Lidocaine Hydrochloride Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 739.57 Million |

| Market Size (2031) | USD 965.03 Million |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

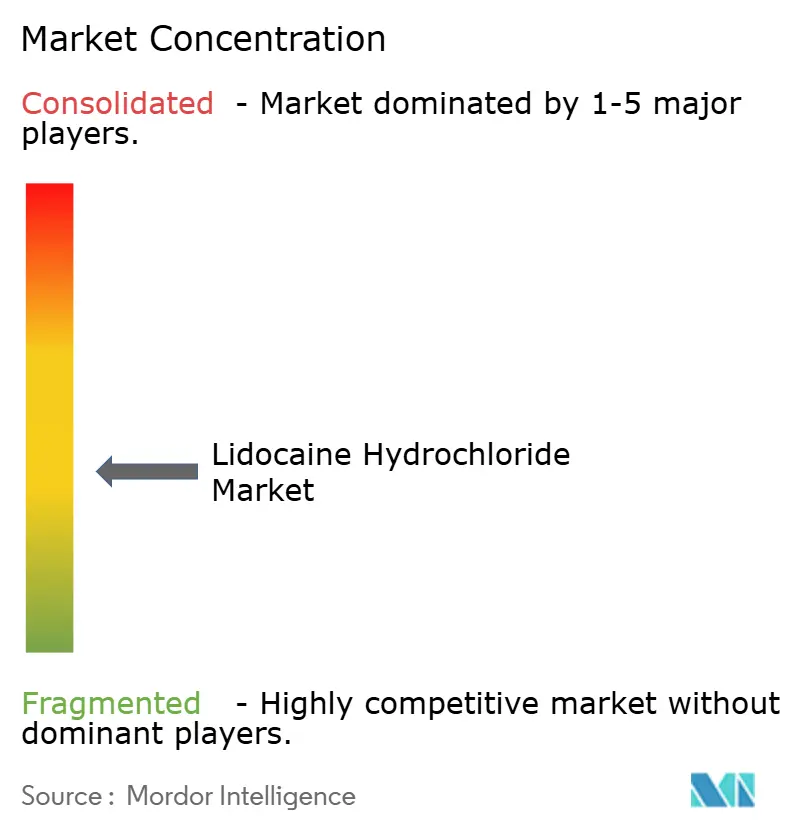

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lidocaine Hydrochloride Market Analysis by Mordor Intelligence

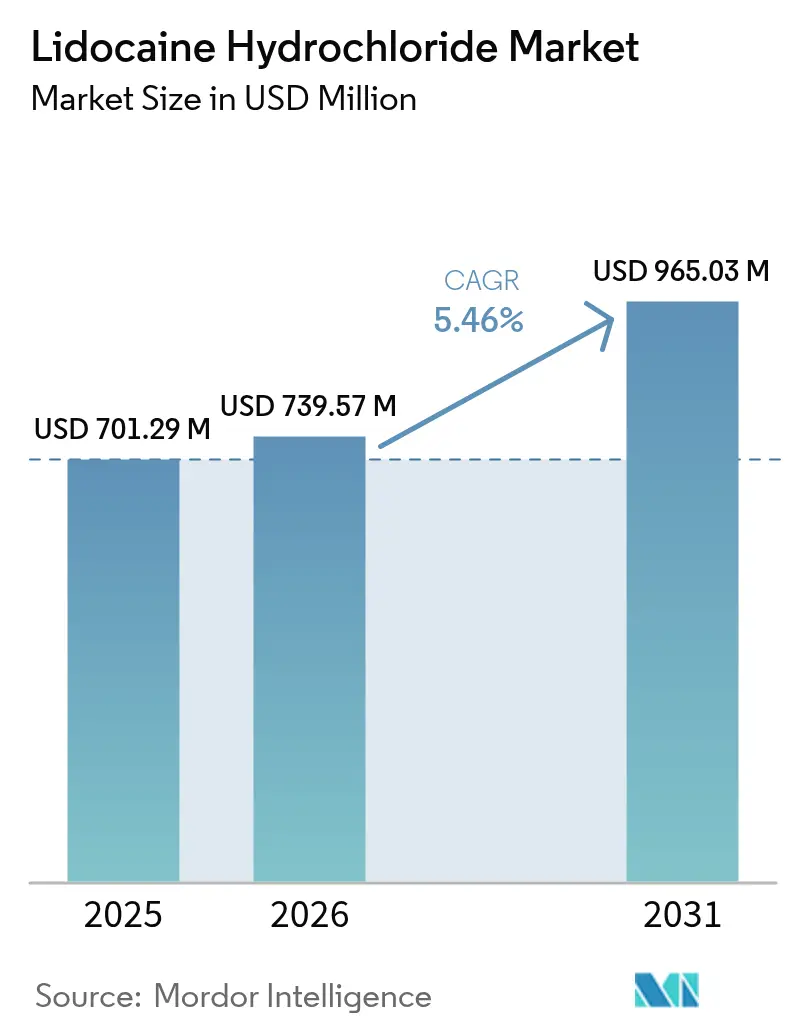

The Lidocaine Hydrochloride Market size is expected to grow from USD 701.29 million in 2025 to USD 739.57 million in 2026 and is forecast to reach USD 965.03 million by 2031 at 5.46% CAGR over 2026-2031.

Consistent demand for a dependable local anesthetic across surgical, dental, and pain-management settings underpins this steady expansion. Growth is reinforced by the shift toward minimally invasive procedures, rising elective surgery volumes, and an expanding base of neuropathic-pain patients who benefit from topical formulations. Competitive intensity is moderate; incumbents rely on broad distribution networks while new entrants exploit supply disruptions. Regulatory approvals of novel delivery systems such as low-dose high-bioavailability transdermal patchesare broadening therapeutic options and stimulating product innovation across the lidocaine hydrochloride market.

Key Report Takeaways

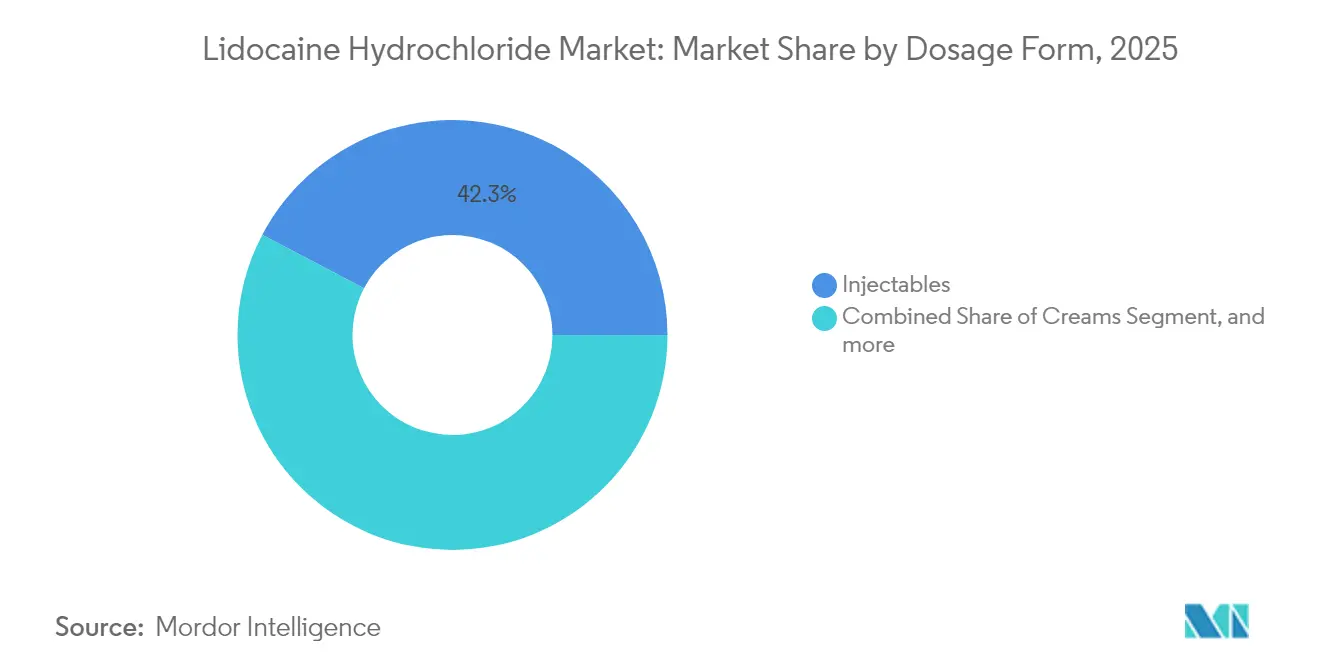

- By dosage form, injectables held 42.28% of the lidocaine hydrochloride market share in 2025, whereas patches are projected to post the quickest 7.33% CAGR to 2031.

- By application, dental procedures accounted for 36.12% of the lidocaine hydrochloride market size in 2025, while post-herpetic neuralgia treatment is set to expand at a 9.47% CAGR.

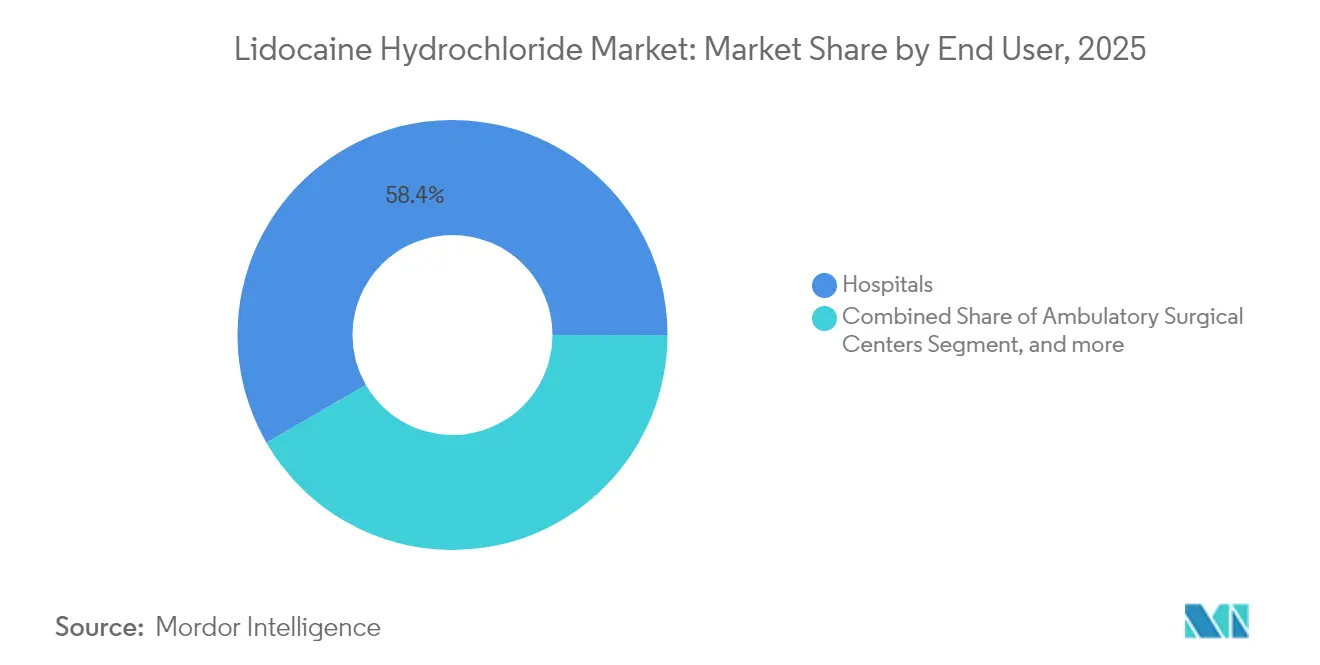

- By end user, hospitals led with 58.35% of the lidocaine hydrochloride market share in 2025; specialty clinics represent the fastest-growing channel at 10.58% CAGR.

- By geography, North America contributed 37.05% revenue in 2025, whereas Asia-Pacific is forecast to grow at an 8.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lidocaine Hydrochloride Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Volume of Minimally-Invasive & Elective Surgeries | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Increasing Prevalence of Ventricular Arrhythmias | +0.8% | Global, aging populations in developed markets | Long term (≥ 4 years) |

| Growing Adoption of Topical Lidocaine Patches for Neuropathic Pain | +1.5% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rapid Expansion of Dental Procedures in Emerging Economies | +1.1% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| FDA Approvals of Low-Dose High-Bioavailability Transdermal Systems | +0.7% | North America, with regulatory spillover to EU | Short term (≤ 2 years) |

| 3D-Printed Personalized Lidocaine Delivery Devices | +0.3% | North America & Europe, early-stage adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Minimally Invasive & Elective Surgeries

Outpatient laparoscopic and endoscopic procedures increasingly rely on lidocaine for swift onset anesthesia that supports same-day discharge. Evidence shows that intravenous lidocaine reduces postoperative pain scores by 40% and lowers opioid consumption in abdominal surgery patients.[1]Tian-Long Ji, “Intravenous Lidocaine Significantly Reduces Postoperative Pain,” Journal of Clinical Medicine, mdpi.comHospitals incorporate the drug into enhanced-recovery pathways to manage costs tied to extended admissions. As ambulatory surgical centers compete on throughput, demand for predictable analgesia augments the lidocaine hydrochloride market. Suppliers able to guarantee continuous injectable supply capture share in regions where elective surgery volumes rebound most rapidly following pandemic-related slowdowns.

Increasing Prevalence of Ventricular Arrhythmias

Cardiovascular disease burdens an aging demographic, elevating the clinical use of lidocaine as a class IB anti-arrhythmic. Emergency departments value its rapid onset and brief half-life for controlled rhythm stabilization, particularly during percutaneous coronary interventions. Updated protocols recommend lidocaine to mitigate arrhythmia-related complications in cardiac catheterization labs.[2]Vault Pfizer Medical Affairs, “Lidocaine Injection in Cardiac Arrhythmia Management,” Pfizer, pfizer.com Broader availability of advanced cardiac care in emerging economies further enlarges the drug’s addressable patient pool.

Growing Adoption of Topical Lidocaine Patches for Neuropathic Pain

Opioid-sparing treatment strategies accelerate uptake of 1.8% and 5% lidocaine patches among chronic-pain patients. The FDA cleared the first generic 1.8% transdermal system in March 2025, spurring price competition that widens access.[3]U.S. Food and Drug Administration, “Warning Letter to TKTX Company,” fda.gov Clinical data confirm significant pain-score reductions when patches are combined with spinal cord stimulation for elderly post-herpetic neuralgia cases. These factors drive sustained double-digit unit growth for the segment, particularly in North America and Western Europe.

Rapid Expansion of Dental Procedures in Emerging Economies

Rising disposable income enables greater uptake of preventive and cosmetic dentistry in Asia-Pacific and Latin America. Lidocaine aerosols, creams, and computer-controlled injection systems improve chairside experience and encourage repeat visits. A 5.6% lidocaine aerosol cut periodontal-procedure pain scores in a 167-patient trial without adverse events. Nanocapsule-based gels that extend mucosal analgesia further differentiate premium offerings, helping manufacturers protect margins in price-sensitive markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse CNS and cardiovascular toxicity risks | -0.9% | Global, heightened regulatory scrutiny in developed markets | Short term (≤ 2 years) |

| Generic price erosion and reimbursement pressures | -1.3% | North America and Europe, spreading to emerging markets | Medium term (2-4 years) |

| Volatility in xylidine raw-material supply | -0.8% | Global, concentrated impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Stricter solvent-emission regulations in API manufacturing | -0.5% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse CNS & Cardiovascular Toxicity Risks

The therapeutic window for lidocaine remains narrow, prompting regulators to monitor high-strength topical products marketed for cosmetic procedures. In March 2024 the FDA warned a manufacturer marketing unapproved 40% lidocaine creams, underscoring safety vigilance. Clinicians must screen for hepatic impairment and methemoglobinemia risk, which can limit dosing flexibility. These concerns moderate uptake in elective aesthetic settings where alternatives with wider margins of safety are gaining traction.

Generic Price Erosion & Reimbursement Pressures

Patent expiry across multiple formulations invites rapid commoditization. Payers increasingly mandate step therapy favoring low-cost generics, compressing branded-product margins. The first generic 1.8% patch received approval in March 2025 and triggered immediate formulary switches at US pharmacy benefit managers. Similar dynamics are expected in Europe once exclusivity lapses, curbing revenue growth for originator companies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Patches Lead Innovation Wave

The injectables sub-segment represented 42.28% of the lidocaine hydrochloride market size in 2025 owing to its indispensability in surgical and emergency settings. Supply shortages from incumbent producers such as Pfizer and Fresenius Kabi prolonged lead times, yet facilitated share gains for agile suppliers introducing ready-to-use vials early in 2024. A second growth engine stems from patches, which post a 7.33% CAGR through 2031 as physicians and patients gravitate to non-invasive regimens. The March 2025 generic approval slashed unit costs by 35% within three months in the United States, broadening payer coverage and accelerating uptake. Creams, gels, and the emerging class of thermoresponsive nanogels sustain demand in dermatology and oral-wound applications where extended release is advantageous. Nanotechnology-enhanced formats employing polymeric nanocapsules improve mucosal permeation and represent a future competitive differentiator for manufacturers seeking margin defense.

Hospital pharmacies still prioritize multidose ampoules for versatility, but ambulatory surgical centers increasingly order pre-filled syringes to minimize preparation time and medication errors. The lidocaine hydrochloride market maintains a strong pipeline of 3D-printed dissolvable microneedle arrays tailored for post-operative incision care. This personalized-delivery trend widens the innovation moat for technology-driven brands and mitigates pure price competition in the injectables space. At the same time, patches address adherence challenges in chronic neuropathic pain, presenting the most compelling opportunity for volume expansion across the lidocaine hydrochloride industry.

By Application: Post-Herpetic Neuralgia Drives Growth

Dental care captured 36.12% of 2025 revenue thanks to high procedure volumes in both developed and emerging markets. Clinics favor computer-controlled injection systems that cut onset time by 15 seconds on average, thus increasing chairside throughput. Post-herpetic neuralgia is forecast to generate the highest 9.47% CAGR, reflecting aging populations and updated pain-management guidelines promoting topical lidocaine ahead of systemic therapies. Combination regimens pairing 5% patches with spinal cord stimulation lowered mean pain scores from 2.7 to 1.6 in a 90-day study of elderly patients.

Cardiology preserves a steady niche where lidocaine’s dual anti-arrhythmic and anesthetic properties streamline intra-procedural care. Dermatology faces tighter oversight after multiple warnings on high-strength compounded creams, yet growth persists for aerosol formats that minimize cross-contamination. The lidocaine hydrochloride market size for oncology-adjunct wound care remains small but exhibits robust clinical-trial activity as nanocarrier formulations advance through Phase II studies.

By End User: Specialty Clinics Capture Growth

Hospitals controlled 58.35% of 2025 volume, anchored by high surgical throughput and continuous emergency-department demand. However, specialty clinics are projected to advance at a 10.58% CAGR to 2031 as payers favor outpatient care pathways. Chronic pain practices embrace long-acting patches that reduce opioid reliance, while dermatology and dental clinics invest in computer-guided injectors to enhance patient comfort.

Supply-chain fragility highlighted by 2024 shortages prompted the American Academy of Dermatology Association to establish a Drug Shortage Workgroup aimed at securing alternate distributors. Clinics increasingly sign direct-ship agreements with nimble manufacturers to protect inventory levels, a move that redistributes bargaining power within the lidocaine hydrochloride industry and fosters tighter integration between manufacturers and point-of-care providers.

Geography Analysis

North America retained a 37.05% revenue share in 2025, underpinned by mature reimbursement systems and high elective-surgery volumes. The region also became the launchpad for the first generic 1.8% patch, which broadened access for Medicare and commercial-plan beneficiaries. United States drug-shortage data reveal recurring deficits in lidocaine vials, prompting hospital groups to diversify suppliers and renegotiate long-term contracts.

Europe follows with consistent demand driven by aging populations and harmonized regulatory pathways that expedite new-format approvals. German ambulatory centers reported a 12% rise in outpatient arthroscopic procedures in 2024, directly lifting lidocaine consumption. The lidocaine hydrochloride market size attributed to France and Italy shows resilient mid-single-digit growth as pain-management guidelines endorse topical routes before opioids.

Asia-Pacific delivers the highest 8.34% CAGR, reflecting broader insurance coverage and investment in domestic API capacity. India’s Bulk Drug Parks scheme incentivizes local production of key intermediates to curb dependency on imports. China’s biopharmaceutical sector benefits from provincial subsidies that lower facility-setup costs, enabling quick scale-up of lidocaine API manufacturing and reinforcing supply security for regional formulators.

Latin America experiences moderate expansion as Brazil and Mexico upgrade surgical infrastructure and dental-tourism inflows increase. Regulatory agencies are adopting fast-track reviews for critical anesthetics to avert shortages, a policy that favors established dossier holders. Middle East and Africa remain nascent but record double-digit volume gains where private hospital chains open day-surgery centers in urban hubs. Increasing public-sector procurement budgets for essential anesthetics establish a baseline demand that suppliers leverage for further penetration of premium topical formats.

Regulatory Landscape

Regulation of lidocaine hydrochloride is grounded in established quality standards and evolving bioequivalence expectations for generics across dosage forms. In the United States, the FDA maintains product-specific guidance for lidocaine formulations used in ANDA development, and in February 2026 it issued draft product-specific guidance that tightened analytical expectations, including a validated method with a 0.20 ng/mL lower limit of quantification for plasma characterization. Compendial requirements from major pharmacopoeias (USP/EP/BP) continue to set assay and impurity limits for lidocaine hydrochloride and lidocaine injection, supporting a compliance baseline for global manufacturers supplying sterile injectables and topical systems.

Safety enforcement and trade policy are also shaping operating conditions. FDA scrutiny of high-strength topical products marketed outside approval pathways has been reflected in enforcement actions tied to toxicity risks, raising the compliance bar for topical creams and compounded formats used in cosmetic settings. On the supply side, an April 2026 White House action establishing a 10% tariff rate on certain patented pharmaceuticals and associated pharmaceutical ingredients imported from the United Kingdom adds a variable procurement and sourcing consideration for companies with transatlantic supply chains, alongside the broader WTO-centered framework that governs tariff and access provisions for health-related products.

Competitive Landscape

The lidocaine hydrochloride market is moderately competitive and consists of several major players. Pfizer, Teva, Fresenius Kabi, and Hikma collectively account for major share of global injectable volumes, but intermittent production interruptions dilute their dominance. Sintetica US capitalized on the February 2024 shortage, supplying alternative vial sizes and capturing premium pricing for on-time deliveries. Aveva’s 2025 generic patch approval intensifies price competition in transdermal formats, compelling originators to accelerate next-generation product launches.

Strategic focus is shifting to differentiated delivery platforms. Multiple firms pilot microneedle arrays that localize lidocaine to the dermis and shorten onset to under one minute. The University of Nottingham showcased multi-material inkjet 3D printing for personalized tablets embedding lidocaine with anti-arrhythmic co-therapies, foreshadowing bespoke dosage regimens. Nanotechnology partnerships with academic labs are common as companies pursue prolonged release profiles without excipients that trigger allergic reactions.

Supply security emerged as a pivotal competitive lever after several FDA-listed manufacturers projected resupply of key injectable SKUs only in January 2026. Players with vertically integrated API capacity or diversified geographic sourcing mitigate this risk and secure multiyear purchase commitments from hospital group purchasing organizations. Marketing strategies emphasize clinical-economic evidence that reduced opioid use and shorter recovery times can offset premium pricing on advanced lidocaine systems. Intellectual-property filings reveal a tilt toward combination products blending lidocaine with anti-inflammatory or antioxidant agents that can extend label life and diversify revenue streams beyond traditional anesthetic indications.

Lidocaine Hydrochloride Industry Leaders

Pfizer Inc.

Merck KGaA

Teva Pharmaceutical Industries Ltd.

Amneal Pharmaceuticals Inc.

Endo International plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A gap remains in supply resilience and compliant capacity for lidocaine hydrochloride API and sterile finished-dose production, particularly given recurring injectable shortages referenced in hospital procurement and manufacturer resupply timelines. Recent CDMO investments reflect active buyer pull for U.S.-based drug-substance manufacturing: in July 2026, Evonik announced a USD 100 million, five-year modernization of its Tippecanoe Labs API manufacturing facility in Lafayette, Indiana, aimed at upgrading production assets and automation to improve reliability. For lidocaine suppliers and marketers, this type of modernization can help support qualification of alternate sources, shorten lead times for critical anesthetic SKUs, and improve tender competitiveness with group purchasing organizations and hospital systems.

Product-format differentiation also continues to offer pathways for value capture beyond commoditized injectables, especially in transdermal and topical systems aligned with opioid-sparing care pathways. The March 2025 FDA approval of the first generic 1.8% lidocaine transdermal system broadened access and intensified price competition, which in turn increases incentives to pursue delivery improvements (including higher-bioavailability low-dose systems, microneedle arrays, and other controlled-release approaches already referenced in the market pipeline). At the same time, tighter scrutiny of high-strength unapproved topical creams is pushing manufacturers toward clearly labeled, guideline-aligned products and unit-dose or facility-friendly presentations that reduce medication-handling variability in hospitals, specialty clinics, and dental settings.

Recent Industry Developments

- May 2026: Pfizer announced availability of a new NDC (00409-3178-01) for Lidocaine Hydrochloride and Epinephrine Injection 1%, USP, in a 200 mg/20 mL multiple-dose glass fliptop vial. The packaging and code update supports standardized hospital ordering and inventory management at a time when injectable continuity has been a competitive differentiator. It also reinforces Pfizer's presence in core procedural-anesthesia use cases where buyers value dependable sourcing and familiar presentations.

- September 2025: MEDRx USA, Inc. received FDA approval for Bondlido (lidocaine topical system), 10%, for relief of pain associated with post-herpetic neuralgia. A higher-strength topical system expands the approved transdermal toolkit in neuropathic pain, a segment where topical lidocaine adoption is rising under opioid-sparing strategies. The approval intensifies differentiation and pricing dynamics among patch and topical-system suppliers competing for formulary placement.

- October 2024: Imbed Biosciences received FDA 510(k) clearance to market Microlyte Ag/Lidocaine, an antimicrobial wound dressing integrating lidocaine for painful skin wounds. The combined silver-based antimicrobial function and local anesthetic delivery targets wound-care settings where pain control and infection management are handled together. The clearance broadens lidocaine use in device-enabled wound applications, adding an adjacent demand stream beyond classic injectables and consumer topicals.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the yearly revenue generated from finished human-use pharmaceutical products where lidocaine hydrochloride is the main active ingredient, across common dosage forms such as injectables, creams, gels, patches, and aerosol solutions.

Scope exclusions: Combination products where lidocaine hydrochloride is not the principal active ingredient, and industrial-grade API volumes sold for chemical synthesis, are not counted.

Segmentation Overview

- By Dosage Form

- Creams

- Patches

- Injectables

- Gels

- Aerosol Solutions

- Other Dosage Forms

- By Application

- Heart Arrhythmia

- Dental Procedures

- Epilepsy Management

- Post-Herpetic Neuralgia

- Cosmetic Dermatology

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with setting boundaries, terminology, and the likely demand pool for lidocaine hydrochloride across therapeutic and procedure settings. For this, we review public sources such as the US FDA drug databases and labeling updates, the World Health Organization essential medicines lists, and US CDC and OECD health statistics to understand procedure intensity and care access patterns.

To ground supply and trade signals, we also refer to sources such as UN Comtrade and national customs publications, along with peer-reviewed literature indexed in resources like PubMed for usage patterns and formulation trends. Company annual reports, investor presentations, and regulated filings are used to sanity check shifts in mix and channel emphasis, and selected paid subscriptions for company financials, patent databases, and shipment-level trade visibility are used where public disclosures are thin. These sources are illustrative, and other public references were also consulted for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary inputs are collected through expert interviews and structured surveys with a mix of manufacturers, distributors, formulators, and healthcare-facing stakeholders, so that our assumptions match purchasing and usage behavior in real channels. Since this is a global market, insights are validated across major regions to check differences in product mix, pricing corridors, and availability, and then the results are used to confirm the final demand and ASP assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 48% |

| Mid tier: 47% | Functional/Unit leaders: 32% | EMEA: 31% |

| Smaller Players: 17% | Managers: 56% | Americas: 21% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where treatment and procedure demand signals are converted into a revenue pool, then filtered by how often lidocaine hydrochloride based products are used in those settings. In practice, we map the demand to indicators such as outpatient and inpatient procedure volumes, dental visit intensity, arrhythmia-related acute care incidence, and topical anesthetic usage patterns, which are then tied to typical dose forms and pack sizes.

To keep the totals realistic, selective bottom-up approximations are used as cross-checks, including sampled price per unit by dosage form, channel mix splits between Rx and OTC where relevant, and supplier and distributor feedback on run-rate demand. Where direct volume visibility is limited in smaller countries, the gaps are handled using proxy ratios such as per-capita procedure rates, healthcare spend, and formulary availability, followed by manual review so no single proxy drives the full result.

For forecasting, we use scenario analysis supported by simple multivariate relationships, where the trajectory is guided by expected changes in procedure volumes, access to outpatient care, generic competition and pricing pressure, and product mix shifts toward topical versus injectable forms. The final growth path is checked against what interviewees expect for utilization and pricing, and then carried into the year-by-year forecast.

Data Validation & Update Cycle

Validation is done through several checks so the final output is not driven by a single data series. We compare modeled revenue with independent signals such as procedure growth, trade and supply patterns, and observed pricing ranges by dosage form, and then outliers are reviewed before sign-off.

If a major variance shows up, analysts re-check the definition boundary, re-contact select experts, and re-run sensitivity around the assumptions that caused the jump, such as ASP timing or country weighting. The report is refreshed annually, and interim updates are triggered when material events occur, including regulatory changes, sharp currency movements, or unusual pricing shifts. Before delivery, a final pass is completed so the version a client receives reflects the most current inputs available.

Mordor Intelligence's Lidocaine Hydrochloride Market Size Compared Against Other Published Estimates

Published market sizes for lidocaine hydrochloride can look far apart even when the growth story sounds similar, because the underlying counting rules and timing choices differ. Differences usually come from what is being counted (API versus finished products), which channels are included, and how prices are converted into USD over time.

Another driver is the refresh cycle and how pricing is treated in the model, because this market can move due to generic price compression and country-level currency effects. When price per unit is refreshed by dosage form and validated with recent channel checks, and the currency conversion is aligned to the stated value year, the total tends to stay closer to the real purchasing environment, which is the approach applied in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 739.57 M (2026) | |

| Global Consultancy A | USD 596.40 M (2026) | Uses a narrower monetization lens that appears closer to pharmaceutical-grade lidocaine hydrochloride supply and selected applications, which can undercount finished-formulation revenues and Rx/OTC channel breadth in multi-country coverage. |

| Industry Publisher B | USD 847.25 M (2025) | Anchors the estimate on a different value year and can reflect broader inclusion across dosage forms and indications without the same year-matched USD conversion and ASP refresh cadence, which shifts the total upward when pricing and mix are changing. |

The comparison mainly shows that scope boundaries and year alignment explain most of the spread. Once the counted product set is clearly limited to finished human-use products, and the pricing and currency timing are kept consistent with the stated year, the market size becomes easier to replicate and interpret for planning.

Key Questions Answered in the Report

How large is the lidocaine hydrochloride market in 2026?

The market is valued at USD 739.57 million in 2026 and is projected to reach USD 965.03 million by 2031 at a 5.46% CAGR.

Which region grows fastest through 2031?

Asia-Pacific records the highest 8.34% CAGR due to wider healthcare access, domestic API incentives, and rising elective-procedure volumes.

What dosage form is expanding most rapidly?

Patches post the fastest 7.33% CAGR as generic launches lower costs and clinical guidelines favor opioid-sparing topical analgesia.

Why are specialty clinics gaining share?

Payers shift procedures to outpatient settings; specialty clinics adopt advanced lidocaine delivery systems that improve patient comfort and throughput, driving a 10.58% CAGR.

What are the main restraints on market growth?

Safety concerns over CNS and cardiovascular toxicity, generic-driven price erosion, and raw-material supply volatility.

Page last updated on: