Thermal Inkjet Printheads Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.15 Billion |

| Market Size (2030) | USD 1.44 Billion |

| Growth Rate (2025 - 2030) | 4.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermal Inkjet Printheads Market Analysis by Mordor Intelligence

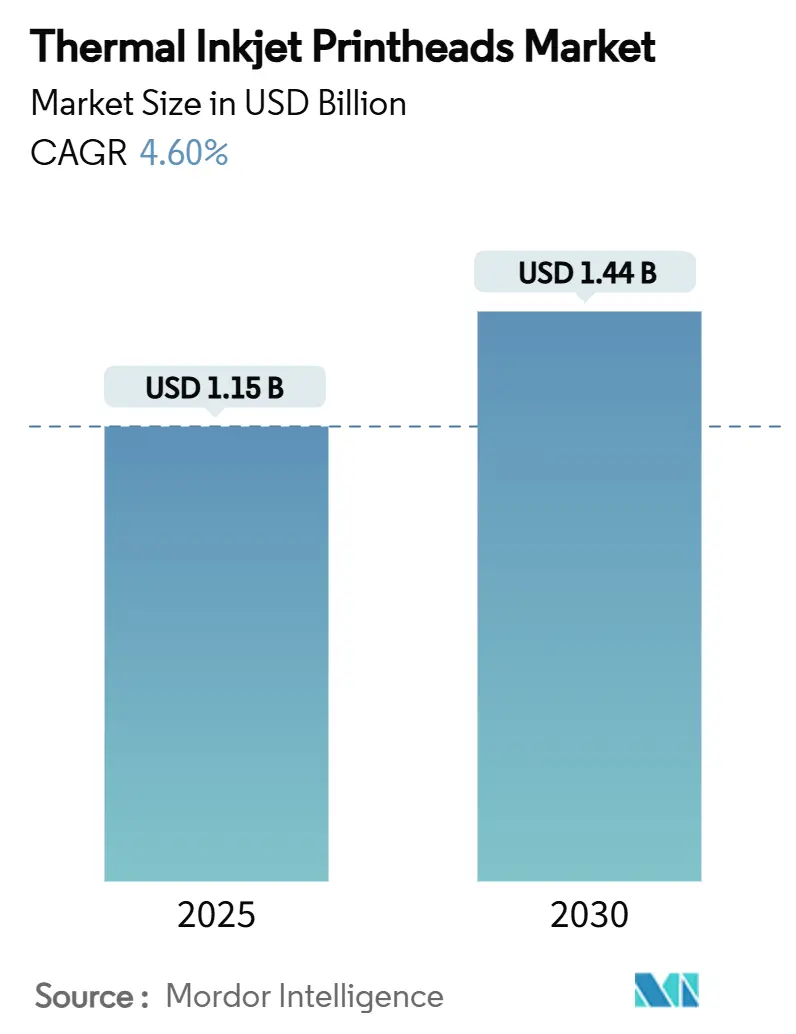

The thermal inkjet printheads market size reached USD 1.15 billion in 2025 and is projected to advance to USD 1.44 billion by 2030, reflecting a 4.60% CAGR. Growth is rooted in the technology’s shift from office printers to high-speed industrial lines where late-stage customization, serialized coding, and sustainable inks are strategic priorities. Higher throw-distance heads, such as HP’s March 2025, ThermaCore release, now let thermal inkjet compete directly with continuous inkjet on fast packaging conveyors. Brand-owner demand for ≥1201 dpi graphics on premium cartons is accelerating high-resolution adoption, while UV-curable inks gain ground as regulations tighten around volatile organic compounds. Simultaneously, MEMS miniaturization is enabling print bars to embed inside fillers and inspection stations, trimming line footprint and elevating code placement accuracy. Competitive dynamics, therefore, hinge on balancing performance with total cost of ownership, particularly in sectors such as pharmaceuticals and craft beverages, where downtime and design flexibility carry heavy weight.

Key Report Takeaways

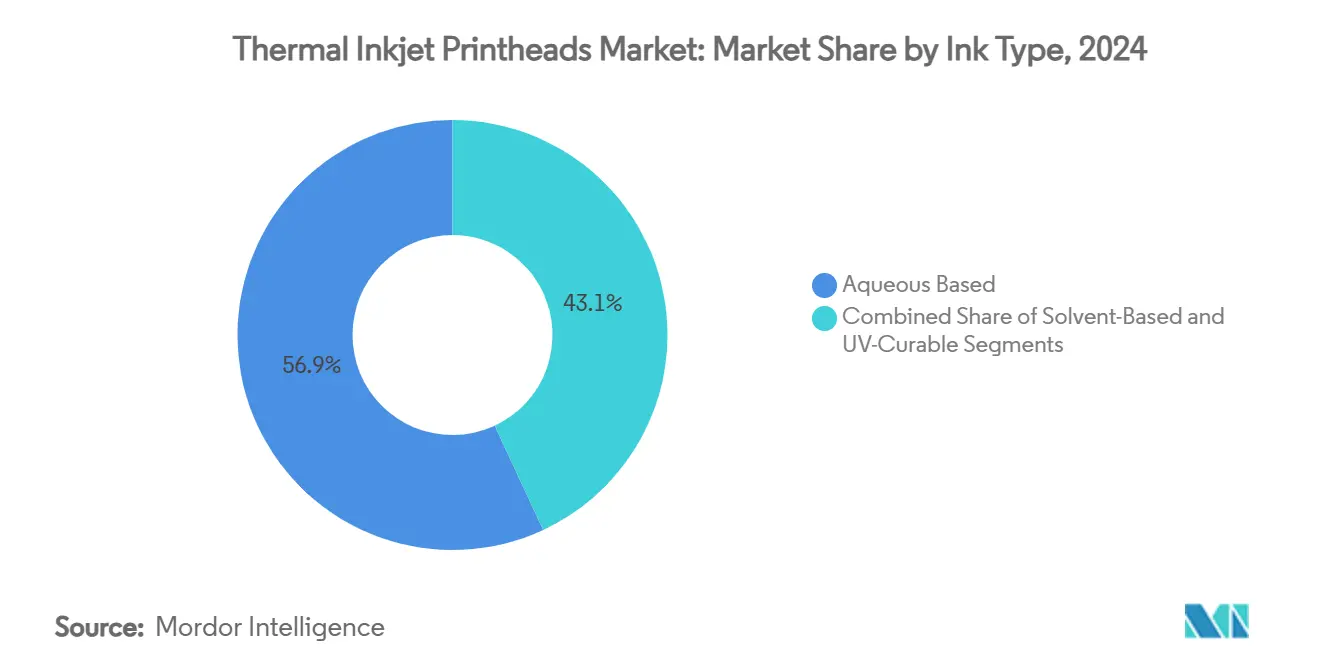

- By ink type, aqueous formulations led with 56.93% of the thermal inkjet printheads market share in 2024.

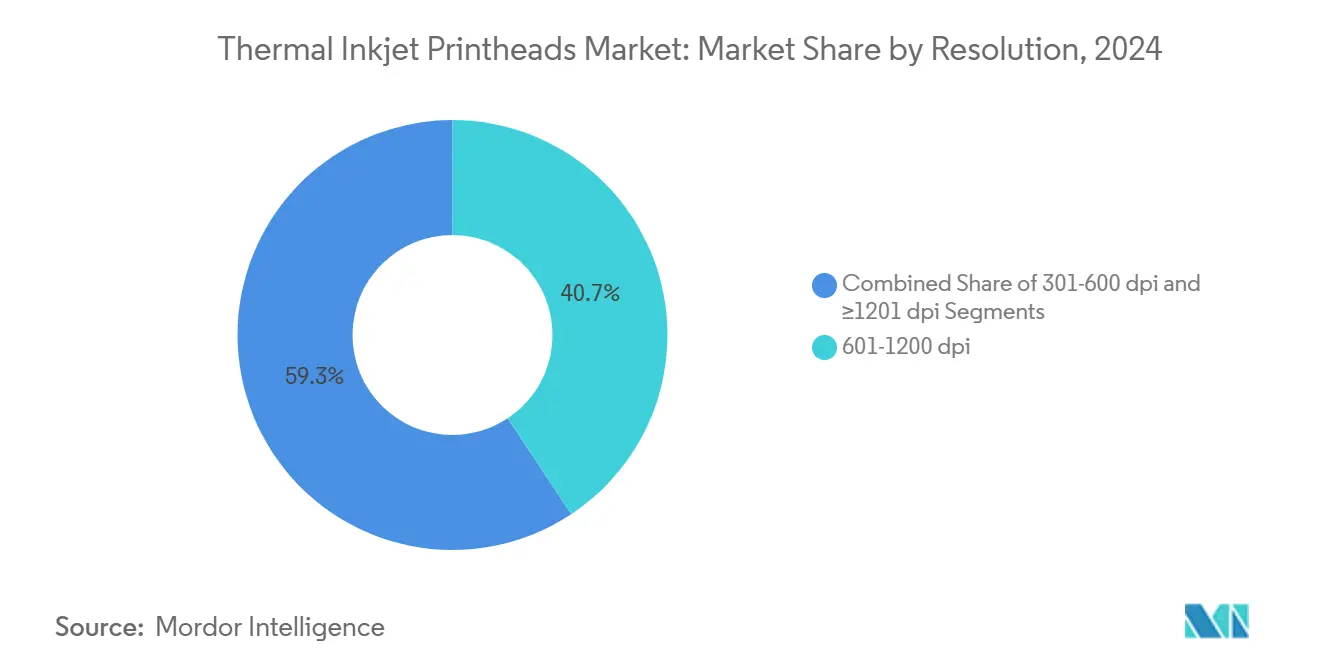

- By resolution, the 601–1200 dpi segment captured 40.69% of the thermal inkjet printheads market size in 2024.

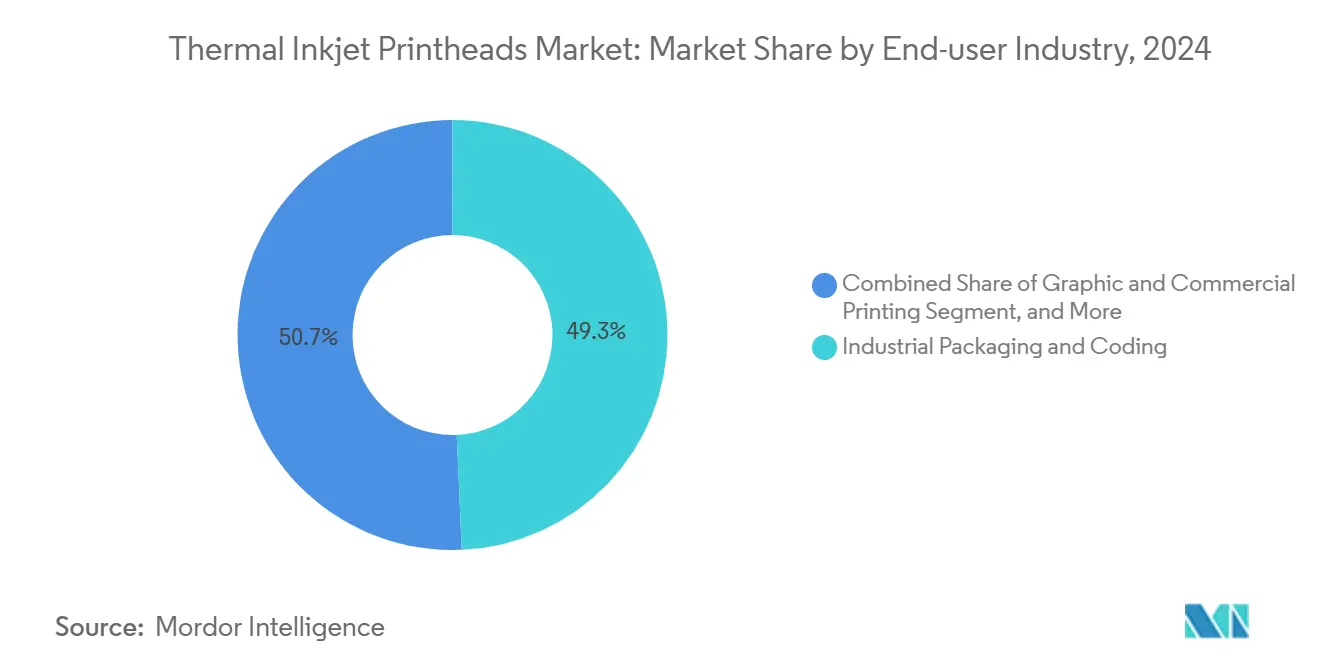

- By end-user industry, industrial packaging & coding held 49.31% of the thermal inkjet printheads market share in 2024.

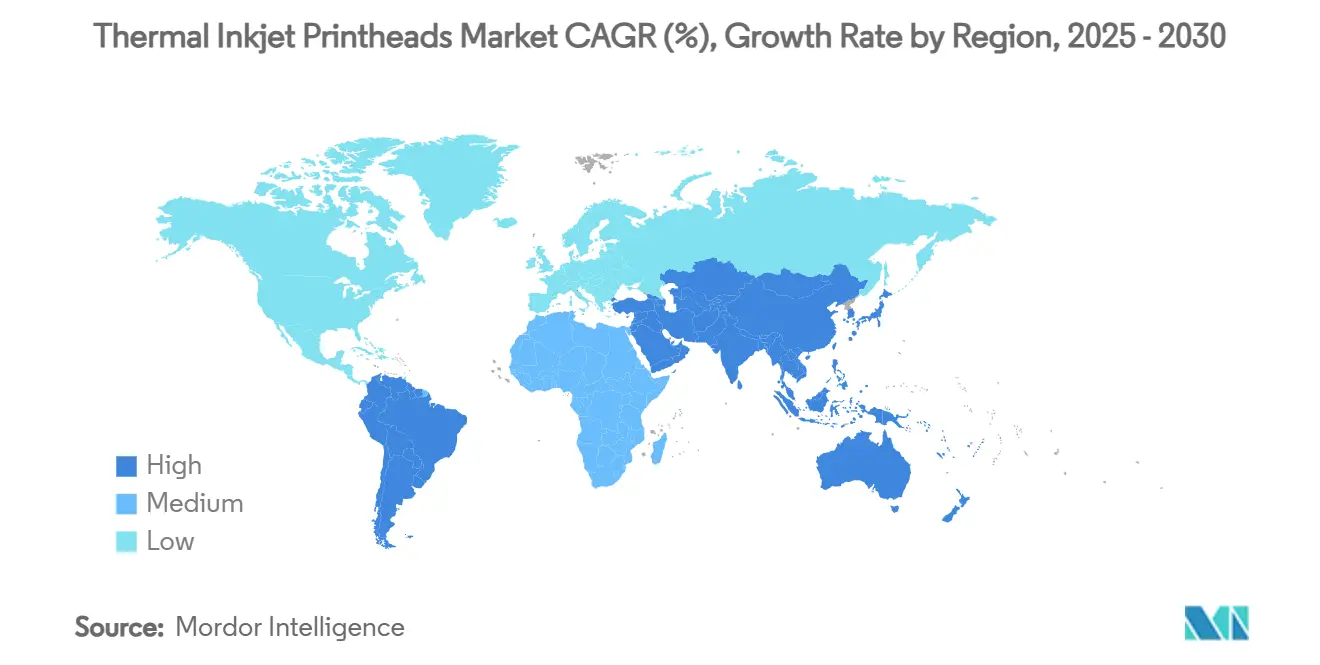

- By geography, Asia-Pacific commanded 43.74% share of the thermal inkjet printheads market size in 2024.

Global Thermal Inkjet Printheads Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Late-stage variable data printing for e-commerce cartons | +1.2% | North America & Europe; emerging Asia-Pacific | Medium term (2-4 years) |

| Mandatory pharma serialization & UDI | +1.5% | Global; strongest in North America, Europe & Japan | Short term (≤ 2 years) |

| Craft-beverage short-run colour labels | +0.4% | North America, Europe, Australia | Short term (≤ 2 years) |

| MEMS print bars integrated into packaging lines | +0.9% | Global; early Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Brand Owner Shift to Late-Stage Variable Data Printing

E-commerce fulfillment models now favor printing after the purchase is confirmed so brands can tailor graphics, languages, and QR codes per order. Thermal inkjet complements this shift because its digital workflow eliminates plates and allows instant artwork changes at line speed. Packaging studies indicate that personalized cartons lift social-media “unboxing” shares by 72% and brand recall by 40% over generic versions. Canon’s dual-printhead array, announced in October 2024, prints background imagery and variable data in a single pass, cutting pre-printed carton inventory and supporting just-in-time packaging. As fulfillment centers scale, the thermal inkjet printheads market gains recurring demand for high-resolution units capable of fast artwork swaps without operator intervention.

Mandatory Pharma Serialization & UDI Requirements

Global drug-safety laws mandate unique identifiers on every saleable unit, elevating code legibility standards. Thermal inkjet excels by producing 300–600 dpi alphanumeric and DataMatrix codes that vision systems read reliably at up to 109 m/min in sterile environments [1]Videojet Technologies, “Videojet 8520 and Wolke m610 Touch,” videojet.com. Pharmaceutical plants value the printhead’s sealed cartridge design, which avoids the messy maintenance routines associated with continuous inkjet solvents. Integrated vision verification closes the loop between printing and inspection, reinforcing thermal inkjet’s standing in regulated packaging lines and fueling the thermal inkjet printheads market across North America, Europe, and Japan.

Craft-Beverage & Micro-Brewery Label Evolution

Small-batch breweries release seasonal SKUs that change artwork frequently, driving interest in digital, on-demand label production. Thermal inkjet delivers photo-quality, CMYK output without plates, helping brewers shrink label inventories by 60% and reduce obsolescence risk[2]Domino Printing, “Guide to Coding,” domino-printing.com . Vivid graphics reinforce premium positioning while accommodating regulatory data such as ABV and batch codes in a single pass. These capabilities draw new entrants into the thermal inkjet printheads market as craft producers prioritize flexibility and branding agility.

Line-Footprint Reduction via MEMS Integration

Micro-electromechanical systems bring nozzle arrays and driver electronics onto silicon, producing slim, rigid bars that mount directly inside fillers or inspection modules. By eliminating standalone coders and conveyor transfers, factories cut line length and improve overall equipment effectiveness. IEEE’s 2024 roadmap cites functional integration as a pathway to 30% footprint savings and tighter code placement tolerances. Over the long term, such architecture will reshape capital-spending decisions and channel greater revenue to vendors able to embed MEMS-based heads, sustaining momentum in the thermal inkjet printheads market.

Restraints Impact Analysis*

| Restraint | Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adhesion limits of aqueous inks on untreated polyolefins | -0.7% | Global; highest impact Asia-Pacific | Medium term (2-4 years) |

| Thermal-cycle fatigue of resistor heaters | -0.6% | Global | Short term (≤ 2 years) |

| Piezo & electrostatic rivals jetting UV/solvent inks | -0.5% | Europe, North America | Medium term (2-4 years) |

| Humidity/temperature swings causing bubble instability | -0.4% | Asia-Pacific, Middle East, Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Adhesion on Polyolefin Films

Polypropylene and polyethylene films resist wetting by water-based inks because their non-polar surface energy is mis-matched with polar aqueous vehicles. Laboratory analysis confirms inferior adhesion and rub resistance without corona or plasma treatment. While UV-curable chemistry alleviates the issue, many brand owners still favor aqueous formulations for food safety and sustainability, constraining the thermal inkjet printheads market in flexible packaging until pre-treatment costs fall or hybrid inks mature.

Thermal-Cycle Fatigue Challenges

Every firing event pushes resistor heaters above 340 °C before rapid cooling, creating mechanical stress that can shorten component life during 24 × 7 duty cycles. Although material advances have prolonged lifespan, high-throughput lines remain cautious, occasionally selecting piezoelectric inkjet for ultra-long runs. This reliability perception moderates some capital expenditure inside the thermal inkjet printheads market, particularly in industries intolerant of unplanned stoppages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ink Type: UV Formulations Gain Traction

Aqueous inks retained 56.93% share of the thermal inkjet printheads market in 2024, thanks to regulatory preference for low-VOC chemistries, especially in food and pharma applications. The segment benefits from simple cartridge architecture and globally harmonized safety approvals. However, adhesion deficits on non-porous films and demands for faster curing have ignited adoption of UV-curable alternatives, pushing that category to a 6.13% CAGR for 2025-2030. The thermal inkjet printheads market size for UV inks is poised to climb as head makers optimize thermal management to jet higher-viscosity photopolymers.

Recent ink launches underscore this shift. INX International’s plant-derived UV series cut petrochemical usage by more than three million pounds while delivering instant cure on high-speed conveyors. At the same time, solvent formulations, though niche at present, address extreme durability needs on metals and plastics where abrasion or chemical exposure is high. Hybrid chemistries combining water, monomers, and specialty binders are emerging, signaling broader formulation diversity that will support future growth within the thermal inkjet printheads market.

By Resolution: Premium Graphics Propel ≥1201 dpi Adoption

The 601–1200 dpi cohort controlled 40.69% of the thermal inkjet printheads market size in 2024, meeting mainstream needs for barcodes and sharp text without sacrificing production speed. Industrial coders in this range reach line velocities above 700 m/min while maintaining code integrity. Demand for photo-grade graphics, security microtext, and elaborate brand imagery now lifts the ≥1201 dpi bracket, which is expanding at 6.81% annually. For example, Formax’s ColorMax7 achieves 1,600 × 1,600 dpi on labels and envelopes, setting a benchmark for high-definition output.

The 301–600 dpi segment, while less glamorous, remains critical for logistics and secondary packaging where machine readability trumps aesthetics. REA JET HR systems print crisp codes at up to 762 m/min, underscoring that lower resolutions still command substantial volumes. Collectively, resolution segmentation illustrates how users right-size investments, selecting heads that cover quality requirements at the highest attainable throughput and reinforcing the layered demand profile inside the thermal inkjet printheads market.

By End-User Industry: Packaging & Coding Keeps the Lead

Industrial packaging and coding contributed 49.31% of the thermal inkjet printheads market share in 2024, anchored by legislative traceability mandates in pharmaceuticals, medical devices, and food. Wolke m610 printers exemplify how integrated software tools simplify serialization compliance while ensuring 600 × 600 dpi clarity on foil blisters and cartons. Manufacturers value cartridge-based consumables that eliminate pump maintenance, underpinning steady cartridge pull-through revenue for vendors.

Graphic and commercial printing is the fastest-rising user base at 5.48% CAGR because digital workflows are eroding minimum-run thresholds for labels, direct mail, and promotional packaging. Small and mid-scale printers leveraging thermal inkjet sidestep lengthy plate setups, enabling profit on quantities under 1,000 units and sustaining a fresh opportunity pipeline for the thermal inkjet printheads market. Office and consumer replacement heads form a mature but stable channel, where incremental gains stem from higher-yield cartridges and recycling programs that resonate with environmentally conscious buyers.

Geography Analysis

Asia-Pacific held 43.74% of the thermal inkjet printheads market size in 2024, buoyed by China’s electronics supply chain and Japan’s precision-manufacturing heritage. Region-wide initiatives to digitize packaging lines in food and pharma plants support a 6.21% CAGR through 2030. India, highlighted by HP as a “pivotal expansion arena,” is scaling adoption as domestic brands pursue serialized coding standards [3]Packaging South Asia, “Canon’s Dual Printhead Strategy,” packagingsouthasia.com.

North America ranks second, powered by stringent UDI enforcement and the continent’s vibrant craft-beverage scene. Breweries leverage modular colour heads to refresh labels monthly, whereas pharma multinationals deploy vision-verified TIJ coders across multi-shift operations. European plants combine sustainability targets with regulatory oversight, steering investments toward aqueous systems and closed-loop waste reductions. EU directives limiting VOCs further increase the relevance of thermal inkjet over solvent-heavy alternatives, cementing market longevity.

Across South America, the Middle East, and Africa, uptake remains nascent yet accelerating. Zebra Technologies’ 2024 report cites growing adoption in retail and logistics, where barcode labelling underpins supply-chain modernization. Climate variability, however, still challenges bubble stability at conveyor speeds above 100 m/min, prompting buyers to seek ruggedized enclosures and temperature-regulated ink reservoirs. Continued engineering progress aims to unlock broader applications in these emerging territories, extending runway for the thermal inkjet printheads market.

Competitive Landscape

The thermal inkjet printheads market is moderately concentrated. HP, Memjet, and FUJIFILM Dimatix secure leadership through patented nozzle architecture and vertical integration across heads, drivers, and inks. HP’s ThermaCore technology triples throw distance while using 65% recycled plastics, showcasing an eco-performance dual strategy that shapes differentiation. FUJIFILM Dimatix bolstered its Asia-Pacific capacity by 35% in 2025 and launched pharma-oriented heads with embedded vision, underscoring a pivot toward application specialization.

Challengers from China, Vietnam, and Singapore, including RYNAN Technologies and new entrants leveraging outsourced MEMS fabrication, compete primarily on price and cartridge compatibility. Their ascendancy exerts downward price pressure, nudging incumbents to emphasize service bundles and performance guarantees. White-space innovation also flows from collaborations: Domino Printing Sciences integrates bespoke TIJ heads into turnkey coding modules for flexible films, while Xaar’s MEMS-based ImagineX platform aligns print bars with vision cameras to boost accuracy in regulated industries. Cross-licensing of substrate-treatment patents, such as Yahiaoui et al.’s adhesion methods, indicates a maturing intellectual-property environment that balances competitive rivalry with ecosystem growth.

Thermal Inkjet Printheads Industry Leaders

HP Inc.

Memjet Ltd.

Funai Electric Co., Ltd.

Domino Printing Sciences PLC

FUJIFILM Dimatix Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: HP introduced ThermaCore, tripling throw distance and doubling print swath while incorporating 65% recycled plastic in cartridges.

- February 2025: FUJIFILM Dimatix increased Asia-Pacific printhead output by 35% and released vision-verified heads for pharma serialization.

- October 2024: Canon unveiled a dual printhead array that prints background graphics and variable data simultaneously, cutting pre-printed carton use by 25%.

- August 2024: Xaar plc commercialized ImagineX MEMS heads integrated into inspection systems, reducing line footprint by 30%.

Global Thermal Inkjet Printheads Market Report Scope

| Aqueous-based |

| Solvent-based |

| UV-curable |

| 301 - 600 dpi |

| 601 - 1200 dpi |

| ≥1201 dpi |

| Industrial Packaging and Coding |

| Graphic and Commercial Printing |

| Office and Consumer Replacement Heads |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Ink Type | Aqueous-based | |

| Solvent-based | ||

| UV-curable | ||

| By Resolution | 301 - 600 dpi | |

| 601 - 1200 dpi | ||

| ≥1201 dpi | ||

| By End-user Industry | Industrial Packaging and Coding | |

| Graphic and Commercial Printing | ||

| Office and Consumer Replacement Heads | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the thermal inkjet printheads market?

The thermal inkjet printheads market size stood at USD 1.15 billion in 2025.

How fast is the market expected to grow?

The market is forecast to register a 4.60% CAGR, reaching USD 1.44 billion by 2030.

Which ink type holds the largest share?

Aqueous inks led with 56.93% of market share in 2024 due to regulatory acceptance in food and pharma packaging.

Why is Asia-Pacific the leading region?

Strong electronics manufacturing, expanding packaging capacity, and rapid adoption of serialization solutions gave Asia-Pacific 43.74% share in 2024 with a 6.21% forecast CAGR.

What makes ≥1201 dpi printheads attractive?

They deliver premium graphics for luxury packaging and variable data, driving a 6.81% CAGR between 2025-2030.

How are MEMS developments influencing the market?

MEMS-based print bars enable direct integration into packaging equipment, reducing line length and improving code accuracy, thereby opening new revenue streams for suppliers.

Page last updated on: