Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 39.68 Billion |

| Market Size (2026) | USD 40.53 Billion |

| Market Size (2031) | USD 45.08 Billion |

| Growth Rate (2026 - 2031) | 2.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Paints And Coatings Market Analysis by Mordor Intelligence

The Europe Paints and Coatings Market size is projected to be USD 39.68 billion in 2025, USD 40.53 billion in 2026, and reach USD 45.08 billion by 2031, growing at a CAGR of 2.15% from 2026 to 2031. While headline growth may seem subdued, it belies a pronounced shift in demand. The spotlight now shines on low-volatile-organic-compound (VOC) chemistries, energy-transition-related infrastructure, and formulation innovations that enhance on-site productivity. EU regulatory deadlines have been instrumental in this transformation. Notably, Directive 2004/42/EC's Phase II VOC ceilings and the recent February 2026 update to the EU Ecolabel are redirecting demand from conventional solvent-borne systems and cobalt driers. At the same time, the EU's Renovation Wave is unlocking significant funding, amplifying architectural volumes. This uptick is further buoyed by expansions in offshore wind, a drive towards automotive electrification, and marine retrofits - all heightening the demand for protective coatings. As multinationals adapt - scaling back on legacy solvent capacity, rolling out water-borne and powder lines, and chasing strategic bolt-on acquisitions for technology or geographic reach - the competitive landscape has intensified. Although fluctuations in input costs and a dearth of skilled applicators have challenged immediate throughput, formulators who harness innovations like fast-cure systems and digital color-matching tools are enjoying wider margins.

Key Report Takeaways

- By technology, water-borne systems led with 66.31% of Europe paints and coatings market share in 2025 and are advancing at a 3.67% CAGR to 2031.

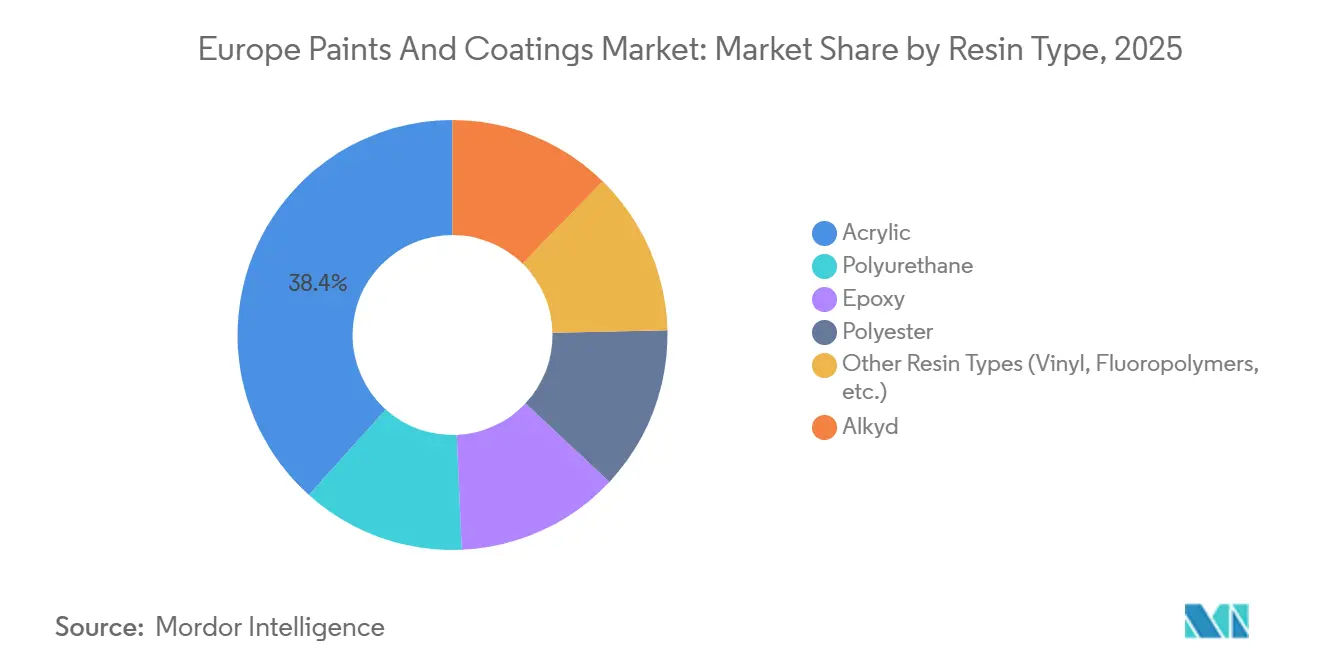

- By resin, acrylics held 38.36% of Europe paints and coatings market size in 2025, expanding at a 3.58% CAGR through 2031.

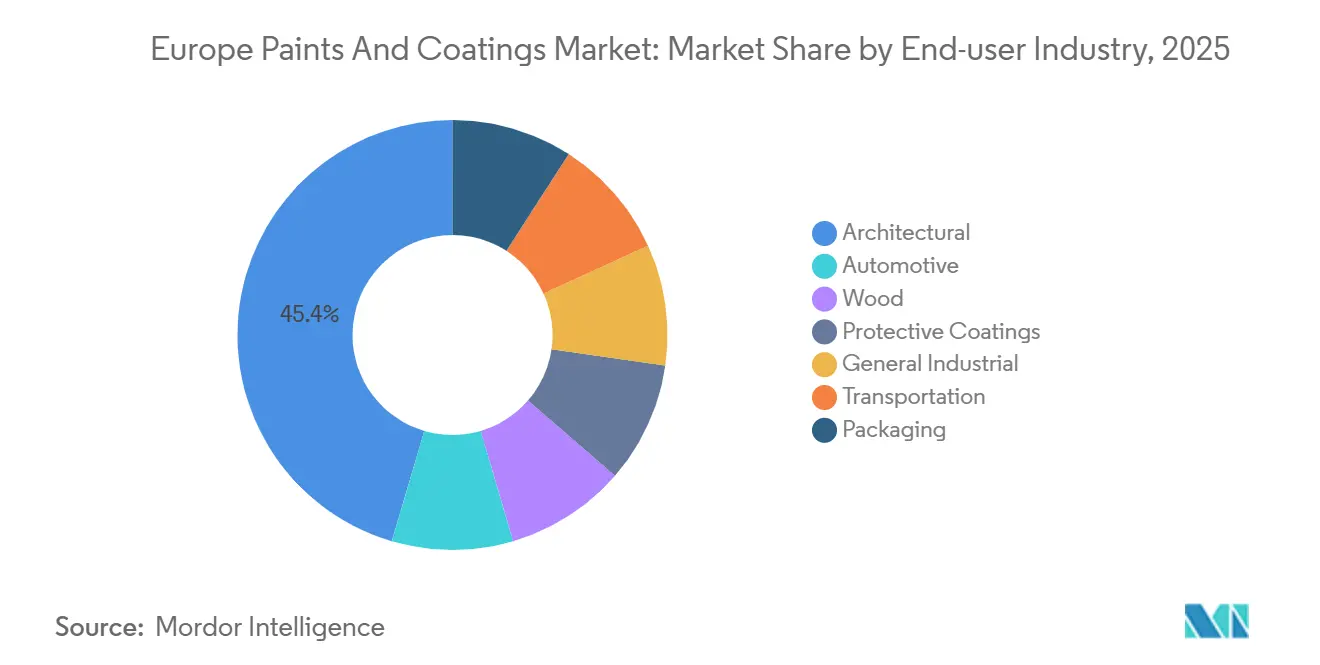

- By end-user, architectural applications accounted for 45.44% of demand in 2025 and are growing at a 3.59% CAGR to 2031.

- By geography, the Rest of Europe captured 24.67% of revenue in 2025 and is projected to expand at the fastest 3.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating wind-turbine installations | +0.40% | Germany, Spain, Denmark, Poland, North Sea offshore zones | Medium term (2-4 years) |

| Growing demand from new electric vehicles | +0.30% | Germany, France, Spain, Czech Republic, Slovakia | Short term (≤ 2 years) |

| Aerospace and marine retrofit demand | +0.20% | France, Germany, Netherlands, Italy, UK | Long term (≥ 4 years) |

| EU building-renovation wave incentives | +0.50% | Germany, France, Italy, Spain, Poland, Netherlands | Medium term (2-4 years) |

| Antimicrobial interior coatings adoption | +0.10% | Western Europe core markets, expanding to Central and Eastern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Wind-Turbine Installations

By the end of 2024, the EU's wind capacity experienced a notable boost, driven by new installations during the year. Each offshore turbine's tower, nacelle, and blades are heavily coated with epoxy and polyurethane. The introduction of larger 15 MW units has significantly increased the demand for these coatings on a per-turbine basis. Germany and Spain led the additions in 2024, while Poland, utilizing Cohesion-Fund programs, expedited its permitting processes. Suppliers introduced fast-cure epoxy hybrids, which reduced tower coating times and improved resistance to high-salinity exposure. Hempel’s marine division, supported by an offshore-wind backlog, reported organic growth. With the EU targeting ambitious wind capacity goals for 2030, the momentum for the European paints and coatings market remains strong.

Growing Demand from New Electric Vehicles

In 2025, Europe assembled over 2.5 million battery-electric vehicles (BEVs), with 70% of production concentrated in Germany, France, and Spain[1]European Automobile Manufacturers Association, “Automobile Production 2025,” acea.auto . While BEVs require less exterior paint, they demand specialized coatings for their battery enclosures and lightweight substrates. Axalta has rolled out its water-borne coating, rated UL 94 V-0 for flame resistance, on three production lines across Europe, specifically designed for battery cases. AkzoNobel's UV-cured powder, utilized for battery components, has achieved a notable reduction in energy consumption. In a forward-looking initiative, Škoda is making a significant investment in a new water-borne paint shop, scheduled to launch in 2029. These industry shifts are driving up the demand for specialty resins, even as the adoption of traditional body colors stabilizes.

Aerospace and Marine Retrofit Demand

In 2024, Europe's aerospace turnover saw a significant contribution from maintenance, repair, and overhaul (MRO) services. As new aircraft deliveries faced delays, airlines opted to extend the lifespans of their airframes, spurring a surge in demand for chromate-free primers and fuel-tank sealants. Meanwhile, in the maritime sector, Dutch and Italian yards experienced a retrofitting boom, largely in response to the IMO's ballast-water and carbon-intensity regulations. In 2025, Jotun and Hempel signed multi-year agreements for hull coatings, projecting fuel savings for operators. With the extended service life of both aircraft and vessels, a consistent demand for retrofitting is expected through 2031, providing a buffer against cyclical downturns in new builds.

EU Building-Renovation Wave Incentives

By 2030, the Renovation Wave aims to double annual building-upgrade rates, mobilizing substantial investments each year. Germany’s “Federal Funding for Efficient Buildings” disbursed considerable funding, while France’s MaPrimeRénov' allocated significant resources. Italy extended owner incentives through its 70 percent Superbonus. In Spain and Italy, architectural volumes are growing faster than new-build activity alone would suggest, bolstering the European paints and coatings market. This is evident as exterior insulation finishing systems now specify acrylic topcoats that achieve U-values below a specific threshold, and photocatalytic facades, which help mitigate heat islands, have gained traction.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC and SVHC regulations | -0.30% | EU-wide, with stricter enforcement in Germany, Netherlands, Nordics | Short term (≤ 2 years) |

| Skilled-applicator labor shortage | -0.20% | Netherlands, Germany, Spain, France, Poland | Medium term (2-4 years) |

| Looming EU PFAS ban on fluoropolymer coatings | -0.10% | Aerospace, chemical processing, food contact applications across EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter VOC and SVHC Regulations

In 2024, Germany's environment agency increased fines for non-compliance, intensifying challenges for smaller firms. These businesses faced compliance costs that tightened their profit margins, indicating a trend toward further consolidation. In 2025, AkzoNobel made strides by upgrading Montataire, notably integrating closed-loop solvent recovery. On the regulatory landscape, Directive 2004/42/EC imposes VOC caps: 30 g/L for interior matt walls and 130 g/L for exterior trim. However, the 2026 EU Ecolabel raises the bar, introducing bans on semi-VOC and cobalt driers.

Looming EU PFAS Ban on Fluoropolymer Coatings

In August 2025, ECHA proposed capping individual PFAS at 25 ppb and limiting fluoropolymers in articles to 50 ppm[2]European Chemicals Agency, “PFAS Restriction Proposal 2025,” echa.europa.eu . The Commission is slated to make a decision in 2027, with the new regulations set to take effect between 2028 and 2029. Aerospace fuel-system linings and food-contact bakeware are particularly vulnerable. While formulators are experimenting with silicone-modified polyesters and ceramic-filled epoxies, they are encountering performance issues at temperatures exceeding 200 degrees Celsius. This uncertainty is holding back investments until the final derogations are clarified.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylics Cement Leadership with Regulatory Advantage

In 2025, acrylic resins constituted 38.36% of the total market value, with projections indicating growth at a 3.58% CAGR during the forecast period of 2026-2031. To address the rising demand for low-VOC products, BASF has increased its production of acrylic emulsions in Germany. Bio-based grades, which incorporate renewable carbon, have secured contracts for public buildings, ensuring compliance with REACH Annex XVII standards. However, alkyds have experienced a decline in market share outside of the price-sensitive regions of Eastern Europe, primarily due to their extended drying times and higher solvent content.

Polyurethane is utilized in niche applications such as automotive clear coats and offshore structures, valued for its abrasion resistance and UV stability. Epoxy resins dominate heavy-duty flooring and chemical tank applications, while polyester resins remain essential for appliance powders. Although vinyl, silicone, and fluoropolymer chemistries collectively represent a smaller segment of the market tonnage, they command high margins due to stringent certification requirements. This resin composition highlights how regulatory changes are driving formulators in Europe's paints and coatings market to increasingly adopt acrylics across various applications.

By Technology: Water-Borne Momentum Reinforced by Ecolabel Criteria

In 2025, water-borne products accounted for 66.31% of sales and are projected to grow at a 3.67% CAGR during the forecast period of 2026-2031. Innovations such as sorbitol-monooleate polyurethane dispersions are achieving zero VOC emissions while retaining flexibility at minus 20 degrees Celsius. Montataire's newly developed reactors are producing acrylics with significantly low VOC levels, underscoring the economic viability of next-generation green chemistries.

Solvent-borne systems remain the preferred choice in aerospace refinishing and heavy industries, where rapid curing and chemical resistance are paramount. Powder coatings, which command a significant market share, are reaping benefits from the surging demand in appliances and metal furniture. Notably, AkzoNobel-IPG's laser curing technology has reduced baking time to five minutes, making it suitable for plastic substrates. Although UV-cured volumes are still modest, they are experiencing the fastest growth in wood flooring and flexible packaging, thanks to their instant curing ability and solvent-free nature.

By End-User Industry: Architectural Demand Anchors Growth While Automotive Shifts to EV

In 2025, architectural coatings led the European paints and coatings market with a 45.44% share and are projected to grow at a 3.59% CAGR during 2026-2031. The EU's Renovation Wave, focusing on facade upgrades and insulation systems, drove this growth. Germany's funding promoted low-VOC acrylic topcoats, while France's MaPrimeRénov’ increased demand for elastomeric wall paints. Italy’s Superbonus incentivized condominium refurbishments, and Spain mandated photocatalytic facades for urban projects. These initiatives boosted architectural coatings, reducing reliance on new-builds and solidifying acrylic dominance.

In 2025, automotive coatings held a significant market share, with BEV production in Germany, France, and Spain driving demand for thinner films and specialty resins. Protective coatings grew due to offshore wind installations and IMO compliance deadlines. Wood coatings thrived on strong furniture exports from Poland and the Czech Republic, supported by UV-cured systems. General industrial, transportation, and packaging sectors leveraged low-VOC chemistries to turn regulatory challenges into opportunities in the Europe paints and coatings market.

Geography Analysis

In 2025, the Rest of Europe accounted for 24.67% of total revenues and is set to grow at a rate of 3.67% through the forecast period of 2026-2031. In 2024, Poland expanded its energy portfolio by adding new onshore wind capacity, making use of epoxy tower-coats. Concurrently, Romania's initiative to enhance building efficiency has led to a surge in the demand for water-borne facades. In the Nordics, stringent environmental regulations necessitate the adoption of low-VOC and bio-based finishes. This shift has led suppliers, such as Teknos, to focus on locally sourced renewable-content emulsions.

Germany is the dominant player in Europe's paints and coatings sector. However, in 2025, construction activities faced headwinds due to tighter financing. In Bavaria and Baden-Württemberg, steady production from automotive OEMs bolstered industrial volumes. Furthermore, federal infrastructure investments cushioned the impact of a softening housing sector. Despite challenges in housing, Scotland's marine and aerospace MRO sectors thrived, buoyed by a busy schedule of protective line work. France, benefiting from subsidies, is actively pursuing nuclear retrofit projects that necessitate radiation-resistant epoxies. Italy's momentum is fueled by ongoing Superbonus projects, while Spain enjoys a dual uplift from a resurgence in residential markets and the expansion of wind farms. While Russia and Turkey navigate outside EU regulations, maintaining a demand for solvent-borne alkyds, both countries face hurdles from currency fluctuations and geopolitical tensions.

Competitive Landscape

The Europe paints and coatings market is moderately consolidated. In a bid to pivot towards green technologies, major players are divesting non-core units. AkzoNobel is making strategic moves with an upgrade in Montataire, complementing its expansion in Como powder. However, the company is also trimming fixed costs by shutting down sites in Wapenveld and Machelen. Meanwhile, BASF has divested its automotive OEM and refinish assets to Carlyle, but with a partial retention, redirecting the capital towards its specialty industrial lines.

In a significant move, AkzoNobel's merger with Axalta, approved by shareholders in January 2026, is set to forge a major powerhouse. The newly formed entity is targeting synergies, primarily through streamlined procurement and collaborative research and development efforts. On the other hand, smaller players like Mankiewicz and Teknos are leveraging water-borne polyurethane patents, securing multiyear supply contracts with OEMs. Arkema, with its ISCC-certified UV-powder range, is strategically positioning itself in the sustainable metal-furniture market. Furthermore, while technical compliance with ISO 12944 and impending PFAS bans benefit established players with advanced test labs, they also present opportunities for disruptors introducing drop-in fluorine-free chemistries.

Europe Paints And Coatings Industry Leaders

Akzo Nobel N.V.

PPG Industries, Inc.

BASF

The Sherwin-Williams Company

Jotun

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CIN has strengthened its European industrial-coatings portfolio through the acquisition of Hempel Industrial B.V. in the Netherlands. This strategic move enhances CIN's presence in the region.

- May 2025: Akzo Nobel plans to close its plants in Wapenveld and Machelen, consolidating production into larger regional hubs. This move aims to streamline operations and improve efficiency.

Europe Paints And Coatings Market Report Scope

Paint is any liquid or liquefiable colored substance that spreads over a surface and dries to leave a thin decorative or protective coating. The coating is a covering applied or deposited onto a substrate to enhance the surface properties for decoration, corrosion, and wear protection. Paints and coatings find major applications in the architectural industry as decorative and protective coatings.

The Europe paints and coatings market is segmented by resin type, technology, end-user industry, and geography. By resin type, the market is segmented into acrylic, alkyl, polyurethane, epoxy, polyester, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, powder coatings, and UV-cured coating. By end user industry, the market is segmented into architectural, automotive, wood, protective coatings, general industrial, transportation, and packaging. The report also covers the market size and forecasts for the paints and coatings in 7 countries across the European region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types (Vinyl, Fluoropolymers, etc.) |

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coatings |

| UV-Cured Coatings |

By End-User Industry

| Architectural |

| Automotive |

| Wood |

| Protective Coatings |

| General Industrial |

| Transportation |

| Packaging |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Turkey |

| Rest of Europe |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types (Vinyl, Fluoropolymers, etc.) | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder Coatings | |

| UV-Cured Coatings | |

| By End-User Industry | Architectural |

| Automotive | |

| Wood | |

| Protective Coatings | |

| General Industrial | |

| Transportation | |

| Packaging | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Turkey | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe paints and coatings market in 2026?

The Europe paints and coatings market size stands at USD 40.53 billion in 2026, and it is projected to reach USD 45.08 billion by 2031 at a 2.15% CAGR.

Which technology dominates European coatings?

Water-borne systems led with 66.31% share in 2025 and continue to outpace other chemistries through 2031.

Which resin type is growing fastest?

Acrylic resins, at 38.36% share in 2025, are advancing at a 3.58% CAGR on the back of bio-based and low-VOC adoption.

Which region inside Europe shows the quickest growth?

Rest of Europe, covering Poland, the Nordics, and Southeastern markets, is forecast to post a 3.67% CAGR to 2031.

Page last updated on: