Drywall Textures Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.97 Billion |

| Market Size (2031) | USD 5.10 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

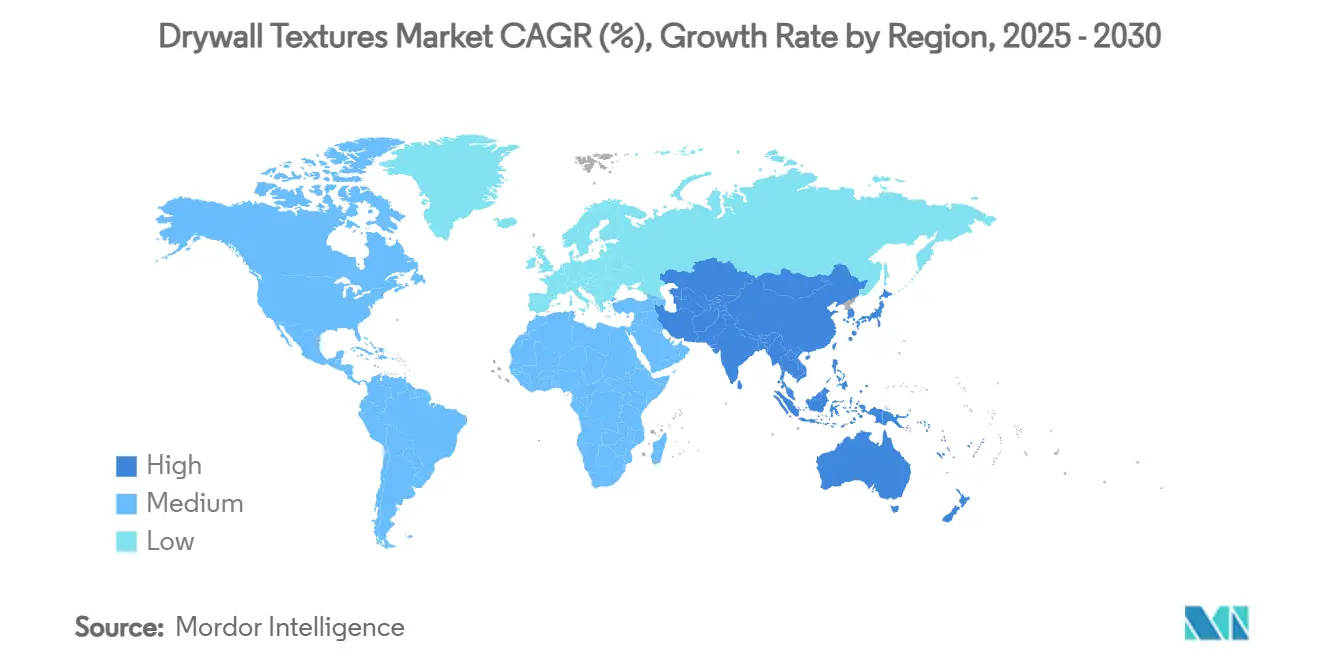

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drywall Textures Market Analysis by Mordor Intelligence

By 2031, the drywall textures market is set to grow from an estimated USD 3.78 billion in 2025 and USD 3.97 billion in 2026, reaching a projected USD 5.10 billion, marking a CAGR of 5.12% from 2026 to 2031. Aesthetic preferences are shifting towards textured finishes that provide depth beyond mere color. This trend is evident in both residential remodels and commercial retrofits, particularly in North America, where remodeling expenditures hovered around USD 524 billion in early 2026. Contractors are increasingly opting for texture solutions that not only enhance aesthetics but also mask minor surface imperfections, thereby expediting punch-list cycles. Concurrently, manufacturers are channeling investments into low-VOC formulations, aligning with the stringent indoor air quality regulations emerging in California and the European Union. The U.S. construction industry faced a notable challenge in 2025, with 439,000 jobs left unfilled. This labor shortage, coupled with rising wages, has catalyzed a pivot towards automated spray systems and robotic finishers, enhancing productivity while mitigating silica exposure risks. On another front, fluctuations in tariffs on gypsum inputs have led distributors to diversify their sourcing strategies and hedge against material costs. This has concurrently heightened interest in dry-mix powders, known for their ability to reduce freight expenses.

Key Report Takeaways

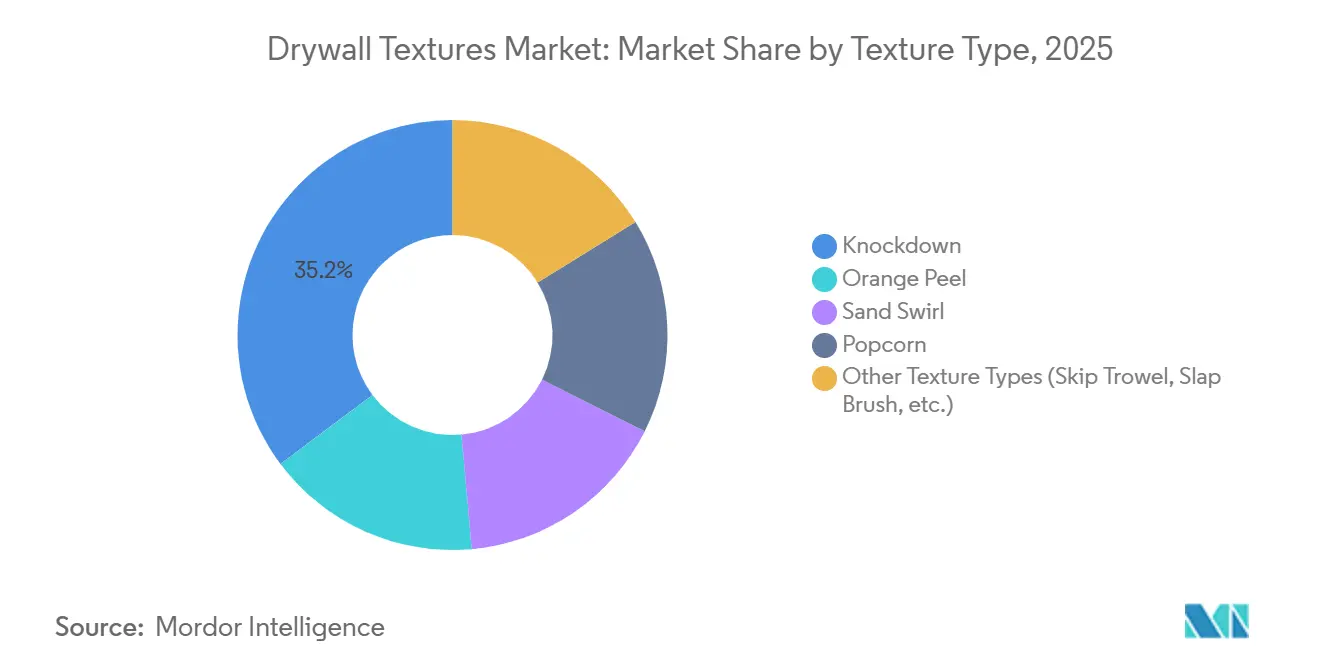

- By texture type, knockdown captured 35.23% of drywall textures market share in 2025, while also posting the fastest projected 5.35% CAGR from 2026 to 2031.

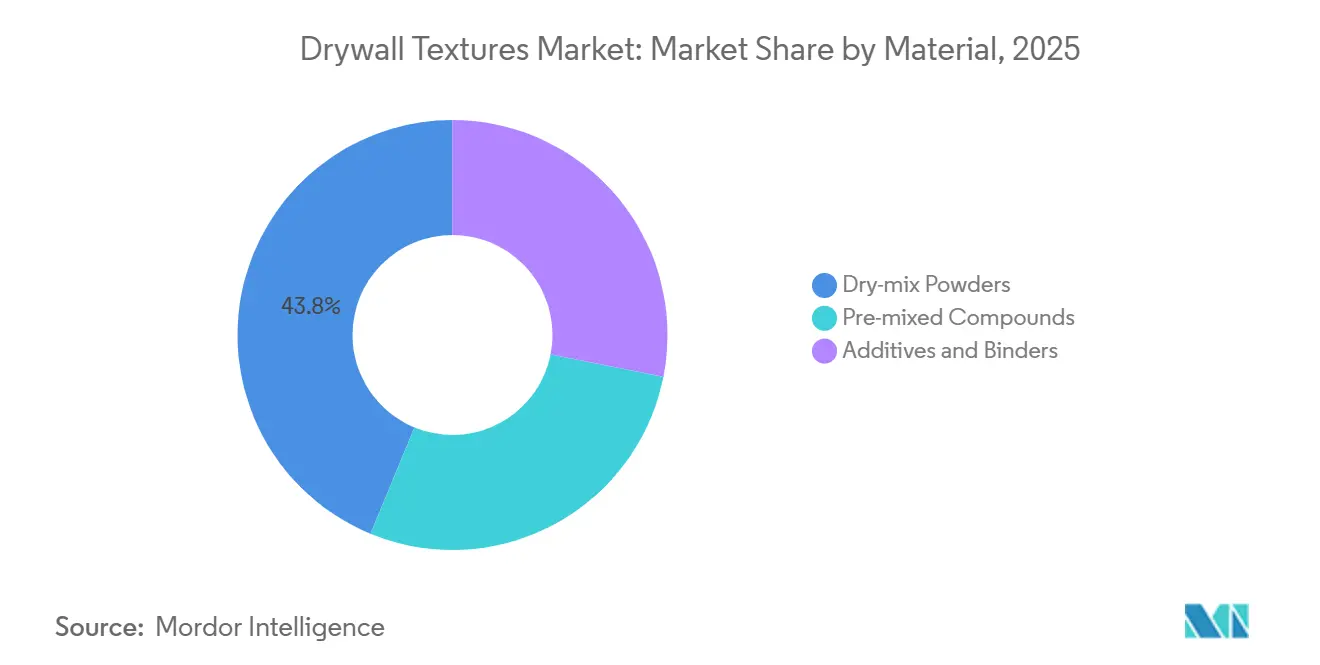

- By material, dry-mix powders held 43.78% share of the drywall textures market size in 2025 and are projected to expand at a 5.71% CAGR from 2026 to 2031.

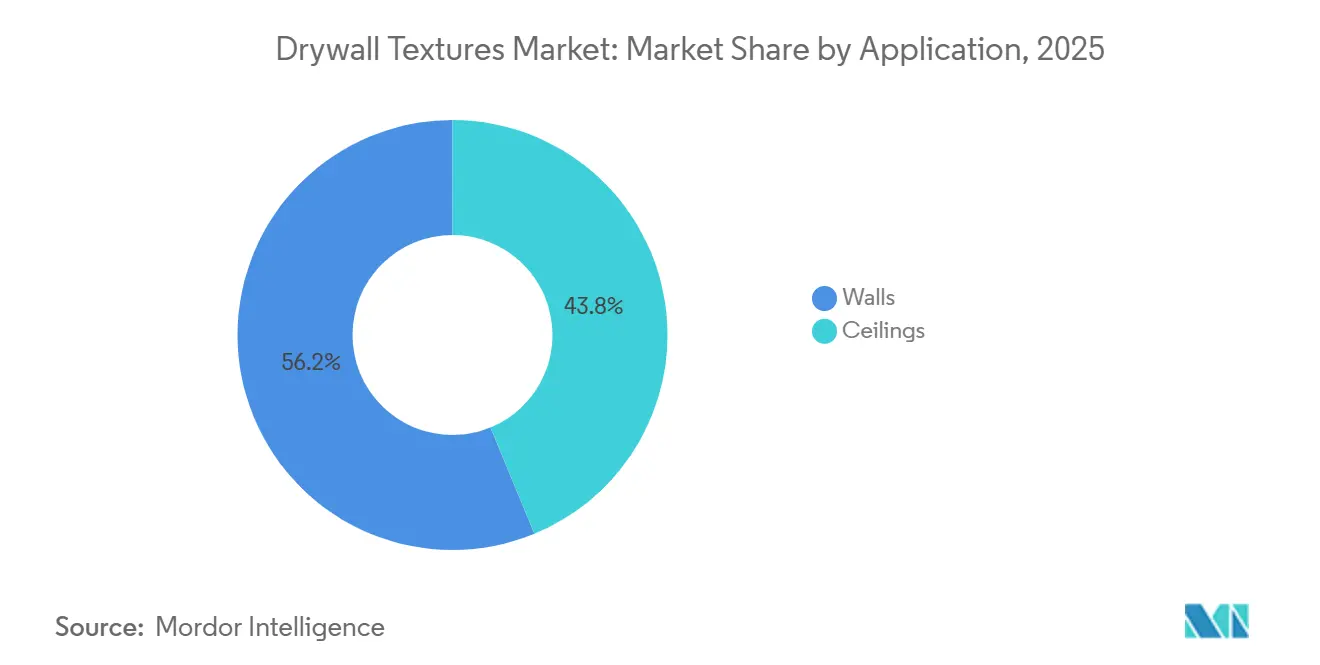

- By application, walls accounted for 56.22% share of the drywall textures market size in 2025; ceilings are advancing at a 5.76% CAGR from 2026 to 2031.

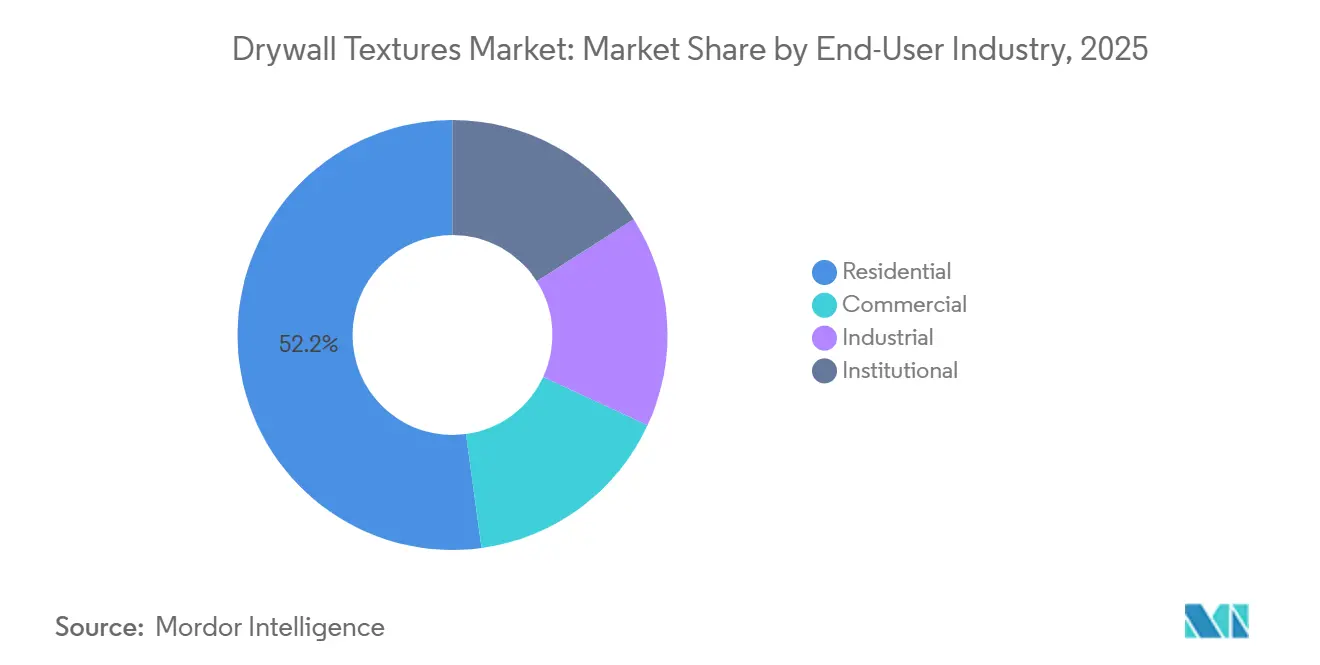

- By end-user industry, residential led with 52.15% drywall textures market share in 2025, while commercial record the highest 5.88% CAGR from 2026 to 2031.

- By geography, North America commanded 33.26% share of the drywall textures market size in 2025; Asia-Pacific is forecast to grow the fastest at 5.63% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Drywall Textures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for aesthetic and decorative finishes | +1.4% | Global (premium uptake in North America & Europe) | Medium term (2-4 years) |

| Increasing renovation and remodeling activities | +1.6% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| ESG-driven shift to low-VOC texture compounds | +0.9% | North America & EU, voluntary APAC | Long term (≥ 4 years) |

| Adoption of automated/robotic spray application systems | +0.7% | North America, Western Europe, Japan | Medium term (2-4 years) |

| AR/VR visualization tools accelerating premium upgrades | +0.5% | North America, select EU & APAC metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Aesthetic and Decorative Finishes

In 2026, industry surveys revealed that social-media imagery emphasizing tactile depth is guiding both homeowners and designers towards dimensional wall treatments. While material costs see a modest uptick of 8–12%, premium textures command a price mark-up of 15–25%, thereby expanding installer margins. Although knockdown and orange-peel finishes dominate in volume, bespoke slap-brush and comb patterns are carving out a niche in custom builds with more relaxed schedules. These finishes not only conceal minor substrate imperfections but also diminish the need for expensive surface preparation, making them appealing for both new constructions and renovations.

Increasing Renovation and Remodeling Activities

While high interest rates are curbing new construction starts, they are simultaneously encouraging upgrades to both existing homes and older office buildings. In early 2026, spending on U.S. residential remodeling increased by 12.5% compared to the previous year. Office landlords are reimagining traditional office layouts, opting for flexible designs that use acoustic ceiling textures to delineate spaces without the need for partitions. As demand for specialty primers, known for their superior adhesion, grows, suppliers offering integrated systems are seeing a preference over those with just single-SKU products. Countries like Germany and Japan, known for their focus on renovations, are also prioritizing low-dust compounds, which significantly reduce re-occupancy times.

ESG-Driven Shift to Low-VOC Texture Compounds

Schools, hospitals, and LEED-targeted assets now consider GREENGUARD and similar ecolabels as essential credentials rather than optional additions[1]UL Solutions, “GREENGUARD Certification Program,” ul.com. In response, manufacturers are re-engineering binders, introducing waterborne resins, and eliminating formaldehyde donors to comply with sub-50 g/L VOC caps. While low-VOC products come at a 5 to 8% premium, they offer access to green-building incentives and reduce litigation risks associated with indoor-air complaints. Adoption, initially prominent in California and the EU, is now extending to multinational projects in India and Vietnam, driven by global developers enforcing consistent procurement standards.

Adoption of Automated/Robotic Spray Application Systems

Contractors, facing a persistent trade-skills gap and median drywall installer wages at USD 38.76 per hour, are now experimenting with robots capable of autonomously achieving Level 4 and Level 5 finishes. Canvas's 1200CX unit not only cuts labor hours by up to 40% but also reduces compound waste by 10 to 15% through its adaptive spray patterns. With payback periods of 12 to 18 months on mid-size commercial jobs, leasing models are emerging as a strategy to reduce capital outlay risk. While early adopters are primarily in North America and Western Europe, pilot projects in Japan indicate a wider adoption, especially as aging workforces tighten the labor supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-applicator shortage in emerging economies | −0.8% | India, ASEAN, Middle East, Latin America | Short term (≤ 2 years) |

| Stricter respirable-silica enforcement delays projects | −0.6% | North America, EU | Medium term (2-4 years) |

| Gypsum-compound tariffs raising material cost volatility | −0.4% | United States, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled-Applicator Shortage in Emerging Economies

In India and Southeast Asia, rapid urbanization is pushing wages for texture specialists up by 40–50% compared to general labor[2]Ministry of Statistics and Programme Implementation, “Annual Construction Survey 2026,” mospi.gov.in. This surge is compelling developers to either simplify their specifications or turn to imported crews. While demand for skilled labor rises, vocational programs struggle to keep pace, and the trade's low prestige further deters youth from entering. As long as automated sprayers remain uneconomical for emerging-market wage levels, the bottleneck in applicators will limit the penetration of premium finishes in these rapidly growing regions.

Stricter Respirable-Silica Enforcement Delays Projects

In 2025, a Georgia contractor faced fines surpassing USD 116,000 due to violations as OSHA tightened its caps on crystalline silica exposure. Meanwhile, California's STOP Act, effective January 1, 2026, prohibited the dry cutting of gypsum. This mandate forced a transition to wet-cutting, increasing project costs by USD 5,000–15,000 and extending schedules by 5–10%. The compliance overhead hits smaller outfits the hardest, reducing competitive intensity and possibly driving up bid prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Texture Type: Knockdown Retains Premium Appeal

In 2025, knockdown finishes commanded a 35.23% share of the drywall textures market and are projected to maintain a 5.35% CAGR through 2031. This technique, known for masking minor board imperfections while offering an upscale look, has become the preferred choice for single-family renovations and boutique hospitality upgrades. Meanwhile, the orange-peel texture serves as a reliable option for multifamily units and commercial interiors, prioritizing speed over artistic flair. Although niche slap-brush and comb patterns occupy a small segment of the market, they are gaining traction in custom homes, where clients value craftsmanship often overlooked in standard developments. To cater to this emerging micro-segment, manufacturers are introducing aerosol formats, such as Homax’s Pro Grade, which debuted in 2025.

Future growth is closely tied to design trends propelled by social media and the presence of skilled applicators adept at artisanal techniques. Once popular, popcorn ceilings are now fading from favor, primarily due to their association with outdated aesthetics and asbestos concerns. In a strategic pivot, suppliers are now offering scrape-off kits. These kits, which combine removal tools with low-dust resurfacers, present an opportunity to transform legacy popcorn ceilings, thereby expanding the drywall textures market.

By Material: Dry-Mix Powders Lead on Logistics Economics

In 2025, dry-mix powders held a 43.78% share of the market, and projections indicate their drywall textures market size will expand at a CAGR of 5.71% through 2031. The lighter freight weight and extended shelf life of these powders provide distributors a hedge against tariff risks and offer contractors flexibility amidst unpredictable job schedules. In labor-scarce metropolitan areas, where hourly wages exceed USD 40, pre-mixed buckets are gaining traction, effectively reducing the cost penalty associated with convenience. Suppliers are increasingly introducing additive-rich formulations, such as antimicrobial, moisture-resistant, and acoustically tuned options, as a strategy to enhance margins through differentiated SKUs.

Georgia-Pacific has invested USD 325 million in its Sweetwater plant, strategically positioning gypsum board and texture compound lines in tandem. This move facilitates bundled tenders, fostering buyer loyalty. Meanwhile, CertainTeed’s M2TECH board, when combined with its proprietary compounds, underscores the advantages of vertical integration. While dry-mix powders are expected to maintain their dominance, pre-mixed options are on track to achieve parity in high-wage markets before 2030. This shift is further bolstered by the increasing prevalence of robotic sprayers calibrated for factory-controlled viscosity.

By Application: Ceilings Outpace Walls in Commercial Retrofits

In 2025, walls dominated the revenue landscape, claiming 56.22%. However, ceiling treatments are on an upswing, with a 5.76% CAGR. This growth is primarily driven by the acoustic dampening needs of open-plan offices and educational institutions. Armstrong’s Tectum DesignArt panels, with an NRC rating of 0.85, can be installed 2.5 times faster than traditional troweled plasters, making them an appealing option for contractors. Meanwhile, the drywall textures market for ceilings is seeing a boost from healthcare retrofits. Here, panels like Ecophon Hygiene Advance, which are both washable and noise-absorbing, align with infection-control protocols.

In egress pathways, regulatory fire ratings are leaning towards spray-applied Class A textures. This niche has caught the eye of additive manufacturers. On the other hand, walls continue to be the preferred choice for residential projects, driving significant volume in North America's remodeling surge. As energy codes tighten, promoting continuous insulation layers, there is growing interest in textured exterior sheathing. This frontier opportunity, however, is still in its pilot stages.

By End-User Industry: Commercial Segment Picks Up Speed

In 2025, residential use held a 52.15% market share, but commercial demand is projected to surge at a 5.88% CAGR. This uptick is driven by landlords modernizing lobbies, corridors, and coworking spaces. The drywall textures market is set to grow in offices, as hybrid workstations prioritize sound control without the need for full partitions. Hospitality chains, refreshing their branding every 5 to 7 years, are now turning to artisan wall textures for differentiation. In contrast, institutional procurement remains price-sensitive, leading to extended bid review periods and a tempered interest in premium compounds.

JSW Paints’ USD 1.08 billion acquisition of Akzo Nobel India highlights the competitive race to dominate commercial-project pipelines in South Asia. Commercial clients are adopting robotic finishing and AR visualization, widening the technology gap with residential installers who predominantly rely on manual skills. Meanwhile, industrial facilities are cautious users, reserving textures for office pods within warehouses.

Geography Analysis

In 2025, North America accounted for 33.26% of the revenue, but projections indicate a decline to a 4.8% CAGR as the market for single-family homes approaches saturation. The drywall textures market in North America grapples with high labor costs and stringent OSHA silica enforcement, while also being at the forefront of automation adoption. With California's dry-cut ban set to take effect in 2026 and GREENGUARD emerging as the standard specification for schools, compliance challenges are increasing. Additionally, tariff-induced spikes in gypsum prices have led distributors to stockpile domestic dry-mix powders, creating a temporary disparity between board and compound costs.

Asia-Pacific is witnessing the fastest growth globally, expanding at a 5.63% CAGR. China's consumption of gypsum boards is projected to reach 12.2 billion square meters by 2027, bolstering the demand for wall textures in urban apartments. In India, rising wage inflation for texture applicators, alongside an INR 200 crore capacity expansion by Nippon Paint, underscores a growing preference for premium finishes. Meanwhile, in the ASEAN region, growth is supported by manufacturing relocations. While Vietnam and Indonesia are leaning towards the quicker orange-peel texture, Jakarta's upscale premium condos are experimenting with knockdown suites.

In Europe, stringent VOC caps and EPD mandates are driving investments in waterborne compounds and ISO 14001-certified plants. While Nordic countries are pushing for ceiling-texture innovations in open-plan offices, Southern Europe is focusing on refurbishing its hospitality sector. Even if there's a dip in new-build permits, energy retrofits mandated by the EU Green Deal are expected to uphold volume.

In South America, Brazil is making strides despite facing currency fluctuations, with a keen focus on decorative ceilings for high-end retail. Meanwhile, in the Middle East, Saudi Arabia's growing hospitality sector is opting for premium wall treatments to distinguish themselves in competitive leisure areas. Jazeera Paints, a local leader, is capitalizing on its five facilities in Saudi Arabia to cater to both domestic and Egyptian projects, leveraging its regional expertise for a competitive edge.

Competitive Landscape

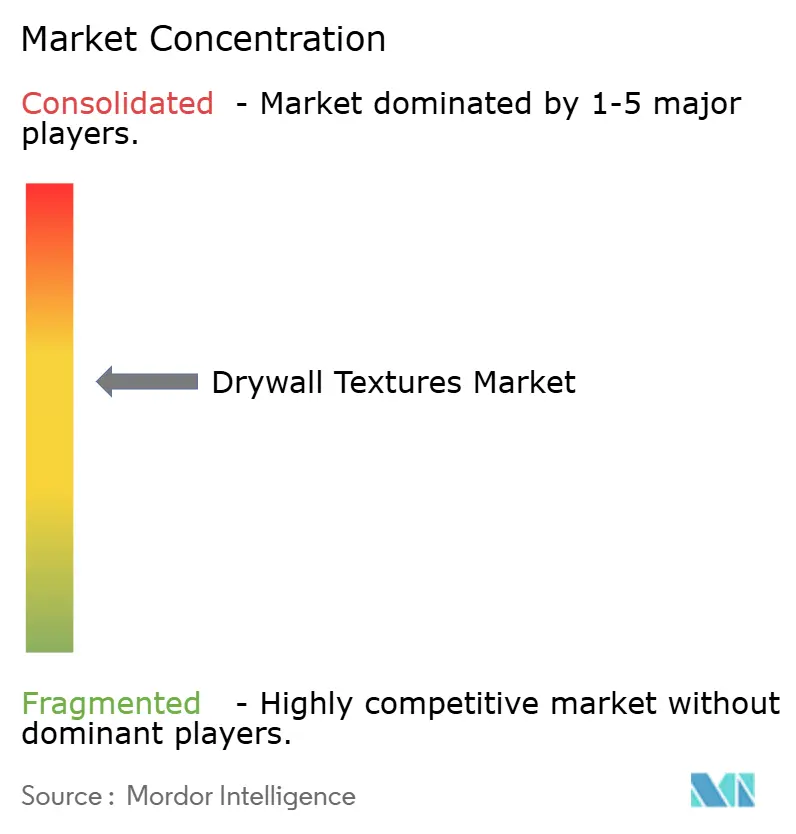

The Drywall Texture market exhibits a moderate level of fragmentation. The market's top five players include The Sherwin-Williams Company, Knauf Group, Georgia-Pacific Gypsum LLC, PPG Industries, Inc., and RPM International Inc. Capacity expansion serves as a significant barrier to entry: Georgia-Pacific’s Sweetwater plant boasts an annual output exceeding 1 billion square feet, and with CertainTeed’s Palatka facility set to double its capacity by October 2025, it will become the largest gypsum facility globally. Such capital-intensive operations create a challenge for smaller entrants to achieve similar economies of scale.

Companies are increasingly focusing on automation, sustainability, and vertical integration. In 2025, RPM restructured into three distinct business units, enabling cross-selling of sealants, waterproofing solutions, and finishes. This strategic move resulted in a 6.5% year-over-year sales boost for their Construction Products Group, reaching USD 881.4 million. Meanwhile, firms like Canvas and WallViewAR are pioneering digital innovations, offering robotic application and AR visualization. These technologies are either licensed or partnered with by established players to hasten their adoption. Smaller companies are carving out niches with specialized products, such as antimicrobial or high-humidity SKUs, targeting hospitals and coastal residences. Certifications from Green Seal and GREENGUARD have become essential for public projects, compelling slower-moving companies to either invest in costly reformulations or exit the market.

Regional specialists are fortifying their positions through deep distributor relationships and comprehensive service offerings. In India, the collaboration between JSW Paints and Akzo Nobel underscores the potential of scaling local reach through acquisitions, as opposed to establishing new greenfield plants. In Latin America, players are honing in on price leadership and introducing lighter-weight bag formats, catering to the needs of fragmented job sites. Looking ahead, the drywall textures industry is expected to consolidate modestly through 2028, driven by mounting regulatory challenges and the capital-intensive nature of automation, which favors larger players.

Drywall Textures Industry Leaders

The Sherwin-Williams Company

Knauf Group

Georgia-Pacific Gypsum LLC

RPM International Inc

PPG Industries, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: California’s STOP Act banning dry gypsum cutting took effect, adding USD 5,000–15,000 per project in compliance costs and lengthening schedules 5–10%.

- October 2025: CertainTeed completed a capacity-doubling expansion at its Palatka, Florida gypsum plant, creating 110 jobs and positioning the facility as the world’s largest.

Global Drywall Textures Market Report Scope

Drywall texture is a decorative, raised finish applied to walls and ceilings using joint compound to hide imperfections, enhance aesthetic appeal, and add depth to a space. It is applied via sprayer or hand-tools, creating patterns like orange peel, knockdown, or swirl that also help conceal taping seams and flaws.

The market is segmented by texture type, material, application, and end-user industry. By texture type, the market is segmented into knockdown, orange peel, sand swirl, popcorn, and other texture types (including skip trowel and slap brush). By material, the market is segmented into dry-mix powders, pre-mixed compounds, and additives and binders. By application, the market is segmented into walls and ceilings. By end-user industry, the market is segmented into residential, commercial, industrial, and institutional. The report also covers the market size and forecasts for Drywall Textures in 17 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| Knockdown |

| Orange Peel |

| Sand Swirl |

| Popcorn |

| Other Texture Types (Skip Trowel, Slap Brush, etc.) |

| Dry-mix Powders |

| Pre-mixed Compounds |

| Additives and Binders |

| Walls |

| Ceilings |

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middl-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Texture Type | Knockdown | |

| Orange Peel | ||

| Sand Swirl | ||

| Popcorn | ||

| Other Texture Types (Skip Trowel, Slap Brush, etc.) | ||

| By Material | Dry-mix Powders | |

| Pre-mixed Compounds | ||

| Additives and Binders | ||

| By Application | Walls | |

| Ceilings | ||

| By End-User Industry | Residential | |

| Commercial | ||

| Industrial | ||

| Institutional | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middl-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the drywall textures market be in 2031?

It is projected to reach USD 5.10 billion by 2031, reflecting a 5.12% CAGR from 2026.

Which texture type is growing fastest?

Knockdown leads both in share (35.23% in 2025) and in appeal, expanding 5.35% CAGR on demand for premium yet forgiving finishes.

Why are dry-mix powders favored over pre-mixed compounds?

Lower freight weight and multiyear shelf life keep distributor costs down, securing 43.78% share in 2025 and a 5.71% CAGR outlook.

What is driving ceiling-texture adoption in offices?

Open-plan designs require acoustic control; products like Armstrong Tectum DesignArt achieve NRC 0.85 and install 2.5× faster than troweled plasters.

Page last updated on: