Paint Protection Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

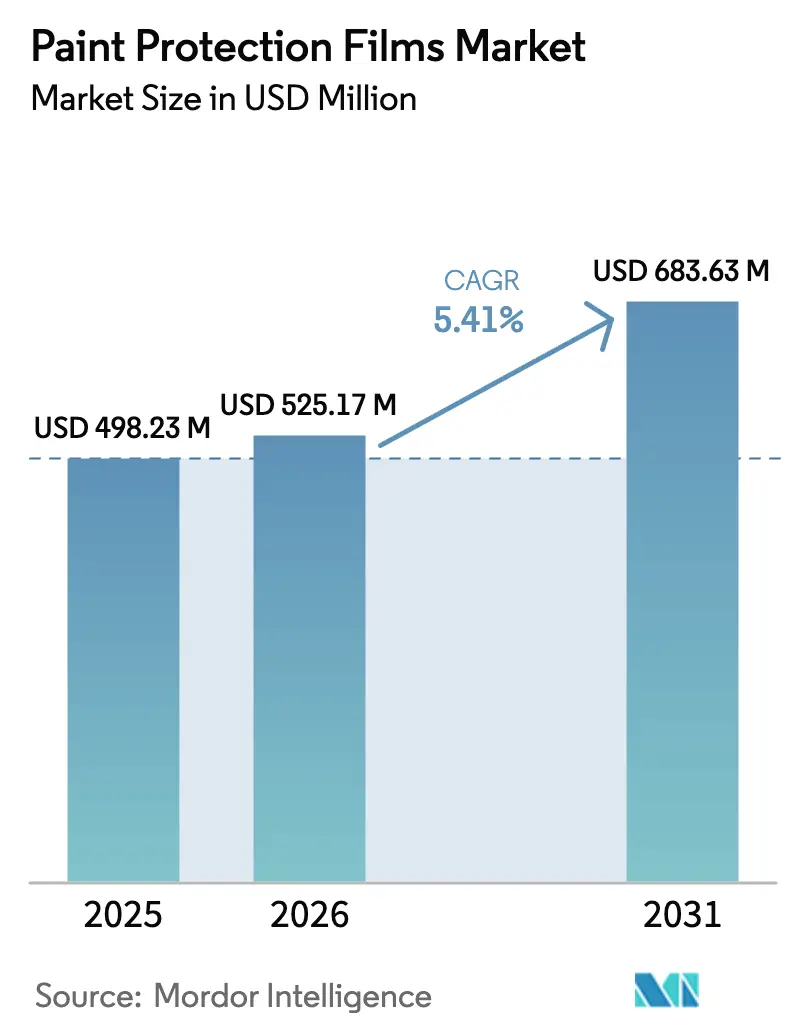

| Market Size (2026) | USD 525.17 Million |

| Market Size (2031) | USD 683.63 Million |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

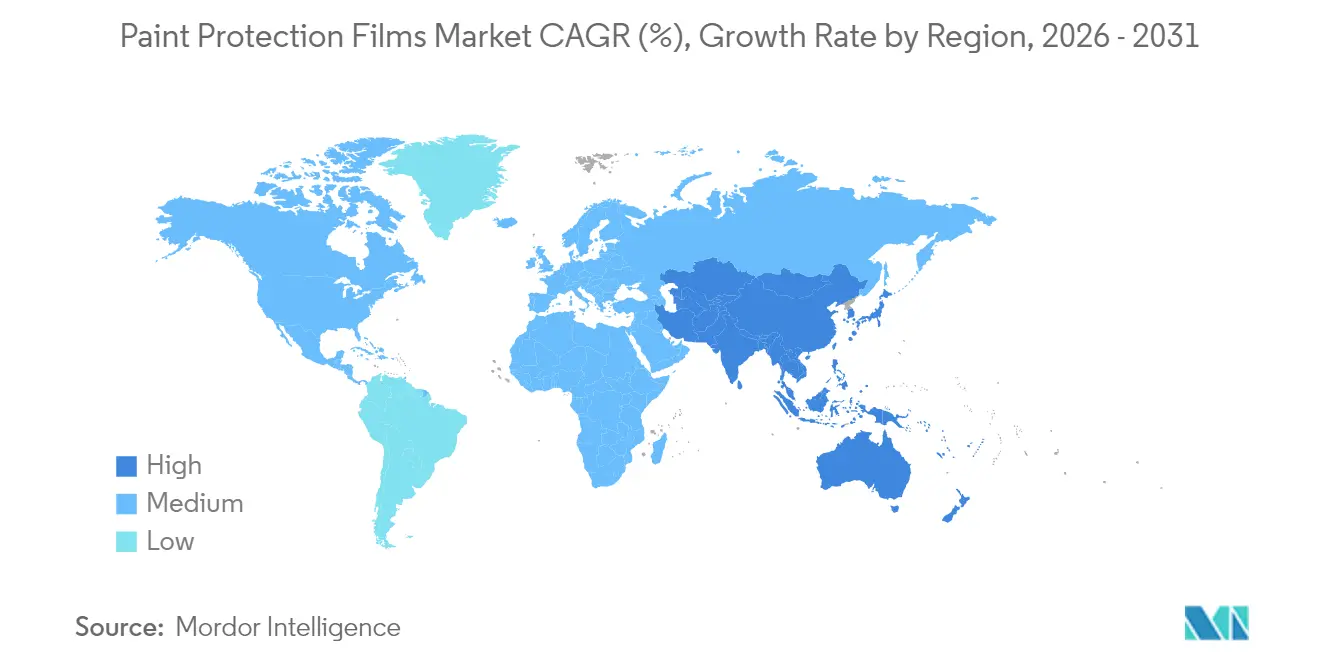

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Paint Protection Films Market Analysis by Mordor Intelligence

Paint Protection Films market size in 2026 is estimated at USD 525.17 million, growing from 2025 value of USD 498.23 million with 2031 projections showing USD 683.63 million, growing at 5.41% CAGR over 2026-2031. This rate outpaces pre-pandemic aftermarket growth because electric vehicle output is accelerating, vehicle owners are holding onto their cars longer, and protective wraps are increasingly transitioning from a luxury accessory to a cost-saving necessity. Nearly every major automotive brand now offers factory-installed panels that reduce repainting expenses over a 7- to 10-year ownership span. Thermoplastic polyurethane dominates because it self-heals scratches at room temperature, while polyvinyl chloride remains a value choice in price-sensitive regions. OEM programs, such as Tesla’s, drive volume into production lines, squeezing independent installers while raising overall demand. The Asia-Pacific region leads as both a TPU importer and a final-assembly hub, while growth in North America and Europe depends on wider OEM adoption and continued consumer enthusiasm for resale value.

Key Report Takeaways

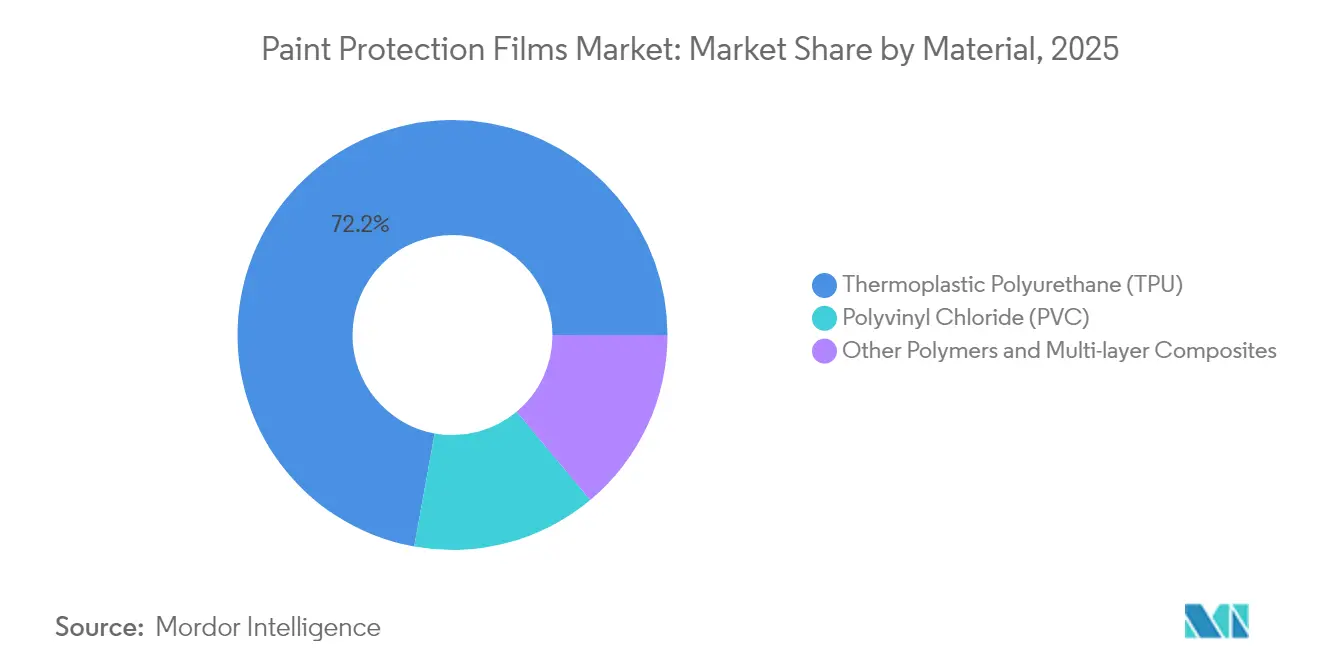

- By material, thermoplastic polyurethane captured 72.15% of the paint protection films market share in 2025 and is projected to grow at a 5.95% CAGR through 2031.

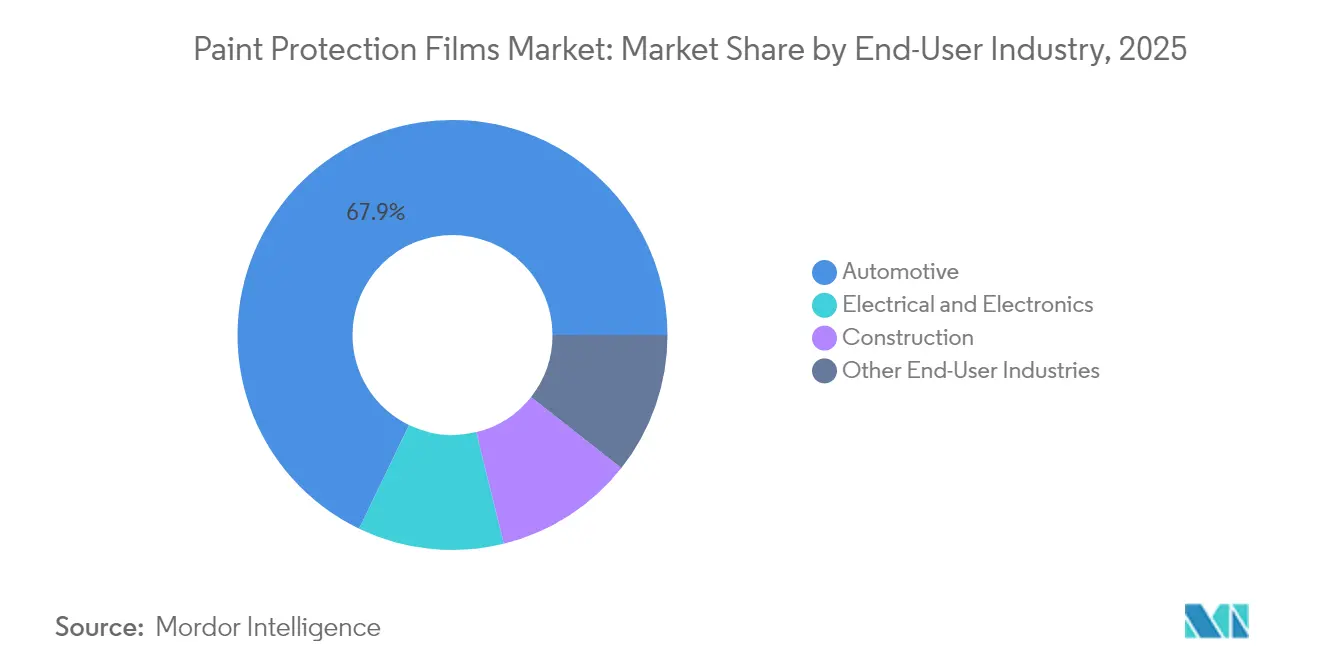

- By end-user industry, the automotive sector contributed 67.85% of the paint protection films market size in 2025, whereas the electrical and electronics sector is expanding at a 5.82% CAGR through 2031.

- By geography, the Asia-Pacific region held 46.10% of the revenue in 2025 and is projected to advance at a 5.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paint Protection Films Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Luxury and electric vehicle production boom fuels OEM/aftermarket demand | +1.5% | Global, with concentration in North America, China, and Europe | Medium term (2-4 years) |

| Advancements in self-healing TPU chemistry | +1.0% | Global, led by Asia-Pacific manufacturing and North American research and development | Long term (≥ 4 years) |

| Growing consumer focus on vehicle aesthetics and resale value | +0.9% | Global, strongest in developed markets with high vehicle ownership | Medium term (2-4 years) |

| Factory-installed PPF options led by EV brands | +0.8% | North America and Asia-Pacific, early adoption in Europe | Short term (≤ 2 years) |

| AI-guided cutting/AR tools slashing installer time and cost | +0.6% | North America and Europe, gradual spread to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Luxury and Electric Vehicle Production Boom Fuels OEM/Aftermarket Demand

Record luxury and electric-vehicle launches channel high-value paint finishes onto platforms where buyers expect premium add-ons. Programs with Tesla and Rivian integrate wraps before delivery, cutting manual labor and widening accessibility to consumers who rarely visit aftermarket shops. A growing fleet of high-mileage electric taxis also favors films that prevent stone-chip repaint costs. As the average age of U.S. vehicles rose, owners saw clearer payback on long-life wraps. Luxury brands in China added certified TPU panels, helping the paint protection films market expand beyond niche enthusiasts. Overall, high-priced vehicle segments now act as the gateway for mainstream adoption.

Advancements in Self-Healing TPU Chemistry

Room-temperature self-repair polymers now heal micro-scratches within seconds rather than minutes, reducing user maintenance. Academic breakthroughs utilizing disulfide and imine bonds validated the rapid reformation of bonds, while commercial launches, such as Avery Dennison Supreme PPF Xtreme, translated lab results into ten-year warranties[1]"Supreme PPF Xtreme Launch," Avery Dennison, averydennison.com. Polycaprolactone-rich polyols underpin the chemistry, delivering elasticity across a temperature range of –40 °C to 90 °C and resisting yellowing. These innovations enhance pricing power and extend replacement intervals, driving premium tiers in the paint protection films market.

Growing Consumer Focus on Vehicle Aesthetics and Resale Value

A UK study found that verified paint protection lifted used-car trade-in offers[2]"Paint Protection Film vs Ceramic Coating: Cost and Performance Comparison," Detailing World, detailingworld.co.uk. This resale upside resonates as buyers keep vehicles longer and prioritize appearance during private sales. Younger drivers associate wraps with personalization, helping to sustain aftermarket channel strength even as OEM programs grow. Ride-hailing fleets apply partial wraps to doors, rocker panels, and bumpers, extending service life and compressing downtime. Awareness campaigns now emphasize durability rather than gloss alone, helping consumers distinguish between films and ceramic coatings.

Factory-Installed PPF Options Led by EV Brands

Electric-vehicle makers prefer matte, satin, or multicoat metallic paints, which can cost thousands of dollars to repair. Therefore, wrapping during final assembly helps lower warranty repaint expenses. Tesla installs XPEL Ultimate Plus under controlled robotics, reducing cycle time to under two hours and integrating coverage into the basic vehicle warranty. FAW-Volkswagen certified BASF’s RODIM TPU, signaling that Asian and European factories are adopting similar lines. OEM integration secures high-volume contracts for large converters and obliges smaller installers to shift their focus toward customization and rapid service.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitute products (ceramic coatings, waxing) | -0.7% | Global, strongest in price-sensitive markets | Medium term (2-4 years) |

| High professional installation cost | -0.6% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| TPU price volatility from 2025 tariff hikes | -0.5% | Asia-Pacific and North America supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Substitute Products (Ceramic Coatings, Waxing)

Ceramic coatings cost less than full-vehicle wrapping, tempting budget-minded buyers and diluting entry-level demand. Yet coatings lack impact absorption and self-healing, so fleets and high-mileage users still prefer films. Periodic recoating every two to five years erodes the price gap over time. In South America and parts of Southeast Asia, do-it-yourself wax remains culturally popular, prolonging the use of substitutes and limiting penetration for the paint protection films market.

High Professional Installation Cost

Partial panels trim outlay but expose unprotected seams. Quality varies significantly, and inferior workmanship can cause edge lifting, tarnishing the brand's perception. AI plotters and augmented-reality guides now cut templates and align panels within millimeter tolerances, thereby lowering errors; however, adoption lags where wages are low. Without scaling skilled labor, many emerging markets will likely trail behind developed regions, despite the latent demand for the paint protection films market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: TPU Extends Lead Through Self-Healing Performance

Thermoplastic polyurethane captured 72.15% of the paint protection film market share in 2025 and is forecasted to rise at a 5.95% CAGR through 2031. Premium polycaprolactone TPU grades offer sustained impact resistance across temperature extremes and rapidly reform micro-scratches, differentiating them from polyvinyl chloride. Some installers still offer PVC at a lower cost, but its tendency to yellow and crack limits uptake in harsh climates. Investments by Covestro in Taiwan and Germany increase global TPU capacity, yet recent Indian anti-dumping duties on Chinese resin raise regional costs. Composite innovations, such as PVDF-PMMA laminates, extend durability to facades and aircraft interiors, thereby broadening the addressable market size for paint protection films.

Covestro’s German line, set for 2025, is expected to augment Desmopan UP output to meet automotive and electronics demand, indicating a long-term bullish outlook. At the same time, U.S. automotive tariffs risk increasing landed costs if waivers are not extended. Resin volatility encourages converters to dual-source materials and explore hybrid films that strike a balance between cost and self-healing functionality.

By End-User Industry: Automotive Dominates While Electronics Accelerates

Automotive applications accounted for 67.85% of the paint protection films market size in 2025, as body panels and high-impact zones continue to be core revenue streams. OEM installations shift revenue upstream, but dealerships and aftermarket shops still thrive on customization, color-change wraps, and partial kits. The segment moves toward robot-assisted booths that wrap multiple panels per shift, standardizing quality at scale. Electrical and electronics devices are projected to post a 5.82% CAGR outlook through 2031, driven by infotainment screens, instrument clusters, and consumer tablets that require anti-fingerprint clarity. As cabin displays grow to sport 20-inch or wider diagonals, protective TPU layers safeguard optical surfaces against scratches and static. Construction, aerospace, and marine comprise small yet rising niches, adopting multi-layer composites with fire retardance or ultraviolet stability.

Geography Analysis

Asia-Pacific generated 46.10% of 2025 revenue and will expand at a 5.56% CAGR through 2031. China is both the largest TPU importer and a leading PPF exporter, hosting high-capacity converters that supply regional automakers and smartphone assemblers. India’s anti-dumping duties on Chinese TPU raise domestic feedstock costs yet encourage local resin investment. Japan’s mature aftermarket enjoys high awareness, but a shrinking vehicle parc restrains absolute growth. South Korean electronics majors create stable demand for display wraps, while Thailand and Vietnam attract new PPF coating lines amid supply chain diversification.

North America contributes a significant portion of the global value. Tesla and Rivian’s factory-installed options lift orders for ISO 9001-certified converters, while independent installers pivot to special-finish wraps and rapid-fit services. U.S. tariffs enacted in 2025 may inflate imported TPU prices, but domestic resin capacity moderates the risk. Canada mirrors U.S. tastes, with a premium vehicle share and harsh winter road debris reinforcing the adoption of wrap. Mexico is emerging as a lower-cost production node, although installer networks are concentrated around Monterrey and Mexico City.

In Europe, Germany, the United Kingdom, and France are the major contributors. REACH restrictions on legacy UV absorbers prompt formulators to shift toward next-generation stabilizers, increasing compliance costs while enhancing environmental credentials. Euro 7 regulations could extend average vehicle life, indirectly supporting demand as owners aim to protect higher-priced models. OEM wrap adoption remains nascent but is advancing as premium German brands test in-plant lines.

Brazil’s recovering economy is spurring luxury-vehicle protection among wealthy buyers, although high import tariffs and a fledgling installer density limit its wider reach. The Gulf Cooperation Council states embrace films for heat and sand abrasion control, and wealthy owners routinely wrap vehicles shortly after purchase. South Africa experiences sporadic demand, primarily in urban centers, which is hindered by currency volatility.

Competitive Landscape

The paint protection films market is moderately consolidated. Scaling strategies define competition. Regional challengers leverage lower manufacturing costs to secure a domestic market share, but often lack a global dealer footprint. OEM contracts exert rising influence. Winning bids require consistent optical clarity, color stability, and robotic lay-down compatibility. Patent filings cluster around room-temperature self-healing and multi-layer architectures that integrate PVDF topcoats or flame-retardant cores. As material science advances, converters with in-house research and development gain an edge in negotiating premium supply agreements. Technology divides installers. North American and European shops invest in AI plotters and AR glasses to reduce labor hours, whereas price-focused markets rely on low-wage manual labor. This disparity reinforces a two-tier structure where premium channels deliver consistent outcomes and budget players compete on cost. Over time, software subscriptions may become table stakes, cementing lead positions for globally branded suppliers.

Paint Protection Films Industry Leaders

-

3M

-

Eastman Chemical Company

-

XPEL, Inc.

-

AVERY DENNISON CORPORATION

-

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: 3M unveiled the Paint Protection Film Series 100 Gloss and Series 150 Gloss, exclusively with the William Smith Group, offering seven- and ten-year warranties, respectively, along with hydrophobic finishes for full-vehicle wraps. This will help 3M to boost its presence in the United Kingdom.

- July 2025: Nippon Paint announced its entry into India’s automotive surface protection market with the launch of its ‘n-SHIELD’ Paint Protection Films (PPF). The launch signals Nippon Paint’s intent to expand its footprint in the growing but largely unorganised vehicle paint protection space. The company has been developing its film-based offerings over the past four years and is now rolling them out across India and other global markets, following an initial launch in Thailand.

Global Paint Protection Films Market Report Scope

The paint protection film (PPF) is a self-healing layer that is applied to the painted surfaces of a new or used car to protect the paint from minor abrasions and others. PPF film is also used on planes, electronics, cell phones, motorcycles, screens, and a wide range of other applications. The paint protection film market is segmented by material, end-user industry, and geography. By material, the market is segmented into thermoplastic polyurethane (TPU), polyvinyl chloride (PVC), and others. By end-user industry, the market is segmented into automotive, electrical and electronics, construction, and other end-user industries. The report also covers the market size and forecasts in 15 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD million).

| Thermoplastic Polyurethane (TPU) |

| Polyvinyl Chloride (PVC) |

| Other Polymers and Multi-layer Composites |

| Automotive |

| Electrical and Electronics |

| Construction |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | Thermoplastic Polyurethane (TPU) | |

| Polyvinyl Chloride (PVC) | ||

| Other Polymers and Multi-layer Composites | ||

| By End-User Industry | Automotive | |

| Electrical and Electronics | ||

| Construction | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the paint protection films market in 2026?

The paint protection film market size is expected to reach USD 525.17 million by 2026.

What CAGR is forecast for paint protection films between 2026 and 2031?

A 5.41% CAGR is projected for the 2026–2031 period.

Which material leads in paint protection films?

Thermoplastic polyurethane holds 72.15% share, driven by self-healing performance.

Which region is the biggest consumer of paint protection films?

The Asia-Pacific region accounted for 46.10% of the revenue in 2025 and remains the largest regional market.

Why are OEM installations growing in paint protection films?

Electric-vehicle brands adopt factory wrapping to protect complex paint finishes and cut warranty repaint costs.

What restrains wider adoption of paint protection films?

High professional installation costs and competition from lower-priced ceramic coatings temper mass-market uptake.

Page last updated on: