Nano Paints And Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.43 Billion |

| Market Size (2031) | USD 16.64 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

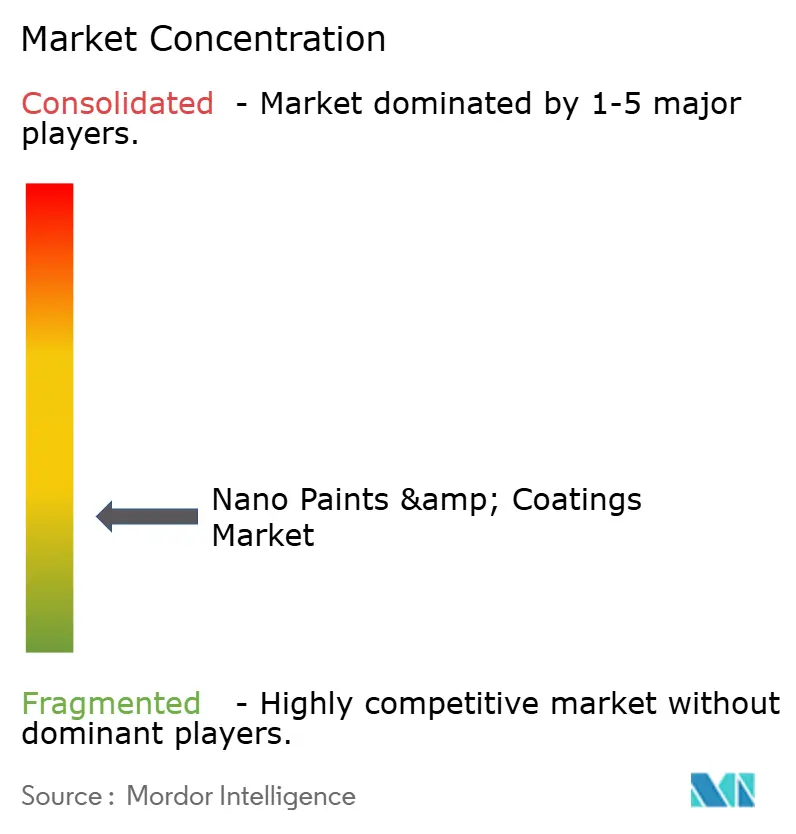

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nano Paints And Coatings Market Analysis by Mordor Intelligence

Nano Paints & Coatings Market size in 2026 is estimated at USD 13.43 billion, growing from 2025 value of USD 12.87 billion with 2031 projections showing USD 16.64 billion, growing at 4.38% CAGR over 2026-2031. Growing aerospace demand for corrosion-lightweight solutions, electric vehicle fire-safety requirements, and infrastructure durability needs keep the market on a steady upward course. A dominant 39.17% nano-TiO₂ share combined with graphene’s rapid 5.17% CAGR underlines the core role of advanced nanomaterials in sustaining competitive advantage. Regional momentum remains firmly with Asia-Pacific, which controls almost half of global revenues and commands the fastest regional growth. Supply advances in chemical vapor deposition (CVD) and a shift toward multifunctional formulations that merge corrosion protection, thermal management, and antimicrobial performance are shaping new business opportunities, while high production costs and evolving nano-toxicity rules restrain rapid scale-up.

Key Report Takeaways

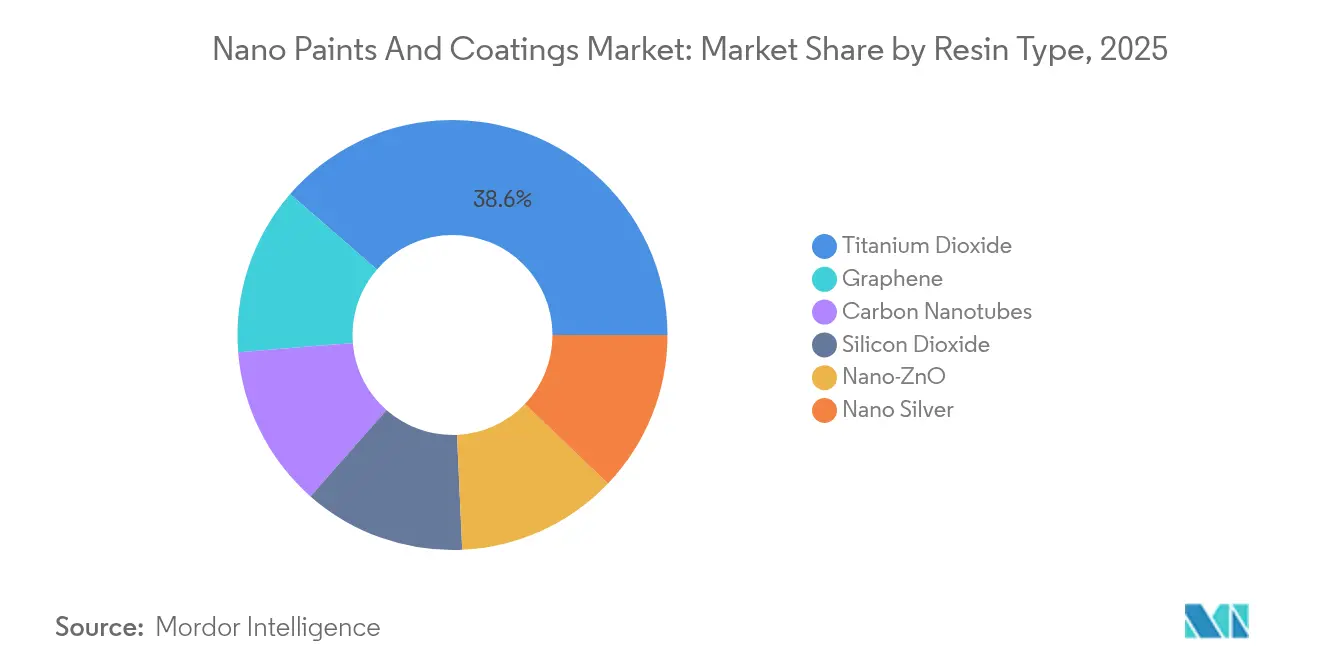

- By resin type, titanium dioxide held 38.62% of the nano paints & coatings market share in 2025, whereas graphene is forecast to expand at a 4.93% CAGR through 2031.

- By application method, chemical vapor deposition led with 38.10% revenue share in 2025, while maintaining a 4.82% CAGR to 2031.

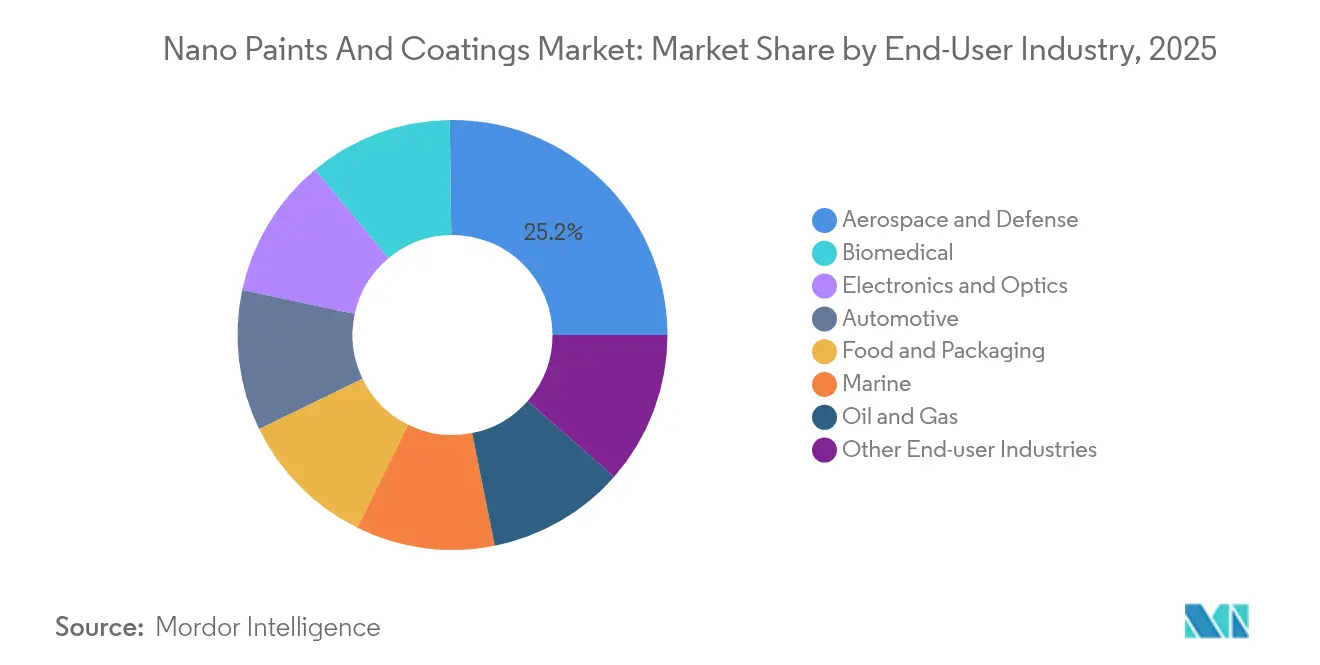

- By end-user industry, aerospace and defense accounted for 25.20% of the nano paints & coatings market size in 2025; biomedical is advancing at a 5.18% CAGR through 2031.

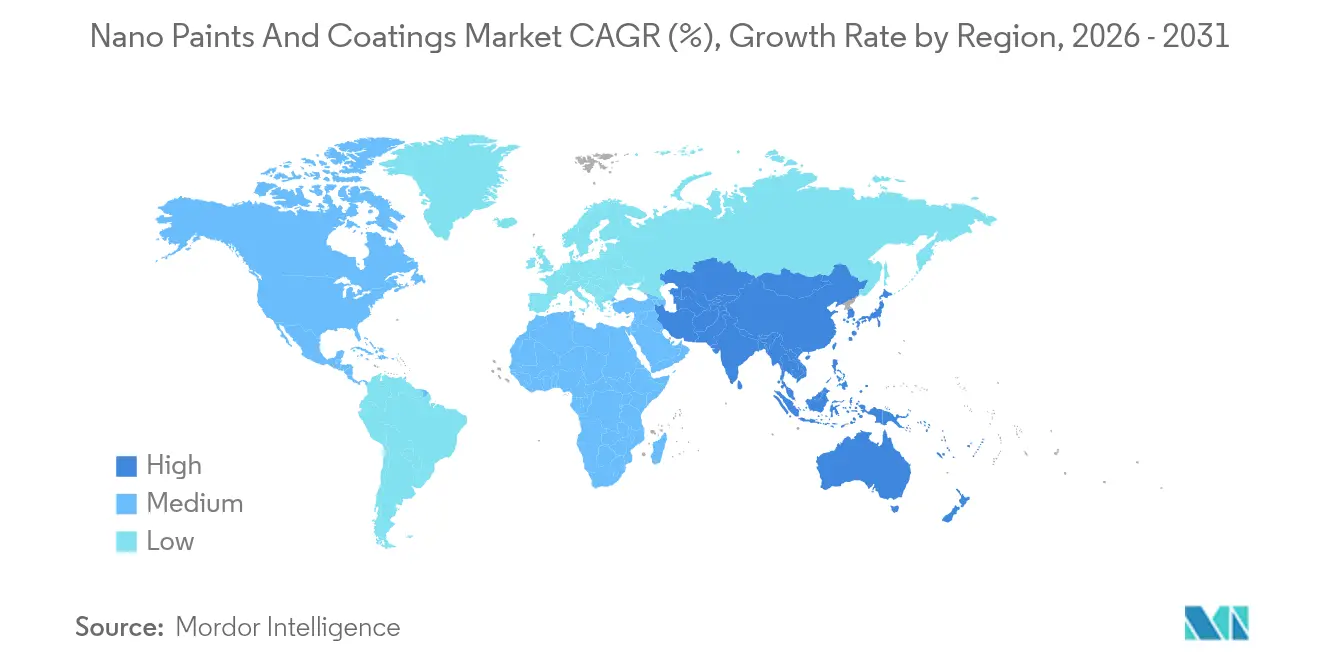

- By geography, Asia-Pacific held 45.05% revenue share in 2025 and is projected to rise at a 4.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nano Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerospace and defense corrosion-light-weight push | +1.20% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Increase in demand for EV thermal-fire-safety coating | +0.90% | APAC core, spill-over to North America & Europe | Short term (≤ 2 years) |

| Growing requirement for high performance coatings | +0.80% | Global | Long term (≥ 4 years) |

| Inceasing demand from infrastructure sector | +0.70% | APAC & Middle East, expansion to emerging markets | Medium term (2-4 years) |

| Rise in utilization from electronics and consumer goods | +0.60% | APAC concentrated, global distribution | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aerospace and defense corrosion-light-weight push

Pentagon estimates that corrosion costs USD 23 billion each year across military equipment, intensifying the adoption of nano coatings that combine structural lightness with superior protection. Field data show nano-engineered layers lowering maintenance cycles on naval airframes, while icephobic properties enhance aircraft readiness in extreme climates. Programs under the U.S. Navy SBIR banner are moving from bench research to fleet trials, illustrating that rigorous certification barriers simultaneously limit new entrants and guarantee durable demand for validated suppliers. As defense procurement strategies favor platforms with reduced total ownership cost, single-application nano formulations that solve weight, durability, and environmental exposure challenges are increasingly specified.

Increase in demand for EV thermal-fire-safety coating

Rapid electrification pushes battery systems toward higher energy density and stricter safety standards. Specialized nano layers dissipate heat swiftly and form fire-retardant barriers, protecting cells and adjacent components. Resonac’s thermal insulation product for EV packs highlights active commercial development. Carbon and graphene dispersions deliver thermal conductivity without sacrificing dielectric strength, matching OEM safety protocols. In parallel, passenger-comfort solutions such as Hyundai’s nano cooling film that cuts cabin temperature by 10 °C demonstrate spill-over into ancillary applications. Regulatory frameworks that incorporate thermal runaway containment accelerate volume adoption, especially in Asia-Pacific, where battery production capacity is highest.

Growing requirement for high performance coatings

Ageing bridges, tunnels, and power infrastructure confront harsher environmental loads, calling for materials that stretch maintenance cycles. Nano-silica-dosed concrete retained 79% bond strength after corrosive exposure, vastly outperforming conventional mixes that fell to 27%[1]H. Nguyen, “Nano-silica concrete durability tests,” World Academy of Science, waset.org . Ultra-high-performance composites reinforced at the nanoscale move the narrative from reactive repair to proactive asset preservation. Self-healing mechanisms—stimulated by encapsulated nanomaterials—further align with reduced lifecycle emissions targets. Government stimulus packages in several regions, notably the United States and Japan, earmark advanced-material spend, translating into pipeline demand for high-specification protective layers.

Increasing demand from infrastructure sector

Ports, railways, and energy corridors prioritize longevity against saline, UV, and mechanical stresses. Iranian advances in self-repairing steel coatings, validated for marine environments, exemplify ongoing R&D to lower the total cost of ownership. Commercial implementations, such as GoNano’s roofing systems that add 10–15 years of service life, illustrate immediate payback for property developers. Cement composites with carbon nanotube additives lift compressive strength by up to 50% and slash permeability, critical in hot, humid regions[2]L. Smith, “Carbon nanotube cement composites,” Buildings, mdpi.com . Consequently, nano formulations earn acceptance in public-private partnership tenders that weigh long-term sustainability metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost of nanomaterials | -0.80% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

| Nano-toxicity regulatory uncertainty | -0.50% | Europe & North America leading, global adoption | Long term (≥ 4 years) |

| Graphene CVD reactor supply bottlenecks | -0.30% | Global, concentrated in advanced manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High production cost of nanomaterials

Specialized CVD reactors, low-yield batch processes, and stringent purity requirements keep unit costs elevated. Capital requirements delay adoption in price-sensitive uses such as consumer furniture, despite technical performance benefits. Venture capital continues to inject funds—Forge Nano’s USD 40 million raise underscored private backing—but many scale-up programs remain in pilot phase, pointing to gradual cost attrition rather than abrupt drops. Producers pursue inline metrology, precursor recycling, and hybrid wet-chemistry steps to cut expenses, yet breakeven economics still hinge on premium applications.

Nano-toxicity regulatory uncertainty

Global agencies refine safety protocols for nanoscale substances across coatings, cosmetics, and medical devices. United States EPA rules now treat specific carbon nanotubes as new chemicals, enforcing pre-manufacture notification, while FDA guidance outlines toxicological data packages for nanomaterial-bearing drugs[3]U.S. Environmental Protection Agency, “Significant New Use Rule for Carbon Nanotubes,” epa.gov . Europe deploys separate Annex entries in REACH, adding characterization burdens. Producers funnel resources into in vivo and in vitro studies, stretching time-to-market. Cross-border projects face duplicated reviews, especially when coatings are destined for multi-regional supply chains. Non-compliance risks product recalls, prompting conservative launch strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Titanium dioxide dominates while graphene accelerates

Nano-TiO₂ kept its 38.62% hold on the nano paints & coatings market in 2025. Stable manufacturing, photocatalytic self-cleaning performance, and cost efficiency drive its acceptance on facades, automotive trims, and indoor anti-smog panels. Korean pilot lines producing ultra-large transparent screens using TiO₂ nanoparticles at one-tenth the price of OLED glass underscore this material’s scalability. Graphene, although capped at a modest base, posts a 4.93% CAGR through 2031 as demand from battery heat spreaders and electromagnetic shielding intensifies. Carbon nanotubes remain a niche choice for aerospace and high-end consumer electronics where structural stiffness, conductivity, and weight savings converge. Nano-SiO₂ extends its presence in cement additions that lengthen infrastructure life, and nano-ZnO secures UV-blocking coatings for medical devices and smartphones. Future growth leans on hybrid recipes pairing multiple nanoparticles to secure synergistic properties.

The nano paints & coatings market size for titanium dioxide resin applications is projected to widen steadily, while graphene’s share expands faster under supply chain releases and reactor capacity additions. Complementing that trajectory is a parallel push for green synthesis routes that use bio-derived precursors or solvent-free dispersion to cut carbon footprint.

By Method: CVD retains lead yet gears toward higher throughput

Chemical vapor deposition delivered 38.10% revenue in 2025 and carries a 4.82% CAGR outlook to 2031. The method’s precise layer control and defect management put it at the center of semiconductor, optics, and aerospace programs. However, traditional flat-bed reactors handle limited substrate widths and slow ramp times, fuelling investments into roll-to-roll, concentric-tube, and plasma-enhanced variants that triple square-meter output while reducing energy intensity. Nano Dimension’s repositioning following the Desktop Metal decision reinforces capital flows toward specialized CVD know-how as providers target both 3D-printed electronics and functional coating subcontracts.

Physical vapor deposition continues as a workhorse for premium cosmetic finishes and micro-electronics passivation layers. Apple’s PVD-boosted aluminum enclosure remains a benchmark, highlighting consumer electronics pull. Atomic layer deposition answers atomic-scale uniformity demands in MEMS sensors and biomedical stents. Electrospray and electrospinning thrive in drug-eluting patches, and sol-gel coatings gather pace in infrastructure where fast, low-temperature curing is prized. Inter-method hybrids emerge, combining CVD seed layers with sol-gel over-coats to mix high adhesion and cost efficiency.

By End-User Industry: Biomedical catches up with aerospace leadership

Aerospace and defense retained 25.20% of 2025 spending, as mission-critical aircraft, drones, and naval assets adopt nano layers to beat weight and corrosion. Composite airframes rely on ultra-thin protective skins that do not hinder radar stealth or dielectric properties. For instance, U.S. fighter upgrade programs now list nano-sealants in corrosion control standards. The biomedical segment, clocking a 5.18% CAGR, climbs on approvals for antibacterial catheters, orthopedic implants, and sustained drug-release coatings. Hospitals value nano-silver barriers on high-touch surfaces, paired with regulatory pathways that now recognize ISO-standard test methods.

Automotive growth links to electric drivetrain cooling and scratch-resistant body trims. Electronics benefit from anti-smudge, EMI-shielding, and moisture-barrier layers critical for foldable screens and wearable devices. Food packaging pilots integrate nano-ZnO to curb microbial spoilage but tread carefully under food safety oversight. Marine and offshore operators deploy foul-resistant nano-filled resins to shave fuel burn and dry-dock costs. Construction upscales nano-TiO₂ façade paints that break down pollutants under sunlight, underpinning urban air-quality initiatives.

Geography Analysis

Asia-Pacific anchored 45.05% of global revenue in 2025, keeping the lead with a 4.65% CAGR outlook. China’s electronics supply chains, Japan’s materials science clusters, and South Korea’s display fabs guarantee a stable baseline. Policy incentives, such as China’s Made-in-China 2025 priorities and Japan’s Moonshot R&D goals, accelerate nano production capability, shortening lead times. Local CVD reactor suppliers help diffuse technology beyond top-tier conglomerates, enabling mid-size coating shops to certify nano offerings.

North America’s demand profile centers on aerospace, defense, and medical devices. U.S. Air Force sustainment commands and space launch primes view nano-layering as strategic maintenance cost reducers. Mexico’s ascending EV assembly ecosystem imports nano thermal films and battery coating systems, integrating seamlessly with regional supply. Europe champions eco-design and worker safety, thus driving the adoption of nano-formulated water-borne coatings that satisfy REACH and green building labels. Germany’s automotive Tier-1 suppliers and France’s aerospace OEMs lock up multi-year framework agreements with nano-coating specialists.

South America injects momentum from infrastructure rehabilitation commitments in Brazil’s transport corridors and Argentina’s shale play servicing. Exposure to salt spray, high humidity, and UV intensity places a premium on high-performance coatings, and local paint majors partner with Japanese and German nanomaterial producers to localize blends. The Middle East’s energy sector trials nano layers on downhole pumps and export pipelines to combat sour corrosion, while Africa’s growth story lies in water networks, where internally applied nano sealants cut leak rates under high ambient heat.

Regulatory Landscape

Nano paints and coatings producers face tighter controls on nanoforms. In the EU, compliance is anchored through REACH and CLP, with dedicated nanoform registration requirements effective since January 1, 2020 under the REACH nanoform annexes overseen by ECHA. In the United States, TSCA continues to shape market access for certain nanomaterials, including carbon-based nano-additives, with EPA using Significant New Use Rules (SNURs) to require advance notification for designated new uses. A final SNUR published May 2026 takes effect July 28, 2026 and reinforces pre-manufacture and processing notification discipline for affected substances.

Standardization also functions as a procurement and qualification gate where performance and release testing are scrutinized. Examples include SIST EN ISO 20427:2026 (published May 2026) covering preparation and dispersion of pigments and extenders for particle size analysis in coatings, ISO 21683 (EN ISO 21683:2020) for experimentally simulated nano-object release from paints and varnishes under mechanical stress, and India’s IS 18563:2024 code of practice for nanomodified paints and coatings, which sets manufacturing, testing, and quality control expectations for domestic supply chains.

Value Chain Analysis

The value chain starts with upstream nanomaterial and additive supply (nano-TiO2, nano-SiO2, nano-ZnO, nano-silver, carbon nanotubes, graphene/graphene oxide) plus supporting chemicals, dispersants, and binders. It then moves through particle functionalization and dispersion, followed by formulation into paints and coatings and conversion into application-ready systems. Midstream deposition and application capability differentiates outcomes: chemical vapor deposition (CVD), physical vapor deposition (PVD), atomic layer deposition (ALD), sol-gel, and spray-based routes influence film uniformity, throughput, and cost. Qualification testing and documentation increasingly run alongside manufacturing because nanoforms are regulated as substances under frameworks such as EU REACH.

Downstream, coatings are sold via direct OEM programs (aerospace, automotive displays, electronics, medical devices) and project-based channels (infrastructure, marine, oil and gas). Acceptance is tied to performance validation and compliance evidence. Value capture concentrates around (i) reactor and processing constraints for high-end carbon nanomaterials, including CVD-related capacity and know-how, (ii) consistent dispersion quality at scale, and (iii) the time and cost of safety dossiers and release testing for multi-regional supply. R&D also points to adoption strategies that reduce application steps, including published work on airbrush-applied graphene-on-metal workflows, while other advances focus on multi-functional systems (self-healing, anti-icing, antifouling) that raise downstream willingness to pay in marine and infrastructure maintenance cycles.

Competitive Landscape

The nano paints and coatings market is fragmented. Market leaders compete on formulation IP, nanomaterial supply integration, and application engineering rather than sheer volume. Traditional paint giants, such as PPG, leverage distribution but still outsource critical nanoparticles. Conversely, niche firms focus on protective films for wearables and automotive displays, anchoring revenue on patent-backed technologies. The value proposition gravitates toward multifunctionality: a coating that blocks corrosion, scatters heat, and neutralizes bacteria secures higher margins and reduces procurement complexity for OEMs.

Joint development agreements proliferate in battery supply chains as cell makers hedge material risk. Barriers to entry stem from nanomaterial sourcing, capital-intensive deposition lines, and stringent aerospace or medical validations. Despite consolidation moves, room remains for start-ups exploiting machine-learning-aided dispersion or bio-sourced precursors.

Industry consortia, including the Graphene Flagship and NNI workgroups, foster pre-competitive standards, but IP fences around dispersion chemistry and substrate adhesion remain tall. The field thus balances collaborative ecosystem building with proprietary edge retention.

Nano Paints And Coatings Industry Leaders

Artekya Teknoloji

BASF

Henkel AG and Co. KGaA

Nanoshine Group Corp

PPG Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities concentrate where nano-enabled coatings address measurable operational constraints for OEMs and asset owners, especially thermal management, durability, and multifunctionality. EV-related thermal and safety requirements create a direct commercialization channel for nano thermal-barrier and heat-spreading layers, supported by visible market activity such as Resonac highlighting EV pack thermal insulation solutions. Adjacent comfort and thermal uses also show traction, including Hyundai’s nano cooling film that reduces cabin temperature by 10 degrees C. A separate whitespace area is coatings that perform under water-lubricated or aggressive-service conditions: published 2026 research on nano-MoS2-PEG modified epoxy coatings reporting large friction and wear reductions points to demand pull from industrial hydraulics and marine-adjacent mechanical systems where maintenance cost is a primary buying metric.

A second opportunity stream is sustainability-driven reformulation and new functional aesthetics that reduce reliance on conventional chemistries while maintaining durability. Structural color and radiative-cooling coatings broaden the end-use set beyond corrosion and scratch resistance, with 2026 work on gold nanoparticle-based structural color paint and separate research on single-layer radiative cooling paint with high NIR reflectance pointing to pathways for UV-cured, low-fading coloration and heat-mitigation surfaces. In parallel, EU nanoform compliance under REACH, along with upcoming reporting obligations tied to microplastics restrictions (Commission Regulation 2023/2055, with annual reporting to ECHA starting May 31, 2027 for certain derogated paint uses), increases the value of data-rich, traceable formulations and compliant dispersion and testing workflows for suppliers targeting European architectural coatings and packaging-adjacent value chains.

Recent Industry Developments

- July 2026: BASF launched certified biomass-balanced additives for architectural coatings, expanding its portfolio with products such as Dispex AA 4145 MB, Rheovis PU 1333 MB, and Rheovis HS 1169 MB. The company’s additions support formulators seeking lower-fossil-content inputs and aim to capture demand linked to sustainability criteria in building and construction coating specifications.

- April 2026: Henkel launched Loctite AF 8810 and Loctite AF 8812, anti-fingerprint coatings for automotive displays formulated without PFAS or fluorine ingredients. This strengthens Henkel's access to electronics and in-vehicle display coating programs, where optical clarity, smudge resistance, and restricted-substance compliance influence OEM material selection.

- February 2025: Pellucere Technologies opened a nano coatings manufacturing facility in Chakan, Maharashtra, India, with annual capacity of 8,500 metric tons for antireflective and anti-soiling applications. Local capacity build-out improves lead times for Asia-Pacific customers and increases competitive intensity for regional suppliers serving solar, glass, and exterior surface protection uses.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the nano paints and coatings market is defined as revenue generated from paints and coatings that use nanoscale materials or structures to improve performance, such as corrosion resistance, UV durability, antimicrobial behavior, or self-cleaning properties.

Scope exclusions: Excludes adjacent nanomaterials sold as standalone additives when they are not sold and priced as finished paint or coating products.

Segmentation Overview

- By Resin Type

- Graphene

- Carbon Nanotubes

- Nano-TiO₂ (Titanium Dioxide)

- Nano-SiO₂ (Silicon Dioxide)

- Nano-ZnO

- Nano Silver

- By Method

- Electrospray and Electrospinning

- Chemical Vapor Deposition (CVD)

- Physical Vapor Deposition (PVD)

- Atomic Layer Deposition (ALD)

- Aerosol Coating

- Self-Assembly

- Sol-Gel

- By End-User Industry

- Aerospace and Defense

- Automotive

- Electronics and Optics

- Biomedical

- Food and Packaging

- Marine

- Oil and Gas

- Other End-user Industries (Energy and Power, Construction and Infrastructure, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set a practical market boundary and to build starting points for demand, supply, and pricing assumptions that can be checked later. We relied on public sources such as the US Census Bureau and US International Trade Commission trade statistics, Eurostat industrial and trade series, and national statistics offices that publish chemicals and manufacturing indicators.

To make sure performance claims and adoption limits were not overstated, we also reviewed peer-reviewed journals and patents for coatings science and deposition route mentions (for example, CVD, ALD, sol-gel, and similar processes), then cross-checked with trade association publications and safety and regulatory references relevant to coatings. Company filings, investor presentations, and reputable press were used to map capacity signals, end-use exposure, and where product launches were actually targeted. In a few places, paid subscriptions for company financials, patent look-ups, and shipment-level trade views were used to fill gaps where public data did not provide sufficient detail. The sources listed here are illustrative only, and many other public documents and datasets were also referenced for cross-checks and clarification.

Primary Interviews and Surveys

Primary work was used to translate the desk inputs into usable sizing assumptions, especially where nano-enabled coatings are blended into broader coating portfolios. We spoke with a mix of raw material participants, formulators, applicators, distributors, and end-use buyers across major regions so that adoption rates, realistic price premiums, and typical use cases could be verified.

Feedback from these discussions was then used to confirm the split between functional nano coatings and conventional products, to sanity-check method-level penetration (for example, sol-gel versus vapor deposition routes), and to align the final demand pool with how procurement and specifications are written in real projects.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 48% |

| Mid tier: 53% | Functional/Unit leaders: 28% | EMEA: 34% |

| Smaller Players: 14% | Managers: 58% | Americas: 18% |

Market-Sizing & Forecasting

The core sizing logic used a top-down build where the broader paints and coatings demand pool was reconstructed by region and end-use, then filtered using penetration rates for nano-enabled formulations that are actually specified for performance needs. Those penetration rates were anchored using signals like construction and infrastructure activity, automotive and aerospace output, electronics manufacturing trends, and the pace of tighter durability and safety requirements.

To keep the totals realistic, the results were corroborated using selective bottom-up approximations such as sampled supplier and formulator revenue disclosures, channel checks on typical project volumes, and an ASP times volume cross-check for common functional use cases. Inputs that mattered most in the model included price premium ranges versus conventional coatings, the share of nano-TiO2, nano-SiO2, nano-silver, graphene, and carbon nanotube based formulations in commercialized products, the split by deposition or application method, and regional adoption differences tied to industrial activity.

For forecasting, scenario analysis was used so that adoption can flex with regulatory tightening, raw material pricing, and changes in end-user capex. Where bottom-up signals were incomplete, gaps were handled by using conservative penetration bands and then re-validating those bands with interview feedback before finalizing the time series.

Data Validation & Update Cycle

Validation was done through multiple checks so that one data series did not drive the whole outcome. Model outputs were compared with independent indicators, such as coatings production trends, trade movements for related chemical categories, patent activity, and observed price premium ranges discussed in interviews. Any unusual jumps were then reviewed and corrected.

Before sign-off, the work is reviewed in steps so assumptions, conversions, and growth logic stay consistent across regions and end uses. The report is refreshed annually, and interim updates are made when a material event changes pricing, supply availability, or adoption expectations. Right before delivery, a fresh analyst pass is completed so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's Nano Paints and Coatings Market Sizing Compared With Other Published Estimates

Published market sizes for nano paints and coatings often do not match because the market boundary is drawn differently, and the underlying price and adoption assumptions are updated on different schedules. A second driver is how firms treat what counts as nano-enabled, since some include broad nano-additive enriched coatings without checking whether nano performance is a priced feature.

The spread is usually explained by refresh cadence and currency timing (which impacts reported USD values), followed by how ASP premiums are applied over the forecast window and whether early-stage methods are counted at commercial scale. In our build, the date used for currency conversion, the annual re-check of price premiums, and the requirement to validate adoption using end-use demand signals are kept consistent, which is why the final total aligns to repeatable checks used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.43 B (2026) | |

| Trade Journal A | USD 3.72 B (2025) | This figure appears to use a narrower product scope that leans toward specialty nanotechnology coatings, which can exclude mainstream nano-additive formulations used in automotive and construction. The base year also differs, and the USD value can shift based on the currency conversion date and the assumed price premium per liter. |

| Regional Consultancy B | USD 13.19 B (2025) | The closer level suggests a similar demand pool, but differences can come from whether 2025 is treated as the base year versus a modeled step into 2026, and how fast ASP premiums are stepped down as volumes scale. Some estimates also smooth adoption too aggressively across end uses, without a separate check on method level commercialization. |

Overall, the table shows that scope and timing choices create most of the gap, even before growth assumptions are discussed. By tying adoption to end-use output indicators, applying a consistent currency timing rule, and rechecking ASP premiums during updates, the final number stays traceable to clear steps that can be repeated.

Key Questions Answered in the Report

What is the current valuation of the nano paints & coatings market?

The nano paints & coatings market size is valued at USD 13.43 billion in 2026.

How fast is the nano paints & coatings market expected to grow?

The market is projected to expand at a 4.38% CAGR from 2026 to 2031.

Which resin type dominates nano paints & coatings demand?

Nano-TiO₂ holds the top position with 38.62% of 2025 revenues, owing to its versatile self-cleaning and photocatalytic benefits.

Why is Asia-Pacific a key region for nano paints & coatings?

Asia-Pacific represents 45.05% of global turnover and offers the fastest growth at 4.65% CAGR due to strong electronics, automotive, and infrastructure activity.

What sectors are driving new nano coating applications?

Aerospace, electric vehicles, biomedical devices, and infrastructure projects are leading adopters, seeking corrosion resistance, thermal management, and antimicrobial functionality.

What main challenges could slow market expansion?

High nanomaterial production costs, evolving nano-toxicity regulations, and limited graphene CVD reactor capacity currently constrain wider adoption.

Page last updated on: