Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

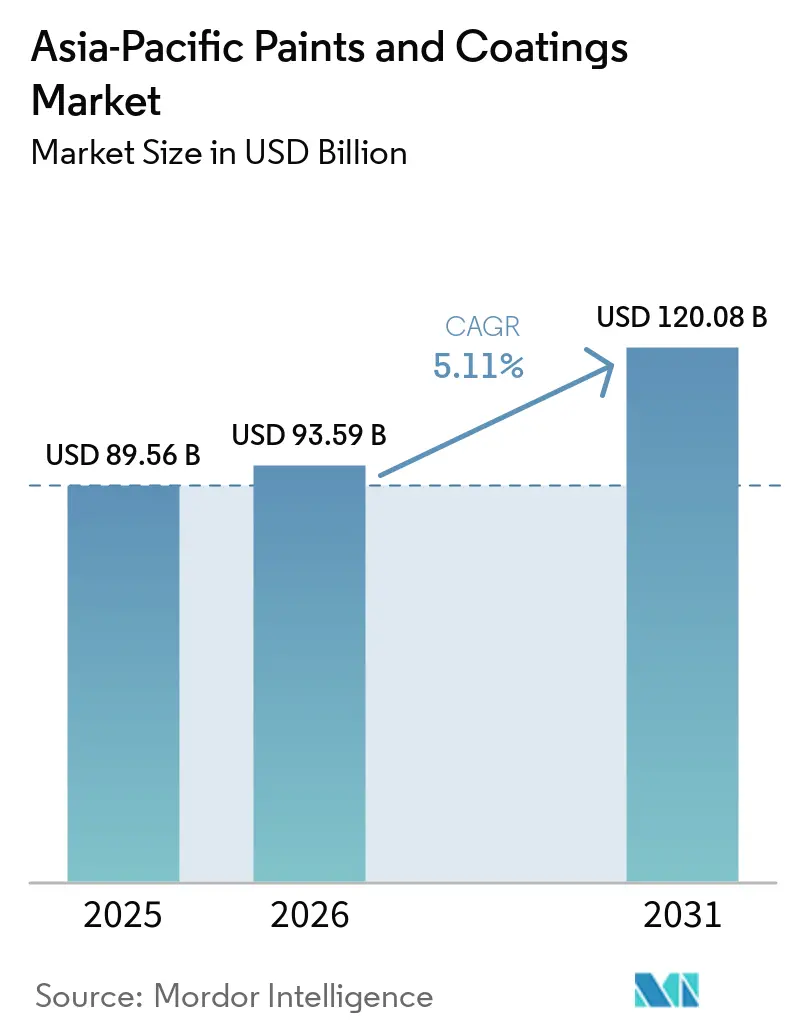

| Base Year Market Size (2025) | USD 89.56 Billion |

| Market Size (2026) | USD 93.59 Billion |

| Market Size (2031) | USD 120.08 Billion |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

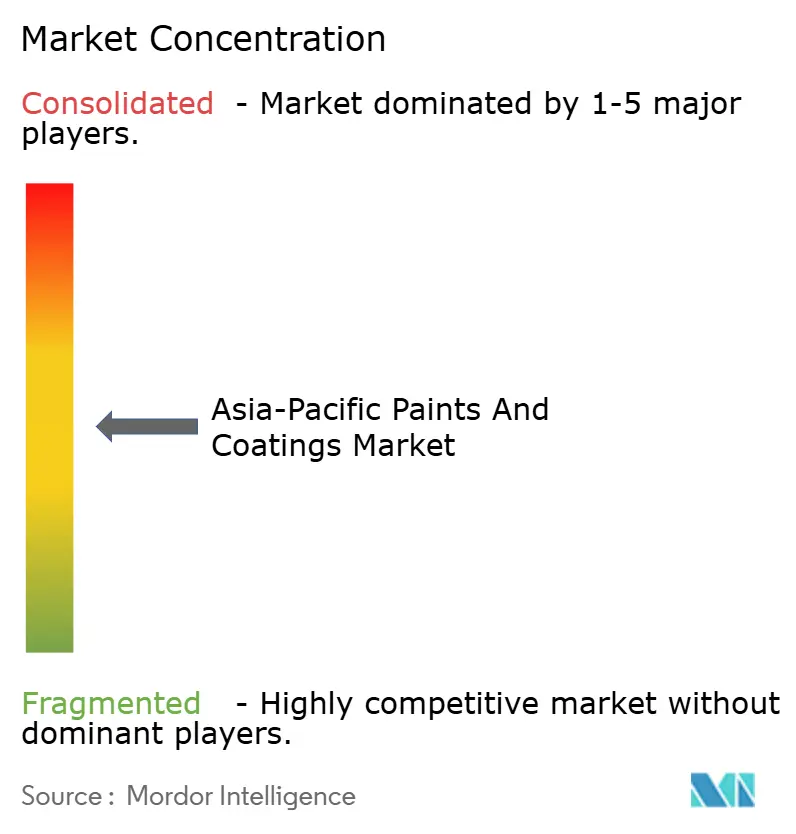

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Paints And Coatings Market Analysis by Mordor Intelligence

The Asia-Pacific Paints And Coatings Market size is expected to grow from USD 89.56 billion in 2025 to USD 93.59 billion in 2026 and is forecast to reach USD 120.08 billion by 2031 at 5.11% CAGR over 2026-2031. Transition toward water-borne chemistries, rapid infrastructure programs in India, and manufacturing expansion in Southeast Asia are sustaining demand even as China’s housing construction cools. Regional OEMs are localizing resins and pigments to buffer titanium-dioxide price swings, and applicators are adopting low-VOC systems to comply with tighter emission rules. Digital color-match kiosks are shortening repaint purchase cycles, while cool-roof mandates in India underpin premium exterior coatings growth. Competitive focus is shifting to logistics agility and backward integration as raw-material volatility compresses margins.

Key Report Takeaways

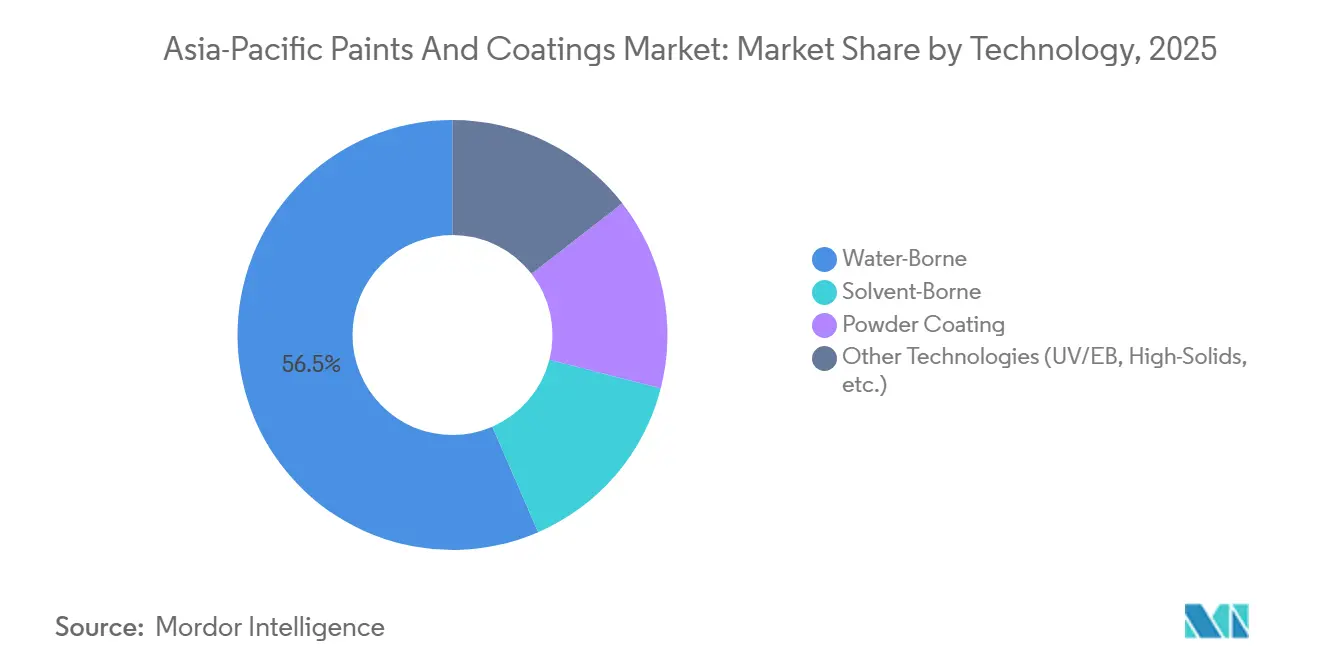

- By technology, water-borne coatings captured 56.52% revenue share in 2025 and are projected to expand at a 5.67% CAGR during the forecast period (2026-2031).

- By resin type, acrylic formulations commanded a 35.33% share in 2025 while advancing at a 5.23% CAGR during the forecast period (2026-2031).

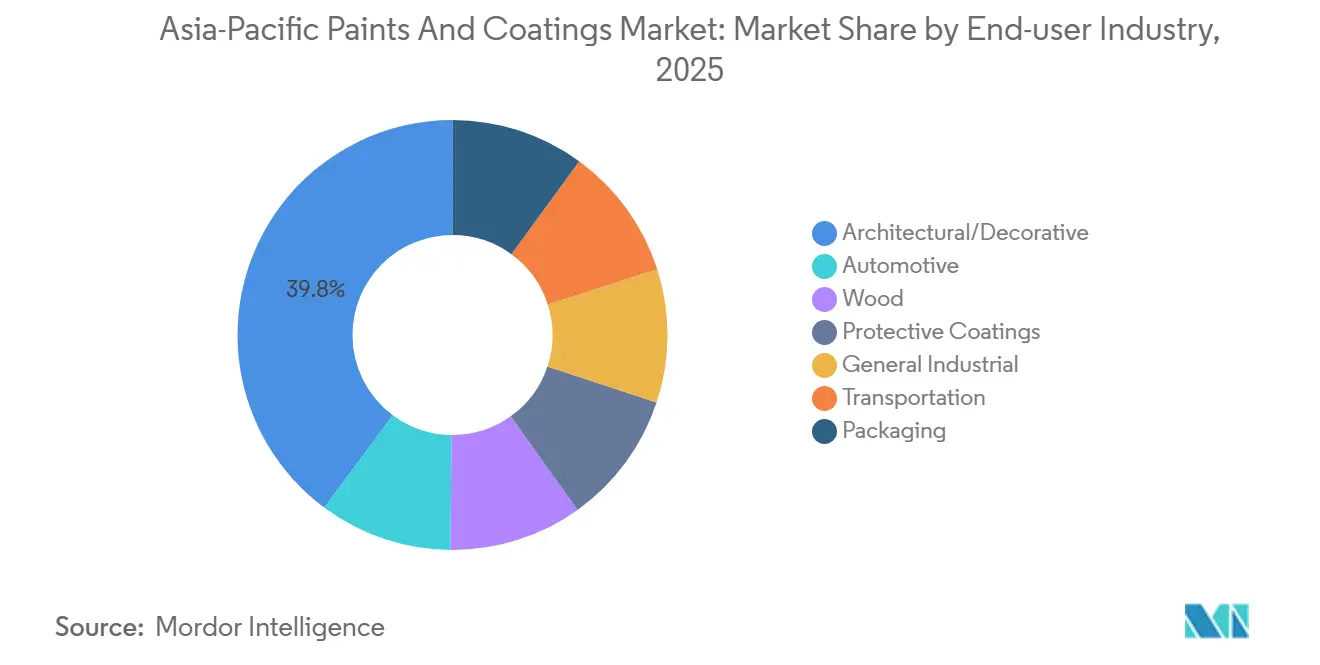

- By end-user industry, the architectural and decorative segment accounted for a 39.82% share in 2025 and is expected to grow at a 5.34% CAGR during the forecast period (2026-2031).

- By geography, China led with a 55.98% share in 2025, while India is poised for the fastest CAGR at 5.41% during the forecast window (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Re-painting cycle compression | +0.8% | China Tier-1 cities | Medium term (2-4 years) |

| OEM shift to water-borne topcoats | +1.2% | Thailand, South Korea, Japan, India | Short term (≤2 years) |

| Cool-roof mandates in India | +0.9% | India metropolitan clusters | Medium term (2-4 years) |

| AI in-store color matching | +0.6% | China, India, Thailand, Philippines | Short term (≤2 years) |

| Belt-and-Road re-coating | +0.7% | China, Indonesia, Malaysia, Thailand, Pakistan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Re-Painting Cycle Compression in Tier-1 Chinese Housing

Housing starts in China’s largest cities fell 20.5% in 2025, yet resale transactions climbed 12%, prompting owners to repaint sooner, reducing the cycle from 7-8 to 5-6 years. Water-borne emulsions now cover 68% of urban repaint jobs, up from 54% in 2023, favored for low-VOC compliance. Distributors benefit from 8-10% higher per-liter margins on premium formulations and faster inventory turnover. Regional producer 3TREES offers next-day delivery and free color advice to defend share against Nippon Paint and Dulux, whose traditional outlets lack the same last-mile reach.

OEM Shift to Water-Borne Auto Topcoats

Thailand, South Korea, and Japan cap automotive paint VOCs at 200-250 g/L. PPG’s Samut Prakan plant, opened in March 2025, supplies 2,000 t/y of water-borne refinish that cuts bake-oven energy 35%[1]PPG Industries, “PPG Opens New Automotive Refinish Plant in Thailand,” ppg.com. Kansai Paint and Toyoda Gosei introduced an in-mold water-borne process in 2025 that trims per-vehicle coating costs by 18%. Electric-vehicle lines favor the lighter 80-100 μm film build of water-borne systems, saving 2-3 kg and extending driving range by up to 0.8%.

Mandated Cool-Roof Coatings in India’s Smart-City Program

India’s Eco Niwas Samhita code now requires solar reflectance ≥0.70; Telangana targets 300 km² of compliant roofs by 2028 and offers a 10% property-tax rebate[2]Government of Telangana, “Cool Roof Policy 2025-2028,” telangana.gov.in. A magnesium-oxide-doped PVDF coating from JNCASR cut roof temperatures by 12-15°C in pilot sites during 2025. Asian Paints and Berger Paints launched elastomeric cool-roof lines that qualify for green-materials incentives, selling 25-30% above standard exterior emulsions.

AI-Driven In-Store Color-Match Kiosks Accelerating DIY Repaints

Asian Paints deployed 1,200 Chromacosm kiosks that tint paint in 90 seconds from smartphone photos, boosting average basket value 18% in pilot stores. Nippon Paint’s “Nong Nippon” chatbot handled 18,000 queries monthly in 2025, routing same-day orders to local franchises. KCC’s AR visualization in South Korea cut color-mismatch returns 34%. These tools compress purchase decisions from weeks to days and carry 12-15% higher margins than pre-mixed SKUs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Titanium-dioxide price volatility | -0.9% | Japan, South Korea, Australia | Short term (≤2 years) |

| Certification gap in ASEAN coaters | -0.5% | Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Escalating PFAS restrictions | -0.4% | Japan, South Korea, Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Titanium-Dioxide Price Volatility

Spot TiO₂ climbed to USD 2,700 t in Japan in June 2025, 29% above China, amid ilmenite shortages and higher freight costs. Gross margins on decorative paints fell 200-300 bps for import-dependent makers. Asian Paints and Nippon Paint are moving upstream into rutile beneficiation, while formulators raise calcium-carbonate loadings and use hollow-sphere opacifiers to cut TiO₂ by up to 20%.

Certification Gap of Industrial Coaters in Indonesia and Vietnam

Under 40% of applicators in Indonesia and Vietnam meet ISO 12944 standards, slowing the uptake of high-performance epoxy systems. Vietnam’s QCVN 19:2024 sets 50 mg/m³ VOC limits but lacks inspection capacity. Suppliers such as Jotun and Hempel bundle on-site training to bridge the skills shortfall until ASEAN’s 2024 mutual-recognition pact is fully implemented after 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Systems Lead Regulatory Compliance

Water-borne systems represented 56.52% revenue in 2025 and are forecast to grow 5.67% annually during the forecast period (2026-2031), eclipsing solvent-borne coatings. This outperformance mirrors stricter VOC rules across Thailand, South Korea, and Vietnam. Powder coatings advance as cure temperatures fall to 150-160°C. BASF’s DURA-COLOR acrylic eliminated primers and cut costs 18-22% across multi-country trials. Covestro’s 2025 expansion in Shanghai integrated bio-based polyols to meet China’s 40% renewable-content threshold.

Powder and UV platforms benefit electronics and furniture exporters needing zero-VOC credentials. Allnex’s waterborne-UV hybrids shorten cure times and satisfy US and EU import standards. Together, these shifts keep the Asia-Pacific paints and coatings market on a low-emission track.

By Resin Type: Acrylic Versatility Drives Cross-Segment Adoption

Acrylics captured 35.33% revenue in 2025 and will climb at a 5.23% CAGR during the forecast period (2026-2031), deployed in everything from exterior emulsions to auto basecoats. Alkyds, with bio-based grades meeting China’s renewable mandate growing faster than petroleum versions. Polyurethanes share, lifted by water-borne dispersions for refinish and two-pack systems for protective steelwork. BASF’s Caojing site scaled to 18,800 t/y in 2025, cutting custom resin lead-times to three weeks.

Epoxies remain critical for marine and flooring, while polyester resins support powder lines for appliances and wheels. Niche phenolic and ketonic chemistries serve high-temperature plants but grow modestly as specialty projects emerge in Singapore and South Korea.

By End-User Industry: Architectural Segment Anchors Volume Growth

Architectural and decorative paints delivered 39.82% revenue in 2025 and will increase at a CAGR of 5.34% during the forecast period (2026-2031), buoyed by India’s cool-roof rules and Chinese urban repaints. Automotive coatings will expand as OEMs swap to water-borne lines. Wood coatings demand rises with Vietnam’s USD 6.99 billion furniture exports in Jan-May 2025. Protective coatings grow due to bridge and wind-turbine maintenance, while packaging lines such as AkzoNobel’s BPA-free Accelshield 300 target the EU’s July 2026 ban.

Diversified demand keeps the Asia-Pacific paints and coatings market resilient despite sectoral downturns, reinforcing growth across consumer and industrial uses.

Geography Analysis

China retained 55.98% of 2025 revenue; its Belt-and-Road recoating, export wood finishing, and repaint cycles offset weaker housing starts. India will record the fastest 5.41% CAGR during the forecast period (2026-2031), supported by per-capita paint use one-third of China’s and government preference for BIS-certified low-VOC lines. Japan’s share grows, lifted by marine upgrades and refinish demand, while South Korea’s share rises on shipbuilding activity. Australia and New Zealand together grow through coastal protective projects.

In Southeast Asia, Thailand hosts PPG’s new refinish plant; Vietnam’s furniture exporters drive wood-coating uptake; Indonesia’s green-industry incentives attract new investments despite applicator gaps. Singapore’s marine coatings hub supports efficiency retrofits to meet IMO carbon indices. These dynamics diversify the Asia-Pacific paints and coatings market, reducing reliance on any single economy.

Competitive Landscape

The Asia-Pacific Paints and Coatings Market is moderately fragmented. Digital retail capabilities such as Asian Paints’ Chromacosm and Nippon’s chatbot compress repaint lead times and lift basket sizes. Regional specialists employ mobile tinting vans and QR loyalty programs to undercut national distributors by up to 20%. Patent filings in water-borne and UV-curable chemistries aim to capitalize on tightening PFAS rules. Protective-coating opportunities in offshore wind and LNG fleets invite entrants with ISO 12944 expertise and training academies, reinforcing skill-based moats.

Asia-Pacific Paints And Coatings Industry Leaders

Asian Paints

Kansai Paint Co., Ltd.

Nippon Paint Holdings Co., Ltd

PPG Industries, Inc.

Akzo Nobel N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Birla Opus Paints, a subsidiary of Aditya Birla Group’s Grasim Industries, launched its new Aerosol paint range, One Aero, promising 15-minute fast-dry technology. The product is designed for both professionals and DIY (Do-It-Yourself) users.

- June 2025: Akzo Nobel N.V. announced plans to sell AkzoNobel India to JSW Group, marking a significant strategic realignment in the Indian market.

- December 2024: AkzoNobel Marine and Protective Coatings signed a cooperation memorandum with Sinopec to supply high-performance anti-corrosive and fireproof systems to supply global expansion.

Asia-Pacific Paints And Coatings Market Report Scope

Paints or coatings are multiphase colloidal systems applied on the desired surface, primarily for aesthetics and protection. They are a mixture of pigments, binders, liquids, and additives, which can easily be applied on surfaces using a spray or brush. Each ingredient plays a crucial role in defining the properties and performance of paints during or after application. Paints and coatings find major applications in the architectural industry, such as decorative and protective coatings.

The Asia-Pacific paints and coatings market is segmented by technology, resin type, end-user industry, and geography. By technology, the market is segmented into water-borne, solvent-borne, powder, and other technologies (UV/EB, high-solids, etc.). By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types (phenolic, ketonic, and others). By end-user industry, the market is segmented into architectural/decorative, automotive, wood, protective, general industrial, transportation, packaging, and other end-user industries (plastic coatings, agriculture, construction and Earthmoving equipment, and others). The report also covers the market sizes and forecasts for the paints and coatings market in 11 countries across the Asia-Pacific. The report offers the market size in value terms (USD) for all the abovementioned segments.

By Technology

| Water-Borne |

| Solvent-Borne |

| Powder Coating |

| Other Technologies (UV/ EB, High-Solids, etc.) |

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Others (Phenolic, Ketonic, etc.) |

By End-user Industry

| Architectural/ Decorative |

| Automotive |

| Wood |

| Protective Coatings |

| General Industrial |

| Transportation |

| Packaging |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| Indonesia |

| Thailand |

| Malaysia |

| Vietnam |

| Philippines |

| Singapore |

| Rest of Asia-Pacific |

| By Technology | Water-Borne |

| Solvent-Borne | |

| Powder Coating | |

| Other Technologies (UV/ EB, High-Solids, etc.) | |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Others (Phenolic, Ketonic, etc.) | |

| By End-user Industry | Architectural/ Decorative |

| Automotive | |

| Wood | |

| Protective Coatings | |

| General Industrial | |

| Transportation | |

| Packaging | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Philippines | |

| Singapore | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How big will Asia-Pacific paints and coatings demand be by 2031?

The Asia-Pacific Paints And Coatings Market size is expected to grow from USD 89.56 billion in 2025 to USD 93.59 billion in 2026 and is forecast to reach USD 120.08 billion by 2031 at 5.11% CAGR over 2026-2031.

Which segment grows fastest within regional coatings demand?

Water-borne systems lead with a 5.67% CAGR through 2031, propelled by tightening VOC limits and OEM transitions.

Why is India emerging as the key growth engine?

India benefits from cool-roof mandates, low per-capita paint use, and government preference for BIS-certified low-VOC products, driving a 5.41% CAGR.

How are companies countering titanium-dioxide volatility?

Leading producers integrate upstream into rutile processing and reformulate with extenders and hollow-sphere pigments to lower TiO₂ loads.

What technologies help shorten repaint purchase cycles?

AI color-match kiosks, chatbots, and augmented-reality tools compress decision times from weeks to days and raise store margins.

Page last updated on: