Thailand Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

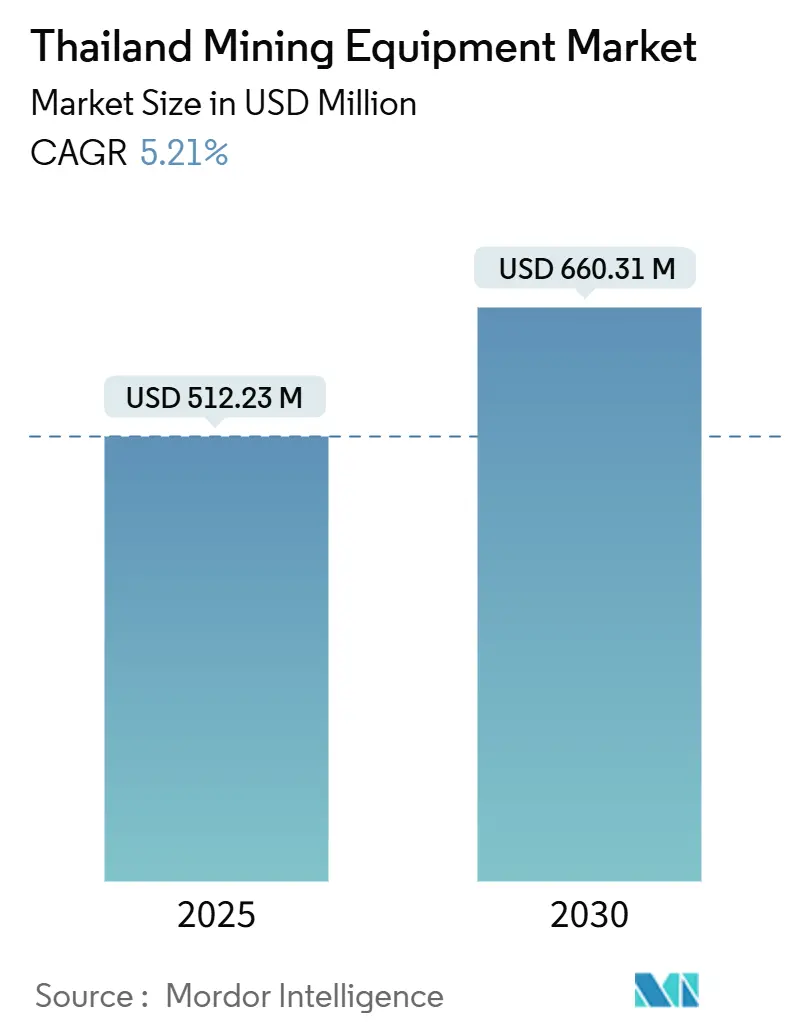

| Market Size (2025) | USD 512.23 Million |

| Market Size (2030) | USD 660.31 Million |

| Growth Rate (2025 - 2030) | 5.21% CAGR |

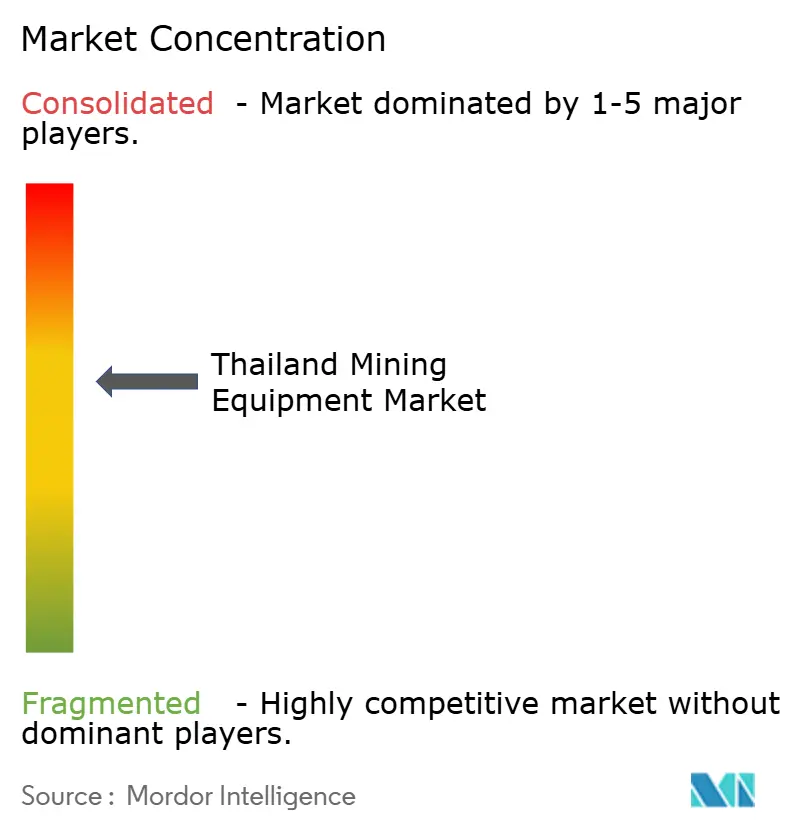

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Mining Equipment Market Analysis by Mordor Intelligence

The Thailand mining equipment market size is valued at USD 512.23 million in 2025 and is forecast to reach USD 660.31 million by 2030, advancing at a 5.21% CAGR during the forecast period. Thailand, recognized as Southeast Asia's manufacturing nucleus, is witnessing a surge in demand for metal-ore extraction and advanced mineral-processing machinery. This uptick is fueled by the government's ambitious "30@30" electric-vehicle production target and recent battery investments. The Eastern Economic Corridor (EEC) in Thailand streamlines operations for global suppliers, offering duty exemptions, efficient customs processes, and state-of-the-art ports for swift and economical equipment landings. Automated haulage and battery-electric drivetrains are growing due to labor shortages, safety mandates, and an eight-year tax incentive. Potash developments in Udon Thani and Chaiyaphum boost underground equipment demand while offsetting challenges from gold-mining regulations and declining thermal coal economics. Caterpillar, Komatsu, and Volvo Construction Equipment dominate with dealer networks, but technology-driven suppliers can tap into autonomous and electric retrofits.

Key Report Takeaways

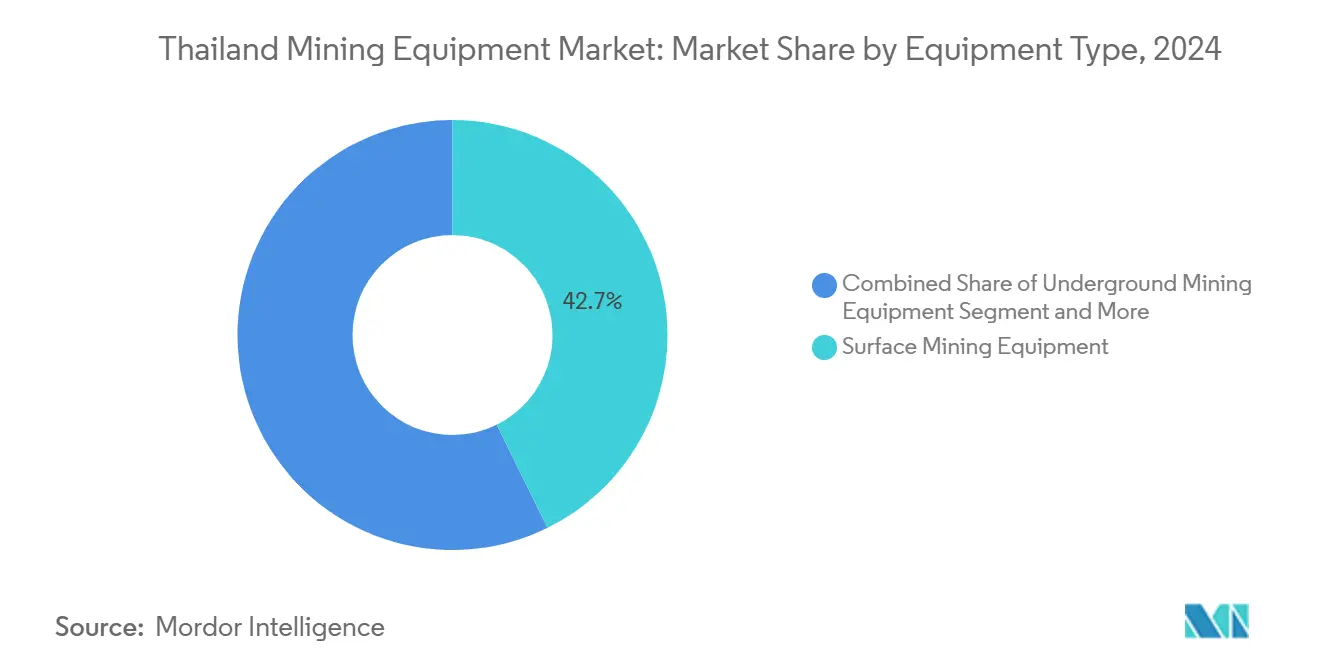

- By equipment type, surface mining equipment led with 42.71% revenue share of the Thailand mining equipment market in 2024; loaders are projected to expand at a 7.41% CAGR through 2030.

- By automation level, manual machines held 66.52% of the Thailand mining equipment market share in 2024, while fully autonomous units are forecast to grow at a 8.52% CAGR to 2030.

- By powertrain, internal-combustion models dominated with 79.29% share of the Thailand mining equipment market in 2024; electric variants are rising at a 8.21% CAGR through 2030.

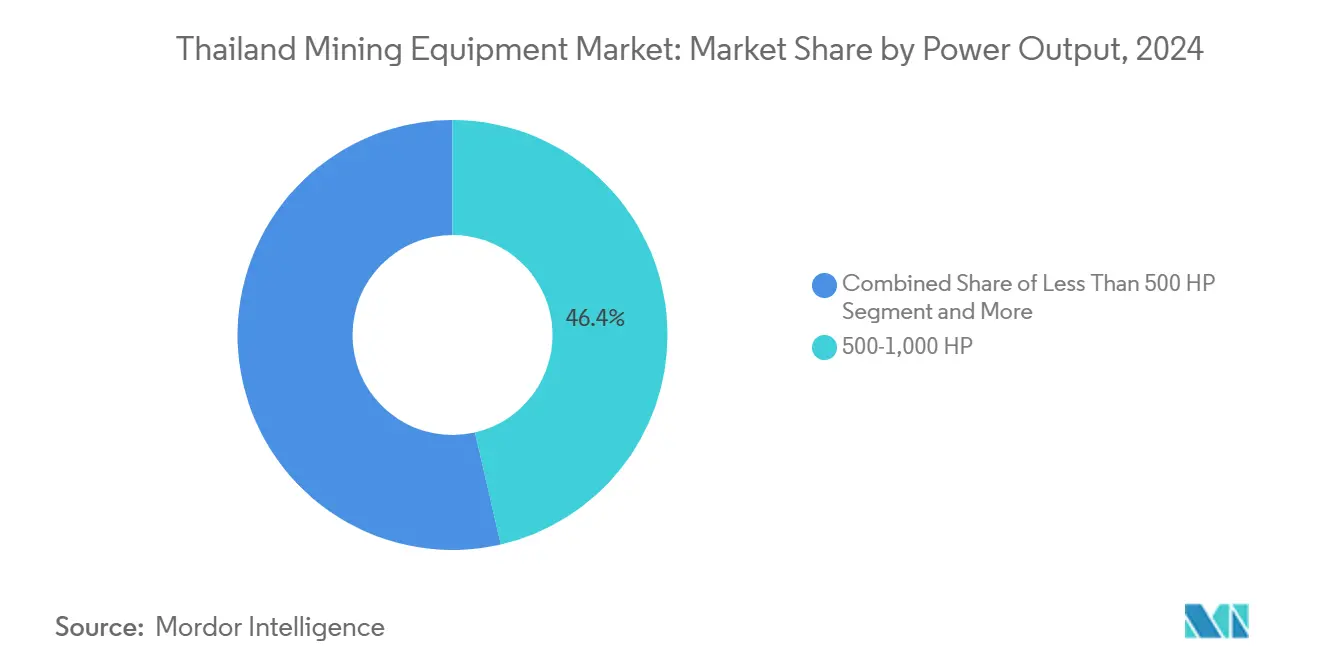

- By power output, the 500-1,000 HP class commanded 46.39% of the Thailand mining equipment market size in 2024, whereas units under 500 HP will climb at a 7.23% CAGR to 2030.

- By application, metal mining accounted for a 49.82% share of the Thailand mining equipment market size in 2024, and mineral mining is advancing at a 8.72% CAGR through 2030.

Thailand Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV and Electronics Drive Metal Ore Demand | +1.8% | Eastern Economic Corridor | Medium term (2-4 years) |

| Domestic Construction Fuels Quarry Expansion | +1.2% | Bangkok region & provinces | Medium term (2-4 years) |

| Govt Incentives for Electric Mining Equipment | +0.9% | Industrial zones nationwide | Short term (≤ 2 years) |

| ASEAN Trade Boosts Capital Equipment Imports | +0.7% | Countrywide | Long term (≥ 4 years) |

| Semi-Autonomous Haulage for Safety & Efficiency | +0.4% | Large-scale pits | Long term (≥ 4 years) |

| Potash Investment Surge in NE Thailand | +0.3% | Udon Thani & Chaiyaphum | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Metal Ores From Electronics and EV Supply Chains

Thailand’s “30@30” EV initiative is catalyzing rapid industrial transformation, attracting investment and scaling battery capacity tenfold. This surge is driving demand for critical minerals like lithium, nickel, and manganese, prompting miners to modernize ore-handling and adopt advanced processing technologies. Specialized equipment tailored for lepidolite-rich ores enables scalable lithium production, while sensor-based grading is helping mid-tier miners meet automaker purity standards. These shifts position Thailand as a rising hub in the global EV supply chain, blending resource development with high-tech manufacturing.

Expansion of Limestone and Quarry Operations for Domestic Construction

Thailand’s investments in logistics plans drive strong demand for limestone and aggregates, boosting profitability for suppliers like Siam City Cement. To meet tight project timelines, quarry operators invest in high-capacity, automated equipment, while low-carbon cement initiatives accelerate the adoption of energy-efficient grinding technologies. Equipment suppliers offering integrated fleet management and cost-per-ton optimization are gaining a competitive edge in long-term contracts, aligning with sustainability and productivity goals.

Government Incentives for Battery-Electric Mining Equipment

Thailand’s Board of Investment offers generous incentives significantly reducing acquisition costs, including extended corporate tax holidays and duty waivers on imported electric machinery. These measures enhance project viability for manufacturers and accelerate the adoption of advanced technologies, positioning Thailand as a competitive hub for electrification and industrial modernization [1]“Investment Promotion Measures,”, BOI Thailand, boi.go.th. A nationwide tariff cap of 3.99 baht/kWh for May–August 2025 keeps operating costs predictable for battery-electric haul trucks. Early pilots at limestone quarries show electric wheel loaders reduce ventilation costs in confined pits and meet Bangkok’s particulate-emission rules. Still, weak grids in remote areas raise transformer and line-extension expenses, so hybrid genset-plus-battery systems remain common during the transition period.

ASEAN Trade Integration: Reducing Import Duties on Capital Equipment

Under AFTA and ASEAN-China FTA rules, most mining machinery enters Thailand at 0-10% duty, and Board of Investment certificates can eliminate the tariff for priority projects [2]“Preferential Machinery Tariffs,”, Customs Bureau, customs.go.th. Rising machinery imports from China—led by crushers and hydraulic excavators—accelerate equipment deployment across Thailand’s construction and mining sectors. Harmonized ASEAN standards streamline commissioning, but complex rule-of-origin documentation poses compliance risks. Distributors offering bundled customs brokerage and post-entry auditing are gaining favor, especially among small operators, by reducing regulatory exposure and ensuring smooth import operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gold Mining Ban Limits Equipment Demand | -0.8% | Northern and central provinces | Long term (≥ 4 years) |

| Thermal-Coal Royalty Volatility Stalls Projects | -0.6% | Mae Moh and northern pits | Medium term (2-4 years) |

| High Grid Tariffs Slow Remote Electrification | -0.4% | Remote sites countrywide | Short term (≤ 2 years) |

| Community Pushback on Rare-Earth Exploration | -0.3% | Northeastern provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ban on Gold Mining Limiting Equipment Demand

The prolonged suspension of the Chatree gold mine significantly constrained Thailand’s gold mining equipment demand, with underground loaders and cyanide circuits idled for years. Although operations resumed in 2022, stricter health and community requirements have raised project costs, deterring new ventures. As a result, equipment distributors are shifting focus to limestone and potash sectors, refurbishing idle rigs for export and reallocating inventory to more active markets.

Community Opposition to New Rare-Earth Exploration Blocks

Environmental groups cite water-table risks and tailings toxicity, referencing past potash protests that stalled projects for over a decade. Thailand’s revised Mineral Act empowers local committees to suspend operations, injecting political risk. Companies must budget for stakeholder-engagement teams and third-party audits, lengthening ROI horizons and delaying machinery orders. Suppliers expand aftermarket services to keep existing fleets productive while green-field projects clear social-license hurdles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Dominance Drives Quarry Expansion

Surface mining equipment captured 42.71% of the Thailand mining equipment market in 2024 as limestone quarries feed Bangkok’s infrastructure projects. The Thailand mining equipment market size for surface machines will grow steadily because contractors replace aging fleets with higher-throughput drills, wheel loaders, and mobile crushers. Loaders, especially 20-ton classes fitted with auto-lube and payload monitoring, will post a 7.41% CAGR to 2030, the fastest among categories. Suppliers bundling predictive-maintenance platforms help operators cut downtime, a major differentiator in competitive bidding. Underground gear holds a niche role in potash and room-and-pillar salt mines but benefits from Chinese investment that packages financing with equipment. Mineral-processing machinery sees incremental gains from battery-metal refiners converting lepidolite and spent catalysts into cathode-grade feedstock, driving orders for high-intensity grinding mills and flotation cells.

The Thailand mining equipment market continues to favor integrated systems. Contractors increasingly source complete load-and-haul packages with telematics, rather than piecemeal machines, to meet project-completion bonuses tied to tonnage quotas. Mobile crushing-and-screening trains that meet low-carbon cement specifications gain traction, capitalizing on the push toward blended and lower-clinker cement. Local dealer inventories now prioritize quick-ship crusher wear parts to support uninterrupted concrete batching during tight road-rail project windows, cementing surface equipment’s dominance.

By Automation Level: Manual Operations Face Technology Disruption

Manual equipment still accounts for a 66.52% share of the Thailand mining equipment market in 2024, reflecting Thailand’s fragmented small-mine structure. Yet the Thailand mining equipment market size for fully autonomous systems is set to expand fastest at 8.52% CAGR because larger quarries chase labor-cost savings and safety metrics. Early adopters deploy collision-avoidance sensors and auto-spotting to raise shift productivity. Semi-autonomous retrofits let operators pilot technology without massive capital risk; these kits integrate with existing hydraulic controls, preserving sunk costs.

Demand for skilled automation technicians stimulates training programs in Chonburi and Rayong, aligning with the EEC’s robotics roadmap. Caterpillar’s plan to localize parts for MineStar in Rayong shortens lead times and nurtures adoption. The Thailand mining equipment market also benefits from local fabricators producing automation-ready brackets and harnesses, trimming conversion costs. Still, imported processors and lidar units expose projects to exchange-rate volatility, a constraint vendors address with multi-currency leasing.

By Powertrain Type: Electric Transition Accelerates Despite ICE Dominance

Internal-combustion models hold 79.29% share of the Thailand mining equipment market in 2024, but electric units will grow at 8.21% CAGR through 2030, supported by 8-year tax waivers and tariff caps. The Thailand mining equipment market encourages battery-electric loaders in dust-sensitive limestone pits where zero tailpipe emissions improve air quality compliance. OEMs collaborate with Thai battery makers to localize pack assembly, cutting freight costs. Hybrid diesel-electric trucks fill gaps where charging infrastructure lags; their regenerative braking trims fuel use, delivering quick savings.

Grid constraints slow adoption in remote potash basins, where connection fees equal 10-15% of project CAPEX. To bridge, suppliers promote containerized solar-battery microgrids that energize chargers and offices. The Thailand mining equipment industry gains a competitive edge as local EPC firms bundle microgrid construction with equipment supply, offering single-contract accountability and accelerated commissioning.

By Power Output: Mid-Range Equipment Leads Market Demand

The 500-1,000 HP range controls 46.39% of the Thailand mining equipment market size in 2024 because it matches typical blast-and-haul cycles in limestone pits. Advances in hydraulic efficiency let midsize excavators rival larger models’ productivity. Units under 500 HP will rise at a 7.23% CAGR as more minor concessions upgrade from second-hand imports to new telematics-equipped machines eligible for BOI incentives. Above-1,000 HP rigs remain essential for high-wall potash and massive overburden, but see slower uptake given their high ticket price.

Komatsu’s affordable 20-ton excavator series, launched in 2025, meets green-tax credit criteria and offers 10% lower fuel burn, driving rapid customer conversion. Local assemblers fit optional quick couplers and tilt buckets to boost versatility, making sub-500 HP gear attractive across multiple job types. Financing arms offer 5-year balloon structures aligned with quarry revenue cycles, further propelling adoption.

By Application: Metal Mining Leads Amid Mineral Diversification

Metal mining claims a 49.82% share of the Thailand mining equipment market in 2024 as Thailand’s EV supply chain scales. The market size in this segment rises steadily due to nickel, manganese, and lithium extraction tied to Sunwoda and BMW contracts. Mineral mining posts the fastest 8.72% CAGR through 2030, fueled by potash and lepidolite projects requiring specialized room-and-pillar machinery and salt-resistant process plants. Coal’s footprint narrows as EGAT schedules Mae Moh's retirement and Banpu shifts CAPEX to gas.

Battery-recycling ventures like PLUS Exploration’s spent-catalyst plant demonstrate new, lower-volume, high-value niches for crushers, leach reactors, and hydrometallurgical cells. Thailand's mining equipment market share in recycling remains small yet strategically important, positioning suppliers for a circular economy future. Stricter environmental review mandates push operators toward enclosed dust-control systems and dry tailings, elevating demand for filter presses and paste-thickening equipment.

Geography Analysis

The Eastern Economic Corridor drives Thailand's most significant slice of mining equipment demand. Chonburi and Rayong host Sunwoda’s USD 1 billion battery plant and BMW’s high-voltage assembly line, each needing continuous limestone, silica, and specialty metals processed with precision equipment. Laem Chabang port streamlines machinery imports, while strong dealer coverage ensures timely service. Bangkok and adjacent provinces anchor limestone quarrying; Siam City Cement and SCG operate kilns requiring uninterrupted crushed-stone supply, spurring investment in mobile crushers and 20-ton loaders.

Northeastern Thailand represents the fastest-growing region as potash licenses move toward construction in Udon Thani and Chaiyaphum. These underground projects demand continuous miners, multi-deck screeners, and corrosion-resistant conveyors. Community-consent processes elongate timelines, but once final permits are issued, bulk purchases follow quickly to meet lender conditions. Northern provinces register stable, if subdued, demand from limestone pits. Gold-equipment orders remain negligible given the singular Chatree operation and lingering regulatory uncertainty.

Competitive Landscape

The Thailand mining equipment market shows moderate concentration. Caterpillar leverages a Rayong facility and MineStar autonomous suite to serve mega-pits and mid-size quarries. Komatsu, via Bangkok Komatsu Sales, adapts midsize excavators to local duty cycles, while Volvo Construction Equipment broadened its reach with a new dealer agreement in 2025. Local specialist P.V. Mining & Exploration partners with Sandvik for crushers and rock breakers, bundling explosives from its in-house plant to provide turnkey solutions.

Automation and electrification create white-space for new entrants. Battery-swap retrofitter start-ups target barges supplying river‐quarry front-loaders. Chinese OEMs bundle low-interest vendor financing tied to potash investments, challenging incumbents on price. Dealers emphasize uptime guarantees, predictive analytics, and parts consignment to defend share.

Thailand Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Hitachi Construction Machinery

Sandvik AB

Epiroc AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sunwoda has invested more than USD 1 billion in a lithium-ion battery plant located in Chonburi, driving increased upstream demand for precision ore equipment.

- January 2025: Volvo Construction Equipment unveiled its New Generation Excavator line, the EC210, and forged a partnership with a new dealer in Thailand, heightening competition in the mid-market segment.

Thailand Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills & Breakers |

| Crushing, Pulverizing & Screening |

| Loaders |

| Mining Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 - 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills & Breakers | |

| Crushing, Pulverizing & Screening | |

| Loaders | |

| Mining Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 - 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining |

Key Questions Answered in the Report

What is the current value of the Thailand mining equipment market?

The market is valued at USD 512.23 million in 2025 and is projected to reach USD 660.31 million by 2030.

Which equipment type holds the biggest share?

Surface mining equipment leads with 42.71% share in 2024, mainly serving limestone and aggregate quarries.

How fast are electric powertrains growing in Thai mines?

Electric-driven machines are forecast to expand at a 8.21% CAGR through 2030, faster than any other powertrain.

Where is demand growing the quickest regionally?

The Northeast, especially Udon Thani and Chaiyaphum, is the fastest-growing area due to large potash projects.

Which factor most restrains market growth?

Thailand’s long-standing restrictions on new gold mining projects limit equipment purchases in that subsector.

Page last updated on: