Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

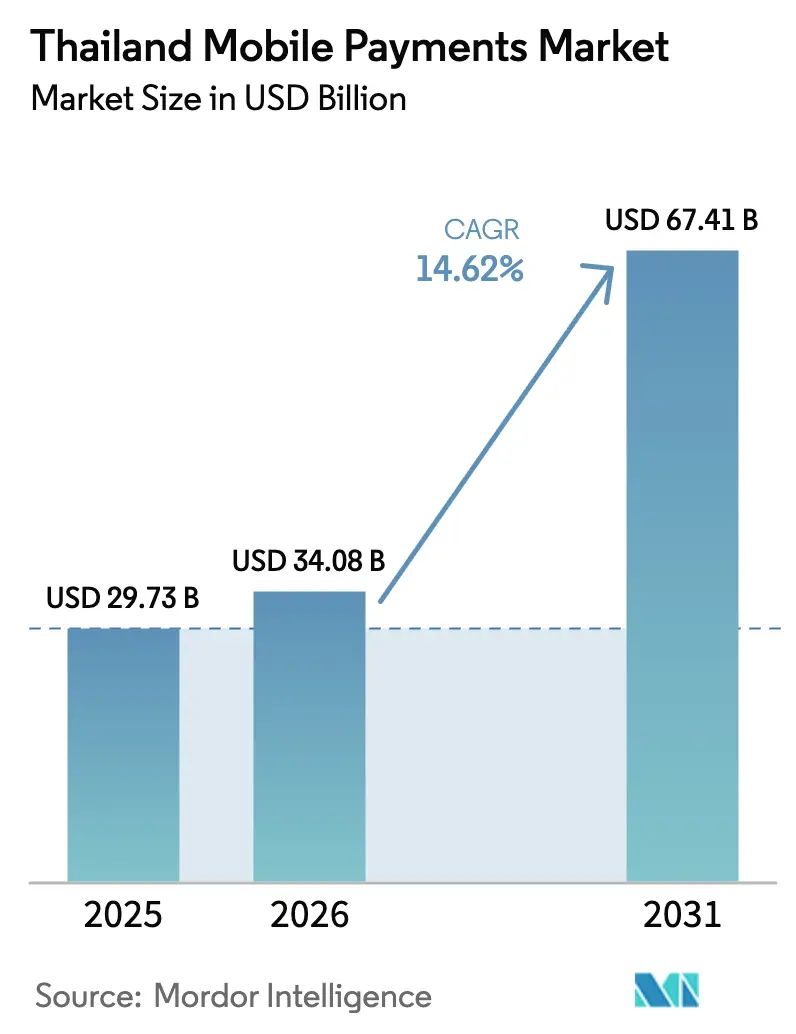

| Base Year Market Size (2025) | USD 29.73 Billion |

| Market Size (2026) | USD 34.08 Billion |

| Market Size (2031) | USD 67.41 Billion |

| Growth Rate (2026 - 2031) | 14.62% CAGR |

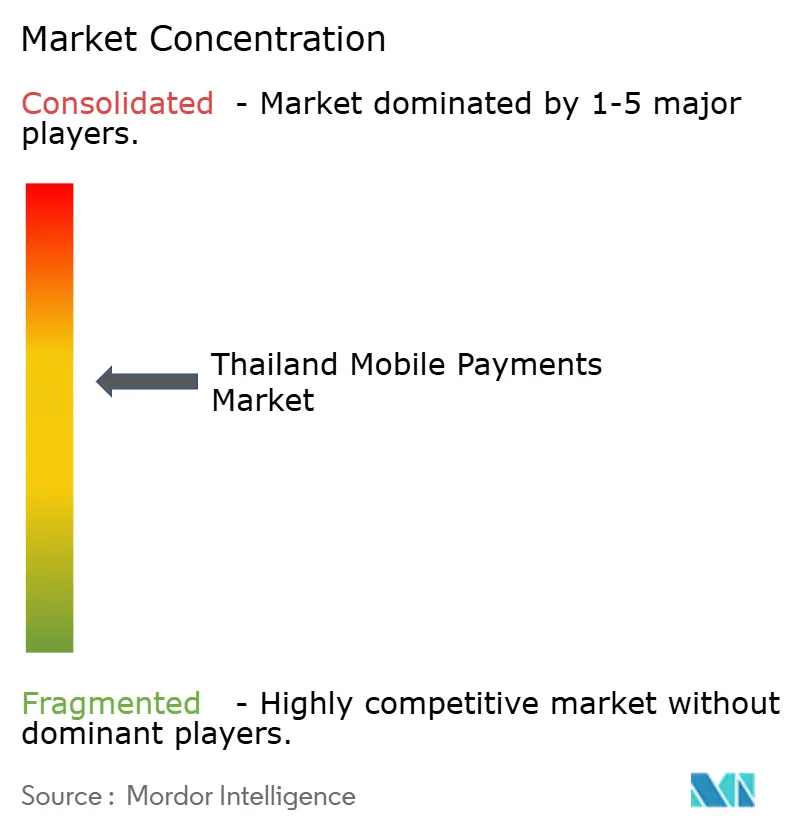

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Mobile Payments Market Analysis by Mordor Intelligence

Thailand mobile payments market size in 2026 is estimated at USD 34.08 billion, growing from 2025 value of USD 29.73 billion with 2031 projections showing USD 67.41 billion, growing at 14.62% CAGR over 2026-2031. Growth stems from universal PromptPay rails, 90% smartphone penetration, nationwide 5G rollout, and a sharp tourism rebound that together accelerate digital payment velocity. QR code ubiquity lowers merchant entry barriers, while the rapid shift to social-commerce shortens the learning curve for remote payments. Government approval of three virtual-bank consortia adds competitive stimulus, and foreign strategic investments such as MUFG’s USD 195 million infusion into Ascend Money supply fresh capital for product innovation. At the same time, rising cybersecurity incidents, rural cash affinity, and compliance costs for micro-merchants temper the growth curve.

Key Report Takeaways

- By transaction channel, e-commerce led with a 46.25% revenue share of the Thailand mobile payments market in 2025, whereas P2P transfers are projected to post the fastest 16.6% CAGR to 2031.

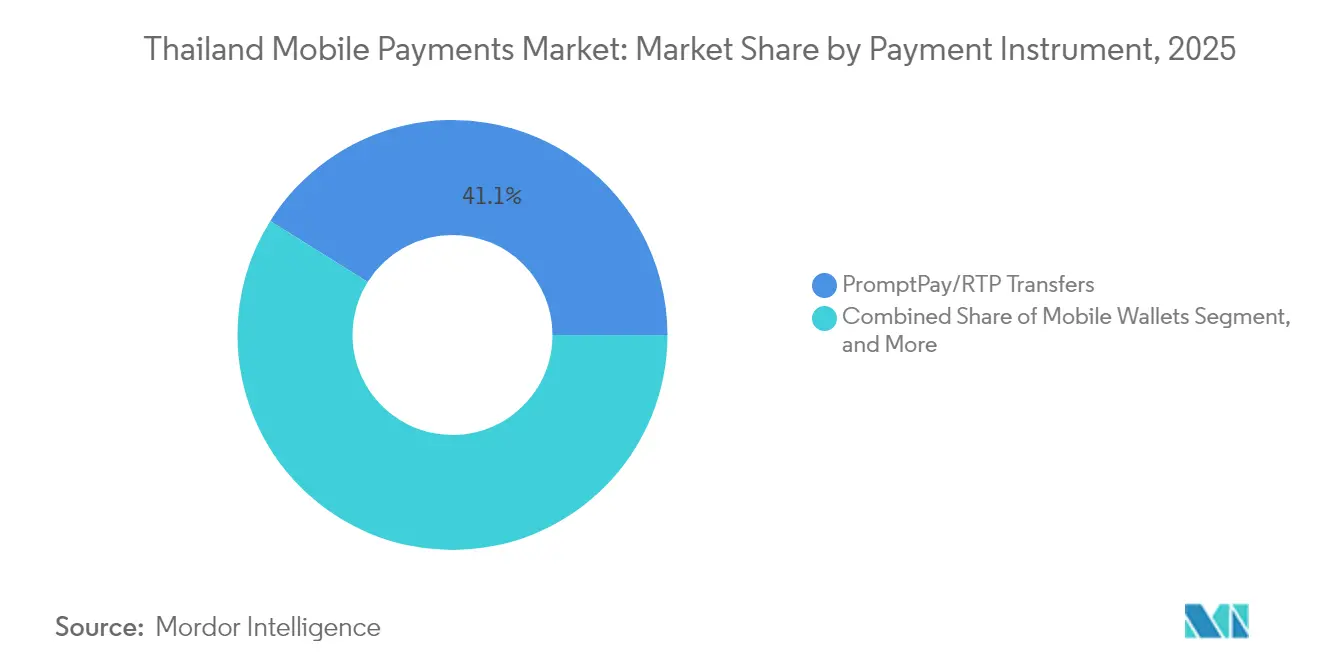

- By payment instrument, PromptPay/RTP transfers captured 41.10% of the Thailand mobile payments market share in 2025, while mobile wallets are forecast to climb at a 16.2% CAGR through 2031.

- By technology, QR code solutions commanded 42.15% of the Thailand mobile payments market size in 2025; sound-wave and other alternative technologies are advancing at a 16.1% CAGR over the same horizon.

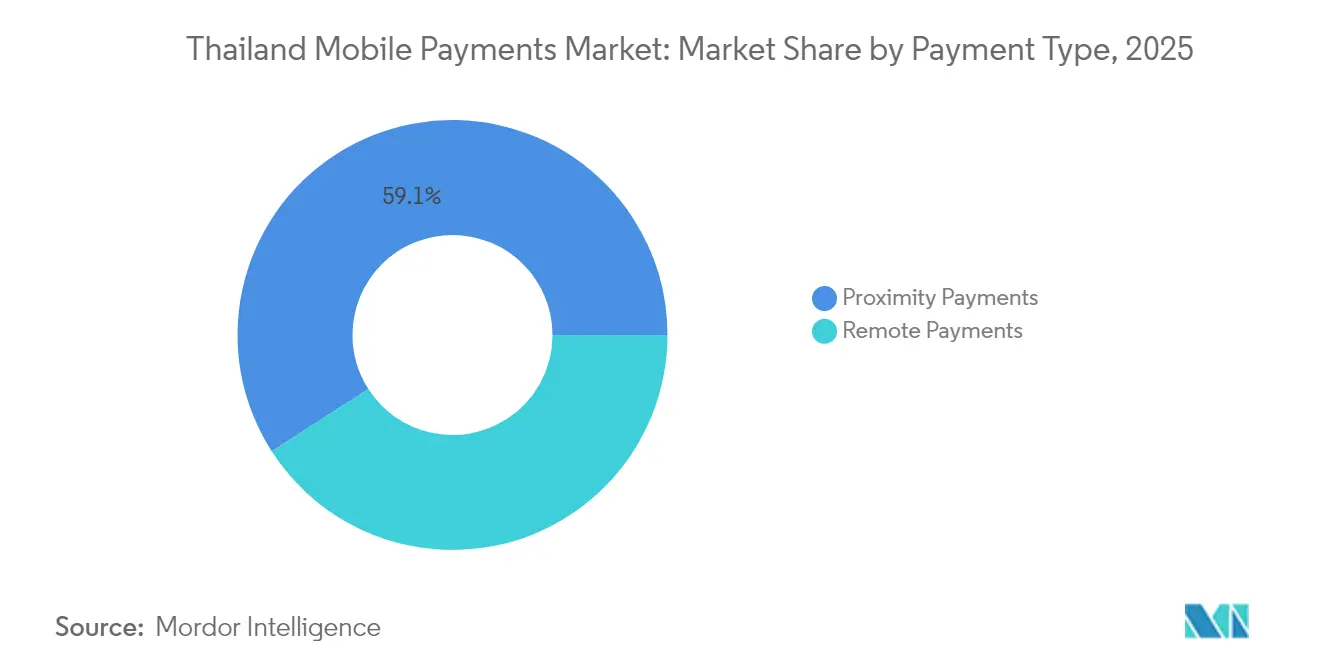

- By payment type, proximity payments accounted for 59.10% of the Thailand mobile payments market 2025 value, yet remote payments represent the fastest-growing category at a 15.3% CAGR.

- By end-user industry, retail and FMCG contributed 33.20% of the Thailand mobile payments market 2025 value, whereas hospitality and tourism payments are projected to rise at a 16.1% CAGR.

- By region, the Bangkok Metropolitan Region held 43.30% share of the Thailand mobile payments market in 2025, while the Northeastern region is expanding at a 15.9% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive e-commerce growth | +3.2% | Bangkok, Central | Short term (≤ 2 years) |

| Smartphone and 5G penetration surge | +2.8% | Nationwide | Medium term (2-4 years) |

| National PromptPay program scaling | +2.1% | Nationwide, ASEAN links | Long term (≥ 4 years) |

| ASEAN cross-border QR interoperability | +1.9% | Border provinces, tourism hubs | Medium term (2-4 years) |

| Tap-to-phone for MSME acceptance | +1.4% | Urban centers, secondary cities | Short term (≤ 2 years) |

| Social-commerce wallet embedding | +1.6% | Nationwide, youth cohorts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive E-commerce Growth Drives Payment Digitization

Thailand’s e-commerce boom fosters habitual mobile checkout, making friction-free wallets indispensable for both merchants and shoppers.[1]Finextra, “MiFinity Expands Payment Options in Asia,” finextra.com Deep wallet integration inside super-apps keeps users within a single ecosystem, locking in repeat spend. Cross-platform payment interoperability now lets buyers preserve preferred payment settings across multiple marketplaces, pushing wallet stickiness from online channels into offline QR-enabled stores. Partnerships such as ShopeePay’s tie-up with the National Savings Fund broaden financial inclusion, funneling fresh users into regulated e-wallet rails. The cadence of flash-sales and live-stream commerce also amplifies micro-transaction frequency, enlarging fee pools for providers.

Smartphone and 5G Network Infrastructure Expansion

Nationwide 5G has lowered latency and boosted bandwidth, enabling biometric verification and AI-driven fraud filters in real time.[2]Grab, “Grab TH—The Everyday Everything App,” grab.com Budget Android handsets priced below USD 100 have pushed smartphone penetration past 90%, minimizing device-access hurdles. Rural towers installed under the Universal Service Obligation Fund shrink the urban–rural gap, widening the Thailand mobile payments market addressable base. High-speed links also power emerging modalities such as sound-wave payments, which sidestep the camera alignment needed for QR codes. Telecom operators monetize network upgrades via bundled wallet promotions, turning connectivity into a direct acquisition lever.

National PromptPay Program Cross-Border Scaling

PromptPay processed over 15 billion domestic transactions in 2024 and now clears retail payments with eight ASEAN peers, flattening foreign-exchange frictions. Thai tourists in Singapore or Vietnam scan familiar QR codes, while inbound travelers remit funds in their home wallets at real-time FX rates. Network effects reinforce domestic dominance: every new overseas tie-in raises local utility, which in turn boosts daily active users. Banks layer value-added services, bulk payroll, escrow, and invoice financing on top of PromptPay rails, migrating B2B flows that traditionally sat on closed-loop card networks.

ASEAN Cross-Border QR Code Interoperability

The joint central-bank framework sets common payload data, encryption, and settlement standards, allowing merchants to accept multiple foreign wallets with a single QR sticker. Transaction fees drop below 1%, undercutting traditional acquirers. For Thailand’s coastal resort towns, the change widens acceptance of Chinese and Malaysian wallets, recovering tourist spend lost during the pandemic lull. Merchants gain incremental traffic without POS hardware upgrades, feeding back into a virtuous cycle of acceptance and usage.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cyber-fraud and data breaches | −2.1% | Urban centers | Short term (≤ 2 years) |

| Persistent cash preference in rural areas | −1.8% | Northern, Northeastern provinces | Long term (≥ 4 years) |

| MDR/compliance burden on micro-merchants | −1.3% | Nationwide | Medium term (2-4 years) |

| Regulatory flux on in-wallet credit/BNPL | −0.9% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Cyber-Fraud and Data Breaches Undermine Consumer Confidence

Thailand logged 168 million scam SMS and calls in 2024, the region’s highest tally, and several multi-million-record breaches seeded personal data on dark-web forums. Consumers equate digital rails with higher theft risk, slowing wallet adoption among risk-averse demographics. Compliance with the Personal Data Protection Act has raised fixed costs for smaller fintechs, diverting funds from innovation to security audits. Media coverage of fraud incidents prompts banks to impose stricter KYC checks, elongating onboarding time and adding friction to first-use transactions.

Persistent Cash Preference in Rural Areas Limits Market Expansion

Cash still represents 46% of national transaction value, with rural districts showing elevated reliance due to habits, spotty connectivity, and thin merchant acceptance.[3]Bangkok Post, “Virtual Banks to Be Announced in June,” bangkokpost.com For many micro-retailers, even a sub-1% MDR is viewed as a tax on razor-thin margins. Farmers receiving cash crop payments often convert e-money to physical notes immediately, blunting digital retention. Government incentive schemes subsidized QR readers or tax rebates soften resistance, yet require sustained funding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Instrument: PromptPay Dominance Faces Wallet Challenge

PromptPay transfers captured 41.10% of the Thailand mobile payments market share in 2025, a lead built on fee-free P2P and merchant acceptance baked into every domestic bank app. Mobile wallets, however, are swelling at a 16.2% CAGR and could expand the Thailand mobile payments market size by USD 13.4 billion between 2026 and 2031 as TrueMoney penetrates cash-centric provinces and Rabbit LINE Pay rides urban transit systems.

TrueMoney leverages its 39,000 agent outlets to convert cash for the unbanked, while Rabbit LINE Pay bundles ride fares with micro-insurance, turning daily commutes into recurring wallet engagement. Card-linked wallets maintain traction among affluent urbanites who prefer revolving credit, whereas carrier billing survives in niche content subscriptions. Siam Commercial Bank’s tap-to-pay feature blurs category lines by embedding NFC directly into banking apps, delivering card-grade convenience without plastic issuance. Biometrics such as facial recognition shorten authentication steps, partly offsetting fraud fears and pushing high-ticket transactions onto wallet rails.

By Transaction Channel: E-commerce Leadership Drives Digital Habits

E-commerce contributed 46.25% of 2025 transaction value, anchoring the Thailand mobile payments market around app-based checkouts and one-click repeat orders. Cross-platform promotions funnel wallet users from Shopee flash sales to offline QR-enabled coffee chains, reinforcing payment familiarity.

P2P transfers, forecast at a 16.6% CAGR, benefit from gig-economy payouts and family remittances that bypass ATM queues. In-store POS volumes rise via camera-based QR scans and nascent tap-to-phone software that turns Android devices into card readers. Bill payments move online as utilities embed PromptPay QR on invoices, while cross-border tourists spend rebounds on QR interoperability, lifting average merchant basket sizes during high-season months.

By Payment Type: Proximity Payments Maintain Edge Despite Remote Growth

Proximity payments held a 59.10% share in 2025, thanks to city-wide QR saturation and consumer comfort with scan-and-go flows. Pandemic-era hygiene preferences entrenched touch-free habits, boosting average daily proximity transactions by 19% year over year.

Remote payments are heading for a 15.3% CAGR, propelled by social-commerce streams where influencers embed buy-links in live video. Sound-wave and tokenized links let users authorize store pickups remotely, blurring lines between payment types. Biometric security now underpins both modes, reducing false-positive declines and maintaining confidence for higher-value online orders.

By End-User Industry: Retail Foundation Supports Tourism Recovery

Retail and FMCG outlets generated 33.20% of 2025 volume, forming a dense acceptance footprint that accelerates new-user onboarding through day-to-day purchases. QR-only small stores avoid card terminal rents, widening acceptance to market stalls and street food vendors.

Hospitality and tourism transactions are on pace for a 16.1% CAGR as inbound visitor numbers rebound to pre-2020 levels. Hotels, duty-free shops, and tour operators adopt multi-currency QR codes to capture spend from Alipay and WeChat Pay users without bearing foreign-card fees. Transportation, utilities, healthcare, and education verticals each unlock steady usage via recurring billing and subsidy distribution programs.

By Technology: QR Code Ubiquity Enables Alternative Innovation

QR systems accounted for 42.15% of 2025 transaction value, their dominance amplified by a central bank-issued common standard and zero hardware cost for merchants. Government stimulus in 2024 distributed free printed QR sheets to 1.1 million micro-SMEs, accelerating countrywide acceptance.

Alternative modalities such as ultrasonic sound waves rise at a 16.1% CAGR, enabling eyes-free transactions useful for visually impaired users and crowded transit. NFC, though secure, remains price-sensitive because dedicated chips push handset costs upward. USSD menus sustain inclusion for feature-phone owners, while IoT-embedded “invisible payments” in fuel pumps and parking meters surface as next-wave pilots.

Geography Analysis

Bangkok held 43.30% of the 2025 value, underpinned by 98% 4G/5G coverage, the highest GDP per capita, and dense clusters of malls and transit merchants. Bangkok Metropolitan Region accounts for nearly half of the current transaction value, powered by universal PromptPay adoption, abundant POS infrastructure, and a large white-collar workforce with high discretionary spending. The city’s app-savvy commuters rely on Rabbit LINE Pay and TrueMoney for daily rail and bus fares, reinforcing usage frequency. The local fintech hub attracts talent and accelerates prototype cycles, keeping Bangkok at the forefront of payment innovation. Foreign tourists also inject cross-border QR volumes, particularly from China, Malaysia, and Singapore, lifting blended yield for acquirers during peak travel periods.

The Central region, Thailand’s manufacturing heartland, pushes B2B digital payments as suppliers migrate invoicing to real-time rails to shorten working-capital cycles. Online grocery and next-day delivery startups, clustered around Ayutthaya and Samut Prakan, broaden consumer wallet usage beyond leisure spending. Government e-procurement portals in the region default to PromptPay settlement, pulling smaller contractors into digital rails and shrinking cash leakage.

Northern provinces marry tourism flows with agribusiness modernization. Chiang Mai’s boutique hotels enable multi-currency QR acceptance to welcome regional travelers. Simultaneously, tea and coffee co-operatives shift producer payments onto wallets, reducing cash-handling losses. Cross-border trucking to Laos and Myanmar leverages QR remittance to bypass costly money changers, further raising mobile payment utility in the region.

The Northeastern region’s 15.9% CAGR is catalyzed by government digital-subsidy payouts and agritech programs that route crop payments through e-money rather than cash. Northeastern Thailand shows the highest trajectory as state-issued digital-wallet stipends for fertilizer and fuel arrive directly on phones, displacing paper vouchers. Community convenience stores now accept QR for everyday staples, shortening round-trip trips to provincial banks. Fintech field officers run digital literacy drives, helping elderly citizens convert government support into wallet purchases without third-party cash-out fees. Agricultural IoT pilots that couple crop-monitoring with instant financing inject additional transaction flows into local wallets.

Southern provinces reflect tourism-led demand peaks. Phuket and Krabi merchants integrate Alipay and WeChat Pay via Thai acquirers, capturing higher-margin duty-free sales. Cross-border commuters from Malaysia use PromptPay’s linked DuitNow network for micro-retail buys, highlighting interoperability dividends. Small fishing communities leverage carrier-billing micropayments for ice, fuel, and daily supplies, diversifying payment channels further.

Competitive Landscape

TrueMoney and Rabbit LINE Pay collectively command over 75% of the e-money float, anchoring moderate concentration in the Thailand mobile payments market. TrueMoney’s parent, Ascend Money, leverages CP Group’s retail empire, 7-Eleven, Lotus’s, and Makro, to lock in merchant density, while Rabbit LINE Pay piggybacks on LINE’s 54 million chat users for instant scale. Both roll out micro-savings and insurance, layering stickier services atop payments.

PromptPay, although a public utility, competes indirectly by embedding free transfers inside every bank app, thus eroding wallet P2P margins. Banks react by enhancing app UX and bundling tap-to-pay NFC to defend their share. International entries such as Alipay and WeChat focus on traveler corridors rather than local accounts, softening head-on rivalry but raising merchant expectations for multi-currency support.

The 2026 debut of three virtual banks, Krungthai-AIS-Gulf-OR, SCBX-KakaoBank-WeBank, and Ascend Money-Ant International, will meld banking, payments, and lifestyle ecosystems. Expect bundled zero-fee accounts, high-yield micro-deposits, and embedded credit lines tied to wallet histories. Smaller gateways such as 2C2P counter with white-label tap-to-pay for SMEs, while telecom operators dtac and True Corp cross-sell top-up wallets utilizing airtime credits. Continual differentiation pivots on AI-driven fraud analytics, biometric UX, and ultra-low-cost merchant onboarding to capture rural greenfield.

Regulatory policy balances competition and security: the Bank of Thailand maintains cybersecurity audits and real-time fraud monitoring, compelling all providers to invest in ISO 27001 compliance. Providers that achieve best-in-class fraud loss ratios gain reputational lift and corporate merchant contracts. Conversely, providers caught in data-leak headlines hemorrhage trust and face tougher KYC mandates, widening the gap between tier-one and fringe players.

Thailand Mobile Payments Industry Leaders

True Money Co., Ltd.

Rabbit LINE Pay Co., Ltd.

ShopeePay (Thailand) Co., Ltd.

Advanced Info Service Public Company Limited

Grab Holdings Limited (GrabPay)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bank of Thailand granted digital bank licenses to Krungthai-AIS-Gulf-OR, SCBX-KakaoBank-WeBank, and Ascend Money-Ant International, paving the way for 2026 launches.

- April 2025: Grab Thailand unveiled its S.M.A.R.T. roadmap to deepen ride-hail, food, and parcel synergies that lift GrabPay throughput.

- March 2025: ShopeePay and the National Savings Fund partnered to distribute social-security top-ups through e-wallet rails.

- March 2025: MiFinity integrated Rabbit LINE Pay via a Finextra-backed switch to ease cross-border wallet top-ups.

- March 2025: GrabX innovation program showcased AI route-optimization and family-account payment delegation.

- February 2025: Grab Holdings disclosed talks to acquire Indonesia’s GoTo Group in a USD 7 billion super-app consolidation move.

Thailand Mobile Payments Market Report Scope

Mobile payment is a payment made for a product or service through a portable electronic device such as a tablet or cell phone. The study tracks mobile payment applications based on transaction type: Proximity and Remote payment. The study tracks key market metrics, underlying growth influencers, and significant industry vendors, supporting Thailand's mobile payments market estimates and growth rates throughout the anticipated period. This report looks at COVID-19's overall influence on the Country's payment ecosystem.

Thailand Mobile Payments Market is segmented by type (proximity payment, remote payment). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Payment Instrument

| PromptPay/RTP Transfers |

| Mobile Wallets (TrueMoney, Rabbit LINE Pay, etc.) |

| Card-based Mobile Payments |

| Carrier Billing/Others |

By Transaction Channel

| In-store POS |

| E-commerce |

| P2P Transfers |

| Bill and Government Payments |

| Cross-border/Tourist |

By Payment Type

| Proximity Payments |

| Remote Payments |

By End-User Industry

| Retail and FMCG |

| Transportation and Mobility |

| Hospitality and Tourism |

| Utilities and Telecom |

| Healthcare and Education |

| Other End-User Industries |

By Technology

| QR Code |

| NFC/Tokenised Card |

| USSD/STK |

| Sound-wave and Other Alt-Tech |

By Region

| Bangkok Metropolitan Region |

| Central |

| Northern |

| Northeastern |

| Southern |

| By Payment Instrument | PromptPay/RTP Transfers |

| Mobile Wallets (TrueMoney, Rabbit LINE Pay, etc.) | |

| Card-based Mobile Payments | |

| Carrier Billing/Others | |

| By Transaction Channel | In-store POS |

| E-commerce | |

| P2P Transfers | |

| Bill and Government Payments | |

| Cross-border/Tourist | |

| By Payment Type | Proximity Payments |

| Remote Payments | |

| By End-User Industry | Retail and FMCG |

| Transportation and Mobility | |

| Hospitality and Tourism | |

| Utilities and Telecom | |

| Healthcare and Education | |

| Other End-User Industries | |

| By Technology | QR Code |

| NFC/Tokenised Card | |

| USSD/STK | |

| Sound-wave and Other Alt-Tech | |

| By Region | Bangkok Metropolitan Region |

| Central | |

| Northern | |

| Northeastern | |

| Southern |

Key Questions Answered in the Report

How large is the Thailand mobile payments market in 2026?

It is projected to rise from USD 29.73 billion in 2025, following a 14.62% CAGR, positioning 2026 value at roughly USD 34.08 billion.

Which payment instrument leads consumer adoption in Thailand?

PromptPay real-time transfers remain the dominant instrument with 41.10% 2025 share, though mobile wallets are growing faster at 16.2% CAGR.

What role do QR codes play in Thai mobile payments?

QR codes processed 42.15% of 2025 transaction value because they require no hardware investment and are now interoperable across eight ASEAN countries.

Will virtual banks intensify competition?

Yes; three consortia licensed for 2026 launch will bundle banking and payments, likely compressing fees and spurring product innovation.

Why is the Northeastern region attractive for payment providers?

Government subsidy disbursement and 5G coverage are accelerating wallet uptake, pushing the region toward a market-leading 15.9% CAGR through 2031.

Page last updated on: