Brazil Two Wheeler Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

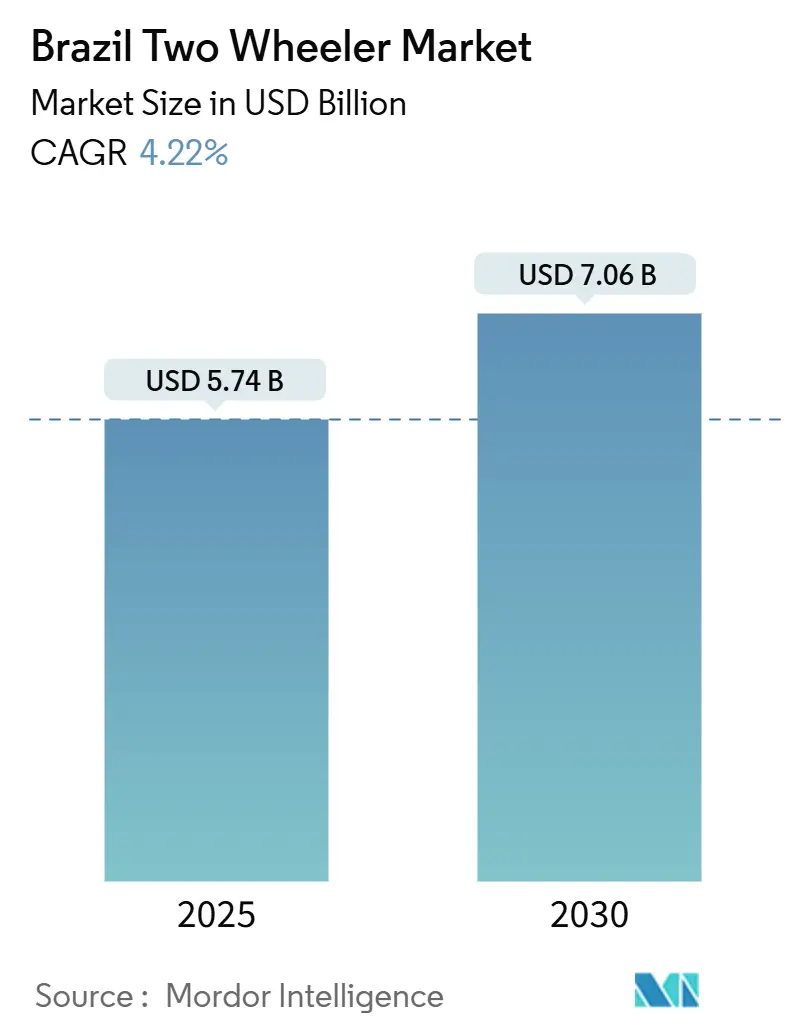

| Market Size (2025) | USD 5.74 Billion |

| Market Size (2030) | USD 7.06 Billion |

| Growth Rate (2025 - 2030) | 4.22% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Two Wheeler Market Analysis by Mordor Intelligence

The Brazilian two-wheeler market size is estimated at USD 5.74 billion in 2025 and is forecast to reach USD 7.06 billion by 2030, reflecting a 4.22% CAGR for the period. Urban congestion, delivery-economy expansion, and flexible credit schemes underpin the growth momentum, while safety regulation and currency swings temper the pace. Manufacturers leverage Manaus-based scale, platform partnerships, and flex-fuel engineering to defend share, yet the rapid rise of electric fleets and belt-drive scooters signals a structural shift. Geography amplifies the story: motorcycle penetration already outstrips cars in most Northern and Northeastern cities, turning two-wheelers from optional rides into essential mobility.

Key Report Takeaways

- By vehicle type, motorcycles captured 70.42% of Brazil's two-wheeler market share in 2024; scooters are forecast to expand at a 7.26% CAGR through 2030.

- By propulsion type, internal combustion engine variants held an 88.32% share of the Brazilian two-wheeler market in 2024; electric two-wheelers are projected to grow at a 12.41% CAGR between 2025 and 2030.

- By drive type, chain drive systems accounted for a 73.72% share of the Brazilian two-wheeler market in 2024; belt drive is anticipated to advance at a 7.88% CAGR through 2030.

- By end use, personal applications commanded 71.23% share of the Brazilian two-wheeler market size in 2024; delivery and fleet services stand out with a 9.43% CAGR forecast to 2030.

- By sales channel, offline distribution retained 84.41% share of the Brazilian two-wheeler market size in 2024; online sales are positioned to rise at 9.87% CAGR during 2025-2030.

Brazil Two Wheeler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Urban Congestion and Demand for Affordable Mobility | +1.2% | National, with highest impact in São Paulo, Rio de Janeiro, Belo Horizonte | Medium term (2-4 years) |

| Growth of On-Demand Delivery Service Fleets | +1.0% | Metropolitan areas, with spillover to secondary cities | Short term (≤ 2 years) |

| Favorable Credit Financing and Low Down-Payment Schemes | +0.8% | National, particularly benefiting lower-income segments in Northeast and North | Short term (≤ 2 years) |

| Expansion of Motorcycle-Taxi Regulation in Secondary Cities | +0.6% | Secondary cities and municipalities outside major metros | Long term (≥ 4 years) |

| Battery-Swapping Pilot Programs Boosting E-2W Confidence | +0.4% | Major metropolitan areas with initial focus on São Paulo and Rio | Long term (≥ 4 years) |

| Domestic Adventure-Touring Boom Supported by Tourism Incentives | +0.3% | Tourism corridors, particularly South and Southeast regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Congestion and Demand for Affordable Mobility

Traffic congestion in Brazil's major cities, particularly São Paulo, causes significant economic losses through wasted time. Commuters experience extensive delays, with traffic queues extending for kilometers. This congestion results in billions of dollars in lost productivity each year. The need for transportation system improvements has become critical, as poor mobility directly affects urban economic output. Motorcycles traverse clogged avenues two to three times faster than cars during peak periods, cutting one-way commutes that average 52 minutes in major cities. Lane-splitting legality and compact footprints enhance this advantage, encouraging first-time buyers and commercial couriers alike. Limited investment in mass transit reinforces the appeal and keeps the Brazilian two-wheeler market on an upward curve. Municipal authorities acknowledge the modal shift but struggle to match infrastructure upgrades with demand.

Growth of On-Demand Delivery Service Fleets

Platform logistics transforms motorcycles into workhorses for last-mile fulfillment. iFood and 99 jointly aim to deploy 10,000 electric motorcycles by 2025 to improve courier earnings and curb emissions. Bulk fleet orders stabilize factory output and encourage models designed for high utilization, GPS tracking, and theft protection. Predictable replacement cycles also anchor dealership service revenue. The Brazilian two-wheeler market thus benefits from an enterprise-scale buyer segment alongside individual commuters.

Favorable Credit Financing and Low Down-Payment Schemes

Financial inclusion initiatives are expanding motorcycle ownership access to underbanked consumers. Financial technology companies like Motocred use alternative data analysis to approve loans for gig-economy workers previously rejected by traditional banks[1]“Motocred,” F6S, f6s.com. In Brazil, Banco Honda's Evolution program and Bank BV's low-entry financing options enable motorcycle purchases beyond middle-income segments. Local manufacturing helps control costs, while digital platforms simplify the loan approval. These developments bring new buyers into the two-wheeler market, particularly those who depend on motorcycles for essential transportation rather than recreational use.

Expansion of Motorcycle-Taxi Regulation in Secondary Cities

Capacities open fastest in cities lacking robust public transit, where mototaxis knit first-mile and last-mile connectivity. Fortaleza and Salvador impose medical tests, age minimums, and passenger insurance, whereas São Paulo still bans services outright. Regulatory convergence would unlock formal financing and insurance for operators, improving fleet renewal rates. Over time, standardized oversight is expected to spread commercial usage beyond traditional delivery into passenger transport, adding depth to the Brazilian two-wheeler market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Accident Rates Triggering Stricter Safety Rules | -0.9% | National, with highest impact in major metropolitan areas | Short term (≤ 2 years) |

| Currency Volatility Inflating Component Import Costs | -0.7% | National, affecting all manufacturers and price-sensitive segments | Medium term (2-4 years) |

| Shortage of Skilled EV Service Technicians | -0.5% | Metropolitan areas with EV adoption, expanding to secondary cities | Long term (≥ 4 years) |

| Competition From Shared Micro-Mobility Schemes | -0.3% | Major cities with bike-sharing infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Accident Rates Triggering Stricter Safety Rules

Motorcyclists account for a large share of traffic fatalities in Brazil, prompting stricter regulations. Cities like Rio and São Paulo report high incident rates involving two-wheelers, leading to bans on mototaxis and new safety mandates. While compliance raises costs and may slow sales, improved safety could support long-term adoption as risk perceptions shift.

Currency Volatility Inflating Component Import Costs

Imported parts incur 14% to 40% fundamental duty before layered taxes, tying local prices tightly to the USD/BRL exchange rate. The Central Bank attributes more than half of recent volatility to domestic factors that firms struggle to hedge[2]“Relatório de volatilidade cambial,” Banco Central do Brasil, bcb.gov.br. Chinese suppliers dominate several component categories, creating single-source risk that magnifies price swings. Quarterly price resets ripple through dealer inventories, pressuring margins and testing consumer budgets. This restraint caps the upside for the Brazilian two-wheeler market during depreciation cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Motorcycles Retain Primacy While Scooters Accelerate

Motorcycles accounted for 70.42% of the Brazilian two-wheeler market share in 2024, a lead grounded in versatility, fuel thrift, and broad dealer service networks. Scooters hold a smaller slice, yet post the segment’s fastest 7.26% CAGR, benefiting younger riders and women who favor automatic transmissions and low-seat ergonomics. The Brazilian two-wheeler market size for scooters is projected to rise steadily as urban parking reforms and congestion pricing favor compact formats. Niche makers like Shineray record triple-digit growth by targeting entry-level commuters, signaling room for new brands under the motorcycle shadow.

Production hubs mirror demand patterns. Honda’s Manaus complex produces 6,500 units daily and supplies roughly three-quarters of the national demand, enabling price competitiveness and localized after-sales parts. Royal Enfield’s jump in registrations indicates a budding premium category, foreshadowing greater segmentation and lifestyle diversification. As scooters claim street space and lifestyle adventurers collect high-torque machines, manufacturers adapt line-ups to defend their standing in the Brazilian two-wheeler market.

By Propulsion Type: ICE Dominance Meets Electric Disruption

Internal combustion engines held an 88.32% grip on 2024 unit sales thanks to ethanol-ready flex-fuel technology and nationwide fueling infrastructure. Engine sizes between 101 cc and 125 cc optimize running costs for a price-sensitive rider base. Yet electric two-wheelers grow at a robust 12.41% CAGR as delivery platforms seek lower operating costs and municipalities announce low-emission zones. Battery-as-a-Service models from Voltz Motors lower upfront prices and smooth range anxiety, widening the appeal among gig-workers.

Policy also nudges demand. Paraná’s 2025 tax waiver for motorcycles up to 170 cc frees cash for buyers to consider electric upgrades. Fleet partners such as 99 commit volume orders that give startups procurement leverage. The Brazilian two-wheeler market size for electric variants, while small today, establishes a technology pipeline poised to dent ICE supremacy over the next decade.

By Drive Type: Chain Resilience Amid Belt Upswing

Chain systems dominated 73.72% of drivetrains in 2024, prized for simple mechanics and easy roadside repair. Informal service networks thrive on chain familiarity, a crucial factor where riders lack formal licenses and often self-maintain vehicles. Belt drives gather momentum via scooters and premium commuters because they offer cleaner, quieter operation at the cost of higher initial spend. A 7.88% CAGR suggests rising incomes and fleet managers favor lower maintenance downtime, even in secondary cities.

Brazil's two-wheeler market dynamics indicate a gradual shift rather than wholesale substitution. Manufacturers integrate belt systems into new urban models while retaining chain options for rural buyers who value robust field repair. Standardization under CONTRAN safety rules ensures both drive types meet minimum reliability thresholds, sustaining healthy coexistence in the medium term.

By End Use: Personal Dominance Faces Commercial Surge

Personal mobility represented 71.23% of 2024 demand, anchored by commuters priced out of car ownership or undersupplied by public transit. Affordability and fuel flexibility remain chief purchase triggers. However, the delivery and fleet services slice grows significantly in a year, supercharged by the e-commerce boom and platform integration. Couriers prioritize durable drivetrains, GPS security, and financing convenience, steering OEMs toward fleet-specific trims and service packages.

The Brazilian two-wheeler market finds revenue upside in this commercial sweet spot. Bulk purchases flatten production cycles, while predictable replacement boosts parts and maintenance trade. Hybrid owner-operator models blur the line between personal and professional use, complicating segmentation yet enlarging total addressable demand.

By Sales Channel: Offline Stronghold Adapts to Online Uptick

Physical dealerships carried 84.41% of the share in 2024, reflecting customer preference for test rides and after-sales reassurance. Financing paperwork, insurance add-ons, and service scheduling all revolve around in-store interactions. Nevertheless, online channels expand at a 9.87% CAGR as digital-native riders grow comfortable completing large purchases remotely. Electric OEMs spearhead direct-to-consumer portals, bundling subscription batteries and doorstep maintenance.

Traditional dealers respond with omnichannel integrations that allow virtual inventory checks and click-and-collect options. The Brazilian two-wheeler market thus heads for a blended distribution landscape where offline trust coexists with online convenience, each reinforcing the other rather than displacing it outright.

Geography Analysis

Regional disparities shape how and where units move. The Southeast posts the most significant absolute sales yet exhibits lower per-capita penetration due to higher car ownership and better transit corridors. São Paulo alone absorbs a sizable slice of the Brazilian two-wheeler market thanks to a metropolitan population exceeding 22 million, but its mototaxi ban illustrates regulatory uncertainty that tempers growth. Manaus production funnels output nationwide, yet most units cycle back to Southeastern urban centers where purchasing power concentrates.

The Northeast and North rank top in vehicle-to-population ratios, with motorcycles outnumbering cars in most municipalities. Penetration reflects lower median incomes and sparse public transport, positioning two-wheelers as daily necessities rather than discretionary purchases.

Southern states offer a hybrid profile. Paraná and neighbors combine robust incomes with policy stimuli such as IPVA tax relief on small-engine bikes. Cross-border component flows with Argentina optimize logistics costs, while adventure-touring incentives promote leisure segments. Collectively, regional nuances illustrate that the Brazilian two-wheeler market is not monolithic but a mosaic of income bands, infrastructure gaps, and policy preferences.

Competitive Landscape

Major players like Honda Motors, Yamaha Motor, Shineray, and Voltz are leading Brazil’s motorcycle market with a commanding share, supported by high-efficiency production at its Manaus facility, where a new unit rolls off the line every few seconds. This scale reinforces its leadership while setting a high benchmark for competitors. Scale underwrites cost leadership and a parts network that stretches into remote Amazonian towns. Electric upstarts such as Voltz Motors bypass traditional dealers to sell subscription-battery models online, chipping at incumbents’ urban strongholds.

Platform economics recast competition. Partnerships with 99 and iFood give OEMs locked-in demand but force innovation in fleet-optimized features. Meanwhile, micro-mobility operators like Tembici deliver more than 2 million monthly bike-share rides, a direct substitute for short urban trips[3]“Tembici atinge 2 milhões de viagens,” Valor Capital Group, valorcapitalgroup.com. Manufacturers answer with subscription financing, extended warranties, and flex-fuel options to preserve relevance.

Regulatory acumen becomes strategic. Compliance with CONTRAN technical rules absorbs engineering bandwidth that favors incumbents. International entrants such as Hero MotoCorp establish wholly owned subsidiaries to localize production and meet flex-fuel standards. This proves that the Brazilian two-wheeler market attracts capital even under competitive pressure.

Brazil Two Wheeler Industry Leaders

Honda Motor Co., Ltd.

Yamaha Motor Co., Ltd.

Shineray

Voltz Motors

Dafra Motos

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: In February 2025, São Paulo-based battery-swapping company Vammo completed over 1 million battery swaps in just over a year. This service saved customers approximately USD 1.3 million in fuel costs and prevented 3,050 tons of CO2 emissions.

- January 2025: The Paraná State Government plans to exempt motorcycles with engine capacities up to 170cc from the Motor Vehicle Property Tax (IPVA) and submit this proposal to the Paraná State Legislative Assembly (ALEP).

Brazil Two Wheeler Market Report Scope

| Motorcycles |

| Scooters |

| Mopeds |

| Internal Combustion Engine (ICE) | Below 100 cc |

| 101-125 cc | |

| 126-250 cc | |

| Above 250 cc | |

| Electric Two-Wheelers (E2W) | Below 1 kW |

| 1 kW - 3 kW | |

| 3 kW - 7.5 kW | |

| Above 7.5 kW | |

| Others (CNG/LPG) |

| Chain Drive |

| Belt Drive |

| Shaft Drive |

| Personal Use |

| Commercial Use |

| Delivery and Fleet Services |

| Online |

| Offline |

| By Vehicle Type | Motorcycles | |

| Scooters | ||

| Mopeds | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | Below 100 cc |

| 101-125 cc | ||

| 126-250 cc | ||

| Above 250 cc | ||

| Electric Two-Wheelers (E2W) | Below 1 kW | |

| 1 kW - 3 kW | ||

| 3 kW - 7.5 kW | ||

| Above 7.5 kW | ||

| Others (CNG/LPG) | ||

| By Drive Type | Chain Drive | |

| Belt Drive | ||

| Shaft Drive | ||

| By End Use | Personal Use | |

| Commercial Use | ||

| Delivery and Fleet Services | ||

| By Sales Channel | Online | |

| Offline | ||

Key Questions Answered in the Report

What is the current value of the Brazil two-wheeler market?

The Brazil two-wheeler market size stands at USD 5.74 billion in 2025 and is forecast to reach USD 7.06 billion by 2030.

How fast is electric adoption growing in Brazil’s two-wheeler space?

Electric two-wheelers are projected to post a 12.41% CAGR through 2030, the fastest rate among propulsion types.

Which vehicle type leads sales volumes in Brazil?

Motorcycles dominate with a 70.42% market share in 2024, driven by versatility and cost-efficiency.

Why are delivery fleets important for manufacturers?

On-demand platforms provide bulk orders that stabilize factory output and fuel the fastest-growing 9.43% CAGR end-use segment.

What regional markets show the highest penetration?

Northern and Northeastern municipalities record higher motorcycle-to-car ratios, making them key growth corridors.

Page last updated on: