Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

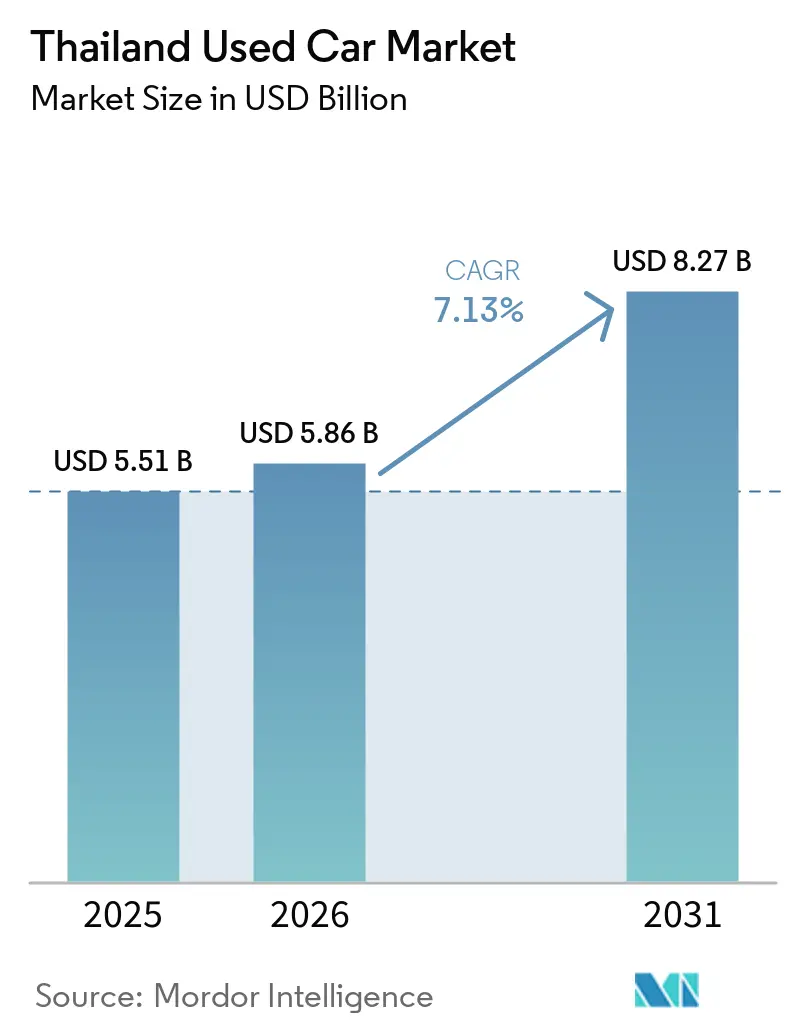

| Base Year Market Size (2025) | USD 5.51 Billion |

| Market Size (2026) | USD 5.86 Billion |

| Market Size (2031) | USD 8.27 Billion |

| Growth Rate (2026 - 2031) | 7.13% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Used Car Market Analysis by Mordor Intelligence

The Thailand used car market size was valued at USD 5.51 billion in 2025 and estimated to grow from USD 5.86 billion in 2026 to reach USD 8.27 billion by 2031, at a CAGR of 7.13% during the forecast period (2026-2031). Recently, with household debt reaching elevated levels and auto-loan rejection rates significantly high, a substantial number of vehicles faced repossession. These factors have shifted consumer preference from new cars to competitively priced pre-owned ones. Meanwhile, digital marketplaces are harnessing AI-driven credit screenings to tap into subprime segments. New-car sales experienced a sharp decline, tightening dealer pipelines. This scarcity led to a notable surge in wholesale valuations over a short period, solidifying the used car market in Thailand as a resilient alternative. While organized vendors, bolstered by original equipment manufacturer certifications and fintech lending, are gaining traction in urban areas, unorganized roadside lots still dominate rural markets. Battery-electric vehicles (BEVs) are the fastest-growing segment, but petrol cars continue to lead in volume, a testament to the existing installed base and buyer concerns over battery longevity. As credit challenges, digital advancements, and a burgeoning electric vehicle supply converge, they will shape the competitive landscape of Thailand's used car market up to 2031.

Key Report Takeaways

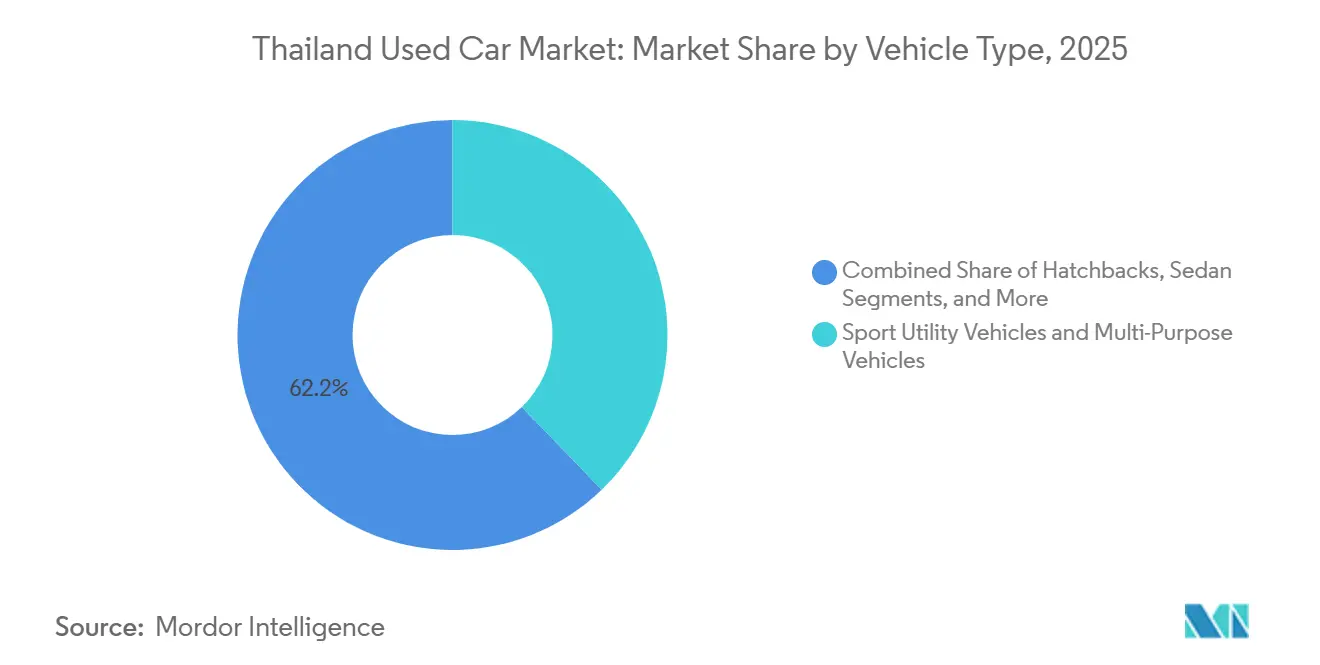

- By vehicle type, sport utility vehicles and multi-purpose vehicles led with 37.81% of volume in 2025, while this segment is forecast to expand at a 7.15% CAGR to 2031.

- By fuel type, petrol-powered units captured a 63.47% share in 2025; battery electric vehicles posted the highest growth at 7.24% through 2031 in the Thailand used car market.

- By booking type, offline transactions accounted for 83.37% of bookings in 2025, whereas online channels are growing at 7.27%.

- By vendor, unorganized vendors held a 67.71% share in 2025, yet organized players are expanding at a 7.18% CAGR in the Thailand used car market.

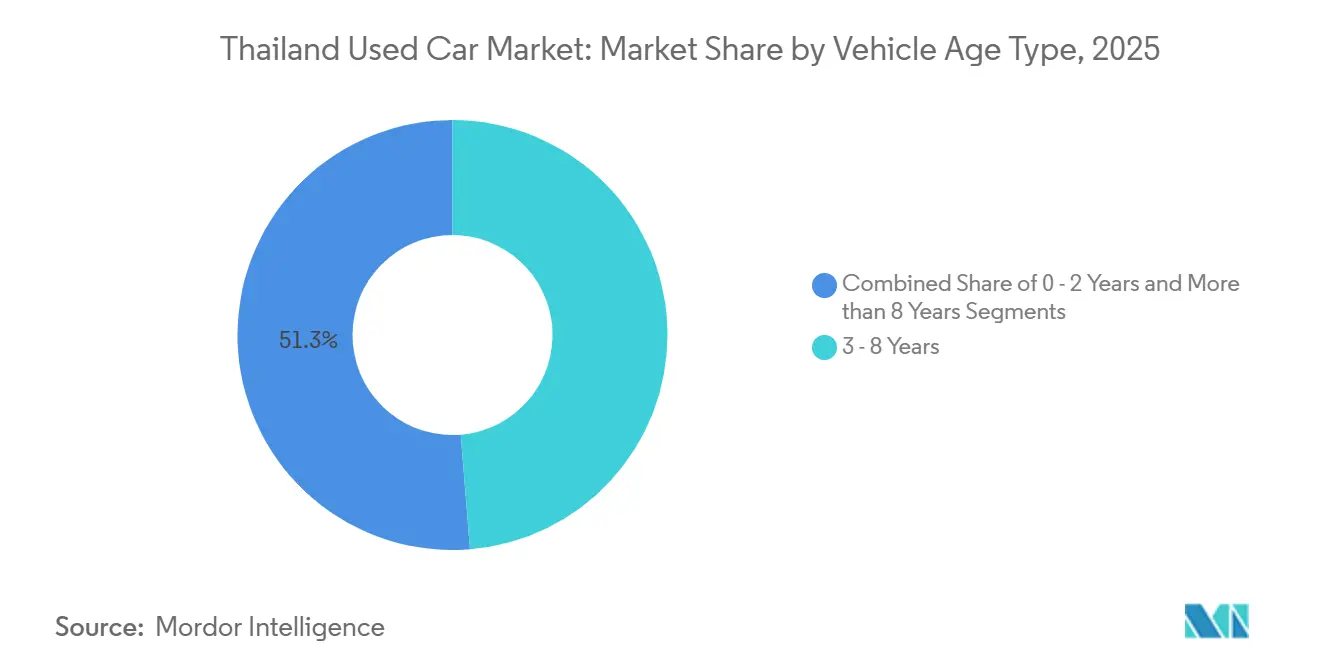

- By vehicle age, vehicles aged 3-8 years commanded 48.71% of trades in 2025; nearly-new units (0-2 years) recorded the fastest growth at 7.29%.

- By price band, inventory priced below USD 10,000 represented 45.63% of demand in 2025, but the premium tier above USD 20,000 is advancing at 7.21% in the Thailand used car market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-Conscious Consumers Amid Economic Headwinds | +1.8% | National, acute in rural and suburban areas | Short term (≤ 2 years) |

| Rapid Rise of Digital Used-Car Marketplaces | +1.5% | National, urban centers leading adoption | Short term (≤ 2 years) |

| Diverse Model Availability Across Price-Points | +1.2% | National, with concentration in Bangkok, Chiang Mai, Phuket | Medium term (2–4 years) |

| Usage-Based Insurance and Fintech Lending Boosting Affordability | +1.1% | National, digital-first urban buyers | Short term (≤ 2 years) |

| Expansion of OEM-Backed Certified-Pre-Owned Programmes | +0.9% | National, Bangkok and provincial capitals | Medium term (2–4 years) |

| Repatriated Expat-Owned Vehicles Enlarging Supply Pool | +0.4% | Bangkok, Pattaya, Phuket | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cost-Conscious Consumers Amid Economic Headwinds

With household debt nearing record highs and loan rejection rates remaining significantly high, consumers are increasingly turning to affordable pre-owned vehicles. These are often several years old, providing reliability without the steep depreciation of new cars. In recent times, repossessions have risen considerably, allowing dealers to stock up at lower prices compared to pre-pandemic levels, a saving they readily passed on to buyers. Sales of pickups have seen a substantial decline, flooding the market with trucks now available to rural operators at more accessible prices. The Bank of Thailand’s Used Vehicle Price Index has shown a notable rebound, hinting at a tighter supply once new-car production sees a modest recovery. This counter-cyclical trend underscores the Thai used car market's role as a safety valve during broader economic stresses [1]“Household Debt and Loan Quality Dashboard,” Bank of Thailand, bot.or.th .

Rapid Rise of Digital Used-Car Marketplaces

In recent years, online channels have accounted for a significant portion of trades and are growing at a faster pace compared to offline channels. Krungsri Auto’s GO Auto Station features a vast inventory of vehicles, offers quick loan approvals through its PromptStart workflow, and provides integrated services such as insurance renewal and maintenance scheduling within the app. Over the past year, the platform has seen a notable increase in monthly active users, solidifying the bank’s position as a leader in the national used-car finance market. The adoption of virtual inspection protocols and standardized grading has effectively reduced odometer fraud risks, aligning with the trust mechanisms familiar to Thai mobile shoppers, most of whom already make purchases via smartphones. With a large portion of the population now online, the digital landscape is expanding its influence beyond Bangkok into secondary cities [2]“GO Auto Station Performance Update,” Krungsri Auto, krungsri.com .

Expansion of OEM-Backed Certified-Pre-Owned Programs

Through multi-point inspections, warranties, and roadside assistance, schemes like Toyota and Honda's Certified Used Car are seamlessly integrating manufacturer reputations into the secondary market. While certified units command a moderate price premium, they also enjoy quicker sales. This is largely because lenders trust the standardized checks, resulting in higher approval ratios. The segment of newer vehicles, which is experiencing steady growth, directly feeds into the Certified Pre-Owned (CPO) pipelines. This dynamic enables Original Equipment Manufacturers (OEMs) to not only sustain dealership throughput but also defend residual values. With new-car production in 2024 reaching its lowest level in several years, brands turned to CPO channels as a strategy to uphold service revenue and safeguard their captive finance portfolios. As adoption rates rise, unorganized vendors face mounting pressure to either embrace third-party certification or risk losing market share in the Thailand used car market.

Repatriated Expat-Owned Vehicles Enlarging Supply Pool

After customs clearance, low-mileage European and Japanese models routinely find their way into domestic listings, due to assignments ending for foreign nationals. Organized dealers, well-versed in Thai Industrial Standards Institute (TISI) compliance, consistently receive inflows in Bangkok, Pattaya, and Phuket. While the volumes may be modest, the margins are notably superior, as these cars fetch premiums from buyers with a penchant for unique specifications. The mandatory Thai Industrial Standards Institute (TISI) safety and emission tests not only restrict participation to vendors with accredited facilities but also contribute significantly to the steady growth of the organized segment [3]“Automotive Standards Overview,” Thai Industrial Standards Institute, tisi.go.th .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter AI-Driven Credit-Scoring Limiting Auto Loans | -1.2% | National, disproportionate impact on rural and low-income buyers | Short term (≤ 2 years) |

| Fragmented Vehicle-History and Odometer Fraud | -0.8% | National, acute in unorganized vendor segment | Short term (≤ 2 years) |

| Counterfeit and Illegally Imported Vehicles | -0.6% | Border provinces, Bangkok port areas | Medium term (2–4 years) |

| Battery-Health Uncertainty in Used Electric Vehicles and Hybrids | -0.5% | National, urban electric vehicle adoption zones | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Illegally Imported Vehicles

Gray-market cars that bypass Thai Industrial Standards Institute (TISI) certification erode buyer trust, expose owners to the risk of registration denial, and impose retrofitting costs to meet safety regulations. Enforcement has tightened, yet the majority of trade still runs through unorganized vendors where oversight is weak. Buyers wary of non-compliant units may delay purchases or default to certified platforms, trimming overall demand in the Thailand used car market. Compliance burdens favor organized dealers but also raise transaction expenses that can dampen price-sensitive segments.

Battery-Health Uncertainty in Used EVs and Hybrids

Battery electric vehicle packs vary widely in degradation, but Thailand lacks standardized state-of-health tests, leaving buyers to rely on seller claims or costly diagnostics. Replacement packs can exceed USD 5,000, a liability depressing resale and constraining liquidity in the Thailand used car market. Original equipment manufacturer CPO programs offer short warranties, yet older high-mileage electric vehicles remain uncovered. Establishing third-party certification standards through agencies such as the Thailand Automotive Institute would unlock significant secondary-market value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Sport Utility Vehicles and Multi-Purpose Vehicles Capture Family Demand

Sport utility vehicles and multi-purpose vehicles accounted for 37.81% of 2025 volume, and this cohort is forecast to post a 7.15% CAGR through 2031. The Thailand used car market share tilted toward spacious cabins and flexible seating, reflecting demographic shifts toward nuclear families and dual-use business needs. Sedans surrendered ground as crossovers deliver comparable fuel economy, and hatchbacks retain urban niches where parking is scarce. Luxury cars remain a thin slice after new-vehicle imports fell 25% in 2024, tightening supply and elevating certified residuals.

Resilience in this segment arises from broad utility: families commute during the week and travel on weekends, while SMEs repurpose multi-purpose vehicles for light cargo. Chinese-brand sport utility vehicles entering off-lease cycles add fresh stock, though dealers still price residuals cautiously. Pickup trucks, counted separately, overflow into this demand after the 41.6% sales collapse in October 2024, supplying rural buyers. Government guarantees for pickup loans could stabilize this spill-over, but remain untested.

By Fuel Type: Petrol Dominates, BEVs Surge

Petrol models accounted for 63.47% of trades in 2025, yet battery electric vehicles are the fastest climber at a 7.24% CAGR through 2031. Diesel share is tapering as Euro-5 rules raise compliance costs, while hybrids fill a middle ground for buyers wary of range anxiety. The Thailand used car market size for BEVs will grow off a small base, as new electric vehicle registrations in the first seven months of 2025 begin flowing into trade-ins. BYD’s Rayong factory and government EV 3.0 incentives until 2026 underpin future supply.

Excise tax hikes on BEVs slightly after subsidies expire could slow fresh entries and keep petrol leadership intact. LPG and CNG conversions remain niche, handicapped by retrofit compliance costs under TIS 3055-2563. Persistent uncertainty about battery health tempers battery electric vehicle liquidity; however, the development of standardized grading would accelerate adoption.

By Booking Type: Offline Channels Retain Majority, Digital Gains Momentum

Physical outlets still executed 83.37% of 2025 bookings, highlighting the tactile requirement of vehicle inspection and accounting for the largest Thailand used car market share by sales channel. Buyers lean on test drives and personal negotiation, especially where vehicle-history data are scarce. Organized showrooms bundle finance and warranties, whereas informal lots entice with price. Conversely, digital channels, led by Krungsri’s GO Auto Station, are compounding at 7.27%, mirroring Thai consumers’ comfort with smartphone retail.

Online momentum is strongest among urban 25–40-year-olds who value one-stop financing, home delivery, and seven-day return guarantees. The Thailand used car market size attributable to online platforms remains modest but rising as AI-assisted valuations and virtual inspections trim search costs. Offline venues will stay dominant through 2031, yet their share will slide as digital trust infrastructure matures.

By Vendor Type: Unorganized Segment Dominates, Organized Players Consolidate

Unorganized vendors commanded 67.71% of 2025 trades, reflecting low entry barriers and cash-based bargaining cultures. However, organized operators are expanding at 7.18% and leverage certification, integrated finance, and digital discovery to win urban customers. The Thailand used car market share for organized dealers will keep rising after CARS24’s 2024 exit, underscoring the need for local credit adaptation.

Krungsri Auto’s vehicle inventory and 30-minute loan approvals illustrate economies of scale. Original equipment manufacturer CPO programs widen factory engagement into second ownership cycles. Informal lots retain rural advantages where speed trumps paperwork, yet tightened enforcement on counterfeit imports and odometer fraud will gradually erode their edge.

By Vehicle Age: Mid-Life Units Lead, Nearly-New Grow Fastest

Cars aged 3–8 years held a 48.71% share in 2025, due to balanced depreciation and reliability. Nearly-new 0–2 year inventory is the quickest climber at 7.29% as corporate fleets refresh and early electric vehicle adopters upgrade batteries. The Thailand used car market size in this cohort benefits from remaining factory warranties and lower default risk, attracting lender preference.

Older than 8 years stock caters to budget and rural buyers but faces looming scrappage incentives discussed in February 2025, potentially accelerating retirements. Dealers anticipate a tighter supply, evidenced by the rebound in the Used Vehicle Price Index, and are positioning trade-in credits to capture replacement demand.

By Price Band: Budget Tier Dominates, Premium Accelerates

Units below USD 10,000 secured 45.63% of 2025 demand, reflecting cost sensitivity and repossession inflows sold at auction discounts. The mid-band USD 10,001–20,000 is a battleground for organized certification versus informal pricing. Premium inventory above USD 20,000 is advancing at 7.21% as affluent consumers, insulated from credit stress, seek late-model imports and certified luxury marques.

Luxury new-car imports slipped drastically in 2024, constricting supply and inflating residuals for certified German and Japanese brands. Wearnes Automotive notes that premium buyers face fewer financing hurdles, sustaining momentum even as mass-market segments grapple with loan rejections.

Geography Analysis

In 2025, Bangkok and its neighboring provinces accounted for a significant share of transactions, buoyed by rising incomes, a dense network of dealers, and a strong charging infrastructure supporting the burgeoning resale market for battery electric vehicles (BEVs). Urban buyers in Bangkok are gravitating towards hatchbacks to navigate city congestion, while suburban families are opting for SUVs and multi-purpose vehicles (MPVs). Meanwhile, cities like Chiang Mai, Phuket, and Pattaya are witnessing a steady influx of repatriated vehicles from expatriates. These vehicles, often low-mileage European models, command premium prices once they meet Thai Industrial Standards Institute (TISI) compliance and are supplied to organized dealers.

In Thailand's Northeast and Southern provinces, pickups are the go-to choice for agriculture and small businesses. However, these regions faced a setback with a high loan rejection rate, leading to a notable decline in new truck sales in late 2024. A proposed scrappage discussion in early 2025 could disproportionately benefit urban areas, where older vehicle fleets are more concentrated. While digital marketplaces are making inroads into secondary cities, rural districts still lean heavily on offline bargaining, largely due to limited internet access.

Credit disparities across regions reflect the structure of vendors: buyers in Bangkok enjoy the advantages of competitive digital financing, while those in rural areas frequently rely on cash payments or turn to informal lending sources. Organized dealerships are channeling investments into urban showrooms and certified service bays, contrasting with the dominance of unorganized lots in rural roadside trades. Given these dynamics, the used car market in Thailand is poised for a pronounced urban-rural divide, a trend likely to persist until there's a leveling of data transparency and credit accessibility across provinces.

Competitive Landscape

Recently, Thailand experienced a decline in the number of active used-car sellers, leaving a few hundred players in the market. However, the industry is undergoing rapid consolidation, driven by advancements in digital technology and increasing compliance requirements. Krungsri Auto has established itself as a key player, holding a significant share of the national finance market. With a large user base and quick approval times, Krungsri effectively shortens sales cycles. Its extensive vehicle listings highlight a strong network effect that smaller, informal sellers find difficult to compete with.

Original equipment manufacturers (OEMs) are strengthening their influence through certified pre-owned programs. These initiatives, which include vehicle inspections and warranties, enable original equipment manufacturers to charge a premium on vehicles. This approach not only stabilizes residual values but also enhances their captive finance portfolios. In a strategic move, Itochu has invested in Eastern Commercial Leasing, signaling a focus on subprime auto finance. The investment reflects confidence in AI-driven underwriting to responsibly serve previously underserved customer segments.

CARS24's decision to exit in early 2024, following significant financial losses, highlights the risks of expanding without adapting to localized credit models. At the same time, new disruptors are introducing innovations such as blockchain-based vehicle identification registries and independent battery grading systems. However, the success of these initiatives depends on regulatory mandates for data sharing. Compliance standards enforced by TISI and the Department of Land Transport appear to favor well-funded players. Nevertheless, the ongoing issue of counterfeit vehicles entering through border provinces continues to challenge consistent enforcement efforts.

Thailand Used Car Industry Leaders

Cars24 Group (Thailand) Co., Ltd

Toyota Sure (Toyota Motor Thailand Co., Ltd.)

CARSOME (THAILAND) CO., LTD.

Carro Thailand

Honda Certified Used Car

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The Thai government opened consultations on a nationwide car trade-in incentive plan aimed at accelerating fleet renewal, potentially boosting used-car supply once enacted.

- July 2024: BYD acquired a 20% stake in Rever Automotive to extend control over Thailand’s certified-pre-owned electric vehicle (EV) channels.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines Thailand's used car market as all passenger vehicles that have had at least one prior registered owner and are resold through online portals, certified-pre-owned programs, franchised dealerships, auctions, or consumer-to-consumer channels. Values are modeled in USD terms and in unit transfers for calendar years 2019-2030.

Out of scope, salvage units stripped for parts or vehicles imported without Thai road registration are not included.

Segmentation Overview

- By Vehicle Type

- Hatchbacks

- Sedans

- Sport Utility Vehicle and Multi-Purpose Vehicle

- Luxury Cars

- By Fuel Type

- Petrol

- Diesel

- Hybrid Electric

- Battery Electric

- Others

- By Booking Type

- Online

- Offline

- By Vendor Type

- Organized

- Unorganized

- By Vehicle Age

- 0 - 2 Years

- 3 - 8 Years

- More than 8 Years

- By Price Band (USD)

- Less than 10,000

- 10,001 - 20,000

- More than 20,000

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with certified-pre-owned program managers, independent dealers across Bangkok, Chiang Mai, and Khon Kaen, online marketplace product heads, and auto-finance officers help validate transfer volumes, typical gross transaction values, and emerging EV resale hurdles. Follow-up surveys with recent buyers clarify channel-shift rates and willingness to pay for warranties.

Desk Research

Our analysts begin with public records from the Department of Land Transport, quarterly vehicle-transfer files, Thailand Automotive Institute fleet data, and Bank of Thailand consumer-credit dashboards. Trade-association yearbooks such as the Federation of Thai Industries and regional bodies like ASEAN Automotive Federation provide production and export context that anchors supply flows. We also screen tier-one news and filings on Dow Jones Factiva, plus company financials on D&B Hoovers, to gauge volumes handled by major platforms. Academic papers on residual-value trends, customs shipment logs on Volza, and patent alerts on Questel (for digital inspection tools) refine technology adoption assumptions. The listed sources are illustrative; many additional publications support data checks and clarifications.

Market-Sizing & Forecasting

A top-down build starts with annual used-vehicle transfers by segment, adjusted for illegal or duplicate records before an average selling-price curve is applied. Supplier roll-ups of inspected units and sampled ASP×volume checks supply bottom-up cross-tests, after which totals are reconciled. Key variables include: (1) transfer filings by vehicle age band, (2) median resale price index from leading platforms, (3) consumer-loan rejection rates that push demand toward pre-owned vehicles, (4) replacement-cycle length derived from insurance renewals, and (5) EV incentive timelines affecting residual values. A multivariate regression blended with ARIMA smooths macro shocks and projects each driver, producing the 2025-2030 view. Gaps in sparse rural data are bridged using regional penetration ratios taken from comparable provinces and vetted with dealers.

Data Validation & Update Cycle

Model outputs undergo variance checks against historic fleet growth, taxable transfer receipts, and platform transaction disclosures. Senior reviewers double-check anomalies, and the study refreshes yearly; material events such as tax changes trigger interim updates. A final pre-publication sweep ensures clients receive the most current baseline.

Why Our Thailand Used Car Baseline Inspires Confidence

Published estimates often diverge because firms apply different scope filters, pricing proxies, and refresh cadences.

Key gap drivers include whether commercial pickups are counted, if warranty premiums are netted, the choice of FX conversion year, and how fast digital-channel volumes are rolled into forecasts. Mordor's disciplined variable selection, dual checks, and annual refresh reduce those variances and keep our baseline decision-ready.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.46 bn (2025) | Mordor Intelligence | - |

| USD 5.22 bn (2024) | Global Consultancy A | Excludes online-only dealers; converts at constant 2021 FX; updates biennially |

| USD 5.70 bn (2023) | Research Publisher B | Uses gross transaction value with accessories; counts light commercial vehicles; base metrics from pre-COVID surveys |

These comparisons show that while figures cluster, variation stems from scope choices and aging assumptions. By grounding every step in transparent variables and timely validation, Mordor Intelligence delivers a balanced, reproducible baseline clients can trust for planning.

Key Questions Answered in the Report

How large is the Thailand used car market in 2026?

The Thailand used car market size is estimated at USD 5.86 billion in 2026, continuing its 7.13% CAGR trajectory.

Which segment leads by vehicle type?

Sport utility vehicles and multi-purpose vehicles lead, accounting for 37.81% of 2025 volume and growing at a 7.15% CAGR through 2031.

What fuel type is expanding fastest?

Battery-electric vehicles hold the highest growth rate at 7.24% per year, albeit from a small base.

How are digital platforms affecting sales?

Online channels handled 16.63% of 2025 transactions and are expanding at a 7.27% CAGR through 2031, driven by AI-enabled financing and virtual inspections.

What is the main restraint on market growth?

Stricter AI-based credit scoring limits loan approvals, cutting access for marginal buyers and lowering financed demand.

Which vendor group is gaining share?

Organized dealers are growing at a 7.18% CAGR due to certification, integrated financing, and digital reach, gradually eroding the dominance of unorganized vendors.

Page last updated on: