Andalusite Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

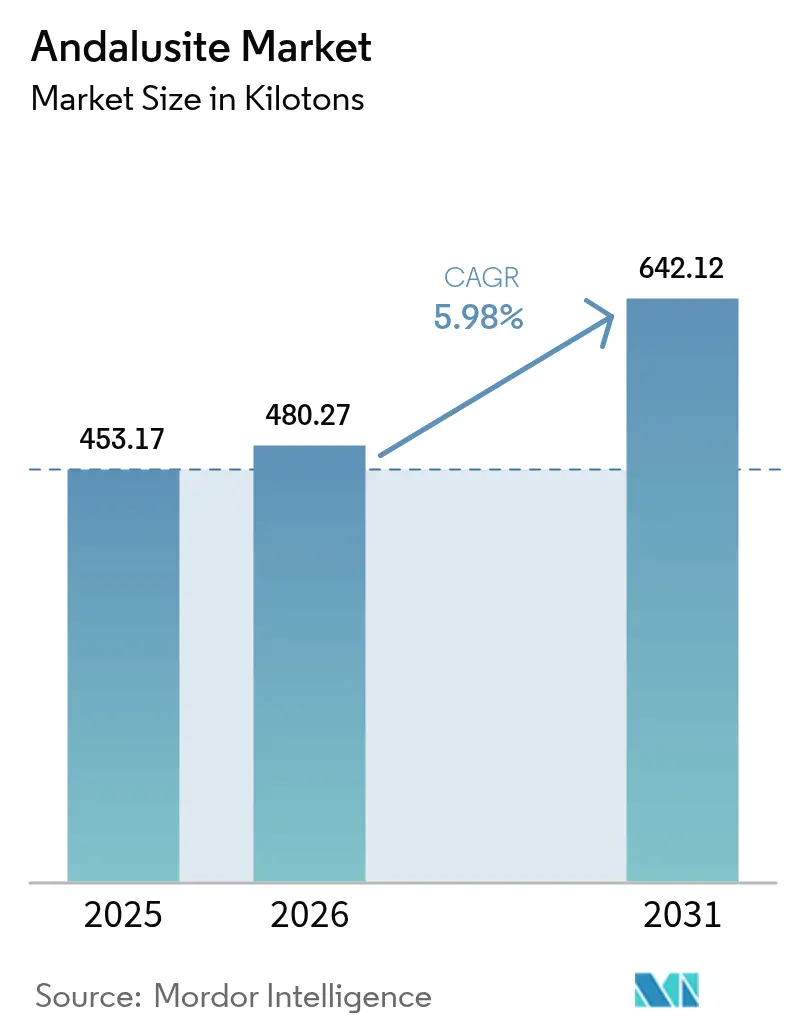

| Market Volume (2026) | 480.27 kilotons |

| Market Volume (2031) | 642.12 kilotons |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

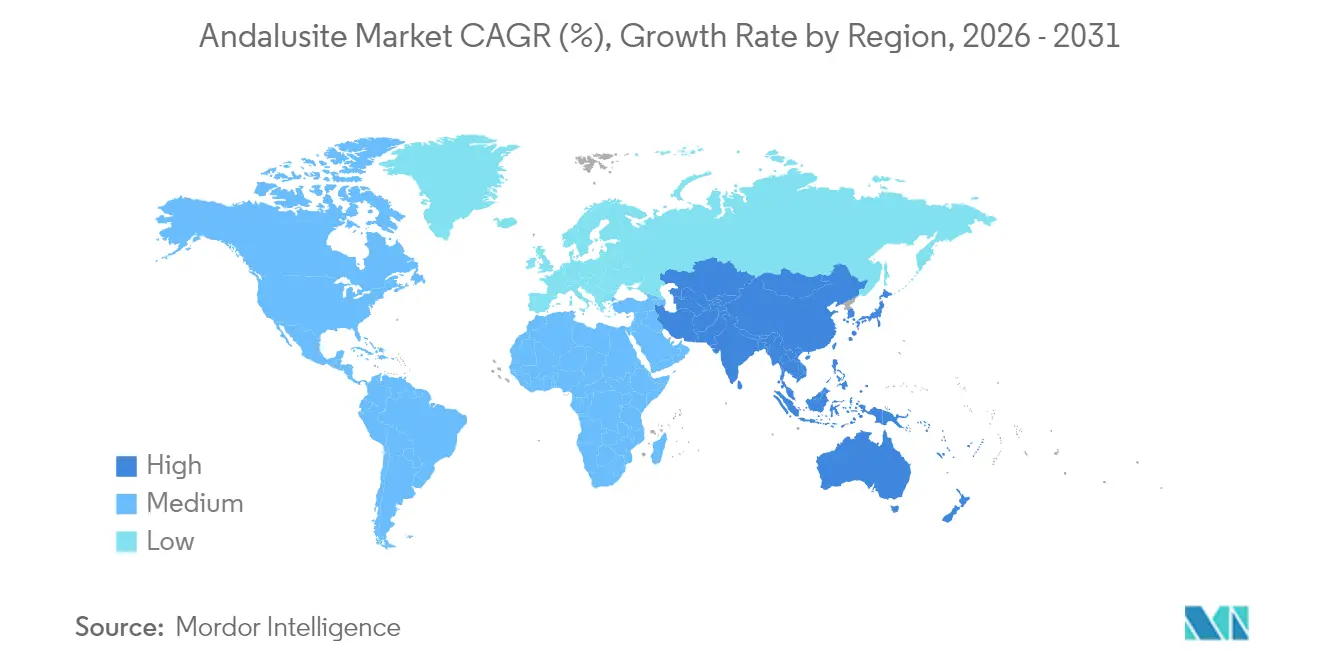

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

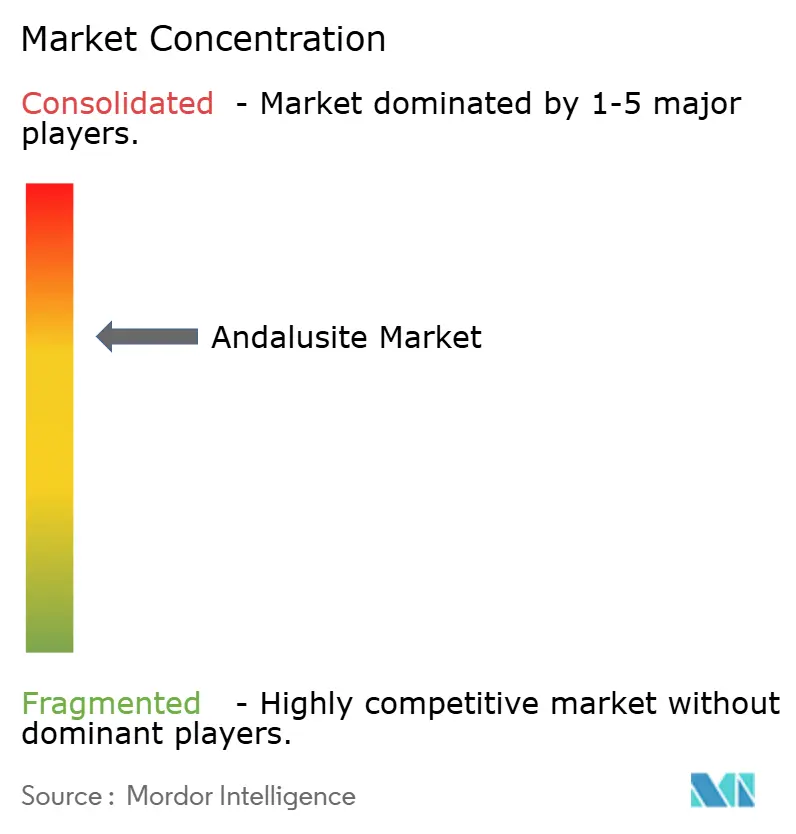

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Andalusite Market Analysis by Mordor Intelligence

Andalusite market size in 2026 is estimated at 480.27 kilotons, growing from 2025 value of 453.17 kilotons with 2031 projections showing 642.12 kilotons, growing at 5.98% CAGR over 2026-2031. Rising refractory demand for electric-arc-furnace steelmaking, expanding Southeast Asian foundry capacity, and North American critical-minerals policies are the primary growth catalysts. Supply, however, remains concentrated in South Africa, exposing buyers to risks of grid instability and freight rate volatility. Advanced beneficiation methods are expanding the economically viable resource base, yet new projects are trailing demand momentum, keeping the Andalusite market finely balanced. Growing circular-economy mandates in Europe and the United States add a further layer of complexity, because recycled refractories still require premium virgin Andalusite grades for performance restoration.

Key Report Takeaways

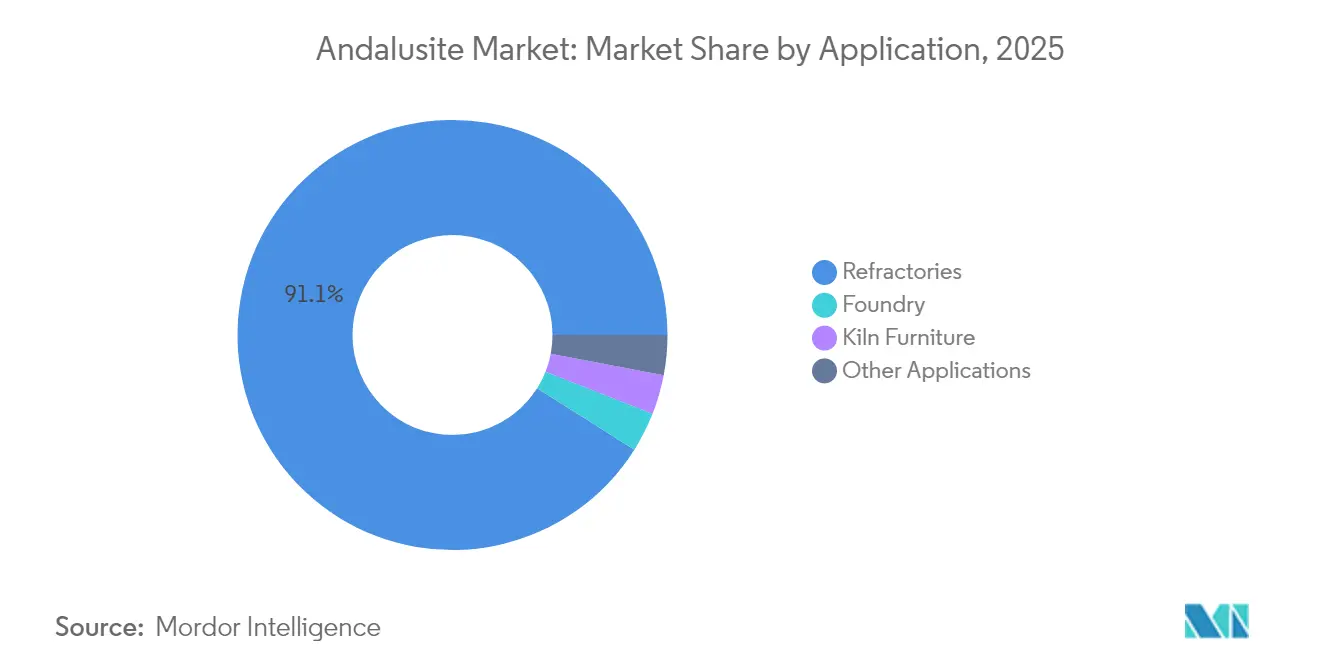

- By application, refractories captured 91.05% of the Andalusite market share in 2025 and are projected to advance at a 7.6% CAGR through 2031.

- By geography, the Asia-Pacific region held 46.21% of the Andalusite market share in 2025 and is projected to expand at a 6.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Andalusite Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging refractory demand from electric arc furnace (EAF) steelmaking | +1.8% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Rapid capacity expansions of South-East Asian foundries | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Advanced beneficiation tech lowering production cost/grade threshold | +0.9% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Circular-economy push for recycled refractories in Europe | +0.6% | Europe primary, expanding to North America | Medium term (2-4 years) |

| Supply-chain localisation incentives in United States Critical Minerals policy | +0.4% | North America, indirect effects on global supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Refractory Demand From Electric Arc Furnace Steelmaking

Global steelmakers are adding electric-arc-furnace capacity because EAF units cut both capital cost and Scope 1 emissions. Carbon-pricing schemes and green-steel premiums further reinforce the shift, while abundant scrap supplies in Indonesia and Vietnam ensure feedstock security. Nippon Steel’s decarbonization outlay through 2030 highlights how low-carbon metallurgy intensifies refractory complexity and increases the demand for high-purity Andalusite[1]Nippon Steel, “Integrated Report 2024,” nipponsteel.com. As electric-arc furnaces operate at temperatures near 1,800 °C, refractory replacement cycles become shorter, thereby amplifying volume growth. The Andalusite market, therefore, benefits directly from each new EAF installation and indirectly from stricter emissions regulation that penalizes less-efficient blast furnaces.

Rapid Capacity Expansions of South-East Asian Foundries

Automotive and electronics supply-chain shifts from China toward Malaysia, Indonesia, and Vietnam are driving a wave of new non-ferrous and ferrous foundries. Each greenfield foundry requires virgin Andalusite for start-up campaigns and high-temperature kiln furniture. Malaysia’s investment incentives promote cluster development, giving suppliers predictable offtake volumes for at least five years. Indonesian industrial parks in Java are securing long-term Andalusite supply agreements to ensure thermal-shock performance and workplace safety compliance. Vietnam benefits from its proximity to Chinese customers, which is facilitated by the absence of the same trade barriers, making it a strategic consumption hub. In aggregate, the rapid build-out compresses regional inventories, magnifying every mining or logistics hiccup in South Africa.

Advanced Beneficiation Technology Lowering Production Cost and Grade Threshold

Process innovations, such as mesofluidic separation, ultrasonic flotation, and machine-learning-driven reagent control, have increased Andalusite recovery rates on lower-grade ores[2]Pacific Northwest National Laboratory, “PNNL technology could help US reduce dependence on foreign critical minerals,” pnnl.gov . Recovery improvements lower the economic cutoff of Al₂O₃, significantly enlarging the resource base. Electro-kinetic mining further unlocks deep, complex formations while shrinking water use and tailings footprints. Western producers are piloting sensor-based sorters that deliver concentrate grades without grinding, preserving crystal integrity valued in premium refractories. The cost curve is therefore flattening, though only producers with sufficient research and development budgets can commercialize these advances. As diffusion widens, incremental tonnage will temper price spikes but not remove supply risk during South African outages.

Circular-Economy Push For Recycled Refractories in Europe

The German National Circular Economy Strategy mandates recycling of industrial materials by 2030, accelerating specialized plants that crush spent bricks and sort phases by X-ray sensor. EU Construction Products Regulation favors natural, low-carbon inputs, tilting demand toward Andalusite over synthetic mullite. Buyers of recycled aggregates still pay a premium for high-purity Andalusite fines to hit quality benchmarks. Consequently, circularity does not cannibalize the Andalusite market; it reallocates demand into cleaner, higher-grade supply channels.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-instability curtailments at South African mines | -1.4% | Global, with primary impact on Africa and secondary effects worldwide | Short term (≤ 2 years) |

| Substitution threat from synthetic mullite and calcined bauxite | -0.8% | Global, with concentration in cost-sensitive applications | Medium term (2-4 years) |

| Freight-rate volatility on bulk minerals shipping | -0.5% | Global trade routes, particularly affecting Asia-Pacific imports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Instability Curtailments at South African Mines

Load-shedding forces andalusite mines to slash power use, resulting in reduced output. Diesel gensets bridge part of the gap but add extra cost, eroding margins on lower-grade product. Supply from Peru and France is insufficient to offset any multi-month disruption. Seasonal demand peaks in Asia-Pacific overlap with South African summer load-shedding, amplifying price volatility and inventory speculation.

Substitution Threat From Synthetic Mullite and Calcined Bauxite

Synthetic mullite and calcined bauxite undercut Andalusite in kiln furniture and low-temperature linings. Almatis is doubling Chinese calcined alumina capacity in early 2026, assuring feedstock for mullite bricks at scale. For applications below 1,500 °C, design engineers prefer materials with tighter particle size control and consistent chemistry. Research into zirconia-mullite and silicon-carbide hybrids is advancing rapidly, promising further inroads. To defend their share, Andalusite suppliers emphasize low porosity, natural crystal morphology, and proven health and safety performance. High-temperature steel ladle linings still rely on Andalusite, yet cost-sensitive customers will pivot if price differentials widen.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Refractories Dominance and Diversification

Refractories accounted for 91.05% of the Andalusite market size in 2025 and are forecast to expand at a 7.6% CAGR to 2031. Steel ladles, EAF roofs, and tundish linings consume the bulk of volumes, yet waste-to-energy and biomass boilers are emerging growth nodes that also demand high-purity grades. Andalusite’s low thermal expansion and high mullite conversion point deliver superior spalling resistance, extending brick life and lowering furnace downtime. Foundry sands are forming the fastest-growing niche within refractories, driven by capacity additions in Southeast Asia for automotive casting. Advanced beneficiation enables the tailoring of crystal size distribution, resulting in bricks that resist both alkali attack and high thermal gradients. In ceramics, Andalusite additions curb warpage in large sanitary-ware parts, although total volumes remain modest. Jewelry makers source translucent pink Andalusite for gemstone use, capturing premium pricing but negligible tonnage.

Secondary applications, such as filters and spark-plug insulators, are small but technically demanding, favoring Andalusite over cheaper bauxite. Circular-economy legislation in Germany and France is boosting recycled refractory volumes. As decarbonization pushes heavy industry toward higher-efficiency furnaces, the performance envelope tightens, enlarging the addressable Andalusite market. No synthetic mullite currently replicates the exact mixture of alumina, silica, and impurity oxides found in natural Andalusite, giving it a defensible technical moat in ultra-high-temperature service.

Geography Analysis

The Asia-Pacific region held 46.21% of the Andalusite market size in 2025 and is projected to grow at a 6.21% CAGR through 2031. China remains the anchor consumer, yet Southeast Asia is the flashpoint where new demand collides with supply risk. Malaysia’s push into electric-vehicle components, Indonesia’s stainless-steel clusters, and Vietnam’s export-oriented foundries are securing multi-year contracts for Andalusite to lock in quality and volume. Japanese and South Korean steelmakers, although mature, are adopting longer off-take terms to hedge against freight volatility and have begun trialing Peruvian Andalusite to diversify their supply lines. India’s refractory industry is expanding, backed by domestic steel capacity approvals.

North America is pivoting toward self-reliance under the critical minerals policy, stimulating exploration in Arizona and Quebec. Although new mines will not deliver large tonnage before 2028, defense and aerospace users already prefer Andalusite-based domestic refractories to meet content rules. Canada’s modest production and Mexico’s foundry integration within USMCA provide regional supply buffers, but both remain exposed to South African outages. Advanced beneficiation pilot plants in Idaho show promise for converting lower-grade schist into commercial-grade product, potentially shaving imports by mid-decade.

Europe’s consumption pattern is shaped by circular economy targets that necessitate recycling by 2030. Germany, France, Italy, and Spain collectively anchor demand, while the United Kingdom shows stable replacement volumes. High energy prices and emissions costs could curb new steel capacity, but waste-to-energy and hydrogen pilot projects compensate, each specifying Andalusite for lining integrity.

South America, the Middle East, and Africa are emerging as key consumption arenas. Brazil’s waste-to-energy plants and Peru’s copper smelters require high-grade brick imports, with Andalusite shipped via Atlantic routes, which are less susceptible to fluctuations in Pacific freight. Gulf Cooperation Council countries are investing in desalination and green-hydrogen schemes that operate at extreme temperatures, creating a premium opportunity for Andalusite suppliers willing to stage inventory in local free zones. Africa outside South Africa remains a marginal consumer today, but as regional steel and cement works scale up, local Andalusite availability could shift the demand curve upward.

Competitive Landscape

The Andalusite market is moderately consolidated. Emerging producers in Peru, France, and China focus on niche grades with low iron and alkali impurities. Junior miners in the United States and Australia are leveraging critical minerals grants to develop deposits previously deemed sub-economic. Technology start-ups are licensing ultrasonic flotation and sensor-based sorting to incumbents, tightening quality consistency across the supply base. Downstream, refractory makers sign multi-year supply agreements with take-or-pay clauses to hedge against outage risk, contributing to a stable baseline demand even in slower macroeconomic years. Competitive differentiation is increasingly based on ESG credentials, with customers requesting traceable mining, renewable power sourcing, and cradle-to-gate life-cycle assessments. Substitution pressure from synthetic mullite triggers continuous product innovation. Industry consolidation may continue as large players pursue regional deposits to de-risk single-country exposure.

Andalusite Industry Leaders

Imerys

ARM Andalusite

Andalucita S.A.

LKAB Minerals

RHI Magnesita

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: RHI Magnesita completed the USD 410 million acquisition of Resco Group, adding U.S. fireclay and pyrophyllite-andalusite assets to its portfolio.

- September 2023: Imerys highlighted its Glomel, France, operation, which produces 65,000 tons of Andalusite annually, and detailed the environmental stewardship measures in place at the site. The company has announced a project to open a new pit, which is currently at the analytical stage.

Global Andalusite Market Report Scope

Andalusite is an alumina-silicate-based raw material majorly used in the manufacturing of heat-resistant refractory products.

The andalusite market is segmented by application and geography. By application, the market is segmented into refractories, foundry, kiln furniture, and other applications. The report also covers the size and forecasts for the andalusite market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Refractories |

| Foundry |

| Kiln Furniture |

| Other Applications (Ceramics and Jewelry) |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Refractories | |

| Foundry | ||

| Kiln Furniture | ||

| Other Applications (Ceramics and Jewelry) | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume of the Andalusite market by 2031?

The Andalusite market is forecast to reach 642.12 kilotons in 2031, up from 480.27 kilotons in 2026.

Which region leads in Andalusite consumption?

Asia-Pacific commands the largest share at 46.21% and is expanding at a 6.21% CAGR through 2031.

How does electric-arc-furnace steelmaking affect Andalusite demand?

Each new EAF installation requires high-purity Andalusite bricks, which boosts global demand for these materials.

What are the main supply risks in the Andalusite market?

Grid instability in South Africa, freight-rate volatility, and substitution by synthetic mullite pose the greatest near-term challenges.

Are recycled refractories diminishing virgin Andalusite demand?

No, recycled aggregates often need premium Andalusite additions to regain performance, resulting in stable net demand.

Page last updated on: