Network Analyzers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

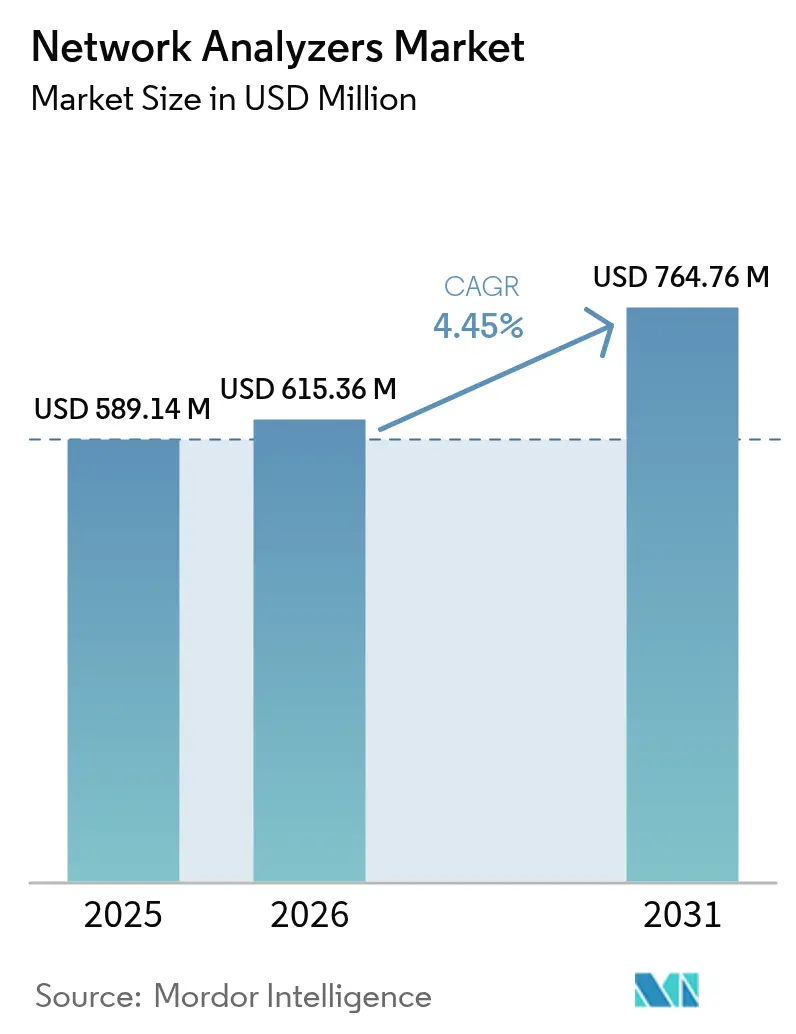

| Market Size (2026) | USD 615.36 Million |

| Market Size (2031) | USD 764.76 Million |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

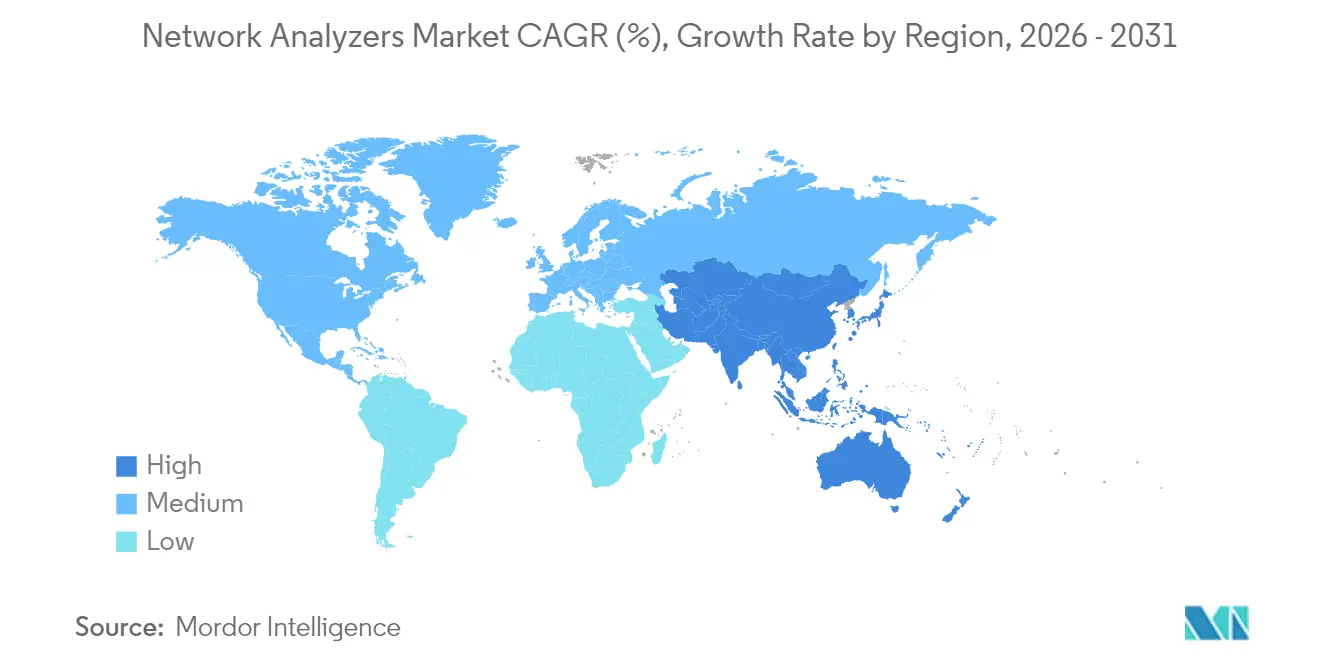

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

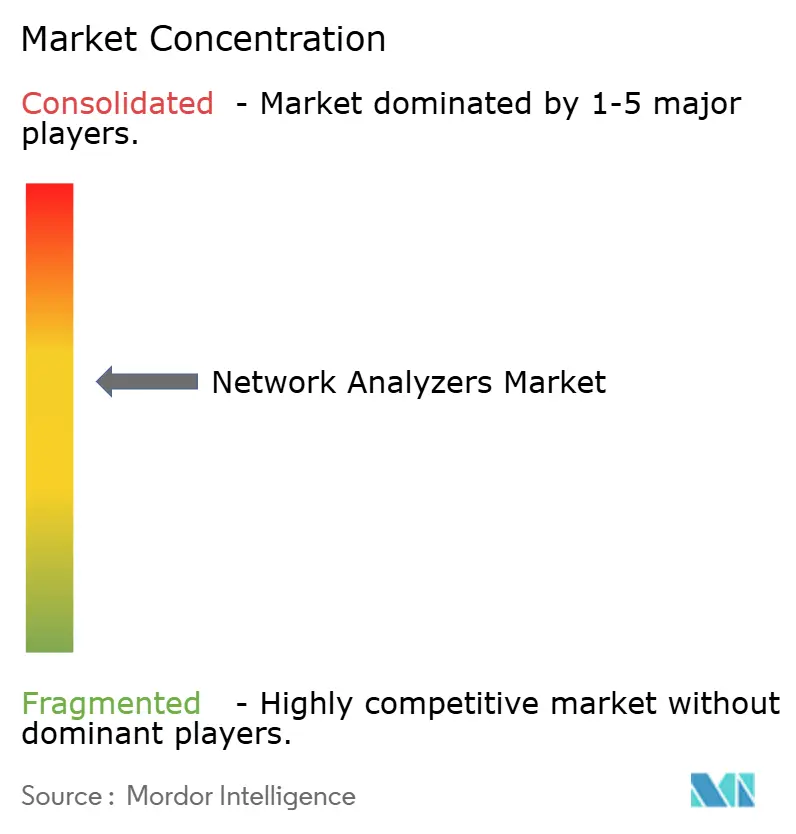

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Network Analyzers Market Analysis by Mordor Intelligence

The Network Analyzer market size is expected to grow from USD 589.14 million in 2025 to USD 615.36 million in 2026 and is forecast to reach USD 764.76 million by 2031 at 4.45% CAGR over 2026-2031. This steady advance is anchored in the rising need for precise RF measurement across 5G infrastructure, quantum-computing research, and aerospace modernization. Vector Network Analyzers (VNAs) dominate thanks to superior phase-and-magnitude capability, while modular PXI-based systems gain traction for automated lines. High-frequency (greater than 40 GHz) analyzers command premium pricing as millimeter-wave use cases multiply. Sustained R&D outlays by leading vendors and government-backed semiconductor programs in Asia-Pacific reinforce growth momentum.[1]Anritsu Corporation, “Test and Measurement | Anritsu America,” anritsu.com

Key Report Takeaways

- By product type, Vector Network Analyzers led with 60.95% Network Analyzer market share in 2025; modular PXI-based systems are projected to expand at a 6.48% CAGR through 2031.

- By frequency range, 1–20 GHz captured 43.75% of the Network Analyzer market size in 2025, while the >40 GHz bracket is set to progress at a 6.11% CAGR over 2026-2031.

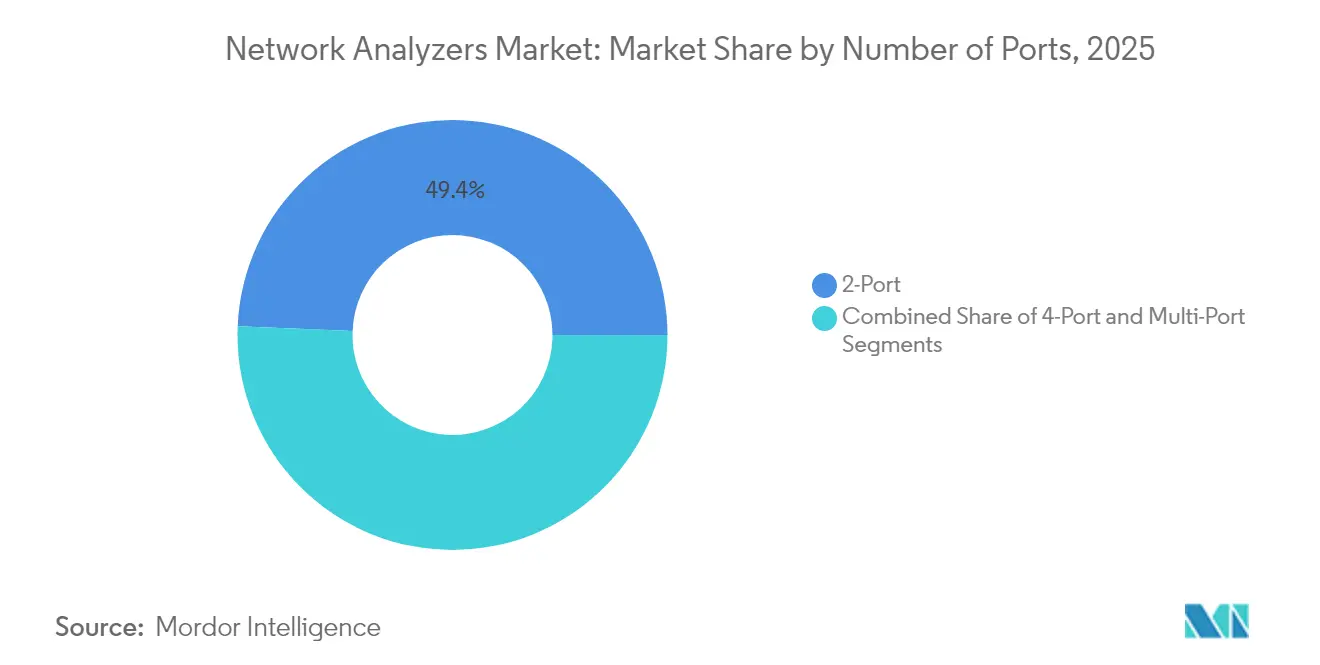

- By number of ports, 2-port instruments held 49.35% share of the Network Analyzer market size in 2025, whereas multi-port systems are forecast to grow at 5.93% CAGR to 2031.

- By application, communications commanded 36.25% of the Network Analyzer market share in 2025; quantum-computing research is expected to surge at a 5.62% CAGR through 2031.

- By geography, Asia-Pacific occupied a 32.75% share of the Network Analyzer market size in 2025, posting the highest regional CAGR at 5.42% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Network Analyzers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G/6G infrastructure rollouts | +1.2% | Global, APAC lead | Medium term (2-4 years) |

| Aerospace and defense RF modernization | +0.8% | North America, Europe, spill-over to APAC | Long term (≥ 4 years) |

| IoT device validation surge | +0.6% | Global, manufacturing hubs | Short term (≤ 2 years) |

| Nonlinear analysis for power-amplifier design | +0.4% | Global RF design centers | Medium term (2-4 years) |

| Quantum-computing cryogenic testing | +0.3% | North America and Europe research nodes | Long term (≥ 4 years) |

| Modular PXI/LXI automation | +0.5% | Global manufacturing bases | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G/6G infrastructure

Rapid 5G base-station deployment and early 6G trials demand VNAs with extended bandwidth, dynamic range, and beam-forming calibration. Keysight’s 1.6 Tbps optical-transceiver test launch shows instrument evolution paralleling network speeds. Millimeter-wave and massive-MIMO designs push >40 GHz analyzers into mainstream labs. Cryogenic options are emerging for quantum-ready 6G links, cementing high-end VNA demand. Continuous spectrum-refarming keeps replacement cycles brisk. Vendors that pair hardware with upgradable analytics software gain recurring revenue and sustain differentiation.

Expansion of aerospace and defense RF programs

U.S. and European radar upgrades require multi-port characterization of AESA modules, elevating accuracy, phase stability, and calibration rigor.[2]Source: IEEE Xplore Editorial Board, “Cryogenic VNA Measurement Papers,” ieee.org Defense primes accept premium pricing for instruments exceeding 110 GHz, boosting margins. Satellite-based EW testing widens frequency coverage needs, while cryogenic assessments for superconducting sensors open niche sales. Long qualification cycles produce predictable demand. Export-control compliance also favors established suppliers with vetted ecosystems.

Rising IoT device validation needs

Edge devices integrate multi-band radios, intensifying antenna and coexistence tests at volume. Manufacturers opt for PXI-based VNAs that blend speed, repeatability, and automation in high-mix production.[3]National Instruments, “Test and Measurement Systems,” ni.com Short product lifecycles make scalable licensing crucial. As smart-factory adoption spreads, inline RF checks become part of manufacturing execution, securing perpetual utilization of mid-range analyzers. The trend alleviates engineer scarcity by embedding guided workflows into software.

Adoption of nonlinear network analysis for PA design

5G beam-forming amplifiers and satellite payloads require behavioral models under complex modulation. Nonlinear VNAs expose memory effects and drive digital predistortion design, raising software content per analyzer. Vendors monetize add-on apps while customers cut time-to-RF-mask compliance. The shift from scalar gain plots to vector-based distortion metrics entrenches higher-value configurations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of high-frequency VNAs | -0.7% | Global, affects SMEs | Medium term (2-4 years) |

| Shortage of RF test engineers | -0.5% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Calibration-related production downtime | -0.3% | Global manufacturing hubs | Short term (≤ 2 years) |

| Volatile supply of >40 GHz connectors | -0.4% | Precision-machining centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital cost of high-frequency VNAs

Top-end analyzers priced above USD 500,000 curb adoption among universities and small labs, throttling broader penetration. Rentals alleviate cash strain yet introduce scheduling complexity and multi-year cost parity concerns. Component scarcity, especially precision waveguide couplers, keeps the bill of materials lofty. Vendors respond with modular upgrades, but overall entry prices remain elevated.

Shortage of RF test engineers

Hiring deficits, forecast to leave 58% of roles unfilled by 2030, undermine full utilization of sophisticated analyzers. High-frequency calibration, fixture design, and scripting need deep expertise that few graduates possess. Companies automate workflows, yet critical-thinking gaps persist. The talent shortfall nudges buyers toward turnkey solutions and locks SME users into service contracts, restraining unit growth despite latent need.[4]Ngram Analytics, “Keysight vs Teledyne R&D Spending,” ngram.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: VNA Dominance Drives Modular Innovation

VNAs accounted for 60.95% of the Network Analyzer market size in 2025, underpinned by their unrivaled ability to capture both magnitude and phase parameters. Scalar analyzers retain relevance for power throughput checks, but price erosion and multi-function firmware make VNAs the default choice for broadband characterization. Emergent PXI chassis lower per-slot cost and integrates seamlessly into automated handlers, enabling manufacturers to expand capacity without duplicating full-rack instruments. Keysight’s AI-backed measurement suites illustrate how software updates lengthen hardware life cycles, converting capital outlay into recurring license streams.

Modularity also appeals to defense primes needing field-deployable test rigs. Engineers can swap frequency-extension heads while preserving base modules, optimizing asset utilization. Software-defined paths foster application-specific packages, from satellite payload verification to quantum-bit readout, thereby broadening addressable verticals without redesigning chassis. As open-standard PXI/LXI ecosystems mature, second-tier vendors gain entry, intensifying competition yet expanding overall shipment volume of mid-range systems.

By Frequency Range: Millimeter-Wave Growth Accelerates

The 1–20 GHz band delivered 43.75% of the Network Analyzer market share in 2025, owing to entrenched telecom and automotive radar use. These units anchor production lines that prize speed and stability over bleeding-edge bandwidth. Conversely, the >40 GHz tier, though smaller, is projected to log a 6.11% CAGR through 2031, fueled by 5G FR2, 77 GHz automotive radar, and emerging 6G explorations. Price premiums persist as waveguide adapters, frequency-extension modules, and on-wafer probes carry high precision-machining costs.

Quantum-computing demands stretch analyzers to deliver ultra-low noise across broad spans while operating at cryogenic temperatures. Such niche yet high-value orders improve average selling prices and buffer margin risk. Manufacturers that bundle waveguide calibration kits and de-embedding software shorten setup time, drawing loyalty from advanced labs. Sub-1 GHz instruments remain staples for power-electronics EMC checks, but incremental revenue shifts toward millimeter-wave portfolios where differentiation is steepest.

By Number of Ports: Multi-Port Systems Enable Complex Testing

2-port systems represented 49.35% of the Network Analyzer market size in 2025, thanks to pervasive component-level uses and cost efficiency. Yet system-level validation forces designers to evaluate multi-antenna arrays in situ, pushing demand for 4-port and higher models. Multi-port analyzers are set to notch the briskest expansion at 5.93% CAGR to 2031, leveraging synchronized receivers and phase-locked sources for simultaneous S-parameter sweeps across integrated subsystems.

Automotive OEMs apply 8-port VNAs to probe radar modules under thermal cycling. Likewise, base-station OEMs validate massive-MIMO panels faster by capturing beam-forming matrix elements in one pass. While higher port counts inflate calibration complexity, fixture innovations and embedded reference standards mitigate setup hurdles. Modular port-extension cards preserve upgrade flexibility, letting customers stage investments as architecture complexity grows.

By Application: Communication Leadership Faces Quantum Challenge

Communications retained 36.25% Network Analyzer market share in 2025, reflecting unrelenting fiber-optic and wireless infrastructure upgrades. Dense wavelength-division multiplexing and PAM4 modulation oblige tighter return-loss and group-delay controls, embedding VNAs within optical-component production. Aerospace and defense remain stable yet premium buyers, budgeting for top-spec dynamic range and ruggedized form factors. Electronics manufacturing, encompassing smartphones and wearables, sustains mid-tier sales.

Quantum-computing research, the fastest-rising slice at 5.62% CAGR, mandates cryogenic operation and phase-noise performance unattainable by standard gear. Vendors innovate with superconducting cabling and noise-floor extensions, carving a lucrative sub-niche. Academic labs and national research centers form early adopters, but commercialization prospects hint at longer-term volume. Medical implants and industrial IoT add incremental demand, particularly where multi-band antennas require validation under constrained form factors.

Geography Analysis

Asia-Pacific commanded 32.75% of the Network Analyzer market size in 2025 and is projected to expand at a 5.42% CAGR through 2031. China’s drive for semiconductor self-reliance funds new RF-lab buildouts, while South Korea’s memory giants and Japan’s quantum-computing consortia spur high-frequency instrumentation orders. Government grants lower acquisition barriers, escalating cumulative shipments across PXI and benchtop categories.

North America follows with robust aerospace and defense allocations underpinning demand for performance-tier analyzers. Keysight’s USD 919 million R&D bill illustrates an entrenched innovation culture, and its forthcoming acquisition of Spirent boosts end-to-end validation coverage. Quantum-computing hubs in the United States and Canada drive specialized cryogenic VNA needs, while Mexico’s contract manufacturing uptick pulls mid-range systems into new facilities.

Europe leverages automotive electronics validation, led by Germany’s radar programs and France’s satellite payload development. Industry 4.0 mandates drive factory-floor PXI deployments, and strict CE/EMC compliance sustains calibrator sales. The United Kingdom’s aerospace sector and Italy’s 5G rollouts add to baseline demand. Though currency fluctuations affect capex cycles, EU research grants partially cushion procurement budgets.

Regulatory Landscape

Network analyzer demand is shaped by RF device compliance regimes and the measurement standards used for certification and acceptance testing. In the United States, the FCC equipment authorization framework and spectrum rules under 47 CFR Part 2 and Part 15 (including Part 15 Subpart E for U-NII devices) drive test requirements such as emission limits and DFS validation in the 5 GHz bands, keeping calibrated RF metrology central to lab and production workflows. FCC 24-125, effective May 5, 2025, expanded unlicensed very low power operations across the full 6 GHz band (5.925-7.125 GHz), which provides a clear trigger for additional mid-band test activity.

On the standards side, laboratories and OEMs are aligning procedures to updated IEC documents that formalize measurement uncertainty and related methods used alongside VNAs. IEC TS 61169-1-7:2025 (published August 2025) defines uncertainty specifications for insertion-loss measurements on RF connectors using VNAs, reinforcing the need for traceable calibration and consistent fixtures in connector and interconnect validation. IEC 61290-3-2:2026 (published June 19, 2026) also updates test method standardization in adjacent optical-noise-figure measurements, which can affect mixed RF and optical component test environments that share instrumentation and metrology practices.

Value Chain Analysis

The network analyzer value chain begins with upstream RF and microwave component ecosystems (high-frequency ADC/DACs, synthesizers, mixers, low-noise receivers, FPGAs/SoCs, precision clocks), alongside mechanical and interconnect inputs such as precision connectors, cables, and waveguide assemblies that become more critical above 40 GHz. These inputs feed instrument OEM design and integration, including benchtop VNAs and modular PXI/LXI architectures, followed by calibration, verification, and application software packaging (automation, de-embedding, nonlinear analysis). As users push into mmWave and multiport test, this software layer increasingly differentiates platforms.

Downstream, instruments move through direct sales and channel partners into communications OEMs, aerospace and defense primes, automotive electronics programs, and research labs, with service organizations and rental houses expanding access for cost-sensitive users. Recent product activity illustrates how OEMs extend capability and reduce friction across the chain: Siglent released the SNA5000X-E two-port VNA (6.5 GHz) positioned for both R&D and production test, while Anritsu introduced the Tenzor VNA platform at IMS 2026 with source-per-port architecture and integrated AI features. Together, these developments point to more automated setup and higher-throughput workflows that reduce operator burden and calibration time in complex test environments.

Competitive Landscape

The Network Analyzer market exhibits moderate concentration. Keysight, Rohde & Schwarz, and Anritsu anchor top-tier share through broad frequency coverage, deep software stacks, and extensive support networks. Keysight’s pending USD 1.46 billion Spirent buy accelerates its shift toward integrated, automated solutions that span physical-layer to security testing.

Second-tier firms such as Advantest exploit modular PXI/LXI niches, bolstered by partnerships like its 2025 stake in Micronics Japan to streamline probe-card supply. Emerging vendors leverage software-defined architectures to offer cost-optimized VNA cards, winning footholds among small labs and contract manufacturers. Rental houses expand inventory to cater to cost-averse users, indirectly widening exposure for leading OEMs.

Competitive levers pivot on measurement speed, calibration wizardry, and AI-driven analytics rather than raw hardware specs alone. Vendors embed subscription-based feature unlocks, securing recurring revenue and deeper customer lock-in. As millimeter-wave and quantum domains mature, alliances with probe-station, cryostat, and fixture specialists become pivotal for delivering turnkey solutions.

Network Analyzers Industry Leaders

Tektronix Inc.

Keysight Technologies Inc.

Transcom Instrument Co. Ltd.

Anritsu Corporation

Rohde & Schwarz GmbH & Co KG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is opening around workflow automation and guided measurement for high-mix production and advanced R&D, particularly where shortages of RF test engineers and calibration downtime constrain utilization. Platform upgrades that reduce setup complexity and shorten time-to-measurement create room for software-led differentiation (automation scripts, calibration wizards, de-embedding, nonlinear characterization) that can be deployed across installed hardware, aligning with the market shift toward subscription and feature-unlock models referenced in the competitive landscape.

Recent launches provide concrete signals of where buyers are tightening requirements on onboarding and repeatability. In June 2026, Anritsu introduced the Tensor MS466XXA VNA platform with an integrated AI engine aimed at natural-language configuration and automated test setup and guidance, targeting faster onboarding and repeatable measurement execution in complex RF test plans. In April 2026, Siglent released the SNA5000X-E (9 kHz to 6.5 GHz) with integrated time-domain functions designed for both R&D and production testing, which reflects demand for multi-function instruments that increase bench utilization and reduce the need for multiple dedicated boxes in space- and budget-constrained labs.

Recent Industry Developments

- June 2026: Anritsu introduced the Tensor MS466XXA (Tenzor) vector network analyzer platform with integrated AI capabilities, including guided setup and automation features highlighted around IMS 2026. The launch targets faster measurement configuration and more consistent execution in complex RF test scenarios, reinforcing the shift toward software-led differentiation in VNA platforms.

- March 2026: Rohde & Schwarz acquired Software Radio Systems (SRS), expanding its software-defined radio expertise for mobile communications. The deal strengthens the company's ability to pair RF instrumentation with modern 5G-focused software stacks, supporting more integrated validation workflows across lab and system test.

- September 2025: Rohde & Schwarz announced new frequency models up to 54 GHz for its R&S ZNB3000 vector network analyzer family. Extending frequency coverage supports higher-bandwidth wireless and radar characterization needs and increases the addressable set of mmWave design and production applications for the platform.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue from network analyzers used to measure RF and microwave network behavior during design, production test, and field verification across major end-use environments.

We exclude general RF test gear that does not perform network analysis functions, along with calibration kits, accessories, and standalone software sold without an instrument.

Segmentation Overview

- By Product Type

- Vector Network Analyzers (VNA)

- Scalar Network Analyzers (SNA)

- By Frequency Range

- Less than 1 GHz

- 1 - 20 GHz

- 20 - 40 GHz

- Greater than 40 GHz

- By Number of Ports

- 2-Port

- 4-Port

- Multi-Port (Greater than 4)

- By Application

- Communication

- Aerospace and Defense

- Automotive

- Electronics Manufacturing

- Research and Education

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by anchoring the model in public signals that tend to stay consistent year to year. We review government spectrum and communications publications, such as FCC materials and ITU documentation, and where available, trade data series using HS-code based export and import trends to track equipment flow.

We also use sources such as IEEE and other peer reviewed journals to capture frequency-band adoption themes, standards bodies like 3GPP for 5G test requirements, and public aerospace and defense budget documents to infer test intensity and program timing. Company filings, product catalogs, investor decks, and reputable press releases are then used to map product families (VNA versus SNA), typical frequency ranges, and the main application drivers. When needed, we use paid subscription sources for company financials and a patent database to cross-check activity levels and product roadmap direction. These examples are illustrative only, and other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what desk indicators cannot fully explain, especially price mix shifts and buying cycles across end users. We speak with instrument OEMs, component and module test teams, distributors, and lab-level users across APAC, EMEA, and the Americas. The interviews help confirm demand pockets by frequency range, port count, and application needs, and they refine the assumptions used in the final triangulation.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 20% | APAC: 51% |

| Mid tier: 48% | Functional/Unit leaders: 25% | EMEA: 31% |

| Smaller Players: 22% | Managers: 55% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where the demand pool is reconstructed from RF test intensity across key application areas, then converted into instrument revenue using validated adoption and replacement patterns. Because network analyzers are tightly linked to RF design and verification, inputs that matter include 5G and advanced wireless rollout pace, higher frequency testing needs (20-40 GHz and above 40 GHz), the mix shift between benchtop and modular PXI systems, typical port configurations used in production lines, and budget timing in aerospace and defense programs.

To keep the model grounded, we corroborate the totals with selective bottom-up approximations, such as rolling up sample supplier revenue exposure to network analyzers, and using channel checks on unit volumes and average selling price bands by frequency range. When a bottom-up view is incomplete, for example smaller local suppliers or lab procurement that is not well disclosed, gaps are handled by applying conservative penetration ranges that were stress-tested during primary discussions.

For forecasting, scenario analysis is used so the baseline track can be adjusted for known program delays and faster-than-expected high-frequency adoption, which is common in this instrument category. Assumptions on ASP progression and mix are reviewed with experts, then applied consistently across regions to control for currency and timing effects.

Data Validation & Update Cycle

Validation is done through several checks so the final numbers do not rely on a single data stream. Model outputs are compared with independent signals such as frequency band adoption trends, public R&D and defense spending direction, and trade flow movement where relevant, and then anomalies are reviewed before sign-off.

We run variance checks across region totals, application shares, and implied pricing to ensure the results align with real buying behavior. Follow-up calls are triggered if any value appears inconsistent with the interview consensus. Reports are refreshed annually, and interim updates are done when a material event changes the demand picture. Before delivery, the analysis gets a final pass so clients receive the latest updated view.

Mordor Intelligence's Network Analyzers Market Size Measured Against Other Published Estimates

Published market sizes for network analyzers can vary more than clients expect because the product boundary is not always handled the same way, and because pricing and mix assumptions can shift the total quickly. Differences also stem from which year is treated as the baseline and how exchange rates are applied when revenues are global.

Evidence such as the split of demand by frequency range and port configuration, alongside checks against application-level spending signals, keeps Mordor Intelligence's estimate tied to instrument revenues rather than broader RF test spending. In other publications, gaps often come from counting adjacent test equipment categories, using aggressive unit growth from early 5G lab activity, or not separating modular systems from benchtop instruments within the ASP logic.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 615.36 M (2026) | |

| Industry Publisher A | USD 618.90 M (2025) | Uses an earlier base setup and a longer forecast window, and it can also broaden the demand discussion into maintenance and general verification activity, which may lift implied unit growth and pricing mix. |

| Market Platform B | USD 522.30 M (2025) | Likely applies a narrower revenue capture for network analyzers and a tighter ASP range by frequency class, which can undercount high frequency instruments where pricing is typically higher. |

Across the table, the spread is mainly explained by boundary choices and how pricing and mix are carried forward year to year. When scope is kept to network analyzers only, and the model is tied back to frequency range demand and application spending signals, the resulting value stays transparent and repeatable for planning discussions.

Key Questions Answered in the Report

What is the 2026 value of the Network Analyzer market?

It is USD 615.36 million, rising to USD 764.76 million by 2031 at a 4.45% CAGR.

Which product type leads current sales?

Vector Network Analyzers command 60.95% share due to superior phase-and-magnitude measurement capability.

Which frequency band is growing fastest?

The >40 GHz segment is projected to log a 6.11% CAGR between 2026 and 2031, propelled by millimeter-wave 5G and 6G work.

Why is APAC the largest regional market?

Concentrated semiconductor fabrication, aggressive 5G rollouts, and government tech incentives give APAC 32.75% share and the highest 5.42% regional CAGR.

What main risk could slow expansion?

High capital cost of premium VNAs and a projected 58% shortfall in qualified RF test engineers pose notable constraints.

Which company recently pursued major M&A activity?

Keysight Technologies is finalizing a USD 1.46 billion acquisition of Spirent Communications to broaden automated test capabilities.

Page last updated on: