Piezo-Based Inkjet Printheads Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

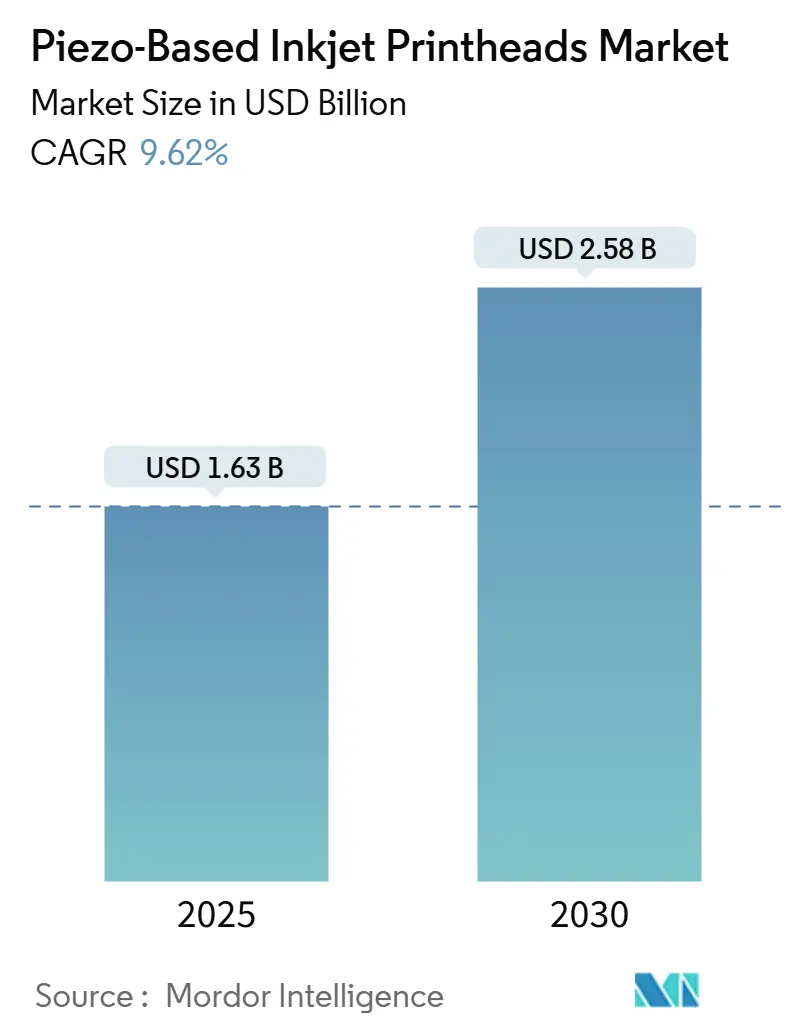

| Market Size (2025) | USD 1.63 Billion |

| Market Size (2030) | USD 2.58 Billion |

| Growth Rate (2025 - 2030) | 9.62% CAGR |

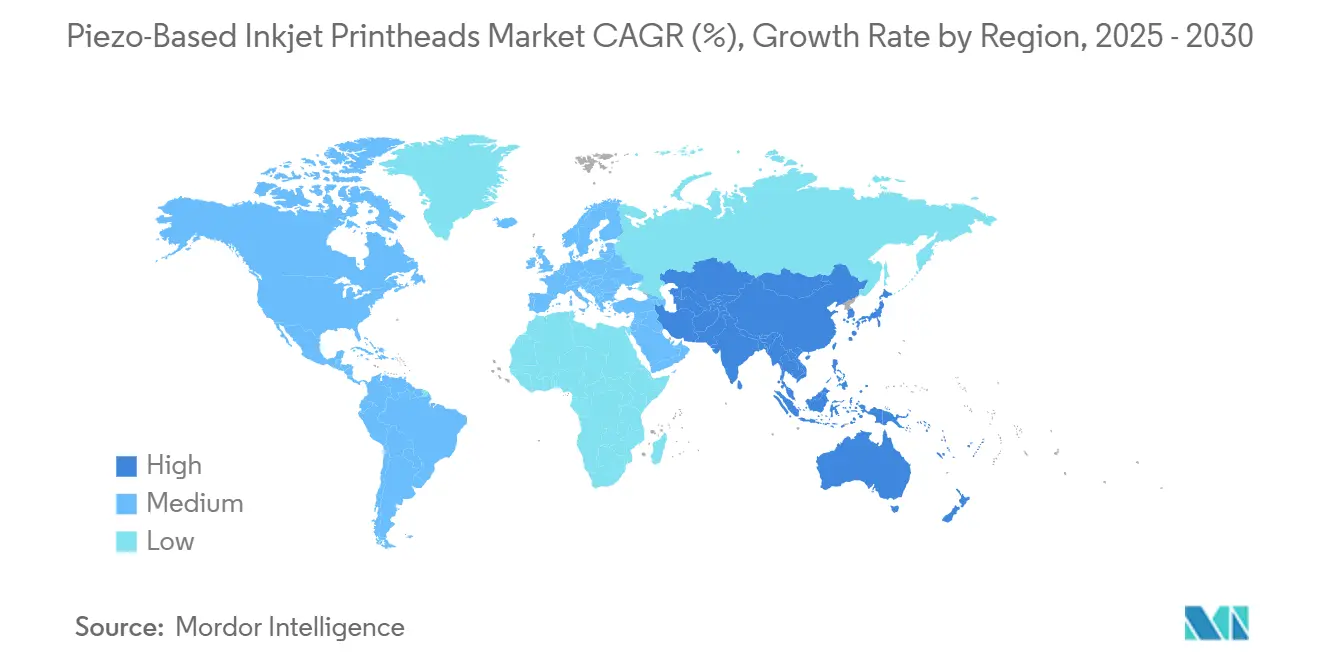

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

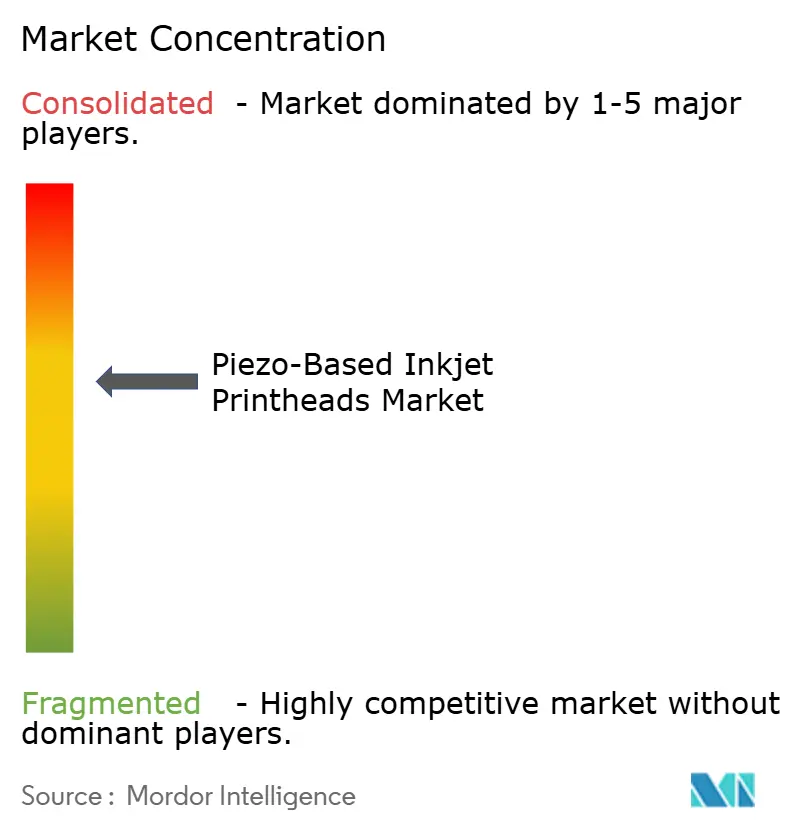

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Piezo-Based Inkjet Printheads Market Analysis by Mordor Intelligence

The Piezo-based inkjet printheads market is valued at USD 1.63 billion in 2025 and is forecast to reach USD 2.58 billion by 2030, reflecting a solid 9.62% CAGR. Momentum stems from the technology’s ability to jet a widening range of inks, especially high-viscosity functional materials that unlock printed electronics and additive manufacturing use-cases. Demand for variable-data coding from e-commerce packaging, rising adoption in flexible electronics, and stricter sustainability standards that favor cold-firing piezo heads are adding further impetus. Suppliers continue to improve nozzle architecture, recirculation, and droplet control, which in turn widens the addressable substrate mix and pushes resolution ceilings higher. Rapid iteration cycles between printhead OEMs and specialty-ink formulators are shortening time-to-market for new industrial workflows and increasing the addressable revenue pool across packaging, décor, biomedical, and semiconductor sectors.

Key Report Takeaways

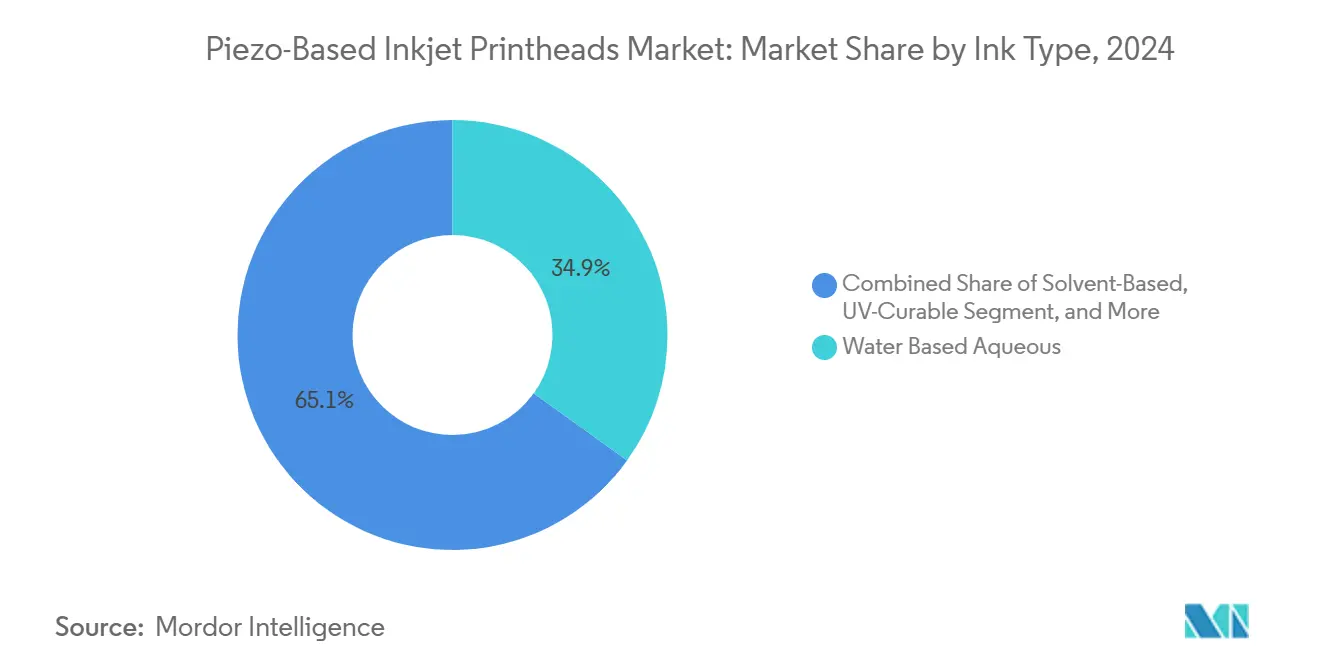

- By ink type, water-based aqueous formulations led with 34.92% of Piezo-based inkjet printheads market share in 2024.

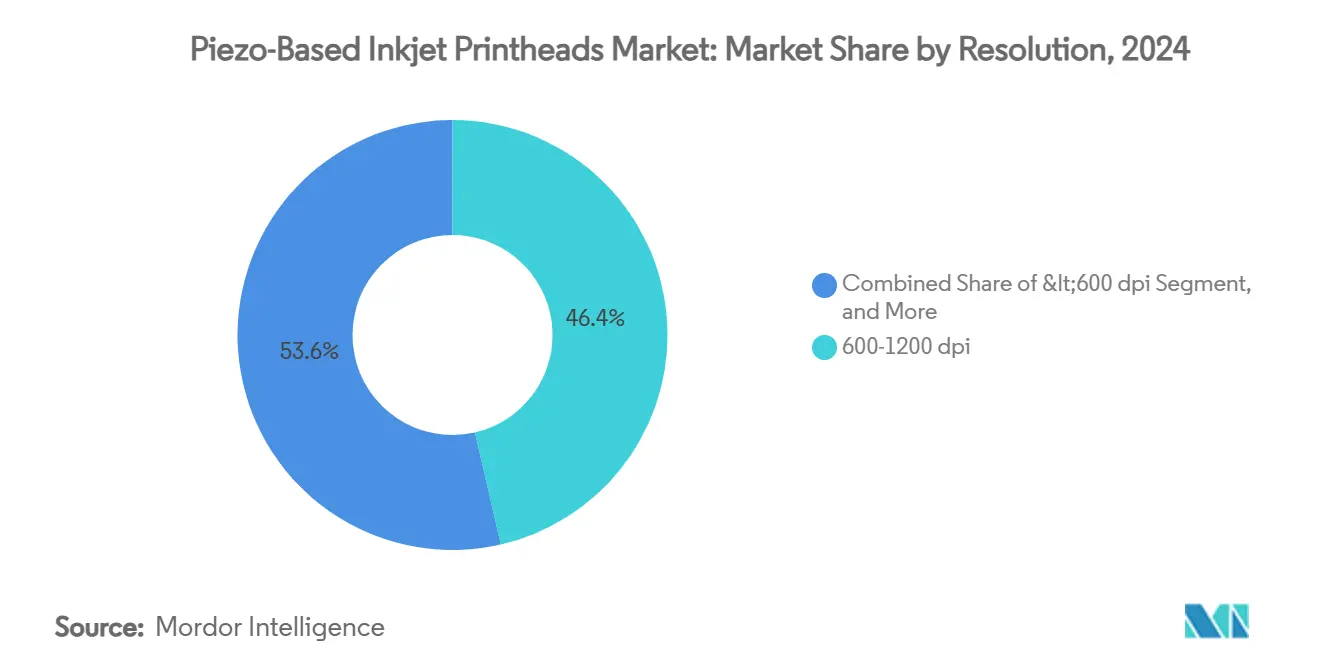

- By resolution, the 600-1200 dpi segment commanded 46.39% of the Piezo-based inkjet printheads market size in 2024.

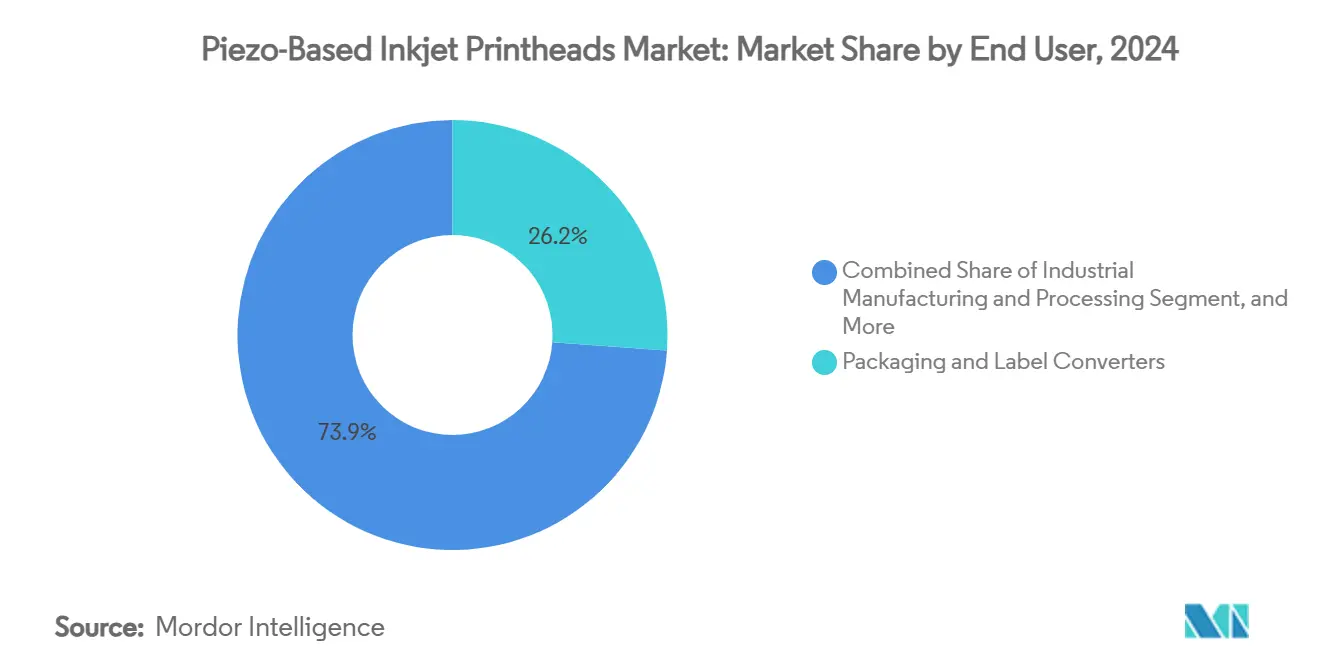

- By end-user industry, packaging & label converters held 26.15% of Piezo-based inkjet printheads market share in 2024.

- By geography, Asia-Pacific captured 44.29% revenue share in 2024.

Global Piezo-Based Inkjet Printheads Market Trends and Insights

Drivers Impact Analysis*

| Driver | %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-commerce packaging driving variable-data coding | +2.1% | Global, led by North America & Asia-Pacific | Short term (≤ 2 years) |

| High-viscosity ink compatibility opens doors in flexible electronics | +2.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| Industrial tile & décor printing demands high-speed bulk piezo | +1.5% | Europe, Asia-Pacific | Medium term (2-4 years) |

| Bioprinting & pharmaceutical need ultra-fine droplet control | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Energy efficiency and ESG compliance favor cold-firing systems | +0.9% | Global, early adoption in Europe | | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce packaging driving variable-data inkjet coding

Expanded online retail flows propel brand owners to print serialized, traceable, and personalized content directly on every parcel. Piezo-based printers deliver crisp codes at more than 100 m/min while handling recycled corrugate without surface pretreatments. Integrated software pulls SKU, batch, and logistics data in real time, enabling opportunistic marketing messages and secure anti-counterfeit graphics. The capability improves last-mile visibility, reduces label inventory, and supports greener pack designs by eliminating extra inserts.[1]Xaar plc, “Annual Report and Financial Statements 2023,” xaargroup.com

High-viscosity ink compatibility opens doors in flexible electronics

Next-generation printheads now jet materials above 25 cP and some beyond 90 cPwithout satellite droplets, enabling direct deposition of conductive silver pastes and dielectric polymers on polyimide or PET. This simplifies circuit fabrication, trims chemical etching steps, and aligns with pick-and-place automation. Wearables, IoT sensors, and low-power displays benefit most as designers embed traces on odd-shaped films that conventional lithography cannot process.

Industrial tile & décor printing demands high-speed bulk piezo

Recirculating nozzle arrays keep abrasive ceramic pigments homogeneously suspended, slashing clog-related downtime. Lines running over 70 m/min produce marble-like finishes with variable drop-size texturing, letting factories pivot from mass volumes to bespoke runs in days. The switch lowers water, glaze, and inventory costs relative to screen printing while complying with tightening emissions rules in Europe.

Bioprinting & pharmaceutical applications require ultra-fine droplet control

Piezo actuation delivers picoliter-scale dosing that arranges living cells, growth factors, or active APIs with sub-50 µm precision. Tissue scaffolds, dissolvable microneedle arrays, and pediatric dosage films emerge as early commercial beneficiaries. Researchers report reliable viability retention above 90% post-jetting and fewer cross-contamination risks versus contact dispensing[3]Source: Prasanta K. Ghosh, “Prospects of Emerging 3D Bioprinting Technologies,” MGM Journal of Medical Sciences, journals.lww.com.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory risk from RoHS pressure on lead-based PZT | -1.3% | Europe; global supply implications | Medium term (2-4 years) |

| Ink fouling with UV-white and metallic inks heightens downtime | -0.8% | Global | Short term (≤ 2 years) |

| Satellite-Droplet Defects with Metallic Nano-Ink Jetting in PCB Lines | -0.6% | Asia-Pacific, North America | Short term (≤ 2 yrs) |

| Rising Availability of Sub-Micron CIJ Alternatives in Pharma Coding | -0.4% | Global, with concentration in North America & Europe | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Regulatory risk from RoHS and export controls on lead-based PZT

Lead zirconate titanate remains the benchmark piezo ceramic yet contains more than 58% lead by weight. European regulators are re-examining existing exemptions, while certain rare-earth inputs face geopolitical export scrutiny. Printhead OEMs fast-track potassium-sodium-niobate and bismuth-based alternatives, but material fatigue and lower coercive fields necessitate redesigned multilayer stacks, longer driver pulses, and modified bonding pastes all adding cost and qualification hurdles[3].

Ink fouling with UV-white and metallic inks increases downtime

Titanium-dioxide-rich whites and aluminum-flake metallics exhibit elevated sedimentation rates, shortening mean-time-between-cleaning events by up to 60%. Even recirculating heads suffer pigment packing at idle unless pressurized agitation and sub-micron filters are in place. Enhanced nozzle-plate coatings and on-carriage ultrasonics mitigate build-up but introduce incremental capex and service complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ink Type: high-viscosity formulations redefine possibilities

High-viscosity functional inks captured momentum with an 11.31% CAGR outlook, signalling appetite for conductive, dielectric, and bio-active layers in printed electronics and life-science workflows. The Piezo-based inkjet printheads market size for this cohort reached USD 0.42 billion in 2024 and benefits directly from printheads capable of jetting up to 98 cP. Water-based aqueous inks retained top ranking due to eco-compliance and broad compatibility with packaging and textile substrates. Hybrid platforms now mix UV, aqueous, and nano-metallic channels within one carriage, giving converters day-one flexibility to print decorative, functional, and serialized data in a single pass.

Continued R&D into rheology modifiers and nanoparticle dispersants improves jet stability and shelf life, encouraging brand owners to migrate from solvent to water or bio-based carriers. Specialty suppliers deliver silver, copper, graphene, and CNT inks in ready-to-print formats that achieve bulk resistivities approaching sputtered films once sintered. As binder chemistries evolve, conductivity thresholds improve even at drop volumes below 10 pL, supporting fine-line deposition vital for high-density interconnects and antenna arrays.

By Resolution: precision drives application expansion

The 600-1200 dpi tranche offers the best trade-off between throughput and definition, explaining its 46.39% share of the Piezo-based inkjet printheads market in 2024. Variable drop-size algorithms create apparent resolutions nearly double the native nozzle pitch by overlapping 6 pL and 15 pL drops to smooth tonal transitions in packaging graphics and décor laminates. At the upper end, >1200 dpi devices post an 8.63% CAGR as security printing, micro-electronics, and bioprinting call for micron-grade accuracy. The Piezo-based inkjet printheads market size for this high-resolution tier is forecast to double by 2030 as alignment tolerances tighten across semiconductor back-end processes.

Meanwhile, <600 dpi heads remain indispensable for high-speed coding, timber marking, and post-press personalization where contrast and adhesion matter more than fine detail. Innovations in throw distance let these lower-resolution heads mount several centimeters away from uneven surfaces yet deposit droplets with ±25 µm placement accuracy, minimizing line stoppages for height calibration.

By End-User Industry: electronics manufacturing drives growth

Electronics and PCB manufacturers form the fastest-expanding customer group, with a 13.62% CAGR projected for 2025-2030 as piezo inkjet systems move conductive inks, resistors, and dielectric layers directly onto boards and flexible films. Recent printhead and silver-paste advances have delivered line widths below 20 µm while maintaining high conductivity, approaching mainstream production tolerances. The shift removes photo-masking and chemical etching steps, which speeds prototyping, lowers material use, and cuts wastewater in small-batch runs. As device designers embrace additive layouts, demand for heads that can jet high-viscosity functional fluids continues to rise, propelling revenue growth within the broader Piezo-based inkjet printheads market.

Packaging and label converters kept the largest 2024 slice at 26.15% of Piezo-based inkjet printheads market share by adopting the technology for decorative graphics, serialization, and emerging smart-pack features. Industrial manufacturing, textile, and wide-format graphics operators follow, each pushing suppliers toward specialized nozzle geometries and ink paths tuned to their substrates. Office, home, and consumer printer brands now deploy piezo heads in premium models to trim consumable waste. Healthcare and bio-printing adopters, though still niche, are scaling as tissue scaffolds and personalized dosage forms gain regulatory traction. High-viscosity jetting also benefits 3D printing and additive manufacturing, where multi-material parts with graded properties are moving from lab to pilot lines.

Geography Analysis

Asia-Pacific generated 44.29% of 2024 revenue for the Piezo-based inkjet printheads market and is projected to advance at an 8.83% CAGR to 2030. Japan anchors material science and ceramic manufacturing leadership, supporting Seiko Epson, Ricoh, and Kyocera printhead production, while China’s expansive PCB and flexible-display base pulls demand for functional jetting. Subsidized semiconductor fabs in South Korea and Taiwan are specifying inkjet deposition for redistribution layers and under-fill barriers, accelerating regional uptake. Government incentives for digital textile printing in India and Vietnam further broaden market reach by easing duty on imported printheads and water-based inks.

Europe holds the second-largest share driven by stringent carbon-reduction mandates that push analog press operators toward digital workflows. Tile, laminate flooring, and architectural glass plants in Spain and Italy have largely completed the switch to bulk piezo printers, trimming glaze waste by more than 30%. Concurrently, EU green-deal funding supports lead-free piezo research at Fraunhofer and IMEC centers, preparing domestic OEMs for upcoming RoHS restrictions. Eastern European contract printers leverage refurbished Japanese heads to serve localized décor and corrugated board markets, creating a sustainable refurbishment ecosystem.

North America shows robust demand for high-margin sectors such as bioprinting, personalized pharma, and aerospace components. Universities and national labs cooperate with start-ups to commercialize droplet-on-demand deposition of living cells, catalyst pastes, and electrically insulating epoxies for advanced packaging. The US CHIPS Act encourages pilot lines that integrate inkjet with pick-and-place and laser-ablation steps, embedding piezo heads into heterogeneous integration flows. Canada’s pulp-and-paper mills deploy piezo coding lines to replace legacy contact stampers, improving traceability of lumber exports.

The Rest-of-World cohort exhibits rising penetration in Latin America and the Middle East where converters leapfrog directly to piezo digital presses. Brazilian textile clusters deploy water-based heads for short-run sports apparel, while Turkish corrugated plants adopt UV piezo systems to reduce solvent emissions. Gulf petrochemical complexes explore piezo coding for HDPE drum marking, capitalizing on cooler operation that minimizes energy draw in hot climates. As printhead ruggedness improves, deployment in less controlled production environments becomes economically viable.

Competitive Landscape

The Piezo-based inkjet printheads market tilts toward moderate consolidation, with the top six suppliers controlling roughly two-thirds of shipments. Vertical integration from ceramic powder synthesis to ASIC driver boards lets incumbents sustain margin and allocate R&D budgets toward next-generation actuation stacks. Seiko Epson broadened its S3200 and D3000 series to target UV packaging lines, adding recirculation channels that extend mean-time-between-purge cycles. FUJIFILM Dimatix leveraged MEMS fabrication advantages to launch the SKYFIRE range, emphasizing drop volume uniformity for semiconductor wafer applications. Kyocera scaled nozzle length while retaining 1200 dpi native resolution, elevating printhead width to cover wider web paths and reduce carriage count.

Chinese challengers accelerate capacity build-out in Suzhou and Shenzhen, focusing on cost-optimized heads for domestic décor and ceramic use-cases. Strategic alliances with local ink formulators and integrators mitigate IP barriers and shorten application engineering cycles. European specialist Xaar positions its Aquinox platform for aqueous textile workflows where sustainability benefits offset higher ASPs. Partnership models are intensifying: software firms bundle color management, inspection cameras, and AI-driven predictive maintenance, compelling hardware suppliers to embed open APIs and secure data channels. Patent filings indicate growing exploration of electrostatic and acoustic actuation that could disrupt conventional multilayer PZT stacks within the coming decade.

Component shortages during 2023-2024 underscored supply-chain fragility, driving OEMs to dual-source ASIC drivers and piezo powders. Some players secured upstream ceramics through equity stakes in material suppliers, while others signed multi-year take-or-pay agreements to lock in capacity. Sustainability credentials now influence buying decisions; heads with lower firing energy and recyclability scores gain preference among European converters pursuing net-zero roadmaps.

Piezo-Based Inkjet Printheads Industry Leaders

-

Seiko Epson Corp.

-

Konica Minolta Inc.

-

FUJIFILM Dimatix Inc.

-

Kyocera Corp.

-

Ricoh Company Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Kyocera unveiled the KJ4A-EX1200-RC, a 1200 dpi UV head that jets at 81.3 m/min with 64 kHz firing, aimed at label and packaging presses

- January 2025: Epson introduced S3200-U1-2, S3200-U3-2, and D3000-U1R printheads with UV-ink readiness and recirculation, reaching 1200 dpi and boosting reliability for industrial graphics .

- January 2025: : Xaar showcased the Aquinox head for water-based textile printing, cutting energy and water use by up to 60% while sustaining 720 dpi at 100 m/min

- August 2024: Mimaki Engineering debuted TRAPIS pigment transfer, which leverages piezo heads to cut wastewater in textile dyeing

Global Piezo-Based Inkjet Printheads Market Report Scope

| Water-based Aqueous |

| UV-Curable |

| Solvent-Based |

| High-Viscosity Functional Inks |

| Nano-Metallic and Conductive Inks |

| < 600 dpi |

| 600 - 1200 dpi |

| > 1200 dpi |

| Packaging and Label Converters |

| Industrial Manufacturing and Processing |

| Textile and Apparel Producers |

| Commercial Graphics and Wide-Format Service Providers |

| Office, Home and Consumer Printer OEMs |

| Electronics and PCB Manufacturers |

| 3-D Printing / Additive Manufacturing Firms |

| Healthcare and Bio-printing Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| Italy | |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Ink Type | Water-based Aqueous | |

| UV-Curable | ||

| Solvent-Based | ||

| High-Viscosity Functional Inks | ||

| Nano-Metallic and Conductive Inks | ||

| By Resolution | < 600 dpi | |

| 600 - 1200 dpi | ||

| > 1200 dpi | ||

| By End-User Industry | Packaging and Label Converters | |

| Industrial Manufacturing and Processing | ||

| Textile and Apparel Producers | ||

| Commercial Graphics and Wide-Format Service Providers | ||

| Office, Home and Consumer Printer OEMs | ||

| Electronics and PCB Manufacturers | ||

| 3-D Printing / Additive Manufacturing Firms | ||

| Healthcare and Bio-printing Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| Italy | ||

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Piezo-based inkjet printheads market?

The market is valued at USD 1.63 billion in 2025 and is projected to reach USD 2.58 billion by 2030.

How fast is the Piezo-based inkjet printheads market growing?

It is expected to expand at a 9.62% CAGR between 2025 and 2030.

Which region leads global demand for piezo printheads?

Asia-Pacific holds the top position with 44.29% revenue share in 2024 and shows the fastest regional CAGR of 8.83% through 2030.

Which application segment is expanding the quickest?

Electronics & PCB manufacturers are forecast to post the highest CAGR at 13.62% from 2025-2030, driven by demand for printed conductive traces and advanced packaging.

What ink type commands the largest share today?

Water-based aqueous inks lead with 34.92% of 2024 revenue, favored for sustainability and broad substrate compatibility.

What are the main regulatory challenges for suppliers?

Potential RoHS restrictions on lead-based PZT materials pose a −1.3% impact on forecast CAGR and may force a transition toward lead-free piezo ceramics in the medium term.

Page last updated on: