Asia Three Wheeler Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

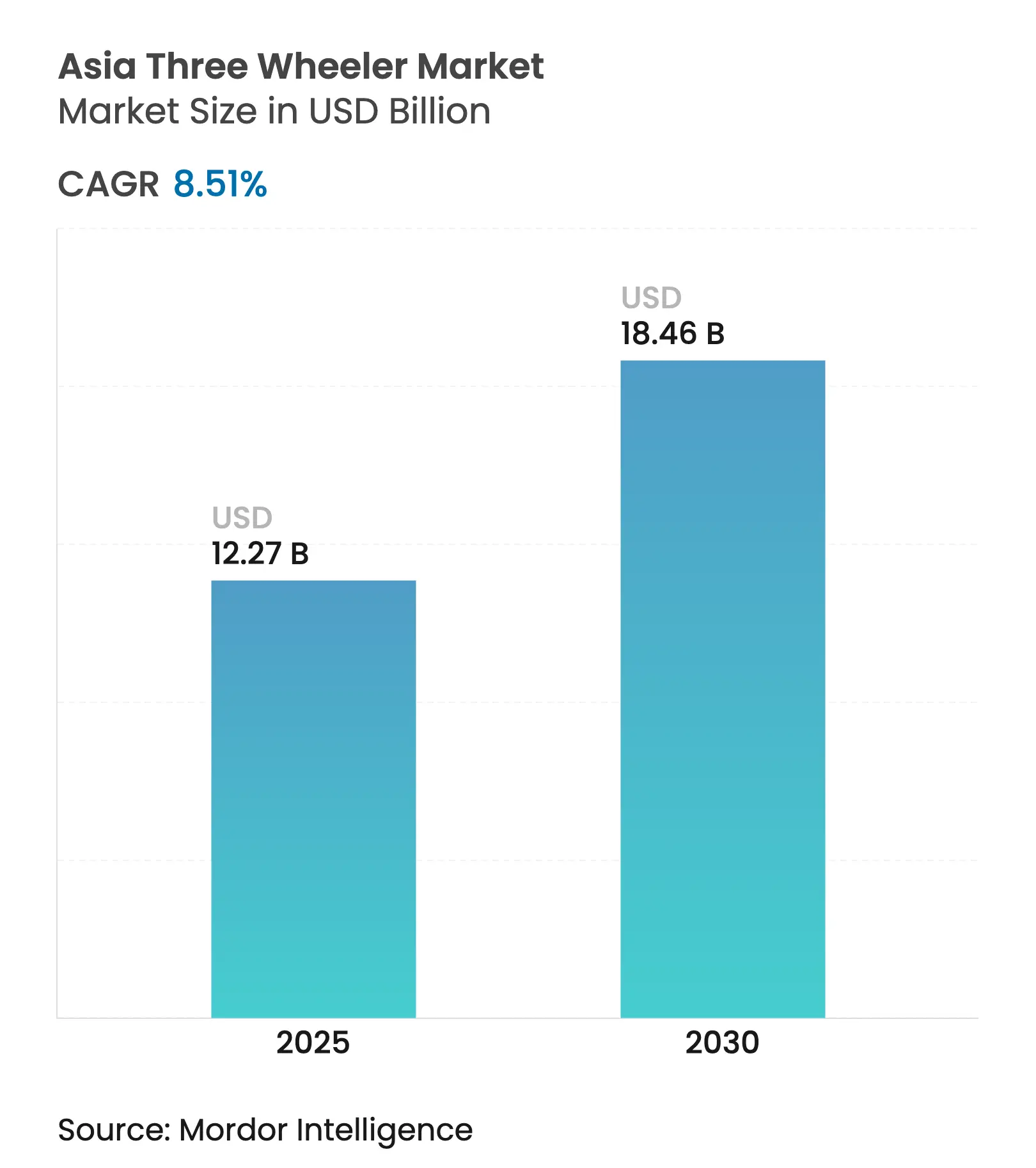

| Market Size (2025) | USD 12.27 Billion |

| Market Size (2030) | USD 18.46 Billion |

| Growth Rate (2025 - 2030) | 8.51 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Asia Three Wheeler Market Analysis by Mordor Intelligence

The Asia Three Wheeler market size stands at USD 12.27 billion in 2025 and is forecast to reach USD 18.46 billion by 2030, expanding at an 8.51% CAGR. Strong policy pushes toward electrification, rapid e-commerce growth, and rising urbanization across tier-2 cities underpin this trajectory. Demand is shifting from internal-combustion dominance to electric powertrains as operators chase lower running costs and governments tighten emissions norms. India’s PM E-DRIVE scheme, Bangladesh’s formalization of its e-rickshaw fleet, and Indonesia’s VAT relief on electric vehicles collectively accelerate adoption. Incumbents respond through strategic investments in battery-swap technology and fleet-as-a-service offerings, while startups leverage purpose-built electric platforms to win share. Challenges persist, however, in the form of patchy charging networks beyond tier-1 cities, volatile lithium-cell supply chains, and uncertain payload regulations that could slow commercial roll-outs.

Key Report Takeaways

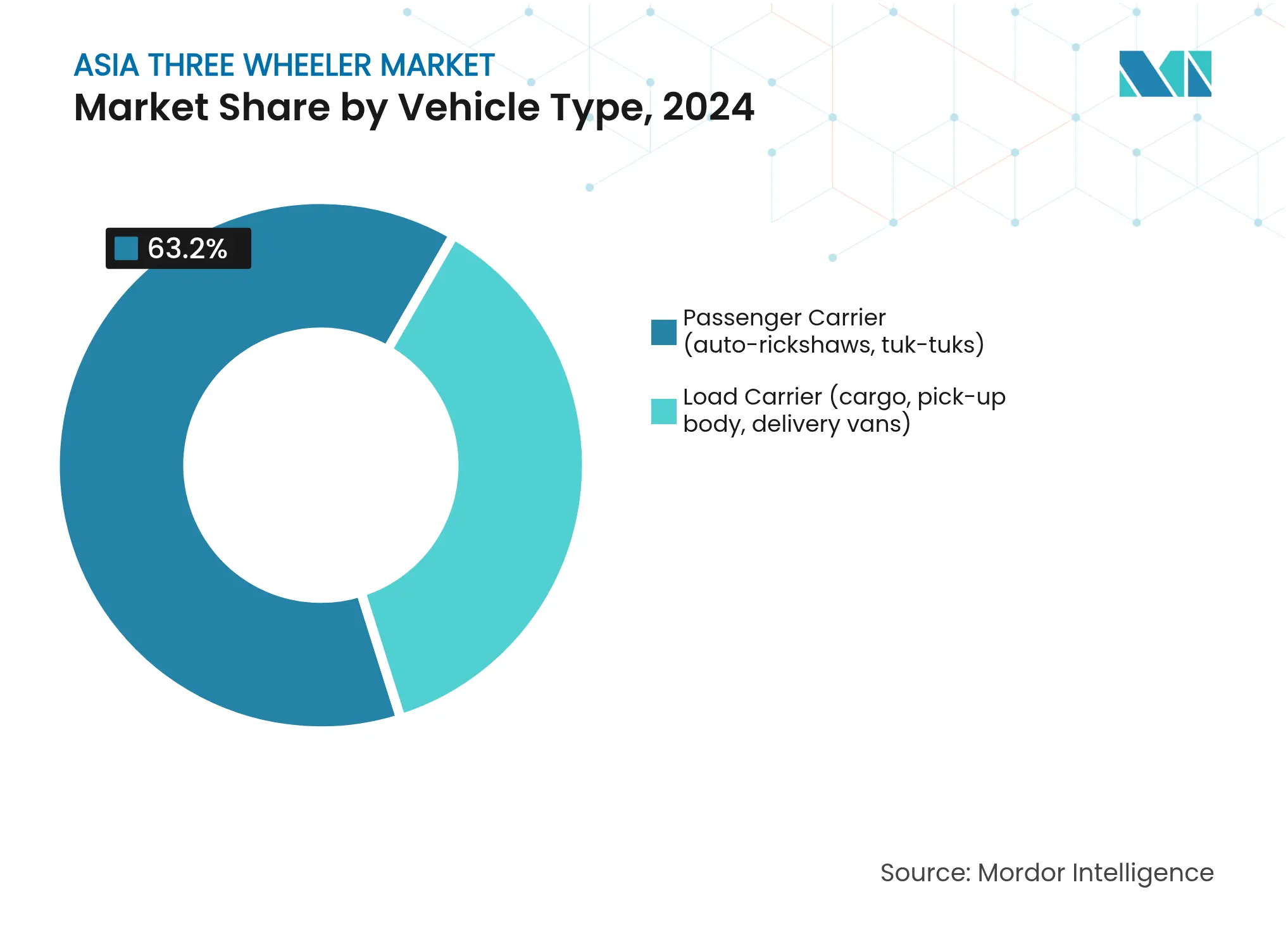

- By vehicle type, passenger carriers led with 63.15% of the Asia Three Wheeler market share in 2024, and advancing at an 8.95% CAGR through 2030.

- By fuel type, petrol retained 44.26% of the Asia Three Wheeler market share in 2024, whereas electric variants recorded the highest projected CAGR at 11.35% through 2030.

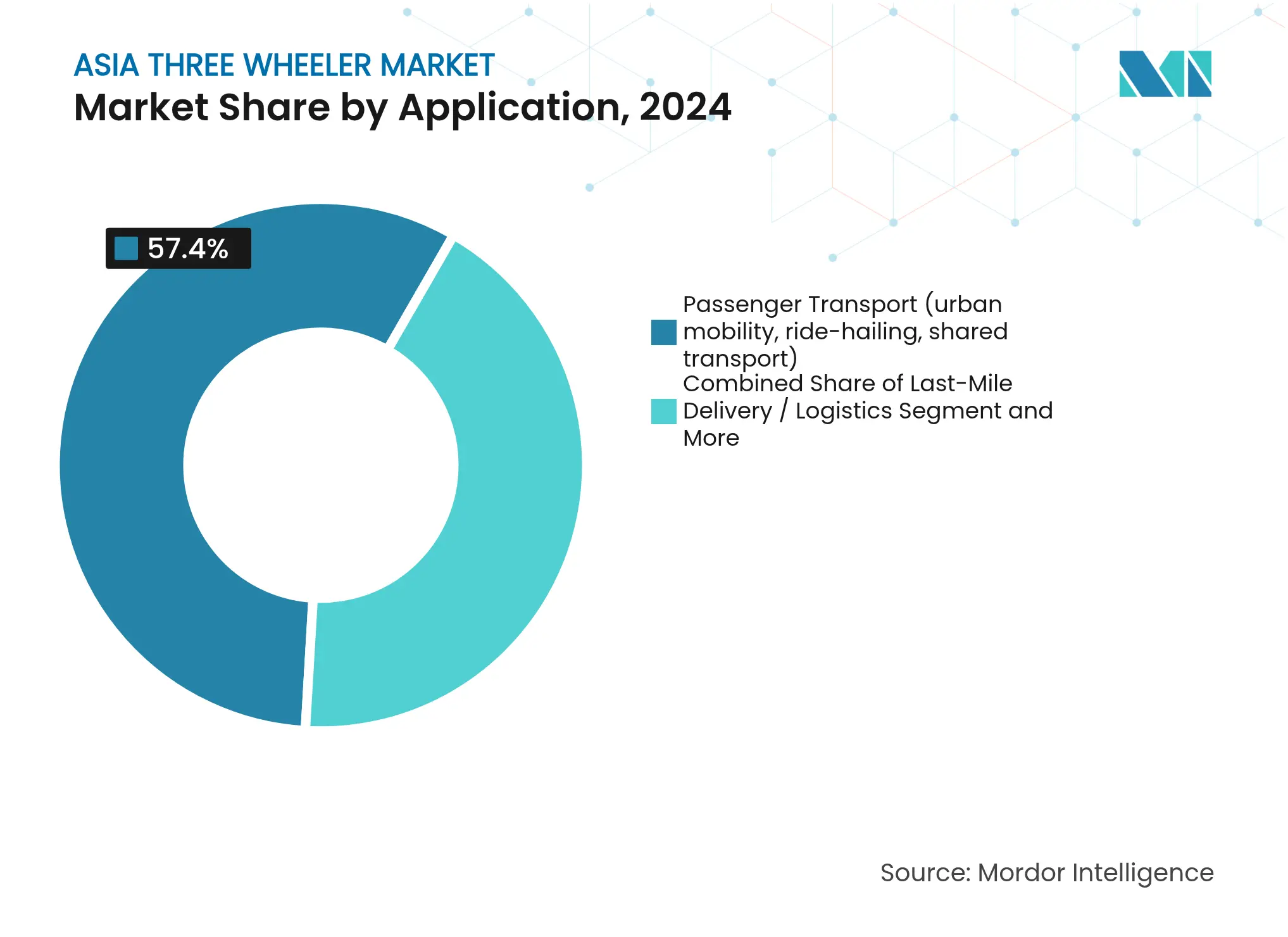

- By application, passenger transport accounted for 57.35% of the Asia Three Wheeler market share in 2024, whereas last-mile delivery/logistics accounted for a 10.24% CAGR by 2030.

- By ownership model, individual owner-drivers controlled 72.16% of the Asia Three Wheeler market share in 2024, whereas fleet operators are expanding at a 9.56% CAGR to 2030.

- By country, India commanded 62.44% of the Asia Three Wheeler market share in 2024; Bangladesh is forecast to post the fastest 9.11% CAGR through 2030.

Asia Three Wheeler Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surging E-Commerce Last-Mile Demand Surging E-Commerce Last-Mile Demand | +2.1% | India, China, Southeast Asia core markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

+2.1%

|

Geographic Relevance

:

India, China, Southeast Asia core markets

|

Impact Timeline

:

Short term (≤ 2 years)

|

Government Incentives for E-3Ws Government Incentives for E-3Ws | +1.8% | India, Indonesia, Thailand, Philippines | Medium term (2-4 years) | |||

Low TCO vs. Other Vehicles Low TCO vs. Other Vehicles | +1.4% | Highest in India, Bangladesh | Long term (≥ 4 years) | |||

Battery-Swap Infrastructure Rollouts Battery-Swap Infrastructure Rollouts | +1.2% | Indian metro cities expanding to tier-2 | Medium term (2-4 years) | |||

Micro-Finance for Driver Ownership Micro-Finance for Driver Ownership | +0.9% | India, Bangladesh, Sri Lanka | Long term (≥ 4 years) | |||

Corporate Zero-Emission Fleet Goals Corporate Zero-Emission Fleet Goals | +0.7% | India, China, Thailand hubs | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Surging E-Commerce Last-Mile Demand

Online retail platforms have multiplied urban delivery runs, lifting three-wheeler utilization as the most maneuverable solution for narrow streets and alleyways. Last-mile logistics surpasses traditional passenger services as Grab, Lalamove, and other platforms scale fleets. Indonesia’s presidential regulation reduces VAT on electric commercial vehicles and enforces local-content rules that favor domestic assembly [1]“Incentives for Battery Electric Vehicles,” Ministry of Industry, Republic of Indonesia, moindustry.go.id. Tier-2 cities see the steepest uptake of two-wheelers, which cannot carry payloads beyond 150 kg, while mini-trucks struggle with congestion and parking. Operators prize three-wheelers for their weather-proof cargo bays and tight turning circles. As volumes grow, e-commerce firms align procurement with electric mandates to cut Scope-3 emissions and meet investor sustainability targets.

Government Incentives for E-3W Adoption

Policy alignment across Asia is unprecedented. India’s PM E-DRIVE sets a battery-electric target for 2/3-wheelers by 2030 [2]“PM E-DRIVE Scheme Details,” Ministry of Heavy Industries, Government of India, heavyindustries.gov.in. The Philippines’ CREVI roadmap waives import duties on electric-vehicle parts, while Thailand’s EV3.5 program offers cash subsidies for battery electric vehicles. Indonesia’s incentives focus on VAT refunds and local-content thresholds. These measures de-risk manufacturer investments in dedicated electric platforms and give fleet operators confidence to sign multi-year lease contracts. By locking in large procurement volumes early, governments compress the learning curve and drive battery-price parity sooner than market forces alone could achieve.

Low TCO vs. Two-/Four-Wheelers

Electric three-wheelers operate at lower costs per km, beating ICE counterparts and closing payback within 18-24 months in high-utilization routes. Insurance, registration, and parking fees are also lower than for mini-trucks. Micro-finance lenders have noticed: new credit products assess daily revenue streams rather than fixed collateral, widening access for driver-owners. The TCO gap widens further as urban fuel prices climb and maintenance intervals shrink on electric drivetrains with fewer moving parts. Small-fleet owners thus pivot from petrol to battery-swap subscriptions, locking in predictable operating costs for multi-shift use.

Battery-Swap Infrastructure Roll-Outs

Battery-as-a-Service models trim upfront vehicle prices, making electric three-wheelers viable for cash-constrained buyers. Omega Seiki Mobility and Exponent Energy launched a 15-minute charge solution in 2024 [3]“Omega Seiki-Exponent Energy Launch 15-Minute Charging 3-Wheeler,” Economic Times, economictimes.indiatimes.com. India’s 2024 battery-swap guidelines ensure interoperability, spurring third-party network build-outs. The hub-and-spoke roll-out begins in metro cores and then radiates to tier-2 cities, mirroring historical LPG-refill patterns. HighSwapp, Charge+Zone, and Sun Mobility are clustering stations around logistics warehouses and transit terminals, ensuring asset uptime that matches ICE benchmarks. As network density rises, operators schedule midday swaps rather than overnight charging, boosting asset utilization and revenue per vehicle.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Competition From Mini-Trucks Competition From Mini-Trucks | -1.3% | India, China, Southeast Asia | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.3% | Geographic Relevance:India, China, Southeast Asia | Impact Timeline:Long term (≥ 4 years) |

Sparse Charging Network Sparse Charging Network | -1.1% | India tier-2/3, rural Bangladesh, Indonesia | Medium term (2-4 years) | |||

Volatile Lithium Supply Chain Volatile Lithium Supply Chain | -0.8% | Global, cost-sensitive segments | Short term (≤ 2 years) | |||

Uncertain Payload Regulations Uncertain Payload Regulations | -0.6% | Philippines, Indonesia, emerging markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Competition from Two-Wheelers and Mini-Trucks

Enhanced electric two-wheelers in Vietnam aim for 75% of sales by 2035, eroding low-payload three-wheeler niches. Mini-truck makers, meanwhile, develop urban variants with tighter turning radii and rising fuel efficiency, encroaching on higher-payload routes. Price gaps narrow as component costs fall, prompting fleet managers to evaluate route-by-route viability rather than defaulting to a single category. Mixed-density geographies lead to switching between two-wheelers, three-wheelers, and mini-trucks, pressuring the Asia Three Wheeler market margins.

Sparse Charging Network Outside Tier-1 Cities

Beyond metro zones, public charging density remains thin. Bangladesh’s 4 million e-rickshaw fleet relies on domestic sockets, posing safety hazards and limiting charging speed. Rural India faces grid-capacity bottlenecks; transformers designed for 3-kW agricultural pumps cannot support high-current chargers. Private operators hesitate to invest where vehicle density is low, creating a chicken-and-egg stalemate that restrains the Asia Three Wheeler market growth in peri-urban corridors.

Segment Analysis

By Vehicle Type: Passenger Carriers Keep Pole Position

Passenger carriers accounted for 63.15% of the Asia Three Wheeler market share in 2024 and are set to register an 8.95% CAGR through 2030. Integration with ride-hailing apps, flexible route scheduling, and municipal support for paratransit bolster volumes in tier-2 cities. Load-carrier demand climbs in parallel with e-commerce, yet lingering payload-cap rules temper the segment’s acceleration.

Electric retrofits gain traction among passenger operators seeking immediate capital-light upgrades. Subsidies in India and Thailand cover up to 30% of conversion costs, delivering rapid emissions gains without buying new chassis. As metro authorities restrict ICE rickshaws in core zones, replacement cycles shorten from 6-7 years to 3-4 years, adding tailwinds to passenger-carrier sales.

By Fuel Type: Electric Takes the Lead in Momentum

Petrol retains a 44.26% of the Asia Three Wheeler market share in 2024 but loses ground as price parity arrives. Diesel declines fastest as urban bans tighten, while CNG/LPG maintain niche adoption in Pakistan and select Indian states where infrastructure already exists. Electric units hold a smaller base today but will grow at an 11.35% CAGR to 2030, outpacing all combustion fuels.

LFP chemistry dominates cost-sensitive models, keeping battery packs low. OEMs now pre-engineer chassis cavities that accept fixed packs or swap units, which are future-proofing designs. China’s material control raises supply-risk consciousness; India’s ACC-PLI scheme offers production incentives for local cathode plants, signaling gradual diversification.

By Application: Last-Mile Delivery Surges Ahead

Passenger mobility, which held 57.35% of the Asia Three Wheeler market share in 2024, is growing at a slower clip as metros invest in rail and bus rapid transit. Agriculture and industrial goods transport remain steady but do not match the velocity of urban parcel flows. Last-mile delivery logs a 10.24% CAGR, propelled by 30-minute delivery promises from grocery and food apps.

Logistics firms co-locate swap stations at fulfillment hubs, halving driver downtime. This network effect further entrenches three-wheelers in courier fleets, particularly for payloads between 150-350 kg, where two-wheelers are inadequate and mini-trucks overkill.

Note: Segment shares of all individual segments available upon report purchase

By End-User Ownership Model: Fleets Consolidate Share

Individual owner/drivers remain pivotal in rural and peri-urban niches, controlling a 72.16% of the Asia Three Wheeler market share in 2024, yet gradually migrate to fleet aggregation models to gain financing and service benefits. Public-sector demand, though modest, sets procurement benchmarks that private carriers follow, especially for zero-emission mandates. Fleet operators exhibit a 9.56% CAGR as digital platforms scale. The Asia Three Wheeler market size controlled by organized fleets will grow between 2025-2030.

Telematics integration allows fleet managers to monitor state-of-charge and schedule just-in-time swaps. High utilization spreads fixed costs over more kilometers, reinforcing electric economics. Aggregators leverage data to negotiate group insurance and tire contracts, lowering per-unit opex versus lone owners.

Geography Analysis

India captured 62.44% of the Asia Three Wheeler market share in 2024, supported by deep manufacturing clusters in Pune, Aurangabad, and Faridabad. PM E-DRIVE accelerates electric uptake with purchase subsidies, GST cuts, and scrappage incentives. Charging networks spread from metro hubs to tier-2 cities such as Lucknow and Coimbatore, mirroring rising demand. Bangladesh records the fastest 9.11% CAGR through 2030. An existing base of significant e-rickshaws provides latent demand once formal financing and standardized manufacturing take hold. The government’s draft EV policy earmarks concessional loans for lithium-iron-phosphate pack assembly, aiming to localize a notable share of components by 2028.

China retains production heft, with Chongqing Zongshen and Dayun exporting to Africa and South America. Domestic uptake grows more slowly, and municipalities prefer buses and metro rail for mass transit, yet export margins cushion revenue. Policy shifts toward heavier four-wheelers could cap China’s three-wheeler unit sales, but technology spillovers keep Chinese suppliers relevant to regional OEMs. Southeast Asia emerges as a multipolar growth arena. Thailand’s local assemblers like TukTuk Factory and Mine Mobility respond with CKD kits.

Indonesia exempts significant VAT for compliant electric models and sets local-content targets by 2026, enticing joint ventures. The Philippines removes import tariffs on power-electronics parts, enabling cost-effective SKD assembly in Laguna and Cebu. Vietnam’s EV roadmap, co-developed with the World Bank, projects significant number of electric three-wheelers on roads by 2030 for postal and food delivery. Infrastructure roll-out concentrates in Hanoi and Ho Chi Minh City, aided by state utility EVN’s plan to convert curbside transformers into fast-charge clusters. Neighboring Cambodia studies similar frameworks, hinting at a follow-on demand pool.

Competitive Landscape

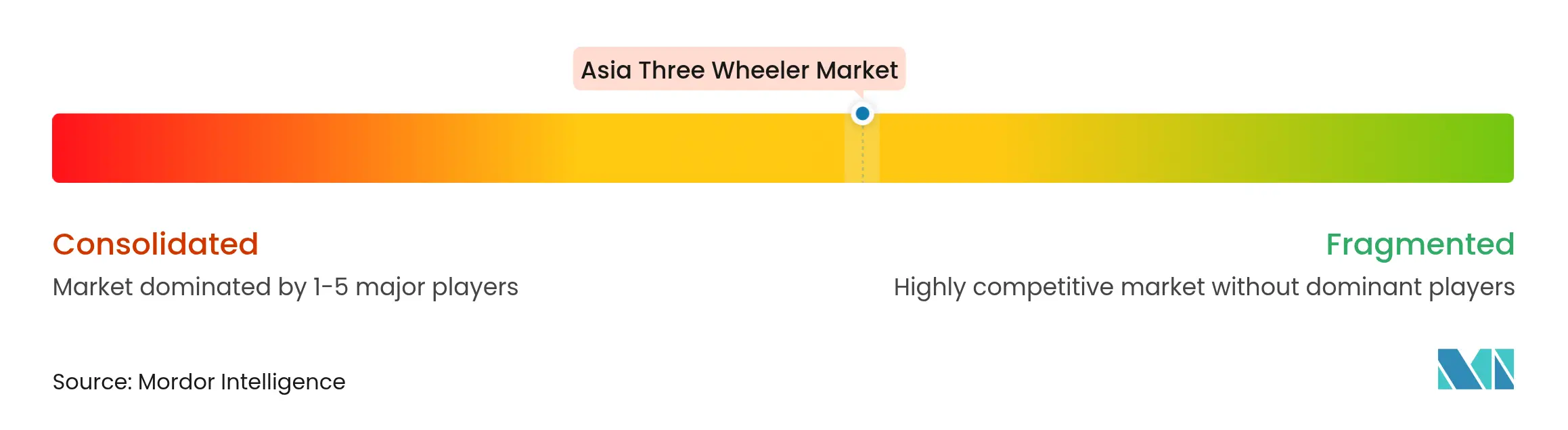

Market Concentration

The Asia Three Wheeler market remains moderately fragmented. Bajaj Auto, Piaggio, and Mahindra collectively hold a significant share, relying on long-tail dealer networks. New-energy entrants like Omega Seiki Mobility, YC Electric Vehicle, and Euler Motors erode share by offering purpose-built electric chassis with connected-vehicle analytics.

Incumbents pivot through alliances: Hero MotoCorp invested INR 525 crore (~USD 59.21 million) in Euler Motors for access to in-house battery IP, while Mahindra injected INR 400 crore (~USD 45.11 million) into subsidiary MLMML to scale battery-swap partnerships. Piaggio licenses modular battery trays from Sun Mobility to retrofit its Ape range. Bajaj Auto introduced the all-electric GOGO brand, boasting 251 km certified range, aiming for export parity across ASEAN. Startups differentiate via asset-light leasing. ALT Mobility commits to deploy 3,000 TVS electric three-wheelers under pay-per-kilometer contracts, bundling insurance and maintenance. Cloud-linked dashboards help fleet owners track state-of-charge and driver behavior, reducing downtime and insurance premiums.

As telematics data accumulates, predictive maintenance lowers service costs, a value incumbents race to replicate. Capital markets favor electrification themes: venture funds poured significant investment into Asian electric three-wheeler startups in 2024.

Asia Three Wheeler Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: TVS Motor signed an MoU with ALT Mobility to lease up to 3,000 electric passenger and cargo three-wheelers in FY 2025-26.

- February 2025: Bajaj Auto unveiled the all-electric Bajaj GOGO, offering a certified 251 km range and fast-charge capability.

- January 2025: TVS Motor launched the TVS King EV MAX, featuring a 179 km range and SmartXonnect telematics.

- April 2024: Omega Seiki Mobility partnered with Exponent Energy to market 15-minute fast-charging electric three-wheelers priced at INR 3.25 Lakh (~USD 3,665.2).

Table of Contents for Asia Three Wheeler Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Surging E-Commerce Last-Mile Demand

- 4.2.2Government Incentives for E-3W Adoption

- 4.2.3Low TCO vs. Two-/Four-Wheelers

- 4.2.4Battery-Swap Infrastructure Roll-Outs

- 4.2.5Micro-Finance Penetration for Driver Ownership

- 4.2.6Corporate Scope-3 Commitments Driving Zero-Emission Fleets

- 4.3Market Restraints

- 4.3.1Competition from Two-Wheelers and Mini-Trucks

- 4.3.2Sparse Charging Network Outside Tier-1 Cities

- 4.3.3Volatile Lithium-Cell Supply Chain

- 4.3.4Uncertainty on Payload Regulations

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1By Vehicle Type

- 5.1.1Passenger Carrier (auto-rickshaws, tuk-tuks)

- 5.1.2Load Carrier (cargo, pick-up body, delivery vans)

- 5.2By Fuel Type

- 5.2.1Petrol

- 5.2.2Diesel

- 5.2.3CNG/LPG

- 5.2.4Electric

- 5.3By Application

- 5.3.1Passenger Transport (urban mobility, ride-hailing, shared transport)

- 5.3.2Last-Mile Delivery / Logistics

- 5.3.3Goods Transport (agriculture produce, industrial goods)

- 5.3.4Others (postal, municipal use)

- 5.4By End-User Ownership Model

- 5.4.1Individual Owner / Drivers

- 5.4.2Fleet Operators (ride-hailing, logistics fleets)

- 5.4.3Government / Institutional Purchases

- 5.5By Country

- 5.5.1India

- 5.5.2China

- 5.5.3Bangladesh

- 5.5.4Sri Lanka

- 5.5.5Thailand

- 5.5.6Indonesia

- 5.5.7Philippines

- 5.5.8Vietnam

- 5.5.9Rest of Asia-Pacific

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1Bajaj Auto Limited

- 6.4.2Piaggio & C. SpA

- 6.4.3Mahindra & Mahindra Ltd

- 6.4.4TVS Motor Company

- 6.4.5Atul Auto Limited

- 6.4.6Lohia Auto Industries

- 6.4.7ChongQing Zongshen Tricycle Mfg

- 6.4.8Scooters India Ltd

- 6.4.9Ningbo Dowedo International Trade

- 6.4.10ElecTrike Japan

- 6.4.11Saera Electric Auto Ltd.

- 6.4.12Kinetic Green Energy & Power Solutions Ltd.

- 6.4.13Omega Seiki Mobility

- 6.4.14YC Electric Vehicle

- 6.4.15Terra Motors Corporation

- 6.4.16J.S. Auto (Pvt) Ltd

7. Market Opportunities & Future Outlook

Asia Three Wheeler Market Report Scope

A three-wheeler is a vehicle with three wheels, usually one at the front and two at the rear axle. It is primarily used for passenger transportation and freight loading for small distances.

The Asia Three-Wheeler Market is segmented by vehicle type, fuel type, and country. By vehicle type market is segmented into passenger carriers and goods carriers. By fuel type market is segmented into petrol, CNG/LPG, diesel, and electric. The report also covers the market size and forecast for the Asia three-wheeler market in 5 major countries, including China, India, Indonesia, Bangladesh, Srilanka, and the Rest of Asia.

For each segment, market sizing and forecast have been done based on volume (million units) and Value (USD billion).