Termite Control Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

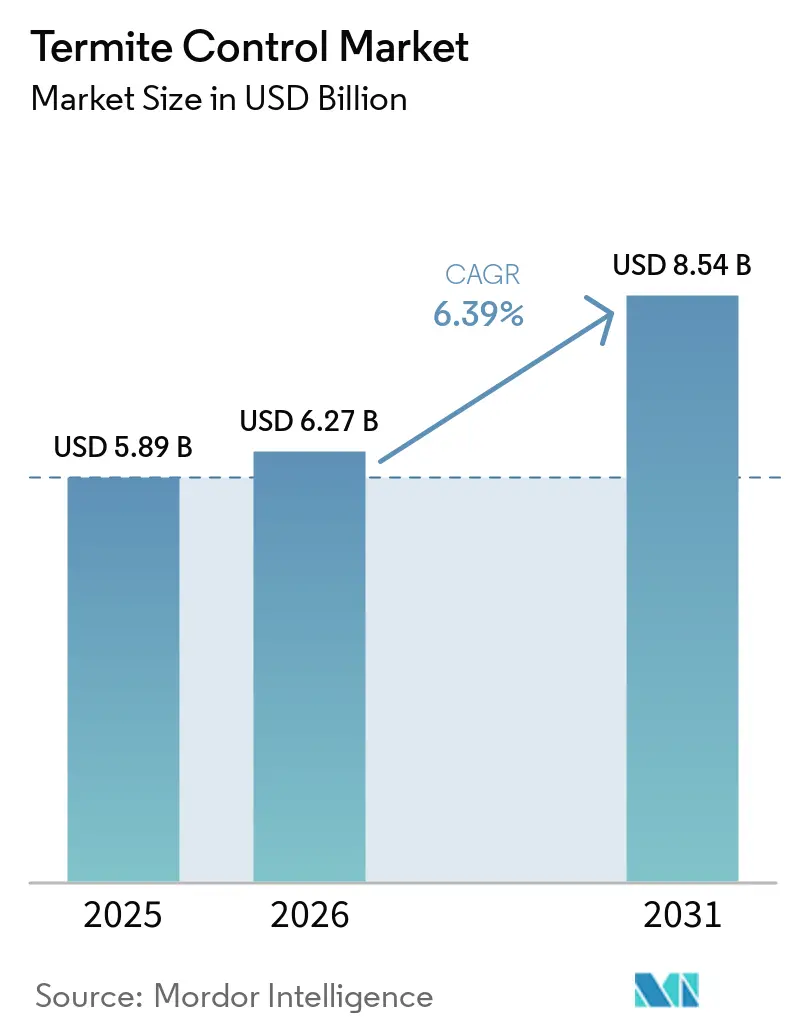

| Market Size (2026) | USD 6.27 Billion |

| Market Size (2031) | USD 8.54 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Termite Control Market Analysis by Mordor Intelligence

The Termite Control Market size is expected to grow from USD 5.89 billion in 2025 to USD 6.27 billion in 2026 and is forecast to reach USD 8.54 billion by 2031 at 6.39% CAGR over 2026-2031. Rising remediation expenses, insurance-driven inspection mandates, and expanding IoT monitoring deployments are shifting the industry from episodic treatment toward data-guided preventive programs. Subterranean species continue to dominate spending because they thrive in moist soils that prevail across the Asia-Pacific and the southeastern United States. Chemical soil barriers still hold the largest revenue share, yet bait systems and physical barriers are gaining ground as regulators phase out legacy actives and building owners prioritize lower-toxicity options. Consolidation among service providers is accelerating, with global operators leveraging digital platforms to cross-sell annual warranties and streamline field logistics.

Key Report Takeaways

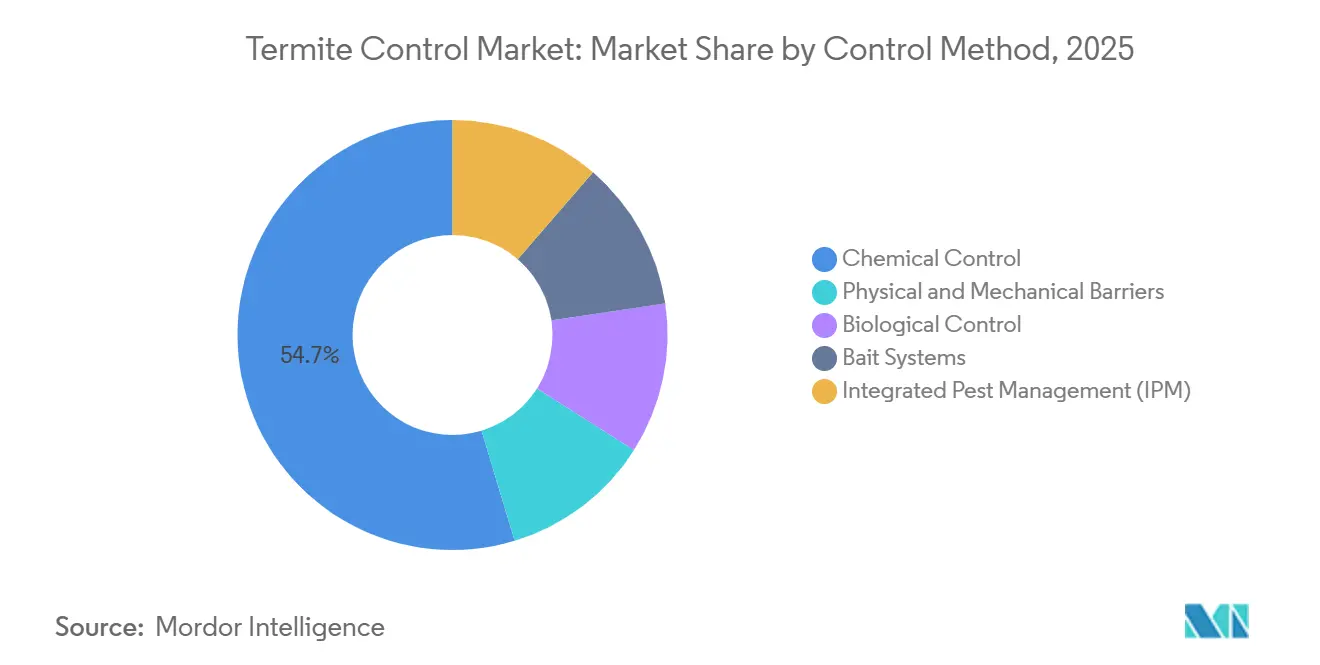

- By control method, chemical solutions retained 54.67% of the global termite control market share in 2025, while bait systems are forecast to expand at a 6.92% CAGR from 2026 to 2031.

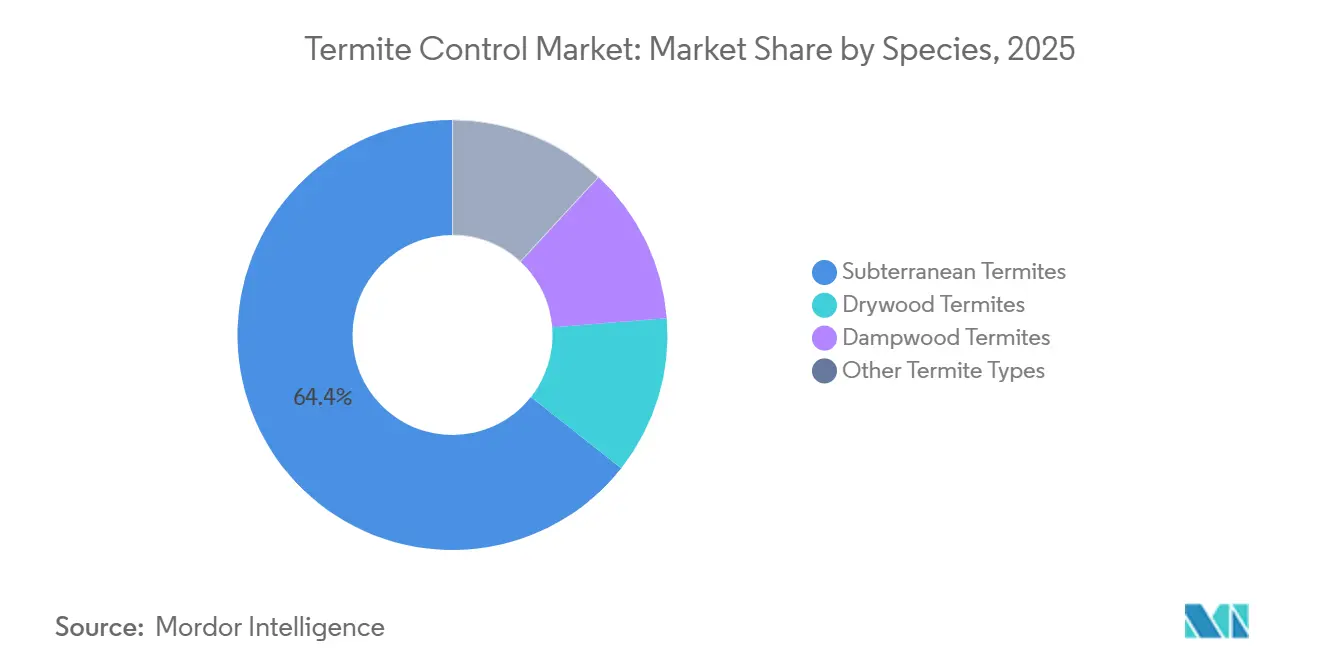

- By species, subterranean termites commanded 64.37% of the global termite control market size in 2025 and are projected to grow at a 7.02% CAGR through 2026 to 2031.

- By application, public infrastructure recorded the fastest trajectory at a 7.22% CAGR through 2026 to 2031, whereas residential properties accounted for 41.91% of 2025 revenue.

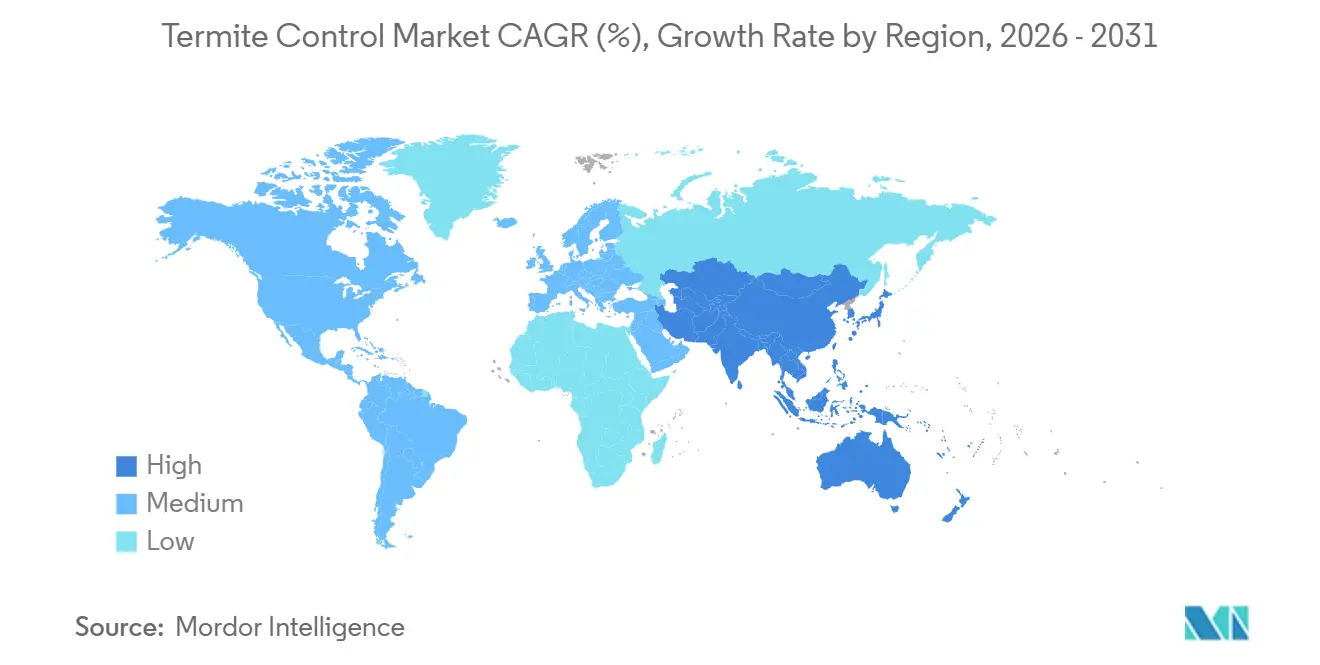

- By geography, Asia-Pacific led with 44.93% of the global termite control market share in 2025 and is set to post a 7.14% CAGR through 2026 to 2031 during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Termite Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing structural-damage remediation costs | +1.20% | Global, concentrated in North America, Australia | Medium term (2-4 years) |

| Construction boom in termite-prone emerging markets | +1.50% | Asia-Pacific core (China, India, ASEAN), spillover to MEA | Long term (≥4 years) |

| Insurance-mandated termite inspections for mortgaged assets | +0.90% | North America, Australia, select EU markets | Short term (≤2 years) |

| Climate-change driven pole-ward termite range expansion | +0.80% | North America (northward into Canada), Europe (Mediterranean expansion), East Asia | Long term (≥4 years) |

| Rapid adoption of smart/IoT termite monitoring platforms | +1.10% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Rise of engineered-timber high-rise projects requiring preventive barriers | +0.60% | North America, Europe, Japan, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Structural-Damage Remediation Costs

In the United States, annual repair bills due to termite damage have reached significant levels. This figure does not account for the indirect losses, such as property devaluation and increased insurance premiums. In humid regions, an aging housing stock with postponed maintenance heightens vulnerability to termite damage. As a result, lenders are tightening their inspection criteria, and insurers are offering premium discounts for active warranties. Municipal agencies are now incorporating multi-year termite contracts into their budgets for bridge, pole, and public-building maintenance. This shift turns what was once discretionary spending into planned capital outlays. Consequently, detection rates have risen, remediation spending has increased, and the global termite control market has expanded, with preventive treatments now seen as a financing necessity. Service providers adept at quantifying avoided repair costs are securing long-term contracts with both public and private owners.

Construction Boom in Termite-Prone Emerging Markets

India's National Infrastructure Pipeline and China's Belt and Road Initiative are investing significant resources into transport corridors and housing projects in tropical and subtropical regions. In Vietnam, Indonesia, and Thailand, new building codes mandate pre-construction soil termiticides or physical barriers for structures intended to last over two decades. Developers now view termite protection as a quality metric, on par with energy efficiency. This shift is prompting global termite control vendors to localize their supply chains and certification programs. Suppliers of stainless-steel mesh and graded-stone barriers are experiencing increased demand. These non-chemical solutions resonate with green-building labels, which are prevalent in premium urban projects. Looking ahead, the combination of expanding floor space and rising specification rates is set to drive the continued growth of the global termite control market in the Asia-Pacific region.Climate-Change Driven Pole-Ward Termite Range Expansion

Climate-Change Driven Pole-Ward Termite Range Expansion

Modeling conducted by the French Agricultural Research Center for International Development indicates that an increase in temperature significantly enhances termite species richness, enabling destructive subterranean species to survive in regions far beyond their historical ranges[1]University of Florida, “Behavioral Bait Aversion,” ufl.edu . Field studies from Auburn University confirmed that Formosan termite colonies are capable of surviving winters in regions previously considered unsuitable, such as Tennessee. This northward spread is also evident in areas of central France and southern Germany. Consequently, new quarantine rules for Reticulitermes have been introduced in the European Union. Regions previously regarded as low-risk are now experiencing increased demand for inspections, bait installations, and educational programs for builders. This shift is driving additional revenue into the global termite control market. While regulatory frameworks often lag behind biological developments, private insurers and mortgage lenders are implementing their own inspection requirements. These measures are accelerating market penetration as formal revisions to building codes progress through legislative processes.

Rapid Adoption of Smart/IoT Termite Monitoring Platforms

Wireless sensors, embedded in bait stations or along slab perimeters, stream data on vibrations and moisture. This technology can flag activity significantly earlier than traditional visual checks. In a pilot conducted across commercial real estate properties in the United States, targeted interventions at confirmed hotspots led to a notable reduction in treatment spending. Technicians now use remote dashboards to triage alerts and optimize routing, alleviating labor bottlenecks common in traditional monthly inspections. Australia's Commonwealth Scientific and Industrial Research Organization has begun to recognize acoustic sensors as valid evidence in pre-purchase reports. With regulators and insurers now accepting digital proof of protection, Internet of Things systems are transitioning from a novelty for early adopters to a mainstream specification, broadening the scope of the global termite control market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental bans on legacy termiticides | -0.70% | North America (California, New York), EU, Australia | Short term (≤2 years) |

| Health and indoor-air-quality concerns among homeowners | -0.40% | Global, concentrated in North America, Western Europe, Japan | Medium term (2-4 years) |

| Accelerating genetic and behavioral resistance to chemical actives | -0.50% | Global, concentrated in Hawaii, Florida, Taiwan, Japan | Medium term (2-4 years) |

| High up-front cost of smart bait and monitoring contracts in price-sensitive regions | -0.30% | Southeast Asia, Latin America, Middle-East and Africa, rural North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Bans on Legacy Termiticides

In recent years, California prohibited the residential use of bifenthrin and chlorpyrifos. Meanwhile, the European Union initiated a review of fipronil due to concerns over its aquatic toxicity. Around the same period, regulatory authorities in Australia canceled the use of several organophosphates. As a result, service firms are now faced with the challenge of retraining their crews, investing in precision-injection rigs, and convincing budget-conscious homeowners to opt for more expensive chemical treatments or physical barriers. While manufacturers are hastening the reformulation of their products, they find that amending labels and validating in the field require significant capital and time investments. This has led to a compression in near-term profits, slowing the growth of the global termite control market until operators adjust their service prices and customers become accustomed to the new range of chemicals.

Accelerating Genetic and Behavioral Resistance to Chemical Actives

Hawaiian Coptotermes colonies, influenced by increased cytochrome P450 enzyme activity, now demonstrate significantly higher tolerance to fipronil compared to baseline strains. In both Florida and Taiwan, technicians are required to rotate matrices or combine active ingredients due to bait aversion behavior, which reduces the effectiveness of chitin-inhibitor stations[2]CIRAD, “Climate Change and Termite Range Expansion,” cirad.fr. The efficacy erosion shortens re-treatment intervals and inflates product usage, lifting customer costs that may deter uptake in price-sensitive regions. Chemical innovators are exploring sodium-channel modulators and mitochondrial disruptors, yet regulatory clearance can take up to a decade. This latency leaves a temporary capability gap that weighs on the Global termite control market momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Control Method: Bait Systems Gain Ground on Chemical Incumbents

Chemical Control held 54.67% of 2025 revenue, reflecting decades-long dominance in pre-construction soil barriers and corrective perimeter drenches. The segment’s share edges downward as regulators restrict organophosphates and pyrethroids, nudging property managers toward lower-toxicity alternatives. Bait systems are expanding at a projected 6.92% CAGR between 2026 and 2031. In the global termite control market, Sentricon and Trelona ATBS, utilizing chitin-synthesis inhibitors, can collapse colonies within a relatively short period. These methods also meet indoor-air and green-building standards, making them suitable for hospitals, schools, and Leadership in Energy and Environmental Design-certified projects. Meanwhile, physical barriers like stainless-steel mesh, polymer films, and graded stone are gaining popularity in regions with building codes that mandate chemical-free solutions. However, their installation costs confine them to high-value structures.

Smart bait stations, now equipped with vibration sensors, relay real-time feeding data. This innovation not only minimizes technician callouts but also enhances subscription renewals. A notable shift in chemical approach is evident with BASF’s Termidor HE: this formulation reduces active-ingredient loading significantly without compromising efficacy, making it easier to adhere to stringent residue limits. While biological controls like Metarhizium anisopliae are still in the pilot phase due to inconsistent field persistence, integrated pest-management programs are already incorporating sanitation, moisture management, and targeted spot treatments to reduce chemical dependency. As property owners recognize the value of life-cycle cost calculations, there's a noticeable shift in demand towards predictive programs over traditional blanket soil drenches, leading to a transformation in product portfolios within the global termite control market.

By Species: Subterranean Termites Dominate Damage and Spending

Subterranean termites captured 64.37% of 2025 revenue, driven by large colony sizes and their ability to navigate significant distances underground. This species group is forecast to post a 7.02% CAGR between 2026 and 2031. Coastal belts, where drywood termites predominantly reside, require localized fumigation or heat treatments. These treatments are relatively expensive but are limited to smaller geographic areas. Dampwood termites, which are less prevalent, are generally managed through moisture remediation instead of chemical solutions, which reduces their commercial potential.

As climate change extends the range of subterranean termites, Formosan termites have started appearing in Tennessee and the Carolinas. This has resulted in updates to building codes, requiring soil treatments in areas that were previously exempt. In Europe, the northward spread of Reticulitermes lucifugus has led regulators to classify it as a quarantine pest. This growing threat has increased demand for inspections and the use of bait stations, ensuring subterranean termites continue to dominate the global termite control market. Manufacturers are focusing their research and development efforts on creating new solutions to address genetic resistance, prioritizing these widespread species due to their significant economic impact.

By Application: Public Infrastructure Emerges as Fastest-Growing Segment

Residential premises generated 41.91% of 2025 revenue. Public infrastructure is rapidly becoming the fastest-growing segment, even as numerous single-family homes renew their warranties periodically, clocking a 7.22% CAGR through 2026 to 2031. Municipalities are grappling with termite damage affecting utility poles, bridge timbers, and heritage assets. The cost of replacing a termite-compromised utility pole is significantly higher than that of preventive treatment. This stark difference is prompting states to allocate budgets for proactive measures like borate pressure dipping and in-ground barrier sleeves.

Commercial and industrial entities are increasingly opting for bundled pest contracts, integrating termite monitoring with food safety and pharmaceutical contamination protocols. Logistics hubs are on alert for termite activity in wooden pallets, while operators of data centers are safeguarding cable trays and raised floors. In Brazil and Australia, agricultural estates are treating eucalyptus and sugarcane fields for termites, though their spending remains cyclical and sensitive to commodity prices. Given this backdrop, the infrastructure sector emerges as the frontrunner, charting the most consistent growth trajectory in the global termite control market, buoyed by public budgets and disaster-resilience grants.

Geography Analysis

Asia-Pacific anchored 44.93% of 2025 revenue and is projected to grow at 7.14% CAGR between 2026 and 2031. As tropical humidity, monsoon moisture, and rapid urbanization converge, Asia-Pacific solidifies its dominance in the global termite control market. Chinese construction standards mandate pre-construction soil treatments, while states like Maharashtra and Karnataka in India now require physical barriers for mid-rise affordable housing. In Vietnam and Indonesia, developers incorporate annual monitoring into strata fees, creating a steady revenue stream for service firms. With construction pipelines showing no signs of slowing down in the foreseeable future, the region's lead in the global market remains unchallenged.

North America, with the United States Department of Veterans Affairs expanding mandatory inspection counties in the near future, ranks second in market value. This expansion has turned many previously discretionary treatments into essential mortgage closing requirements. Warmer winters have enabled subterranean termites to migrate into the Midwest and southern Canada, regions where building codes have traditionally overlooked termite barriers. In response to emerging risk zones, insurance carriers are now mandating proof of coverage, spurring a rise in smart monitoring solutions equipped with remote documentation features. Furthermore, Canadian provinces are contemplating code amendments, potentially introducing a new layer of demand in the coming years.

Europe witnesses moderate growth, predominantly in Mediterranean nations where Reticulitermes activity is on the rise. European Union phytosanitary regulations mandate builders to integrate termite protection in new constructions south of a specific latitude. In Spain and Italy, heritage masonry is being retrofitted with stainless-steel shields, as chemical soil treatments face environmental challenges in densely populated historic centers. Meanwhile, the northern spread of termite risks has led German and French building authorities to initiate hazard mapping studies.

In South America, Brazil takes the lead, with plantations using preventive termiticides to protect timber and irrigation systems. Argentine urban centers are now specifying borate pre-treatments in tender documents for social housing blocks. While the Middle-East and Africa have been slow to adopt, megaprojects in the Gulf Cooperation Council, from Saudi Vision housing initiatives to Qatari logistics parks, are now mandating termite barriers to meet international insurer standards. Japan, despite its maturity in the market, continues to command a premium per-capita spend. This is largely due to stringent Japanese construction standards, which necessitate periodic inspections and the renewal of chemical zones. These regional dynamics collectively underscore the diverse growth trajectory of the global termite control market.

Competitive Landscape

The termite control market is moderately fragmented. Technology serves as a pivotal differentiator. Operators utilizing Internet of Things sensors and mobile applications secure substantial commercial portfolios, thanks to their ability to digitally document compliance and minimize emergency callouts. In response, smaller independent firms carve out niches in heritage conservation and physical-barrier installation, areas that require artisanal expertise and are less susceptible to price competition. Chemical suppliers are ascending the value chain, leveraging patented actives and micro-encapsulation techniques to prolong product efficacy; a prime example being BASF’s 2026 introduction of Termidor HE. Meanwhile, biotechnology startups are experimenting with RNA-interference baits targeting crucial termite genes, although a commercial launch remains several years away, awaiting regulatory approval.

Termite Control Industry Leaders

Bayer AG

Rentokil Initial plc

Rollins, Inc.

Terminix Global Holdings

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Rollins Inc. is set to acquire Romex Pest Control, expanding its Southwestern United States presence by adding 18,000 customer accounts. This acquisition will strengthen its service network, enhance regional market coverage, and intensify competition in the global termite control services market.

- March 2026: BASF Agricultural Solutions has finalized its acquisition of AgBiTech. This move is set to accelerate the scaling and wider adoption of biological solutions, underscoring BASF's dedication to providing farmers with enhanced and varied insect control alternatives.

Global Termite Control Market Report Scope

Termite control refers to the systematic prevention, management, and elimination of termite infestations that damage wood, crops, and infrastructure. It involves chemical treatments, bait systems, biological methods, and physical barriers to protect residential, commercial, agricultural, and public structures. Effective termite control reduces economic losses, safeguards property value, and ensures long-term sustainability by integrating modern pest management practices with environmentally responsible approaches.

The Global Termite Control Market is segmented by control method, species, application, and geography. By Control Method, the market is segmented into Chemical Control, Physical and Mechanical Barriers, Biological Control, Bait Systems, and Integrated Pest Management (IPM). By Species, the market is segmented into Subterranean Termites, Drywood Termites, Dampwood Termites, and Other Termite Types. By Application, the market is segmented into Residential, Commercial and Industrial, Agricultural Lands, and Public Infrastructure. The report also covers the market size and forecasts for the Global Termite Control Market in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Chemical Control |

| Physical and Mechanical Barriers |

| Biological Control |

| Bait Systems |

| Integrated Pest Management (IPM) |

| Subterranean Termites |

| Drywood Termites |

| Dampwood Termites |

| Other Termite Types |

| Residential |

| Commercial and Industrial |

| Agricultural Lands |

| Public Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Control Method | Chemical Control | |

| Physical and Mechanical Barriers | ||

| Biological Control | ||

| Bait Systems | ||

| Integrated Pest Management (IPM) | ||

| By Species | Subterranean Termites | |

| Drywood Termites | ||

| Dampwood Termites | ||

| Other Termite Types | ||

| By Application | Residential | |

| Commercial and Industrial | ||

| Agricultural Lands | ||

| Public Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the termite control market?

The termite control market stands at USD 6.27 billion in 2026 and is forecast to reach USD 8.54 billion by 2031 at a 6.39% CAGR from 2026 to 2031.

Which control method is growing fastest?

Bait systems are projected to advance at a 6.92% CAGR, outpacing chemical barriers and physical shields.

Why is Asia-Pacific the largest regional contributor?

Tropical humidity, year-round termite pressure, and rapid construction activity drive sustained demand across China, India, and ASEAN economies.

What is driving higher adoption of IoT termite monitoring?

Wireless sensors deliver early detection, cut unnecessary chemical use, and provide digital compliance records favored by insurers and regulators.

Page last updated on: