Thyroid Function Test Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 2.6 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thyroid Function Test Market Analysis by Mordor Intelligence

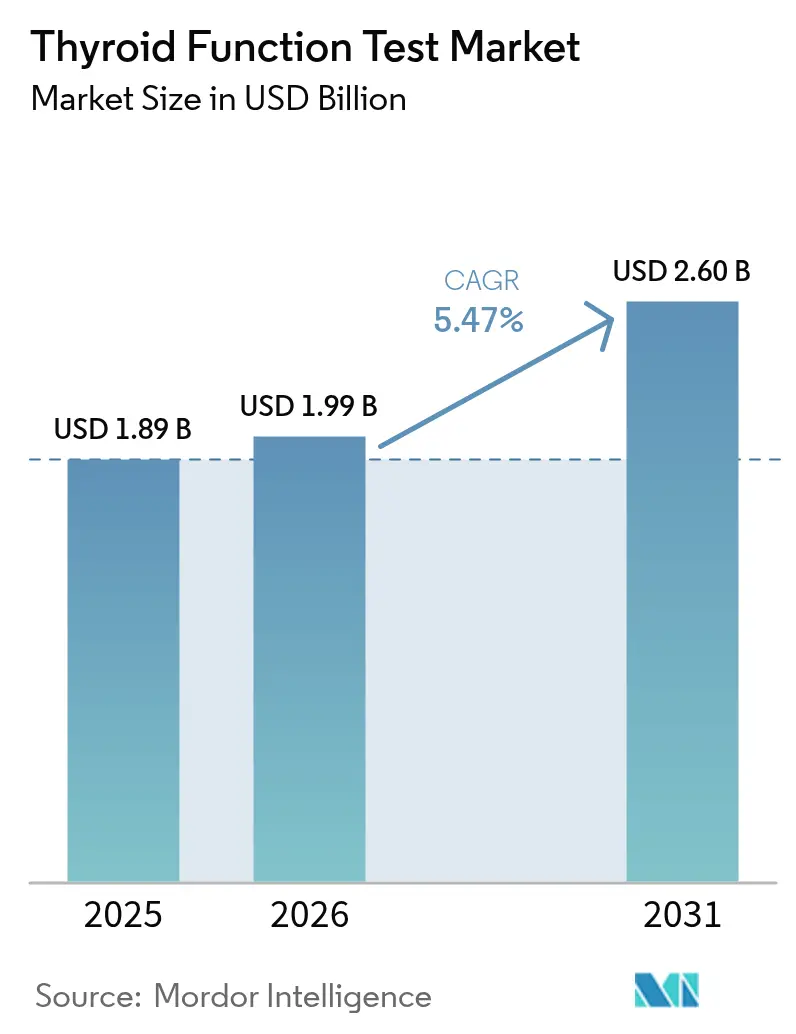

The thyroid function testing market size was valued at USD 1.89 billion in 2025 and estimated to grow from USD 1.99 billion in 2026 to reach USD 2.6 billion by 2031, at a CAGR of 5.47% during the forecast period (2026-2031). Rising global thyroid disease prevalence, an expanding elderly population, and the spread of newborn screening programs anchor this growth. Technology integration—especially high-sensitivity third-generation immunoassays, emerging mass-spectrometry methods, and AI-guided reflex-testing algorithms—elevates diagnostic accuracy while easing the workload created by endocrinologist shortages that affect 70% of US counties. Regulatory changes such as the US FDA’s 2024 framework for laboratory-developed tests introduce higher compliance costs yet promise greater standardization[1]US Food and Drug Administration, “Laboratory Developed Tests Final Rule,” fda.gov. Price transparency laws and bundled-contract negotiations are shifting volumes toward lower-cost independent laboratories, intensifying competition but expanding patient access.

Key Report Takeaways

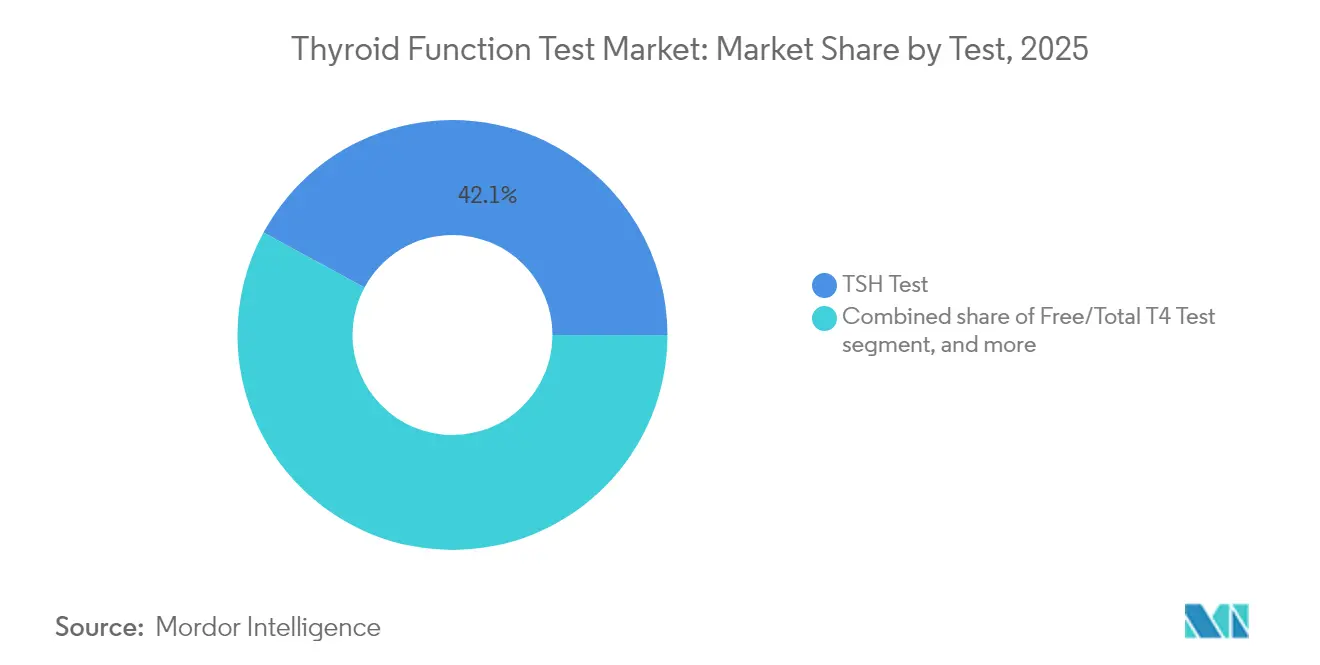

- By test type, the TSH assay held 42.10% of thyroid function testing market share in 2025; Anti-TPO/Anti-TG antibody tests are poised for a 7.42% CAGR to 2031.

- By technique, immunoassay methods accounted for 59.65% share of the thyroid function testing market size in 2025, whereas point-of-care tests will grow at an 8.72% CAGR.

- By end user, hospitals captured 41.10% share of the thyroid function testing market size in 2025, while diagnostic laboratories are advancing at an 8.19% CAGR.

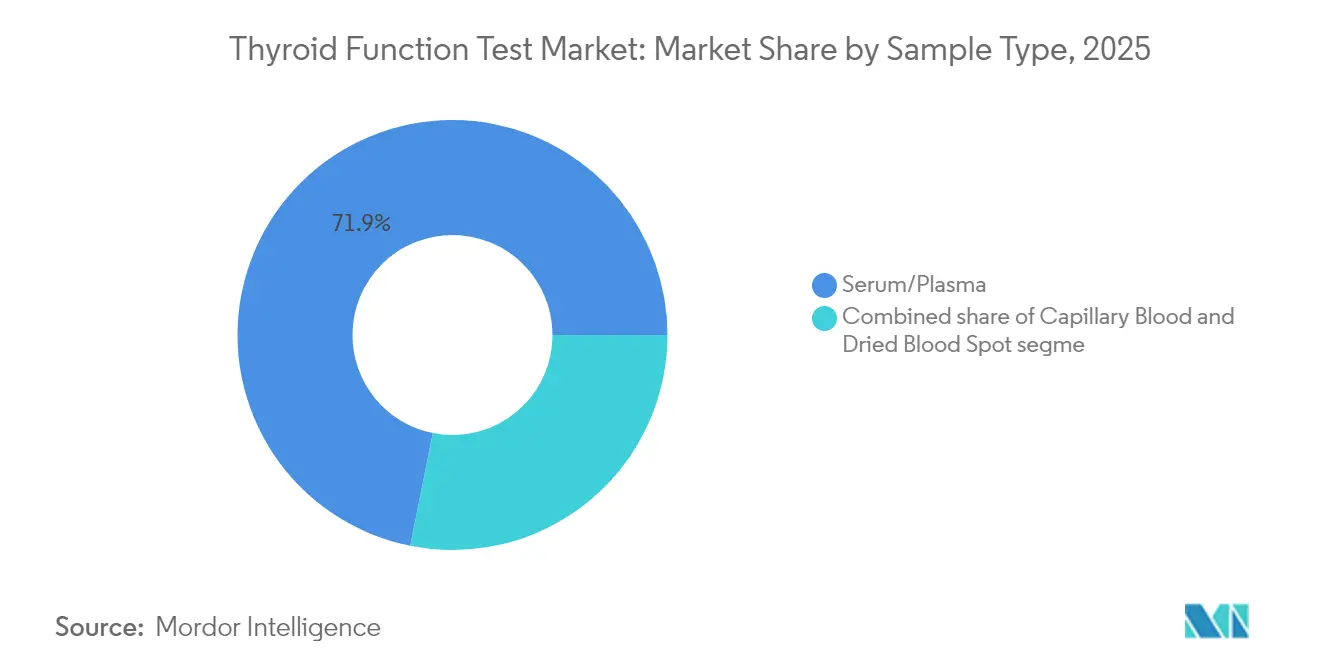

- By sample type, serum/plasma captured 71.85% share of the thyroid function testing market size in 2025, while capillary blood (finger-prick) are advancing at an 7.33% CAGR.

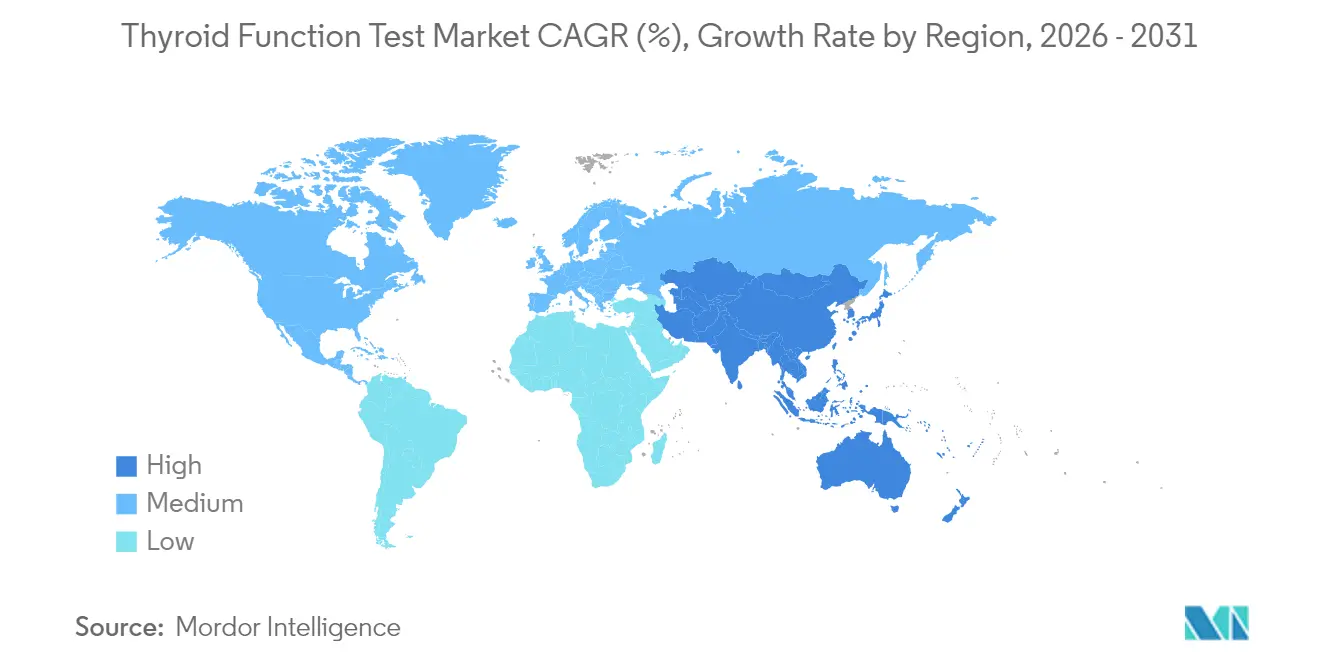

- By geography, North America led with 34.50% revenue share in 2025, while Asia-Pacific is projected to expand at a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thyroid Function Test Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of thyroid disorders | +1.2% | Global; highest in iodine-deficient regions | Medium term (2-4 years) |

| Aging population raises routine screening | +0.9% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| High-sensitivity 3rd-gen immunoassays | +0.8% | Global; led by developed markets | Short term (≤ 2 years) |

| Government-funded newborn screening | +0.7% | Asia-Pacific core; spreading to emerging markets | Medium term (2-4 years) |

| Direct-to-consumer at-home test kits | +0.6% | North America & Europe; early uptake in urban Asia | Short term (≤ 2 years) |

| AI-driven reflex-testing algorithms | +0.5% | Digitally mature health systems worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Thyroid Disorders

Hypothyroidism prevalence reaches 11% in India versus 2–4.6% in Western nations, underscoring geographic differences in iodine sufficiency, genetics, and environmental exposures. Subclinical hyperthyroidism affects 4.4% of US adolescents, highlighting an undiagnosed cohort that fuels screening programs. Growing autoimmune thyroid disease awareness expands demand for antibody panels alongside traditional hormone measures. Earlier detection reduces downstream cardiovascular and cognitive complications, giving payers economic incentives to broaden screening coverage. Collectively these forces underpin steady expansion of the thyroid function testing market.

Aging Population Raises Routine Screening Volumes

Population aging, especially among women older than 60, correlates with higher hypo- and hyperthyroidism rates. A projected US physician shortfall of up to 86,000 by 2036, with endocrinology among the hardest-hit specialties, is accelerating adoption of automated platforms and primary-care-based testing pathways[2]Association of American Medical Colleges, “Physician Workforce Projections 2025-2036,” aamc.org. Insurer reimbursement for preventive screening pushes thyroid panels into routine checkups, transforming test ordering from reactive to proactive. Digitally enabled population-health initiatives further scale testing volumes, reinforcing long-term growth in the thyroid function testing market.

High-Sensitivity 3rd-Gen Immunoassays Improve Clinical Utility

Third-generation TSH assays now detect levels below 0.02 mIU/L, enabling confident diagnosis of subclinical disorders and improved therapy monitoring. Enhanced antibodies, signal amplification chemistries, and automated calibration underpin this performance. Studies confirm superior detection of central hypothyroidism and tighter dose titration in replacement therapy. Ongoing R&D into novel detection chemistries keeps competitive pressure high and sustains innovation momentum within the thyroid function testing market.

Government-Funded Newborn & Population Screening Programs

Near-universal congenital hypothyroidism screening in developed nations contrasts with only 29.6% global newborn coverage, pointing to substantial room for expansion [eurothyroid.com]. Thailand’s rural rollout achieved 98.6% coverage and identified one case per 1,208 births, validating scalable models in resource-constrained settings. Switching from T4-first to TSH-first protocols drops false positives to 0.45% and cuts follow-up costs. Government investment secures predictable demand and encourages private-sector laboratory build-outs, enlarging the thyroid function testing market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex interpretation & biotin interference | -0.8% | Global; pronounced where supplement use is common | Short term (≤ 2 years) |

| Shortage of endocrinologists | -0.6% | North America & Europe; emerging in Asia-Pacific | Long term (≥ 4 years) |

| Lab-test price compression | -0.5% | North America core; expanding globally | Medium term (2-4 years) |

| Guideline push-back against over-screening | -0.4% | Global; led by evidence-based groups | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Interpretation & Biotin Interference Issues

High-dose biotin supplements distort immunoassay results in up to 10% of tested patients, forcing laboratories to impose 7-day cessation windows that delay diagnosis[3]Health Canada, “Biotin Interference in Laboratory Testing,” canada.ca. Interference varies by platform, complicating harmonization across hospital networks. Additionally, hormone-binding protein shifts in pregnancy and critical illness demand nuanced interpretation, prompting some primary-care clinicians to limit ordering, which tempers near-term gains for the thyroid function testing market.

Shortage Of Endocrinologists Slows Diagnosis & Follow-Up

With only 8,000 US endocrinologists and 40.0% approaching retirement, access gaps worsen outside urban hubs. Training programs add roughly 300 specialists annually—insufficient for surging thyroid and diabetes caseloads. Rural patients often face months-long waits, reducing follow-up compliance and capping potential test volumes despite rising disease incidence. Tele-consultation and AI-driven primary-care support partially mitigate but do not fully offset this restraint on the thyroid function testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test: TSH Dominance Faces Antibody Test Disruption

The TSH assay held a 42.10% slice of the thyroid function testing market in 2025, reflecting guideline preference for a sensitive first-line screen. Anti-TPO and Anti-TG antibody assays, while smaller in absolute volume, are expanding at 7.42% CAGR as autoimmune thyroiditis recognition accelerates. Turbo TSI bioassays cut turnaround time from days to hours, and point-of-care antibody kits deliver actionable results inside 10 minutes. Emerging mass-spectrometry panels gain favor in complex cases, promising higher specificity and lower interference, thereby broadening the thyroid function testing market.

Free/total T4 assays remain indispensable for dose titration and differential diagnosis, whereas free/total T3 holds a niche role given low prevalence of isolated T3 toxicosis. Specialized markers—thyroglobulin for differentiated thyroid cancer follow-up and calcitonin for medullary carcinoma—provide incremental revenues but do not materially shift overall thyroid function testing market size. AI-based pattern-recognition tools now help clinicians interpret multi-analyte profiles, reducing diagnostic ambiguity and encouraging wider antibody-panel adoption.

By Technique: Immunoassay Leadership Challenged by POCT Innovation

Immunoassays controlled 59.65% of 2025 revenues, leveraging automated chemiluminescent and ELISA platforms that process thousands of samples per shift. Growth continues but moderates as decentralized care models fuel an 8.72% CAGR for point-of-care formats. Lateral-flow strips using gold nanoshells cut TSH detection thresholds to 0.16 µIU/mL, matching lab-grade sensitivity. Digital immunoassays provide cloud-connected results for remote monitoring, widening the thyroid function testing market.

Mass spectrometry adoption rises within reference labs seeking unparalleled specificity, especially for free hormones where protein binding skews immunoassays. Fluorescence polarization and electrochemiluminescence remain specialty tools in research. COVID-19 heightened appreciation for rapid, minimally attended diagnostics, a behavioral shift sustaining post-pandemic uptake of portable devices and reshaping investment priorities across the thyroid function testing industry.

By Sample Type: Serum Supremacy Yields to Capillary Innovation

Serum and plasma samples still constitute 71.85% of volume, favored for multiparameter panels and regulatory familiarity. Yet capillary blood testing posts a 7.33% CAGR on convenience benefits. Correlation coefficients exceed 0.97 for TSH and free T4 when comparing finger-stick with venous draws, reassuring clinicians of clinical equivalence [endocrinesociety.org]. Dried blood spots streamline newborn programs in remote settings, while smartphone-linked readers transform self-testing into actionable care pathways. As telehealth normalizes, capillary sampling expands overall thyroid function testing market size by recruiting previously undertested populations.

By End User: Hospital Dominance Shifts Toward Laboratory Efficiency

Hospitals generated 41.10% of 2025 revenue, leveraging integrated electronic records and immediate turnaround for acute care. Nonetheless, their higher cost structure—2-6 times that of independent labs—drives payer migration to central laboratories posting an 8.19% CAGR. Price transparency rules expose variability up to 600% for identical thyroid panels, intensifying the push toward lower-cost channels labcorp. Consolidation among reference labs enhances bargaining power, while specialized thyroid centers adopt mass-spectrometry and AI analytics to carve differentiation. Home-testing providers ride rising consumer engagement and remote-care models, adding new demand strata within the thyroid function testing market.

Geography Analysis

North America retained the largest regional share at 34.50% in 2025, propelled by broad insurance coverage, high disease awareness, and sophisticated lab infrastructure. Endocrinologist shortages in 70% of US counties, however, risk pockets of under-service, prompting wider deployment of AI triage tools and tele-endocrinology consults. Price-benchmarking regulations spur health systems to reroute non-urgent panels to independent labs, altering channel mix but sustaining overall thyroid function testing market growth.

Asia-Pacific is the fastest-growing arena at 6.78% CAGR. India’s 11% hypothyroidism prevalence signals a substantial screening opportunity [ijmedicine.com]. China’s rising thyroid cancer incidence and large population base fuel volume, while Japan’s rapidly aging society drives routine monitoring. Government-backed newborn screening expansions in Thailand and elsewhere demonstrate near-universal coverage feasibility, unlocking predictable volumes and elevating regional thyroid function testing market size. Regulatory heterogeneity and reimbursement gaps remain challenges, yet digital health investments and public–private lab partnerships offset barriers.

Europe shows steady but slower expansion, anchored by universal health systems and stringent clinical guidelines. Budget constraints encourage centralized procurement and bundled contracts, favoring cost-efficient suppliers. Regulatory realignment post-Brexit adds complexity, yet established quality standards sustain clinician confidence. Middle East & Africa and South America emerge as longer-term growth pockets as healthcare infrastructure matures. Mobile testing units and telehealth platforms help overcome geographic obstacles, extending reach of the thyroid function testing market into underserved locales.

Regulatory Landscape

Thyroid function tests sold as in vitro diagnostics are regulated as medical devices, with many hormone and antibody immunoassays in the United States typically falling under Class II device controls and clearing the FDA 510(k) pathway (for example, Siemens Healthineers received 510(k) clearance in February 2026 for an Atellica IM TSH assay and in April 2025 for a Dimension LOCI TSH reagent cartridge). The FDA approach focuses on substantial equivalence to predicates for established thyroid stimulating hormone assay types, which supports iterative sensitivity and workflow upgrades on installed immunoassay platforms.

In Europe, thyroid IVDs are governed by the In Vitro Diagnostic Medical Devices Regulation (IVDR 2017/746), which raises expectations for clinical evidence and performance documentation across the product lifecycle; the Medical Device Coordination Group (MDCG) has continued to publish guidance such as MDCG 2025-5 on performance studies. Laboratory quality compliance is also tightening through the ISO 15189:2022 transition, with laboratories required to move from the 2012 edition by December 2025, reinforcing risk-based quality management and documentation requirements that affect assay verification, interference management (including biotin-related controls), and supplier qualification practices.

Competitive Landscape

The thyroid function testing market is moderately consolidated. Abbott, Roche, and Siemens Healthineers leverage broad installed bases, integrated platforms, and service contracts to lock in laboratories. The FDA’s 2024 LDT rule shifts compliance burden toward larger firms with regulatory muscle, potentially thinning smaller outfits. Nonetheless, innovation windows remain: Polaris DX’s EUR 2,250 (USD 2605.9) portable analyzer offers disruptive cost-to-serve economics; HEI Therapeutics progresses patent-protected home-monitoring solutions.

Strategic playbooks center on AI augmentation, mass-spectrometry differentiation, and point-of-care expansion. Midsize vendors pursue geographic partnerships to access fast-growing Asia-Pacific markets, while incumbents bolster menus with calcitonin, antibody, and reflex-algorithm add-ons. Acquisition pipelines target niche assay developers and cloud-analytics specialists, evidencing sustained deal flow even amid rising regulatory costs. Competitive intensity should remain moderate as installed-platform switching barriers and service reliability outweigh pure reagent price in purchasing decisions.

Thyroid Function Test Industry Leaders

Abbott

Siemens Healthineers

Danaher Corporation (Beckman Coulter)

F. Hoffmann-La Roche Ltd

DiaSorin SpA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace sits at the intersection of higher-sensitivity assays, automation, and compliance-driven standardization, where large installed-base vendors can pair new menu items with workflow tools. FDA 510(k) clearances such as Siemens Healthineers Atellica IM TSH3-Ultra II (February 2026) and prior Siemens thyroid reagent clearances (April 2025) show continued room to refresh core TSH testing with improved analytical performance, while fitting payer and health-system demands for reproducible, auditable results across multi-site networks.

Menu expansion around autoimmune thyroid disease and more targeted clinical pathways is another active lane. DiaSorin launched the LIAISON TSH-R Ab assay (September 2025) for Graves disease diagnosis and therapy monitoring, supporting broader antibody testing on routine immunoassay platforms beyond TSH-first screening. At the same time, payer medical policies that emphasize TSH as the primary first-line test and constrain add-on antibodies to specific indications create practical demand for reflex-testing algorithms and decision support that optimize ordering in systems facing specialist shortages, while protecting test appropriateness and reducing avoidable repeats tied to known interference issues such as biotin.

Recent Industry Developments

- June 2026: Viridian Therapeutics announced US FDA approval and launch of Lumvoa (veligrotug-vvze) for thyroid eye disease. The product launch raises the need for structured thyroid-related monitoring pathways and coordinated endocrine and ophthalmology care, which can increase the role of routine thyroid status assessment alongside disease management.

- September 2025: DiaSorin launched the LIAISON TSH-R Ab immunodiagnostic assay in CE Mark recognizing countries for Graves disease diagnosis and therapy monitoring. The launch expands autoimmune thyroid testing availability on consolidated immunoassay platforms and supports labs building more comprehensive thyroid panels beyond core TSH and free T4 testing.

- October 2024: Siemens Healthineers completed verification of the Atellica DL IM1600 analyzer for anti-TPO and anti-TG detection to support autoimmune thyroid diagnosis workflows. Analyzer verification and menu readiness help laboratories tighten turnaround times and standardize antibody testing as demand rises for autoimmune panels alongside traditional hormone assays.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from thyroid function testing used to assess thyroid hormone status through blood-based in vitro assays that are ordered and reported in clinical care and screening workflows.

Scope exclusions: We exclude imaging, biopsies, and genetic testing that may be used in thyroid cancer workups or broader endocrine evaluations.

Segmentation Overview

- By Test

- TSH Test

- Free/Total T4 Test

- Free/Total T3 Test

- Anti-TPO/Anti-TG Antibody Tests

- Other Test

- By Technique

- Immunoassay (CLIA, ELISA, RIA)

- Rapid Point-of-Care Tests

- Mass Spectrometry

- Other Techniques

- By Sample Type

- Serum/Plasma

- Capillary Blood (Finger-prick)

- Dried Blood Spot

- By End User

- Hospital

- Diagnostic Laboratory

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with understanding the tested population and the clinical triggers for ordering thyroid panels, so our assumptions stay tied to real care pathways. We referred to public sources such as the Centers for Disease Control and Prevention, the National Institutes of Health, the World Health Organization, and the OECD health statistics for screening context, testing intensity signals, and disease burden direction.

We also reviewed guidance and technical references from sources such as the FDA, peer-reviewed clinical chemistry and endocrinology journals, and lab medicine association publications to understand test menus, reflex testing patterns, and quality controls that influence adoption. Company filings, investor presentations, reputable press, and a paid subscription for company financials and news were used to map product mix shifts and commercialization timelines without relying on supplier claims. This list is illustrative, and many other sources were also checked to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work was used to pressure test the model inputs that desk sources do not publish cleanly, such as typical thyroid test panel mix, how diagnostic laboratories contract and price testing, and how price changes translate into realized test revenue. We spoke with stakeholders across kit and reagent supply, diagnostic laboratories, hospital lab teams, and clinical users, and then used their feedback to align regional utilization and pricing assumptions across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 20% | APAC: 38% |

| Mid tier: 44% | Functional/Unit leaders: 34% | EMEA: 36% |

| Smaller Players: 20% | Managers: 46% | Americas: 26% |

Market-Sizing & Forecasting

The core sizing uses a top-down and bottom-up approach where diagnosed and screened populations, typical testing frequency, and lab channel split are used to reconstruct annual test volumes, which are then converted to value using region-specific realized pricing. To keep it grounded, we corroborated the output with selective bottom-up checks such as sampled menu-level ASPs from labs, channel discussions on reagent pull-through, and supplier-side volume signals, and then the total was adjusted when a mismatch persisted.

Key inputs used in the model include hypothyroidism and hyperthyroidism burden direction, newborn screening coverage trends, the share of tests that follow reflex algorithms (for example, TSH first followed by free T4), the split between hospital labs and independent labs, and inflation-linked changes in reagent pricing and service contracts. For forecasting, scenario analysis was applied around utilization growth and pricing, and the final path was selected after expert feedback on what adoption and reimbursement conditions look most likely over the next few years. When local data was thin, proxy ratios from similar health systems were used and then rechecked in follow-up calls before locking the final series.

Data Validation & Update Cycle

Validation is done through cross-checks across multiple signals, so the final number is not dependent on a single dataset. We compare implied test volumes, price levels, and regional shares against independent indicators, and anomalies are reviewed in analyst peer checks before sign-off.

The report is refreshed annually, and interim updates are triggered when material events occur such as major regulatory changes, large pricing shifts, or meaningful changes in screening practices. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Thyroid Function Test Market Sizing Compared With Other Published Estimates

Published market sizes for thyroid function testing can look far apart because each publisher sets its own scope and then applies different assumptions for utilization and pricing. Differences usually show up in what is counted as a test, how panels are valued, and how fast the model lets volumes and prices move year to year.

Some estimates bundle thyroid testing into broader endocrine diagnostics or extend the count to adjacent screening and services that do not always map to a thyroid function lab order. In the Mordor Intelligence model, value is limited to laboratory-validated blood-based in vitro thyroid assays (such as TSH and free or total T3 and T4 panels), and imaging and genetic workups are kept outside scope to avoid inflated totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.99 B (2026) | |

| Global Research Group A | USD 1.81 B (2025) | Uses a different base year and can mix a wider set of thyroid-related indications into one pool, which shifts test mix and average realized pricing assumptions. |

| Global Consultancy B | USD 5.45 B (2025) | Applies a broader revenue capture that can expand beyond assay revenue into wider diagnostic and service components, and it may rely on higher ASP progression across regions. |

The spread in these benchmarks mainly comes from scope choices and how value is assigned to a test event, especially when broader diagnostic bundles or higher price points are assumed. Our method stays tied to test-volume signals, realistic panel mix, and region-level realized pricing, which makes the steps easier to repeat and validate over time.

Key Questions Answered in the Report

What is the current global thyroid function testing market size?

The thyroid function testing market is valued at USD 1.99 billion in 2026.

Which region is growing fastest?

Asia-Pacific is expanding at a 6.78% CAGR to 2031, driven by newborn screening and rising awareness.

Why are TSH tests still dominant?

Clinical guidelines position TSH as the first-line screen, giving it 42.10% market share in 2025.

How is AI transforming thyroid diagnostics?

AI-driven reflex-testing algorithms automate ordering and interpretation, improving accuracy and easing specialist shortages.

What regulatory change affects laboratories most?

The US FDA’s 2024 rule on laboratory-developed tests introduces significant compliance costs and tighter oversight.

Page last updated on: