Netherlands Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

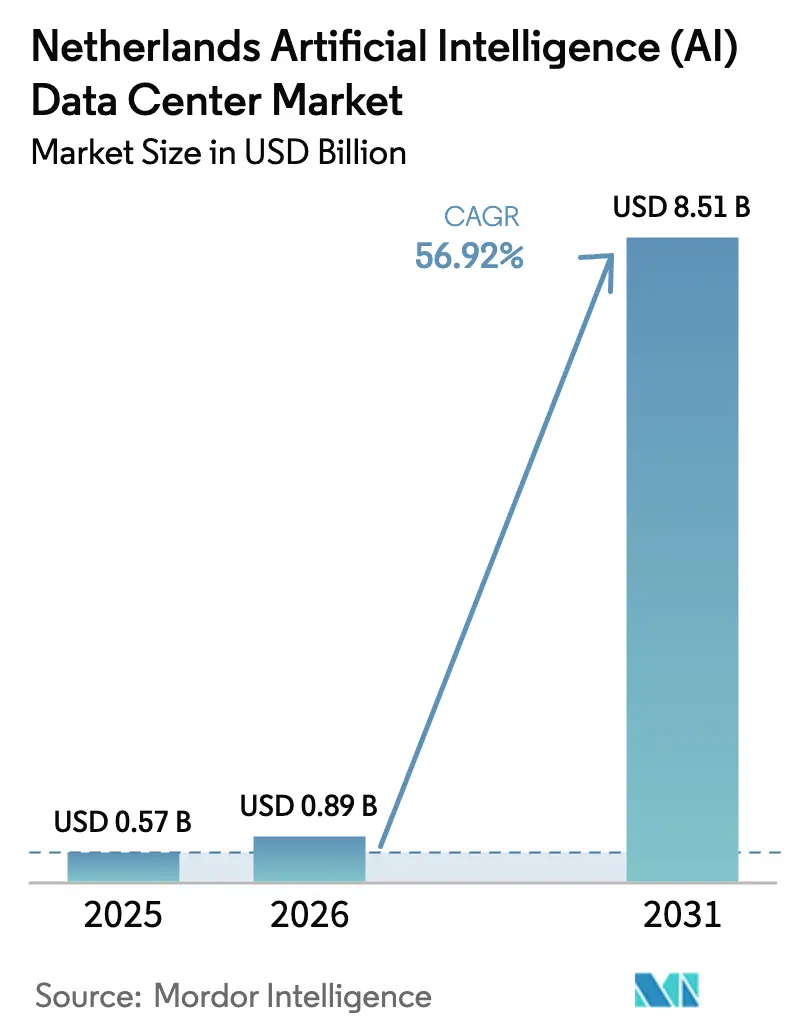

| Base Year Market Size (2025) | USD 0.57 Billion |

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 8.51 Billion |

| Growth Rate (2026 - 2031) | 56.92% CAGR |

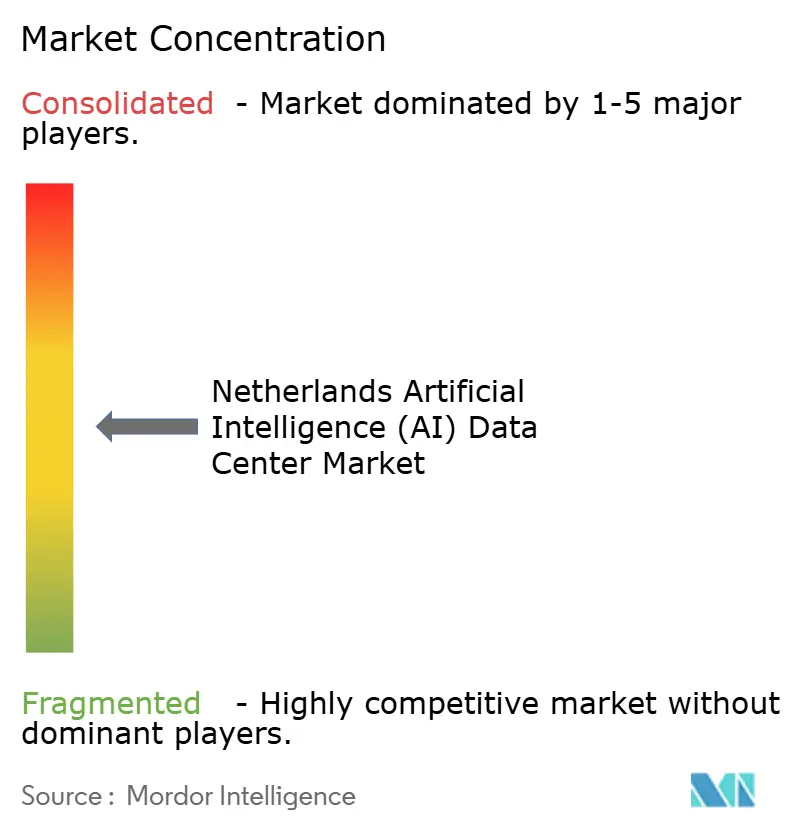

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Netherlands artificial intelligence data center market size is expected to grow from USD 0.57 billion in 2025 to USD 0.89 billion in 2026 and is forecast to reach USD 8.51 billion by 2031 at 56.92% CAGR over 2026-2031. This surge reflects the country’s role as Europe’s digital gateway, where sovereign-cloud mandates, renewable-energy sourcing, and district-heating incentives are collapsing traditional barriers to large-scale GPU deployment. Cloud hyperscalers anchor most capacity additions, but domestic colocation specialists are winning enterprise workloads that must remain under Dutch jurisdiction. Fast-maturing immersion-cooling innovations, a national pipeline of AI-focused subsidies, and accelerating demand from FinTech, healthcare, and digital-media players together compound infrastructure requirements across Amsterdam, Rotterdam, Almere, and Eindhoven. Grid congestion, however, forces operators to incorporate flexible power architectures, while nitrogen-emission rules lengthen permitting cycles, nudging developers toward secondary metros and hybrid redundancy designs.

Key Report Takeaways

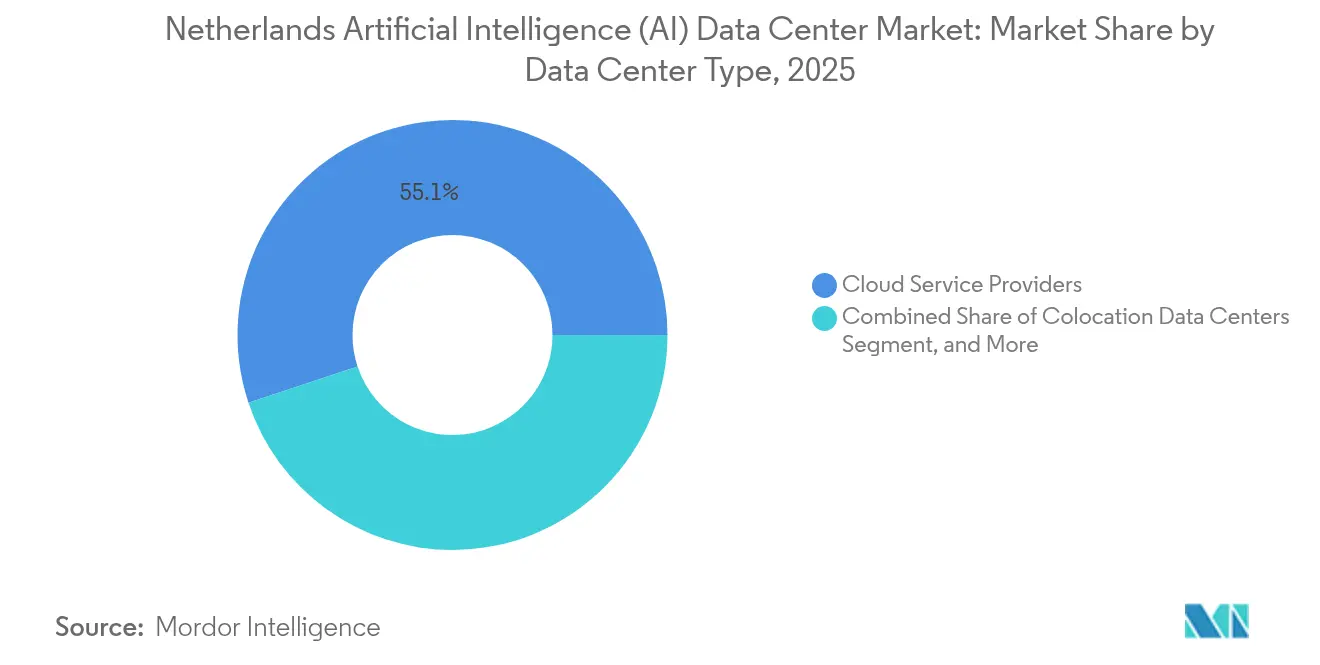

- By data center type, cloud service providers held 55.10% of the Netherlands artificial intelligence data center market share in 2025, while colocation data centers are climbing at a 60.02% CAGR through 2031.

- By component, software accounted for 45.10% of the Netherlands artificial intelligence data center market size in 2025, whereas hardware is forecast to advance at a 59.48% CAGR to 2031.

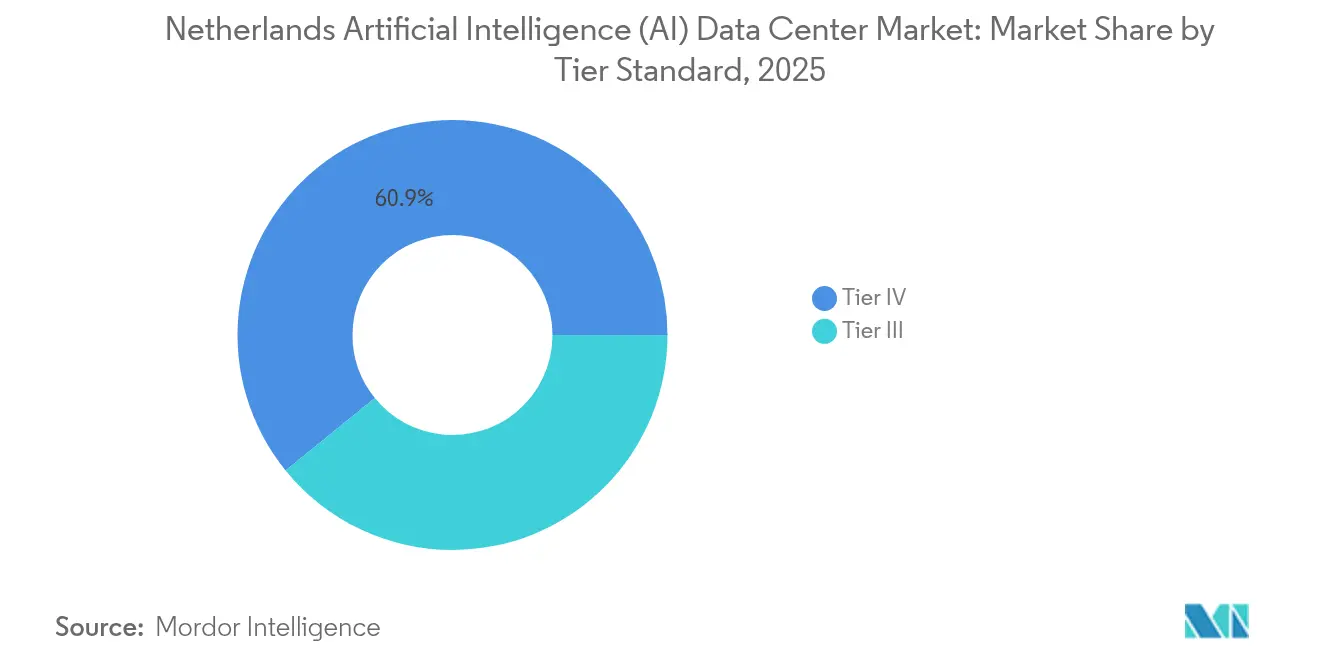

- By tier, Tier IV facilities led with a 60.85% share in 2025; Tier III designs are the fastest-growing segment, with a 60.75% CAGR over the same horizon.

- By end-user industry, IT and ITES represented 33.20% of the Netherlands artificial intelligence data center market size in 2025, while internet and digital media is expanding at a 59.96% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands forms part of a network that extends across countries and regions, each contributing to a shared international environment. The global artificial intelligence (ai) data center market outlook by Mordor Intelligence consolidates those connections.

Netherlands Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging AI Workloads and Hyperscale Cloud Expansion | +18.5% | Netherlands national, spillover to DACH region | Medium term (2-4 years) |

| Rapid Advances in AI Accelerators and Liquid-Cooling Tech | +15.2% | Global with Netherlands innovation leadership | Short term (≤ 2 years) |

| Accelerating Dutch FinTech and Digital-ID GPU Demand | +12.8% | Netherlands national, early gains in Amsterdam, Rotterdam | Medium term (2-4 years) |

| National AI Strategy 2024 Data-Center Subsidies | +8.9% | Netherlands national | Long term (≥ 4 years) |

| Heat-Reuse Tax Incentives Feeding District-Heating Grids | +6.2% | Netherlands national, concentrated in urban areas | Medium term (2-4 years) |

| Sub-Surface Salt-Cavern Storage for 24×7 Renewable Power | +4.1% | Netherlands national, focused on coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging AI Workloads and Hyperscale Cloud Expansion

Hyperscale cloud providers continue to reshape the Netherlands artificial intelligence data center market by locking in renewable power and sovereign-cloud zones to support GPU-dense clusters that serve both European and global inference traffic. Google secured 478 MW of offshore wind exclusively for Dutch facilities, while Amazon pledged EUR 1.4 billion for sovereign EU cloud expansion through 2027.[1]Alfred Monterie, “Wereldwijd forse groei datacenters,” Computable, computable.nl New builds such as Switch Datacenters’ AMS4 site deliver 18 MW of AI-tuned capacity with district-heating integration, underscoring a shift toward circular-energy economics. Enterprises pre-lease GPU rooms 12-18 months ahead of delivery, signaling confidence in both regulatory clarity and hyperscale investment pipelines. As a result, the Netherlands artificial intelligence data center market absorbs regional overflow from DACH and Nordics where latency and policy constraints limit comparable deployments.

Rapid Advances in AI Accelerators and Liquid-Cooling Tech

Dutch innovators are exporting immersion-cooling know-how that cuts cooling energy by up to 90%, enabling rack densities above 100 kW, crucial for NVIDIA H100 and Blackwell GPUs.[2]Asperitas, “Leading Datacenter Immersion Cooling Solution Providers Partner to Dispel Datacenter Immersion Cooling Misconceptions,” asperitas.com Eindhoven University of Technology’s DGX B200 cluster will be among Europe’s first production Blackwell implementations by H1 2025. With PUE figures falling below 1.1 and waste-heat capture hitting 99%, Dutch facilities now bundle sustainability with extreme compute, lowering total cost of ownership and drawing R&D-heavy tenants from life sciences and semiconductor sectors.

Accelerating Dutch FinTech and Digital-ID GPU Demand

Domestic banks, insurers, and digital-identity platforms demand sovereign GPUs for generative-AI copilots and fraud-detection engines. ABN AMRO’s internal “ABN AMRO GPT” reached 50% employee adoption, pushing the bank to deploy on-premises A100 clusters for regulated data handling. Hospitals mirror this trajectory: 90% test AI, while 75% already use generative transcription tools, driving colocation bookings that guarantee Dutch residency and ISO 27001 accreditation. This enterprise layer complements hyperscale nodes, widening total demand for the Netherlands artificial intelligence data center market.

National AI Strategy 2024 Data-Center Subsidies

The EUR 13.5 million GPT-NL program anchors the government’s commitment to domestic language-model development, ensuring GDPR alignment and reinforcing calls for Dutch-based compute. Additional AI-MIT and HPC grants, plus the EUR 34 million MISD sustainability consortium, channel public funds toward GPU clusters, heat-reuse research, and grid-interactive designs. These incentives widen private investment pools, compelling both greenfield and retrofit projects to align with sovereign-AI objectives and further enlarging the Netherlands artificial intelligence data center market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Randstad Grid Congestion and Power-Connection Moratoria | -8.7% | Randstad region, spillover to secondary Dutch markets | Short term (≤ 2 years) |

| Scarcity of AI-Ready Colocation Capacity | -5.3% | Netherlands national, acute in Amsterdam metro | Medium term (2-4 years) |

| Nitrogen-Emission Rules Delaying Generator Permits | -3.8% | Netherlands national, stricter in Natura 2000 zones | Medium term (2-4 years) |

| Public Push-back on Ground-Water-Heavy Immersion Cooling | -2.4% | Netherlands national, concentrated in water-stressed regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Randstad Grid Congestion and Power-Connection Moratoria

TenneT now juggles 70 GW in connection requests, triggering stricter queueing rules and 12-18-month delays for new feeds to AI-heavy campuses.[3]Heleen van der Helm, “TenneT’s Position on Battery Energy Storage Systems,” TenneT, tennet.eu Municipal moratoria in Amsterdam and Haarlemmermeer further complicate permitting, shifting interest toward Almere, Rotterdam, and Eindhoven. Flexible-tariff schemes favor battery storage, yet continuous AI workloads gain little relief, forcing developers to blend demand-response algorithms with local renewable microgrids. These constraints moderate near-term capacity growth within the Netherlands artificial intelligence data center market.

Scarcity of AI-Ready Colocation Capacity

Amsterdam’s 581 MW colocation stock absorbed 135 MW of pre-leasing in H1 2024, while just 10 MW new supply reached the grid. High-density AI racks need 40-100 kW, yet legacy halls top out at 15 kW, leaving a gap that even NorthC’s 11 MW rollout cannot close fast enough. Lead times for liquid-cooling retrofits, high-voltage switchgear, and GPU clusters prolong deployment cycles, capping short-run expansion of the Netherlands artificial intelligence data center market despite robust demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Sovereign Cloud Drives Colocation Surge

Colocation Data Centers are pacing the Netherlands artificial intelligence data center market with a 60.02% CAGR from 2026 to 2031, as enterprises balance public-cloud elasticity against the need for Dutch data residency. Juvoly’s DGX B200 cluster at NorthC Rotterdam illustrates how sovereign health-care workloads gravitate to domestic colos that guarantee GDPR and EU AI Act compliance. Cloud Service Providers, while holding 55.10% market share in 2025, increasingly pair sovereign partitions with hyperscale cores, yet face municipal scrutiny over water use and land zoning.

Hybrid architectures now dominate design briefs, blending colocation flight rooms for sensitive inference with hyperscale zones for burst training, thereby expanding the Netherlands artificial intelligence data center market. Regional operators differentiate through 100% renewable power sourcing, immersion-cooling service catalogs, and cross-connect fabrics that shortcut long-haul latency. Greenfield builds lean on integration of district-heating loops that yield new revenue and appease municipal sustainability targets, further propelling colocation demand beyond Amsterdam’s grid limits.

By Component: Hardware Acceleration Outpaces Software Investment

Hardware spending is growing at 59.48% CAGR, propelled by GPU accelerators, liquid-cooling rigs, and 25/100/400 GbE spine fabrics essential for model training at scale. Immersion-cooling racks from Asperitas achieve 100 kW densities while reducing cooling energy use by 90%, slashing operating costs across the Netherlands artificial intelligence data center market. The software stack still commands 45.10% share in 2025, with GPT-NL funneling public resources into open-source Dutch-language models that run on domestic clusters.

Lifecycle-automation suites, containerized ML frameworks, and observability layers now ship bundled with DGX-powered nodes, blurring lines between hardware and software procurement strategies. Managed-service providers capitalize on skills shortages, offering “cluster-as-a-service” contracts that include firmware tuning, model fine-tuning, and compliance reporting, thereby expanding the Netherlands artificial intelligence data center industry’s value chain.

By Tier Standard: Tier III Gains Ground Through Efficiency Innovation

Tier III builds record a 60.75% CAGR as designers trade dual-utility feeds for advanced microgrid resilience and workload-aware scheduling. Switch Datacenters’ AMS4 targets PUE below 1.15 while exporting surplus heat to the Diemen district network, reducing total energy bills by 15%. Tier IV sites still captured 60.85% market share in 2025, favored by banks and insurers running real-time customer analytics with zero-downtime SLAs.

Cost premiums for Tier IV, however, steer training workloads toward Tier III halls, where containerized checkpointing tolerates brief interventions for grid-balancing. As nitrogen caps tighten diesel-generator permitting, Tier III operators integrate green-hydrogen fuel cells and long-duration batteries, aligning uptime requirements with evolving Dutch environmental policy while enlarging the Netherlands artificial intelligence data center market size for mid-redundancy facilities.

By End-User Industry: Digital Media Accelerates Past Traditional IT

Internet and Digital Media workloads grow at a 59.96% CAGR, reflecting surging generative-content pipelines, personalized recommendation engines, and live-translation services. Streaming platforms colocate GPU farms in Amsterdam Science Park to minimize round-trip latency for pan-European viewers, leveraging local peering fabrics and bilingual model repositories. IT and ITES companies retained 33.20% of the Netherlands artificial intelligence data center market share in 2025, channeling GPU cycles into software-engineering copilots and service-desk chatbots.

BFSI firms intensify secure on-prem deployments to satisfy European Banking Authority guidelines, while hospitals refine AI-driven diagnostics after nationwide pilots validated productivity gains. Manufacturing players integrate computer-vision QC systems with existing MES stacks, boosting inference traffic at edge micro-data centers. Together these verticals keep the Netherlands artificial intelligence data center market diversified across latency requirements, compliance needs, and growth trajectories.

Geography Analysis

Amsterdam surpassed the 500 MW colocation milestone in 2024 and now anchors more than one-third of the Netherlands artificial intelligence data center market size, yet faces strict zoning caps and power-grid queuing that redirect new-build interest to Almere, Rotterdam, and Eindhoven. Customers commit to space 12 months ahead to secure scarce high-density suites, registering record pre-leasing volumes.

Rotterdam benefits from port-city fiber connectivity and district-heating schemes that monetize server exhaust at scale, drawing healthcare and maritime-AI tenants alike. Eindhoven, home to semiconductor and photonics hubs, leverages academic-industry ties to house research-grade GPU clusters under university power allocations. Almere and Aalsmeer serve as pressure valves for Amsterdam’s grid, welcoming Tier III pods that connect back to capital-city exchange points via redundant dark-fiber rings.

Nationwide, the Netherlands artificial intelligence data center market commands attention from multinational hyperscalers because EU-AI-Act compliance and renewable-energy quotas are easier to satisfy when infrastructure resides in a politically stable, connectivity-rich venue. The Dutch spatial plan through 2030 promotes secondary-city development to balance economic gains with power-infrastructure limits, ensuring sustained geographic diversification of AI-optimized capacity.

Mordor Intelligence delivers a comprehensive view of the artificial intelligence (ai) data center market across all major regions such as Europe, South America, and Asia, alongside country-level analysis for France, United Kingdom, Brazil, China, Japan, and Malaysia, each offering a view of the local market realities.

Competitive Landscape

The Netherlands artificial intelligence data center market shows moderate concentration, with hyperscalers, domestic colocation providers, and cooling-technology specialists forming a multi-layer competitive matrix. Google and Amazon expand sovereign clouds secured by long-term renewable-power purchase agreements, raising entry barriers for latecomers. Yet operators such as NorthC carve out share by offering 40-100 kW racks, liquid-cooling white-space, and green-hydrogen backup, attributes hyperscalers rarely extend to mid-market firms.

Cooling vendors hold strategic sway: Asperitas licenses immersion IPCEI-funded patents to local operators, underscoring technology ownership as a differentiator. Power partners, including Eneco, integrate offtake guarantees that bundle renewable supply with heat-reuse obligations, giving compliant operators an advantage in municipal tenders. As EU-level digital-sovereignty agendas crystallize, domestic players leverage local governance familiarity to counterbalance the scale economies of US hyperscalers, ensuring dynamic rivalry across all layers of the Netherlands artificial intelligence data center industry.

Netherlands Artificial Intelligence (AI) Data Center Industry Leaders

Cisco Systems

NVIDIA Corporation

Schneider Electric

Alfa Laval Corporate AB

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Juvoly commissioned the country’s first NVIDIA DGX B200 supercomputers at NorthC Rotterdam, inaugurating sovereign AI infrastructure for healthcare.

- February 2025: Cisco and NVIDIA have expanded their partnership to offer AI technology solutions for enterprises. This collaboration aims to provide organizations with flexible and efficient options to handle the growing demand for AI workloads. These solutions focus on delivering high-performance, low-latency, and energy-efficient connectivity across data centers, clouds, and users.

- December 2024: NorthC announced new sites in Frankfurt and Berlin and added 11 MW across four Dutch cities, showcasing green-hydrogen backup and heat-reuse loops.

- November 2024: Eindhoven University of Technology secured DGX B200 clusters for H1 2025 deployment in low-carbon Finnish data.

Netherlands Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications. Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-User Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How large is the Netherlands artificial intelligence data center market in 2026?

The market is valued at USD 0.89 billion in 2026, on track to reach USD 8.51 billion by 2031 at a 56.92% CAGR.

Which data center type is growing fastest for AI workloads in the Netherlands?

Colocation facilities built for sovereign hosting are expanding at a 60.02% CAGR as enterprises demand Dutch-resident GPU infrastructure.

What is the main technical innovation aiding Dutch AI data centers?

Immersion cooling, pioneered by local firms such as Asperitas, enables 100 kW rack densities and cuts cooling energy by up to 90%.

How does grid congestion affect new Dutch AI data centers?

Power-connection moratoria in the Randstad add 12-18 months to project timelines, pushing developers toward secondary markets and on-site microgrids.

Which end-user vertical shows the fastest AI-driven infrastructure demand?

Internet and Digital Media workloads lead with a 59.96% CAGR, fueled by streaming, content generation, and personalization engines.

Page last updated on: