Oncology Molecular Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.13 Billion |

| Market Size (2031) | USD 7.33 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

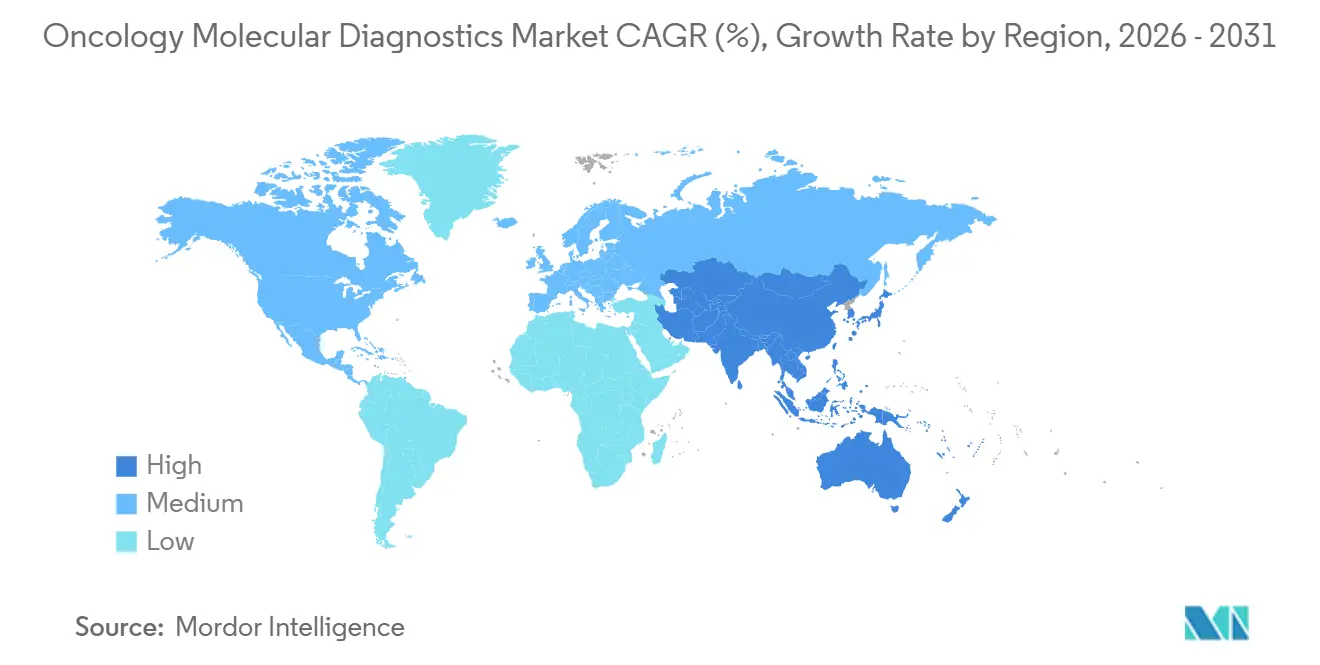

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

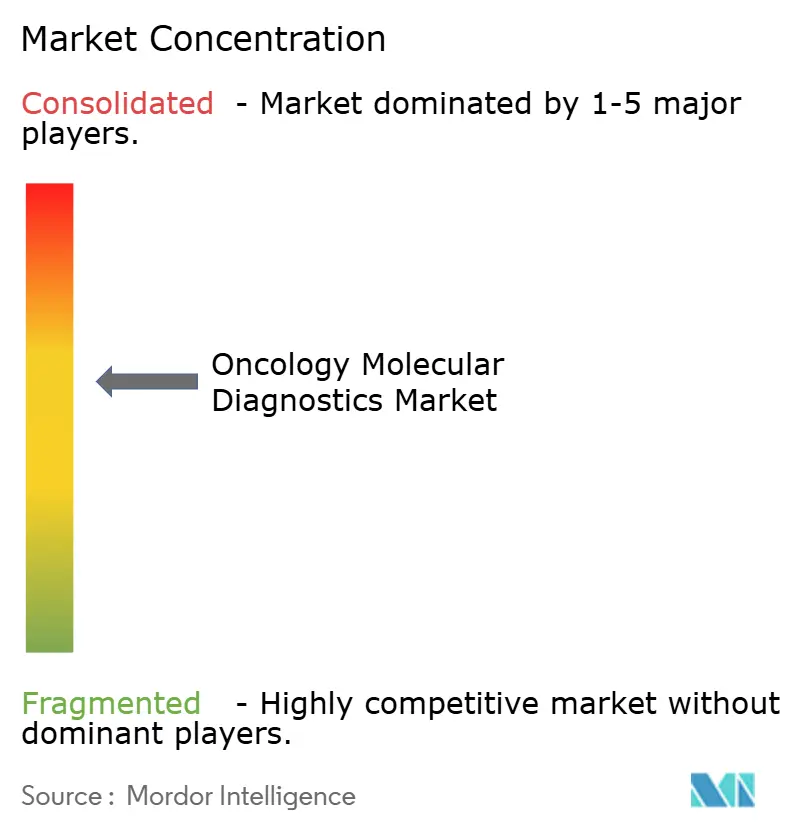

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oncology Molecular Diagnostics Market Analysis by Mordor Intelligence

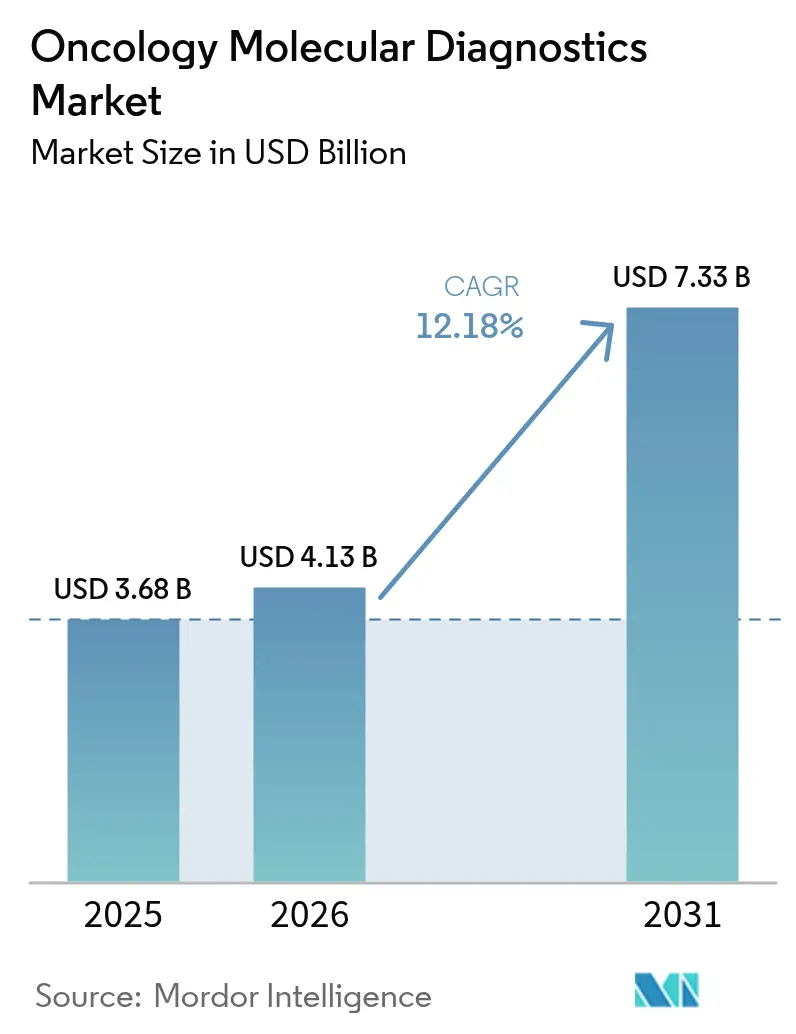

The Oncology Molecular Diagnostics Market size is projected to be USD 3.68 billion in 2025, USD 4.13 billion in 2026, and reach USD 7.33 billion by 2031, growing at a CAGR of 12.18% from 2026 to 2031.

Companion diagnostics linked to targeted therapies, expanding approvals for liquid biopsies, and AI-enabled bioinformatics are accelerating clinical uptake. Demand is also fueled by national genomics programs that improve reimbursement frameworks and by the rising prevalence of cancer, which drives multiple molecular tests per patient along the treatment continuum. Meanwhile, point-of-care platforms are moving sophisticated assays out of centralized laboratories, shrinking turnaround times, and broadening access. Competitive dynamics favor vertically integrated leaders that pair proprietary reagents with analytics software. At the same time, niche innovators leverage AI and liquid biopsy technologies to capture white-space opportunities within the oncology molecular diagnostics market.

Key Report Takeaways

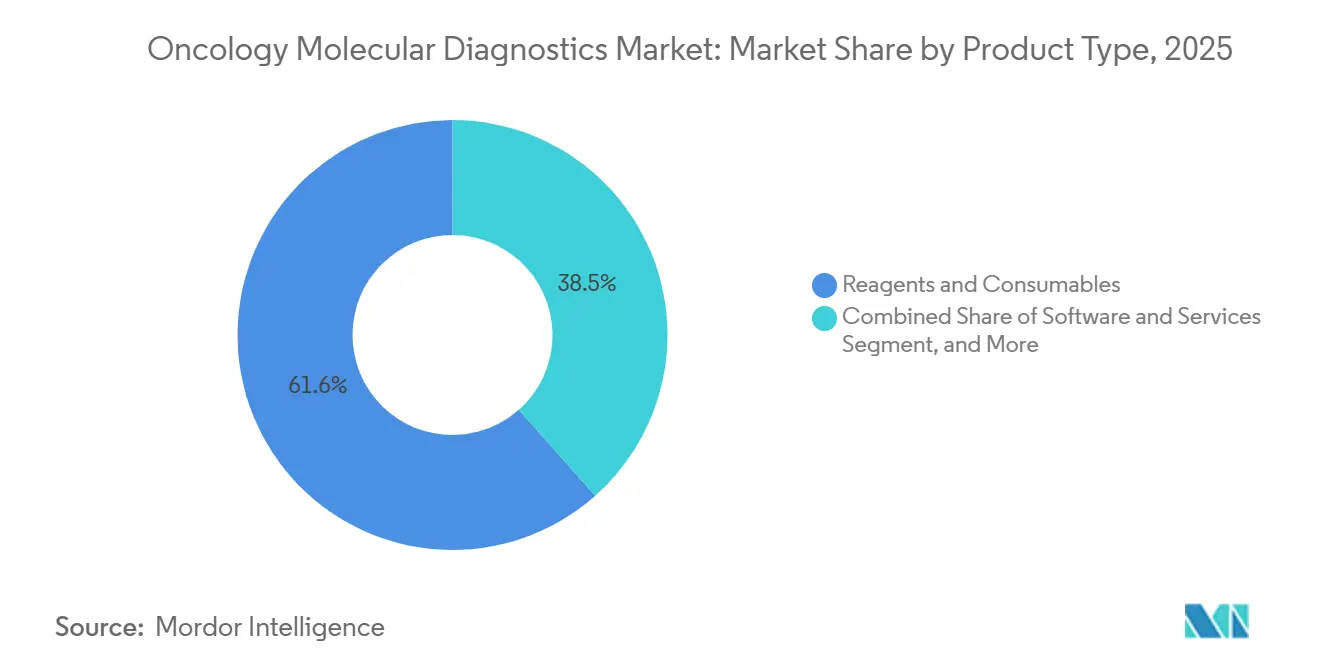

- By product type, reagents and consumables held 61.55of % of the oncology molecular diagnostics market share in 2025, whereas software and services posted a 15.21% CAGR through 2031.

- By technology, PCR led with 34.62% revenue share in 2025; next-generation sequencing expands at a 13.5% CAGR through 2031.

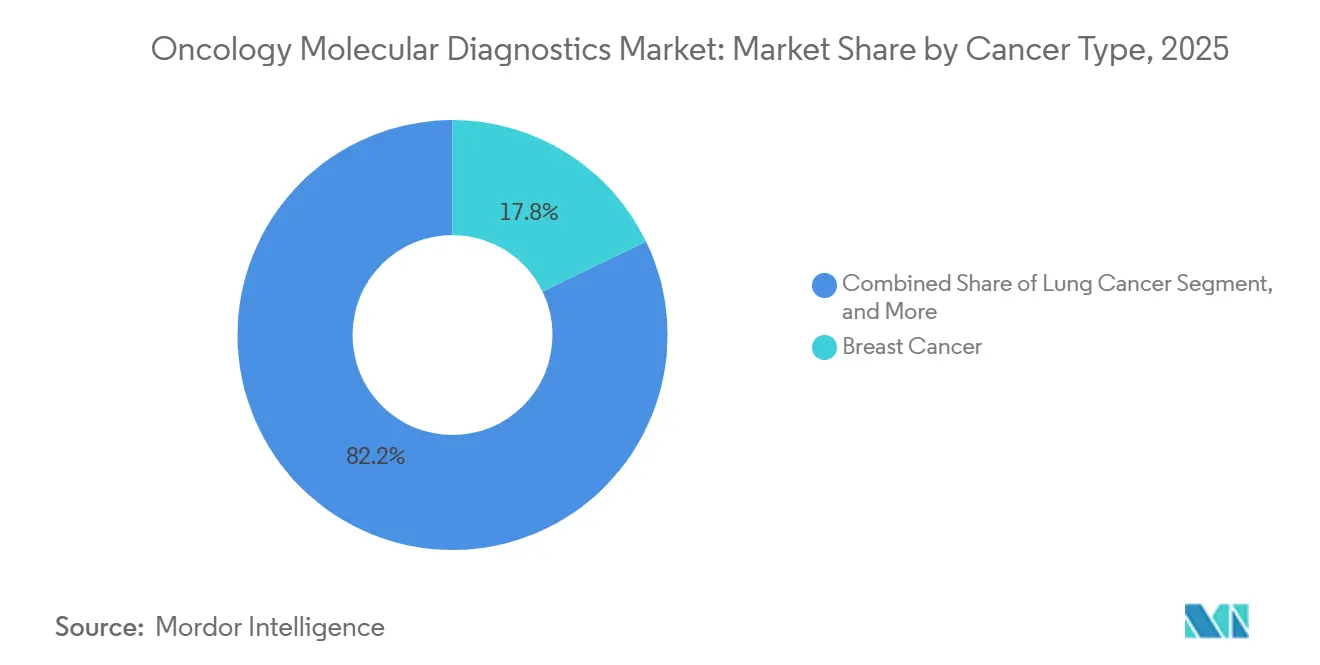

- By cancer type, breast cancer commanded 17.84% of the oncology molecular diagnostics market size in 2025, while lung cancer recorded the highest 12.71% CAGR to 2031.

- By sample type, tissue biopsy retained a 70.62% share of the oncology molecular diagnostics market in 2025; liquid biopsy is advancing at a 14.14% CAGR through 2031.

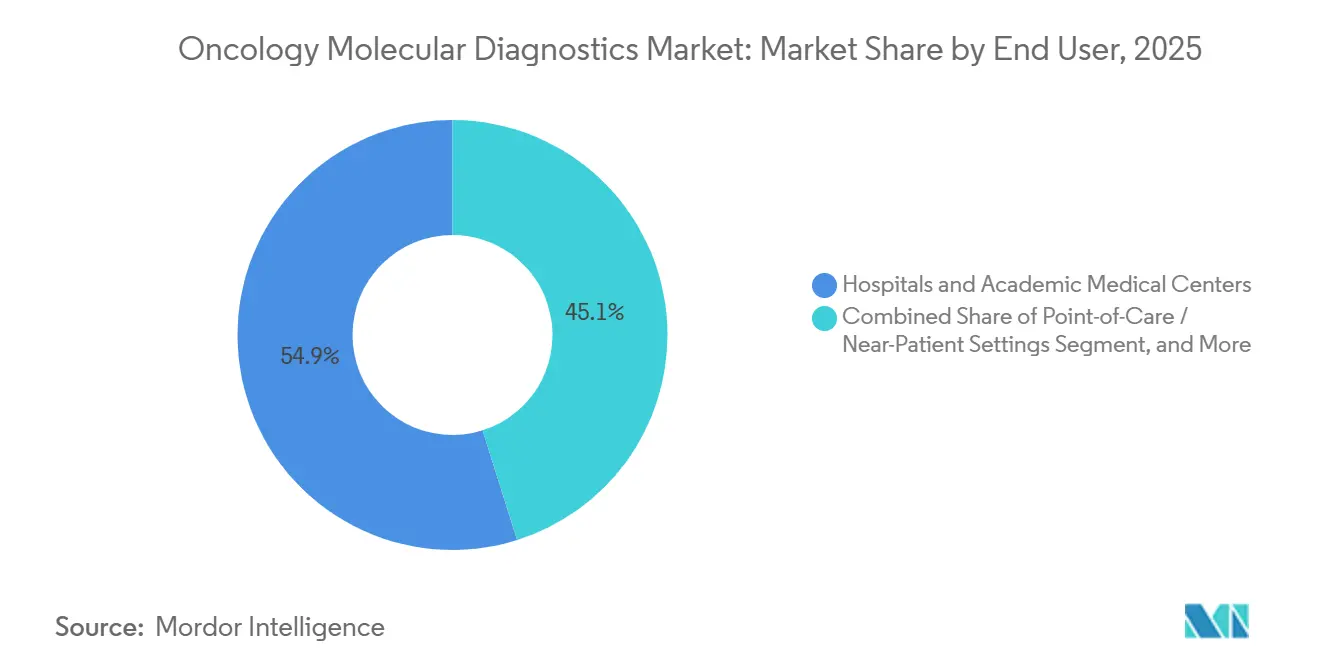

- By end user, hospitals and academic centers accounted for 54.86% of revenue in 2025, whereas point-of-care sites grew at a 13.02% CAGR through 2031.

- By geography, North America led with a 39.72% revenue share in 2025. Asia-Pacific registered the fastest 15.89% CAGR from 2026-2031, outpacing North America’s mature base.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oncology Molecular Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Uptake of liquid-biopsy companion diagnostics | +2.8% | North America, Europe, early APAC | Medium term (2-4 years) |

| National genomics reimbursement initiatives | +2.4% | North America, Europe, Japan | Short term (≤ 2 years) |

| Rising prevalence of cancer | +1.9% | Global | Long term (≥ 4 years) |

| Increasing demand for point-of-care molecular testing | +1.6% | APAC core, MEA, South America | Medium term (2-4 years) |

| AI-enabled synthetic-control trials fast-tracking assay approvals | +1.4% | North America, EU | Short term (≤ 2 years) |

| Bio-economy reagent tax incentives in APAC | +1.2% | China, India, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uptake of Liquid-Biopsy Companion Diagnostics

FDA approvals for liquid biopsy companion diagnostics have multiplied since 2023, enabling real-time genomic monitoring without invasive tissue sampling. FoundationOne Liquid CDx now guides MET exon 14 skipping therapy in non-small cell lung cancer, expanding precision care to patients with limited tissue.[1]Foundation Medicine Editorial Team, “FoundationOne Liquid CDx Receives New FDA Approval,” Foundation Medicine, foundationmedicine.com

Between 2024 and 2025, ctDNA assays received FDA breakthrough status for EGFR, ALK, and KRAS G12C mutations, reinforcing liquid biopsy as a key alternative to traditional tissue genotyping. The turnaround time for these assays has been reduced to 3–5 business days, enabling faster decisions on targeted therapies during the critical first-line treatment phase. AstraZeneca’s FLAURA2 trial leveraged plasma selection to cut enrolment time by 22%, leading to osimertinib approval in August 2024. However, reimbursement challenges persist in emerging markets; for example, in India, public health plans continue to exclude ctDNA, restricting its adoption primarily to private payors.

National Genomics Reimbursement Initiatives

Programs such as Australia’s PrOSPeCT offer 23,000 patients free genomic testing funded by USD 185 million, demonstrating how coordinated policy, clinical trial access, and coverage decisions converge to democratize precision oncology.[2]UNSW Media Office, “PrOSPeCT to Deliver Genomic Testing for 23,000 Australians,” UNSW, unsw.edu.au In January 2025, Medicare established a rate of USD 3,200 for panels covering 324 genes, streamlining the process by eliminating prior-authorization delays that previously lasted up to 3 weeks. By December 2025, Japan plans to reimburse NGS panels at JPY 560,000 (equivalent to USD 3,800), enhancing access to 58 primary hospitals. In 2024, the United Kingdom allocated GBP 175 million to expand whole-genome sequencing to 100,000 cancer patients annually by 2027. Collectively, these measures address significant cost barriers, driving growth and expanding the oncology molecular diagnostics market footprint.

Rising Prevalence of Cancer

In 2024, the global incidence of new cancer cases reached 20 million, reflecting a 7.8% increase from 2020.[3]International Agency for Research on Cancer, “GLOBOCAN 2024,” iarc.fr This growth has driven the demand for molecular profiling to support personalized therapies. Lung cancer alone accounted for 2.5 million of these new diagnoses, boosting the need for assays targeting EGFR, ALK, ROS1, and BRAF. In the United States, 154,000 colorectal cancer cases are projected for 2025, emphasizing the importance of earlier, molecularly-guided screenings. Meanwhile, China reported 4.8 million new cancer cases in 2024 and is allocating resources to hepatitis-B and H. pylori control programs, which rely on PCR-based detection.

Increasing Demand for Point-of-Care Molecular Testing

In February 2025, Cepheid introduced the GeneXpert Xpress EGFR, capable of delivering mutation results within 90 minutes using a finger-stick sample. India implemented 42 GeneXpert systems across tier-2 cities, significantly reducing the median time for treatment initiation from 28 days to just 9 days for patients with EGFR-positive lung cancer. Additionally, Bio-Rad launched the QX600 AutoDG in August 2025, reducing droplet-generation time to 15 minutes and enabling same-day ctDNA quantification. These advancements collectively enhance oncology testing capabilities in outpatient settings and rural clinics.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cost of molecular diagnostic tests | −1.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Shortage of genomic pathologists | −1.3% | Global, severe in APAC & MEA | Long term (≥ 4 years) |

| Cross-border genomic-data sovereignty regulations | −0.9% | EU, China | Short term (≤ 2 years) |

| Volatile supply of specialty nucleotides for NGS reagents | −0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Molecular Diagnostic Tests

In the United States, comprehensive gene panels, covering 300 to 500 genes, are priced between USD 3,000 and 5,800. This pricing leaves under-insured patients facing out-of-pocket fees of USD 1,500, even after coverage adjustments. A 2024 study revealed that 23% of eligible stage IV lung-cancer patients declined testing due to cost concerns. This decision led to a 6.2-week delay in therapy initiation and a reduction of 1.8 months in progression-free survival. In India, the cost of tests, ranging from 80,000 to 150,000 INR (approximately USD 960 to 1,800), represents four to eight months of household income. This financial burden limits access primarily to urban centers. In Brazil, the exclusion of comprehensive profiling from the national health plan confines such services largely to private hospitals.

Shortage of Genomic Pathologists

In 2025, the United States faced a significant shortage of 1,200 board-certified molecular genetic pathologists. Despite a demand for approximately 190 fellows annually, only 87 graduated in 2024. Report turnaround times at community sites can take up to 2 weeks, delaying therapy compared to large academic centers that streamline processes through in-house tumor boards. In India, the National Cancer Grid launched a fellowship program in July 2025, aiming to train 50 fellows annually. However, this initiative is projected to meet only 18% of the required demand through 2030. While AI annotation tools have reduced manual review time by 60%, regulatory frameworks for autonomous sign-outs remain undefined.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Surge on Bioinformatics Demand

Reagents and consumables generated 61.55% revenue in 2025, reflecting recurrent demand and proprietary chemistries that capture low-abundance mutations. This strong position anchors steady cash flows for manufacturers within the oncology molecular diagnostics market. Software and services, although smaller today, rise at a 15.21% CAGR as cloud-hosted analytics automate interpretation and reduce the need for scarce genomic pathologists.

Growth in AI-powered platforms positions bioinformatics as a strategic moat. Vendors bundling reagents with subscription-based interpretation tools secure end-to-end integration, fostering customer stickiness. The oncology molecular diagnostics software solutions market size is projected to expand markedly as laboratories seek efficiency gains and standardized reporting.

By Technology: NGS Gains as Panel Costs Decline

PCR delivered 34.62% revenue in 2025 as laboratories value its cost efficiency and reliability. Digital PCR further extends sensitivity for detecting rare variants in liquid biopsy. In parallel, next-generation sequencing enjoys a 13.5% CAGR, propelled by declining run costs and broader clinical utility. Hybrid capture panels detect hundreds of genes in one assay, transforming treatment selection.

NGS adoption also benefits from combined tissue and plasma workflows that reveal tumor heterogeneity. As laboratories validate liquid biopsy NGS panels, the oncology molecular diagnostics market size for comprehensive profiling grows faster than single-gene PCR assays, yet PCR remains indispensable for rapid single-mutation confirmation.

By Cancer Type: Lung Surges on Liquid-Biopsy Adoption

Breast cancer testing contributed 17.84% of 2025 revenue, sustained by established biomarkers such as HER2 and estrogen receptors. Routine testing ensures consistent volume and underpins reagent consumption in the oncology molecular diagnostics market. Lung cancer, however, records the highest 12.71% CAGR thanks to extensive biomarker panels that include EGFR, ALK, ROS1, and KRAS mutations.

Liquid biopsy companion diagnostics for lung cancer remove tissue constraints, broadening eligible patient pools. Consequently, the oncology molecular diagnostics market share of lung cancer assays is projected to narrow the gap with breast cancer, driven by payer coverage and inclusion in clinical guidelines.

By Sample Type: Liquid Biopsy Climbs on MRD Utility

Tissue biopsy retained 70.62% share in 2025, remaining the histopathological gold standard for initial diagnosis. Yet liquid biopsy revenue climbs at a 14.14% CAGR as non-invasive blood tests facilitate continuous monitoring. Regulatory approvals establish clinical confidence, and patients prefer serial blood draws over repeat tissue procedures.

Serial molecular monitoring detects emerging resistance sooner than imaging, an advantage that fuels adoption. As laboratories standardize circulating tumor DNA workflows, the oncology molecular diagnostics market size for liquid biopsy is set to rise in parallel with expanding companion diagnostic indications.

By End User: Point-of-Care Expands on Portable Devices

Hospitals and academic centers generated 54.86% revenue in 2025, aided by advanced infrastructure and multidisciplinary teams. Yet point-of-care locations register a 13.02% CAGR as cartridge-based platforms simplify testing. Community oncologists gain timely genomic insights without sending samples to central labs.

The trend aligns with value-based care goals that favor rapid decision making. Vendors offering compact analyzers with integrated bioinformatics will capture share as the oncology molecular diagnostics market shifts toward patient-centric delivery models.

Geography Analysis

North America accounted for 39.72% of revenue in 2025, leveraging early regulatory approvals and broad insurance coverage for comprehensive genomic profiling. Testing rates for actionable biomarkers approach 90% in leading cancer centers. Expanded Medicare coverage for minimal residual disease tracking further enlarges the oncology molecular diagnostics market.

Europe adopts a cost-effectiveness lens, leading to selective uptake but consistent reimbursement once clinical utility is proven. Harmonized companion diagnostic and drug approvals by the European Medicines Agency ensure synchronized market entry, supporting stable growth moderated by budget impact assessments.

Asia-Pacific posts the fastest 15.89% CAGR, supported by China’s precision medicine plan and Japan’s genomic cancer program. Investments in national sequencing networks and public-private partnerships lower per-test costs and accelerate technology transfer. As local innovators refine assays for region-specific mutations, the oncology molecular diagnostics market in Asia-Pacific is expanding rapidly, driven by rising cancer incidence and improving healthcare infrastructure.

Competitive Landscape

In 2025, major players Roche, Illumina, Thermo Fisher Scientific, QIAGEN, and Danaher collectively accounted for about 48% of the oncology molecular diagnostics market revenue, while regional firms provided cost-effective alternatives. Illumina's USD 7.1 billion acquisition of GRAIL in 2024 strengthened its position in multi-cancer early detection, showcasing vertical integration. The growing adoption of liquid biopsies is evident from Guardant Health's Guardant360 CDx, which experienced a year-over-year volume increase of 89% in 2025, driven by its use in 14 drug trials.

Emerging companies such as Natera, Veracyte, and BillionToOne are differentiating themselves through proprietary ctDNA panels and direct-to-consumer sampling strategies. Significant opportunities exist in personalized MRD monitoring, where advancements in sensitivity, turnaround time, and AI-driven interpretation enhance pricing potential. Recent patent filings highlight a focus on chemistry kits that reduce library preparation time to under 90 minutes, streamlining workflows in the oncology molecular diagnostics market.

Oncology Molecular Diagnostics Industry Leaders

Illumina Inc.

Qiagen N.V.

F. Hoffmann-La Roche Ltd

Thermo Fisher Scientific Inc.

Danaher Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: BillionToOne rolled out two add-on applications for its Northstar Select liquid-biopsy platform, guiding therapy decisions for advanced solid tumors.

- February 2026: Quest Diagnostics launched Flow Cytometry MRD for Myeloma, matching NGS sensitivity at lower cost.

- January 2026: Metropolis Healthcare opened a dedicated genomics center to bolster precision diagnostics capacity in India.

- January 2026: Caris Life Sciences partnered with Everlywell to merge AI-powered biomarker intelligence with home sample collection.

- September 2025: Guardant Health received FDA approval for the Shield blood test for average-risk colorectal cancer screening, the first liquid-biopsy screening assay to clear regulators.

Global Oncology Molecular Diagnostics Market Report Scope

As per the scope of the report, oncology molecular diagnostics are tests that detect genetic material, proteins, or related molecules that provide cancer information. The market consists of sales of molecular diagnostic instruments, kits, and reagents for diagnosing cancer.

The oncology molecular diagnostics market is segmented by product type, technology, cancer type, sample type, end user, and geography. By product type, the market is segmented into instruments, reagents & consumables, and software & services. By technology, the market is segmented into PCR, isothermal NAAT, next-generation sequencing (NGS), In-situ hybridization (FISH/CISH), mass spectrometry, chips & microarrays, and transcription-mediated amplification. By cancer type, the market is segmented into breast cancer, lung cancer, colorectal cancer, prostate cancer, hematological malignancies (leukemia, lymphoma), liver cancer, cervical & gynecologic cancers, and other solid tumors. By sample type, the market is segmented into tissue biopsy, liquid biopsy (blood/plasma/serum), and fine-needle aspirates & cytology samples. By end user, the market is segmented into hospitals & academic medical centers, diagnostic centers, and point-of-care / near-patient settings. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Instruments |

| Reagents & Consumables |

| Software & Services |

| Polymerase Chain Reaction (PCR) |

| Digital PCR |

| Isothermal NAAT (LAMP/TMA) |

| Next-Generation Sequencing (NGS) |

| In-situ Hybridization (FISH/CISH) |

| Mass Spectrometry |

| Chips & Microarrays |

| Breast Cancer |

| Lung Cancer |

| Colorectal Cancer |

| Prostate Cancer |

| Hematological Malignancies |

| Liver Cancer |

| Cervical & Gynecologic Cancers |

| Other Solid Tumors |

| Tissue Biopsy |

| Liquid Biopsy (Blood/Plasma/Serum) |

| Fine-Needle Aspirates & Cytology Samples |

| Hospitals & Academic Medical Centers |

| Diagnostic Centers |

| Point-of-Care / Near-Patient Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Instruments | |

| Reagents & Consumables | ||

| Software & Services | ||

| By Technology | Polymerase Chain Reaction (PCR) | |

| Digital PCR | ||

| Isothermal NAAT (LAMP/TMA) | ||

| Next-Generation Sequencing (NGS) | ||

| In-situ Hybridization (FISH/CISH) | ||

| Mass Spectrometry | ||

| Chips & Microarrays | ||

| By Cancer Type | Breast Cancer | |

| Lung Cancer | ||

| Colorectal Cancer | ||

| Prostate Cancer | ||

| Hematological Malignancies | ||

| Liver Cancer | ||

| Cervical & Gynecologic Cancers | ||

| Other Solid Tumors | ||

| By Sample Type | Tissue Biopsy | |

| Liquid Biopsy (Blood/Plasma/Serum) | ||

| Fine-Needle Aspirates & Cytology Samples | ||

| By End User | Hospitals & Academic Medical Centers | |

| Diagnostic Centers | ||

| Point-of-Care / Near-Patient Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected size of the oncology molecular diagnostics market by 2031?

The market is projected to reach USD 7.33 billion by 2031, growing at a 12.18% CAGR.

Which product segment holds the largest revenue share in 2025?

Reagents and consumables command 61.55% revenue due to their recurring demand.

Why is Asia-Pacific the fastest growing region?

National precision medicine initiatives, expanding sequencing infrastructure, and rising cancer incidence drive a 15.89% CAGR in Asia-Pacific.

How are liquid biopsy tests changing cancer diagnostics?

Liquid biopsies enable non-invasive, real-time genomic monitoring and now guide therapy selection through multiple FDA-approved companion diagnostics.

What limits wider adoption of molecular diagnostics in emerging markets?

High test costs and limited reimbursement frameworks remain significant barriers despite falling sequencing prices.

How does AI improve next-generation sequencing workflows?

AI automates variant calling and clinical annotation, reducing manual review time by up to 60% and delivering results within hours.

Page last updated on: