Australia Floriculture Market Analysis by Mordor Intelligence

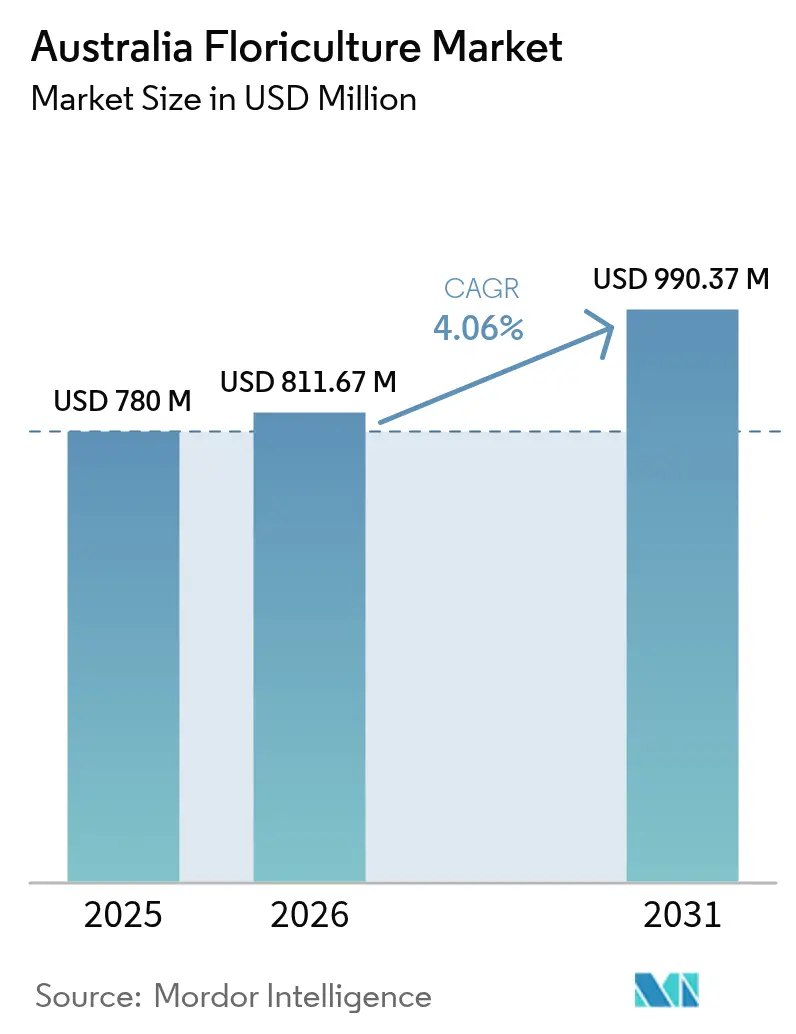

The Australia floriculture market size is expected to grow from USD 780 million in 2025 to USD 811.67 million in 2026 and is forecast to reach USD 990.37 million by 2031 at 4.06% CAGR over 2026-2031. Growth reflects resilient consumer demand, wider adoption of protected cultivation, and expanding export channels for native flowers. Consolidation among retail florists is giving large growers predictable order volumes while allowing supermarkets to expand private-label floral programs. Protected cropping now underpins roughly USD 1.5 billion of annual horticultural output, enabling growers to lengthen production windows and lift stem quality. Native-species breeding, spearheaded by AgriFutures Australia grants, positions Australian producers to command export premiums as global buyers seek distinctive, low-water flowers that support sustainability goals. E-commerce platforms are capturing urban consumers who prefer same-day delivery and transparent pricing, thereby widening domestic addressable demand and offsetting freight-related export headwinds.

Key Report Takeaways

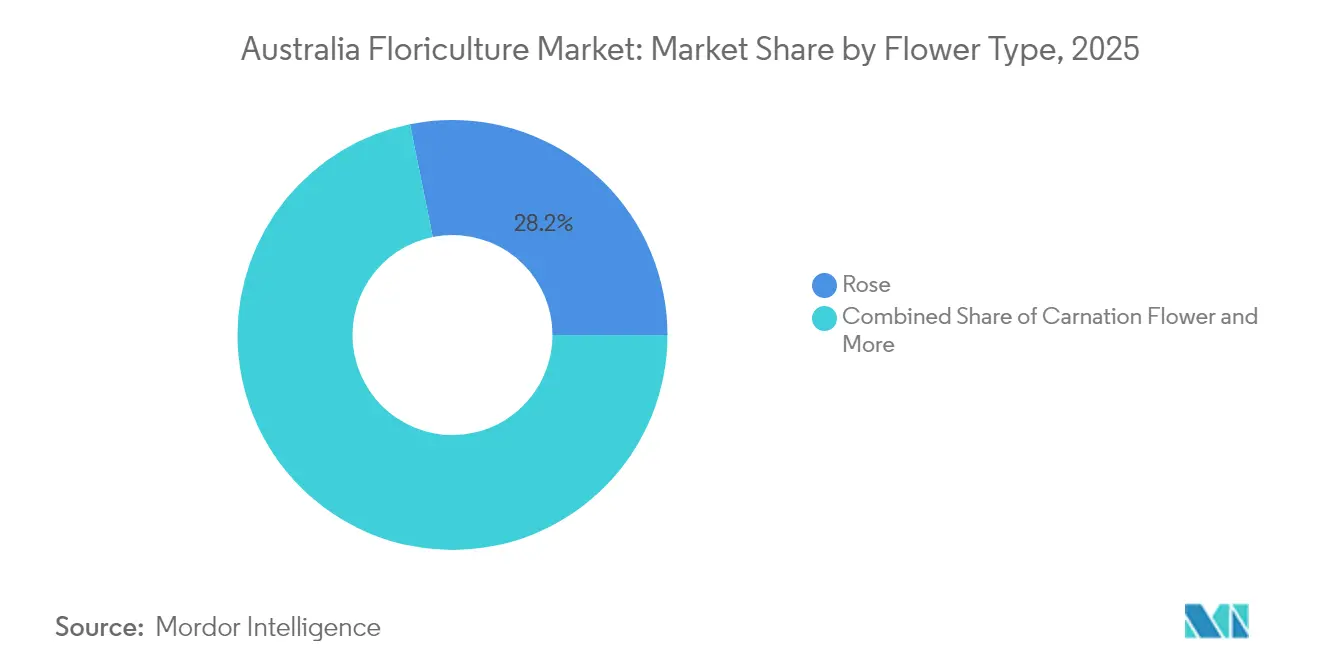

- By flower type, roses led with 28.17% of Australia floriculture market share in 2025, while orchids are forecast to post the fastest 6.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Floriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing retail-florist consolidation boosts wholesale demand | +0.8% | Nationwide, strongest in Sydney, Melbourne, and Brisbane | Medium term (2-4 years) |

| Rising popularity of native Australian cut flowers in export markets | +0.6% | Victoria and New South Wales export hubs | Long term (≥ 4 years) |

| Growth in e-commerce floral gifting platforms | +0.5% | Major urban centers | Short term (≤ 2 years) |

| Expansion of protected cultivation technologies | +0.4% | South-east production belt | Medium term (2-4 years) |

| Government Research and Development grants for floriculture breeding programs | +0.3% | National research nodes | Long term (≥ 4 years) |

| Rising corporate sustainability procurement for locally-grown flowers | +0.2% | Corporate clusters in capital cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing retail-florist consolidation boosts wholesale demand

Australia’s integrated floral chains and supermarkets are centralizing procurement, which allows scale growers to secure multi-year supply contracts that stabilize cash flows. Independent florists align with national wholesalers to access volume pricing, pushing growers to standardize grades and invest in post-harvest cooling. Consolidation is most visible in metropolitan areas where high rents force mom-and-pop florists either to upscale or exit. Supermarket leader Bunnings estimated a 25% retail share for plants and flowers in 2024, signaling further room for channel concentration. Large chains’ weekly replenishment cycles motivate mechanized bouquet assembly at the farm level, trimming logistics costs.

Rising popularity of native Australian cut flowers in export markets

AgriFutures-funded breeding of Leptospermum, Acacia, Waxflower, and Boronia has improved vase life and stem uniformity, helping shipments win premium positioning with U.S. and Japanese buyers. Australia shipped USD 408,890 worth of native cuts to the United States in 2024, up 11% year-on-year. Native species exhibit up to 40% lower water demand than traditional roses, aligning with global corporate social responsibility sourcing. First Nations enterprises benefit from government Indigenous Procurement Policy contracts valued at USD 9.5 billion since 2015, channeling new capital into native flower production.

Growth in e-commerce floral gifting platforms

Pandemic-induced online adoption cemented digital ordering as a permanent buying behavior. Younger consumers prize real-time delivery tracking and curated subscriptions, which drives higher purchase frequency. Lynch Group’s value-added floral packs for supermarket click-and-collect illustrate how omnichannel models capture impulse demand outside conventional florist hours. Basket sizes grow during peak gifting events such as Valentine’s Day and Mother’s Day because platforms upsell vases and chocolates. Domestic e-commerce mitigates exposure to volatile export freight rates.

Expansion of protected cultivation technologies

Greenhouses and high tunnels shield crops from weather extremes and cut pesticide use by enabling biological control. Protected cropping is Australia’s fastest-growing food production subsector at roughly USD 1.5 billion annually. Growers using smart-farm sensors report up to 50% water savings versus open-field beds. Government-backed demonstration sites in Great Barrier Reef catchments show climate control systems lift premium-grade stem yield by 25%. Capital cost remains the key adoption barrier, but grant programs under the Rural Research and Development for Profit scheme subsidize technology trials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages during peak harvest windows | -0.9% | Rural production clusters nationwide | Short term (≤ 2 years) |

| Increasing incidence of thrips and botrytis under warming climate | -0.6% | Humid coastal regions | Medium term (2-4 years) |

| Volatile freight rates erode export competitiveness | -0.4% | Export-oriented farms | Short term (≤ 2 years) |

| Water-allocation caps in Murray–Darling Basin | -0.3% | Basin irrigated districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor shortages during peak harvest windows

Farms reporting difficulty sourcing workers improved from 57% in 2022 to 34% in 2023, yet busy harvest weeks still spark bidding wars in the Riverina, where daily wages climbed to USD 200-300. Contract labor now represents 64% of seasonal horticulture staffing, adding agency fees to the cost of goods. Mechanization options remain limited in delicate cut-flower picking, perpetuating dependency on transient labor.

Water-allocation caps in Murray–Darling Basin

The Basin Plan recovered 2,100 gigaliters for environmental flows, constraining irrigation availability and lifting water prices by USD 45 per megaliter under modeled buyback scenarios.[1]Source: Australian Bureau of Agricultural and Resource Economics and Sciences, “Impacts of Further Water Recovery,” agriculture.gov.au Floriculture competes against almonds, which require 12.5 megaliters per hectare annually, intensifying market bidding for scarce water. Growers pivot to drought-tolerant natives and micro-irrigation to protect margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flower Type: Market Leadership and Emerging Niches

Roses retained 28.17% of Australia floriculture market share in 2025, owing to entrenched gifting traditions and a reliable year-round supply through protected cropping. Orchids, while holding 9.95% share, are projected to capture the highest 6.86% CAGR, contributing markedly to Australia floriculture market size growth driven by longer vase life and rising consumer preference for exotic aesthetics. Chrysanthemums and lilies together account for a 30.74% share, benefiting from seasonal events and broad color palettes that suit supermarket merchandising. Carnations anchor value-oriented bouquets, but their share edges down as buyers trade up to premium natives.

Production economics differ: roses and orchids profit most from high-tech greenhouses that stabilize temperatures and automate feeding. Native cuts such as Waxflower gain ground in open-field blocks with low water inputs, reinforcing sustainability messaging. Import pressure hits carnations hardest because their long post-harvest life makes sea freight viable for overseas suppliers, whereas quarantine restrictions and shorter shelf life insulate rose and native categories. Growers integrate bouquet assembly lines to add value. Lynch Group leads with vertically integrated farms and retail packaging that support supermarket programs.

Geography Analysis

Victoria and New South Wales contribute more than 60.25% of national output, leveraging proximity to Melbourne and Sydney wholesale markets and the Murray-Darling Basin’s irrigation network. Water caps elevate operational risk yet incentivize efficiency upgrades that preserve Australia floriculture market size expansion. Queensland’s tropical zones support specialty natives such as Leptospermum that demand warm nights, securing export premiums in winter months. Western Australia’s wildflower harvest delivers niche export volumes to Europe, supported by state biodiversity.

Protected-cultivation clusters expand fastest in southeastern regions where extreme weather swings and frost risk justify greenhouse investment. Tasmania maintains a cool-climate advantage for bulb crops, including lilies, extending national supply windows. Northern Territory output contracts as veteran growers retire without successors, underscoring labor challenges and logistic costs that thin margins. Freight access influences regional export share: Sydney’s cargo capacity favors New South Wales growers, whereas Western Australia producers face costlier east-to-west domestic transit before exporting.

Climate change prompts region-specific strategies: coastal growers battle humidity-driven disease and therefore adopt ventilated greenhouses inland farms conserve water via subsurface drip and focus on drought-resilient natives. Micro flower farms emerge around Canberra and Adelaide to serve hyper-local farmers' markets, aligning with consumer interest in provenance and lower carbon footprints.

Recent Industry Developments

- December 2024: The Australian government tightened import protocols, banning Adiantum, Dryopteris, Rosa, and Viburnum from Argentina and Japan to avert Phytophthora ramorum, redirecting demand to local growers.

- May 2023: A Victorian flower farmer created "Grown Not Flown," a digital marketplace connecting consumers directly with local flower farms. The platform supports the slow flower movement by facilitating direct relationships between flower buyers and local producers while promoting sustainable, locally grown flowers.

Australia Floriculture Market Report Scope

Floriculture is a type of horticulture practice that focuses on cultivating flowering and ornamental plants for gardens and commercial use. The Australian floriculture market is segmented by type of flowers into roses, tulips, chrysanthemums, gerberas, freesias, lilies, orchids, nursery stocks, and other types of flowers. The report offers market size and forecasts in terms of value (USD) for the above segments.

By Flower Type

| Rose |

| Chrysanthemum |

| Lily |

| Carnation |

| Orchid |

| By Flower Type | Rose |

| Chrysanthemum | |

| Lily | |

| Carnation | |

| Orchid |

Key Questions Answered in the Report

What is the 2026 value of the Australia floriculture market?

The market is valued at USD 811.67 million in 2026.

How fast is the market projected to grow through 2031?

It is forecast to expand at a 4.06% CAGR through 2031.

Which cut-flower segment is growing fastest?

Orchids are projected to record a 6.86% CAGR between 2026 and 2031.

What is the main challenge restricting export growth?

Volatile air-freight rates continue to erode export margins for perishable flowers.

Page last updated on: