Hydrolyzed Vegetable Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.64 Billion |

| Market Size (2031) | USD 5.13 Billion |

| Growth Rate (2026 - 2031) | 7.09% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hydrolyzed Vegetable Protein Market Analysis by Mordor Intelligence

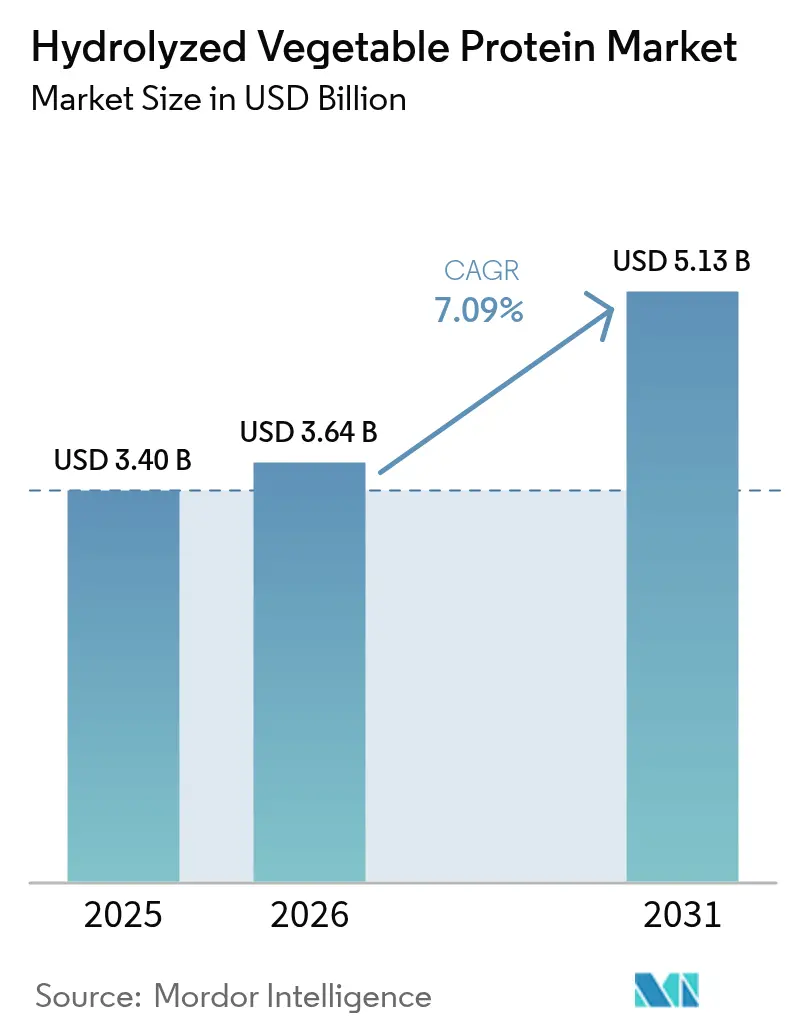

The hydrolyzed vegetable protein market size is expected to grow from USD 3.40 billion in 2025 to USD 3.64 billion in 2026 and is forecast to reach USD 5.13 billion by 2031 at 7.09% CAGR over 2026-2031. The market growth aligns with increasing demand for clean-label, plant-based, and allergen-free ingredients. Consumers prefer products with transparent ingredient sourcing that provide both functional and nutritional benefits, which drives hydrolyzed vegetable protein adoption across food and beverages, personal care, nutraceuticals, and pet nutrition sectors. Regulatory bodies in major regions support this trend by promoting natural protein sources and implementing restrictions on synthetic additives and allergens. The growing demand for plant-based meat alternatives, hypoallergenic pet foods, and fermentation-based bioprocessing expands hydrolyzed vegetable protein applications. As global focus on health, sustainability, and dietary personalization increases, hydrolyzed vegetable protein serves as an essential ingredient in modern product formulations, allowing manufacturers to meet consumer and regulatory requirements while improving flavor, nutrition, and functional performance.

Key Report Takeaways

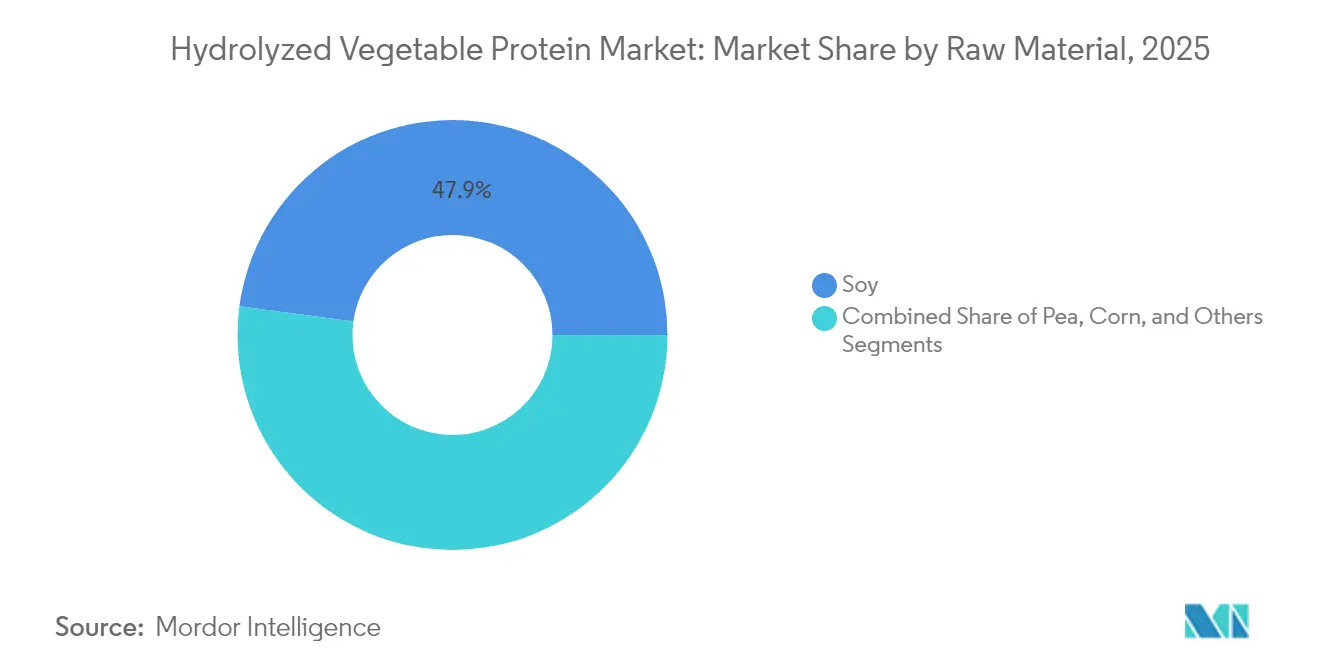

- By raw material, Soy held 47.86% of the hydrolyzed vegetable protein market share in 2025, while Pea Protein is projected to expand at an 7.98% CAGR to 2031.

- By application, Food and Beverages accounted for 69.68% of the hydrolyzed vegetable protein market size in 2025; Personal Care and Cosmetics is set to grow at a 9.34% CAGR through 2031.

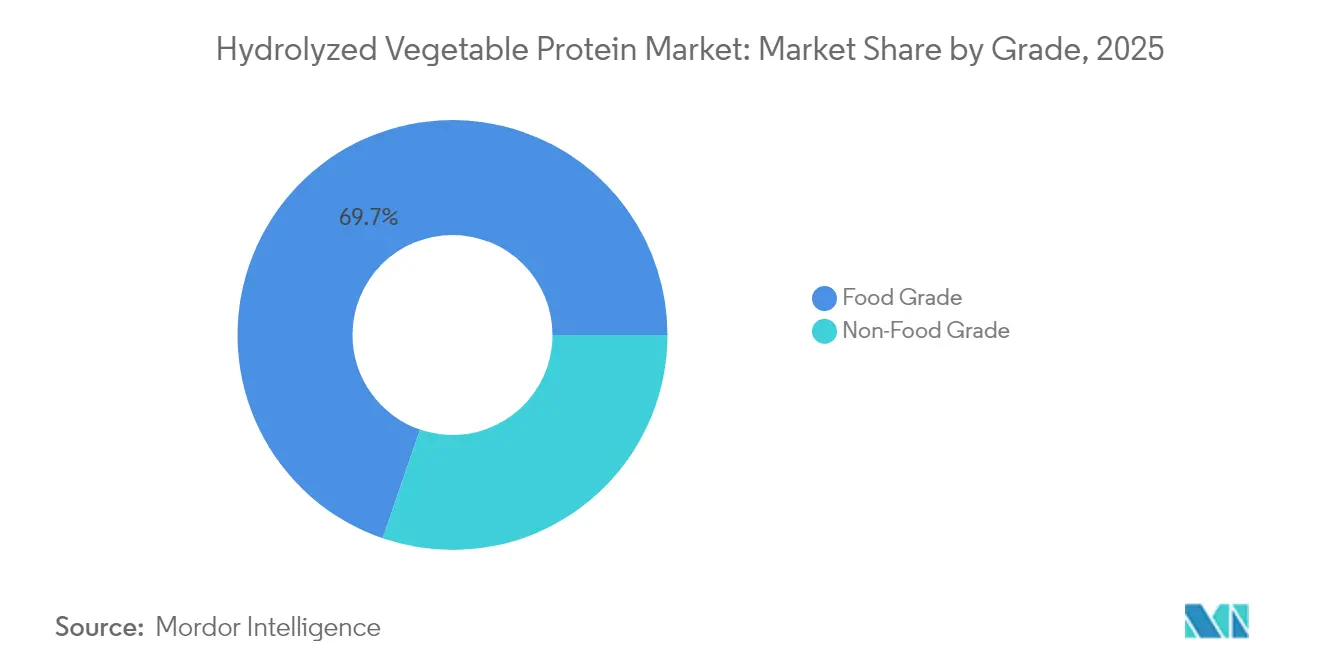

- By grade, Food Grade captured 69.74% of the hydrolyzed vegetable protein market share in 2025, whereas Non-Food Grade is forecast to register the fastest growth at an 7.82% CAGR up to 2031.

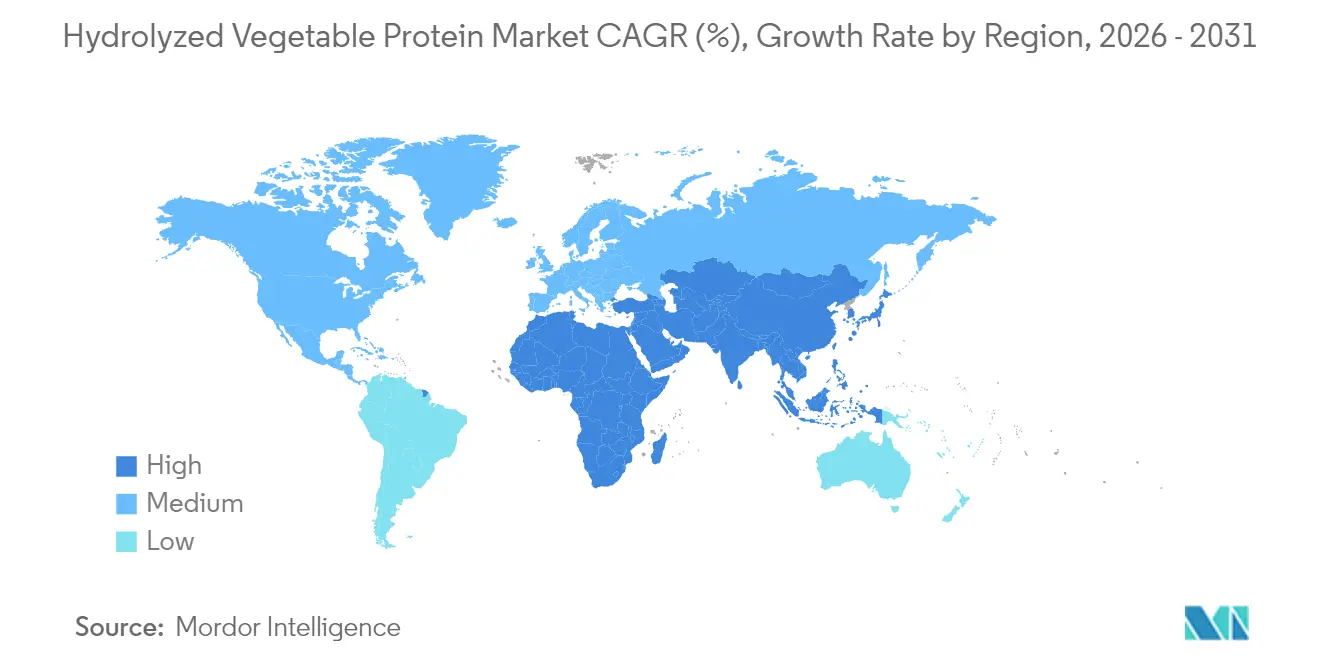

- By geography, Asia-Pacific led with 35.05% revenue share in 2025; the Middle East and Africa region records the quickest trajectory at a 7.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrolyzed Vegetable Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of clean label and natural ingredients | +1.8% | Global, with strongest impact in North America and European Union | Medium term (2-4 years) |

| Growing demand for hydrolyzed vegetable protein in plant-based meat products | +1.5% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising demand for hypoallergenic pet Food increases hydrolyzed vegetable protein usage | +1.2% | North America and European Union, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing demand for convenience foods drives hydrolyzed vegetable protein market | +0.9% | Global, with emphasis on urban centers | Short term (≤ 2 years) |

| Inclination towards vegan food products drives demand for hydrolyzed vegetable protein | +0.8% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Rising demand for umami-rich flavor enhancers | +0.6% | Asia-Pacific core, spill-over to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Clean Label and Natural Ingredients

The demand for clean label and natural ingredients drives growth in the global hydrolyzed vegetable protein market. Consumers increasingly seek food products with transparent ingredient lists and minimal artificial additives, reflecting the clean label movement. This consumer behavior stems from concerns about synthetic chemicals and preservatives, along with preferences for sustainable and ethically sourced foods. The global hydrolyzed vegetable protein market benefits from plant sources such as soy, corn and peas, which meet these requirements by providing a natural protein alternative. Apart from food and beverages, there's a steady demand for vegetable protein in the persocal care products too. According to the National Sanitation Foundation (NSF), in 2024, 74% of Americans considered organic ingredients important in personal care products, while 65% emphasized the need for clear ingredient lists to identify potentially harmful substances [1]Source: National Sanitation Foundation (NSF), "Consumers Consider Organic Ingredients Important in Personal Care Products", nsf.org. These statistics demonstrate the broader consumer preference for ingredient transparency across consumable goods. As a result, the increasing focus on clean label products and natural ingredients positions the global HVP market for sustained growth in the coming years.

Growing Demand for Hydrolyzed Vegetable Protein in Plant-based Meat Products

The increasing demand for hydrolyzed vegetable protein in plant-based meat products is driving the market. The rise in flexitarian, vegetarian, and vegan diets has increased the demand for plant-based meat alternatives. Hydrolyzed vegetable protein serves as both a flavor enhancer and protein source in these products, replicating the umami taste and mouthfeel of traditional meat. Its effectiveness in enhancing savory notes without animal-derived ingredients makes it essential in plant-based burgers, sausages, and deli slices. Hydrolyzed Vegetable Protein also improves texture and moisture retention, which are essential characteristics for meat alternatives. Health concerns, animal welfare considerations, and environmental sustainability drive consumer preferences toward meat alternatives. In Europe, meat consumption is declining, particularly in countries like Germany and Austria. The Federal Office for Agriculture and Food reported that German per capita meat consumption was approximately 430 grams in 2023, while Statistics Austria documented a decrease of 1.7 kilograms per person compared to the previous year [2]Source: Federal Office for Agriculture and Food, "Consumption of meat per capita falls below 52 kilograms", ble.de. These global consumption patterns and the increasing incorporation of Hydrolyzed Vegetable Protein in plant-based alternatives indicate sustained market growth for hydrolyzed vegetable protein in the coming years.

Rising Demand for Hypoallergenic Pet Food Increases Hydrolyzed Vegetable Protein Usage

The global hydrolyzed vegetable protein market is experiencing growth due to increased demand for hypoallergenic pet food, as pet owners seek specialized diets for animals with food allergies and sensitivities. The pet humanization trend, particularly prominent in North America and Europe, has led owners to prioritize high-quality, health-focused nutrition for their pets. Hydrolyzed vegetable proteins, created through enzymatic breakdown of proteins into smaller peptides, offer enhanced digestibility and reduced allergenicity, making them suitable for pets with food intolerances. Pet food manufacturers are expanding their hypoallergenic product lines in response to the increasing cases of pet allergies and growing awareness of pet nutrition. Regulatory bodies, including the Association of American Feed Control Officials (AAFCO) and the European Union's Feed Regulation 767/2009, establish guidelines for pet food safety and labeling, ensuring product quality and maintaining consumer confidence. The increasing adoption of hydrolyzed vegetable protein in pet food formulations, combined with stringent quality standards, indicates sustained market growth in the coming years.

Growing Demand for Convenience Foods Drives Hydrolyzed Vegetable Protein Market

The global hydrolyzed vegetable protein (HVP) market is experiencing growth due to increasing demand for convenience foods, as consumers seek quick, nutritious meal solutions. Factors such as urbanization, higher disposable incomes, and dual-income households have increased the preference for time-saving food options, boosting the market for ready-to-eat meals, snacks, and pre-packaged foods. Hydrolyzed vegetable proteins enhance flavor, texture, and protein content in food products while meeting consumer requirements for clean-label and natural ingredients. These proteins are essential components in various convenience foods, including soups, sauces, instant noodles, and ready-to-eat meals. The expansion of the convenience food market, supported by consumer behavior changes and advancements in food processing and packaging, continues to increase the use of hydrolyzed vegetable proteins. The International Food Information Council reports that 61% of Americans purchased food and beverages for convenience in 2023, compared to 56% in 2022, indicating a significant shift in consumption patterns [3]Source: International Food Information Council (IFIC), "2023 Food and Health Survey", foodinsight.org. This trend suggests sustained growth potential for the global Hydrolyzed Vegetable Protein market as convenience food consumption continues to rise worldwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.70% | Global, with heightened sensitivity in North America and European Union | Medium term (2-4 years) |

| Availability of alternative protein ingredients | -0.50% | Global, with competitive pressure intensifying in Asia-Pacific | Long term (≥ 4 years) |

| Strict FDA and EU regulations on labeling and safety increases Costs | -0.40% | Global, with strongest impact in Europe and North America | Medium term (2-4 years) |

| Concerns regarding Potential Allergies | -0.30% | North America and European Union, regulatory focus expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict FDA and EU Regulations on Labeling and Safety Increases Costs

Strict labeling and safety regulations in the United States and the European Union push compliance costs higher for hydrolyzed vegetable protein suppliers. The FDA now expects detailed allergen statements, sodium declarations, and validated production controls under its updated plant-based labeling guidance issued in 2025. Manufacturers must also submit extensive toxicology data when filing GRAS notices, a process that can take more than a year and often requires third-party scientific studies. In Europe, the Novel Food Regulation mandates pre-market approval for new or significantly altered hydrolysates, adding application fees and rigorous safety assessments according to European Commission. The EU Food Information to Consumers Regulation further compels clear origin and nutritional information, forcing companies to redesign packaging and update digital traceability systems. Together, these rules lengthen product development timelines and raise the cost floor, which can squeeze smaller producers that lack dedicated regulatory teams. Larger players pass some of the overhead to customers, but price sensitivity in end-use markets limits how much cost recovery is possible.

Availability of Alternative Protein Ingredients

The growth of alternative protein ingredients significantly constrains the global hydrolyzed vegetable protein market. Food manufacturers and consumers seek innovative, sustainable, and functional protein sources, leading to increased adoption of mycoprotein, insect-based protein, and fermentation-derived proteins. These alternatives compete with hydrolyzed vegetable protein by offering comparable functionality and protein content, while providing additional benefits such as allergen-free properties, enhanced digestibility, and cleaner processing methods. Proteins derived from precision fermentation deliver new functionalities and reduced environmental impact. The expanding protein ingredient landscape creates competitive pressure on traditional plant-based proteins like hydrolyzed vegetable protein. As a result, the market penetration and growth potential of hydrolyzed vegetable protein face substantial challenges as food manufacturers increasingly diversify their protein ingredient portfolios to meet evolving consumer preferences and sustainability requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Soy Dominance Faces Pea Protein Challenge

The global hydrolyzed vegetable protein market demonstrates significant segmentation, with soy protein maintaining its dominant position at 47.86% market share in 2025. This predominance stems from well-established international supply chain networks, superior cost-effectiveness in commercial applications, and extensive functionality across industrial food processing operations. Food manufacturers worldwide consistently select soy-based proteins for large-scale production requirements, implementing it extensively in meat alternatives, bakery, and ready-to-eat meal solutions. The sophisticated global processing infrastructure, developed over decades of industrial application, ensures dependable production capabilities and maintains consistent quality standards across international markets, further solidifying soy protein's position as the primary choice for industrial food applications.

Pea protein is emerging as the fastest-growing segment, projected to expand at an 7.98% CAGR through 2031. This significant market expansion correlates directly with its allergen-free status and comprehensive amino acid profile, addressing the evolving requirements of health-conscious consumers across international markets. The regulatory validation through FDA's GRAS Notice 581 establishes concrete safety parameters for pea protein applications, considerably strengthening its position in the global marketplace. Corn protein benefits from non-GMO positioning and is finding opportunities in premium applications, while rice protein is carving out niche markets in hypoallergenic formulations especially in infant nutrition, where regulatory requirements favor easily digestible and allergen-safe proteins.

By Application: Food Sector Leadership with Personal Care Emergence

The Food and Beverage segment holds 69.68% share of the global hydrolyzed vegetable protein market in 2025. This dominance reflects its essential role in enhancing flavor, improving mouthfeel, and fortifying protein content in processed foods. The ingredient's ability to provide umami flavor and enhance palatability has established its importance across various food applications. Meat products and plant-based meat alternatives represent the highest-growth subsegment, as manufacturers use hydrolyzed vegetable protein to achieve authentic meat-like taste, aroma, and texture. hydrolyzed vegetable protein provides an effective solution for delivering savory characteristics in these alternatives while supporting clean-label requirements.

The Personal Care and Cosmetics segment is expected to grow at a CAGR of 9.34% through 2031. This growth stems from increased incorporation of hydrolyzed proteins in hair strengthening, skin hydration, and anti-aging products. Consumer preference for natural and functional ingredients has encouraged cosmetic manufacturers to use Hydrolyzed Vegetable Protein to enhance absorption and repair damaged hair and skin. The nutraceuticals and dietary supplements industry uses hydrolyzed vegetable proteins to improve bioavailability and digestibility in protein shakes, bars, and clinical nutrition products for seniors and athletes. The animal feed and pet food sector shows increasing adoption, particularly in premium pet food formulations, where protein hydrolysates help reduce allergic reactions and improve digestive tolerance in companion animals.

By Grade: Food Grade Dominance with Industrial Applications Rising

Food Grade hydrolyzed vegetable protein holds 69.74% market share in 2025, driven by stringent quality standards and regulatory compliance in human nutrition applications. This dominance stems from strict regulatory frameworks and quality standards that ensure food safety, purity, and traceability - essential factors for consumer acceptance and brand trust. Food-grade hydrolyzed vegetable protein undergoes rigorous testing and compliance protocols to ensure the absence of contaminants like 3-MCPD in acid-hydrolyzed products. These standards, along with consumer preferences for clean-label and plant-based ingredients, enable food-grade hydrolyzed vegetable protein to maintain premium pricing in high-margin applications like health foods, infant nutrition, and high-protein snack formulations. The increasing adoption of natural flavor enhancers and investment in enzymatic processing methods further strengthens food-grade adoption in segments prioritizing flavor, safety, and nutritional integrity.

Non-food grade hydrolyzed vegetable protein, used in industrial, agricultural, and biotechnological applications, represents the fastest-growing segment with a projected CAGR of 7.82% through 2031. This growth stems from expanding applications in biotechnology, where hydrolyzed proteins function as nutrient sources in fermentation processes, particularly in precision fermentation systems for producing lab-grown enzymes, bio-based chemicals, and alternative proteins. The agriculture and specialty chemical industries are incorporating hydrolyzed vegetable protein in biofertilizers, microbial inoculants, and plant growth enhancers, utilizing its amino acid profile to support microbial activity and soil health.

Geography Analysis

Asia-Pacific commands the largest regional market share at 35.05% in 2025 in the global hydrolyzed vegetable protein industry, attributed to China's strategic investments in fermentation-based protein production and comprehensive government policies supporting alternative protein development. The region's competitive advantage stems from its robust manufacturing infrastructure and efficient production capabilities for hydrolyzed protein manufacturing. Japan demonstrates significant market maturity through widespread consumer acceptance of plant-based foods, indicating market progression toward premium applications. South Korea's implementation of alternative protein standards through the Ministry of Food and Drug Safety establishes a structured regulatory environment for market advancement. The regional market expansion is further strengthened by accelerating urbanization and increasing disposable incomes in India, generating substantial demand for protein-fortified processed foods.

The Middle East and Africa (MEA) region demonstrates the highest growth potential in the global hydrolyzed vegetable protein market, projecting a CAGR of 7.31% through 2031. This substantial growth is attributed to the systematic development of domestic food processing industries, increasing urbanization rates, and evolving dietary preferences emphasizing convenience and affordability. The requirement for halal-certified ingredients remains a primary market driver across major markets including Saudi Arabia, the United Arab Emirates, Egypt, and South Africa. Hydrolyzed vegetable protein derived from plant sources with halal certification presents manufacturers with a regulatory-compliant flavor enhancement solution.

North America and Europe exhibit sustained growth in the global hydrolyzed vegetable protein market, characterized by comprehensive regulatory frameworks and evolving consumer preferences for product transparency, safety protocols, and sustainability measures. The Food and Drug Administration, European Food Safety Authority, and national regulatory organizations implement stringent food safety regulations, necessitating manufacturers to incorporate clean-label, non-GMO, and plant-based ingredients in their product formulations.

Competitive Landscape

The hydrolyzed vegetable protein market exhibits moderate concentration, comprising established global companies and specialized niche players. Major companies including Ajinomoto Co., Inc., Kerry Group plc, Sensient Technologies Corporation, Titan Biotech, among others maintain significant market presence through extensive product portfolios, established client relationships, and comprehensive distribution networks. Their vertical integration strategies enable control over sourcing, processing, and quality assurance, ensuring consistent flavor profiles and regulatory compliance. These companies leverage their scale and Research and Development capabilities to serve diverse industries, from processed food and beverages to cosmetics and nutraceuticals, while maintaining control over pricing and product development.

Specialized entrants and regional players are gaining market share by focusing on technical innovation and application-specific solutions. These companies differentiate themselves through specialized hydrolysis techniques, non-GMO sourcing, clean-label certifications, and allergen-free products for specific markets such as plant-based foods, infant nutrition, and hypoallergenic products. Their operational flexibility enables rapid adaptation to consumer trends and regulatory requirements.

Significant opportunities exist in high-value, regulated applications, particularly in veterinary nutrition, where therapeutic diets for pets and livestock require hydrolyzed proteins with specific amino acid profiles. These applications require exact formulation, extensive safety testing, and regulatory approval, creating entry barriers that benefit companies with specialized technical expertise. Additional opportunities exist in biotechnology applications, where hydrolyzed vegetable protein serves as a nutrient base for microbial cultivation in precision fermentation systems.

Hydrolyzed Vegetable Protein Industry Leaders

-

Ajinomoto Co., Inc.

-

Kerry Group plc

-

Sensient Technologies Corporation

-

Titan Biotech

-

Foodchem International Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ACI Group established a long-term distribution agreement with International Flavors and Fragrances (IFF) to distribute IFF's plant-based proteins in the United Kingdom and Ireland. The agreement covers hydrolyzed vegetable proteins, and specialized blends for specific formulations.

- March 2025: Herbal Isolates has developed a Hydrolyzed Vegetable Protein using technology that meets European standards. The company's process ensures that the levels of 3-MCPD conform to CODEX guidelines, providing safe products to customers.

- February 2024: Roquette introduced four new pea protein ingredients: NUTRALYS Pea F853M, NUTRALYS H85, NUTRALYS T Pea 700FL, and NUTRALYS T Pea 700M. The NUTRALYS H85, a hydrolyzed pea protein, is designed for use in snack bars and beverages.

Global Hydrolyzed Vegetable Protein Market Report Scope

The global hydrolyzed vegetable protein market is segmented by form into a dry powder, liquid, and paste; by application into food and beverage, personal care products and others. Food and beverage can be further bifurcated into the bakery, snack foods, soups, sauces & dressings, meat & meat products, beverages, and others. Also, the study provides an analysis of the hydrolyzed vegetable protein market in the emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

| Soy |

| Corn |

| Pea |

| Others |

| Food and Beverage | Bakery |

| Snack Foods | |

| Soups, Sauces and Dressings | |

| Meat Products and Analogues | |

| Seasonings and Ready Meals | |

| Others | |

| Nutraceuticals and Dietary Supplements | |

| Personal Care and Cosmetics | |

| Animal Feed and Pet Food |

| Food Grade |

| Non-Food Grade |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Raw Material | Soy | |

| Corn | ||

| Pea | ||

| Others | ||

| By Application | Food and Beverage | Bakery |

| Snack Foods | ||

| Soups, Sauces and Dressings | ||

| Meat Products and Analogues | ||

| Seasonings and Ready Meals | ||

| Others | ||

| Nutraceuticals and Dietary Supplements | ||

| Personal Care and Cosmetics | ||

| Animal Feed and Pet Food | ||

| By Grade | Food Grade | |

| Non-Food Grade | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the hydrolyzed vegetable protein market in 2031?

The market is forecast to reach USD 5.13 billion by 2031, supported by a 7.09% CAGR over 2026-2031.

Which raw material currently leads the hydrolyzed vegetable protein market?

Soy maintains leadership with 47.86% market share in 2025 due to cost efficiency and wide availability.

Why is pea protein gaining traction in hydrolyzed applications?

Pea protein is allergen-friendly and has a neutral flavor, helping it record an 7.98% CAGR as consumers seek non-soy options.

Which region is growing fastest for hydrolyzed vegetable proteins?

The Middle East and Africa posts the fastest growth at a 7.31% CAGR through 2031, driven by halal-certified ingredient demand.

Page last updated on: