Head And Neck Cancer Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.13 Billion |

| Market Size (2031) | USD 12.26 Billion |

| Growth Rate (2026 - 2031) | 11.44% CAGR |

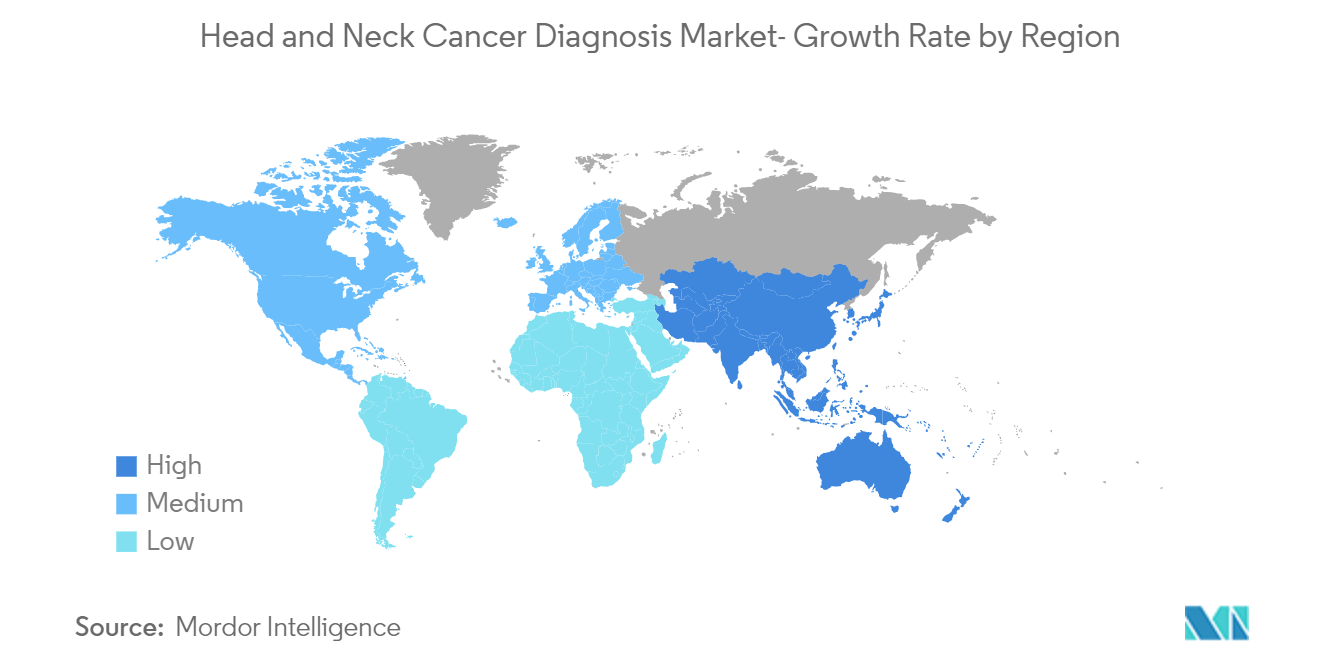

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Head And Neck Cancer Diagnostics Market Analysis by Mordor Intelligence

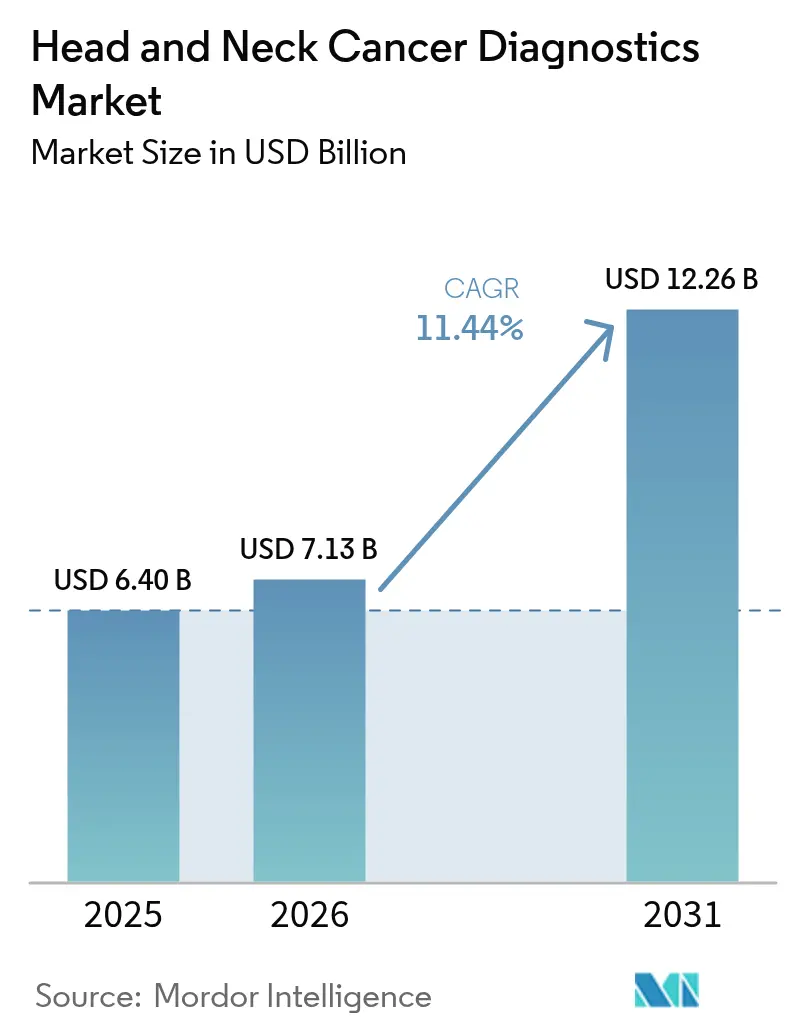

The Head and Neck Cancer Diagnostics Market size was valued at USD 6.40 billion in 2025 and estimated to grow from USD 7.13 billion in 2026 to reach USD 12.26 billion by 2031, at a CAGR of 11.44% during the forecast period (2026-2031).

The COVID-19 pandemic has affected healthcare systems globally and significantly impacted the head and neck cancer diagnosis market. For instance, as per the article published in the Sage Journal in December 2021, approximately 88% of cancer centers across 54 countries reported difficulties in providing care, suggesting the pandemic's significant impact on cancer care. Early in the pandemic, there were proponents of delaying care for patients with mild symptoms of head and neck cancers (HNCs), given the vulnerability of this patient population to pulmonary complications associated with the virus. Thus, the COVID-19 pandemic has impacted the head and neck cancer diagnostics market. However, since the lockdown restrictions were lifted, the industry has been recovering well. Post-pandemic, the market is expected to gain traction over the coming years because of declining COVID-19 cases and the resumption of hospital services.

The growing burden of head and neck cancer and the rising geriatric population are expected to propel the market's growth over the forecast period. Oropharyngeal cancer is the most common type of head and neck cancer. It can affect several areas in and around the mouth, including the lips and tongue. According to the 2022 American Cancer Society Report, there were around 11 230 fatal cases and 54,000 new cases of the oral cavity or oropharyngeal cancer, respectively, in the United States. Thus, the increasing prevalence of head and neck cancer is expected to raise demand for its early diagnosis, thereby boosting the market's growth over the forecast period.

Additionally, a growing number of diagnostic procedures for head and neck cancer is expected to propel the growth of the market. Endoscopy, head MRI, CT of the sinuses, head CT, panoramic dental x-ray, dental cone beam CT, PET/CT, or chest imaging is utilized to confirm a cancer diagnosis and determine the spread of malignancy. The increased adoption of these diagnostic techniques is expected to boost market growth over the forecast period. For instance, according to the study published in the American Journal of Roentgenology in November 2022, CT, MRI, and FDG PET/CT all play essential roles in the diagnosis, staging, therapy planning, and monitoring of head and neck cancers. Thus, the availability of several diagnostic techniques for head and neck cancer is expected to propel the growth of the market.

Moreover, various strategies taken by research institutes to increase awareness about head and neck cancer are expected to support market growth. For instance, in May 2021, the Head and Neck Cancer Alliance (HNCA) and PDS Biotechnology Corporation established a collaboration. This cooperation aims to improve knowledge of novel and developing treatment options for individuals with HPV-related head and neck cancer diagnoses, including available clinical trials.

Thus, all the factors above, such as the growing burden of head and neck cancer, are expected to boost the market over the forecast period. However, the high cost of diagnostic devices and reimbursement issues may restrain the market's growth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Head And Neck Cancer Diagnostics Market Trends and Insights

Diagnostic Imaging Equipment is Expected to Hold a Significant Share in the Head and Neck Cancer Diagnostics Market

In cancer care, diagnostic imaging has many benefits, including real-time monitoring, accessibility without destroying tissue, low or no invasiveness, and higher accuracy. Diagnostics Imaging is the technique and process of creating visual representations of the interior of a body for clinical analysis and medical intervention, as well as a visual representation of the function of some organs or tissues (physiology). Head and neck cancer is a group of cancers that usually originate in the squamous cells that line the mouth, nose, and throat. To confirm a cancer diagnosis and determine if it has spread, head MRI, CT of the sinuses, head CT, panoramic dental x-ray, dental cone beam CT, PET/CT, or chest imaging are some of the most common procedures.

Additionally, new product launches and approvals in the market will also push the market to continue growing to new heights. For instance, in May 2021, Philips Healthcare received approval from the US Food and Drug Administration for the computed tomography system Spectral CT 7500, which uses intelligent software to deliver high-quality spectral images on every scan 100% of the time without the need for special protocols. Thus, all the aforementioned factors, such as an increase in the use of diagnostic imaging technology in the diagnosis of head and neck cancer, are expected to boost segment growth.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

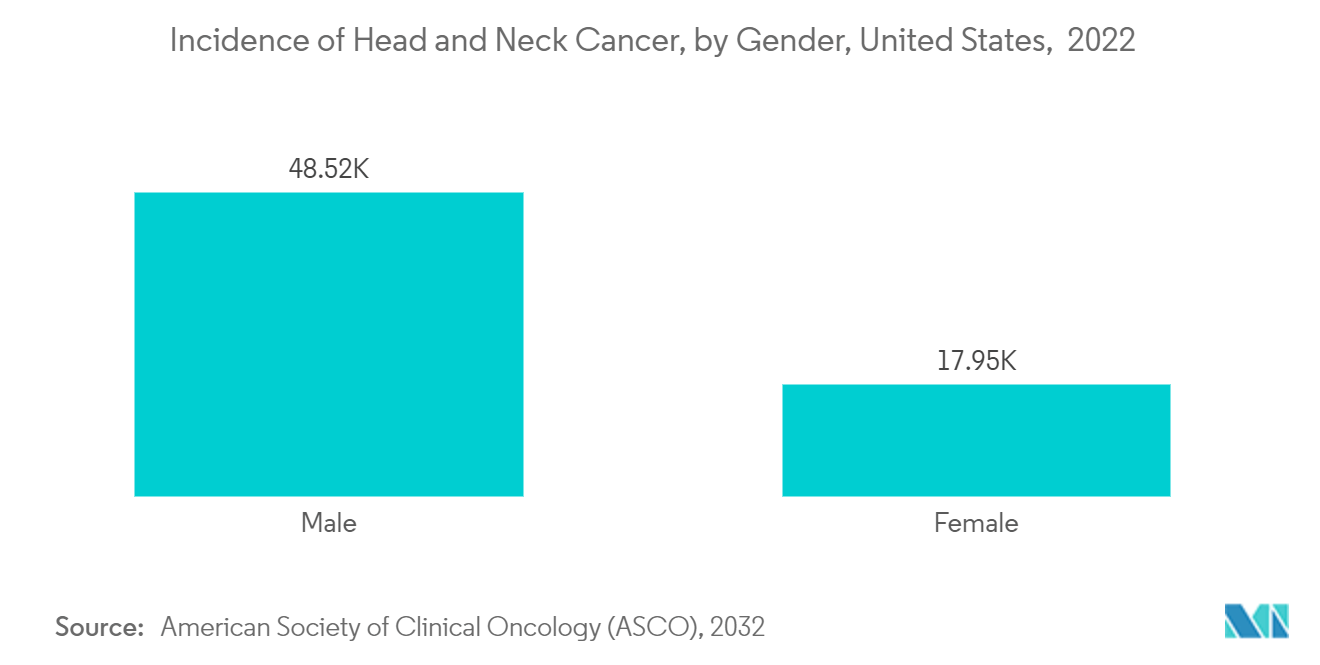

North America is expected to hold a significant market share in the future, owing to the increased adoption of cancer diagnostics and the growing burden of cancer in the United States. For instance, according to the Canadian Cancer Society, in May 2022, 7,500 Canadians were expected to be diagnosed with head and neck cancer. In 2022, 5,400 men and 2,000 women had been diagnosed with head and neck cancer. Thus, a significant head and neck cancer burden is expected to boost market growth over the forecast period.

Every year from April 11 to 17, Oral, Head, and Neck Cancer Awareness Week is commemorated in the United States. These cancers, which are dedicated to head and neck cancers in particular, are usually caused by tobacco use, but they can also be inherited. Such initiatives are expected to increase head and neck cancer awareness, ultimately driving the market's growth.

The product launches by the market players are expected to boost the market in the region. For instance, in August 2022, Viome Life Science launched an at-home test called CancerDetect for oral and throat cancer. CancerDetect brings unprecedented accuracy to early cancer detection and prevention as the only oral and throat cancer test to offer detection with 95% specificity and 90% sensitivity. Hence, the increasing geriatric population in North America, combined with government and private sector initiatives, is one of the other factors contributing to the market's growth.

Competitive Landscape

The head and neck cancer diagnostics market is consolidated with the presence of global players. Market leaders with more funds for research and a better distribution system have established their position in the market. Some of the major players include GE Healthcare, Philips, Siemens Healthineeer, etc.

Head And Neck Cancer Diagnostics Industry Leaders

GE Healthcare

Philips

Siemens Healthineers

Identafi

Shimadzu Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clinical and commercial demand is growing for non-invasive and workflow-automating diagnostics that can reduce reliance on high-cost imaging capacity and specialist availability. In 2026, ErlySign received US FDA Breakthrough Device Designation for a saliva-based oral cancer detection test with rapid turnaround, which points to continued momentum in point-of-care and decentralized screening for oral and oropharyngeal cancer pathways.

Another opportunity is software-assisted imaging and radiation-planning tools that reduce manual segmentation and contouring effort across head and neck cases. In June 2026, GE HealthCare received FDA 510(k) clearance for MIM Contour ProtegeAI+ 2.0 for AI-assisted auto-contouring in radiation therapy planning, reflecting demand for approaches that standardize planning quality and shorten cycle times for complex anatomies. In parallel, liquid biopsy and MRD monitoring are expanding within regulated clinical use in Europe, supported by EU IVDR, as Natera Signatera received EU IVDR Class C certification in 2026 that includes head and neck cancer, creating potential for wider adoption in surveillance and recurrence monitoring alongside imaging and endoscopy.

Recent Industry Developments

- June 2026: GE HealthCare received US FDA 510(k) clearance for MIM Contour ProtegeAI+ 2.0, an AI-enabled auto-contouring software used in radiation therapy planning workflows. The clearance broadens access to automation for complex head and neck planning tasks where contouring workload and variability can be high.

- July 2025: Shimadzu Corporation received US FDA premarket notification (510(k)) for its PositView PET system and initiated US marketing of the device for dedicated examinations including head applications. The clarification supports Shimadzu's positioning in nuclear medicine imaging options that are used across diagnosis, staging, and follow-up in oncology care pathways.

- October 2024: Philips received US FDA clearance for its AI-enabled MR-only head and neck radiotherapy application. MR-only simulation supports radiation planning workflows by reducing reliance on multi-modality image fusion and aligns with the market shift toward software-enabled imaging upgrades.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers diagnostic procedures and related equipment and tests used to detect and confirm head and neck cancers, across care settings such as hospitals and diagnostic centers, measured as annual revenue from these diagnostics.

Scope exclusions: It excludes treatment revenues (such as surgery, radiation therapy, and drug therapy) and general cancer screening not specific to head and neck cancer suspicion.

Segmentation Overview

- By Diagnostic Method

- Diagnostic Imaging Equipment

- Endoscopy Screening Equipment

- Bioscopy Screening Tests

- Dental Diagnostic Methods

- Other Diagnostic Methods

- By End User

- Hospitals

- Diagnostic Centers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean structure of what gets tested, where it gets tested, and how often it is done, because diagnostics markets are driven by procedures and utilization as much as by device sales. We relied on public health statistics and clinical references to understand incidence patterns and diagnostic pathways, and then paired that with pricing context and utilization signals.

Sources reviewed included, as examples, global cancer incidence and mortality datasets (such as WHO and IARC), national cancer registries, CDC publications for screening and risk factors, peer reviewed clinical guidelines and journals, and trade and customs statistics for medical device flows where relevant. We also used public company filings and investor presentations for segment revenue clues, along with reputable press and association websites for technology adoption signals. For specific company financial intelligence, patent lookups, and selective trade shipment checks, we used paid databases that support those use cases. These are illustrative only, and many other sources were also consulted to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work was used to pressure test how diagnostics are actually used in suspected cases, and to sanity check volumes and pricing across hospitals, diagnostic centers, and labs. We spoke with a mix of clinicians, lab and imaging managers, and commercial leaders across APAC, EMEA, and the Americas so the model reflects regional differences in access, referral patterns, and reimbursement behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 18% | Managers: 54% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool reconstruction that starts from head and neck cancer case load, suspected patient workups, and the typical diagnostic pathway, which is then translated into test and procedure volumes by setting. Those volumes were valued using blended pricing ranges for key modalities and tests, followed by adjustments for region level access and reimbursement realities that were confirmed through interviews.

To keep the totals anchored, selective bottom-up approximations were used as checks, such as sampled revenue roll ups for key diagnostic categories, sampled ASP times volume logic for major test types, and channel checks with distributors and labs where data was available. Inputs used in the model included incidence and age mix trends, imaging and endoscopy utilization rates in suspected patients, biopsy and pathology confirmation rates, HPV related testing uptake for relevant tumor sites, and average realized pricing by setting (hospital versus diagnostic center). For forecasting, we used scenario analysis supported by short regressions on incidence, access expansion, and technology adoption so the growth path is explainable and not overly sensitive to one assumption. When bottom-up signals were incomplete in smaller countries, gaps were handled using proxy utilization rates from comparable markets and then re-scaled using local healthcare spend and capacity indicators.

Data Validation & Update Cycle

Outputs were cross checked against independent signals, including procedure intensity expectations from clinical pathways, regional capacity indicators for imaging and endoscopy, and revenue plausibility versus public financial disclosures. If a region produced an unusual jump or an implied price that did not match interview ranges, assumptions were revisited and, when needed, respondents were re-contacted for clarification before sign-off.

A multi step internal review is followed so calculation logic, units, and currency conversion timing are consistent across regions. Reports are refreshed annually, and interim updates are made when material events occur, such as guideline changes, reimbursement shifts, or major diagnostic technology adoption. Right before delivery, a final review pass is completed so clients receive the most current view possible.

Mordor Intelligence's Global Head Neck Cancer Diagnostics Market Market Size Measured Against Other Published Estimates

Published estimates for head and neck cancer diagnostics can look far apart because each publisher picks different definitions of what counts as diagnostics, and they also use different anchors for volume and price. The biggest swings usually come from whether broad oncology testing is blended in, how procedure volumes are inferred, and how pricing is normalized across countries.

Some estimates group wide oncology imaging and lab testing into the same pool even when the test is not ordered for head and neck cancer suspicion. In Mordor Intelligence, revenues are counted only for head and neck cancer diagnostic pathways mapped to imaging, endoscopy, biopsy screening tests, and dental diagnostic methods, and treatment and unrelated screening are kept out of the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.40 B (2025) | |

| Industry Data Publisher A | USD 2.45 B (2024) | Uses a narrower valuation base that appears to emphasize selected test types and reported test categories, which can undercount full workup pathways that include imaging, endoscopy, and confirmatory biopsy steps across care settings. |

| Healthcare Research Group B | USD 2.72 B (2025) | Often frames scope around a limited product and method basket and may apply conservative utilization assumptions for suspected patient workups, which reduces implied procedure volumes and keeps the total smaller even for the same year. |

Taken together, the spread mainly reflects different scope choices and how volumes are translated from patient pathways into priced procedures. By tying volumes to expected workups and then checking realized pricing and access assumptions with field inputs, the estimate stays traceable to clear demand drivers and repeatable calculation steps.

Key Questions Answered in the Report

How big is the Head and Neck Cancer Diagnostics Market?

The Head and Neck Cancer Diagnostics Market size is expected to reach USD 7.13 billion in 2026 and grow at a CAGR of 11.44% to reach USD 12.26 billion by 2031.

What is the current Head and Neck Cancer Diagnostics Market size?

In 2026, the Head and Neck Cancer Diagnostics Market size is expected to reach USD 7.13 billion.

Who are the key players in Head and Neck Cancer Diagnostics Market?

GE Healthcare, Philips, Siemens Healthineers, Identafi and Shimadzu Corporation are the major companies operating in the Head and Neck Cancer Diagnostics Market.

Which is the fastest growing region in Head and Neck Cancer Diagnostics Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Head and Neck Cancer Diagnostics Market?

In 2025, the North America accounts for the largest market share in Head and Neck Cancer Diagnostics Market.

What years does this Head and Neck Cancer Diagnostics Market cover, and what was the market size in 2025?

In 2025, the Head and Neck Cancer Diagnostics Market size was estimated at USD 6.40 billion. The report covers the Head and Neck Cancer Diagnostics Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Head and Neck Cancer Diagnostics Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: