Computational Creativity Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

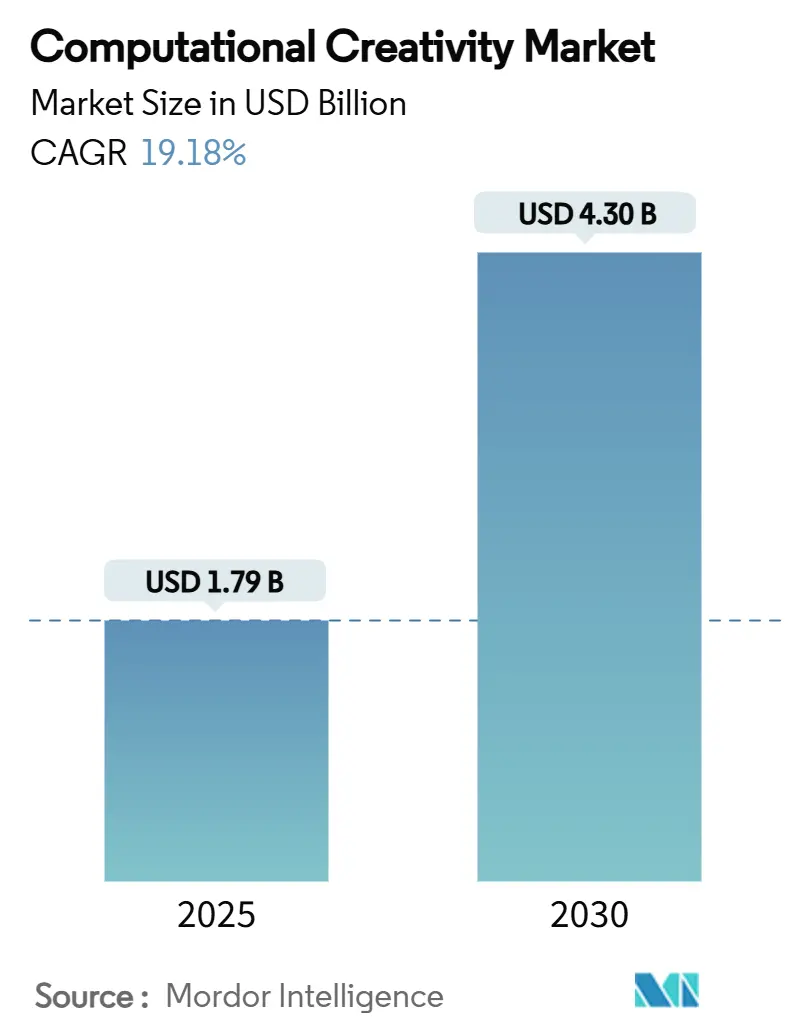

| Market Size (2025) | USD 1.79 Billion |

| Market Size (2030) | USD 4.30 Billion |

| Growth Rate (2025 - 2030) | 19.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

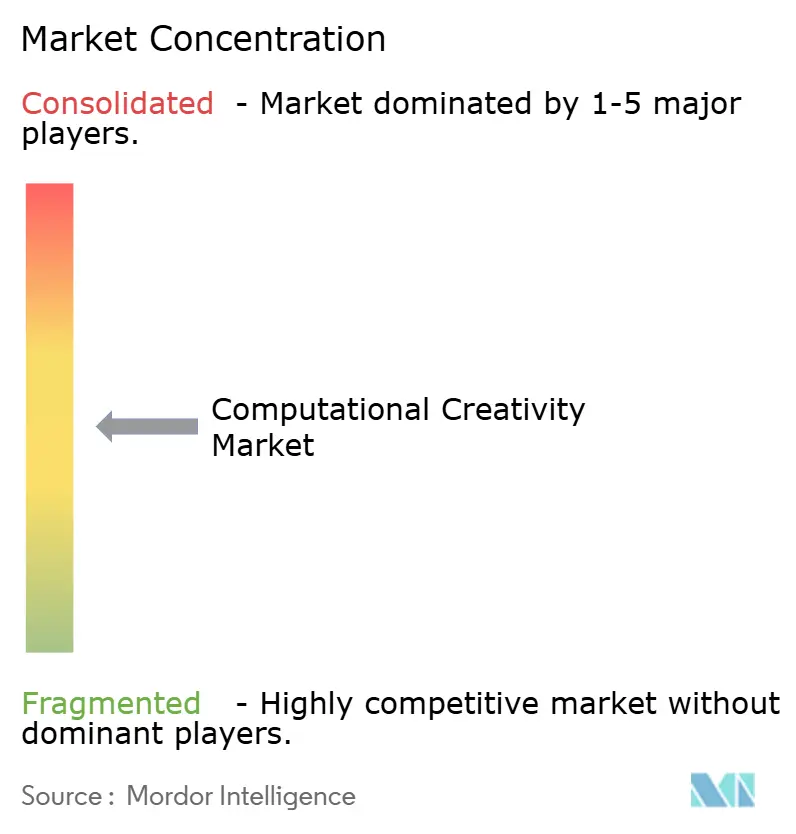

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Computational Creativity Market Analysis by Mordor Intelligence

The computational creativity market size is valued at USD 1.79 billion in 2025 and is forecast to reach USD 4.30 billion by 2030, reflecting a 19.18% CAGR during the period. Growth stems from converging factors: enterprises racing to automate content production, falling cloud-compute prices that cut model-inference costs, and AI toolkits that require little coding expertise. Transformer-based multimodal models boost creative productivity by unifying text, image, and video generation inside one architecture, while integrated creative-suite plug-ins shorten learning curves for non-technical users. Content owners increasingly demand audit trails that prove copyright compliance, favoring vendors that rely on licensed or internally generated data. Rising procedural-generation use cases in gaming and virtual worlds further widen the addressable base for the computational creativity market, encouraging incumbents and startups alike to expand model catalogs and pre-built templates.

Key Report Takeaways

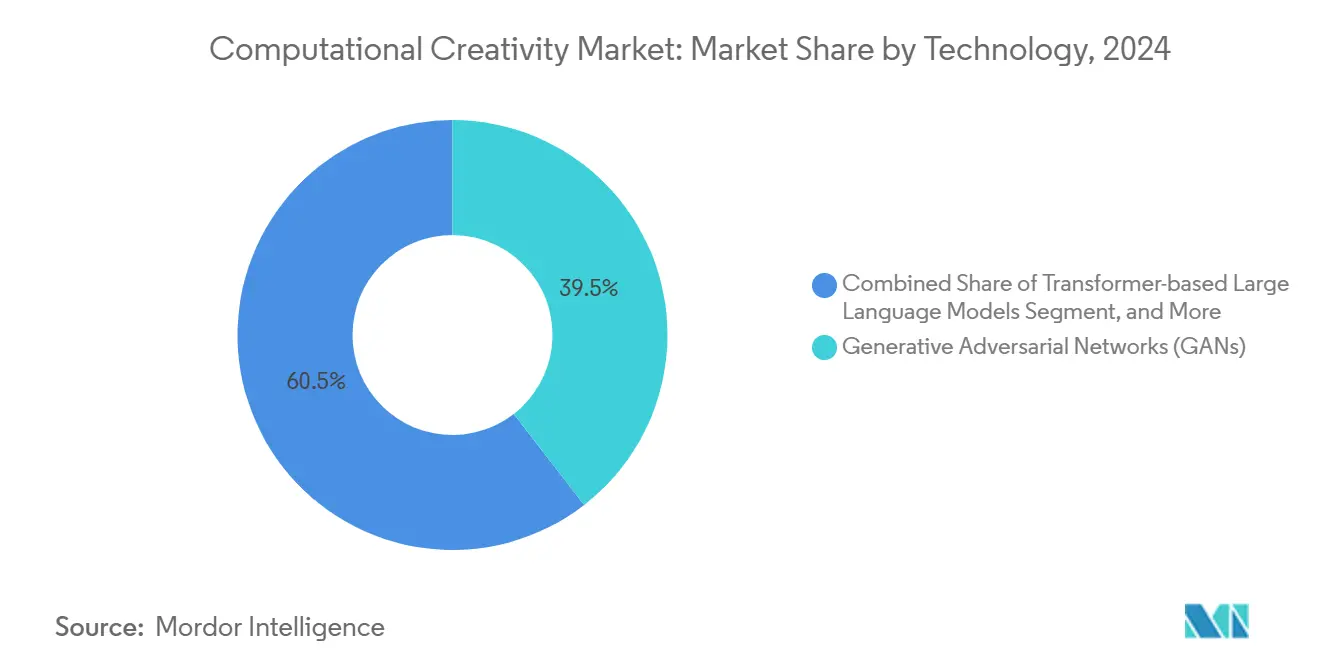

- By technology, Generative Adversarial Networks held 39.5% of computational creativity market share in 2024, and Transformer-based Large Language Models are projected to expand at a 29.2% CAGR through 2030.

- By application, Marketing and Advertising Content commanded 29.5% share of the computational creativity market size in 2024; Gaming and Virtual World Building is advancing at a 24.6% CAGR through 2030.

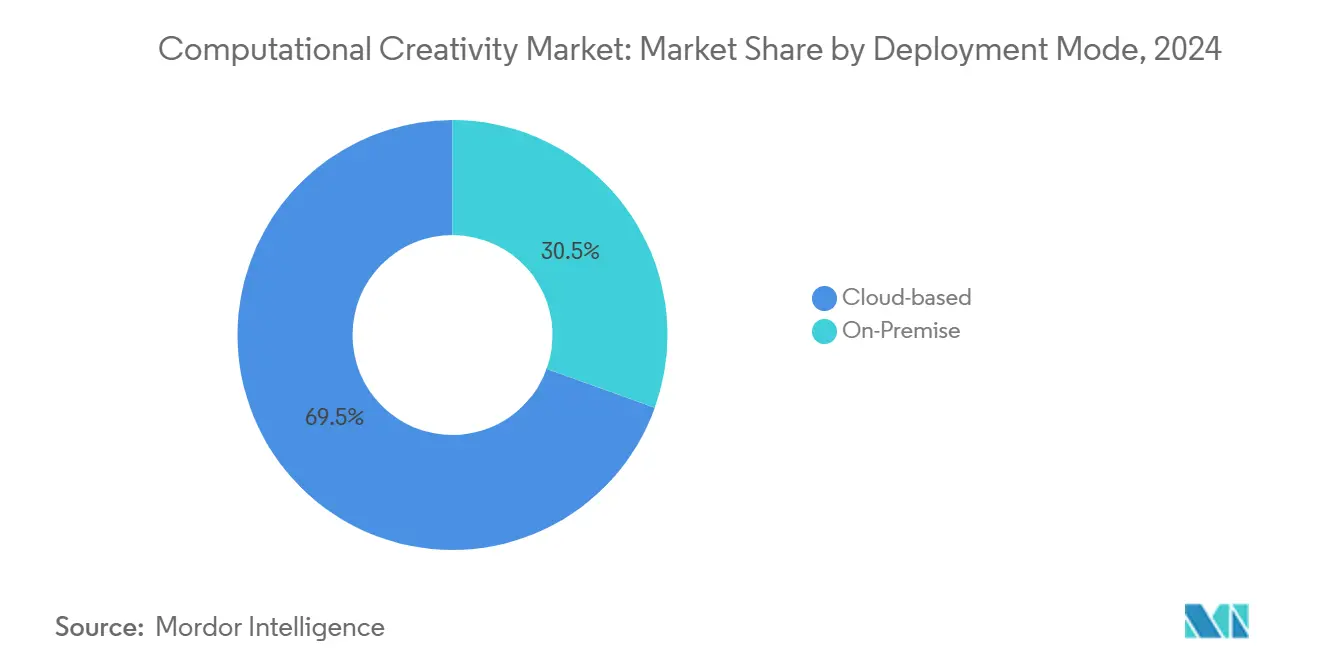

- By deployment mode, cloud-based solutions accounted for 69.5% of the computational creativity market size in 2024 and are rising at a 20.1% CAGR.

- By end-user industry, Media and Entertainment Companies led with 34.2% revenue share in 2024; Gaming Studios and Publishers record the fastest CAGR at 22.7% through 2030.

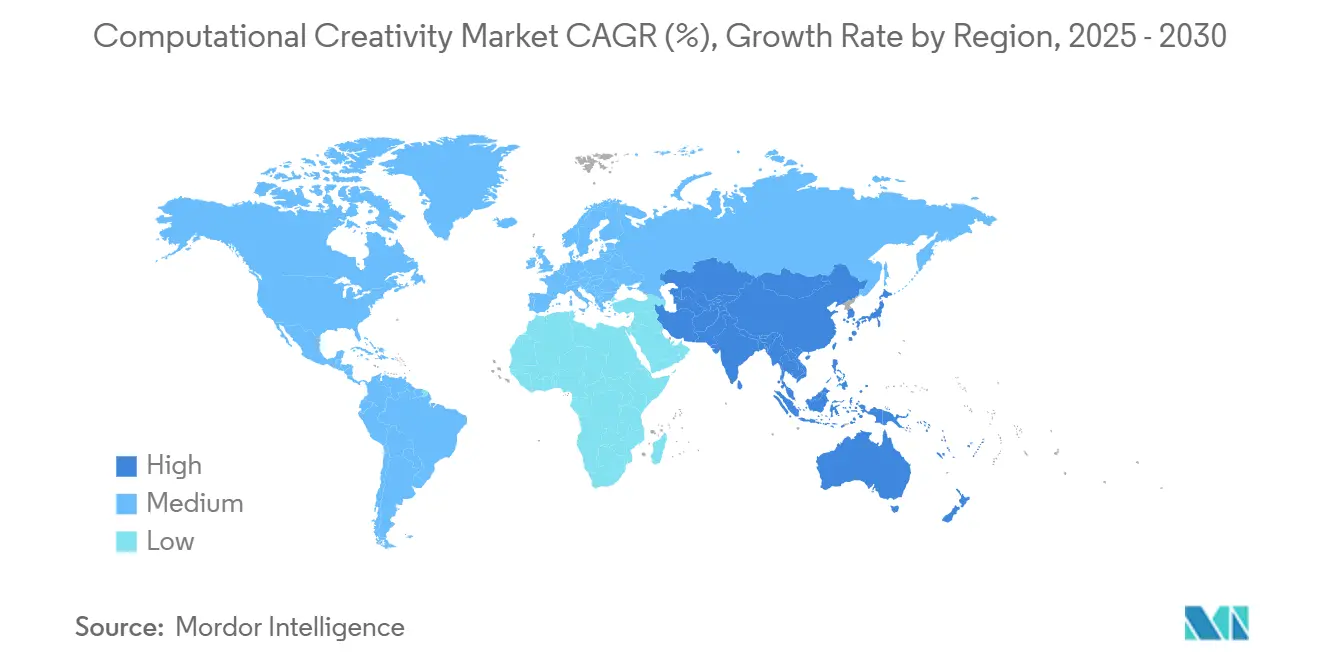

- By geography, North America captured 38.5% of 2024 revenue, but Asia-Pacific is forecast to be the fastest-growing region at 21.9% CAGR to 2030.

Global Computational Creativity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Democratization of Generative AI Toolkits | +3.2% | North America, Europe, expanding Asia-Pacific | Medium term (2–4 years) |

| Falling Cloud-Compute Costs and API Pricing | +2.8% | Global, price-sensitive Asia-Pacific markets | Short term (≤ 2 years) |

| Integration into Creative-Suite Ecosystems | +2.1% | North America, Europe | Medium term (2–4 years) |

| Enterprise Demand for Hyper-Personalized Content | +4.3% | North America, China | Long term (≥ 4 years) |

| Emergence of Multimodal Foundation Models | +3.7% | United States, China | Long term (≥ 4 years) |

| Rise of Procedural Generation in Digital Twins | +2.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Democratization of Generative AI Toolkits

No-code development environments and pre-trained foundation models are removing specialist barriers to entry. Creatives can prompt-engineer assets directly inside Adobe Firefly, which now hosts models from OpenAI and Google, generating more than 22 billion images to date. Amazon Bedrock Studio follows a similar path, letting corporate teams orchestrate multiple models without building infrastructure. As toolkits proliferate, competitive advantage shifts toward workflow design and brand-safe guardrails. Mid-market firms that once lacked ML skills are now early adopters, broadening the computational creativity market.

Falling Cloud-Compute Costs and API Pricing

Optimization chips, model quantization, and prompt-caching reduce run-time costs by double-digit percentages, letting smaller studios test high-resolution video generation that was unaffordable two years ago. Microsoft cites a 3.7x ROI on generative AI deployments, attributing savings chiefly to lower inference fees.[1]Mackenzie Ferguson, “Microsoft Reports 3.7x ROI with Generative AI,” opentools.ai Amazon introduced Intelligent Prompt Routing that automatically steers queries to the most cost-efficient model instance, cutting latency and spend for heavy users. Cost deflation encourages experimentation in Asia-Pacific, where generative-AI budgets tripled in 2024.

Integration into Creative-Suite Ecosystems

Embedding AI agents inside productivity software reduces context switching and accelerates adoption. Adobe and Microsoft integrate brand-safe generation into Microsoft 365 Copilot, enabling marketers to draft visuals, copy and layouts without leaving Office apps. IBM links its watsonx models to Salesforce’s Einstein 1 platform, showing that creative AI will permeate business workflows beyond design teams. Integrated ecosystems create lock-in effects that favor incumbents able to bundle storage, asset libraries and AI inference under single subscriptions.

Enterprise Demand for Hyper-Personalized Content

Brands compete on relevance at scale, needing thousands of localized variations of ads, packaging and in-app experiences. Automotive OEMs employ generative design to tailor vehicle interiors for individual buyers while optimizing energy efficiency. Retailers that automate creative iterations report shorter campaign cycles and higher click-through rates, pushing the computational creativity market toward essential-infrastructure status for customer-experience teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copyright and IP Ownership Uncertainty | −2.7% | EU, United States | Medium term (2–4 years) |

| High-Quality Data Acquisition Costs | −1.9% | Global, affects emerging developers | Short term (≤ 2 years) |

| Data-Privacy Compliance Overheads | −1.4% | Europe, North America | Medium term (2–4 years) |

| Model Hallucination and Brand-Risk Concerns | −1.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Copyright and IP Ownership Uncertainty

The US Copyright Office continues a multipart inquiry into AI authorship, maintaining ambiguity over whether AI outputs qualify for copyright if human contribution is minimal.[2]John Hines, “U.S. Copyright Office to Issue Further AI Guidance,” natlawreview.com Hollywood studios question liability for AI-generated video content, slowing adoption of longer-form tools. In the EU, the Artificial Intelligence Act demands disclosure of copyrighted training material, adding compliance costs that small vendors struggle to absorb. Vendors such as Adobe mitigate risk by training exclusively on licensed or stock content, but this narrows data diversity and raises development budgets.

High-Quality Data Acquisition Costs

Premium text, image and video archives now command multimillion-dollar licensing agreements. OpenAI’s deal with Condé Nast unlocks decades of journalism but illustrates the high cost of quality data. Academic researchers with limited budgets turn to synthetic data, yet fidelity gaps surface in fine-grained tasks such as photorealistic shadow rendering. Rights-cleared datasets thus become competitive moats for well-capitalized players, potentially slowing market democratization in less funded regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Transformers Reshape Creative AI Architecture

Generative Adversarial Networks retained 39.5% of the computational creativity market share in 2024, thanks to their maturity in image and video generation workflows. Transformer-based Large Language Models, however, are registering a 29.2% CAGR that will realign vendor roadmaps toward unified multimodal stacks. Google’s Gemini demonstrates text-to-video and audio capabilities within one model, signaling consolidation around transformer backbones. Evolutionary algorithms and probabilistic models survive in niche optimization tasks such as industrial digital twins, while hybrid ensembles support uncertainty-aware creative decisions. Vendors emphasizing single-modality excellence face erosion as enterprises prefer holistic model catalogs that cover concepting, editing, and deployment in one interface.

The computational creativity market size for transformer-based models is expected to surpass USD 2 billion by 2030, mirroring the pivot of SaaS platforms that now embed text-to-anything capabilities. As training moves toward trillion-parameter scales, specialized acceleration chips and efficient fine-tuning methods become critical purchase criteria for buyers evaluating the long-term cost of ownership.

By Application: Gaming Drives Creative AI Innovation

Marketing and Advertising Content captured 29.5% of the computational creativity market size in 2024, anchored by social-media video variants and dynamic banner creation. Gaming and Virtual World Building is growing fastest at a 24.6% CAGR, accelerated by real-time procedural asset generation that cuts level-design timelines from months to days. Studios integrate scene-expansion APIs and AI-directed non-player characters, widening gameplay variety without proportional headcount increases.

Art and Design creation maintains relevance as creative-suite giants roll out style-transfer and vector-generation models. Music Composition benefits from transformer audio decoders capable of minute-long tracks, expanding use cases in advertising jingles and in-game scores. Industrial-design workflows tap generative CAD to iterate lightweight components; Autodesk’s Project Bernini converts sketches into manufacturable 3D models within seconds. Scriptwriting and long-form storytelling lag owing to unresolved legal debates, but experiments continue in preview-only modes on major streaming platforms.

By Deployment Mode: Cloud Infrastructure Dominates Creative AI

Cloud environments accounted for 69.5% of the computational creativity market share in 2024 and will compound at a 20.1% CAGR as firms seek always-current model catalogs and elastic GPUs. Amazon Bedrock now aggregates more than 100 foundation models, turning deployment into a marketplace experience rather than a build-or-buy decision. On-premise remains relevant for latency-sensitive and regulated workloads, notably in financial services, video KYC, and government content redaction. Hybrid patterns emerge where inference runs locally while model updates sync from the cloud, balancing security against innovation velocity.

Competitive pricing wars among hyperscalers will likely compress margins yet expand the total computational creativity market. Vendors that layer proprietary editing UIs atop generic APIs differentiate through workflow depth rather than raw model access.

By End-User Industry: Entertainment Leads AI Creative Adoption

Media and Entertainment Companies generated 34.2% of 2024 revenue, leveraging AI to automate trailer cuts, subtitle localization, and thumbnail optimization. Netflix publicly confirmed the use of generative AI in series production, validating creative-grade quality levels. Gaming Studios and Publishers will post the highest CAGR at 22.7% as they embed real-time generation into player experiences.

Automotive and Industrial Designers deploy generative design to balance aerodynamics with aesthetic preference in electric vehicles, shrinking prototype cycles. Education and EdTech firms apply prompt-driven lesson builders that tailor content to learning styles, although ethical use guidelines remain under development. Research Institutes experiment with AI-augmented musical instruments that enable live creative exchange between performers and models.[3]Joseph Paradiso, “AI-Augmented Musical Instruments,” MIT Press, mit.edu Cross-industry diffusion suggests that implementation maturity, not industry type, will determine future spending acceleration.

Geography Analysis

North America held 38.5% of the computational creativity market in 2024. Deep venture-capital pools, mature cloud infrastructure and active policy discussions around AI copyright underpin adoption. The US Department of Defense’s multivendor generative-AI pilot contracts, each worth up to USD 200 million, highlight governmental appetite for AI-generated simulation assets. Yet unresolved copyright guidance keeps risk-averse media firms in experimental modes, slowing volume deployment until 2025 frameworks arrive.

Asia-Pacific is the fastest-expanding territory at a 21.9% CAGR. Chinese investment reached USD 2.1 billion in 2024, fueling local foundation-model development as regulatory sandboxes stabilize datasets for commercial training. Japan’s supportive policy and reliable power grid attracted OpenAI’s first Asian office in Tokyo, reinforcing regional talent pools.[4]Asia Pacific Foundation of Canada, “Why OpenAI Chose Tokyo,” asiapacific.ca Enterprises prioritizing localized language models in Korean and Bahasa Indonesia are expanding vendor opportunities across Southeast Asia.

Europe combines steady demand with rigorous regulation. The Artificial Intelligence Act, effective July 2024, mandates transparency on copyrighted training data, pushing vendors to certify datasets and thereby gaining trust from regulated industries. France leads funding flows, evidenced by Paris-based Aive’s EUR 12 million (USD 14 million) raise for multimodal video automation. London hosts a dense cluster of creative-AI startups leveraging access to global advertising agencies. Pan-European public-private initiatives aim to secure sovereign GPU capacity, ensuring the computational creativity market can scale without external bottlenecks.

Competitive Landscape

The computational creativity market is moderately fragmented but trending toward tighter concentration. Adobe leverages its Creative Cloud franchise, with Firefly users creating 22 billion assets and benefiting from brand-safe training sets. Microsoft embeds generative AI into Office, Teams and Azure AI Studio, claiming 3.7x ROI for early enterprise adopters. Amazon positions Bedrock as a neutral model marketplace, onboarding Stability AI and Anthropic models to attract multi-cloud users.

Specialized players innovate on vertical workflows. Runway, valued at USD 3 billion, pioneered text-to-video editors and is extending into interactive gaming experiences. Stability AI stabilized finances through fresh funding and leadership change, refocusing on open-weights diffusion models. Autodesk acquired Wonder Dynamics to pull AI-driven character animation into its 3D-design suite, signaling that large software incumbents will buy niche innovations rather than build in-house [5]Dan Sarto, “Autodesk Acquires Wonder Dynamics,” awn.com.

Regulation acts as a scale moat that favors well-capitalized vendors able to afford dataset disclosures and risk assessments. Firms that develop “commercially safe” training pipelines secure enterprise deals faster, whereas startups reliant on web-scraped data find procurement cycles lengthening. As multimodal foundations commoditize, differentiation shifts to domain-specific fine-tuning, user experience and compliance certifications.

Computational Creativity Industry Leaders

Adobe Inc.

OpenAI, Inc.

Google LLC (Alphabet, Inc.)

Microsoft Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Meta approached AI startup Runway about a takeover before finalizing a USD 14.3 billion investment in Scale AI.

- June 2025: Runway, valued at USD 3 billion, announced plans for an interactive gaming experience launching later in 2025.

- June 2025: Aive raised EUR 12 million (USD 14 million) in Series A funding to scale multimodal video post-production automation.

- May 2025: IBM and Scuderia Ferrari HP rolled out a watsonx-powered mobile app to enhance the Formula 1 fan experience for 400 million supporters.

Global Computational Creativity Market Report Scope

| Generative Adversarial Networks (GANs) |

| Transformer-based Large Language Models |

| Evolutionary and Genetic Algorithms |

| Probabilistic and Bayesian Models |

| Hybrid and Ensemble Systems |

| Art and Design Creation |

| Music Composition and Sound Design |

| Gaming and Virtual World Building |

| Marketing and Advertising Content |

| Product and Industrial Design |

| Storytelling and Scriptwriting |

| Cloud-based |

| On-Premise |

| Media and Entertainment Companies |

| Gaming Studios and Publishers |

| Advertising and Creative Agencies |

| Automotive and Industrial Designers |

| Education and EdTech |

| Research Institutes and Academia |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Technology | Generative Adversarial Networks (GANs) | ||

| Transformer-based Large Language Models | |||

| Evolutionary and Genetic Algorithms | |||

| Probabilistic and Bayesian Models | |||

| Hybrid and Ensemble Systems | |||

| By Application | Art and Design Creation | ||

| Music Composition and Sound Design | |||

| Gaming and Virtual World Building | |||

| Marketing and Advertising Content | |||

| Product and Industrial Design | |||

| Storytelling and Scriptwriting | |||

| By Deployment Mode | Cloud-based | ||

| On-Premise | |||

| By End-User Industry | Media and Entertainment Companies | ||

| Gaming Studios and Publishers | |||

| Advertising and Creative Agencies | |||

| Automotive and Industrial Designers | |||

| Education and EdTech | |||

| Research Institutes and Academia | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the computational creativity market?

The computational creativity market size stands at USD 1.79 billion in 2025.

How fast will the computational creativity market grow through 2030?

The market is projected to expand at a 19.18% CAGR, reaching USD 4.30 billion by 2030.

Which technology segment is expanding the quickest?

Transformer-based Large Language Models record the fastest growth, registering a 29.2% CAGR through 2030.

Why do cloud-based deployments dominate the computational creativity market?

Cloud platforms offer elastic GPU capacity, frequent model updates and usage-based pricing, capturing 69.5% market share in 2024.

Page last updated on: