Test And Measurement Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 19.84 Billion |

| Market Size (2031) | USD 24.27 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Test And Measurement Market Analysis by Mordor Intelligence

The test and measurement market size was valued at USD 19.06 billion in 2025 and estimated to grow from USD 19.84 billion in 2026 to reach USD 24.27 billion by 2031, at a CAGR of 4.11% during the forecast period (2026-2031). Automotive electrification, 5G and early-stage 6G deployments, and rising semiconductor design complexity are shifting demand toward higher-bandwidth, software-defined instruments, even as aggregate revenue grows steadily. Modular architectures are eroding the dominance of traditional benchtop equipment, as aerospace and electric-vehicle OEMs favor reconfigurable test cells to shorten validation cycles. Service business models are moving from capital purchases to usage-based subscriptions, a trend that is compressing average selling prices but widening the addressable customer base. Asia Pacific leads regional growth, yet the Middle East shows the fastest trajectory as national technology programs diversify economies away from hydrocarbons.

Key Report Takeaways

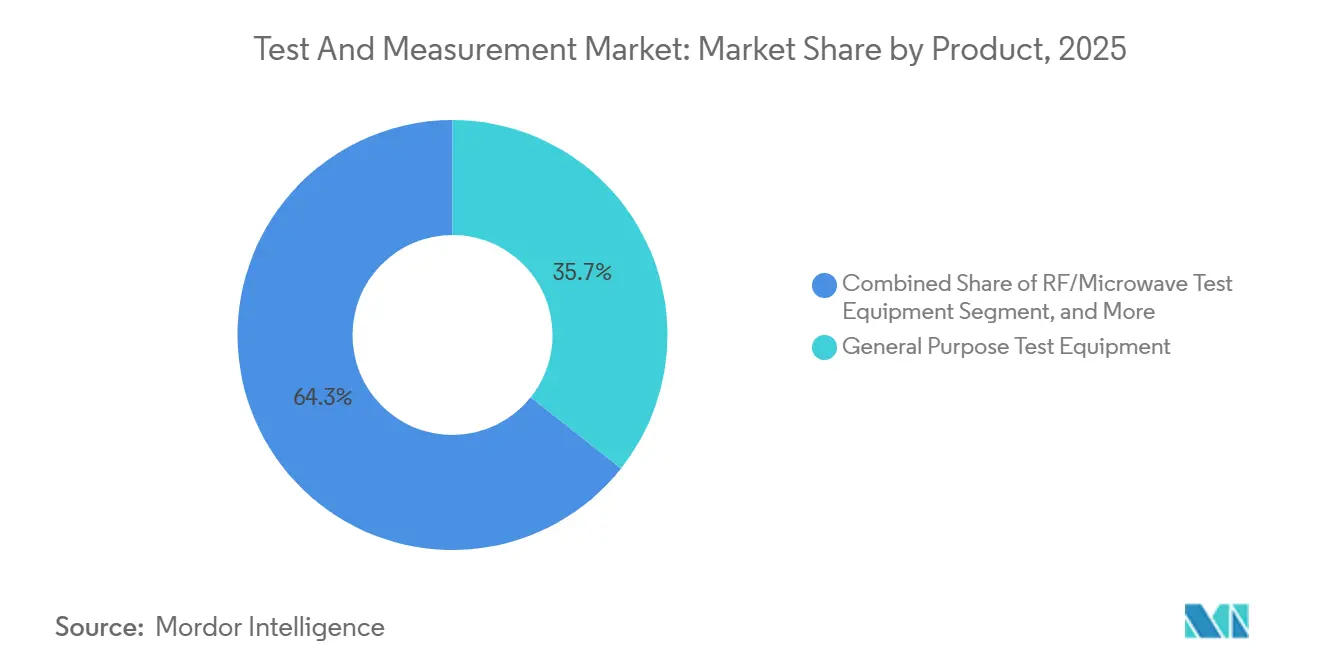

- By product category, General Purpose Test Equipment led with 35.67% of the test and measurement market share in 2025, while Modular Instrumentation is forecast to advance at a 5.44% CAGR through 2031.

- By service type, Calibration Services accounted for 39.33% of revenue in 2025, whereas Asset Management and Rental Services are projected to expand at a 5.12% CAGR over 2026-2031.

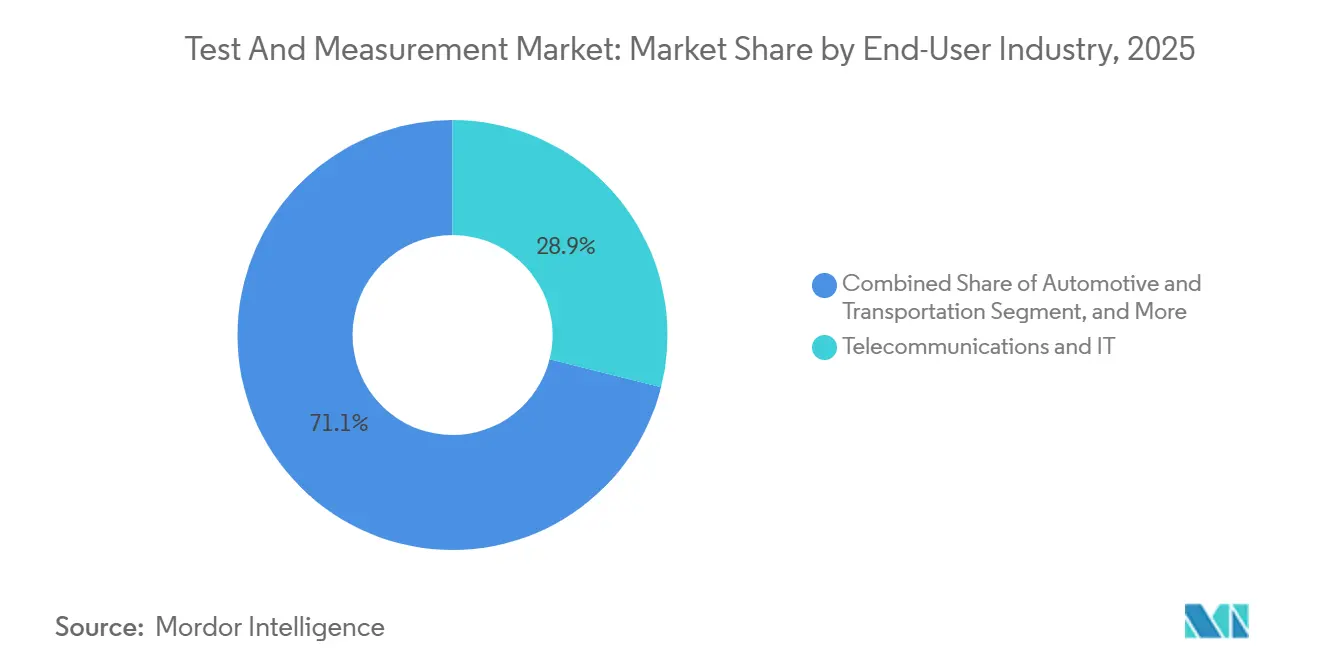

- By end-user industry, Telecommunications and IT held 28.91% of revenue in 2025, while Automotive and Transportation are poised to grow at a 5.67% CAGR during the same period.

- By form factor, Benchtop and Rack-Mounted Instruments accounted for 45.76% of revenue in 2025, yet Embedded and In-System Test Modules are set to grow at a 5.03% CAGR through 2031.

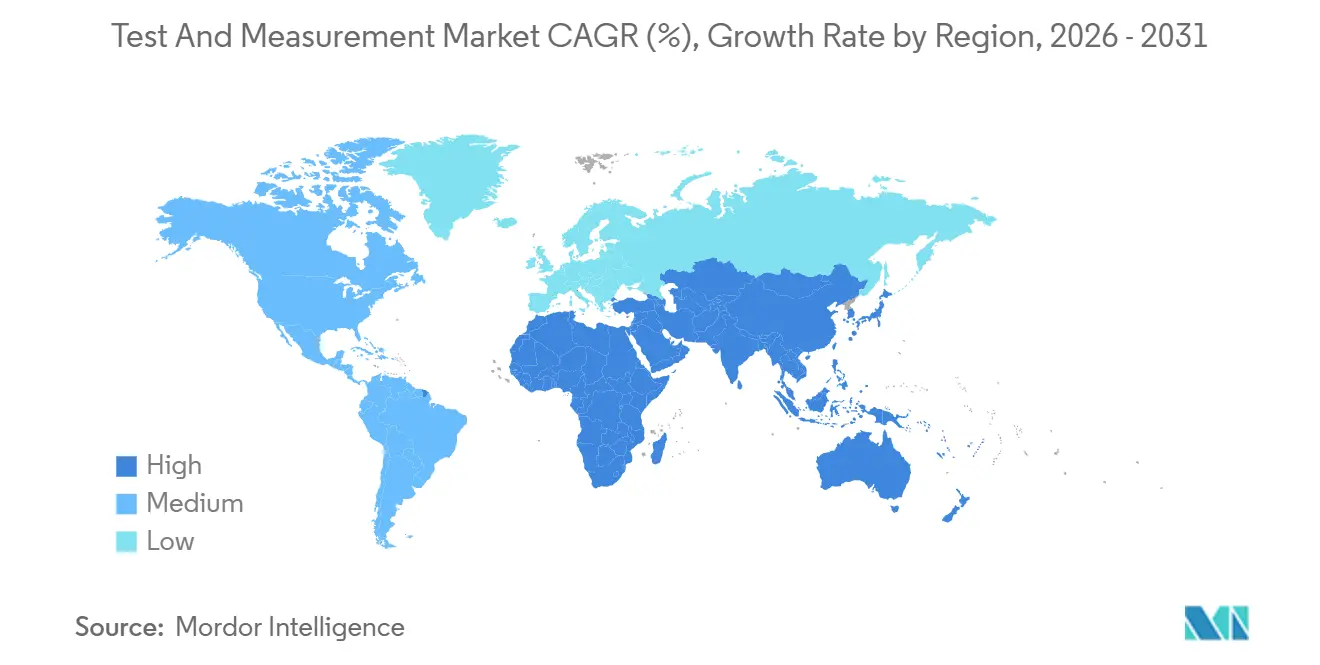

- By geography, Asia Pacific captured 32.46% of 2025 revenue, whereas the Middle East is projected to record a 5.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Test And Measurement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive E-Mobility Demand for High-Voltage, High-Bandwidth Testing | +0.9% | China, Europe, North America | Medium term (2-4 years) |

| Rapid 5G and 6G Roll-outs Requiring Sub-6 GHz and mmWave Capacity | +0.8% | Asia Pacific core, spill-over to Middle East and Latin America | Short term (≤ 2 years) |

| AI-Enabled Design-for-Test Tools Shortening Semiconductor Time-to-Market | +0.7% | Taiwan, South Korea, United States | Medium term (2-4 years) |

| Increasing Adoption of Integrated EV Battery Cyclers | +0.5% | Europe expanding to North America and China | Medium term (2-4 years) |

| Tightening EMC and EMI Norms for Medical Electronics | +0.4% | North America with influence in Europe and Japan | Short term (≤ 2 years) |

| Transition from CapEx to Test-as-a-Service Models | +0.6% | Global, early adoption in India, Southeast Asia, Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automotive E-Mobility Demand for High-Voltage, High-Bandwidth Testing Solutions

Electric-vehicle architectures operating at 800-volt and 1,200-volt levels require oscilloscopes, power analyzers, and isolation testers that far exceed legacy 400-volt thresholds. European OEMs were early adopters because the 2024 update of UN ECE R100 mandated stricter battery safety validation. Keysight Technologies disclosed double-digit automotive revenue growth in fiscal 2025, underscoring rising demand for bidirectional power supplies and regenerative load banks that absorb energy during braking simulation.[1]Keysight Technologies, “Fiscal 2025 Annual Report,” KEYSIGHT.COM Tier-1 suppliers are layering AI-driven anomaly detection onto automated test equipment to flag cell-level defects before pack assembly, reducing warranty risk and accelerating production ramp-ups. The migration from engine dynamometers to electric-drive test cells is widening opportunities for modular instrumentation that can be reconfigured across battery, inverter, and motor validation benches.

Rapid 5G and 6G Roll-outs Driving Sub-6 GHz and mmWave Test Capacity in Asia

China, South Korea, and Japan deployed over 3 million 5G base stations by the end of 2025, triggering purchases of spectrum and network analyzers that operate to 110 GHz. The International Telecommunication Union allocated additional spectrum for 6G research at the 2023 World Radiocommunication Conference, urging early investment in test equipment capable of characterizing terahertz components. Rohde and Schwarz extended its vector network analyzer line to 500 GHz in February 2025 to address satellite and automotive radar validation, exemplifying the arms race in bandwidth expansion.[2]Rohde and Schwarz, “R&S ZNA Series Launch,” ROHDE-SCHWARZ.COM Nonetheless, mmWave expertise is scarce in Southeast Asia, so operators rely on third-party calibration labs, which lengthen deployment timelines. India’s Department of Telecommunications also mandated 5G equipment testing at accredited facilities from 2024, creating short-term bottlenecks as labs upgraded for wideband and over-the-air validation.

AI-Enabled Design-for-Test Tools Shortening Semiconductor Time-to-Market

Semiconductor fabs now embed machine-learning algorithms into automated test equipment to reduce pattern count and improve fault coverage. TSMC reported that AI-assisted test program development cut validation cycles by 20% for advanced packaging nodes in 2024.[3]Taiwan Semiconductor Manufacturing Company, “2024 Annual Report,” TSMC.COM Advantest added generative AI models to its V93000 platform in fiscal 2025, enabling adaptive sequencing triggered by real-time yield data. Chiplet architectures intensify this need because traditional boundary-scan cannot isolate defects across multiple dies. IEEE working groups finalized universal chiplet interconnect specifications in 2025, prompting demand for high-speed digital instruments capable of verifying compliance at production scale. As design windows compress, AI-driven test optimization is becoming a competitive differentiator that aligns with shrinking product lifecycles.

Increasing Adoption of Integrated EV Battery Cyclers in Europe

European cell makers and OEMs deploy cyclers integrating impedance spectroscopy, thermal imaging, and gas chromatography to verify lithium-ion and solid-state cells under abuse conditions. Germany’s Federal Ministry for Economic Affairs and Climate Action funded EUR 150 million (USD 165 million) test infrastructure in 2024, catalyzing installations at Fraunhofer institutes. Chroma ATE recorded a 35% sales increase in European battery test systems in 2025, driven by expansions from Northvolt and Automotive Cells Company. The European Union’s Battery Regulation, fully applicable in 2024, requires carbon footprint disclosures, so manufacturers link serialized cell data to blockchain-based audit trails. These regulatory drivers push the adoption of cloud-connected cyclers that log gigabytes of charge-discharge data per pack, reinforcing modular, software-centric measurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rental-Shift Depressing New Instrument ASPs | -0.5% | India, Southeast Asia, Latin America, Africa | Medium term (2-4 years) |

| Scarcity of RF Talent Hindering mmWave Adoption | -0.3% | Global, acute in Southeast Asia and Middle East | Long term (≥ 4 years) |

| Fragmented Global Calibration Standards | -0.2% | Global, higher impact in multi-region operations | Long term (≥ 4 years) |

| Trade Barriers on Precision Semiconductors | -0.4% | China, Russia, export-controlled markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rental-Shift Depressing New Instrument ASPs in Emerging Markets

Contract manufacturers in India, Vietnam, and Mexico increasingly favor rental agreements when project-based production limits capital budgets. Electro Rent indicated utilization above 85% in Asia Pacific during 2025, the highest in a decade, reflecting customer preference for monthly subscriptions over hardware purchases. As multiple lessors aggregate idle fleets onto cloud platforms, competition centers on price, compressing average selling prices for oscilloscopes and multimeters. While customers gain flexibility and mitigate obsolescence, manufacturers face elongated revenue recognition and thinner aftermarket service margins. Over time, this structural change forces vendors to bundle analytics and calibration into service contracts to defend profitability.

Scarcity of RF Talent Hindering mmWave Test Adoption

The shift to mmWave frequencies for 5G, satellite links, and automotive radar is constrained by a shortage of engineers trained in waveguide calibration and over-the-air chamber design. An IEEE workforce study found that fewer than 15% of electrical-engineering graduates in India and Indonesia gained hands-on experience with vector network analyzers above 40 GHz, compared with over 40% in South Korea and Japan. Telecom operators in Saudi Arabia and the United Arab Emirates sponsor vendor-led academies, yet certification takes up to a year, delaying private-network deployments in logistics and manufacturing. The talent gap inflates project timelines and raises reliance on external service providers, especially for conformance testing that regulators now mandate before commercial launch.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Modular Platforms Gain Traction

Modular Instrumentation, covering PXI, VXI, and AXIe chassis, is forecast to grow at a 5.44% CAGR from 2026 to 2031, outpacing General Purpose Test Equipment despite the latter’s 35.67% test and measurement market share in 2025. Aerospace and defense primes migrate from racks of standalone instruments to PXI systems that slot oscilloscopes, digitizers, and waveform generators into a single chassis, reducing cable and floor space requirements. The test and measurement market size for PXI solutions in automotive battery validation is expanding as manufacturers seek higher channel density. Emerson’s acquisition of National Instruments accelerated the integration of LabVIEW into industrial automation, enabling closed-loop control of battery-cell formation benches.

General-purpose instruments still dominate in laboratories that require broad functionality, but margins face pressure from Chinese entrants pricing 30%-50% below Western rivals. RF and Microwave equipment remains essential as operators densify 5G networks and prototype 6G radios, sustaining demand for wide-bandwidth spectrum analyzers. Automated Test Equipment retains a stronghold in semiconductor fabs, where Advantest and Teradyne integrate AI models to cut pattern counts. Specialized instruments such as battery cyclers and signal integrity analyzers are carving out high-growth niches tied to electric vehicles and data-center power delivery. Mechanical test gear, including tensile and hardness testers, continues a steady replacement cycle in automotive and aerospace materials labs.

By Service Type: Asset Management Reshapes Economics

Calibration Services contributed 39.33% of 2025 revenue, anchored by ISO 17025 traceability mandates that obligate periodic verification of high-value instruments. However, the test and measurement market is witnessing faster growth in Asset Management and Rental Services, which are projected to expand at a 5.12% CAGR through 2031 as semiconductor fabs move to usage-based economics. Cloud dashboards now track instrument location, utilization, and calibration status, reducing idle time and enhancing return on assets. The test and measurement market size is linked to rental pools; therefore, it scales with manufacturing volatility rather than capital plans.

Repair and after-sales services remain a recurring stream, though independent labs undercut OEM pricing, especially on legacy oscilloscopes. Training and consulting gain prominence as mmWave measurements and AI-enabled optimization raise complexity. Keysight’s PathWave upgrades bundle training credits into annual licenses, ensuring customer proficiency with each revision. Nonetheless, commoditization of basic calibration drives consolidation among smaller labs lacking funds for 70 GHz network analyzer standards, prompting mergers that create regional super-labs.

By End-User Industry: Automotive Overtakes Legacy Leaders

Telecommunications and IT accounted for 28.91% of 2025 revenue, but Automotive and Transportation is forecast to grow at a 5.67% CAGR, reflecting investment in high-voltage battery packs, inverters, and onboard chargers. The test and measurement market for electric-powertrain validation is surging as Tesla and emerging Chinese brands scale gigafactories and demand integrated cyclers, isolation testers, and high-bandwidth oscilloscopes. Semiconductor and electronics manufacturing remains a core buyer because tighter design rules require more wafers to be probed and packages to be screened. Aerospace and defense spending is resilient due to avionics upgrades and radar modernization, sustaining demand for microwave signal generators.

Healthcare and medical devices focus on electromagnetic compatibility and safety, especially following the FDA's 2024 guidelines tightening. Education and research labs favor mid-range instruments due to budget constraints, while industrial automation and energy sectors use handheld meters for field commissioning of solar inverters and wind turbines. As 5G deployment plateaus in advanced economies, telecom operators pivot to software-defined networking, tempering their incremental hardware spending. Consequently, automotive validation is positioned to surpass telecom revenue share during the next planning cycle.

By Form Factor: Embedded Modules Address Edge Testing

Benchtop and rack-mounted instruments accounted for 45.76% of revenue in 2025, a testament to their feature-richness and metrology-grade accuracy for laboratory work. Yet Embedded and In-System Test Modules are projected to grow at a 5.03% CAGR, as manufacturers embed current sensors and voltage monitors directly into production lines. The test and measurement market for embedded modules is expanding as edge computing pushes measurement closer to the product, reducing downtime from offline sampling. Portable and handheld instruments support field service where ruggedness trumps bandwidth.

Modular plug-in cards, including USB oscilloscopes, appeal to universities and startups seeking lower acquisition costs. Teledyne LeCroy exemplified the trend with the 2024 WaveSurfer 4000HD series that trades some dynamic range for portability. USB-C power delivery now energizes 18-bit ADCs without external bricks, although motherboard noise limits ultra-low-level measurements. Customers, therefore, segment workloads between portable gear for installation and high-performance benchtops for precision tasks, sustaining a dual-track demand pattern within the test and measurement market.

Geography Analysis

Asia Pacific generated 32.46% of 2025 revenue, led by semiconductor clusters in Taiwan, South Korea, and mainland China and by large-scale 5G infrastructure across India and Southeast Asia. China’s 14th Five-Year Plan earmarked subsidies for domestic test-equipment development, but export controls on advanced ADCs constrained progress. Japanese exports of precision instruments climbed 12% in 2025, driven by automotive electrification and overseas demand for 5G, according to METI statistics. South Korean memory giants allocated over 30% of revenue to capital expenditures, buoying automated test-equipment orders.

North America maintains a sizeable base because the CHIPS and Science Act unlocked USD 52 billion in incentives that drew Intel, TSMC, and Samsung into new fabs in Arizona, Ohio, and Texas. These megaprojects stimulate localized demand for high-density probe cards and wafer-level metrology. Europe continues to invest under the EUR 43 billion (USD 47 billion) Chips Act, though permitting delays hold back facility starts. Germany’s automotive sector invested EUR 180 billion (USD 198 billion) in electrification through 2027, boosting demand for high-power battery cyclers.

The Middle East is forecast to post the fastest regional CAGR of 5.23% through 2031, anchored by Saudi Arabia’s USD 500 billion NEOM smart-city program, which includes semiconductor and electronics parks. The United Arab Emirates funded metrology laboratories under its Advanced Technology Research Council, upgrading calibration capacity for aerospace contractors. Turkey expanded EMC chamber capacity to meet updated conformity procedures introduced in 2024, in line with rising electronics exports. Collectively, sovereign diversification agendas translate into incremental opportunities for calibration, rental pools, and modular instrumentation across the Middle East, while Latin America and Africa trail due to weaker industrial bases.

Competitive Landscape

The competitive landscape is moderately consolidated, with the five largest suppliers controlling roughly half of global revenue in 2025. Keysight Technologies leads in RF and high-speed digital domains because its continuous bandwidth upgrades keep legacy customers on multi-year refresh cycles. Rohde & Schwarz reinforces its microwave leadership with the 2025 launch of the 500 GHz ZNA analyzer, expanding its reach into satellite and radar validation. National Instruments, now part of Emerson, has sustained software lock-in by bundling LabVIEW with industrial automation workflows since the 2023 acquisition closed.

Fortive deepened its asset-management franchise by acquiring Fluke Reliability in September 2024, adding vibration analytics and thermal imaging to its installed base. Anritsu differentiates through early 6G collaborations, including a 2024 agreement with Qualcomm to co-develop over-the-air test methods for sub-terahertz devices. These moves signal a pivot from pure hardware specifications toward software, analytics, and ecosystem depth, which creates switching costs that newer entrants struggle to match. Still, the rise of Test-as-a-Service erodes upfront margins, so incumbents are experimenting with subscription bundles that mix instruments, calibration, and cloud analytics.

Chinese manufacturers such as Rigol Technologies and GW Instek undercut Western price points by 30%-50%, giving them traction in universities and startups that value cost over premium performance. Their penetration into high-reliability aerospace and medical segments remains limited because many customers require long-term calibration traceability and stringent compliance certifications. Niche specialists like Pico Technology and Spectrum Instrumentation thrive by offering PC-based digitizers and oscilloscopes that integrate directly with open-source software stacks. Venture-backed startups are also targeting quantum computing and battery cyclers with modular platforms that emphasize rapid firmware updates. As differentiation shifts to software and services, competitive intensity is expected to increase, but the established players’ combined 50% share still gives the market a concentration score of 6.

Test And Measurement Industry Leaders

Keysight Technologies Inc.

Rohde and Schwarz GmbH and Co. KG

National Instruments Corporation

Fortive Corporation

Anritsu Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Electro Rent launched an AI-driven cloud portal that optimizes global rental fleets by matching idle test instruments with customer demand, boosting utilization rates across Asia Pacific and North America.

- May 2025: Advantest introduced generative-AI capabilities on its V93000 platform, enabling adaptive test sequencing that cuts semiconductor validation time by an estimated 20%.

- February 2025: Rohde and Schwarz expanded its R&S ZNA vector network analyzer family to 500 GHz, targeting satellite communications and automotive radar component validation.

- January 2025: Keysight Technologies announced a strategic alliance with NVIDIA to co-develop 800 Gbps and 1.6 Tbps Ethernet test solutions for AI data-center infrastructure, with joint products slated for release in H2 2025.

Global Test And Measurement Market Report Scope

The Test and Measurement Market Report is Segmented by Product (General Purpose Test Equipment (GPTE), Mechanical Test Equipment (MTE), Modular Instrumentation, RF/Microwave Test Equipment, Automated Test Equipment (ATE), Specialized Instruments), Service Type (Calibration Services, Repair/After-Sales Services, Asset Management and Rental Services, Training and Consulting), End-user Industry (Automotive and Transportation, Aerospace and Defense, Telecommunications and IT, Semiconductor and Electronics Manufacturing, Healthcare and Medical Devices, Education and Research Laboratories, Industrial Automation and Energy), Form Factor (Benchtop/Rack-Mounted Instruments, Portable/Handheld Instruments, Modular/Plug-in Cards, Embedded/In-System Test Modules), and Geography (North America, Europe, Asia Pacific, South America, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| General Purpose Test Equipment (GPTE) |

| Mechanical Test Equipment (MTE) |

| Modular Instrumentation |

| RF/Microwave Test Equipment |

| Automated Test Equipment (ATE) |

| Specialized Instruments |

| Calibration Services |

| Repair/After-Sales Services |

| Asset Management and Rental Services |

| Training and Consulting |

| Automotive and Transportation |

| Aerospace and Defense |

| Telecommunications and IT |

| Semiconductor and Electronics Manufacturing |

| Healthcare and Medical Devices |

| Education and Research Laboratories |

| Industrial Automation and Energy |

| Benchtop/Rack-Mounted Instruments |

| Portable/Handheld Instruments |

| Modular/Plug-in Cards |

| Embedded/In-System Test Modules |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordics (Denmark, Sweden, Norway, Finland) | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product | General Purpose Test Equipment (GPTE) | ||

| Mechanical Test Equipment (MTE) | |||

| Modular Instrumentation | |||

| RF/Microwave Test Equipment | |||

| Automated Test Equipment (ATE) | |||

| Specialized Instruments | |||

| By Service Type | Calibration Services | ||

| Repair/After-Sales Services | |||

| Asset Management and Rental Services | |||

| Training and Consulting | |||

| By End-user Industry | Automotive and Transportation | ||

| Aerospace and Defense | |||

| Telecommunications and IT | |||

| Semiconductor and Electronics Manufacturing | |||

| Healthcare and Medical Devices | |||

| Education and Research Laboratories | |||

| Industrial Automation and Energy | |||

| By Form Factor | Benchtop/Rack-Mounted Instruments | ||

| Portable/Handheld Instruments | |||

| Modular/Plug-in Cards | |||

| Embedded/In-System Test Modules | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Nordics (Denmark, Sweden, Norway, Finland) | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Southeast Asia | |||

| Australia | |||

| Rest of Asia Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the test and measurement market?

The sector was valued at USD 19.06 billion in 2025 and is projected to reach USD 24.27 billion by 2031.

Which segment is expanding fastest within test equipment products?

Modular Instrumentation is forecast to grow at a 5.44% CAGR between 2026 and 2031, driven by reconfigurable PXI and AXIe platforms.

How significant is automotive demand for test and measurement solutions?

Automotive and Transportation is set to register a 5.67% CAGR, outpacing telecom as electric-vehicle validation ramps up worldwide.

Which region offers the highest growth potential?

The Middle East is expected to post a 5.23% CAGR through 2031, propelled by sovereign investment in semiconductor and electronics manufacturing.

How are service models changing in the sector?

Adoption of Test-as-a-Service and rental pools is rising, causing asset management and rental services to expand at a 5.12% CAGR to 2031.

What role does AI play in modern testing?

AI-enabled design-for-test tools and adaptive sequencing reduce semiconductor validation cycles by roughly 20%, boosting throughput and yield.

Page last updated on: