Agriculture Termite Control Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

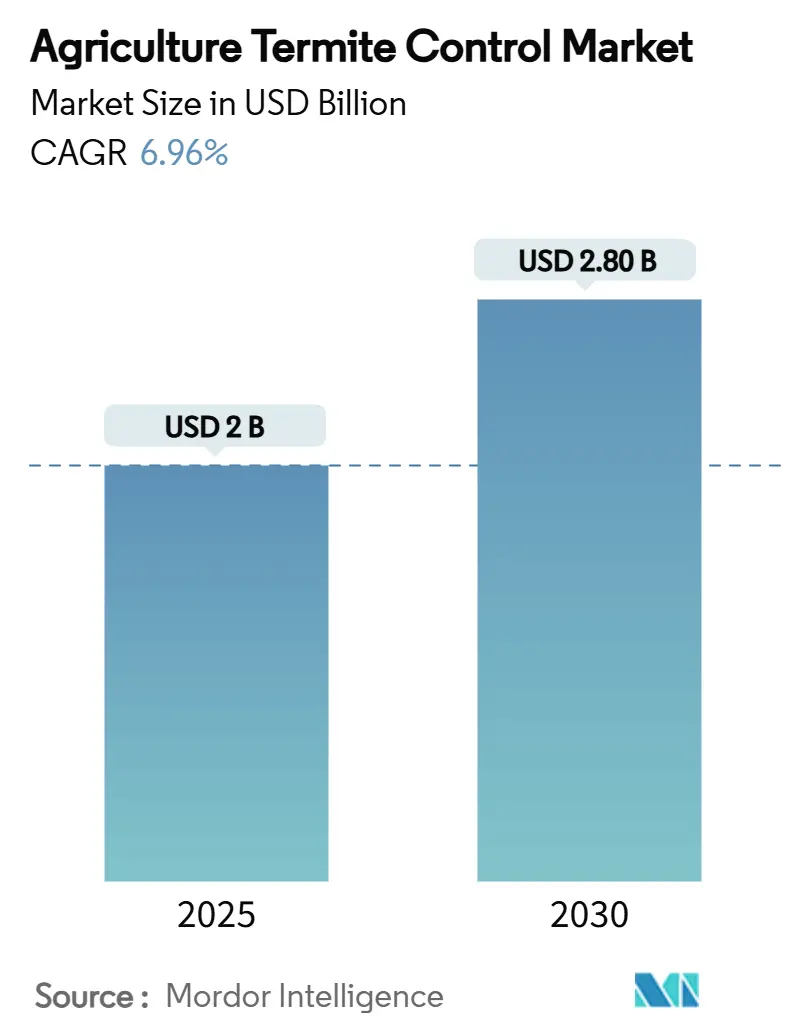

| Market Size (2025) | USD 2 Billion |

| Market Size (2030) | USD 2.80 Billion |

| Growth Rate (2025 - 2030) | 6.96% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

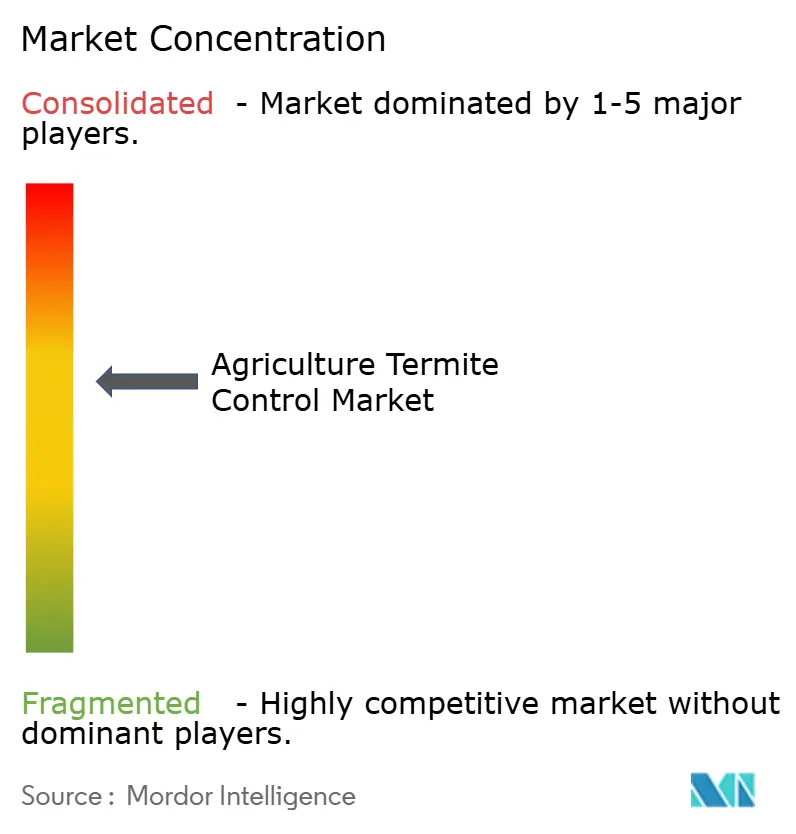

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agriculture Termite Control Market Analysis by Mordor Intelligence

The agriculture termite control market size reached USD 2.0 billion in 2025 and is projected to grow to USD 2.8 billion by 2030, at a CAGR of 6.96% during the forecast period 2025-2030. This growth is driven by the significant economic impact of termite infestations, which cause USD 40 billion in annual crop losses, with subterranean termites accounting for 80% of the damage in 2024. Increasing global temperatures have extended termite activity periods and expanded their presence into previously unaffected semi-arid regions, creating new market opportunities. The integration of precision agriculture technologies and the emergence of crop-loss insurance products have transformed termite management from reactive treatments to preventive programs, offering farmers more predictable cost management. Climate-induced pest migration patterns, regulatory emphasis on low-risk pesticides, and increased adoption of Internet of Things-based soil monitoring systems further support the market's growth trajectory.

Key Report Takeaways

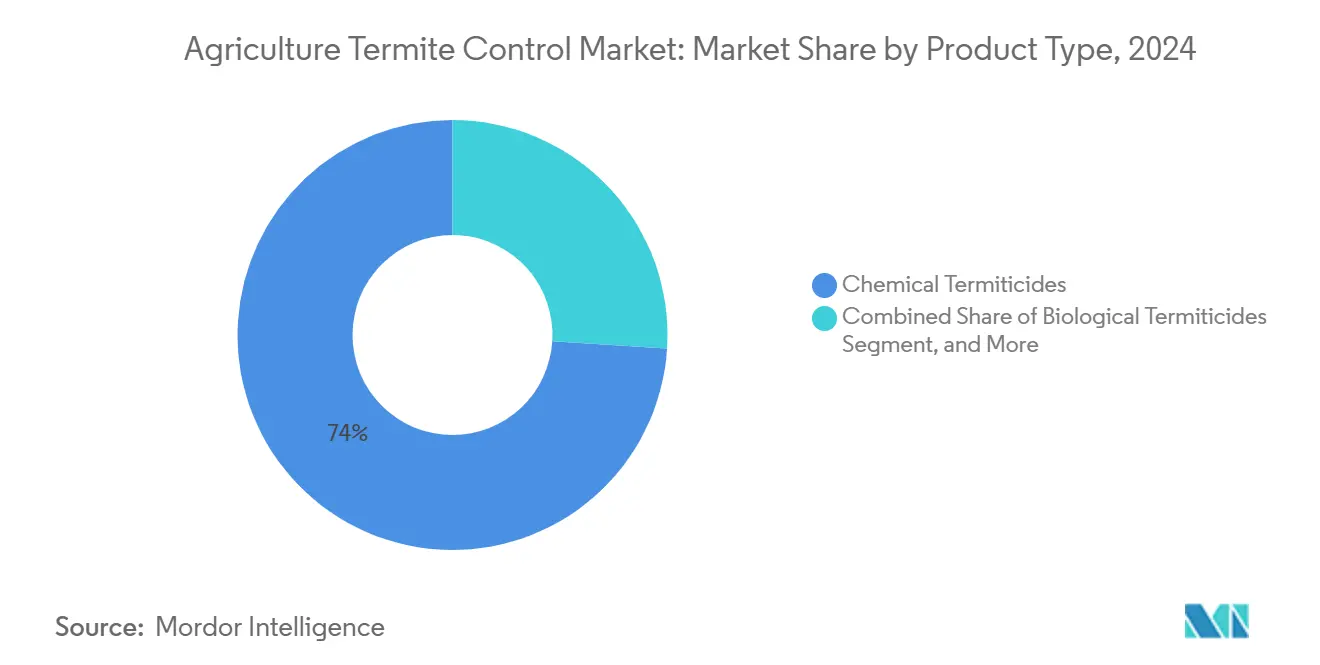

- By product type, chemical termiticides dominated with 74% of the agriculture termite control market share in 2024, while biological termiticides are projected to grow at a 9.7% CAGR through 2030.

- By crop type, cereals and grains represented 31% of the agriculture termite control market size in 2024, with commercial crops growing at an 8.3% during 2025-2030.

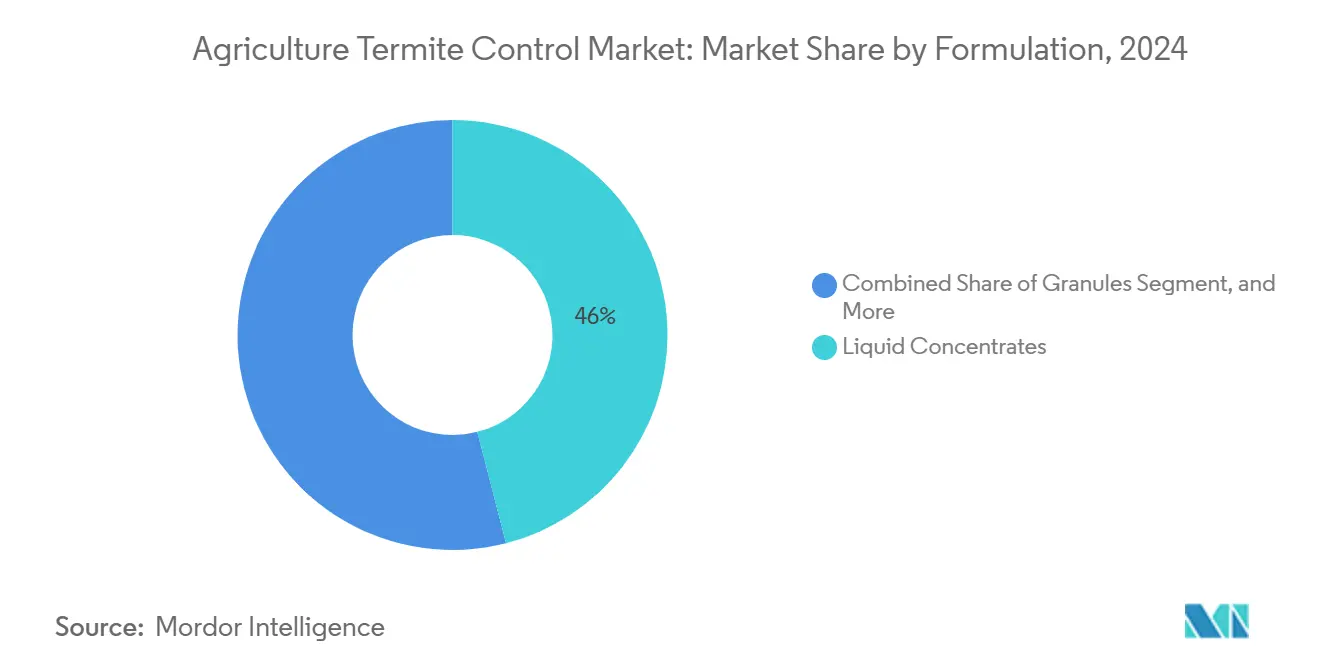

- By formulation, liquid concentrates captured 46% market share in 2024, while seed-treatment coatings are projected to grow at a 9.4% CAGR between 2025 and 2030.

- By mode of application, soil drench applications occupied 53% of the agriculture termite control market share in 2024, with seed treatment growing at 9.2% CAGR through 2030.

- By geography, Asia-Pacific maintained market leadership with a 41% share in 2024, while Africa is anticipated to grow at a 9.1% CAGR through 2030.

- The market maintains moderate consolidation, with BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, and FMC Corporation together holding 60.9% market share in 2024.

Global Agriculture Termite Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising termite-related crop-loss insurance claims driving bundled treatment uptake | +1.2% | Global, concentration in North America and Australia | Medium term (2-4 years) |

| Expansion of no-till farming accelerating residue-borne termite pressure on roots | +0.8% | Asia-Pacific core, spill-over to South America and Africa | Long term (≥ 4 years) |

| Regulatory green-light for diamide seed treatment labels | +1.1% | North America and European Union, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Climate-induced termite migration into semi-arid agriculture belts | +0.9% | Mediterranean and Sub-Saharan regions | Long term (≥ 4 years) |

| Surge in export-oriented agriculture demanding Food Safety Compliance (FSC)--compliant biorational termiticides | +0.7% | South America, Africa and Southeast Asia | Medium term (2-4 years) |

| On-farm IoT soil probes enabling data-driven prophylactic drenches | +0.6% | North America and European Union, early pilots in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Termite-related Crop-loss Insurance Claims Driving Bundled Treatment Uptake

Insurance carriers reported a 34% increase in termite-related indemnity payouts since 2024, leading to policies requiring preventive treatments for premium discounts[1] John S. Bernhardt, “Crop-loss Insurance and Pest Control,” NCSU.EDU. Corn growers experience 4% annual yield losses (610 million bushels) in untreated fields, creating financial exposure for insurers. Insurance companies now consider integrated termite control programs essential for risk mitigation. Premium discounts of 15-25% encourage wider adoption of soil drench treatments and diamide seed dressings, transforming the agricultural termite control market from localized treatments to comprehensive seasonal protection.

Expansion of No-till Farming Accelerating Residue-borne Termite Pressure on Roots

No-till fields contain 40-60% higher subterranean termite populations compared to conventionally tilled fields, as surface residues provide carbon-rich food sources that support termite colonies. The rotation of soybeans and corn enhances this effect by maintaining continuous organic matter coverage, while cover crops extend termite feeding periods. In response, manufacturers have developed termiticides that bind effectively to residue-rich soil and provide sustained release of active ingredients during extended termite foraging periods.

Regulatory Green-light for Diamide Seed-treatment Labels

The United States Environmental Protection Agency's 2024 approval of chlorantraniliprole and cyclaniliprole seed treatments established an efficient pathway for diamide chemistry use in row crops[2]United States Environmental Protection Agency, “Registration Decisions for Diamide Seed Treatments,” EPA.GOV. Field trials demonstrated 90- to 120-day pest control using application rates 40% lower than traditional soil treatments, reducing environmental impact and meeting pollinator protection requirements. Seed companies integrated diamide coatings with genetic trait packages, advancing the adoption of comprehensive soil pest management solutions.

Climate-induced Termite Migration into Semi-arid Agriculture Belts

The northward and southward migration of tropical termite species has increased termite attacks on vineyards in California and South Australia, as well as olive groves in the Mediterranean region[3]M. A. Jones, “Climate Change and Termite Range Expansion,” PMC.US. Since these agricultural areas traditionally did not require termite management systems, agricultural extension services are implementing local monitoring networks and suggesting chemical and biological control methods suitable for arid soil conditions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residual-toxicology scrutiny of termiticides in food-chain audits | –0.4% | European Union and North America | Short term (≤ 2 years) |

| High cost of biological inoculum refrigeration in tropical supply chains | –0.3% | Africa, Southeast Asia and tropical South America | Medium term (2-4 years) |

| Limited label claims for subterranean termite control in seed treatments | –0.2% | North America and European Union | Short term (≤ 2 years) |

| Fragmented smallholder plots reducing return on investment for perimeter soil barriers | –0.1% | Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Residual-toxicology Scrutiny of Termiticides in Food-chain Audits

The maximum residue limits for organophosphates decreased by 50-70% in major importing regions in 2025. This reduction compelled growers to either extend pre-harvest intervals or switch to biological alternatives with lower persistence[4]ANSES, “Updated Residue Thresholds for Soil Insecticides,” ANSES.FR. Root and tuber crops face higher scrutiny due to their systemic absorption of residues in edible parts, resulting in enhanced audit requirements from European retailers.

High Cost of Biological Inoculum Refrigeration in Tropical Supply Chains

Cold chain requirements for Beauveria and Metarhizium formulations increase costs by USD 15 per hectare in remote areas, compared to USD 3-5 for chemical alternatives that are stable at room temperature. Power outages lasting over 48 hours can damage entire shipments, limiting adoption in markets including northern Mozambique and eastern Indonesia, where termite pressure is high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biologicals Challenge Chemical Dominance

Chemical termiticides hold 74% of the agriculture termite control market share in 2024, driven by their rapid effectiveness and established distribution networks. Biological controls are projected to grow at a 9.7% CAGR through 2030, primarily driven by export certification requirements that encourage farmers to replace organophosphates with Food Safety Compliance-compliant fungal and botanical solutions. Entomopathogenic formulations achieve 85-95% efficacy in controlled soil temperatures and maintain presence in rhizosphere zones, enabling reduced chemical applications that decrease residue levels. Combined treatments using chlorantraniliprole and Beauveria spores demonstrate improved performance, reducing active ingredient requirements by 30% while extending treatment duration.

Chemical manufacturers are adapting by acquiring biological control companies and developing hybrid formulations that combine synthetic compounds with biological enhancers for better performance in high-residue environments. While sustainable certification premiums support the transition to biologicals, storage constraints and temperature control requirements limit adoption in tropical regions. Consequently, integrated approaches using both chemical and biological controls are projected to lead the agriculture termite control market through 2030.

By Crop Type: Commercial Crops Drive Future Growth

Cereals and grains accounted for 31% of the agriculture termite control market size in 2024, driven by termite pressure across 600 million hectares of global rice, corn, and wheat acreage. Commercial crops, including sugarcane, cotton, and tobacco, are experiencing the fastest growth at an 8.3% CAGR, as increased mechanization in Brazil and West Africa enables the cultivation of previously termite-affected areas. In northeast Brazil, sugarcane plantations experience 15-25% yield losses when termite tunnels damage vascular bundles, prompting major buyers to implement mandatory drench protocols in cane-supply contracts.

High-value perennial crops such as cocoa and coffee are also classified under commercial crops, as termite damage to root systems reduces plantation lifecycles by up to five years, impacting overall profitability. The premium prices associated with certification programs offset the increased costs of implementing combined biological-chemical control methods. Meanwhile, oilseeds and pulses demonstrate moderate growth, primarily following the expansion of no-till soybean cultivation in Argentina and the United States.

By Formulation: Seed Coatings Reshape Application Paradigms

Liquid concentrates maintain a 46% of the agriculture termite control market share in 2024, primarily due to their broad compatibility with ground application equipment and effective penetration of clay loam soils after heavy rainfall. Seed-treatment coatings demonstrate a 9.4% CAGR, driven by expedited regulatory approvals for diamide compounds and increased adoption of on-board seed treatment equipment. The agricultural termite control market for seed-coating applications shows growth potential based on current adoption trends, supported by precise dosing capabilities that reduce active ingredient usage per hectare and meet residue compliance requirements.

Granular formulations remain essential for large-scale cereal operations in Australia and Kazakhstan, where aerial broadcasting enables rapid coverage of extensive agricultural areas. Bait stations have gained renewed importance through IoT-guided placement systems, achieving effective pest control with 90% less active ingredient compared to perimeter treatments. Dust and powder applications decline except in organic farming segments, where approved ingredient options remain limited. Controlled-release microcapsule technology emerges as an innovative solution, designed to provide season-long protection while reducing chemical movement in sandy soil profiles.

By Mode of Application: Precision Methods Gain Momentum

Soil drenches accounted for 53% of the agriculture termite control market demand in 2024, primarily due to their ability to create immediate chemical barriers around root zones, which is essential for long-term perennial orchards. Seed treatments are projected to grow at a 9.2% CAGR through 2030, leveraging existing planting operations while ensuring consistent protection across uneven terrain. The increasing adoption of seed treatments aligns with regenerative agriculture practices by minimizing the need for in-season chemical applications and reducing soil disruption.

Foliar applications serve specific purposes, primarily addressing stem damage from above-ground termite activity during later plant development stages. In-row baiting systems are being integrated with precision agriculture techniques, using acoustic monitoring to target treatments to active termite colonies. The industry is developing integrated platforms that combine soil moisture data, termite detection systems, and plant health monitoring to enable automated termiticide application through robotic systems.

Geography Analysis

Asia-Pacific generated 41% of the agriculture termite control market share in 2024, driven by extensive rice cultivation systems in China and India, where conservation tillage increases termite damage to root systems. China's modernization initiatives fund IoT monitoring networks across Hubei and Jiangsu provinces, while India's public-private partnerships distribute Beauveria-based products through agricultural dealer networks. Japan continues to advance formulation technology, developing silafluofen-based products that demonstrate superior performance against Asian termite species with reduced mammalian toxicity compared to organophosphates.

Africa projects the highest growth rate at 9.1% CAGR through 2030, driven by increased mechanization and climate stress that expand termite presence in maize and sorghum cultivation regions. Kenya's research integrating indigenous neem extracts with synthetic compounds shows 20-30% crop yield improvements. Nigerian cotton production centers implement integrated drench-bait systems supported by out-grower financing, while South African vineyard regions conduct seed-coat trials to extend vine longevity.

North America and Europe maintain a stable market demand. The United States leads as the largest single-country market due to continuous corn-soybean rotation practices requiring preventive soil treatments. European restrictions on neonicotinoids accelerate diamide adoption and create opportunities for microbial products, especially in Spanish olive cultivation and French sugar beet production. In South America, Brazil leads innovation through sugarcane cultivation, developing soil surfactant-enhanced drench formulations for deeper penetration in porous latosols. Argentina expands market volume through soybean farmers adopting dual-purpose seed coatings that provide both termite and nematode protection.

Competitive Landscape

The agriculture termite control market exhibits moderate concentration, with the top five suppliers holding 60.9% market share in 2024. BASF SE maintains market leadership through its global dealer network and the Teraxxa diamide seed platform launched in 2024. Bayer AG holds a significant market share following Environmental Protection Agency approval for cyclaniliprole coatings. Syngenta Group enhanced its position through its 2024 DuPont asset acquisition, combining diamide products with satellite-guided prescription mapping capabilities.

Companies are integrating advanced technologies into their products. Manufacturers incorporate Bluetooth beacons in bait cartridges to collect consumption data for farm analytics platforms, allowing agronomists to monitor treatment effectiveness. Regional African companies focus on indigenous fungi solutions, addressing market gaps in multinational product portfolios. Patent applications are increasing for hybrid molecules that combine phenylpyrazoles with neonicotinoid microcaps to address resistance issues observed in Australian sugarcane farms.

Companies are restructuring their portfolios through strategic transactions. FMC Corporation divested its legacy chemical products to Envu for USD 350 million to fund biological research and development. Corteva Agriscience invested USD 75 million in new fungal production facilities in Brazil and Kenya to optimize supply chains and reduce cold-storage constraints. These strategic decisions indicate an industry shift toward specialized biological solutions supported by digital technology platforms.

Agriculture Termite Control Industry Leaders

BASF SE

Bayer AG

Syngenta Group

Corteva Agriscience

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bayer AG announced a strategic refocusing of its Crop Science division's production and research and development efforts in Germany on advanced technologies, including next-generation termiticide formulations and precision application systems for agricultural markets.

- May 2025: University of Florida confirmed the establishment of hybrid termite colonies in South Florida, involving Formosan and Asian subterranean species, raising concerns about increased agricultural damage potential and the need for enhanced control strategies.

- January 2025: Acadian Plant Health and Koppert expanded their partnership to enhance biocontrol technologies across Europe, the Middle East, and Africa, with a specific focus on sustainable termite-management solutions for export-oriented agriculture.

- February 2024: Syngenta Group has teamed up with Lavie Bio Ltd., a subsidiary of Evogene Ltd., to discover and develop new biological insecticides, including termiticides. This collaboration leverages Lavie Bio's cutting-edge technology platform for the swift identification and optimization of bio-insecticide candidates, complemented by Syngenta’s extensive global expertise in research, development, and commercialization.

Global Agriculture Termite Control Market Report Scope

| Chemical Termiticides | Organophosphates |

| Neonicotinoids | |

| Phenyl-pyrazoles | |

| Diamides | |

| Biological Termiticides | Entomopathogenic Fungi (Metarhizium, Beauveria) |

| Botanical Extracts and Oils | |

| Integrated Treatments and IPM Kits |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Turfs and Ornamentals |

| Commercial Crops |

| Liquid Concentrates |

| Granules |

| Seed-Treatment Coatings |

| Bait Stations |

| Dusts and Powders |

| Soil Drench |

| Seed Treatment |

| Foliar Spray |

| In-row Baiting |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Israel | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Nigeria | |

| Egypt | |

| Ethiopia | |

| Ghana | |

| Rest of Africa |

| By Product Type | Chemical Termiticides | Organophosphates |

| Neonicotinoids | ||

| Phenyl-pyrazoles | ||

| Diamides | ||

| Biological Termiticides | Entomopathogenic Fungi (Metarhizium, Beauveria) | |

| Botanical Extracts and Oils | ||

| Integrated Treatments and IPM Kits | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Turfs and Ornamentals | ||

| Commercial Crops | ||

| By Formulation | Liquid Concentrates | |

| Granules | ||

| Seed-Treatment Coatings | ||

| Bait Stations | ||

| Dusts and Powders | ||

| By Mode of Application | Soil Drench | |

| Seed Treatment | ||

| Foliar Spray | ||

| In-row Baiting | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Israel | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Egypt | ||

| Ethiopia | ||

| Ghana | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected growth rate of the agriculture termite control market from 2025 to 2030?

The market is projected to grow at a 6.96% CAGR, rising from USD 2.0 billion in 2025 to USD 2.8 billion by 2030.

Which region currently dominates revenue in agriculture termite control?

Asia-Pacific leads with 41% of global revenue in 2024, driven by intensive rice and conservation-tillage systems that exacerbate termite exposure.

Why are biological termiticides gaining share?

Export certification rules, residue limits and consumer preference for sustainable inputs are accelerating biological adoption at a 9.7% CAGR, outpacing chemical growth.

How are precision agriculture tools influencing termite control strategies?

IoT soil probes and variable-rate drench systems cut chemical use by up to 40% while retaining protection, steering growers toward data-driven prophylactic treatments.

What formulation segment is expanding fastest?

Seed-treatment coatings represent the fastest-growing formulation, with a CAGR of 9.4%, driven by regulatory approvals for diamide actives and the adoption of planter-integrated equipment.

Which crop segment offers the strongest growth outlook?

Commercial crops such as sugarcane and cotton are projected to expand at an 8.3% CAGR through 2030 as mechanization and export incentives boost acreage in termite-prone zones.

Page last updated on: