost discipline. Nonetheless, the abdominal pads market remains sufficiently large for niche players focusing on specialized clinical indications or regional distribution strengths.

Abdominal Pads Industry Leaders

Solventum

Cardinal Health

Medline Industries

Dynarex Corporation

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Johnson & Johnson MedTech introduced a nationwide recycling initiative in the United Kingdom covering its single-use portfolios, converting recovered plastics into construction materials.

- January 2025: Hollister expanded its Lithuanian operations by opening a new product-development center aimed at medical devices, with plans to add more than 100 specialists during 2025.

Global Abdominal Pads Market Report Scope

| Sterile abdominal pads |

| Non-sterile abdominal pads |

| X-ray detectable abdominal pads |

| Super-absorbent abdominal pads |

| Cotton |

| Rayon |

| Non-woven polypropylene |

| Blended fabrics |

| Surgical wounds |

| Traumatic wounds |

| Chronic ulcers |

| Post-operative dressing |

| Other applications |

| Hospitals |

| Ambulatory surgical centers |

| Home healthcare |

| Clinics |

| Direct tenders |

| Retail pharmacies |

| Online pharmacies |

| Wholesalers & distributors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Sterile abdominal pads | |

| Non-sterile abdominal pads | ||

| X-ray detectable abdominal pads | ||

| Super-absorbent abdominal pads | ||

| By Material | Cotton | |

| Rayon | ||

| Non-woven polypropylene | ||

| Blended fabrics | ||

| By Application | Surgical wounds | |

| Traumatic wounds | ||

| Chronic ulcers | ||

| Post-operative dressing | ||

| Other applications | ||

| By End User | Hospitals | |

| Ambulatory surgical centers | ||

| Home healthcare | ||

| Clinics | ||

| By Distribution Channel | Direct tenders | |

| Retail pharmacies | ||

| Online pharmacies | ||

| Wholesalers & distributors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the abdominal pads market?

The abdominal pads market size reached USD 1.19 billion in 2025.

How fast is the abdominal pads market expected to grow?

Revenue is forecast to expand at a 6.41% CAGR from 2025 to 2030, reaching USD 1.62 billion.

Which product segment is expanding the quickest?

Super-absorbent abdominal pads are projected to post a 9.83% CAGR through 2030.

Why are outpatient surgery trends important for demand?

Ambulatory centers now perform 57.8% of hospital-based surgeries, driving need for extended-wear, single-use pads that manage drainage at home.

Which region offers the highest growth potential?

Asia-Pacific is set to achieve an 8.44% CAGR thanks to healthcare modernization and demographic shifts.

How are environmental concerns influencing product design?

Vendors are investing in recyclable and bio-based materials to align with European waste-reduction policies and hospital sustainability targets.

Page last updated on: