Diatomite Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

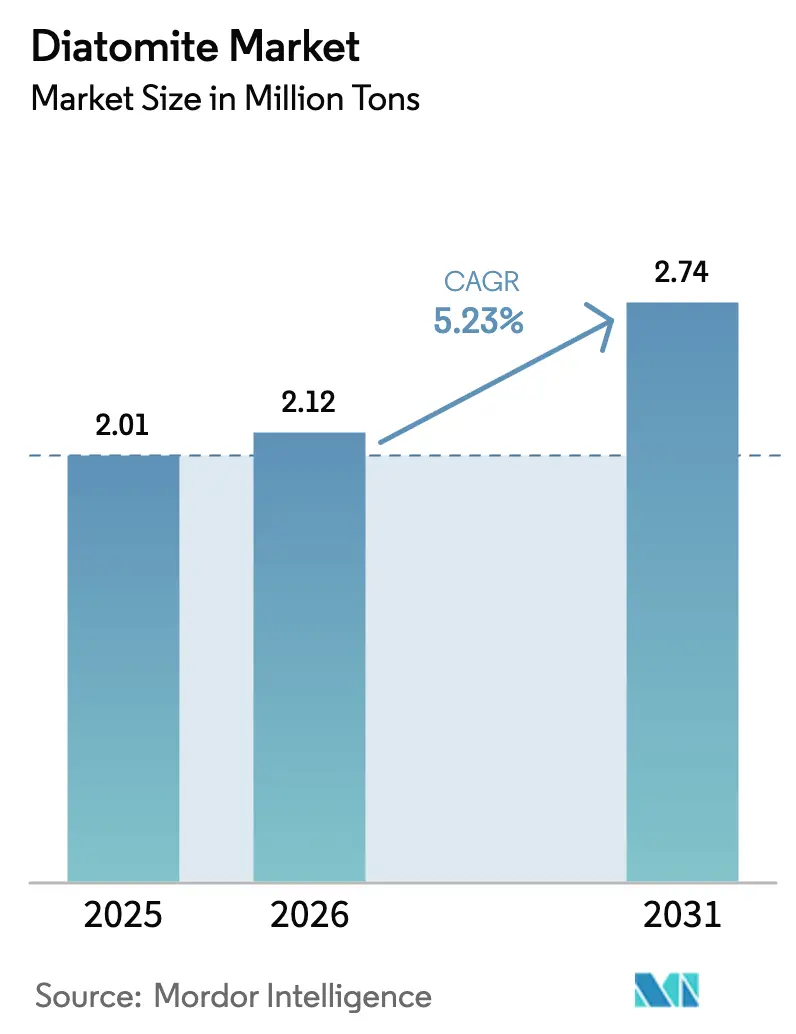

| Market Volume (2026) | 2.12 Million tons |

| Market Volume (2031) | 2.74 Million tons |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

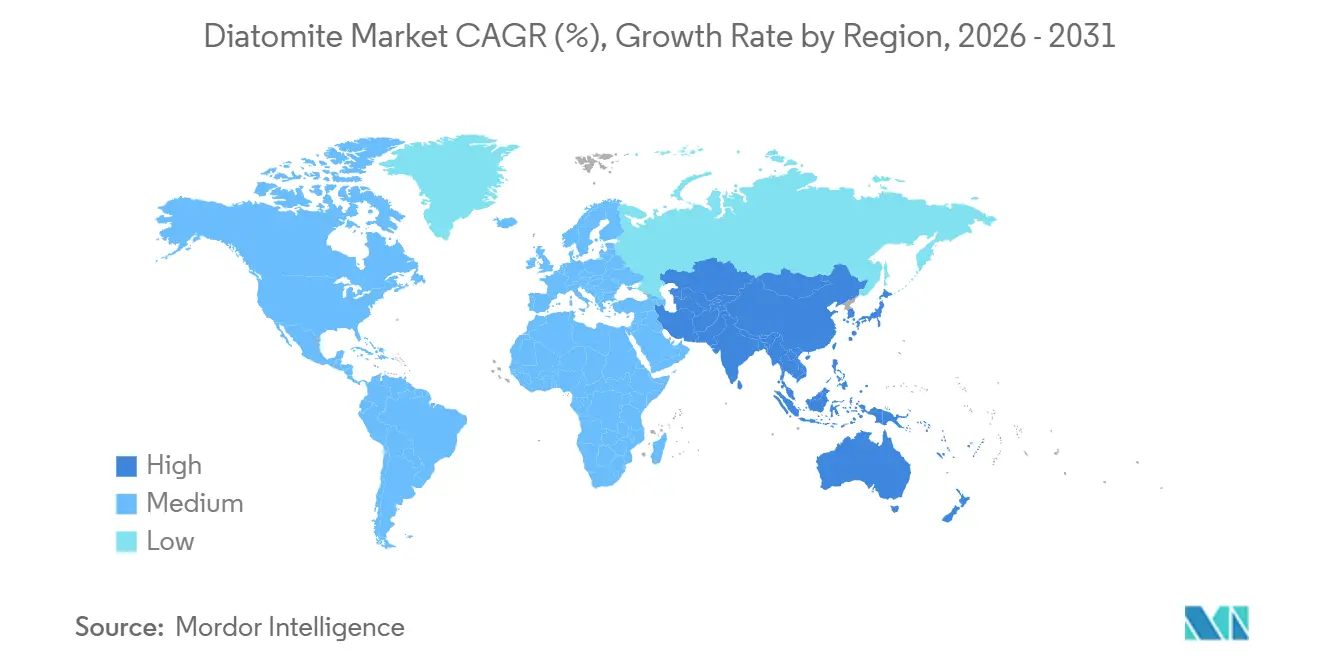

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

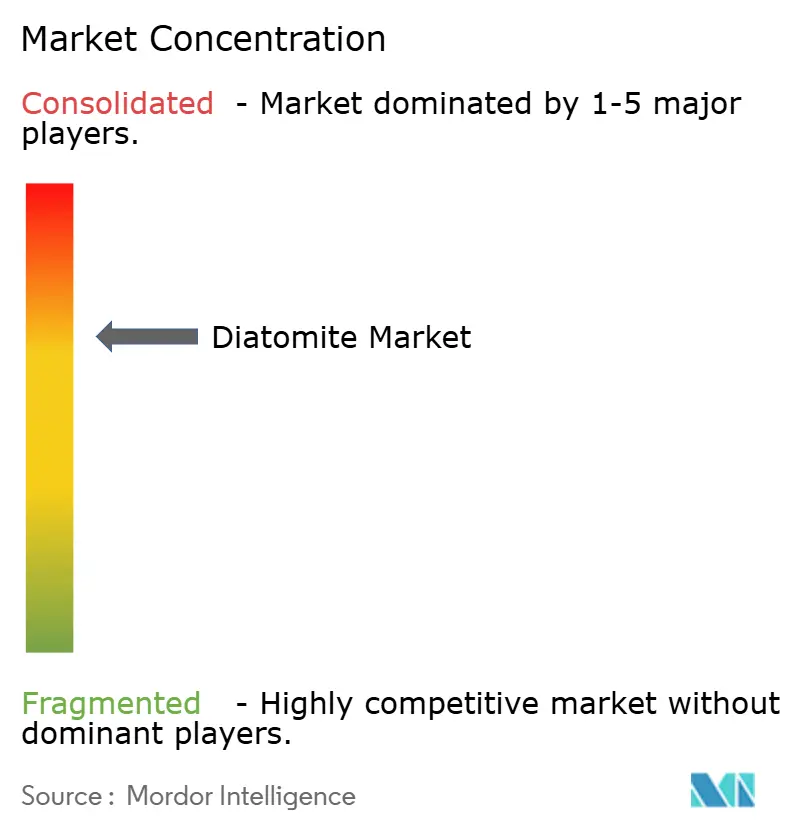

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diatomite Market Analysis by Mordor Intelligence

The Diatomite Market size is expected to grow from 2.01 Million tons in 2025 to 2.12 Million tons in 2026 and is forecast to reach 2.74 Million tons by 2031 at 5.23% CAGR over 2026-2031. Structural shifts in beverage filtration, water treatment, and lightweight construction are reshaping demand, while deposit depletion in the Western U.S. accelerates the development of marine sources. Asia-Pacific dominates current trade flows, supplying almost one-half of worldwide tonnage and absorbing sizable volumes for cement additives and municipal water schemes. Flux-calcined grades are displacing standard calcined material in high-throughput brewery operations, and the insecticides segment is benefiting from organic-farming mandates. Competitive rivalry remains moderate because mine ownership is regional and logistics-intensive, yet scale advantages in kiln control and technical servicing allow the top five suppliers to capture the most profitable food-grade contracts.

Key Report Takeaways

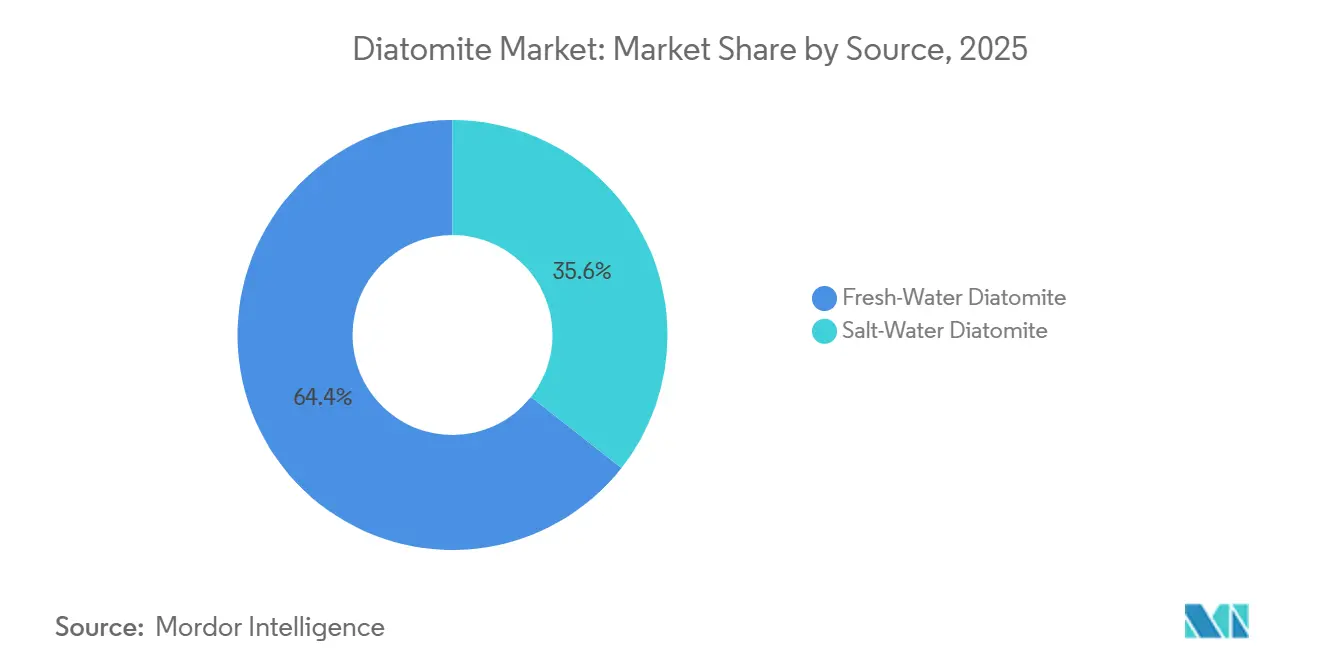

- By source, freshwater material commanded 64.38% of the 2025 volume, while saltwater grades are projected to grow at a 5.84% CAGR to 2031.

- By process, calcined grades led with 46.27% of the 2025 supply, whereas flux-calcined variants record the highest 6.18% CAGR.

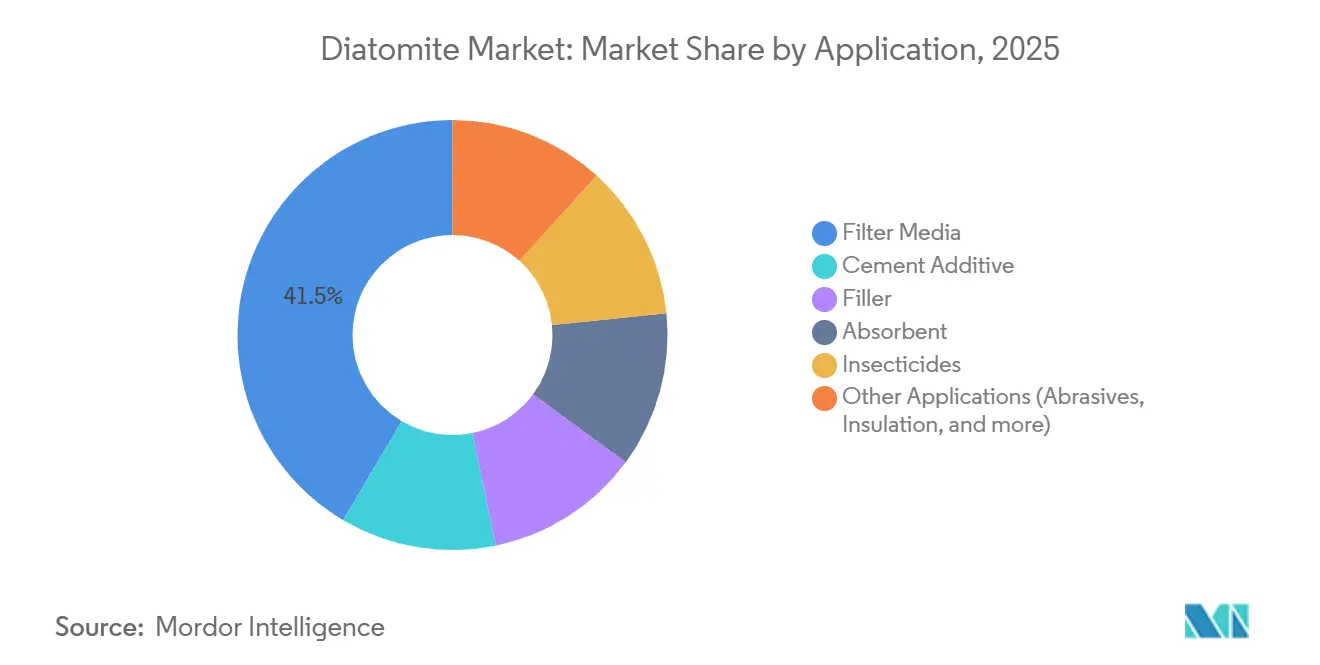

- By application, filter media accounted for 41.52% of 2025 demand; insecticides are advancing at a 6.27% CAGR.

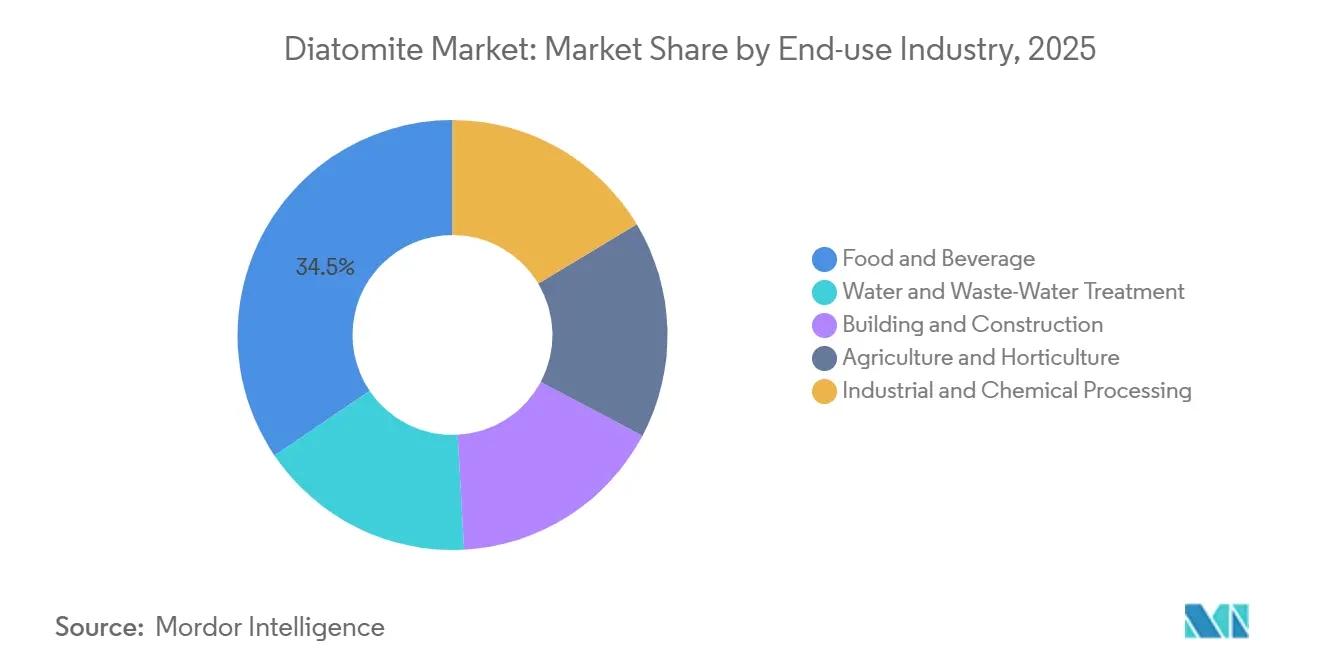

- By end-use industry, food and beverage held 34.46% of 2025 tonnage, but water and wastewater treatment is expanding at the fastest 6.34% pace.

- Asia-Pacific captured 47.63% of 2025 shipments and is set to rise at a 5.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Diatomite Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for diatomite as filter media in beverages and water treatment | +1.2% | Global, with concentration in Asia-Pacific (India, China) and North America | Medium term (2-4 years) |

| Expansion of water and wastewater treatment infrastructure worldwide | +1.4% | Asia-Pacific (India, Southeast Asia), Middle East, North Africa | Medium term (2-4 years) |

| Growing use of calcined grades in lightweight concrete and cement additives | +0.9% | Asia-Pacific (China, India), Europe (Germany, Italy, Spain) | Long term (≥ 4 years) |

| Increasing consumption as absorbent in agricultural and pet-litter products | +0.7% | North America, Europe, emerging markets in South America | Short term (≤ 2 years) |

| Scale-up of diatomite-derived silicon for Li-ion battery anodes | +0.6% | Asia-Pacific (China, Japan, South Korea), North America (battery gigafactories) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Diatomite as Filter Media in Beverages and Water Treatment

Breweries and wineries specify diatomite because its multi-level pore structure removes yeast, bacteria, and haze while preserving flavor and operating at low pressure. The U.S. FDA continues to affirm the material as GRAS for food filtration, and the International Organisation of Vine and Wine maintains its approval, giving producers regulatory certainty[1]U.S. Food and Drug Administration, “GRAS Notice No. 87,” fda.gov. Municipal utilities employ diatomite precoat filters that meet the U.S. EPA’s 3-log protozoan-removal standard, and India’s Jal Jeevan Mission allocates more than USD 50 billion for rural schemes that mandate low-maintenance filtration media. Lower sludge generation than coagulation methods further reduces disposal cost in water-scarce regions.

Expansion of Water and Wastewater Treatment Infrastructure Worldwide

Programs such as India’s AMRUT 2.0, China’s rural wastewater mandate, and Middle East desalination upgrades collectively underpin long-cycle demand. Diatomite filters suit decentralized plants serving smaller populations because they require minimal energy and short replacement intervals, creating a stable offtake for producers. Pilot data from Saudi Arabia show a reduction in reverse-osmosis fouling that cuts the levelized water cost up to 12%.

Growing Use of Calcined Grades in Lightweight Concrete and Cement Additives

Calcined diatomite reacts with calcium hydroxide to form dense calcium silicate hydrates, trimming concrete thermal conductivity 20–30% with negligible strength loss, a property welcomed by European building codes focused on energy efficiency. China’s green-building program also incentivizes pozzolanic substitution. Consistency hinges on a narrow firing window; producers investing in real-time X-ray diffraction monitoring secure higher-value contracts.

Increasing Consumption as Absorbent in Agricultural and Pet-Litter Products

The U.S. EPA lists diatomite as a minimum-risk pesticide, enabling organic growers to replace synthetic actives. Premium pet litters in North America and Western Europe shift to diatomite blends that suppress odor and dust, expanding value per ton. Competition from super-absorbent polymers persists where extremely high uptake is required, but disposal advantages keep diatomite cost-competitive in moderate-volume uses[2]U.S. Environmental Protection Agency, “Surface Water Treatment Rule,” epa.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution threat from expanded perlite, silica sand and synthetic media | -0.8% | Global, with higher intensity in Europe and North America (mature markets) | Short term (≤ 2 years) |

| Limited availability of high-purity deposits drives cost inflation | -0.5% | North America (Western U.S.), Europe (Spain, France) | Medium term (2-4 years) |

| Rising ESG-driven controls on crystalline-silica exposure | -0.4% | North America, Europe, Australia (stringent OSHA/EU enforcement) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Substitution Threat from Expanded Perlite, Silica Sand and Synthetic Media

Expanded perlite offers similar insulation at lower density, while silica sand undercuts diatomite on price in filler applications. Ceramic and polymer membranes lure pharmaceutical users needing sterile, closed systems that reduce batch variability. These pressures are strongest in mature Western markets that emphasize lifecycle cost and sealed operation.

Limited Availability of High-Purity Deposits Drives Cost Inflation

Near-surface zones in California and Nevada are depleting, elevating strip ratios and clay contamination, and tightening supply for food-grade customers. Shipping economics limit profitable reach to about 500 km by truck and 1,500 km by rail, encouraging development of marine deposits in Turkey, Peru, and Mexico that still require costly washing to remove soluble salts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Freshwater Dominance Masks Emerging Coastal Potential

Freshwater deposits held 64.38% of the 2025 volume, reflecting their superior purity and well-documented performance in beverage filtration. Marine resources are expanding at a 5.84% CAGR as high-purity inland basins mature. Investors are funding coastal projects in Peru, Turkey, and Mexico to reduce inland haulage, despite extra USD 20–35 per-ton beneficiation charges. Species variation demands tight beneficiation to match pore-size profiles required by long-standing customer specifications.

Marine producers can leverage port proximity to ship directly to Asian buyers, offsetting higher processing costs. Standardizing quality remains the main barrier; breweries conduct rigorous validation, and any deviation from legacy grades risks production downtime. Suppliers integrating on-site labs and ISO-certified protocols are the first to win approvals. Long-term, broader adoption of saltwater material could rebalance regional supply and stabilize pricing.

By Process: Flux-Calcined Grades Gain Traction in High-Throughput Filtration

Calcined material accounted for 46.27% of the 2025 supply because of its mechanical strength and low turbidity in the filtrate. Flux-calcined grades are the fastest-growing slice, climbing 6.18% yearly as breweries seek 30–50% lower pressure drop. Soda-ash addition during firing partially fuses frustules, producing wider channels without collapsing the structure. Producers must monitor residual sodium to keep it below 0.5% for wine compliance, which requires precise flux control and washing.

Capital intensity restricts flux-calcination to a few multinationals equipped with automated kilns and real-time XRD. These firms command premium margins by bundling technical support that improves throughput at customer sites. Smaller players focus on natural grades for absorbents and fillers where price, not pore architecture, dictates purchase choices.

By Application: Insecticides Segment Rides Organic Agriculture Wave

Filter media retained the top slot with 41.52% of 2025 demand, underpinned by food and beverage processing and municipal water projects. Insecticides, however, register the quickest 6.27% CAGR as regulatory bans on neonicotinoids and consumer preference for residue-free produce fuel uptake. Diatomite operates mechanically, abrading insect exoskeletons and averting resistance issues plaguing chemical actives.

Europe’s organic acreage and California’s specialty-crop sector illustrate this growth, while tropical regions utilize diatomite to safeguard stored grain where cold-chain infrastructure is sparse. Efficacy depends on a 10–50 µm particle band and low crystalline content for worker safety, encouraging suppliers to refine air classification lines.

By End-Use Industry: Water Treatment Outpaces Food and Beverage

Food and beverage maintained 34.46% of 2025 tonnage but is slowing as large brewers adopt centrifuges and haze-reducing recipes. Water and wastewater treatment is accelerating 6.34% yearly on the back of India’s USD 50 billion rural-water push and the U.S. EPA’s revised Lead and Copper Rule that mandates filtration upgrades. Builders continue to employ diatomite in cement and lightweight panels, yet clinker-reduction policies nudge some demand toward alternative binders.

Geography Analysis

Asia-Pacific supplied 47.63% of 2025 demand and is forecast to expand 5.91% CAGR to 2031 as China mines roughly 1.5 million tons yearly and ramps wastewater spending under the 14th Five-Year Plan. India’s Jal Jeevan Mission and AMRUT 2.0 contribute repeat orders for filter media, while Japan and South Korea pilot diatomite-based silicon for batteries. Southeast Asia adopts diatomite for textile-sector effluent polishing where low energy and moderate capital outlay fit cluster economics.

North America grows slower because mature users switch to membranes. U.S. Silica’s Lovelock, Nevada mine remains the world’s largest, and recent operational gains delivered segment revenue of USD 142.8 million in Q1 2024. Canada imports for oil-sands filtration, and Mexico consumes for tequila clarification, two niche uses that reward consistent pore profiles.

Europe’s share faces compliance headwinds. Imerys’ 2025 purchase of Chemviron’s assets consolidates regional supply with three new sites in France and Italy and about EUR 50 million (USD 56.53 million) revenue, allowing closer-to-customer delivery and perlite cross-selling. Ultrahigh energy-performance building codes encourage calcined pozzolan blends, but free fly ash and slag limit growth. Strict crystalline-silica exposure proposals may further elevate costs.

South America and the Middle East and Africa remain emerging. Brazilian housing adopts diatomite-lightened panels for thermal relief, and Argentina’s wine sector imports for clarification. Saudi Arabia studies diatomite as a supplementary cementitious material to reduce clinker in its 52.4 million-ton cement industry. South African mineral processors use diatomite absorbents, but local perlite and vermiculite temper volumes.

Competitive Landscape

The Diatomite market is moderately consolidated. Vertical integration and technical service differentiate leaders. Firms owning rail spurs or coastal terminals achieve 15–25% freight savings, critical because logistics can exceed mine-gate value. On-site process-optimization teams help breweries and water utilities fine-tune dosing, reinforcing stickiness. Innovation white spaces include battery-grade silicon, photocatalytic air filters, and depth-filter sheets integrating cellulose fibers. Asian challengers are upgrading acid-leach capacity to move into premium beverage grades, but certification barriers remain.

Diatomite Industry Leaders

EP Minerals

Showa Chemical Industry Co., Ltd

Imerys

Dicalite Management Group, LLC

Diatomit CJSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Local officials, including the Member of Parliament for Ardèche, along with representatives from regional and departmental councils and neighboring municipalities, visited Saint-Bauzile. Their itinerary included a guided tour of the quarry and processing facilities, showcasing recent investments aimed at minimizing environmental impact and enhancing biodiversity.

- February 2025: Imerys finalized its acquisition of Chemviron's European diatomite and perlite operations. Chemviron is a subsidiary of Calgon Carbon Corporation. This move allowed Imerys to bolster its European presence, as it took over three premium mining and industrial assets located in France and Italy.

Global Diatomite Market Report Scope

Diatomite is a naturally occurring siliceous white sedimentary rock. It is a fine-grained rock composed of the fossilized skeletal remains of diatoms, which are single-celled organisms related to algae. It is white and consists of the siliceous remains of diatoms deposited in the ocean, in ponds, or lakes. Diatomite is typically used as an absorbent, insulator, filtering medium, filler, etc.

The diatomite market is segmented by source, process, application, and geography. By source, the market is segmented into freshwater diatomite and saltwater diatomite. By process, the market is segmented into natural grades, calcined grades, and flux-calcined grades. By application, the market is segmented into filter media, cement additives, fillers, absorbents, insecticides, and other applications (abrasives, insulation, etc). The report also covers the market size and forecasts for the market in 15 countries across the globe. For each segment, the market sizing and forecasts have been done based on volume (tons).

| Fresh-Water Diatomite |

| Salt-Water Diatomite |

| Natural Grades |

| Calcined Grades |

| Flux-Calcined Grades |

| Filter Media |

| Cement Additive |

| Filler |

| Absorbent |

| Insecticides |

| Other Applications (Abrasives, Insulation, etc.) |

| Food and Beverage |

| Water and Waste-Water Treatment |

| Building and Construction |

| Agriculture and Horticulture |

| Industrial and Chemical Processing |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Source | Fresh-Water Diatomite | |

| Salt-Water Diatomite | ||

| By Process | Natural Grades | |

| Calcined Grades | ||

| Flux-Calcined Grades | ||

| By Application | Filter Media | |

| Cement Additive | ||

| Filler | ||

| Absorbent | ||

| Insecticides | ||

| Other Applications (Abrasives, Insulation, etc.) | ||

| By End-Use Industry | Food and Beverage | |

| Water and Waste-Water Treatment | ||

| Building and Construction | ||

| Agriculture and Horticulture | ||

| Industrial and Chemical Processing | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the global diatomite market in 2026 and how fast is it growing?

The diatomite market size is 2.12 million tons in 2026 and is forecast to grow at a 5.23% CAGR to reach 2.74 million tons by 2031.

Which region leads global consumption?

Asia-Pacific holds 47.63% of 2025 volume, driven by China’s cement, filtration, and water-treatment demand.

What application segment is expanding the fastest?

Insecticide use of diatomite is rising at a 6.27% CAGR as organic farming spreads.

Why are flux-calcined grades gaining share?

Breweries and wineries adopt flux-calcined diatomite because its larger pore channels cut filtration pressure drop 30–50% and raise throughput.

Which end-use industry offers the quickest growth?

Water and wastewater treatment leads with a 6.34% CAGR, supported by large infrastructure programs in India and regulatory upgrades in North America.

Who are the major players in the sector?

Who are the major players in the sector?

Page last updated on: