Thyroid Cancer Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 260.94 Billion |

| Market Size (2031) | USD 357.01 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

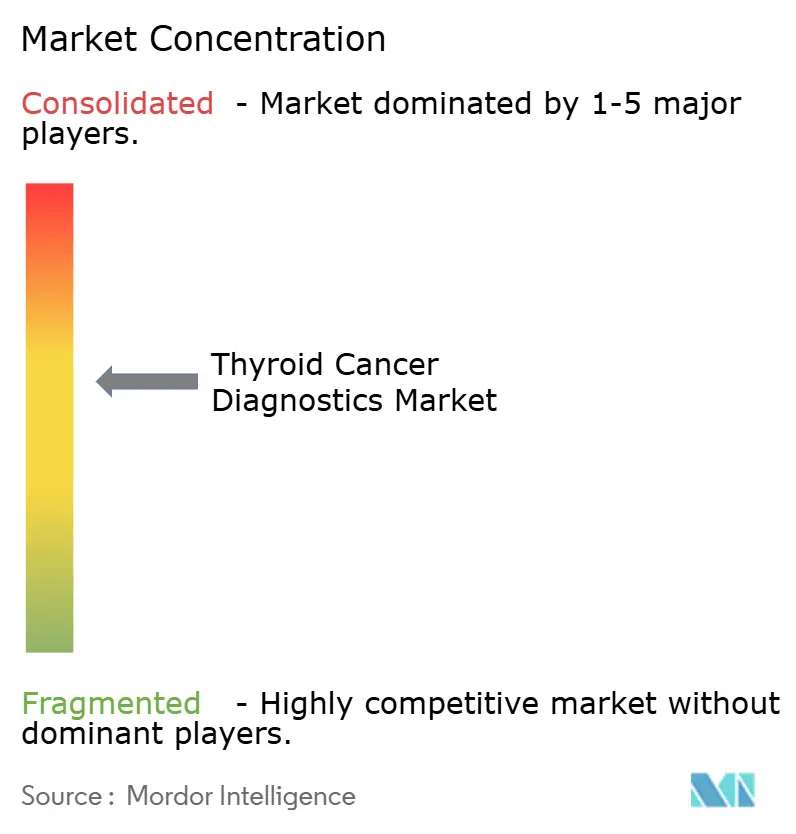

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thyroid Cancer Diagnostics Market Analysis by Mordor Intelligence

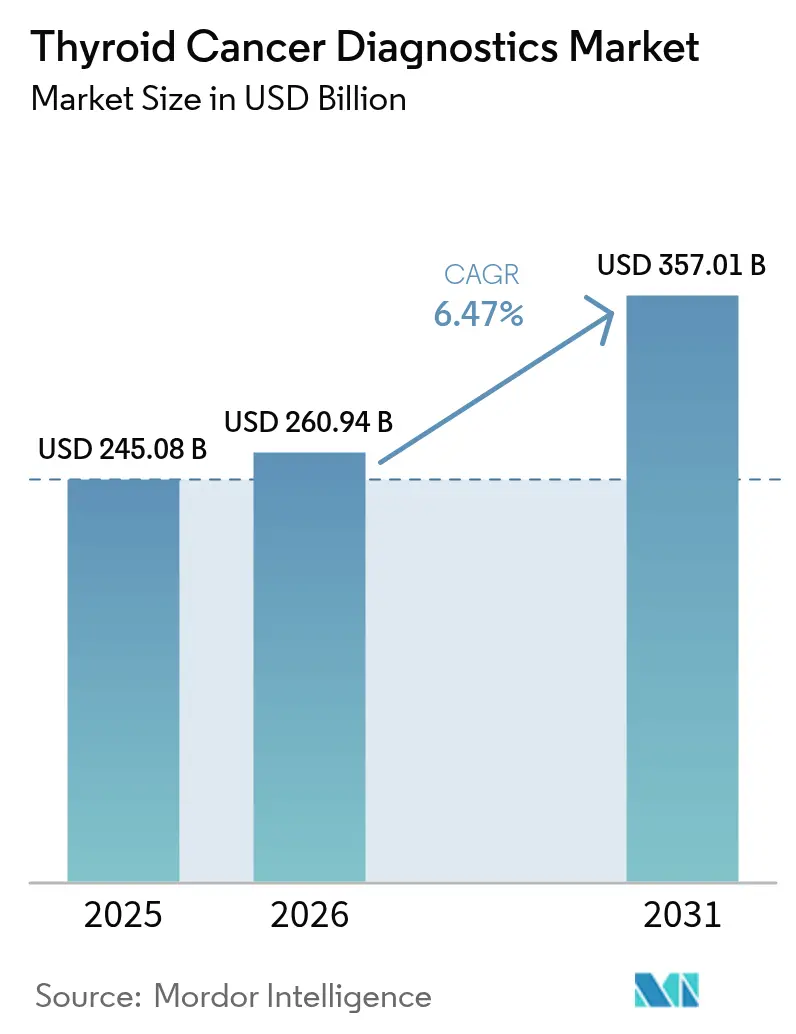

The thyroid cancer diagnostics market size in 2026 is estimated at USD 260.94 billion, growing from 2025 value of USD 245.08 billion with 2031 projections showing USD 357.01 billion, growing at 6.47% CAGR over 2026-2031. Consistent demand for earlier and more accurate detection, widespread availability of next-generation sequencing (NGS) assays, and rapid integration of artificial intelligence (AI) in imaging workflows invigorate the thyroid cancer diagnostics market. Continued gains in reimbursement for molecular panels across the United States, Canada, Germany, Japan and Australia further widen clinical acceptance. Meanwhile, liquid biopsy advances enable non-invasive surveillance, expanding testing volume beyond initial diagnosis. Competitive momentum is fueled by partnerships between imaging vendors and semiconductor companies that deliver real-time decision support, easing the shortage of endocrine cytopathologists. Against this backdrop, regulatory agencies now fast-track companion diagnostics, shortening time-to-market for genomic assays that pair with targeted therapies.

Key Report Takeaways

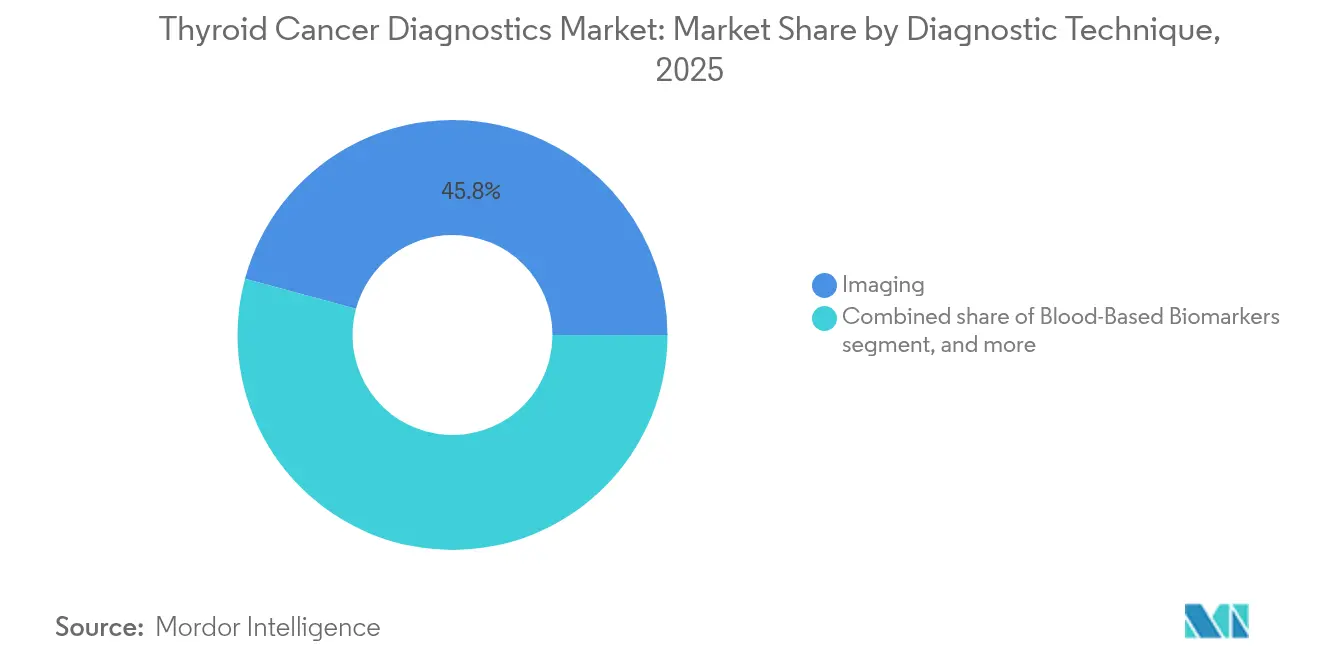

- By diagnostic technique, imaging modalities led with 45.78% revenue share in 2025, while liquid biopsy is poised to accelerate at a 10.10% CAGR through 2031.

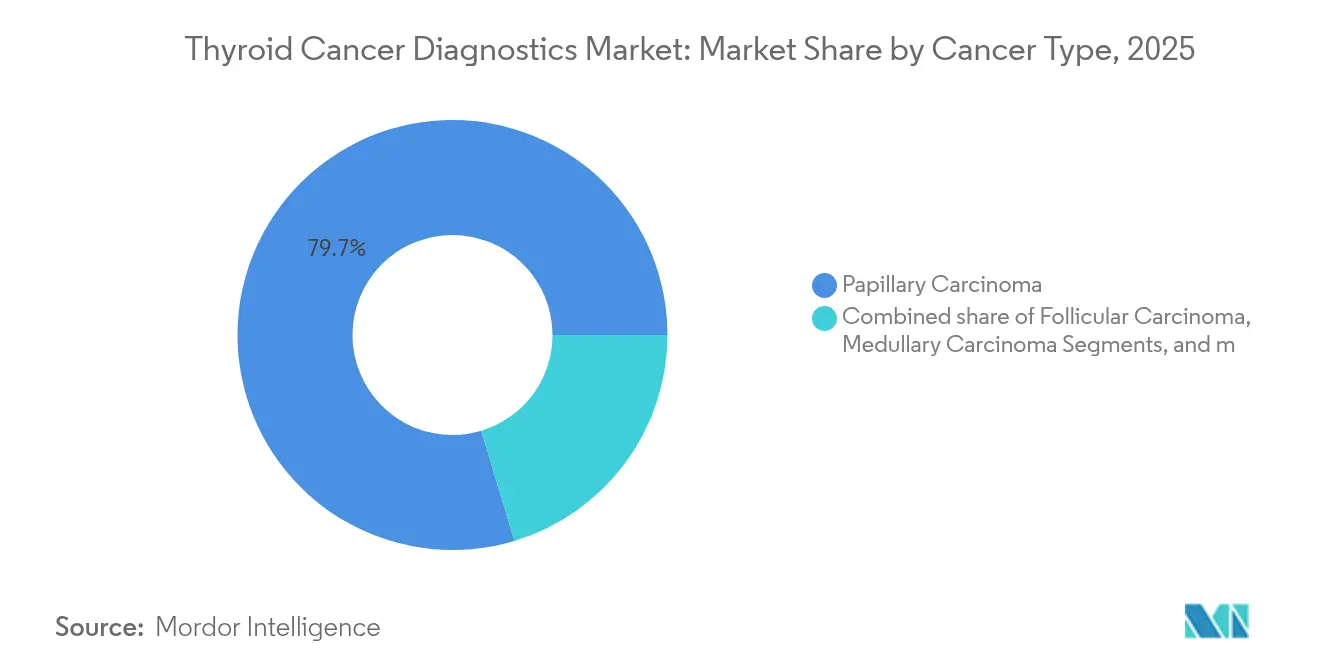

- By cancer type, papillary carcinoma captured 79.65% of thyroid cancer diagnostics market share in 2025; anaplastic carcinoma is projected to record the fastest 7.88% CAGR during 2026-2031.

- By end user, hospital laboratories controlled 53.64% of the thyroid cancer diagnostics market size in 2025, whereas independent reference laboratories are forecast to expand at 9.12% CAGR through 2031.

- By geography, North America held 38.74% of 2025 revenue, while Asia-Pacific is anticipated to advance at a 7.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thyroid Cancer Diagnostics Market Trends and Insights

Driver Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence from improved imaging sensitivity | +1.2% | North America, Europe | Medium term (2-4 years) |

| Government-led thyroid cancer screening & awareness programs | +0.8% | Asia-Pacific, MEA, Latin America | Long term (≥ 4 years) |

| Rapid adoption of NGS-based genomic classifiers | +1.5% | OECD markets, expanding to emerging economies | Short term (≤ 2 years) |

| Expanding reimbursement for molecular tests in OECD markets | +1.1% | North America, EU, selective APAC | Medium term (2-4 years) |

| AI-driven ultrasound triage tools in primary care | +0.9% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Shift toward PET/MRI hybrid restaging protocols | +0.7% | North America & EU, limited penetration in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence from Improved Imaging Sensitivity

AI-enabled ultrasound probes now detect sub-centimeter nodules with 89% accuracy, narrowing the gap between community clinics and tertiary centers[1]International Journal of Surgery, “Deep learning assists ultrasound diagnosis of follicular thyroid carcinoma,” journalsurgery.net. Siemens Healthineers’ Acuson Sequoia platform adds automated organ labeling, cutting scan-to-report time and driving referral rates to endocrine surgeons[2]Siemens Healthineers, “ACUSON Sequoia ultrasound system with AI Abdomen technology,” siemens-healthineers.com. Increased sensitivity boosts biopsy volume, which lifts utilization of genomic classifiers and liquid biopsy tests that follow in the diagnostic cascade. While earlier capture fuels revenue, clinicians remain vigilant about over-diagnosis and overtreatment, spurring adoption of risk-stratification algorithms that flag indolent lesions for active surveillance instead of immediate surgery.

Government-Led Thyroid Cancer Screening & Awareness Programs

National initiatives in China, Japan and South Korea incorporate thyroid palpation and ultrasound into multi-cancer campaigns, standardizing referral pathways and lifting testing adherence. Japan’s Cancer Center publishes granular incidence maps that guide mobile screening vans toward underserved prefectures[3]National Cancer Center Japan, “Cancer statistics 2024,” ncc.go.jp. Mandatory reporting feeds regional cancer registries, creating large datasets that validate AI triage models. Screening regulations typically reference guideline-endorsed molecular panels, putting pressure on local laboratories to acquire NGS workflows. The programs’ long-term funding ensures recurring demand while encouraging manufacturers to localize production for cost efficiencies.

Rapid Adoption of NGS-Based Genomic Classifiers

The FDA-cleared TruSight Oncology Comprehensive kit underscores regulatory confidence in broad genomic profiling for indeterminate nodules. Veracyte processed 15,700 Afirma samples in Q2 2024 after U.S. Medicare extended coverage to Bethesda V nodules. ThyroSeq v3 demonstrated 89.6% sensitivity in Southeast Asian cohorts, signaling cross-ethnic reliability. These assays reduce unnecessary thyroidectomies by 42.0%, saving hospital resources and accelerating pay-for-performance models. AI-assisted variant curation cuts reporting time, allowing laboratories to scale without linear head-count expansion.

Expanding Reimbursement for Molecular Tests in OECD Markets

The U.S. MolDX program codifies payment for genetic classifiers, and European payers adopt similar fee schedules that stabilize laboratory cash flow[4]Centers for Medicare & Medicaid Services, “MolDX: Molecular testing policy for thyroid nodules,” cms.gov. UnitedHealthcare now reimburses ThyroSeq, ThyGenNEXT and ThyraMIR, expanding private-sector backing. FoundationOne Liquid CDx secured multiple companion-diagnostic indications, paving a path for blood-based profiling in thyroid cancer. Broader coverage narrows out-of-pocket costs, prompting community endocrinologists to order molecular panels earlier in the care pathway.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled endocrine cytopathologists | −0.9% | Global, most acute in rural/emerging markets | Long term (≥ 4 years) |

| High out-of-pocket cost for advanced molecular panels | −0.6% | Emerging markets, uninsured populations | Medium term (2-4 years) |

| Guideline pushback on over-diagnosis & active-surveillance preference | −0.4% | North America & EU, limited impact in APAC | Short term (≤ 2 years) |

| Regulatory uncertainty for AI decision-support algorithms | −0.3% | Global, varying regulatory frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Endocrine Cytopathologists

Anatomic pathology vacancy rates rise annually; only 3.0% of U.K. laboratories meet recommended staffing levels. The shortage lengthens biopsy-to-report cycles and delays treatment decisions. Hospitals adopt cloud-based AI slide reviewers from Roche to triage low-risk smears, yet confirmatory reads still need board-certified experts. Training programs expand fellowship seats, but incumbents face retirement cliffs, extending the constraint well into the next decade.

High Out-Of-Pocket Cost for Advanced Molecular Panels

Comprehensive panels cost USD 3,000–5,000 per test, burdening patients without robust insurance. The American Thyroid Association notes that biopsy reimbursement cuts shift fine-needle aspiration toward hospital settings, inflating procedural costs. Liquid biopsy monitoring compounds expenditure because serial draws are recommended for aggressive disease. Manufacturers pilot tiered pricing and subscription models, yet broad affordability remains elusive in lower-income countries, restraining the thyroid cancer diagnostics market in those regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cancer Type: Papillary Carcinoma Volume Sustains Growth

Papillary carcinoma generated the bulk of testing demand, holding 79.65% of the thyroid cancer diagnostics market in 2025. This dominance ensures steady baseline volume for ultrasound, cytology and NGS classifiers. Papillary lesions present favorable outcomes, so clinicians increasingly deploy molecular risk panels to spare low-risk patients from surgery, channeling them to active surveillance instead. Anaplastic carcinoma, despite accounting for less than 2% of incidence, drives a 7.88% CAGR by necessitating broad genomic profiling and liquid biopsy monitoring for rapid therapeutic adjustments. RET-fusion positivity now guides use of selpercatinib, which in turn mandates companion diagnostics at diagnosis and relapse.

The thyroid cancer diagnostics market size for rare subtypes such as medullary and follicular carcinoma is projected to scale steadily on the back of calcitonin assays and core-needle biopsy adoption. Follicular lesions still evade cytology, so ThyroSeq and Afirma uptake is brisk in endocrine clinics. Targeted testing for RET and RAS mutations refines prognostication and follow-up strategies, widening the overall serviceable market. Rising investigator-initiated trials for kinase inhibitors further entrench comprehensive genomic profiling across all histologies, sustaining long-term revenue.

By Diagnostic Technique: Imaging Remains Cornerstone, Liquid Biopsy Gains Pace

Imaging accounted for 45.78% revenue in 2025, underlining ultrasound’s ubiquity as first-line triage. Integration of AI contouring into handheld probes allows primary-care physicians to grade TI-RADS risk levels accurately. PET/MRI hybrid scanners, while costly, produce high-contrast maps that guide re-operations in recurrent disease. As PET tracer availability widens, tertiary centers refine patient selection, minimizing unnecessary explorations.

Liquid biopsy, logging a 10.10% CAGR, is the fastest-rising technique within the thyroid cancer diagnostics market. Guardant Health expands its cfDNA panel to include rearranged during transfection (RET) and BRAF mutations, extending applicability across main subtypes. The thyroid cancer diagnostics market size for liquid biopsy could reach a double-digit share by 2030, driven by oncologists who favor blood-based surveillance over repeated tissue biopsies in surgically altered necks. Meanwhile, conventional fine-needle aspiration endures as a confirmatory test, especially where blood-based tests lack payer coverage. Core-needle biopsy emerges for large nodules that need architectural detail, bridging cytology and histology. Multiplex immunohistochemistry on core tissue complements NGS panels, creating a layered diagnostic workflow.

By End User: Hospital Laboratories Anchor Demand, Reference Labs Outpace in Growth

Hospital laboratories produced 53.64% of market revenue in 2025 given their embedded position in surgical pathways and immediate turnaround requirements. Integrated health-system labs invest in closed-tube NGS sequencers that run barcode-heavy workflows overnight, returning results within 48 hours. Surgical oncologists value in-house cytopathology during intraoperative consultations, a capability less accessible in independent facilities.

Reference laboratories, advancing at 9.12% CAGR, tap multi-hospital contracts, ship-to-lab logistics and economies of scale in reagent procurement. Quest Diagnostics’ acquisition of LifeLabs augments its Canadian footprint, enabling specimen routing to high-throughput genomic hubs in Ontario and British Columbia. The thyroid cancer diagnostics market size serviced by reference labs rises as community hospitals outsource complex assays. Academic medical centers play a pivotal role in early adoption of AI digital pathology suites, validating algorithms before wider roll-out. Cancer specialty centers round out demand by bundling diagnostic, therapeutic and follow-up services, streamlining patient journeys and amplifying test volume.

Geography Analysis

North America generated 38.74% of 2025 revenue, cementing its status as the largest regional contributor to the thyroid cancer diagnostics market. Medicare’s MolDX coverage and private payer alignment underpin broad access, while U.S. clinical guidelines promote molecular classifiers for Bethesda III-V nodules. Canada covers ultrasound and cytology through provincially funded plans but reimburses genomic sequencing selectively, creating mixed public-private demand. Mexico improves urban oncology services through federal investment, although rural disparities persist. The region’s innovation ecosystem propels AI model development, with GE HealthCare and NVIDIA co-engineering real-time ultrasound triage that mitigates pathologist shortages.

Asia-Pacific posts the fastest 7.90% CAGR. China’s tiered cancer screening initiatives embed thyroid ultrasound in community clinics, escalating specimen submission to regional molecular hubs. Japan’s population-based registry supports precision screening thresholds that reduce unnecessary biopsies yet ensure high testing volume where risk is elevated. India’s rapid expansion of private oncology chains increases access to NGS panels, although pricing remains a hurdle. South Korea’s insurance-backed check-up culture produces high scan rates, encouraging AI start-ups to commercialize triage platforms domestically before seeking U.S. Food and Drug Administration (FDA) clearance. The thyroid cancer diagnostics market share in Asia-Pacific will grow as local manufacturers release cost-optimized sequencing kits.

Europe maintains mature uptake of advanced diagnostics, guided by the European Medicines Agency’s centralized review that clarifies companion-diagnostic pathways. Germany pilots nationwide AI ultrasound quality registries, while the United Kingdom’s National Health Service (NHS) uplifts genomic classifier adoption through the Genomic Medicine Service. Southern European nations accelerate procurement of hybrid PET/MRI scanners, supported by EU recovery funds. Pan-European reimbursement parity remains a work in progress; however, collaborative procurement reduces per-unit reagent costs, benefiting smaller member states. These dynamics collectively boost the thyroid cancer diagnostics market, albeit at lower relative growth than Asia-Pacific.

Competitive Landscape

The thyroid cancer diagnostics market features moderate concentration. Roche Diagnostics, Abbott and Thermo Fisher Scientific leverage broad assay portfolios spanning immunochemistry, cytology staining and NGS panels, reinforced by long-standing distributor networks. Roche’s cobas 5800 platform targets mid-volume hospitals looking for consolidated molecular workloads. Abbott integrates free thyroxine (T4) and thyroglobulin immunoassays on the Alinity ci series, ensuring high throughput for large laboratories.

Disruptive entrants amplify competition. Veracyte, with Afirma and the recently acquired C2i minimal-residual-disease technology, pushes into longitudinal monitoring niches. Guardant Health expands beyond ctDNA to include multiomic readouts, differentiating on biomarker breadth. AI champions such as PathAI and Paige collaborate with scanner manufacturers to automate follicular lesion classification, tackling the cytopathologist gap. Strategic collaborations flourish: GE HealthCare signs a multi-year pact with NVIDIA to embed GPU-accelerated models in ultrasound carts, reducing inference latency to sub-second.

Mergers and acquisitions intensify as incumbents pursue end-to-end capabilities. LabCorp bought assets from Incyte Diagnostics to deepen oncology testing expertise. Quest Diagnostics absorbed LifeLabs to expand specimen volume in Canada, unlocking cross-border logistics synergies. RadNet’s acquisition of See-Mode adds AI vascular and thyroid modules to its imaging chain, signaling vertical integration from scanning to interpretation. Competitive differentiation now hinges on the depth of AI integration, turnaround speed, and payer-aligned test menus rather than hardware alone.

Thyroid Cancer Diagnostics Industry Leaders

F. Hoffmann-La Roche Ltd

Siemens Healthineers

Abbott

Thermo Fisher Scientific, Inc.

GE HealthCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: RadNet completed the purchase of See-Mode Technologies to incorporate AI-driven ultrasound analysis for thyroid nodule stratification, broadening its early-detection portfolio.

- May 2025: Guardant Health launched comprehensive immunohistochemistry markers, including HER2 and PD-L1, to complement its Guardant360 Tissue profiling service.

- May 2025: LabCorp acquired clinical pathology assets from Incyte Diagnostics to enhance oncology test offering breadth.

- April 2025: RadNet closed a USD 103 million all-stock deal to purchase iCAD, adding AI breast and thyroid imaging algorithms to its diagnostics suite.

- April 2025: F. Hoffmann-La Roche Ltd. gained FDA Breakthrough Device Designation for the VENTANA TROP2 RxDx immunohistochemistry assay coupled with AI digital image analysis, marking the first AI-guided companion diagnostic for solid tumors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the global thyroid cancer diagnostics market as every imaging platform, in-vitro assay, biopsy kit, and decision-support software that clinicians use to detect, stage, or surveil malignant tumors originating in thyroid tissue, from first screening through post-treatment follow-up.

Scope exclusion: benign-nodule work-ups, therapeutic radio-iodine tracers, and surgical devices lie outside this study.

Segmentation Overview

- By Cancer Type

- Papillary Carcinoma

- Follicular Carcinoma

- Medullary Carcinoma

- Anaplastic Carcinoma

- Other Cancer Types

- By Diagnostic Technique

- Imaging

- Ultrasound

- CT / MRI

- PET / SPECT

- Blood-Based Biomarkers

- TSH / T4 / T3 Panel

- Thyroglobulin & Anti-Tg

- Calcitonin / CEA

- Tissue Biopsy

- Fine-Needle Aspiration Cytology

- Core Needle Biopsy

- Liquid Biopsy

- Other Diagnostic Techniques

- Imaging

- By End User

- Hospital Laboratories

- Cancer Diagnostic Centers

- Independent Reference Labs

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed endocrine oncologists, cytopathologists, hospital lab managers, and imaging-center heads across North America, Europe, Asia-Pacific, and the Gulf. Their insights helped us validate average test panels per patient, biopsy-to-surgery conversion, and emerging AI-ultrasound adoption patterns, filling data gaps that desk work alone cannot close.

Desk Research

Analysts first mine public datasets, including GLOBOCAN incidence files, American Thyroid Association guidelines, U.S. FDA 510(k) clearances, Eurostat procedure volumes, and OECD health-expenditure tables, to ground service-volume and tariff assumptions. Company reports and SEC 10-Ks enrich price and installed-base checks, while news curated through Dow Jones Factiva flags regulatory or reimbursement swings. For competitor cost structures, we reference D&B Hoovers, and patent intensity is tracked in Questel. This list illustrates, not exhausts, the secondary sources reviewed.

Market-Sizing & Forecasting

A top-down model translates national thyroid-cancer incidence into diagnostic encounters, adjusting for screening uptake, repeat imaging rates, and referral leakages. Selective bottom-up cross-checks, including lab reagent shipments and sampled ultrasound ASP multiplied by units, moderate totals. Key inputs include (i) age-standardized incidence, (ii) fine-needle-aspiration utilization, (iii) ultrasound replacement cycles, (iv) reimbursement tariffs, and (v) liquid-biopsy penetration. Multivariate regression with scenario analysis projects each driver through 2030, and missing bottom-up datapoints are interpolated from matched hospitals before reconciliation.

Data Validation & Update Cycle

Every draft model runs variance checks versus external incidence curves and import statistics; anomalies trigger re-interviews or recalibration before senior analyst sign-off. Reports refresh annually, and material events, such as major guideline shifts or blockbuster assay launches, prompt interim updates so clients receive the latest view.

Why Our Thyroid Cancer Diagnostics Baseline Commands Reliability

Published estimates often diverge because firms select different product mixes, geographic spreads, and refresh cadences.

Key gap drivers include whether capital equipment is counted alongside consumables, how outpatient imaging is valued, and the cadence at which currency and tariff shifts are rolled into models. Mordor's definition covers hardware, reagents, and AI software worldwide and is refreshed yearly, thereby producing a broader but current baseline that decision-makers can trace back to transparent variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 245.08 billion (2025) | Mordor Intelligence | - |

| USD 3.07 billion (2024) | Global Consultancy A | Excludes capital equipment and software; narrower country list |

| USD 2.9 billion (2023) | Industry Association B | Derives from hospital claims only; omits reagent sales, slower update cycle |

The comparison shows how limited scopes or infrequent updates compress other figures, whereas Mordor's annually reviewed, incidence-anchored model offers the balanced, reproducible baseline organizations rely on when sizing opportunities or vetting investments.

Key Questions Answered in the Report

What is the current size of the thyroid cancer diagnostics market?

The thyroid cancer diagnostics market is valued at USD 260.94 billion in 2026 and is projected to reach USD 357.01 billion by 2031.

Which diagnostic technique generates the most revenue?

Imaging modalities led the market with 45.78% revenue share in 2025, driven by widespread ultrasound use and AI image-analysis upgrades.

Which region is expanding fastest?

Asia-Pacific shows the highest growth, advancing at an 7.90% CAGR through 2031 due to government-backed screening programs and rising healthcare investment.

How are liquid biopsy tests influencing clinical practice?

Liquid biopsy panels enable non-invasive tumor profiling and treatment monitoring, supporting a 10.10% CAGR and reducing dependence on repeat tissue biopsies.

Why is the shortage of cytopathologists a concern?

Limited specialist availability lengthens diagnostic turnaround times and forces laboratories to adopt AI triage tools, slightly constraining market growth until workforce gaps narrow.

What competitive strategies are top players adopting?

Established vendors pursue acquisitions and AI partnerships, such as GE HealthCare’s alliance with NVIDIA, while molecular specialists like Veracyte and Guardant Health broaden their assay menus to capture emerging liquid biopsy demand.

Page last updated on: