Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

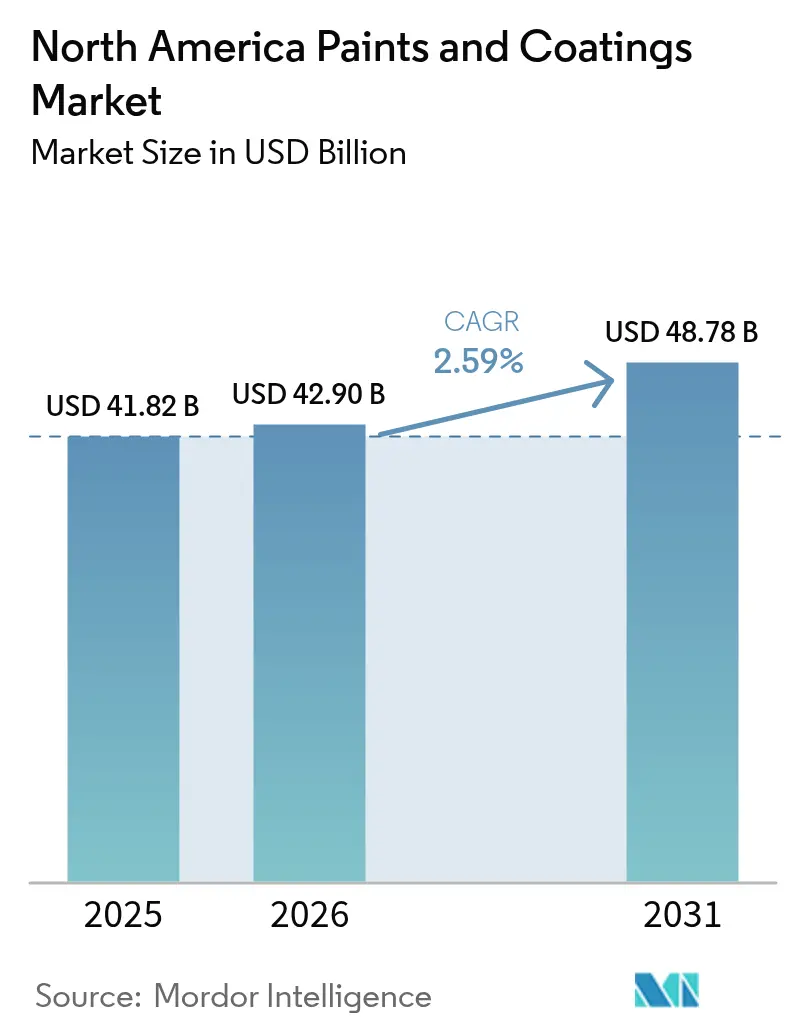

| Base Year Market Size (2025) | USD 41.82 Billion |

| Market Size (2026) | USD 42.9 Billion |

| Market Size (2031) | USD 48.78 Billion |

| Growth Rate (2026 - 2031) | 2.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Paints And Coatings Market Analysis by Mordor Intelligence

The North America Paints and Coatings Market size in 2026 is estimated at USD 42.9 billion, growing from 2025 value of USD 41.82 billion with 2031 projections showing USD 48.78 billion, growing at 2.59% CAGR over 2026-2031. Steady gains stem from deeper penetration of water-borne technologies, which command a 57.23% share, and resilient architectural renovation alongside commercial construction outlays. The United States generates 85.64% of all regional demand based on extensive building stock and reshoring-led industrial activity. Acrylic resins remain the volume cornerstone at 37.67% share, yet polyurethane lines expand quickest as OEMs (original equipment manufacturers) prioritize toughness and weather resistance. Margin discipline hinges on mitigating 15-25% quarterly swings in petrochemical feedstocks while automating production and color-matching workflows to offset skilled-labor deficits.

Key Report Takeaways

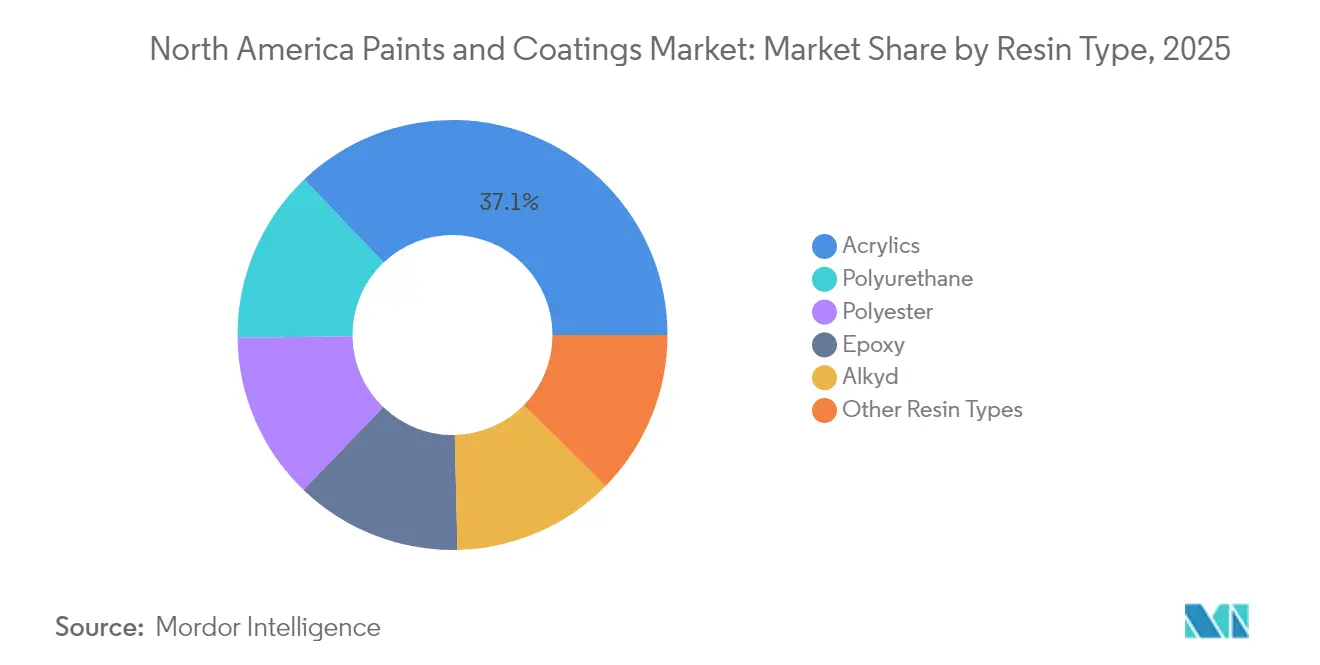

- By resin type, acrylics led with 37.12% of the North American Paints and Coatings market share in 2025, while polyurethanes posted the highest projected CAGR at 2.95% through 2031.

- By technology, water-borne systems accounted for a 57.05% share of the North American Paints and Coatings market size in 2025; powder coatings are set to advance at a 3.18% CAGR between 2026-2031.

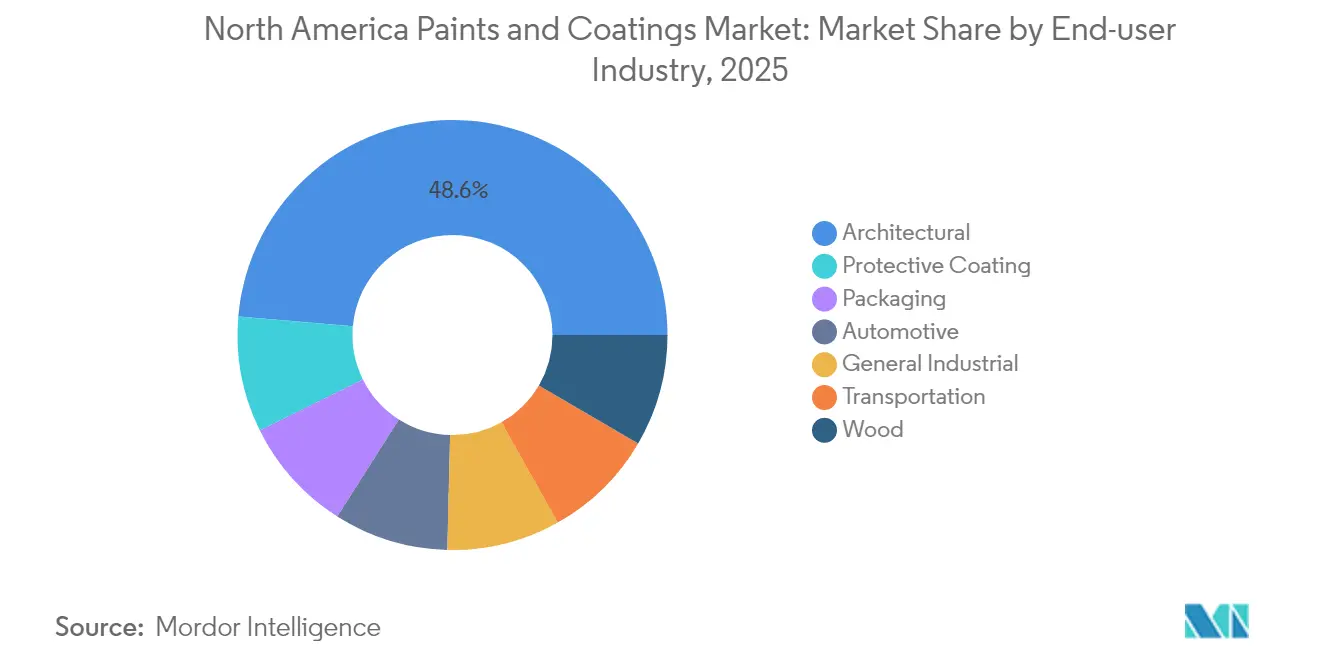

- By end-user industry, architectural applications captured 48.62% of the North American Paints and Coatings market size in 2025 and are tracking a 3.22% CAGR to 2031.

- By geography, the United States held 85.18% revenue share in 2025, reflecting scale advantages in manufacturing, construction, and distribution networks.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Commercial and Institutional Construction | +0.8% | United States core; spillover to Canadian cities | Medium term (2-4 years) |

| Rapid Shift to Low-VOC Water-borne Technologies | +0.6% | Region-wide, led by California and Northeast | Long term (≥ 4 years) |

| OEM Demand for High-performance Powder Coatings | +0.5% | U.S. manufacturing belt; Mexico maquiladora zones | Medium term (2-4 years) |

| AI-driven Color-matching Platforms Accelerating Repaint Cycles | +0.4% | United States and Canada metros | Short term (≤ 2 years) |

| Reshoring of US Manufacturing Boosting Anti-corrosion Demand | +0.3% | Rust Belt and Southeast corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Commercial and Institutional Construction

Commercial outlays reached USD 180 billion in 2024, translating directly into greater demand for premium architectural coatings that meet strict indoor-air requirements[1]U.S. Census Bureau, “Value of Construction Put in Place,” census.gov. Healthcare builds alone represented USD 12 billion in coating-intensive projects as antimicrobial finishes became baseline specifications. Renovation cycles across logistics hubs, data centers, and educational facilities sustain high-margin orders for fire-retardant and static-dissipative paints. Low-emission mandates such as the South Coast Air Quality Management District cap of 50 g/L VOC further shift preference toward advanced water-borne lines. The driver, therefore, locks in steady architectural pull for the North American paints and coatings market.

Rapid Shift to Low-VOC Water-borne Technologies

Eighteen U.S. states now enforce VOC limits below federal thresholds, accelerating water-borne adoption across all usage classes. Architectural variants fetch 15–20% price premiums, cushioning margin pressure even as solvent inputs spike. Hybrid chemistries marry water clean-up with solvent-level endurance in protective segments, helping suppliers capture long-cycle industrial contracts. The regulatory tide effectively institutionalizes higher specification, lifting average selling prices within the North American paints and coatings market.

OEM Demand for High-performance Powder Coatings

Automotive and appliance OEMs favor powder lines for near-zero emissions and 98% transfer efficiency, a tangible cost advantage over liquid finishes. Electric-vehicle battery housings, thermal shields, and appliance panels add functional parameters such as dielectric strength and heat dissipation, moving powder beyond aesthetics. Mexico’s maquiladora clusters rely on these coatings to meet US import standards, reinforcing demand integration across the North American paints and coatings market.

AI-driven Color-matching Platforms Accelerating Repaint Cycles

Sherwin-Williams’ ColorSnap processed more than 2 million digital matches monthly in 2024, cutting color selection cycles from weeks to hours[2]Sherwin-Williams, “ColorSnap Usage Statistics,” sherwin-williams.com. BASF’s Refinity brings similar speed to body-shop refinishing, slashing booth downtime and material waste. Contractors report 25% productivity gains, turning rapid repaint into a volume lever for the North American paints and coatings market. The technology particularly impacts architectural repaint markets, where color uncertainty traditionally delayed project initiation by 2-4 weeks while customers evaluated options.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Petrochemical Raw-material Prices | -0.4% | Region-wide; acute in Gulf Coast | Short term (≤ 2 years) |

| Stringent and Diverging VOC Regulations Across US/Canada/Mexico | -0.3% | Most rigorous in California and Northeast | Medium term (2-4 years) |

| Skilled-applicator Labor Shortage in Industrial Coatings | -0.2% | U.S. industrial hubs; Canadian manufacturing centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Petrochemical Raw-material Prices

Titanium dioxide swings of 25% per quarter and acrylic-monomer spikes of 30% keep procurement budgets unstable, eroding contractual margins for smaller players. Supply chain disruptions from Gulf Coast weather events and refinery maintenance cycles amplify price volatility, with Hurricane Beryl's 2024 impact on Texas petrochemical facilities demonstrating the sector's vulnerability to operational disruptions. Manufacturers with hedging programs and integrated resin capacity can shield profitability, hastening consolidation within the North American paints and coatings market.

Stringent and Diverging VOC Regulations Across North America

Rule 1113 in California limits architectural paints to 50 g/L VOC, whereas Texas permits 380 g/L, forcing multi-formula inventories that fragment scale economics. Mexico’s draft limits mirror California thresholds but rely on different testing protocols, adding another compliance tier. Regulatory inconsistency increases cost-to-serve and slows time to market. The regulatory constraint particularly impacts industrial coatings, where performance requirements often conflict with emission limitations, forcing manufacturers to invest in advanced polymer chemistry research to achieve compliance without sacrificing durability characteristics

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance with Polyurethane Momentum

Acrylic systems occupied 37.12% of the North American paints and coatings market share in 2025, benefiting from balanced cost, weatherability, and color retention across architectural and automotive finishes. The sub-segment also captures early wins from bio-based feedstock innovation, meeting sustainability mandates without sacrificing performance. While smaller in absolute terms, polyurethane grades log the fastest 2.95% CAGR through 2031 on demand for high-abrasion durability in OEM assemblies. Epoxies stay indispensable in marine and infrastructure applications where chemical resistance outweighs initial cost concerns. Alkyd displacement accelerates as VOC norms tighten, yet modified alkyd-water hybrids prolong relevance in niche trim and primer roles. Blended chemistries that marry acrylic elasticity with polyurethane hardness present fertile ground for differentiated offerings inside the North American paints and coatings market.

In industrial maintenance and asset-protection projects, silicone and fluoropolymer niches command premium pricing due to extreme heat or chemical exposures, although their aggregate revenue share remains modest. Polyester resins gain ground in powder lines, reinforcing the zero-VOC narrative while delivering 25-year façade warranties for aluminum extrusions. Resin choice therefore centers less on commodity cost and more on life-cycle value as facility owners calculate total operating expense. Suppliers with cross-technology R&D capacity enjoy a service moat that newcomers struggle to replicate, reinforcing competitive stratification throughout the North American paints and coatings industry.

By Technology: Water-borne Pre-eminence, Powder Acceleration

Water-borne platforms captured 57.05% of the total value in 2025, cementing their position as the baseline chemistry for interior and exterior architectural work. Transfer efficiency gains, odor reduction, and easier equipment cleanup help contractors save labor time, enhancing pull-through for distributors. Powder coatings, at a 3.18% CAGR to 2031, ride electrification and appliance output as zero-VOC policies converge with production-line automation. UV-cured segments diversify into flooring and packaging, where instant handling offsets higher resin cost, and solvent-borne grades retreat into specialist assignments demanding solvent-level outcomes. Digital viscosity monitoring enables painters to hit water-borne spray windows with repeatable results, tackling historical humidity sensitivity issues. The technology mix underscores how sustainability plus productivity jointly influence capital-purchase decisions inside the North American paints and coatings market.

Hybrid solutions bridge extreme-service gaps—for example, water-borne primers topped with solvent-free polysiloxane clears for coastal bridges—proving that innovation leans toward system thinking rather than single-product swaps. Equipment makers align by integrating electrostatic guns, curing ovens, and data analytics into turnkey cells, raising switching barriers and locking in powder-line growth. Such total-ecosystem orientation solidifies the future trajectory of the North American paints and coatings market.

By End-user Industry: Architectural Core with Emerging Industrial Diversity

Architectural work flowed through USD billions of commercial towers, warehouses, and multifamily renovations, capturing 48.62% of 2025 revenue and charting the fastest 3.22% CAGR through 2031. Sustainability certifications, including LEED (Leadership in Energy and Environmental Design) v4.1 low-emitting criteria, intensify demand for zero-solvent and antimicrobial lines. Automotive coatings confront drivetrain electrification: battery casings need electrostatic shielding, while lightweight substrates require flexible finishes, each commanding higher selling prices. Wood furniture and millwork benefit from reshored cabinetry plants and consumer interest in non-yellowing clearcoats. Protective coatings become mission-critical as bridge agencies and oil-and-gas operators replace legacy epoxy coal-tar with novolac hybrids that double service intervals, limiting downtime costs. Packaging evolves via BPA-free liners in food cans and UV-flexo overprints on metal tubes. Collectively, this industrial diversity insulates the North American paints and coatings market from single-sector cyclicality.

Contractors and OEMs alike now weigh coatings through a total-ownership lens that factors accelerated assembly, warranty risk, and disposal compliance. High-performance formulations win bids where maintenance shut-downs carry six-figure opportunity costs per day. Suppliers that outfit technical service teams and digital support portals secure preferred-vendor status, elevating service value alongside product volume across the North American paints and coatings industry.

Geography Analysis

The United States delivered 85.18% of 2025 turnover and is forecast for a 2.84% CAGR to 2031 as infrastructure renewal, commercial space builds, and semiconductor fabs broaden coating consumption. State-by-state VOC discrepancies complicate logistics, yet they also steer premium uptake where the lowest-emission benchmarks apply. Manufacturing credits under the Inflation Reduction Act channel investment toward battery, solar, and chip plants that require highly specified anti-corrosion and clean-room coatings, cementing the country’s central role within the North American paints and coatings market.

Canada positions itself as a specialized niche emphasizing resource extraction and harsh-climate durability. Protective systems for pipelines, mining equipment, and hydroelectric structures wield strong pricing power due to extreme service conditions. Regulatory harmonization with the US EPA (Environmental Protection Agency) simplifies cross-border approvals, letting producers leverage continental manufacturing footprints while tailoring for cold-weather cure windows. Urban housing upgrades in Toronto, Vancouver, and Calgary additionally feed architectural repaint demand, providing balanced volume continuity for the North American paints and coatings market.

Mexico offers the growth lever as OEMs realign supply chains under USMCA (United States-Mexico-Canada Agreement). Automotive, appliance, and electronics plants around Monterrey, Saltillo, and the Bajío corridor specify powder and low-VOC water-borne systems to comply with corporate sustainability pledges. SEMARNAT’s tightening draft rules heighten the need for compliant local supply. AkzoNobel’s USD 3.6 million powder-line expansion in Tlalnepantla signals broader multinational confidence in Mexican throughput potential. The tri-national dynamics underline the integrated yet varied geography of the North American paints and coatings market.

Competitive Landscape

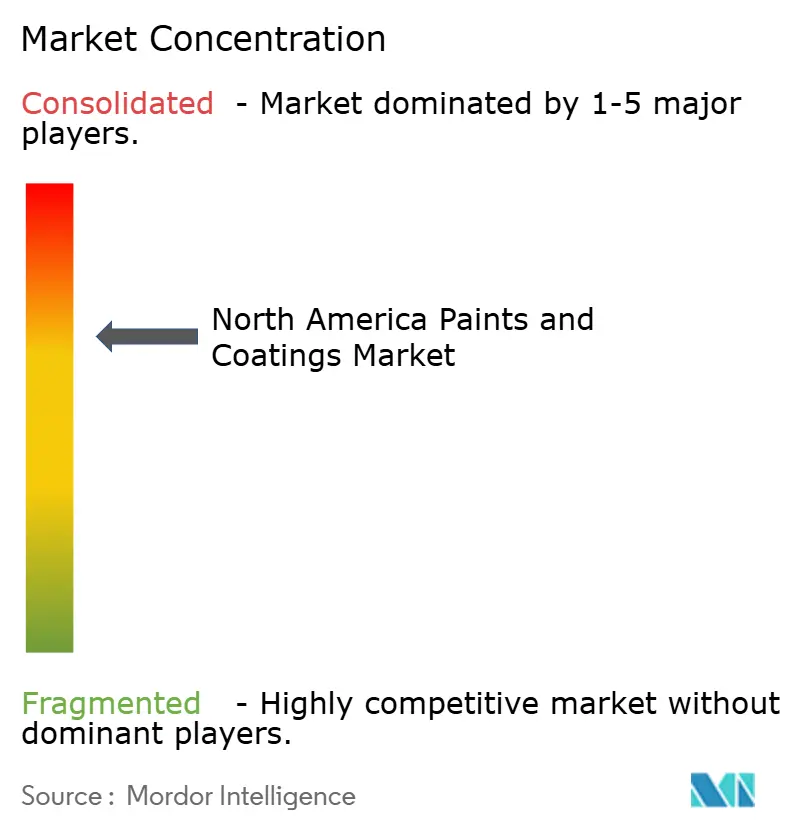

The North America Paints and Coatings market is consolidated. Market leadership rests with global brands such as PPG, Sherwin-Williams, AkzoNobel, BASF, and Axalta, each balancing scale with segment specialization. PPG divested its United States and Canadian commodity architectural arm for USD 550 million in September 2024 to refocus on higher-margin industrial lines. Simultaneously, sustainability initiatives—recycled-content powders, bio-based binders, and low-energy cure technologies—position incumbents for premium tiers. Competitive dynamics, therefore, hinge on balancing margin protection with transformative innovation across the North American paints and coatings industry.

North America Paints And Coatings Industry Leaders

The Sherwin-Williams Company

PPG Industries, Inc.

RPM International Inc.

Akzo Nobel N.V.

Axalta Coating Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Benjamin Moore & Co. unveiled its latest Eco Spec line in the United States, marking its commitment to eco-friendliness with its greenest and least odorous paint. Even after tinting, Eco Spec achieves zero VOCs and zero emissions for consumers and professionals.

- May 2024: PPG Industries, Inc. announced plans to invest USD 300 million in advanced manufacturing across North America to cater to the surging demand for automotive paints and coatings. Central to this initiative is a new manufacturing plant, spanning 250,000 sq. ft, established in Loudon County, Tennessee, with a projected completion date in 2026.

North America Paints And Coatings Market Report Scope

Paints and coatings are a homogeneous mixture of pigments, binders, and additives, which are applied to make a thin layer of the solid film once polymerization or evaporation occurs. The paints and coatings market is segmented by resin type, technology, end-user, and geography. The market is segmented by resin: acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, powder-coating, and UV-cured coating. The end-user industry segments the market into architectural, automotive, wood, protective coatings, general industrial, transportation, and packaging. The report also covers the market size and forecasts for the market in 3 regions. For each segment, the market sizing and forecasts have been done based on value (USD million).

By Resin Type

| Acrylics |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coating |

| UV-cured Coating |

By End-user Industry

| Architectural |

| Automotive |

| Wood |

| Protective Coating |

| General Industrial |

| Transportation |

| Packaging |

By Country

| United States |

| Canada |

| Mexico |

| By Resin Type | Acrylics |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder Coating | |

| UV-cured Coating | |

| By End-user Industry | Architectural |

| Automotive | |

| Wood | |

| Protective Coating | |

| General Industrial | |

| Transportation | |

| Packaging | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will the North American paints and coatings market be by 2031?

Forecasts point to USD 48.78 billion by 2031, up from USD 42.9 billion in 2026.

Which technology segment is expanding fastest across North America?

Powder coatings are projected to grow at a 3.18% CAGR through 2031 thanks to zero-VOC credentials and high transfer efficiency.

What share do water-borne coatings command in 2025?

Water-borne formulations hold 57.05% of regional value, reflecting tightening VOC rules.

Why are polyurethanes gaining traction?

OEM buyers favor their superior abrasion resistance and durability, driving a 2.95% CAGR to 2031.

Which end-user category leads demand?

Architectural applications generate 48.62% of revenue due to steady new-build and renovation cycles.

Page last updated on: