Thailand Floriculture Market Size and Share

Thailand Floriculture Market Analysis by Mordor Intelligence

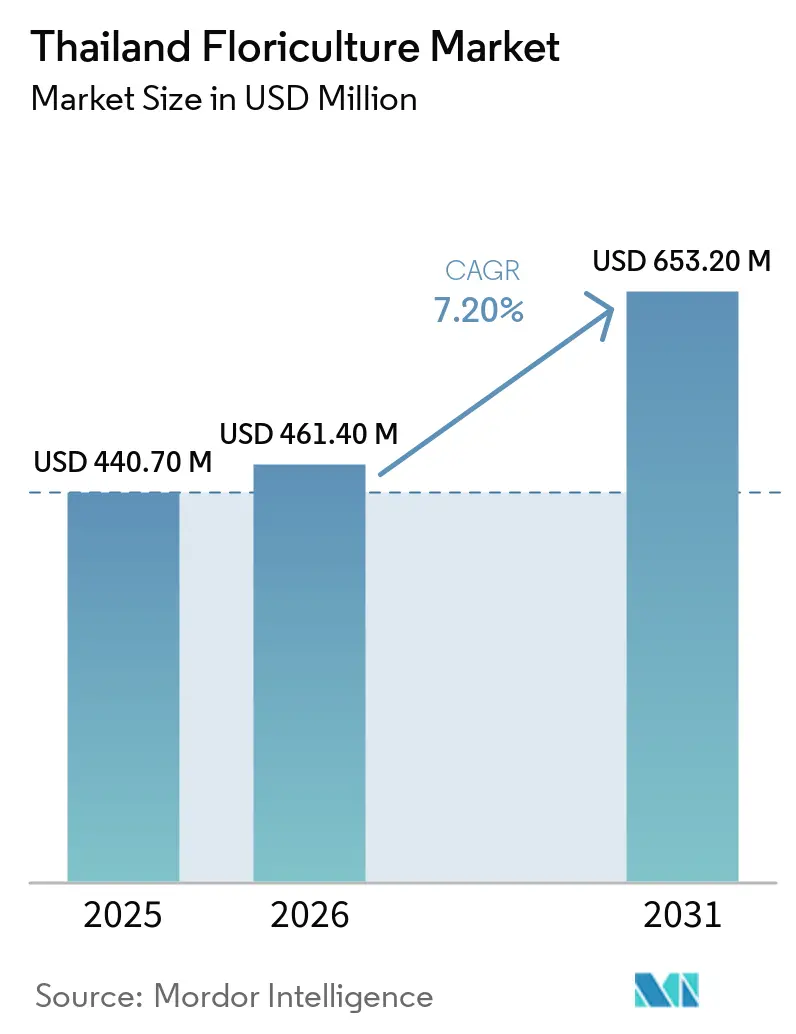

The Thailand floriculture market size was valued at USD 440.7 million in 2025 and estimated to grow from USD 461.4 million in 2026 to reach USD 653.2 million by 2031, at a CAGR of 7.2% during the forecast period (2026-2031). The Thailand floriculture market is supported by strong domestic demand, as flowers such as jasmine, marigold, and lotus are widely used in daily religious practices, ceremonies, and garland-making. Local consumption remains the primary driver of the market, with domestic sales significantly outweighing export-oriented ornamental trade. The Thailand floriculture market also benefits from the country’s strong orchid position, with fresh-cut orchids contributing more than 70% of export value and helping Thailand keep its standing as the world’s top orchid exporter[1]Source: Oramon Sapthaweetham, “Thailand Retains Crown as World's No 1 Orchid Exporter,” The Nation Thailand, nationthailand.com. Urban flower buying is widening through online florists and social commerce, which supports premium bouquet sales and helps growers respond faster to shifts in demand in Bangkok and other large cities. Decorative demand is also rising as hotels, events, and destination weddings add recurring floral requirements, while exporters are widening their reach beyond traditional Asia-Pacific buyers into Europe and the Middle East. At the same time, the Thai floriculture market still faces pressure from climate volatility, cold-chain gaps, and export compliance requirements, which reward larger integrated growers that can manage postharvest quality, documentation, and long-haul logistics better than smaller farms can.

Key Report Takeaways

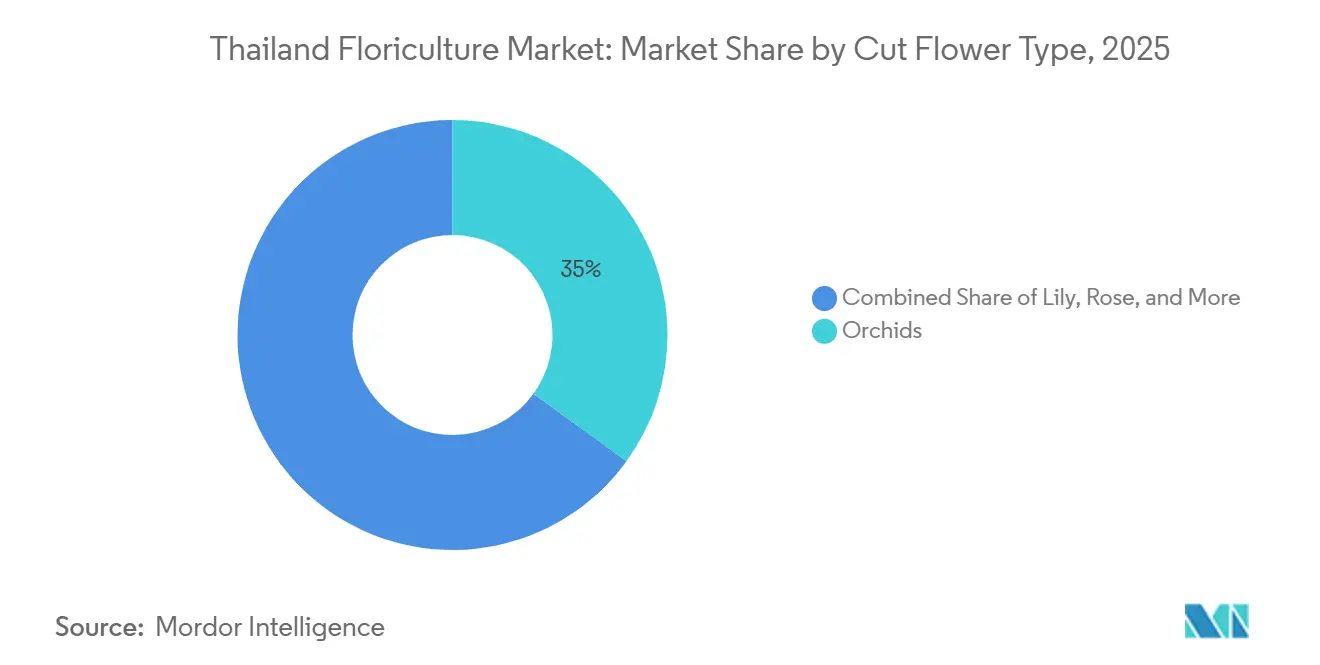

- By cut flower type, orchids held 35% of the Thailand floriculture market share in 2025, while the lily segment market size is projected to grow at an 8.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Floriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural and religious flower use anchors daily demand | +1.8% | Domestic Thailand, with spillover to Thai diaspora communities in Asia-Pacific and North America | Short term (≤ 2 years) |

| Tourism and hospitality recovery lifts decorative flower demand | +1.6% | Domestic Thailand, strongest in Bangkok, Phuket, and Chiang Mai, with secondary pull from Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Thailand's orchid export reputation supports premium positioning | +1.4% | Global, strongest in the United States, Japan, Vietnam, the European Union, and the Middle East | Long term (≥ 4 years) |

| Online florists and social commerce widen urban reach | +1.0% | Domestic Thailand, strongest in Bangkok and secondary cities, with early spillover to Asia-Pacific and North America | Medium term (2-4 years) |

| International horticulture expo activity boosts showcase demand | +0.5% | Domestic Thailand, especially Udon Thani, Chiang Rai, and Korat, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Orchid development plan improves quality and postharvest readiness | +0.6% | Domestic Thailand and export corridors to Europe, the Middle East, and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cultural and Religious Flower Use Anchors Daily Demand

The Thailand floriculture draws unusual stability from daily cultural and religious consumption that is less exposed to income swings than discretionary gift buying. Jasmine, marigold, and lotus are bought each day for home shrines, temple offerings, and garlands, which creates a steady base for growers and traders across the country. Local consumption remains the primary driver of the market, with domestic sales significantly outweighing export-oriented ornamental trade. This pattern also channels a large share of daily volume through wholesale centers such as Pak Klong Talad, where ritual demand rises at predictable points around Songkran, Buddhist Lent, and Loy Krathong. That seasonal rhythm gives growers a hedge when export pricing weakens because local buying does not disappear during softer external cycles. Younger urban buyers are also shifting part of their spending toward packaged bouquets, which adds premium layers to a demand base that already exists, instead of replacing traditional flower use. As a result, the Thailand floriculture market has a domestic floor that many export-led flower economies do not have.

Tourism and Hospitality Recovery Lifts Decorative Flower Demand

Decorative demand is rising as hotel investment, property openings, weddings, and event activity create recurring procurement contracts for floral suppliers in the Thailand floriculture market. Thailand’s hotel investment volume in 2025 increased 11.0% above 2024 levels, which expanded the base of properties that need lobby arrangements, restaurant displays, spa flowers, and event florals. Bangkok and Phuket added more than 5,100 new rooms during the year, which means flower demand is tied not only to visitor flows but also to the physical growth of the hospitality stock. That matters because hotel flower spending is often linked to brand standards and service formats, which makes it more repeatable than casual tourist purchases[2]Source: JLL, “Bangkok Hotel Market Report Q4 2025,” JLL Asia Pacific Research, research.jllapsites.com . Songkran booking surges in Chiang Mai, Phuket, and Koh Samui in 2025 also widened the seasonal demand window for floral decoration and event use. Destination weddings in Phuket are adding another high-value channel, and larger growers are already shaping product lines around these repeat contracts. This keeps decorative procurement as one of the clearest volume and value growth paths within the Thailand floriculture market.

Thailand's Orchid Export Reputation Supports Premium Positioning

Thailand’s orchid record now works as a quality signal in foreign procurement, and that has become a direct support for pricing in the Thailand floriculture market. The country continues to lead global orchid exports, with orchids accounting for a significant share of the decorative plant trade. Thai suppliers maintain a competitive edge by offering a wide range of orchid varieties such as Dendrobium, Mokara, Vanda, Aranda, Oncidium, and Phalaenopsis, allowing them to cater to multiple price segments rather than relying on a single product type. This diversity provides buyers with greater sourcing flexibility and encourages repeat purchases. Rising demand from both established and emerging international markets further reinforces Thailand’s export position, keeping orchids at the core of the country’s floriculture market and supporting its premium positioning globally.

Online Florists and Social Commerce Widen Urban Reach

The Thailand floriculture market is also changing because online florists and social commerce are making flower buying easier for urban consumers. Ordering through LINE, Instagram, and TikTok Shop shortens the path from browsing to checkout, which is especially important for repeat gifting and same-day bouquet demand. Online channels often support better pricing than loose wholesale trade because they bundle packaging, design, and delivery into the final offer. This shift matters for growers because digital orders reveal demand patterns faster and help them reduce excess production of lower-margin stems. Growers near Bangkok are beginning to use those signals to move more area toward higher-value orchids and lilies while managing common ritual flowers more carefully. Thailand has a well-established base of registered businesses across flowers, decorative plants, and perennial plants, with the sector showing improving profitability in recent years. This trend indicates that digital channels are expanding overall revenue generation in the Thailand floriculture market, rather than simply shifting sales between traditional and online outlets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate volatility and disease pressure reduce yield stability | -1.2% | Domestic Thailand, strongest in Central, Northern, and Northeastern production areas, with spillover to export markets | Short term (≤ 2 years) |

| Phytosanitary and CITES compliance slows export cycles | -0.8% | Global, strongest on Europe, North America, and Middle East corridors | Medium term (2-4 years) |

| Cold-chain gaps increase spoilage risk for fresh orchids | -0.6% | North America, the Middle East, and Africa, with the greatest pressure on long-haul routes | Medium term (2-4 years) |

| Imported temperate flowers pressure local bouquet margins | -0.5% | Domestic Thailand, especially Bangkok and other urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climate Volatility and Disease Pressure Reduce Yield Stability

Climate pressure remains one of the clearest limits on the Thailand floriculture market because production quality and harvest timing are highly sensitive to rainfall shifts, flooding, drought, and temperature stress. Orchid cultivation in Thailand has faced a period of contraction, influenced by climate-related stress and broader supply disruptions. Beyond direct production impacts, inconsistent supply can weaken exporter reliability, prompting international buyers to diversify sourcing to alternative countries such as Kenya, Colombia, and Ecuador, often with lasting effects on trade relationships. In response, controlled-environment agriculture is emerging as a key pathway for climate adaptation in the floriculture sector, creating opportunities for the adoption of advanced greenhouse technologies. However, the transition may be challenging for smaller growers due to high investment requirements. Overall, climate volatility is likely to affect yields, reduce export consistency, and contribute to increased market consolidation in the Thailand floriculture industry.

Phytosanitary and CITES Compliance Slows Export Cycles

Compliance is another major drag on the Thailand floriculture market because orchid shipments face layered documentation requirements before they can leave the country and clear foreign borders. Exporters need phytosanitary certificates, CITES (Convention on International Trade in Endangered Species of Wild Fauna and Flora) permits, and Certificates of Origin, and some destinations also require additional supporting paperwork. This squeezes already-short handling windows because fresh-cut stems lose value with every hour that passes between harvest and arrival. The burden is heaviest for smaller producer-exporters that do not have in-house compliance staff or fixed broker relationships. Larger integrated operators can manage the process more smoothly, which shifts export power toward companies that control their own paperwork and postharvest systems AIPH.ORG. Another issue is that customs offices in different countries may not interpret permit conditions identically, creating unpredictable delays. That makes exporters more cautious about entering unfamiliar destinations and slows the pace at which the Thailand floriculture market can open new routes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cut Flower Type: Orchids Dominate, Lily Captures Premium Growth

Orchids led with 35.0% share in 2025, which kept them at the center of the Thailand floriculture market and reflected the country’s long investment in tissue culture, hybrid breeding, and export-grade handling. The segment’s position rests on depth across Dendrobium, Mokara, Vanda, and Aranda, along with dense grower networks in Nakhon Pathom and Samut Sakhon, and established air freight routes through Suvarnabhumi Airport. Orchid exports from Thailand continued to show steady growth, with Dendrobium remaining the dominant variety in terms of export volume, reflecting its strong commercial demand and suitability for large-scale production. This base makes orchids the benchmark product for price realization, export reputation, and product consistency in the Thailand floriculture industry. Lily is the fastest-growing flower type at an 8.9% CAGR through 2031, reflecting a supply gap in premium hospitality and event use that local farms still do not fully meet. That gap keeps imports important, but it also signals room for local expansion where growers can shorten nursery and crop cycles.

Jasmine, marigold, and lotus occupy the middle tier of the Thailand floriculture market because each serves a stable ceremonial role with lower demand volatility than decorative-only stems. Jasmine and marigold move the highest domestic volume due to temple offerings and garland use, while lotus commands better pricing in ceremonial and hospitality settings. Rose and chrysanthemum remain more exposed to import competition, which limits their growth without stronger productivity gains at the farm level[3]Source: International Association of Horticultural Producers, “Country Profile – Thailand,” AIPH, aiph.org. Research on controlled cultivation conditions for Vanda tissue culture indicates that nursery timelines can be significantly reduced, creating a practical pathway for faster commercialization of high-value flower varieties. In parallel, new varietal introductions from regional research centers are supporting diversification beyond traditional orchid lines. Together, these developments suggest that the Thailand floriculture market is gradually expanding its crop mix, while orchids continue to serve as the core segment.

Geography Analysis

Thailand’s domestic demand is concentrated in key population and cultural centers, where daily ritual flower use across households, temples, ceremonies, and local wholesale markets sustains steady consumption. This geographic concentration of demand supports steady offtake for growers and traders, reinforcing the domestic market as a stable foundation for the overall floriculture sector. The presence of dense urban markets and established wholesale networks further strengthens distribution efficiency across regions. This also enables faster product movement and reduces postharvest losses, supporting overall supply chain stability.

Central Thailand remains the core production hub, with a high concentration of orchid farms, packing facilities, and distribution networks centered around Bangkok and nearby provinces such as Nakhon Pathom, Samut Sakhon, Nonthaburi, and Ratchaburi. This regional clustering supports efficient supply chains, better postharvest handling, and strong connectivity to domestic wholesale markets.

Northern Thailand is gradually increasing its role through specialty orchid cultivation and floriculture tourism. Regional events and growing interest in high-value and niche varieties are supporting diversification within the domestic market. Together, these dynamics highlight a well-established and geographically concentrated market structure with steady growth potential.

Competitive Landscape

The Thailand floriculture market remains fragmented at the grower level, with more than 2,993 registered businesses currently across flowers, decorative plants, and perennials, but export capability is more concentrated among integrated producer-exporters[4]Source: Oramon Sapthaweetham, “Thailand Retains Crown as World's No 1 Orchid Exporter,” The Nation Thailand, nationthailand.com. Those larger operators control tissue culture facilities, postharvest systems, compliance handling, and buyer relationships that smaller farms usually cannot replicate. In practice, competition is shaped less by farm count and more by who can deliver consistent quality, pass phytosanitary checks, and manage long-haul shipments on time. Established players such as Thai Orchids Co., LTD. demonstrate the scale advantages present in the Thailand floriculture market, operating large cultivation areas and supplying multiple international markets. This level of scale supports consistent production, stronger export capabilities, and better cost efficiencies for leading growers.

Strategic moves by leading companies indicate that the Thailand floriculture market is shifting toward deeper vertical integration and product diversification, with firms expanding beyond traditional export models to strengthen resilience and unlock new revenue streams. For instance, Thai Orchids Co., LTD. is advancing its sustainability strategy through solar energy adoption while also developing orchid-based skincare under the WAII brand, broadening its business beyond floriculture. At the same time, LEE & U CO.LTD. is focusing on eco-friendly cultivation and edible orchids, creating access to food and beverage applications and niche markets.

The next phase of competition in the Thailand floriculture market is likely to favor firms that can spread risk across export destinations and sell more than one product format. Tissue-culture-first businesses have room to expand by supplying disease-free flasks and seedlings to rising orchid production areas in Asia, including Indian programs seeking Thai know-how and plant material. Direct contracts with Gulf hospitality buyers also remain an open opportunity because some procurement still moves through multi-layer intermediary chains. Regional Comprehensive Economic Partnership (RCEP)-related documentation advantages should continue to favor larger operators that can certify origin and move quickly through export procedures. This means fragmentation is likely to remain high at the farm tier even as concentration increases in the export-facing layer of the Thailand floriculture market.

Recent Industry Developments

- January 2026: The Ministry of Agriculture and Cooperatives launched the “Blooming Siam Thai Orchid Exhibition” in Nonthaburi, highlighting orchid competitions for the Royal Trophy of H.R.H. Princess Maha Chakri Sirindhorn and promoting orchids under a market-driven, innovation-focused policy framework, thereby strengthening Thailand’s floriculture market through enhanced global branding and export positioning.

- August 2025: Suwannaphum Orchids showcased sustainable orchid cultivation practices at its Nakhon Pathom facilities, emphasizing its international export operations to markets including the United Kingdom, the United States, and the Netherlands. These efforts contribute to Thailand's floriculture industry by strengthening its sustainability profile and export-focused market presence.

- February 2025: The International Association of Horticultural Producers held its Spring Meeting in Chiang Rai in February 2025 and presented the Thailand Country Profile Report, confirming the country’s strong global position in orchid and flower exports, thereby reinforcing Thailand’s floriculture market through improved international visibility and credibility.

Thailand Floriculture Market Report Scope

Floriculture encompasses the cultivation, production, and marketing of flowering and ornamental plants for decorative, gifting, landscaping, and commercial use. It includes the greenhouse and field production of cut flowers and ornamental plants, including orchids, roses, lilies, marigolds, jasmine, lotus, and chrysanthemums. These plants are commonly utilized in floral arrangements, indoor decoration, gardens, hospitality venues, events, and retail floral programs.

The Thailand Floriculture Market Report is Segmented by Cut Flower Type (Orchids, Jasmine, Marigold, Rose, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Orchids | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Jasmine | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Marigold | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Lotus | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Rose | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Chrysanthemum | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Lily | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| By Cut Flower Type | Orchids | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Jasmine | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Marigold | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Lotus | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Rose | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Chrysanthemum | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Lily | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

Key Questions Answered in the Report

What is the 2031 value forecast for cut flowers in Thailand?

The Thailand cut flowers market is forecast to reach USD 653.2 million by 2031 from USD 461.4 million in 2026, growing at a 7.2% CAGR over 2026 to 2031.

Which flower type leads sales in Thailand?

Orchids led by flower type with a 35.0% share in 2025, supported by Thailand’s strong tissue culture base, export reputation, and buyer network.

Why is local demand so important for flower producers in Thailand?

Daily purchases for shrines, temples, ceremonies, and garlands keep domestic demand strong.

Which export region is seeing the fastest growth?

The Middle East is the fastest-growing export geography, helped by rising demand in the UAE, Qatar, and Saudi Arabia.

Page last updated on: